Frax Finance: Examining The Protocol’s Holy Trinity of De-Fi

FEB 01, 2023 • 11 Min Read

Introduction

Frax Finance is a household name for seasoned DeFi users. In our report on the protocol last year, we highlighted its long-term vision to build out the “holy trinity of DeFi.” This includes three important components: a stablecoin system, a lending market, and an exchange.

A lot has transpired since then. In the last year, they’ve launched Fraxlend and Fraxswap to complete the trinity, alongside several other products. This post will look at Frax’s newer product launches and examine their traction.

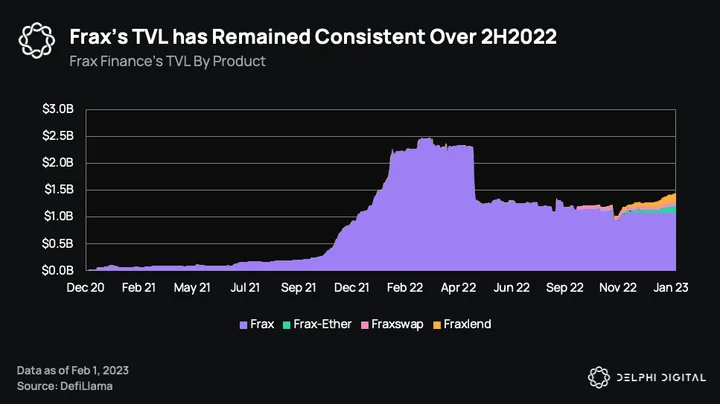

The FRAX Stablecoin

Frax’s USD-pegged stablecoin has grown to become the fifth largest stablecoin, with a market capitalization of $1B. The market cap dipped meaningfully after the UST crash last year, which sent demand for FRAX lower due to concerns about the fractional algorithmic stablecoin protocol. Although the FRAX supply hasn’t quite recovered to ATHs, it is still the largest stablecoin in the market with an algorithmic component.

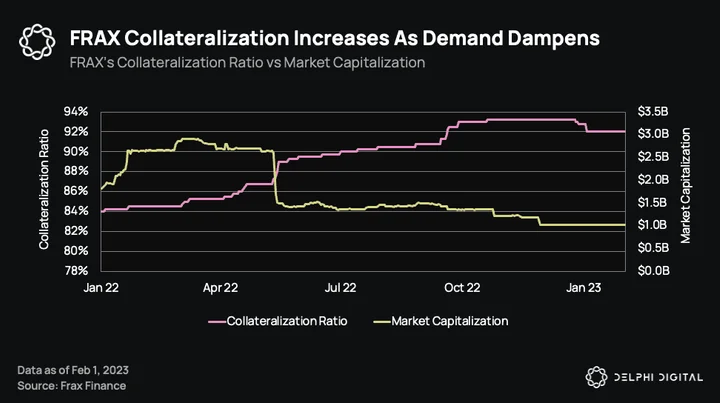

FRAX is not truly an algo-stable in the way UST was. It’s partially backed by collateral and the protocol’s native governance token, FXS. Each FRAX token can be minted and redeemed from the protocol for $1 of value. The collateralization ratio indicates the proportion of collateral that backs FRAX. This number sits at 92% currently, up from 82% a year ago. This means that every FRAX minted requires $0.92 of collateral and $0.08 of FXS burnt. A higher collateralization ratio versus a year ago reflects comparatively lower demand for FRAX.

