The Aftermath of FTX's Downfall

NOV 11, 2022 • 32 Min Read

This week has been one of the worst we’ve seen in crypto. So much has happened in such a short period of time, it’s difficult to know where to start. Plenty has been written (and speculated) about what led to the events that transpired, so we wanted to come together and share our view on where we are and, more importantly, what this means going forward. We’ve linked to several threads and posts at the end of the report that give more context around this week’s events for those interested.

It’s important to note there’s a lot we still don’t know. We don’t know the exact details or timeline for when (or if) depositors will regain access to funds trapped on FTX. We don’t know how they’ll be treated now that the company (and its affiliates) have filed for bankruptcy. We also don’t know the full extent of potential contagion risk in the aftermath of its collapse. What we do know is that FTX entered this week as the third-largest crypto exchange by volume, and it’ll end the week as one of the largest disasters we’ve ever seen unfold in the space. Regardless of what happens from here, plenty of damage has already been done – both financial and psychological – which will linger for weeks and months to come.

Deciphering On-Chain Flows

Looking at capital flows is the easiest way to figure out the on-chain part of the equation. For obvious reasons, coins held in large quantities by FTX and Alameda have been hit hardest. FTT, SOL, and SRM are a few noteworthy examples.

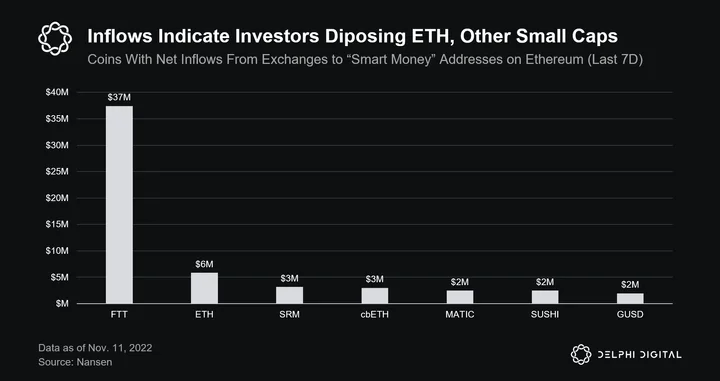

According to Nansen’s Ethereum exchange flows dashboard, the top coins moving into exchanges from wallets labeled as “smart money” over the last week have been FTT, SRM, cbETH, MATIC, SUSHI, and GUSD. In FTT’s case, just 12 addresses contributed to $37M FTT moving into exchanges. Note that this analysis is focused on Ethereum, and does not account for chains like Solana and Avalanche.

According to Nansen’s Ethereum exchange flows dashboard, the top coins moving into exchanges from wallets labeled as “smart money” over the last week have been FTT, SRM, cbETH, MATIC, SUSHI, and GUSD. In FTT’s case, just 12 addresses contributed to $37M FTT moving into exchanges. Note that this analysis is focused on Ethereum, and does not account for chains like Solana and Avalanche.

ETH previously had net outflows from exchanges, but this has flipped in the last 24 hours, with $288M of deposits and $283M of withdrawals.

ETH previously had net outflows from exchanges, but this has flipped in the last 24 hours, with $288M of deposits and $283M of withdrawals.

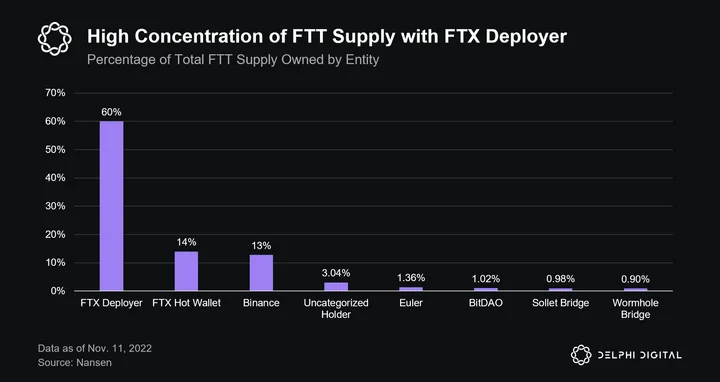

The vast majority of FTT flows into exchanges came from addresses labeled as “market makers” on Nansen. Given FTX/Alameda’s alleged use of FTT as collateral, this is not entirely unexpected. Lenders trying to offload the FTT collateral may have engaged one of these market makers to dispose of these assets. However, FTX’s deployer address owns 60% of FTT’s total supply.

The market cap of FTT currently stands at $363M while this address owns $536M worth of FTT, implying some or all is locked FTT – though Etherscan shows the token to be the same liquid FTT token trading in the market today. With so much FTT sitting idly in the deployer account, it lends credence to the theory that Alameda posted FTT obtained from the ICO as collateral against the loans given to them by FTX.

The market cap of FTT currently stands at $363M while this address owns $536M worth of FTT, implying some or all is locked FTT – though Etherscan shows the token to be the same liquid FTT token trading in the market today. With so much FTT sitting idly in the deployer account, it lends credence to the theory that Alameda posted FTT obtained from the ICO as collateral against the loans given to them by FTX.

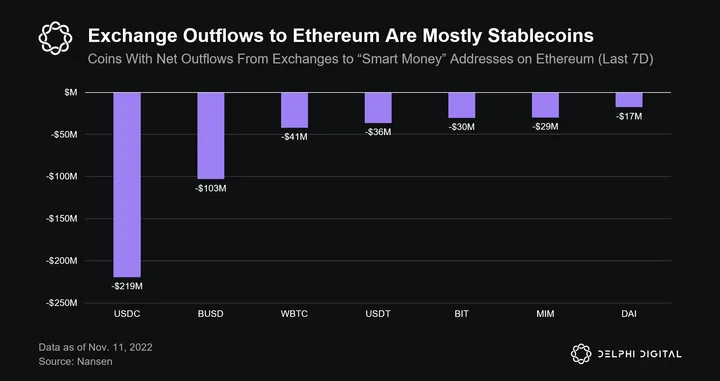

The data largely indicates the flight of quality assets from exchanges, presumably into cold storage or self-custody wallets. Over the last seven days, the assets with the largest net outflows from exchanges from “smart money” wallets were USDC (-$218M), BUSD (-$102M), WBTC (-$41M), USDT (-$36M), BIT (-$30M), MIM (-$29M), and DAI (-$17M).

The data largely indicates the flight of quality assets from exchanges, presumably into cold storage or self-custody wallets. Over the last seven days, the assets with the largest net outflows from exchanges from “smart money” wallets were USDC (-$218M), BUSD (-$102M), WBTC (-$41M), USDT (-$36M), BIT (-$30M), MIM (-$29M), and DAI (-$17M).

The inclusion of BIT and MIM is surprising. But for context, FTX owned a large amount of BIT, and it seems reasonable to suspect the exchange outflows are linked to this. BitDAO has one of the largest on-chain treasuries, but roughly 60% of it is held in their own token (BIT). Further, Alameda owned a fair share of MIM via debt, so perhaps they are moving it off exchanges to close out their loans.

