Re-Evaluating The Decentralized Derivatives Landscape

JUN 07, 2022 • 37 Min Read

Report Summary

The market share of decentralized derivatives exchanges is up 10x from one year ago but still only sits at 2% vs CEXs. DEXs are a flagship product for crypto but still have a long way to go in terms of speed, liquidity, UX, and composability in order to truly compete with their centralized counterparts.

The first iteration of vAMMs with no real liquidity — Perpetual Protocol v1 and Drift Protocol — have ran into significant obstacles, the most prominent of which is “terminal price reversion”. Critical issues with this model have led us to the conclusion that pure vAMMs with no liquidity do not work as intended.

The second iteration of vAMMs looks to learn from its predecessors and incorporate real liquidity. Rage Trade puts an interesting spin on vAMMs with real liquidity by using the concept of “recycled liquidity” where they allow users to deposit LP positions to back the virtual liquidity. Perpetual Protocol v2 uses USDC liquidity to create range orders consisting of virtual tokens in Uniswap v3.

Using oracle-based pricing, GMX has built a sleek DEX to facilitate spot swaps and margin trading. By importing pricing from exchanges like Binance rather than incurring the cost of finding an asset’s true price a la Uniswap/Perpetual Protocol, GMX’s model gives traders a good UX without punishing LPs. But this model isn’t without its flaws.

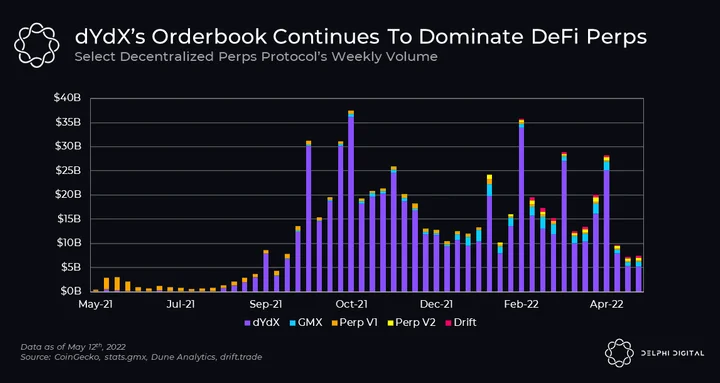

dYdX is the king of decentralized futures, accounting for over 85% of on-chain perp volume. However, this smooth experience is partly facilitated by dYdX hosting their trading and matching engine on Amazon Web Services (AWS). With dYdX v4, the team plans to further decentralize the trading and matching engine. v4 may also help DYDX become a value accruing token.

The decentralized futures market is quite young and different models are still being tried and tested. Ultimately, we think the end game leads us back to orderbooks and exchanges like dYdX that can rival CEXs in user experience but also have the added benefits of composability that blockchains can bring. But the final word is far from in.

Introduction

Decentralized exchanges (DEX) are arguably the most successful applications in the smart contract era. Blockchains are built to secure high value transactions, and applications like Uniswap consistently account for a large portion of Ethereum’s everyday usage. DEXs, at large, have established themselves as marquee applications across each and every smart contract platform.

Being a successful DEX is no easy feat, especially when you look at the broader crypto ecosystem, including centralized competitors. In this world, DEXs must offer similar speed, fees, and liquidity to customers in order to rival centralized counterparts. All this while dealing with the current scaling limitation of blockchains.

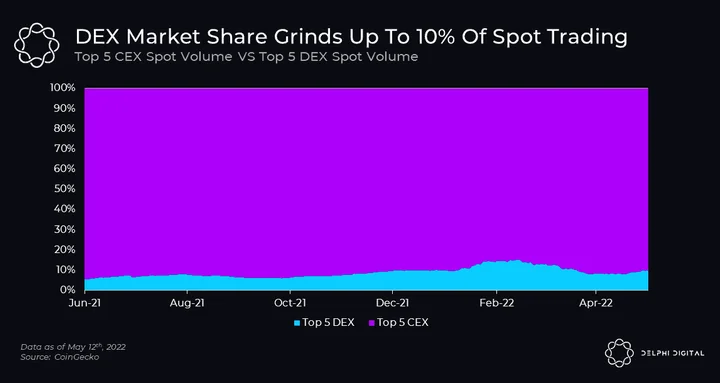

Currently, the top DEXs account for nearly 11% of all crypto spot volume. This figure has been slowly growing, sitting at roughly 6% a year ago. As these products become more advanced alongside the underlying blockchains, we expect activity to expand and DEXs to capture more market share.

DEXs have had significant improvements since the launch of Bancor and Uniswap’s X*Y=K liquidity pools in 2018. We are now unearthing more efficient models like concentrated liquidity and, if the chain is fast enough, oracle-based pricing as well as orderbooks.

However, the end game is not yet in sight for DEXs. There’s still a long, arduous path of painstaking innovation and consumer adoption to make these platforms truly competitive with CEXs like Binance, Coinbase, and FTX. Blockchains are beginning to find their feet in the race to build scalable distributed systems. As we expand the speed and amount of activity these networks can support, the design space for DEXs progressively becomes more inviting.

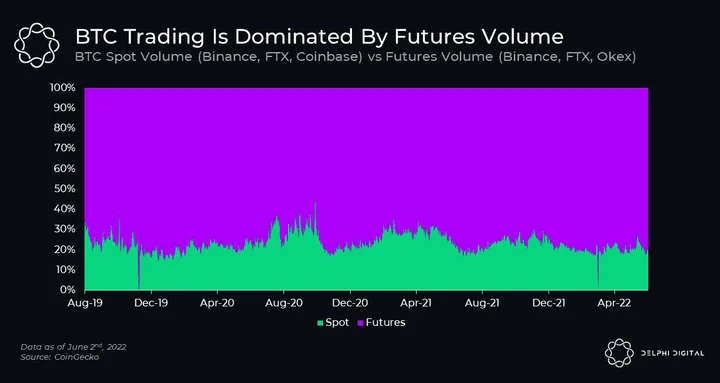

Derivatives are cumulatively the largest market in the world by notional size. Crypto is no stranger to this phenomenon, with volume dominated by derivative instruments.

The most popular derivative contract within crypto is the perpetual swap, or perpetual future. If you’ve been in crypto for more than a few months, you’ve definitely at least heard of “perps.”

For those who are unfamiliar, perpetual contracts are derivatives that constantly settle and have no expiration. This contract allows users to go long or short assets with significant leverage. They anchor themselves to the underlying asset’s market price through a funding rate mechanism. When the price of the perpetual contract is higher than the underlying’s spot price, the funding rate is positive – meaning longs pay the funding rate to shorts. The opposite occurs when the perp contract trades lower than the underlying spot price.

There are indeed decentralized perpetual swap contracts, however, their traction relative to centralized platforms isn’t quite there yet. Constructing instruments like perpetual futures is a more complex process than simple spot swaps.

As a result, the shift from centralized to decentralized will take some time. However, this also presents a potential opportunity to investors. If you expect the trends of the spot market to be reflected in the burgeoning derivatives market, decentralized derivatives platforms suddenly look a lot more interesting.