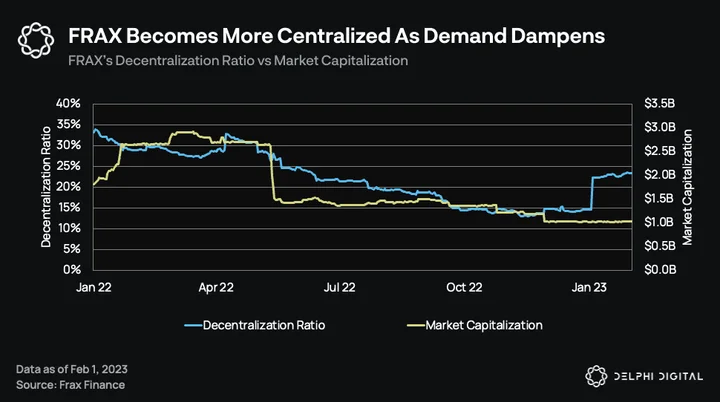

FRAX’s decentralization ratio (DR) is 22.5%. The DR is the ratio of decentralized collateral value over the total stablecoin supply that can be redeemed for those assets. Put simply, it represents the proportion of collateral value coming from decentralized sources. Centralized stablecoins like USDC and USDT are counted as 0% decentralized, while assets like ETH, CVX, or lending AMOs where borrowers overcollateralize their loans with sOHM are considered 100% decentralized.

A decentralization ratio of 22.5% means that FRAX’s collateral backing heavily relies on censorable assets — even more so than stablecoins like LUSD and DAI, which have ratios of 100% (being backed fully by ETH) and 33%, respectively.

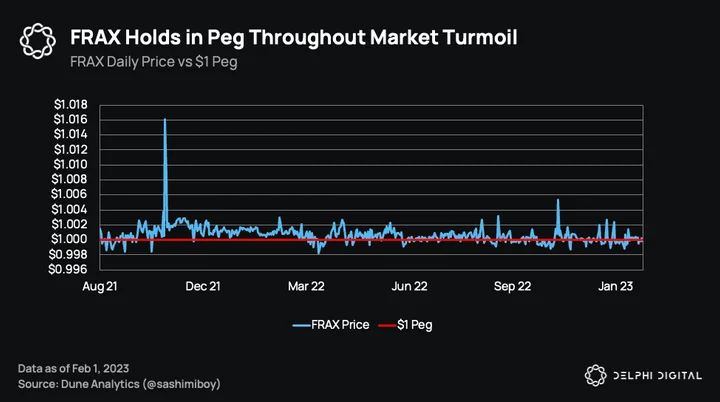

Although FRAX’s decentralization ratio is far from ideal and collateralization has increased from last year, this can be interpreted as a system that works to manage the price stability of FRAX. Over the same period, FRAX has barely deviated from its $1 peg, managing to survive the LUNA/UST fallout and recent market downturn. So while the reliance on centralized assets isn’t great, Frax’s ability to adjust its collateralization and decentralization ratios according to market conditions has proven to be an advantage in keeping FRAX’s price peg — by far the most important thing for a stablecoin.

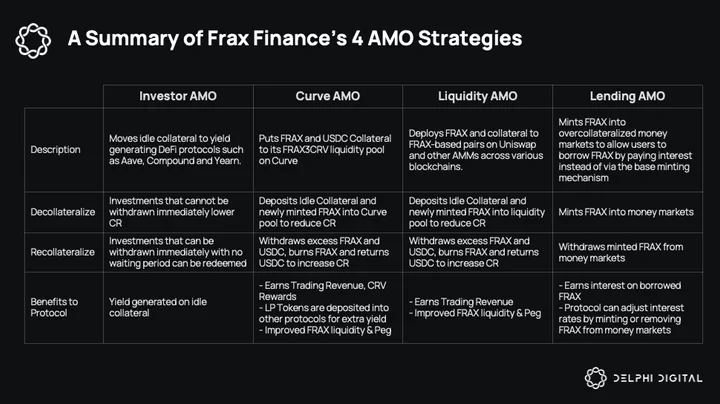

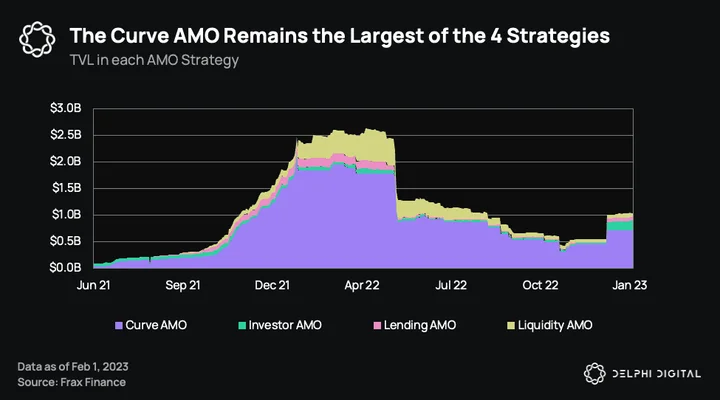

Algorithmic Market Operations (AMOs)