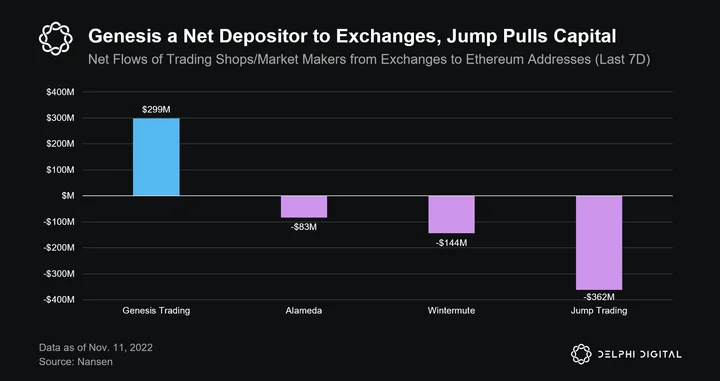

A week charged with volatility and steep drawdowns is bound to catch the attention of market makers and trading shops. As of Nov. 9, Jump Capital and Wintermute – two of the largest market makers in crypto – had net withdrawals of ~(-$362M) and ~(-$144M) from exchanges and brokerages.

A week charged with volatility and steep drawdowns is bound to catch the attention of market makers and trading shops. As of Nov. 9, Jump Capital and Wintermute – two of the largest market makers in crypto – had net withdrawals of ~(-$362M) and ~(-$144M) from exchanges and brokerages.

Genesis Trading, a large centralized crypto firm offering several financial services, was actually a net depositor to exchanges over the last week, to the tune of $299M. Note that these figures are all net; most of these entities had substantial withdrawals and deposits to exchanges.

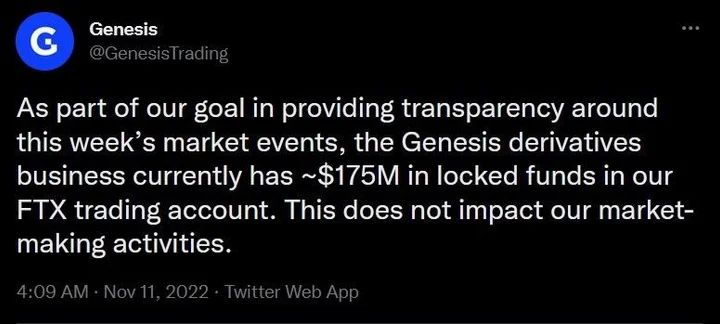

Genesis’ deposits mostly stem from lower-cap assets they were probably moving into exchanges to liquidate. The firm may be trying to re-capitalize with higher-quality assets given the recent announcement that they have $175M locked in FTX. However, it’s worth noting that Genesis Trading is still a net depositor to exchanges even if you just look at stablecoin movements. So these flows may just be them continuing to service their clients. Genesis also landed a $140M equity infusion from its parent company DCG this morning.

However, two of the largest market makers (Jump and Wintermute) pulling liquidity from exchanges is notable, but not too surprising given this week’s events. Note that this only tracks exchange flows into Ethereum, so those numbers are likely higher, especially for Jump, after taking chains like Solana into account.

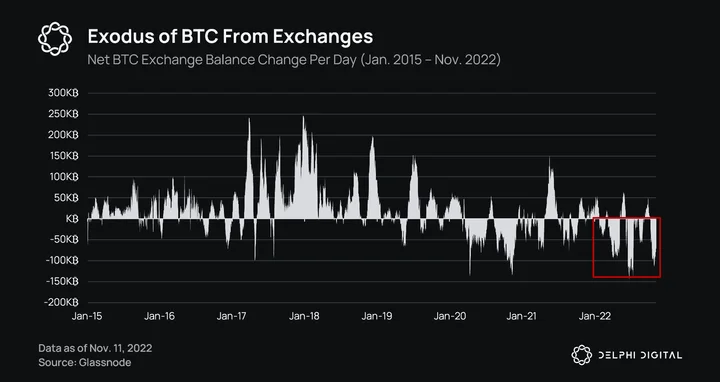

It also isn’t just institutions pulling capital from centralized exchanges. CEXs are losing capital across the spectrum. Observable in the BTC net-exchange flows data, 2022 has already seen two of the largest exoduses of BTC out of exchanges ever. The metric peaked at 135k BTC per day in July 2022 and 115k BTC in late October 2022.

It also isn’t just institutions pulling capital from centralized exchanges. CEXs are losing capital across the spectrum. Observable in the BTC net-exchange flows data, 2022 has already seen two of the largest exoduses of BTC out of exchanges ever. The metric peaked at 135k BTC per day in July 2022 and 115k BTC in late October 2022.

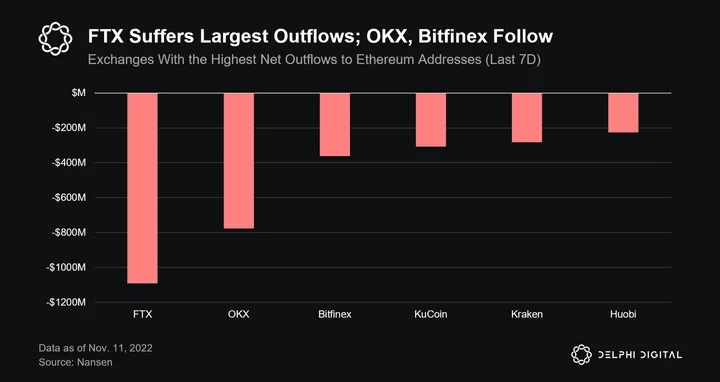

Broader exchange flows into Ethereum don’t paint the picture one would expect. According to Nansen, FTX unsurprisingly leads the pack in net outflows to the Ethereum network, with close to $1.1B of excess withdrawals over deposits in the last week. OKX comes in second with -$776M of net outflows from the exchange, with Bitfinex in third at -$360M.

Broader exchange flows into Ethereum don’t paint the picture one would expect. According to Nansen, FTX unsurprisingly leads the pack in net outflows to the Ethereum network, with close to $1.1B of excess withdrawals over deposits in the last week. OKX comes in second with -$776M of net outflows from the exchange, with Bitfinex in third at -$360M.

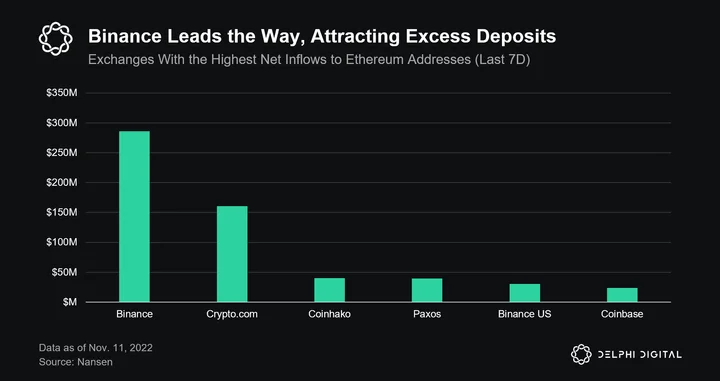

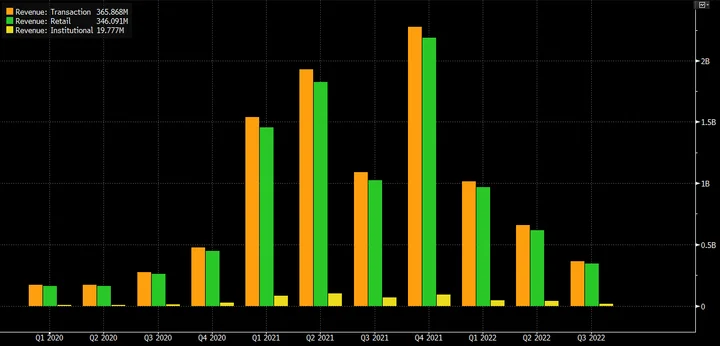

As expected, Binance has been the biggest beneficiary of the past week, attracting $285M in excess deposits. It’s not surprising that Binance has been the biggest beneficiary and FTX the worst hit, as many speculated would be the case. But make no mistake – centralized exchanges as a whole are still under pressure with some seeing large exoduses of capital from their businesses. This comes at a time when trading volumes have suffered significant declines from their peaks last year. Total spot volumes for exchanges peaked back in Q2 2021, according to data tracked by The Block.