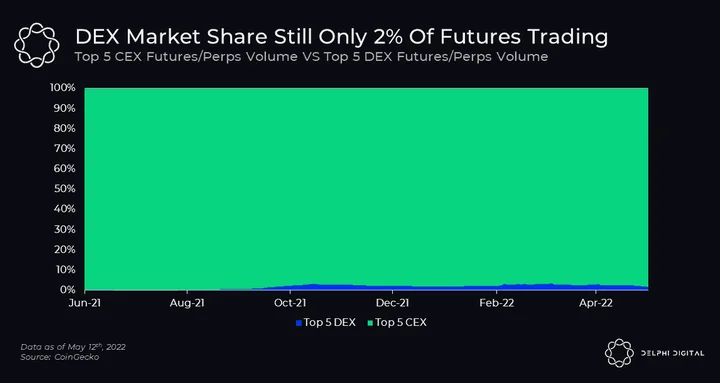

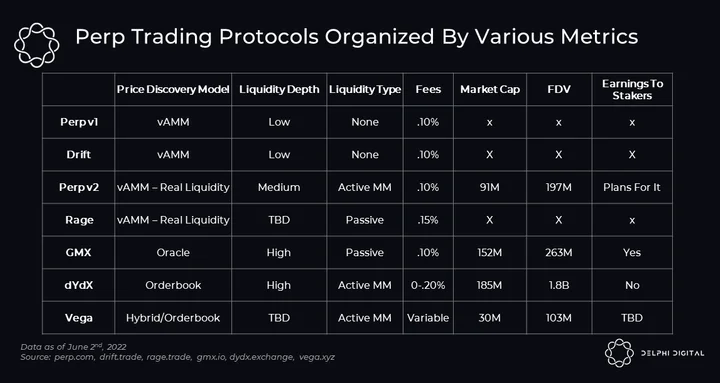

The top five decentralized perp exchanges accounted for 20 bps (0.2%) of total volume a year ago and have grown to ~2% today – a 10x increase with way more room to grow. The following are the top five decentralized perpetual trading platforms by recent volume: dYdX, GMX, Perp v2, Perp v1, and Drift.

This post examines the top models for on-chain trading and touches upon their pros and cons from the perspective of three entities: traders, liquidity providers, and token holders. We will examine four different models: vAMMs, vAMMs with real liquidity, oracle pricing, and orderbooks.

Fundamentally for these decentralized exchanges to compete, we believe they must achieve the following:

- Overcome the chicken and egg problem of liquidity and utilization. You need good liquidity to incentivize trading, but you need high trading volume (high fees) to attract significant liquidity.

- Composability and cross margining. Ex: being able to use native forms of crypto collateral (like LP shares) to collateralize leveraged positions. Composability is a distinct advantage DEXs hold over their centralized counterparts.

- A strong UX for both traders and liquidity providers. The winner of the decentralized derivatives race will be able to create a UX that rivals centralized exchanges for all involved parties.

- A token that makes sense, provides holders with value, and generates more earnings than it pays out in emissions.

Without further ado, let’s look at the leading perpetual trading platforms and examine their strengths and weaknesses.

Perpetual Protocol v1

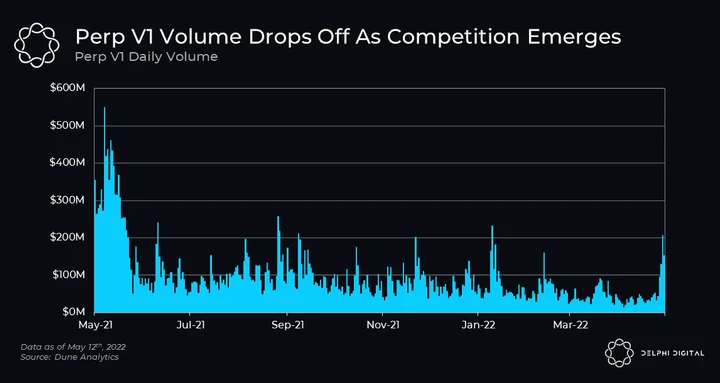

Perpetual Protocol v1 was the first implementation of a virtual AMM (vAMM), used to create perp contracts on the xDAI network. While successful in attracting volume, much of this came from arbitrageurs (explained later) rather than organic demand, and the protocol ran into some critical issues that resulted in the creation of v2.

vAMMs are trading systems designed to replicate the liquidity depth of an AMM without actually having any liquidity. As the name suggests, the liquidity depth of these AMMs is derived from setting virtual parameters. Instead of setting up a Uniswap v2 pool with $5M in each of ETH and USDC, you create a virtual AMM that is a replica of the v2 pool’s liquidity curve as if it had $5M of ETH and USDC.

The key problem with this version of vAMMs is that the protocol has a static K factor per the XYK equation that constant product AMMs abide by. X*Y=K is the core equation that governs liquidity behavior in 50-50 AMMs pools. X is the amount of asset 1, Y is the amount of asset 2, and K is the product of X and Y. In traditional Uniswap pools, K is a continuously changing number since liquidity is constantly being removed and added for both assets.

Now because vAMMs have a static K, liquidity depth stays the same. So when the price of one asset in a pool moves heavily in one direction, liquidity for the appreciating asset contracts as it moves closer and closer to the tail end of liquidity. This poses a major risk during a period of trending price action as it doesn’t reflect true liquidity conditions.

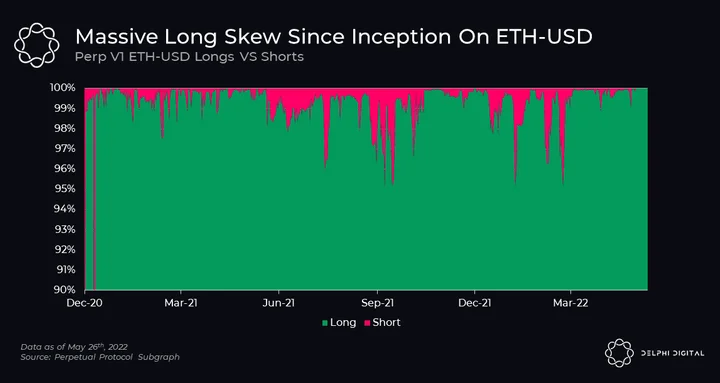

Perp v1’s ETH market was launched in Dec. 2020 as ETH traded around $800 and was mounting a rally towards its previous all-time high of $1.4K. We all know what happened next. Within six months, ETH was trading around $4K. To make Perpetual Protocol a viable place to trade, the vAMM had to keep up with the increase in spot prices.

This was done by arbitrageurs entering long positions (and keeping them open) on ETH to push the vAMM price up. Arbitrageurs were compelled to do this because the vAMM price was lagging the spot price, and if you recall from our explanation of perps, when perp price < index price, shorts have to pay longs. Additionally, a meaningful portion of open interest – at least early on – was held by the Perpetual Protocol team’s trading bot. This bot was essentially a public good that tried to keep prices in line with other venues rather than turn a profit.

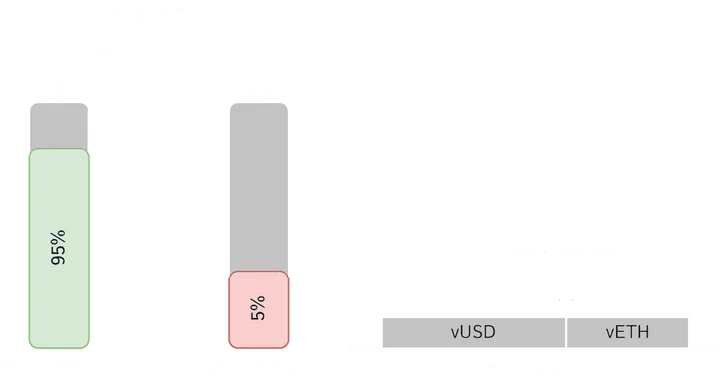

In order to keep the ETH price in line with spot markets, it required a sizeable amount of long positions on the platform to stay open, leading to the ratio of longs-to-shorts consistently being upwards of 95:5.