FRAX maintains its stability via “algorithmic market operations controller” (AMOs), which allow the protocol to programmatically regulate the supply and demand of FRAX and its collateral in the market. Frax is running four such AMOs, which we briefly explained in our previous report. A summary of how each strategy works is outlined in the table below:

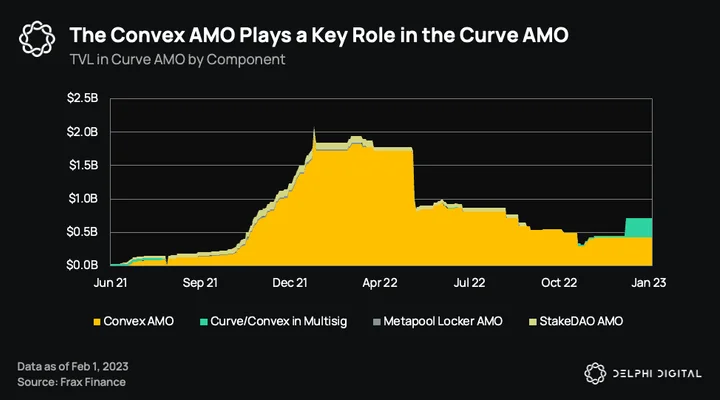

Curve AMO

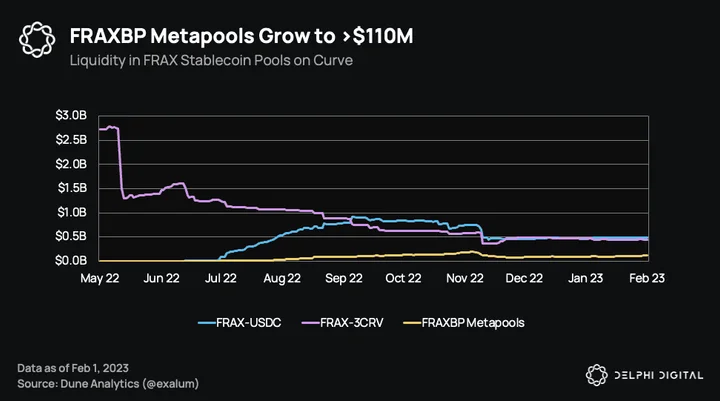

A look under the hood shows that the majority of the Convex AMO LP positions are FRAX-USDC basepool (FBP) LP tokens, which are owned by the protocol. Their ownership makes up 54% of the FBP, allowing them to farm CRV and CVX emissions on Convex with this LP position. These rewards are recycled back into bribes that increase the Curve rewards directed to LPs in that pool. Before Frax launched the FBP in May 2022, they were primarily doing this with the FRAX3CRV liquidity pool, which at its peak had a value of nearly $3B (that number has now dropped to ~$450M).

Frax has encouraged the formation of metapools by redirecting token incentives to these newly created Frax pairs. Pairing another stablecoin with FBP in a metapool increases demand for FRAX-USDC. Since the Curve AMO can mint FRAX into the FBP to balance this new demand, it results in Frax earning more fees and rewards from CRV and CVX emissions.

The Frax team has thus agreed to direct the rewards back to the third-party stablecoin’s metapool, benefiting both the stablecoin and FRAX with deeper liquidity. Furthermore, the Frax team also seeded a few metapools including BUSD, GUSD, LUSD, and sUSD. The total liquidity in FBP metapools currently amounts to over $110M.