As expected, Binance has been the biggest beneficiary of the past week, attracting $285M in excess deposits. It’s not surprising that Binance has been the biggest beneficiary and FTX the worst hit, as many speculated would be the case. But make no mistake – centralized exchanges as a whole are still under pressure with some seeing large exoduses of capital from their businesses. This comes at a time when trading volumes have suffered significant declines from their peaks last year. Total spot volumes for exchanges peaked back in Q2 2021, according to data tracked by The Block.

For example, Coinbase’s transaction revenue, which historically has made up >85% of the company’s sales, has taken a substantial hit this year. Coinbase saw a 66% decline in transaction revenue year-over-year in Q3, in part driven by a 72% decline in retail trading volume, which is a big driver of the company’s top line.

This isn’t just unique to Coinbase though. If anything, this week gave the incumbent an opportunity to showcase why it’s regarded as one of the most trusted exchanges, an attribute that’s only going to become increasingly important in the aftermath of FTX’s downfall.

Collateral Damage – Who’s Left Holding the Bag?

As alluded to previously, the potential for contagion across the entire crypto industry is massive because of how big and integrated both FTX and Alameda Research became. FTX grew to become the third-largest exchange by volume and FTX Ventures began investing in a broad swath of projects and companies in the crypto industry. Alameda Research, a quantitative trading firm and once industry-leading market maker, had ties to many counterparties as well as its own investments in crypto protocols and companies. The blast radius of this is likely to be massive, and these contagion risks will likely weigh on markets until we get more clarity on the extent of the damage.

Alameda and FTX broke headlines this morning when they officially filed for Chapter 11 bankruptcy. The biggest question now is how big is the actual hole? Several sources are now estimating it’s in the range of $8-10B. Speculation is already swirling as to the net asset gap at Alameda, but it’s difficult to pinpoint given the ranges for both their assets and liabilities are so wide (filings indicate between $10-$50B). The filing does, however, indicate that Alameda will have funds left over to distribute to unsecured creditors (but take this with a grain of salt because if we’ve learned one thing this week it’s not to put too much stock into any disclosures until the truth comes out).

Quantifying the total collateral damage from this will be difficult, and we’re unlikely to know how far the contagion spreads for some time – it’s going to be a while before we uncover the full gravity of the situation. But thinking through which parties could be most affected helps paint a picture of how bad this could get. Some of the main players in question are:

-

Companies and projects that had a portion of their treasuries in FTX

-

Hedge funds and venture funds that had a portion of their AUM in FTX

-

Market makers with liquidity trapped in FTX

-

Funds that were backed by FTX

-

Projects that received funding from FTX/Alameda Research (no existential risk, but tokens/SAFTs likely to be sold off in the event of liquidation)

-

Projects Alameda Research was a market maker for

-

Centralized lenders that extended Alameda Research credit lines

-

Entities that FTX/Alameda Research extended credit lines to

-

Exchanges where Alameda Research possibly had privileged accounts to market make on (mainly capital efficiency, margin benefits)

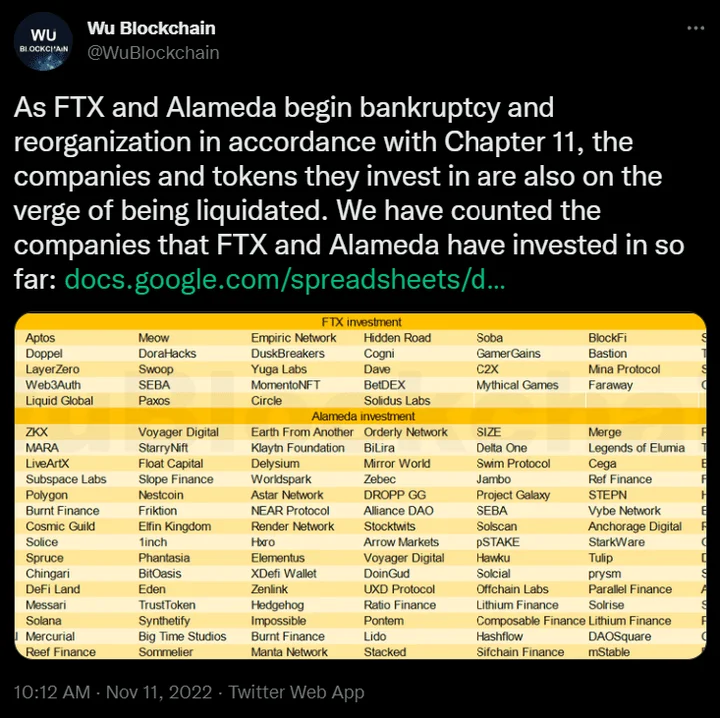

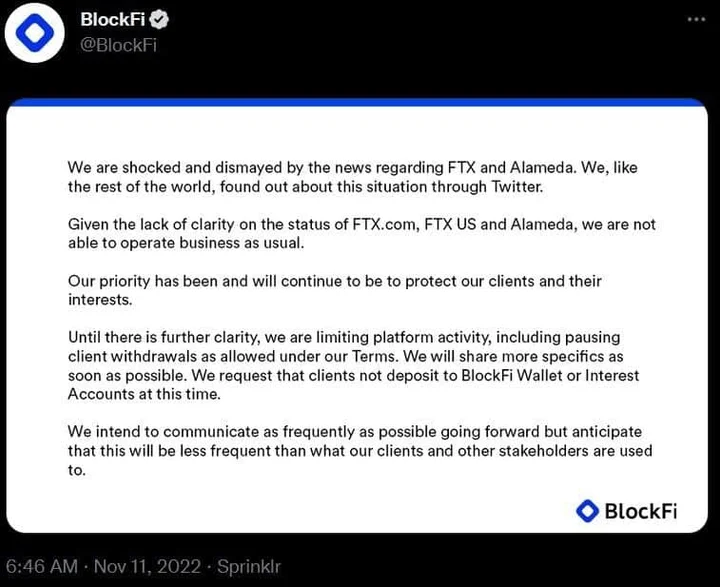

Here’s one running list of well known companies with varying degrees of exposure to FTX. Let’s also look through some isolated examples related to the players above. BlockFi seemed to be on the brink of insolvency back in July when FTX stepped in to offer a $400M credit line, seemingly saving the day. We can’t be sure how much of this promised credit line was given to BlockFi thus far, but either way it doesn’t seem to have been enough. BlockFi confirmed last night that it was unable to operate business as usual given the FTX news.