You might wonder how shorts even managed to pay longs if 95% of open interest were longs and only 5% were shorts. Well, the protocol’s insurance fund essentially backstopped this and paid longs. Again, the reason the protocol was needed to do this was because of a “terminal price reversion” issue. Since liquidity was virtual and the K factor was static, if all positions on Perpetual Protocol v1 were closed out, the contract price would revert to where it was when the pool was initiated in Dec. 2020 – $800 per ETH.

In essence, if a decent amount of longs closed their positions on Perp v1, the contract price would tank far below the market value of the underlying asset — which happened a few times during volatile periods. This means that arbitrageurs were incentivized to keep prices inline with other exchanges by earning high funding rates on their open positions. But at the end of the day, if these long positions were to close, they would not be able to sell their ETH at the “true” spot price. They would have to sell at the price of the vAMM — which could lead to significant losses.

While this iteration of vAMMs unlocked superior capital efficiency, the core mechanisms holding it in place weren’t suited to cater to a market with high volatility and monster trend expansions.

Note: we will discuss the PERP token as we unpack Perpetual Protocol v2.

Drift Protocol

Building on Perpetual Protocol’s v1 model, Drift is a vAMM that introduced a few elements in the hopes of tackling some core issues.

Firstly, Drift uses a dynamic K factor in their X*Y=K equation, which changes liquidity depth as an asset’s price normalizes at a new level. Recall that in Perp v1 the K factor is static, so the liquidity curve stays the same from inception. By introducing a dynamic K, liquidity rebalances, allowing for deeper liquidity around current prices.

Note: Drift’s take on the vAMM was dubbed “dAMMs” or dynamic AMMs by the team. For the sake of comparison, we will continue to term it as an iteration of the vAMM model — which it is.

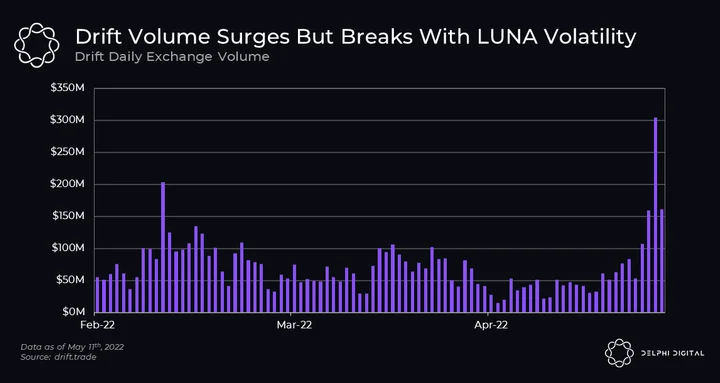

Thus, Drift created perp markets that were more resilient to the terminal price issue, but not enough to fully fix it. The recent Terra (LUNC) collapse showed us just how bad these issues can be, essentially breaking Drift due to its crazy volatility last month — which we’ll get to shortly.

With an understanding of Drift’s vAMM model (Perp v1 with some tweaks), we can now dive into the different participant groups.

As a vAMM, there are no liquidity providers. The closest thing to liquidity providers are the limit orders stacked against the AMM. But this doesn’t affect liquidity depth, as that’s derived from the vAMM.

Traders on the platform have a better experience versus older vAMMs. Aside from the obvious benefit of limit orders, the dynamic K means liquidity depth doesn’t get out of whack as price drifts further and further away from where it was when the perp contract was first initiated.

By operating on a high-speed chain like Solana, Drift was able to build an orderbook on top of the vAMM. This means you can place limit orders that trade against the vAMM. Now if you’re familiar with how orderbooks work vs AMMs, you’re probably wondering how you can have limit orders placed against an AMM.

The way this works is relatively simple: a user submits a limit order, and that limit order is essentially a way of saying “when market price hits x, execute the order on the AMM.” Because it’s not a true limit order but rather a mandate to trigger a market order at a certain price, there is some slippage involved with limit orders depending on position size. But at least it gives users the ability to execute within certain price bands. Limit orders are a key component to dynamic market making and trading, making for better UX overall.

Now, back to the core mechanics. We’ve established Drift has learned from the misgivings of Perpetual Protocol v1 by using a dynamic K factor to ensure liquidity is strong during any market condition. At first glance, the issues with a static K seem to have more or less been neutralized. Or have they?

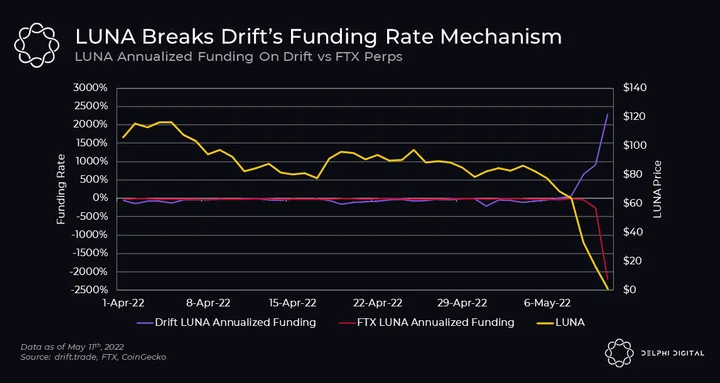

Funding rates on Drift can and have deviated very meaningfully from CEX perps, precisely because the long-short skew problem was never really rectified. While all Drift positions can be closed without moving market price all the way to the “terminal price,” it still causes a significant deviation in the perp contract’s price from other trading venues. Simply put, this model still needs open interest to scale in accordance with price moves to function correctly. Meaning excess longs as price goes up, and excess shorts as price goes down.

This was put on display amidst the Terra collapse last month. As LUNA’s (now LUNC) price fell from around $70 to under $1 over a few days.

With LUNA’s price in a free fall, many traders were pilling into shorts on centralized exchanges like FTX, looking to profit, and they needed to pay extremely high funding for the privilege of getting this downside exposure. On the contrary, Drift needed a significant amount of shorts to be opened on the platform in order to keep their vAMM price (initiated at a much higher LUNA price) in line with the broader market or “true price” of LUNA. This caused Drift’s LUNA funding rate to skyrocket, meaning longs/the protocol had to pay astronomical funding to incentivize the short side to keep Drift’s vAMM prices accurate.

The LUNA fiasco on Drift unearthed a bug that led to the team deciding to sunset Drift Protocol v1 and focus on the second iteration of the product. While the bug is unrelated to the efficacy of vAMMs, it’s strikingly clear that real liquidity is much more valuable and resilient than virtual liquidity. On the whole, the flaws in this iteration of the vAMM model (with no liquidity) make it difficult for this type of DEX to reflect true market prices. Despite the obvious capital efficiency benefits of vAMMs, it’s difficult to back a model that can’t be autonomously successful.

Perpetual Protocol v2

After learning from the struggles of fully virtual liquidity with Perp v1, the team launched the second iteration of Perpetual Protocol in Nov. 2021.