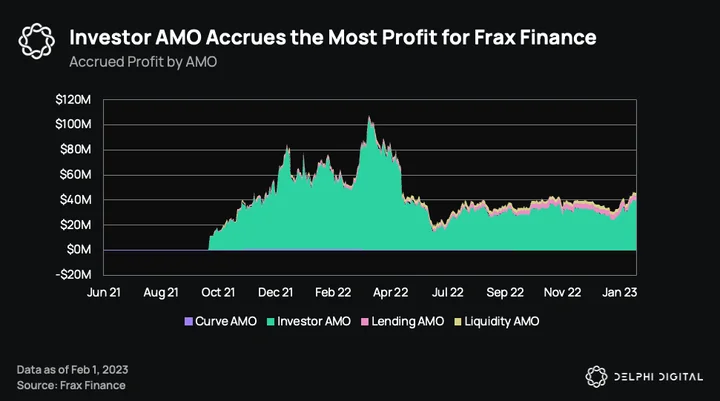

Investor AMO

A smaller but synergistic AMO we’d like to touch on is the investor AMO, which has generated over 90% of all accrued profits. The investor AMO holds the protocol’s profits and deploys them to other protocols to generate yield. Some of the AMO revenue is held by the protocol, such as farmed CVX and CRV tokens, which gives Frax influence over governance and token emissions while some of the revenue goes to veFXS holders.

The largest component of the investor AMO is stkcvxFPIFRAX, which is protocol-owned liquidity in the FPI-FRAX Curve pool generating yield on Convex.

To explain what Frax does with the yield generated on this holding, we must first understand how the FPI token works.

FPI Stablecoin/FPIS

FPI (Frax Price Index) is a token pegged to real inflation measured by the 12-month inflation rate reported by the US Federal Government. Like the first FRAX stablecoin, all FPI assets and market operations are on-chain and use AMO contracts. Users can mint FPI by depositing FRAX, which acts as the collateral backing FPI.

In February of last year, Frax conducted a Frax Price Index Share (FPIS) airdrop to veFXS holders, which resulted in a surge of FXS stakers. FPIS is the governance token for FPI.

FPI is designed to keep a 100% collateralization ratio at all times, which means that the collateral backing it must minimally grow at the rate of CPI inflation. FRAX collateral backing FPI is thus deployed into yield-bearing strategies proportional to CPI. If the yield generated is lower than the CPI rate, the AMO will mint and sell FPIS tokens for FRAX to keep the CR at 100%. If the yield generated is higher than the inflation rate, excess yield will be directed to FPIS holders. FPIS has experienced a significant drawdown since it first launched, falling over 90% post-airdrop. A lower FPIS price gives the protocol less wiggle room if yields do indeed fall below the rate of inflation.

Going back to Frax’s protocol-owned stkcvxFPIFRAX, the yield generated on this is used to keep the FPI collateral ratio at 100% should the rate of inflation increase. If FPI is 100% collateralized by FRAX, excess yields technically belong to the FPI balance sheet controlled by FPIS holders.

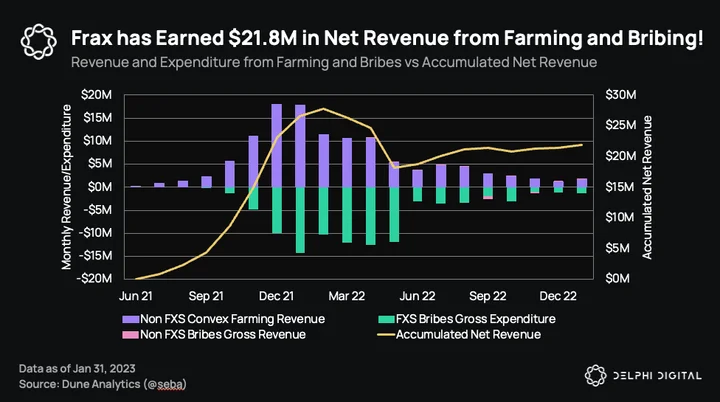

The next largest holding in the investor AMO is locked CVX. With 3.52M CVX, Frax is the largest holder of CVX, which makes up ~6.5% of all locked CVX. Locking CVX allows Frax to earn fees and vote for token emissions to be directed to its stablecoin pools on Curve. Combined with the ability to bribe CVX holders to direct token emissions to their Curve pools and their ownership of said pools, they’ve managed to farm over $21M in token rewards net of bribe expenditures. They’ve done all of this while ensuring deep liquidity for stablecoin pools on Curve.