Core Scientific was recently revealed to have taken an $80M loan from BlockFi. But a few weeks ago, Core Scientific announced the suspension of debt repayments due to a dire situation with Bitcoin mining profitability. Assuming the FTX credit hasn’t fully come through, the news this week will likely have a detrimental impact on BlockFi’s ability to continue operating. The company’s announcement acknowledged the precarious position they’re in, including the decision to halt withdrawals/deposits on the platform.

Unfortunately, one of the most tragic downstream impacts is for projects/protocols that held a significant portion of their treasury reserves on FTX, as they may be forced to engage in a down round or shut down altogether. Projects that received funding from FTX Ventures and Alameda Research could see their token prices further plummet if the situation escalates to a formal liquidation of assets. Companies directly owned by FTX, like LedgerX (FTX’s CFTC-registered derivatives exchange) are likely to be caught in the crossfire too.

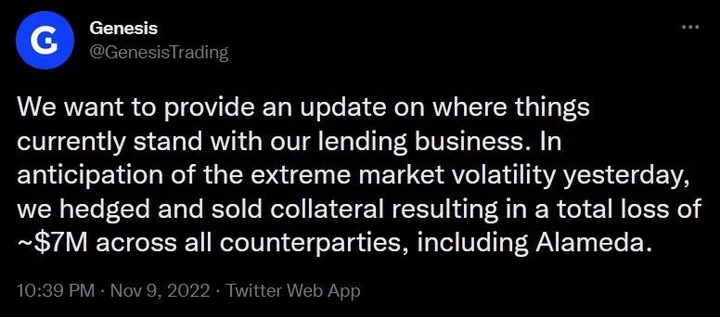

We’ve already seen round one of a similar situation play out with creditors due to Three Arrows Capital and the Terra contagion. If Alameda Research is in trouble, we could see a second round of hits to centralized crypto lenders. Genesis Trading indicated about -$7M of losses on account of Alameda a couple days ago, which is a pretty healthy figure given the size of Alameda and Genesis’ lending book.

Many of the industry’s largest investors and traders have funds that are still trapped on FTX. That represents a lot of would-be volume for other exchanges, especially DEXs and derivatives protocols that likely stand to benefit from the distrust FTX has sowed.

Trapped funds also mean less liquidity for the broader crypto market. Smaller tokens are particularly at risk, as we’ve seen market markers pull liquidity and reduce risk exposure amid heightened uncertainty.

If those market participants do wind up getting access to those funds sooner than later, we may see a sizable inflow back into alternative trading venues. The more time this takes though, the more likely we’ll see a dampening effect on risk appetite. Events as traumatic as this one tend to leave a lot of scars in their wake.

Another concern is the potential impact FTX’s collapse may have on some of the industry’s largest and most active VCs. Many have already marked their investment in FTX to zero, which may accelerate the downtrend in new funding and accessibility to much-needed capital. This only adds insult to injury for many crypto startups and companies that are already being squeezed to cut costs anyway they can in order to survive.

Limited access to affordable funding is one of the biggest risks facing the crypto market heading into next year, especially given this week’s likely impact on liquidity and risk appetite. This year’s brutal bear market has taken a toll on many in the industry, and the certainty surrounding its end will continue to weigh on investor allocations.

Solana Caught in the Crossfire

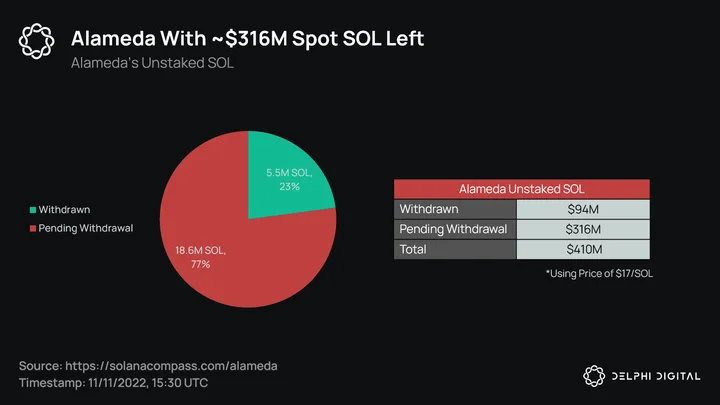

From an ecosystem perspective, Solana will take the largest hit out of all of them. It’s no secret that FTX and Alameda were huge investors in Solana and thus have large spot SOL positions to liquidate, along with numerous other ecosystem tokens. As of the timestamp in the chart below, Alameda still has ~18.6M SOL ($316M) remaining, which was un-staked in epoch 370 (the “pending withdrawal” tokens are free to move now). Of course, it is unclear how much of this has already been effectively sold using perps, as at one point they were trading at a ~50% discount to spot ($7 perp vs. $13 spot) on some exchanges. SOL/USD has recovered to ~$17 from a $12 spot low on Binance.

*Note: Now that Alameda has filed for bankruptcy, these funds “pending withdrawal” should not be touched and are effectively frozen.

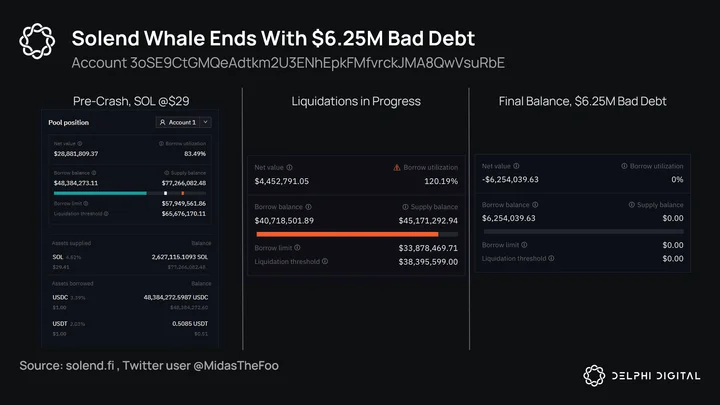

The next direct fallout was with the “Solend Whale.” This was an infamous position in Solana DeFi, the largest single borrow of ~$50M USDC against SOL collateral, with a liquidation price of $21. With Alameda being one of the largest on-chain liquidity providers on Solana and the extreme price fluctuations in SOL from them needing to sell and accompanying panic, there was risk of a substantial amount of bad debt here.

The next direct fallout was with the “Solend Whale.” This was an infamous position in Solana DeFi, the largest single borrow of ~$50M USDC against SOL collateral, with a liquidation price of $21. With Alameda being one of the largest on-chain liquidity providers on Solana and the extreme price fluctuations in SOL from them needing to sell and accompanying panic, there was risk of a substantial amount of bad debt here.

The liquidation process happens in chunks of 20%, and while it started off okay, it eventually became significantly undercollateralized as the price of SOL dropped to $12. To illustrate the challenge here, selling 500k SOL (~$9M) on-chain currently incurs 62% slippage.

Somewhat miraculously, this position ended up being liquidated with only $6.25M of bad debt. And with a treasury of $17M USDC, there is a path for users to be covered (pending DAO vote + other potential bad debt arising).

Somewhat miraculously, this position ended up being liquidated with only $6.25M of bad debt. And with a treasury of $17M USDC, there is a path for users to be covered (pending DAO vote + other potential bad debt arising).