Perp v2 works off a vAMM deployed on Uniswap v3 – but this time, it’s backed with real liquidity in the form of USDC. For example, in an ETH-USDC market, LPs deposit USDC into the clearinghouse (Perp v2’s trading engine) which allows them to deploy a range order of virtual USDC and virtual ETH. These orders can take three different forms:

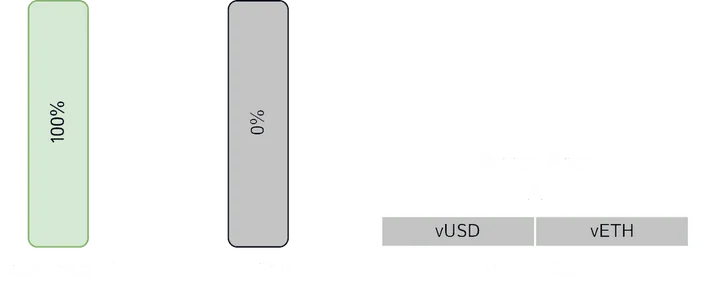

- The price of ETH is above your range order; this means 100% of your liquidity is in vUSDC.

- The price of ETH is within your range order; this means your liquidity is in a mix of vUSDC and vETH.

- The price of ETH is below your range order; this means 100% of your liquidity is in vETH.

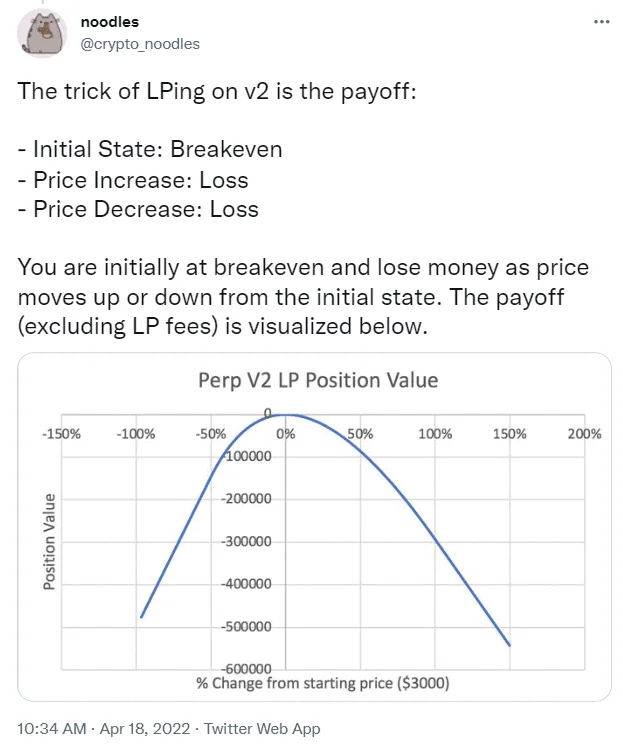

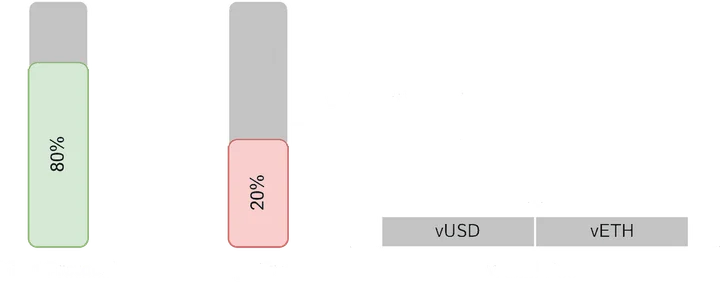

Let’s go through an example to help us better understand how providing liquidity here works. Let’s say Perpetual Protocol deploys a range order with equal parts vUSDC and vETH around the current price. When the price of ETH goes up, due to natural trades and arbitrage, it causes the LP to sell their vETH to traders for vUSDC, giving LPs short ETH exposure. If the price of ETH continues to go up, LPs lose out in two ways — firstly, because they are short ETH (counterparty to traders who can swap back the vETH into the pool whenever they want), and secondly, because they don’t actually own any ETH (vETH).

Remember, in options 2 and 3, since you are providing all liquidity in USDC, you receive the vETH by a “loan”. This means that when LPs withdraw liquidity, they must pay back the value of the ETH at the current price, not the price they borrowed it at. This can result in very poor returns for un-hedged LPs in an upward trending market. LPs can also lose money if the price of ETH goes down. If the price of ETH goes down due to natural trades and arbitrage, it causes the LP to sell vUSDC to traders for vETH, putting them in a long position. Like we said before, traders can now sell this vUSDC back into the pool at any time with LPs acting as the counterparty. This means as an LP, your payoff function looks something like the image below (shout out to @crypto_noodles who helped inspire this research).

Being an LP in Uniswap v3 is hard enough on its own — you can read this paper for a detailed analysis of LP profitability. Allowing LPs to only provide liquidity in USDC exacerbates this problem even further. LPs are making an implicit bet that prices won’t move meaningfully from where they deployed their liquidity and if it does, fees will make up for this. This is a bet with limited upside but huge downside risk, making Perp v2 unattractive for LPs unless they are a sophisticated market maker that can hedge out exposure on other exchanges.

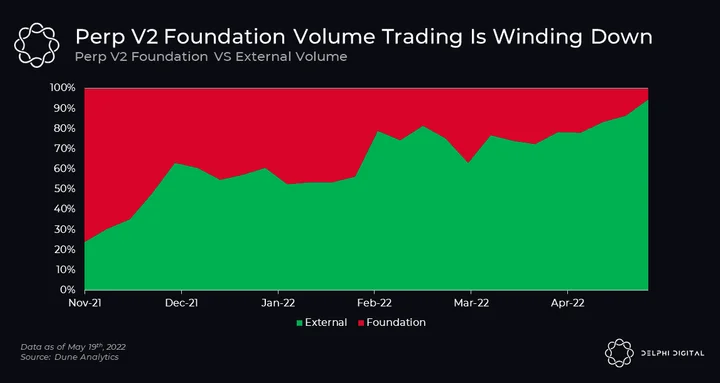

Given how hard it is to be a passive LP, the Perpetual Protocol team has been providing liquidity and trading in their own markets to bootstrap depth and activity. They have also been hard at work onboarding market makers to ensure tighter spreads and deeper liquidity (more on this later).

From a trader’s point of view, you have a wide selection of assets to trade with up to 10x leverage. Traders bridge over to Optimism and deposit USDC or ETH into the Perp v2 clearinghouse. This will automatically mint you 10x the tokens in the form of vUSDC or vETH. Users can then use some or all of these tokens to trade in various markets depending on the leverage they wish to use.

When opening positions on Perp v2, you must account for open/close fees, funding, and slippage. Open/close fees are fixed at 10 bps; funding, as we know, depends on the difference between the perp price (mark price) and the spot price of the underlying asset (index price). If the mark price is greater than the spot price, then longs must pay shorts funding and vice versa.

As mentioned earlier the Perp team has been trading and LPing in their own markets but is slowly weaning off, which is a good sign for the health of the ecosystem and platform.

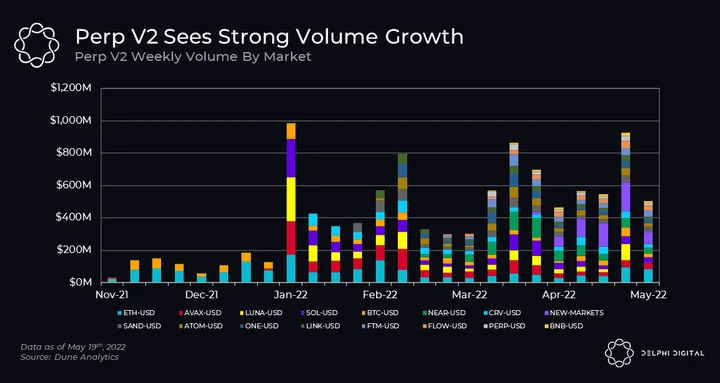

We have seen foundation trading volumes decrease significantly since launch in Nov. 2021. More market markers seem to be coming to Perp v2 and the team is hard at working making deals like this to onboard them.