As you may have already gathered, Frax’s AMOs depend heavily on liquidity infrastructure protocols across the DeFi stack, and we’ve seen how their reliance on Curve’s liquidity pools and Convex’s reward mechanism has benefited both FPI and FRAX.

Fraxlend and Fraxswap somewhat reduce this reliance on third-party protocols to operate Frax’s AMOs.

Fraxswap

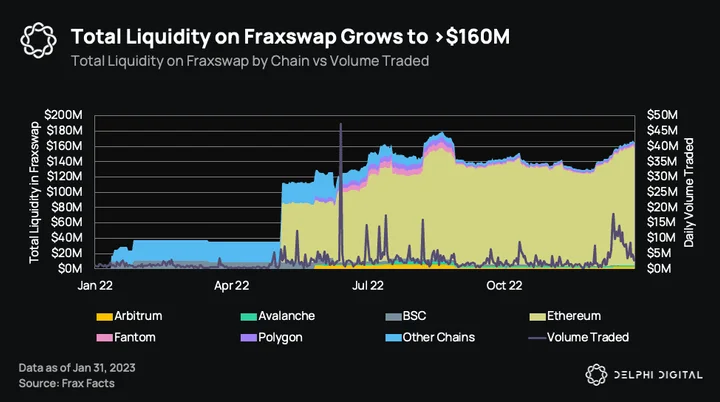

Fraxswap is the first constant-product automated market maker with an embedded time-weighted average market maker (TWAMM) for trustlessly conducting large trades over long periods of time. Since its launch, Fraxswap has been used to increase the stability of Frax’s stablecoins and for minting and burning FRAX. The total liquidity on Fraxswap is around $160M, with average daily volume of $6.3M over the last 30 days.

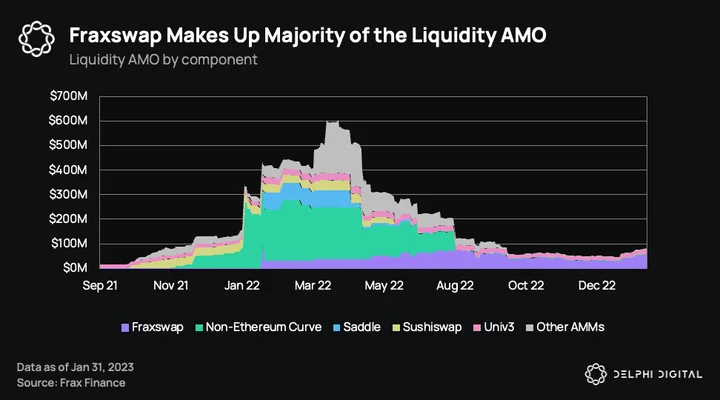

Fraxswap has become a major component of the protocol’s liquidity AMO. About 70% of FRAX in the liquidity AMO is in Fraxswap. Prior to the launch of Fraxswap, Curve had the most abundant FRAX liquidity, followed by Uniswap. Clearly, the launch of Fraxswap has allowed Frax to reduce its reliance on other AMMs for its AMO strategy. However, its usage and total value locked are a drop in the ocean compared to other decentralized exchanges.

Fraxlend

Similar to Fraxswap, Fraxlend has reduced the lending AMO’s load on other money markets. Frax’s native money market allows the protocol to lend FRAX directly and earn interest income.

Fraxlend’s money market is made of isolated token pairs, allowing users to deposit one type of crypto asset and borrow another. For typical money markets, such a design might be considered capital inefficient, as many different combinations of token pairs would have to be created (resulting in fragmented liquidity). However, this is not a problem for Frax at the moment since the only asset being borrowed is FRAX.

Fraxlend also supports custom term sheets for OTC debt structuring by allowing DAOs to customize parameters such as maturity dates, whitelisting, borrowers and lenders, etc.

With Fraxlend and Fraxswap making up the majority of the lending and liquidity AMOs, Frax looks to be on track to build a fully (and natively) permissionless economy around the FRAX stablecoin. Yet another product recently introduced to the Frax Finance ecosystem is Frax Ether.

Frax Ether

Frax Ether (frxETH), as the name suggests, is a liquid staking derivative (LSD) pegged to the price of ETH. Frax built an entire staking strategy around the product and used the same tools in its toolkit to incentivize deep liquidity in its curve liquidity pools as well as offer superior yields compared to other LSDs.