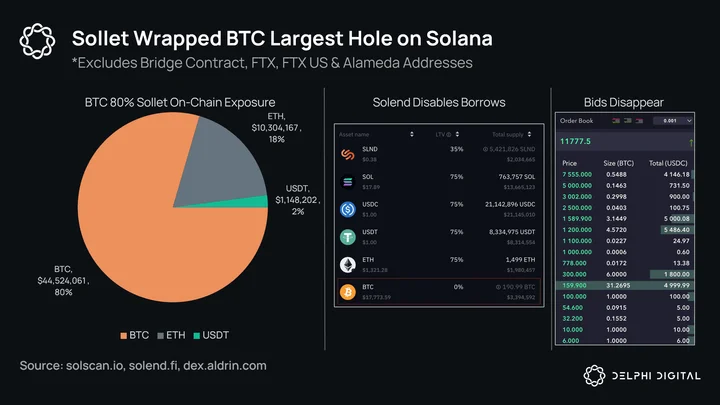

The next major implication for Solana DeFi is around Sollet-wrapped tokens. These are tokens for non-Solana assets like BTC, ETH, & USDT that are affiliated with FTX. There are not a lot of details around these tokens, and the solvency of them is unclear. Fortunately, most of the ERC-20 assets (ETH and USDT) went through a migration process a few months ago as Solana DeFi transitioned to the Wormhole-based versions of these assets instead. Unfortunately, this did not apply to BTC, and thus the BTC outstanding on Solana has unclear backing (potentially $0, though this is not confirmed).

Protocols like Solend took proactive measures here – with others following after – and reduced LTV to 0%, liquidating any users who had outstanding loans against soBTC. While frustration from users due to this split-second decision is understandable, there was still some on-chain liquidity for soBTC and, according to their team members, they were left with $0 bad debt on soBTC as a result of liquidating when they did. With the recent FTX bankruptcy announcement (which includes FTX US), liquidity on-chain has essentially evaporated.

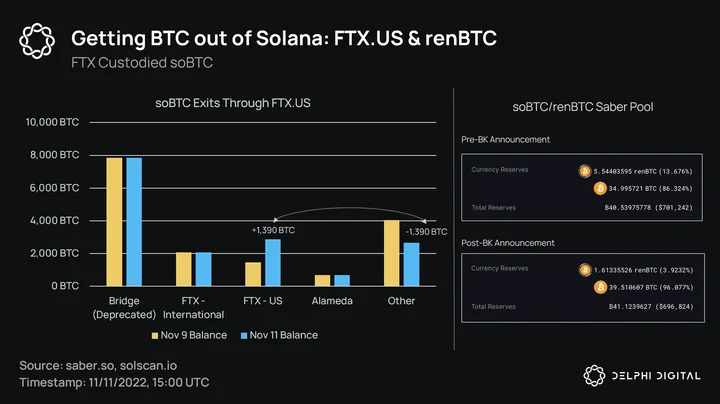

For the few hours before FTX’s bankruptcy, there were anecdotal reports of people being able to deposit soBTC to FTX US and get funds out. We can see this movement on-chain, as all of the soBTC flows over the past two days were from un-tagged/other addresses to FTX US.

For the few hours before FTX’s bankruptcy, there were anecdotal reports of people being able to deposit soBTC to FTX US and get funds out. We can see this movement on-chain, as all of the soBTC flows over the past two days were from un-tagged/other addresses to FTX US.

It looks like ~1,390 BTC ($24M USD) was deposited to FTX US and (hopefully) able to get out. Now that bankruptcy has been filed, the remaining soBTC on Solana seems to be trapped. After the bankruptcy announcement, the remaining renBTC was emptied from the Saber pool rather quickly. Solana DeFi seems stuck with a >2k BTC (~$44M) hole.

Speaking of renBTC, it’s important for us to highlight here that Alameda is the parent company for them, and while transactions are still going through, DeFi protocols like BadgerDAO (the largest BTC platform on Ethereum) are deprecating and warning all users to redeem. While the bridge is still operational, the Ren team has been receiving funding from Alameda for the past 12 months, and with Alameda now in bankruptcy the future is unclear. There have not been clear answers over the past 24 hours on who actually controls the keys, and if the largest BTC application on Ethereum is warning users, that warning should be taken seriously.

Speaking of renBTC, it’s important for us to highlight here that Alameda is the parent company for them, and while transactions are still going through, DeFi protocols like BadgerDAO (the largest BTC platform on Ethereum) are deprecating and warning all users to redeem. While the bridge is still operational, the Ren team has been receiving funding from Alameda for the past 12 months, and with Alameda now in bankruptcy the future is unclear. There have not been clear answers over the past 24 hours on who actually controls the keys, and if the largest BTC application on Ethereum is warning users, that warning should be taken seriously.

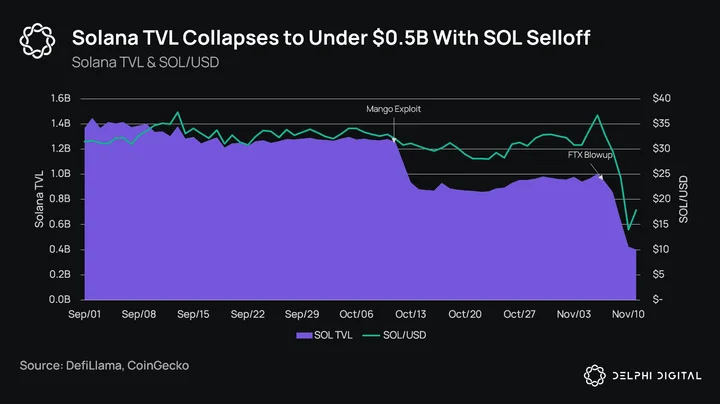

There’s no sugar-coating it, the Solana ecosystem has taken a massive hit here. On-chain DeFi has been nearly wiped out completely: TVL is down from $10B at the peak, to $1B a couple days ago, to less than half that today.

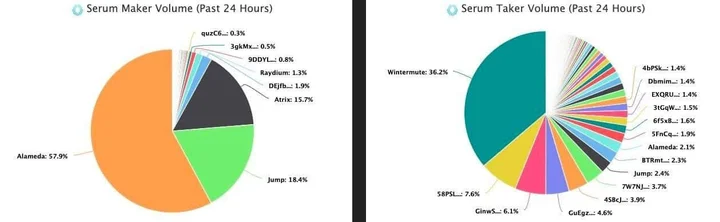

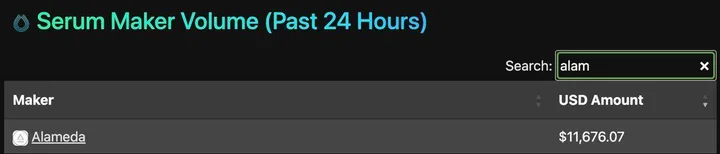

There will be a lot of rubble to sort through with the final tally of bad debt on various borrow/lend protocols and whoever unfortunately still holds Sollet-wrapped assets. In addition, Alameda was the largest on-chain market maker, routinely accounting for >50% of Serum maker volume. That now goes to zero.

There will be a lot of rubble to sort through with the final tally of bad debt on various borrow/lend protocols and whoever unfortunately still holds Sollet-wrapped assets. In addition, Alameda was the largest on-chain market maker, routinely accounting for >50% of Serum maker volume. That now goes to zero.

While it may seem like grasping at straws right now, there can be a bright side to this. The Solana ecosystem was always known as an Alameda/FTX chain, and removing them from the picture allows Solana to rebuild and forge their own image with a clean slate.