Now for the good stuff. Perpetual Protocol is currently revamping their token economics to a veToken model. If you are not familiar with the veToken model, it’s a bit outside the scope of this report, but you can read our veToken research here. The basic idea is that PERP holders will be able to lock up their tokens as vePERP for up to 1 year. vePERP holders are then entitled to a portion of fees and are able to direct future PERP emissions to various vaults (ex ETH-USDC), which are then distributed to LPs. This incentivizes DAOs or projects to accumulate vePERP and direct emissions to their asset pairs, incentivizing deeper liquidity/usage.

Currently, the majority of fees generated on Perp v2 are returned to liquidity providers. In the future, the fees will be split between liquidity providers, the insurance fund, the treasury and vePERP. Initially the fees will solely be split between LPs and the insurance fund. Once the insurance fund is full, its portion of fees will flow to the treasury and vePERP holders.

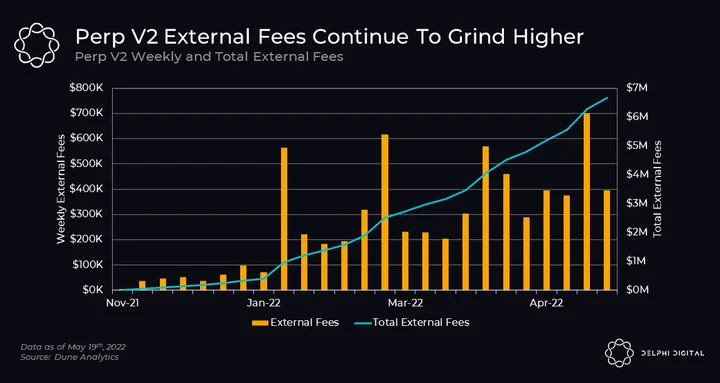

Fees generated by non-foundation trading amount to nearly $7M. Currently, 90% of this is distributed to LPs. The exact flow of fees to token holders is yet to be established, but you can learn more and follow along on the Perp governance forum here. Perp v2 is still relatively young and its token economics have not been finalized. Given the inflationary nature of PERP in the veToken model, and number costs that must be covered by fees (LPs, Treasury, Insurance Fund), we would need to see a significant uptick in volume to see meaningful value accrue back to vePERP token holders.

In conclusion, we are generally skeptical that any form of AMM or vAMM will be the end game for decentralized perps. AMMs incur a high cost of price discovery versus an oracle model (that always uses the “true” price) or orderbooks, which allow market makers to pull and re-add liquidity as they see fit. The Perp v2 model also doesn’t seem to capture one of the main benefits that is associated with AMMs — a passive liquidity provision experience.

GMX

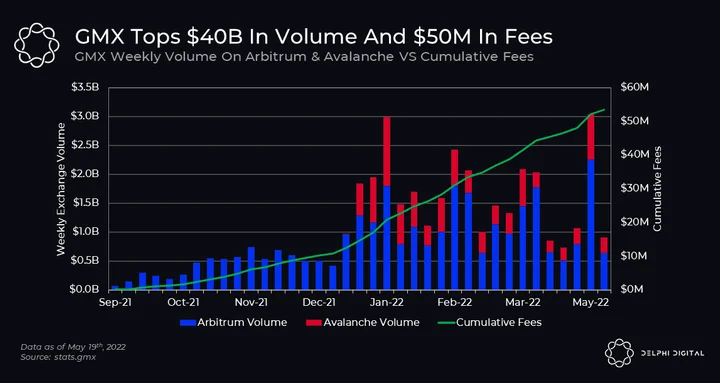

GMX offers spot swap and margin trading, allowing users to execute the full size of their trade with zero slippage by pricing assets using an oracle. GMX launched Sept. 1, 2021 on Arbitrum and Jan. 5, 2022 on Avalanche. It’s worth noting GMX doesn’t technically offer perps, but the integrated margin trading model reflects the simplicity of opening or closing a perp position. For this reason, we believe it’s a genuine competitor to the projects listed in this report.

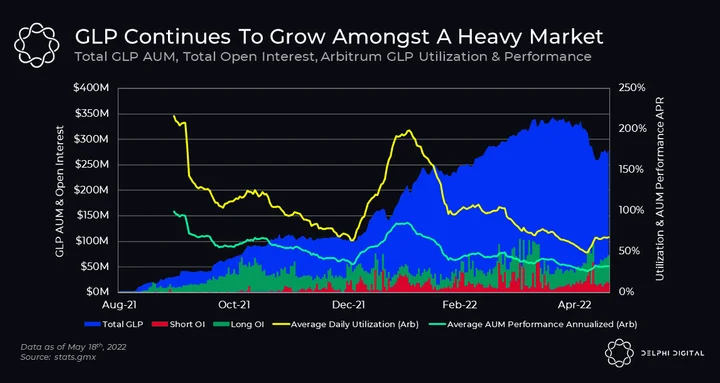

Users provide liquidity to GMX through GLP. GLP is a basket of assets that includes BTC, ETH, AVAX, UNI, LINK, and stablecoins. Unlike a traditional AMM, GLP does not incur the cost of finding or readjusting to prices as they change, it instead uses a fast oracle to borrow the “true price” from other trading venues. This allows GLP to be extremely capital-efficient, and doesn’t require it to maintain a certain ratio of one asset to another at all times, allowing it to handle large trades.

GLP also gives traders the ability execute the full size of their trade at this “true price” within liquidity limits, making GMX one the most attractive places to execute spot swaps and margin trades on-chain. Given its superior pricing and ability to facilitate spot and margin trading, it allows GLP to generate an extremely high natural yield. Even with compressing yields across DeFi, GMX has been consistently returning ~30-40% to GLP since February. GLP is entitled to 70% of GMX trading fees, while the other 30% goes to GMX stakers.

Even though these are some pretty incredible statistics, the GLP and oracle model are not without limitations.

The oracle model can not support price discovery on its own. This is not an issue for BTC or ETH, but the limitation kicks in when you begin dealing with longer-tail, illiquid assets. Since in GMX’s current state the full size of the trade is executed with zero slippage, this could allow traders to buy or sell less liquid assets at a price cheaper or more expensive than the true cost.

This can be addressed to a certain extent by GMX implementing some sort of synthetic slippage, but for now, this will likely limit the assets GMX can offer to only the most liquid of names.

In GMX’s model, the counterparty to positions on the platform is always the GLP basket (i.e. LPs). If a user wishes to enter a levered long on ETH, it can be described as “renting out” the upside of ETH in GLP to the trader. If the trader wants 2 ETH of leverage, 2 ETH from GLP is “rented out” to give the trader their desired exposure. This means that “open interest” for margin positions on the platform is capped at the availability or utilization of each respective asset in the pool. Similarly, a 2 ETH short at $4,000 per ETH is akin to renting $8,000 worth of USDC/USDT exposure to the trader.

When traders make a profit, GLP incurs a loss and has to payout. But when traders lose money, GLP benefits as the counterparty to traders’ positions. This can expose GMX to edge case scenarios that are very unfavorable (market is going down + traders on the platform are net short = GLP’s BTC/ETH are losing value while they pay out stablecoins to profitable traders).