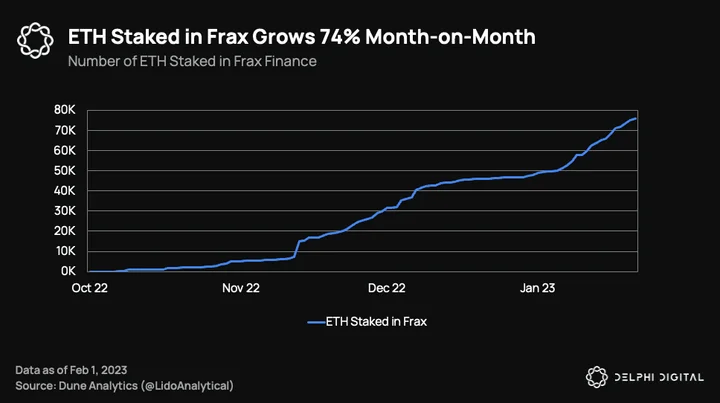

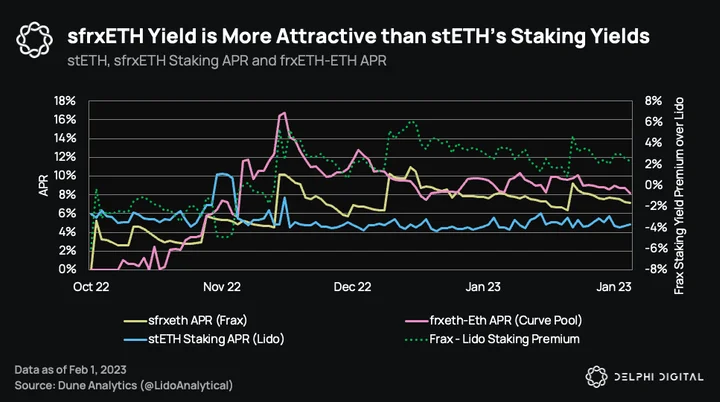

We recently covered Frax’s LSD model in a report titled “The Future of ETH Liquid Staking,” where we detailed how Frax provides enhanced ETH staking yields. Frax Ether is the fastest growing liquid staking service, with over 75k ETH staked — up 74% MoM.

This is likely attributable to its superior staking yields (~7.2%) compared to other liquid staking derivatives like stETH (~4.8%). This yield premium will be sustained as long as the APR on the frxETH-ETH Curve pool exceeds the ETH staking yield.

Conclusion

On the surface, Frax seems to have a hand in many things, but zooming out and viewing each piece and how they complement one another brings everything into focus.

With that in mind, they are certainly on the path to growth. They’ve added two new Frax tokens — FPI and frxETH — to their portfolio, and even completed the DeFi trinity with Fraxswap and Fraxlend.

However, there is still room for improvement. Both their in-house lending market and decentralized exchange remain a small piece of the entire Frax ecosystem compared to other pieces of liquidity infrastructure Frax relies on. Perhaps comparing these newer products to incumbent DeFi protocols is premature. Nevertheless, it’s important to monitor the growth of these newer products to determine Frax’s ability to become self-reliant.

Frax’s cross-chain liquidity also leaves much to be desired. The amount of FRAX deployed on non-Ethereum AMMs is down 70% YoY.

Frax isn’t alone in its goal of creating a comprehensive, self-reliant DeFi stack. Protocols like Curve and Aave have already announced plans to create their own stablecoins. These projects are well established in their respective sectors, with triple the TVL of Frax, and may well threaten Frax’s dominance in the stablecoin arena.

Interestingly, Frax has relied on both of these protocols for its AMOs and has established a mutually beneficial relationship with them. Perhaps we could see this synergy play out in the near future with GHO and crvUSD. For now, what Frax has is a firm footing with a battle-tested decentralized stablecoin and a head start in building out infrastructure for a thriving DeFi ecosystem.

Special thanks to Cheryl Ho for designing the cover image for this report and to Ashwath Balakrishnan and Brian McRae for editing.

0 Comments