There’s short-term (and medium-term) pain to deal with, but if Solana survives this then they will have earned their keep in this industry. I don’t think it’s too bold to say that this will be the toughest test any ecosystem has gone through, even more devastating than what Ethereum went through in 2018 when it traded down to $80. Just a week ago, there was a rejuvenation of excitement around the ecosystem during the Breakpoint conference. There are legitimate builders there, they just need to stick around.

Impact on NFT Markets

There have been strong ripple effects on NFTs from the FTX blowup. Alameda holds an insignificant number of NFTs (81 Sandbox lands & 2 Mutant Apes). No major project team has publicly reported a loss of their treasury funds yet. But it’s likely that there are NFT teams that are affected. We will find out in time.

There are two notable trends we’re monitoring. First, it seems people who lost their money in the FTX blowup are selling their NFTs for liquidity.

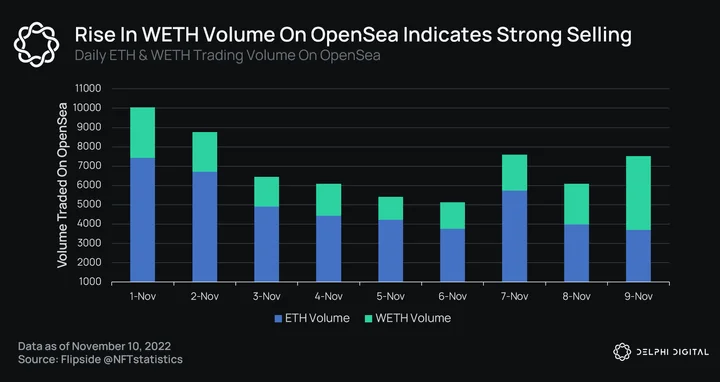

The volume of WETH bids accepted on OpenSea has seen a sharp rise in the past two days. This now accounts for almost half of all trades (by volume) on OpenSea. This indicates that people are more willing to sell their NFTs at below-floor prices in order to obtain instant liquidity. It is a good time to place WETH bids on NFTs you want to collect, as there is a higher chance they will be accepted.

The volume of WETH bids accepted on OpenSea has seen a sharp rise in the past two days. This now accounts for almost half of all trades (by volume) on OpenSea. This indicates that people are more willing to sell their NFTs at below-floor prices in order to obtain instant liquidity. It is a good time to place WETH bids on NFTs you want to collect, as there is a higher chance they will be accepted.

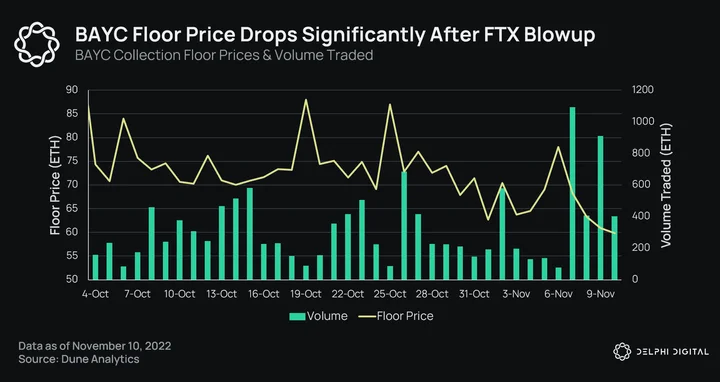

Bored Apes have been one of the largest-volume collections since the FTX blowup, with sellers outnumbering buyers. The floor price fell as low as 55E (-25% from last week), triggering a wave of BAYC liquidations on BendDAO, a peer-to-pool NFT lending protocol.

Bored Apes have been one of the largest-volume collections since the FTX blowup, with sellers outnumbering buyers. The floor price fell as low as 55E (-25% from last week), triggering a wave of BAYC liquidations on BendDAO, a peer-to-pool NFT lending protocol.

Another ~50 BAYCs on BendDAO are at high risk of liquidation and will be put up for auction if the floor price falls another 10-20%. This could lead to continued downward pressure on BAYC prices.

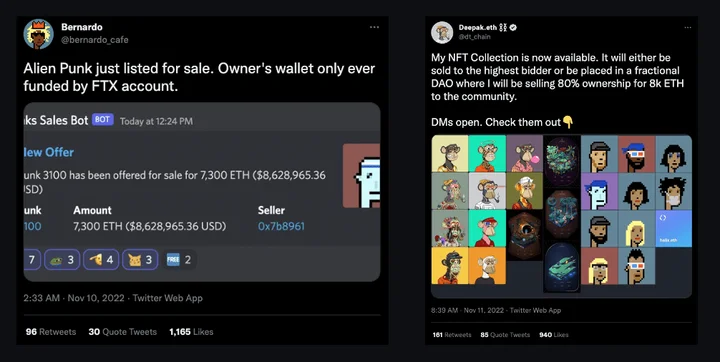

Anecdotally, there are many cases of individual collectors (also likely impacted by FTX) selling their prized NFTs, including two alien CryptoPunks that are now on the market.

The second trend is the significant hit to the Solana NFT ecosystem.

SBF and FTX were the main patrons of Solana, and it gave Solana NFT people comfort that their blockchain was supported by one of the most influential people in crypto. Now, their king has been “beheaded,” and the overhang is quite large.

As mentioned, Alameda owns large amounts of SOL, which will likely be liquidated as FTX attempts to patch up the hole or goes into bankruptcy (spoiler alert: we now know this is the case).

The price of SOL dropped over 60% this week. Solana NFTs are denominated in SOL, so their prices have also fallen significantly in USD terms. This led to:

The price of SOL dropped over 60% this week. Solana NFTs are denominated in SOL, so their prices have also fallen significantly in USD terms. This led to:

-

Collectors panic selling to minimize losses and SOL exposure

-

Builders and creators considering moving out of Solana

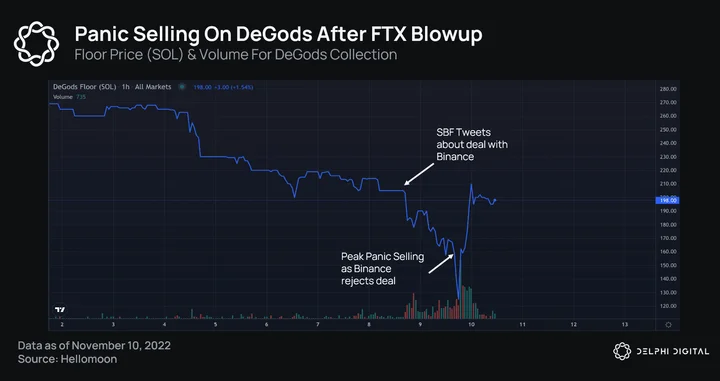

DeGods is a stellar example of this, with floor prices crashing and its founder Frank publicly tweeting asking if they should move to Ethereum. The good news is that after the initial shock, it seems that Solana NFT communities are coming together in strong solidarity and support for the ecosystem.

The events of this week highlight how the choice of blockchain can have major implications for NFT projects which are out of their control. A stain remains on Solana’s branding, as it was closely associated with SBF and FTX. Future founders will likely think twice about building on Solana and may favor other chains such as ImmutableX and Polygon, at least in the short term.

Where Does the Market Stand?

As the full extent of the FTX <> Alameda blow up continues to reveal itself, there are several market-related implications that we think people should be aware of. Firstly, if we can bring ourselves to think back to the traumatic events of June 2022, perhaps we may find some insight as to what we can expect going forward.