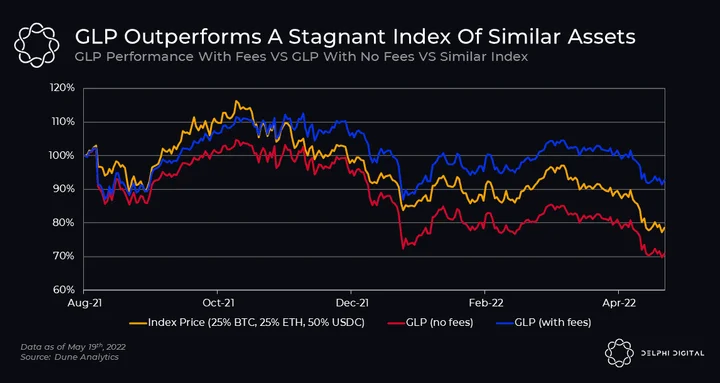

Although this is a genuine risk of the model, so far, traders on GMX have net lost money, meaning the GLP basket has significantly outperformed an index consisting of BTC, ETH and stablecoins with similar weightings.

Overall, this sounds like a pretty good deal for passive LPs, but what about traders? It is also a pretty sweet deal for them too, allowing users to trade any asset within GLP with up to 30x leverage and zero slippage. On Arbitrum, this includes BTC, ETH, UNI, and LINK. On Avalanche, this includes BTC, ETH, and AVAX.

Spots swap fees vary between 0-80 bps depending on whether an asset moves towards or away from their target weights within GLP. The dynamic fee helps keep GLP’s assets at their target weights while keeping it competitive with other AMMs – especially for larger traders, given the zero slippage. For margin trading, fees are fixed at 10 bps and zero slippage while position funding is determined by asset utilization.

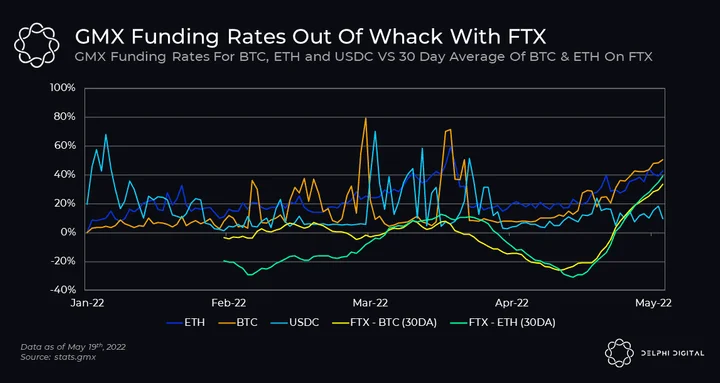

Utilization-based funding can be problematic when balancing out longs and shorts on GMX. Since crypto funding rates have historically been positive (longs pay shorts), it gives traders little reason to hold shorts on GMX for extended periods. But this can also have the opposite effect for longs.

As you can see, both longs and shorts are consistently paying positive funding over time, which differs from that of centralized exchanges like FTX. This is a potential area for improvement with GMX – making funding cheaper across the board or at least somewhat tethered to centralized exchanges. LPs and GMX stakers certainly won’t be complaining about this, given higher rates relative to other platforms increases their returns. However, to remain long-term competitive and scale volumes, it’s important for GMX to ensure some degree of equilibrium with other exchanges.

Beyond this, possibly the most exciting part about GMX is its token economics, which are a big standout in this piece. GMX has strong value accrual that favors long-term investors in the project. Single-sided GMX stakers are entitled to 30% of total fees, which have been ~$16.2M since launch ~ 9 months ago. Annualized, this is a 6.5x P/E at current GMX price of $20.

GMX stakers are paid out in real-time; stakers also accumulate esGMX and Mulitplier Points (MPs) which enforces a “soft lock” on GMX staking and rewards long-term investors.

esGMX can be used in 2 ways:

- Staked for rewards (same as regular GMX token)

- Vested to become actual GMX tokens over 1 year

- To vest your esGMX you must continue to stake the GMX or GLP you earned these tokens with. esGMX is non-transferable.

Multiplier points are earned every second and boost a staker’s share of overall fees. When you unstake your GMX, a portion of your multiplier points are burned. This is a great way to incentivize a “soft lock” on staking and reward long-term investors in the project.

GMX has proven out the efficacy of the oracle model for on-chain trading with liquid assets. Holding GLP has been very profitable thus far for passive LPs. We believe that the oracle model is a very strong niche, but it can never become “the most liquid” or “the top venue” to trade crypto. This is a result of the secret sauce coming from borrowing “the true price” from centralized exchanges rather then incurring the cost of finding that price. This ultimately leads us back to orderbooks as a potential endgame for decentralized derivatives.

dYdX

The most successful on-chain derivatives exchange by volume, dYdX enjoys over 85% market share by volume across on-chain perp exchanges. Unlike the others which utilize either a synthetic asset model (oracle derived pricing) or an AMM to facilitate price discovery, dYdX sticks with the tried and tested orderbook.

For this reason, dYdX’s model doesn’t need much elaboration. Most of finance is built on orderbooks — including centralized exchanges like FTX, Binance, and Coinbase. The funding mechanism, use of an external spot price to index against perp contract prices, and order types (market/limit) are exactly what you would see on a CEX. Most of the time, dYdX funding and pricing is comparable with CEXs.

If you’ve been in crypto for a while, you’ll know orderbooks have historically fared poorly in the Ethereum ecosystem. The names EtherDelta and IDEX are likely to trigger some trauma for Ethereum OGs. So it seemed natural to be skeptical of dYdX’s ability to scale.

dYdX is built on a zk-rollup powered by Starkware (called StarkEx), and as we explain in our previous report titled “The Dawn of Decentralized Derivatives,” dYdX hosts their trading and matching engine through Amazon Web Services (AWS). This essentially means they traded away some decentralization for efficiency gains. However, actual money flows — or settlement — happen on-chain.

dYdX’s use of orderbooks means passive liquidity provision of AMMs or asset baskets like GLP are not feasible. Liquidity provision is left to the more sophisticated players who run algorithms to provide multi-sided liquidity and create a vibrant orderbook. One of the biggest achievements of AMM and oracle-based projects is making the process of providing liquidity accessible to the average asset holder. So while dYdX does not benefit from this advantage, it also means they don’t need to think about liquidity curves and how to maximize LP profitability.

Since market makers are most comfortable with orderbooks, dYdX presents a great opportunity for these entities to wade into on-chain finance. Bolstered by liquidity incentives via the DYDX token, the platform has become the most liquid place to trade perps on-chain. As a result, this has created a great UX for traders: a wide variety of assets to trade, gasless deposits, and an easy-to-use CEX-like interface. They also support a whole host of order types: market orders, limit orders, stop markets, stop limits, fill or kill, good till date, etc. And that’s not all, dYdX offers extremely competitive fees ranging from 0-5 bps for maker fees and 5-20 bps for taker fees, with added discounts for DYDX token holders.