During the June market sell off, 3AC blew up, likely suffering from a fatal wound due to their exposure to the LUNA/Terra ecosystem – which had collapsed just a month prior. Due to the massive sell pressure of 3AC’s holdings, and the uncertainty and contagion risk surrounding CeFi lenders and counterparties, prices took a massive hit (BTC dropped nearly 40%). It took many days, if not weeks, for the picture to become clear as to who was affected and the total damage done. Unfortunately, the FTX-Alameda blow up is even worse in many respects, as we’ll discuss in this report. We are likely to see a similar unfolding of events over a potentially much longer period of time.

Fast forward to today. The 5-month consolidation range spawned by the liquidation events of June has broken down on the back of arguably the worst crypto catalyst to date, rivaling even the most infamous scandals of the past. What many had thought was the bottom has been breached. What does this mean for markets? Let’s start with a high-level view of where we find ourselves on the BTC chart.

As mentioned, BTC has finally broken out of the consolidation range (roughly $18.5k-$24k) from the better part of the last six months, with an extremely strong catalyst fueling the move. During this period, we have consistently warned that when this price range is inevitably broken, either to the upside or downside, it is likely not a move to be faded. There are two big reasons for this.

As mentioned, BTC has finally broken out of the consolidation range (roughly $18.5k-$24k) from the better part of the last six months, with an extremely strong catalyst fueling the move. During this period, we have consistently warned that when this price range is inevitably broken, either to the upside or downside, it is likely not a move to be faded. There are two big reasons for this.

Firstly, think of the consolidation range like a spring, coiled up over time and full of potential energy. Each successful bounce off of support and rejection from resistance adds more potential energy. When prices do eventually break from the range, the impulse move can be extremely strong, much like the initial unwind of a coiled spring.

Secondly, this breakdown has been accompanied by one of the worst crypto catalysts to date, weighing on investor sentiment and asset prices. Combine the native crypto catalyst in the FTX-Alameda blowup with a continued bleak macroeconomic backdrop that has not materially changed, and continuation to the downside is the path of least resistance at this point as opposed to a reversal.

We are watching the following key levels for BTC:

-

Support: $14k-$16k

-

Support: $9k-$12k

-

Resistance: $18.5k-$20k

-

Resistance: $21.5k-$22k

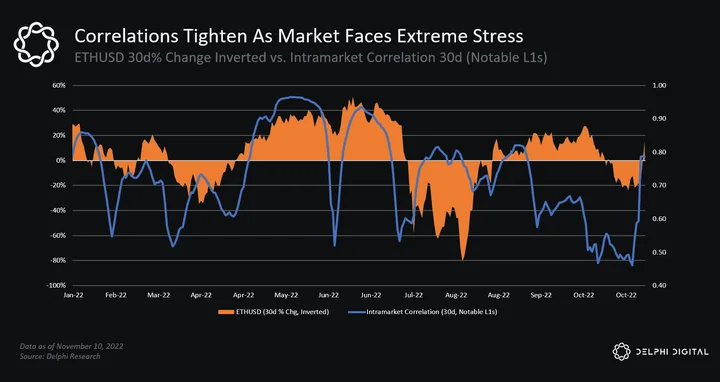

ETH is holding up slightly better than BTC in light of recent events, not yet breaching the lows set back in June. Realistically, it is very likely that no coin is going to be spared while the details of what happened continue to be brought to light and the true ramifications become more clear. A finance cliché seems prudent here; “in times of extreme stress and turmoil, correlations of risk assets trend towards 1.”

The below video is from yesterday’s special edition of Delphi Office Hours. Please give it a watch for more context and live charting around this week’s market moves. For the full recording, click here.

As we noted, Solana took one of the biggest hits this week. SOL was down over 60% at one point, but has since recovered a bit of its losses. This was more of a liquidity-driven selloff, but as we highlighted before, there are some real challenges for the Solana ecosystem to overcome in the aftermath of this.

Solana wasn’t the only one caught in the crossfire though. Many crypto assets saw substantial intraweek drawdowns as the whole market reacted to the once unthinkable.

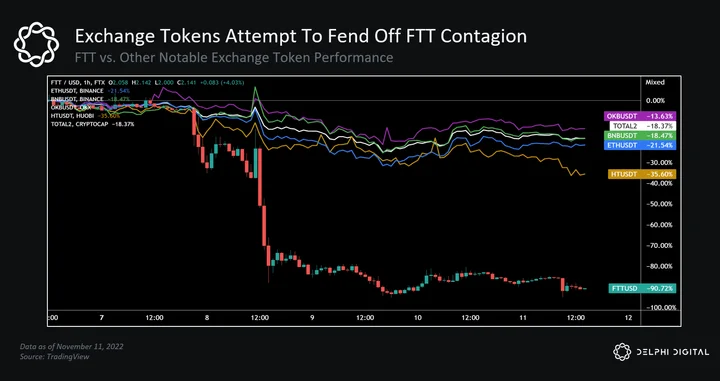

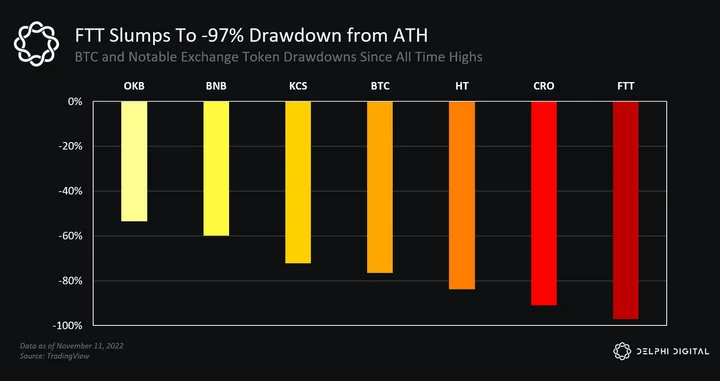

Intramarket correlations tightened between tokens across several major sectors, which isn’t uncommon during periods of market distress. Despite FTT’s >80% drawdown the last few days, rival exchange tokens have held up relatively well, even compared to mega-caps like BTC and ETH. We noted how Binance potentially stands to be one of the biggest beneficiaries over time.

Despite FTT’s >80% drawdown the last few days, rival exchange tokens have held up relatively well, even compared to mega-caps like BTC and ETH. We noted how Binance potentially stands to be one of the biggest beneficiaries over time.

This week’s price action aligns with the ranks of major centralized exchange tokens when comparing their intraweek drawdowns from all-time highs.

This week’s price action aligns with the ranks of major centralized exchange tokens when comparing their intraweek drawdowns from all-time highs.

The collapse of FTX should give Coinbase a welcomed boost once the dust settles. COIN popped off its lows as the scale of FTX’s downfall became more known. We’ve seen a big rally in equities the last two days, though, so it’s too early to read into the market’s reaction quite yet.

The collapse of FTX should give Coinbase a welcomed boost once the dust settles. COIN popped off its lows as the scale of FTX’s downfall became more known. We’ve seen a big rally in equities the last two days, though, so it’s too early to read into the market’s reaction quite yet.

Other exchanges stand to benefit from FTX’s demise, but the amount of trapped funds may hamper trading volumes in the near term. Centralized exchanges were already facing substantial declines in trading revenue, and it’s hard to see how FTX’s collapse will change that.