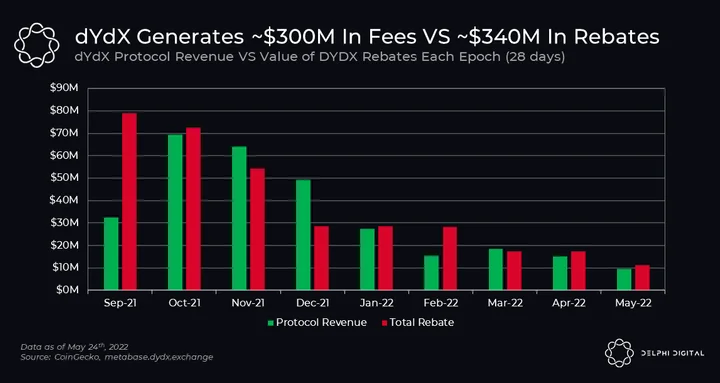

While this does sound quite commendable, lets talk a little bit about the DYDX token. So far the DYDX token has been used to bootstrap activity and liquidity on the exchange. This comes down to their trading rewards where every epoch (28 days) 3,835,616 DYDX tokens are distributed to traders on the platform. The criteria for distribution is primarily based on the fees they generate, but also the open interest they account for.

As you can see in the above chart, in most epochs, total rebates in the form of DYDX tokens are greater than the total fees the platform generates. If we sum these numbers up across all epochs so far, traders have paid ~$300M in fees for ~$340M worth of DYDX tokens.

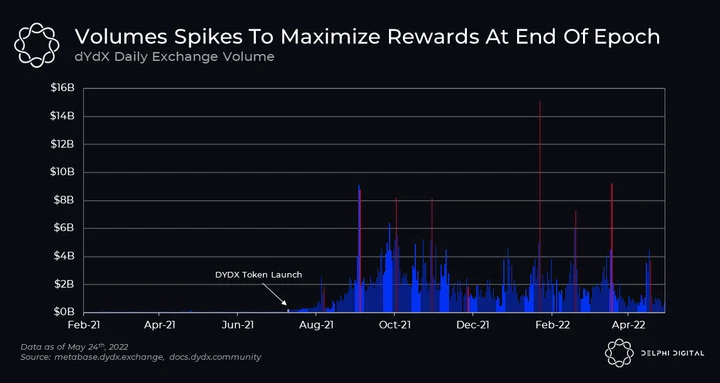

The red lines on the above chart mark the end of each epoch. As you can see, trading typically skyrockets on the last day of each epoch. Unfortunately, this is likely wash trading from larger players looking to take advantage of DYDX token rewards and has led to a severe under-performance of the DYDX token since launch. Market makers essentially trade an abnormal amount of size on the last day of each epoch to maximize their DYDX rewards with the least amount of uncertainty.

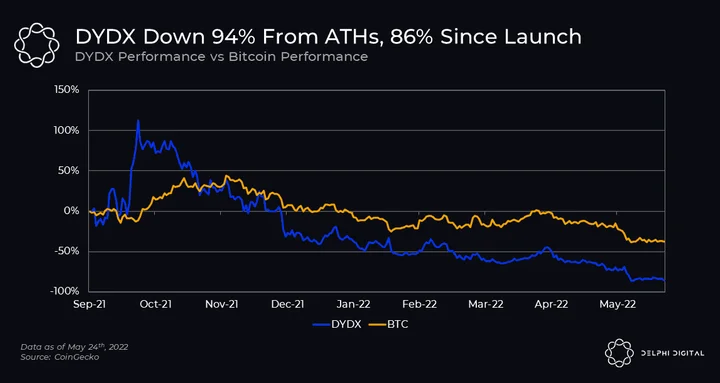

DYDX is down 86% since its launch, while BTC is only down 38% over the same period. This significant under-performance can be attributed to the massive farming game that has gone on with the token alongside DYDX’s current lack of value accrual and utility.

But it’s far from pure doom and gloom for the project. With the release of dYdX v4 slated for the end of 2022, we could see things shake up radically with a fully decentralized trading engine and potential value accrual back to the token. We are excited for the launch of v4, as it could potentially be a shift in token economics that provides value accrual back to DYDX.

With a value accruing token, dYdX would be the most obvious front-runner in the race for decentralized derivatives. v4 is a pretty radical change to the project’s architecture, removing reliance from AWS and attempting to re-create that same process on-chain. The scope for things to be buggy and less-than-ideal is non-trivial, and will take an strong effort from the team to pull off.

Rage Trade

Rage Trade is a perpetual swap protocol looking to launch one of the most liquid ETH perpetual swaps based on its newly developed concept of “recycled liquidity”. Rage Trade is not live yet, but given it’s unique model and goal of catering to passive LPs, we thought it would be worth covering.

Rage Trade adopts a vAMM powered by Uniswap v3 – much like Perpetual Protocol v2. But, its secret to liquidity provision lies in their “80-20 vaults.” As we discussed in the Perp v2 section, the biggest issue for LPs was how difficult it can be to make money, especially for the average user.

Rage Trade looks to create a more passive LP experience, but with juiced returns. The platform’s 80-20 vaults work as follows:

- Users deposit their existing LP positions into Rage. For example, Curve’s Tri-Crypto LP token, GMX’s GLP, or DPX-ETH LP tokens from SushiSwap.

- From here, Rage Trade keeps a minimum of 80% of the underlying LP position in the original protocol while drawing upon a maximum of 20% of it to provide concentrated liquidity on Uniswap v3.

- These vaults are designed to give users a very similar payoff to Uniswap v2, but with extra yields from the fees that their concentrated liquidity positions generate.

Lets break down how these vaults function. There are four main operations we must get acquainted with:

#1 Initial State

Initially, 100% of TVL lives in yield generating LP positions outside of Rage Trade (Curve’s Tri-Crypto, GMX’s GLP, DPX-ETH, etc). Meanwhile, the vault provides a concentrated liquidity position around the current price with equal parts virtual USDC and virtual ETH.

#2 Rebalance PnL (Daily)

As the price of ETH moves, the LP vault accumulates directional perp positions. For example, as the price of ETH increases, the vault becomes short ETH perps (there is more vUSDC and less vETH in the vault, the vault has been selling it’s vETH to traders/arbitrageurs). The Rebalance PnL operation realizes the PnL from these perp positions and transfers the assets to/from the yield generating service into the 20% portion of the vault. This way Rage will have funds to pay out if users close their positions.

#3 Update Range (Daily)

As the ETH price moves, the concentrated liquidity position will hold an imbalance of vUSDC and vETH. If the price of ETH has risen, then the vault will hold more vUSDC and less vETH (vice versa if the price has gone down). Once a day, using the “Update Range” operation, the vault withdraws the current range order and deploys a new range order with equal parts vUSDC and vETH around the new price.

#4 Reset Liquidity (Infrequent)

After a large price move (estimated at ~100% increase or ~50% decrease), the vault will have accumulated a large directional perp position. Once the size of this position exceeds 20% of the vault’s value, the “Reset Liquidity” operation will begin closing it to manage risk.

As an example, let us say the vault has accumulated a 10 ETH short position, to manage risk the vault will start selling off this position in clips of 2 ETH i.e. it will start submitting 2 ETH buy orders. These clips are determined by maximum slippage parameters to not incur unneeded losses. As they begin to submit these buy orders, it’s expected that arbitrageurs will come in, taking the other side and hedging on another exchange. For example, if the 2 ETH buy order slips the price 2%, ETH will trade higher on Rage versus another exchange. Arbitrageurs will come in and sell short on Rage Trade while hedging their position on a CEX. This offloads the potential “unlimited” risk to arbitrageurs in exchange for a smaller immediate loss.

Rage Trade is not yet live, so it is difficult to say exactly how it will perform in practice. However, there is potential for tapping into existing capital and boosting yields. Rage is partnering with Layer Zero and Stargate, allowing users to provide collateral from any compatible chain, opening the door to massive amounts in prospective liquidity.

For traders, Rage Trade will offer 10x leverage on Arbitrum and initially start only with an ETH perp. Fees will be 15 bps to open and close positions. Funding can be kept in line with centralized exchanges using three different methods. Firstly, an on-chain calculation that takes the difference between the perp and index price. Secondly, using a Chainlink oracle that gets rates from Binance. And finally, if needed, it can be manually updated through a governance vote.

Historically funding across various decentralized derivative exchanges has been very different from their centralized counterparts. This is a key detail to consider when traders look to make a platform their go-to exchange.

Details surrounding the Rage token are still scarce, but we do know the protocol will take a 5 bps out of the 15 bps open and closing fee alongside 10% of the yield generated by the “80%” portion of the vault. These fees could be quite significant if they attract a large amount of capital.

If Rage Trade can execute on their promise of mimicking a Uniswap v2 style payoff while enhancing yields, they could capture a massive amount of TVL. There is already so much capital sitting in these various LP positions across crypto that is severely underutilized. Rage Trade looks to improve capital efficiency without introducing too many new risks and layers. As long as crypto spot DEXs stay AMM based, there is room for Rage Trade to find traction, effectively enhancing returns for LPs across EVM chains.

Keep in mind, while the Rage Trade model seems effective on paper, it’s still unproven in the wild – which is all that matters. We expect to revise our opinions on the model as data becomes available once Rage Trade launches on mainnet.

Vega

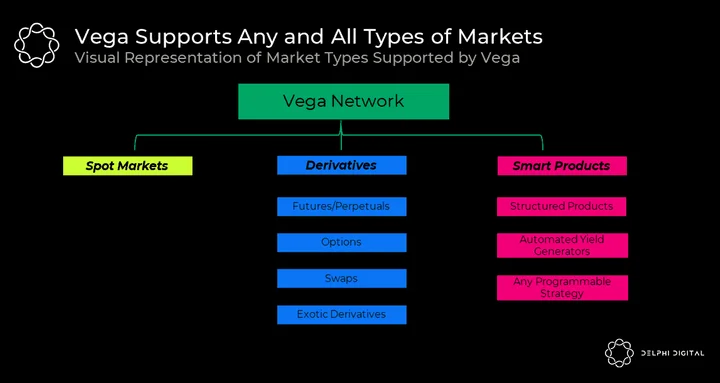

Another decentralized exchange we’re excited about is Vega Protocol — a full-stack exchange built on a sovereign Tendermint chain. Explaining Vega in detail would probably turn this from a long report into a book, so instead, we’ll just ask you to refer to our Vega deep dive if you want to learn about how it works and what it enables.

At its core, Vega will support multiple types of trading modes: orderbooks, custom AMM curves, auctions, and other less popular price discovery mechanisms. For the purpose of succinctness, we’ll focus on the orderbooks. And yes, it makes sense to do so as the Vega MVP will only support orderbooks.

Liquidity providers on Vega, as you can guess, will be professional market makers. As discussed in the dYdX portion, orderbooks aren’t ideal for passive liquidity provision; they require experienced liquidity providers to create a robust market.

From a user perspective, interacting with Vega requires the utilization of Vega’s native wallet. Not being able to use popular wallets like Metamask, Phantom, etc., is an obvious UX barrier for traders. Getting people to download and move money into their Vega wallet will, in our opinion, prove to be the most difficult part in Vega’s initial adoption. However, if there’s relatively deep liquidity, it should entice traders to move some money over to Vega. And as more trading activity comes through, this would put the onus on market makers to start providing deeper liquidity. Vega would do well to take a page from the dYdX playbook and deploy incentives to onboard a strong cohort of market makers.

Vega has a live token. It’s meant to be a governance token, and is fairly easy to stake passively (i.e. delegate to a validator), like any other Tendermint chain. A portion of trading fees collected on Vega will be routed to stakers, making it a value accruing token — eventually. However, as we note in a follow up to our Vega deep dive (that focuses on the VEGA token and how it stacks up against competitors), a slew of token unlocks for the team and investors have begun recently. Keeping an eye on token flows and whether entities are de-risking their VEGA or holding tight will be vital in figuring out the sentiment for the token.

We recommend you read our Vega deep dive. The scope of the project is massive and it is the closest thing to a “decentralized Binance” given the various types of markets and price discovery mechanisms the exchange can support.

Vega’s success now entirely boils down to three things: execution (shipping a functional exchange), improving UX/strong adoption drives, and incentivizing market makers to move chunks of capital to Vega. Each of these is a significant challenge in itself.

Conclusion

With Perp v1 and Drift being sunset, we feel confident in saying that vAMMs in their original form with no liquidity are not feasible. This model exposes the protocol and its users to many risks given the terminal price reversion issues, and they can not sustainably keep their prices in line with the broader market. Furthermore, the lack of balance in funding payments puts stress on the insurance fund. Insurance funds are meant to backstop black swan events, not get protocols through their day-to-day. Once the insurance fund is depleted, this puts the onus of backstopping on token holders.

This leads us to the next iteration: vAMMs with real liquidity. While this model is quite interesting and solves some of the more glaring issues found in original vAMMs, we are not convinced they are the end game for on-chain perps.

Perp v2 falls into a strange category where it still requires professional market makers yet its performance is not comparable to that of an orderbook exchange like dYdX. We believe as blockchain scalability improves, decentralized perp projects will opt for the orderbook model over vAMMs with real liquidity. In the meantime, Rage Trade finds an interesting niche here since they cater to passive LPs and their concept of recycled liquidity could tap into a sizeable amount of liquidity tokens in DeFi. If Rage Trade can successfully replicate a Uni v2 style payoff with enhanced returns, it could fill a gap in the current market as we wait for the technology to catch up and support these faster, more scalable blockchains.

The oracle model is quite fascinating as it gives users excellent execution while also capturing significant returns for liquidity providers. Of course, the secret sauce to this model is the little cheat code of borrowing the price from centralized exchanges and letting the market makers over there do all the work. This means while projects like GMX are doing well in this niche right now, it’s impossible for them to become market leaders. GMX cannot be the most liquid place to trade any asset. GMX has, however, nailed its token economics – a task that has so far eluded many other projects in this category.

Lastly, we are back to orderbooks. Orderbooks feel like the endgame for DeFi perps, but we are still a way off from seeing an “orderbook takeover.” dYdX has crushed competition in terms of volume and user experience so far. But it did so by relying on pieces of centralized infrastructure and creating a value-depleting farming loop on the DYDX token.

Again, we want to reiterate our excitement for v4 and the potential for dYdX to possibly return value back to holders; this could really change everything for the protocol and decentralized exchanges at large. We are also (cautiously) optimistic about Vega. While it has spent a long time in the research and development stage, Vega is getting close to launching its first MVP. We think this will be a landmark moment for them — seeing how their Tendermint chain operates in the wild and if it provides a comparable experience to centralized exchanges.

There are so many projects digging their feet into this space, but unfortunately, we can’t talk about all of them. Synthetix and MCDEX stand out amongst these, and perhaps as more data becomes available, we’ll publish an update to this post to unravel other mechanisms for on-chain perps.

All in all, the potential for decentralized derivatives is shaping up as market players start to understand the true size of the opportunity here. Only time will tell which projects will be successful in creating the most scalable, usable on-chain derivatives platforms. But, we have conviction that DeFi derivatives volume will follow a similar trajectory to DeFi spot volumes, in that they will continue to increase their market share relative to centralized exchanges.

0 Comments