Other exchanges stand to benefit from FTX’s demise, but the amount of trapped funds may hamper trading volumes in the near term. Centralized exchanges were already facing substantial declines in trading revenue, and it’s hard to see how FTX’s collapse will change that.

Aside from that, if we take a step back, this entire debacle only furthers the case for decentralized platforms.

The Silver Lining for DeFi & Potential Catalysts

All may seem lost at this moment. Negative sentiment is running amok, and understandably so. It’s difficult to see a silver lining in a situation like this. But there is, and it’s a big one.

This week was a public advertisement for the benefits DeFi offers. If you think about it, this is a significant tailwind for the advent of decentralized technology in the long run. The big advantages of public ledger blockchains and applications built on them are radical transparency and real-time monitoring.

Could an FTX-type situation have unfolded with a DEX? Customer funds either sit in the customer’s self-custodied wallet (traders) or in immutable smart contracts (LPs). There’s no scope for such a situation with truly-decentralized exchanges. dYdX is one example, where the matching engine and orderbook are currently centralized infrastructure, but all money flows happen on-chain and can be monitored 24/7 in depth.

Looking forward, this could serve as a long-term tailwind for decentralized exchanges at large. DeFi already has successful spot markets in the form of Uniswap, Curve, 0x, and others. When it comes to derivatives, only dYdX has really shown signs of product-market fit, yet their ability to serve a large number of traders comes from using a centralized matching engine and orderbook.

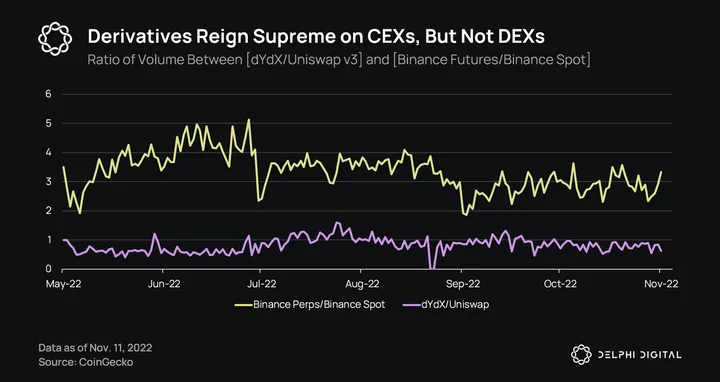

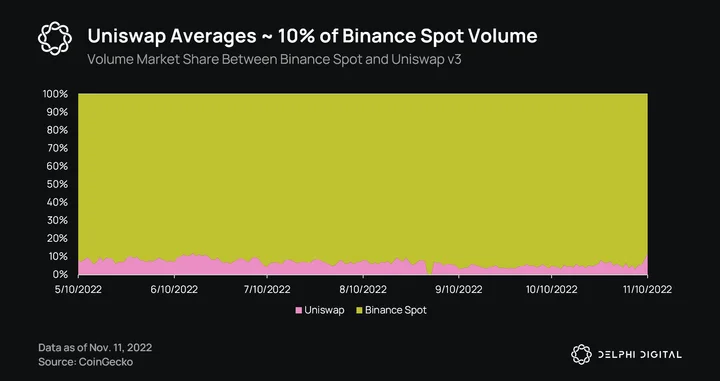

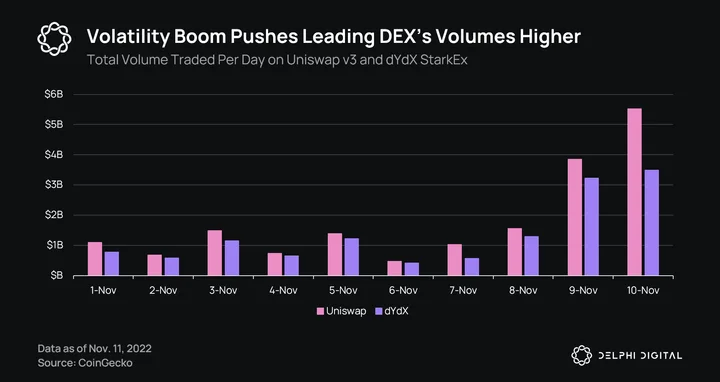

There’s a big dislocation in the ratio of spot:derivatives volume of CEXs to DEXs. While derivatives markets on CEXs do multiples of corresponding spot volume, DeFi protocols are still in a relatively immature phase as the top spot DEX’s volume eclipses the top perpetuals DEX.

There’s a big dislocation in the ratio of spot:derivatives volume of CEXs to DEXs. While derivatives markets on CEXs do multiples of corresponding spot volume, DeFi protocols are still in a relatively immature phase as the top spot DEX’s volume eclipses the top perpetuals DEX.

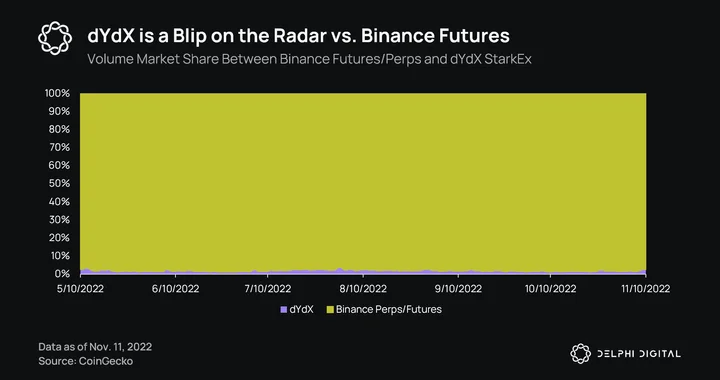

To ascertain the gap for DEX trading volume to CEX trading volume, let’s look at volume market share between the top spot DEX and top spot CEX (Uniswap vs. Binance), and the top DEX derivatives platform vs. the top CEX derivatives platform (dYdX vs. Binance).

dYdX’s market share relative to Binance derivatives is low and pretty insignificant.

dYdX’s market share relative to Binance derivatives is low and pretty insignificant. Uniswap and dYdX, however, have had pretty significant volume bumps in recent days. That’s more likely attributed to higher volatility and investors/traders racing to exit positions rather than a migration of users from CEXs to DEXs though. We saw a similar spike back in mid-May during the LUNA/UST crash.

Uniswap and dYdX, however, have had pretty significant volume bumps in recent days. That’s more likely attributed to higher volatility and investors/traders racing to exit positions rather than a migration of users from CEXs to DEXs though. We saw a similar spike back in mid-May during the LUNA/UST crash.Token prices of certain DEXs and derivatives protocols have held up quite well considering the chaos of this week. dYdX in particular has not only recovered its losses, but been on a consistent uptrend over the last 48 hours.

This is definitely a tailwind for DEXs, but not one we will see come to fruition anytime soon. The UX of CEXs and DEXs are currently worlds apart – DEXs need to bridge this gap in order to gain meaningful market share against centralized counterparts.

This is definitely a tailwind for DEXs, but not one we will see come to fruition anytime soon. The UX of CEXs and DEXs are currently worlds apart – DEXs need to bridge this gap in order to gain meaningful market share against centralized counterparts.

Market makers have also gotten a wake up call this week – they cannot entirely trust that their exchange is operating as it should, irrespective of their relationship. This erosion of trust could serve as another catalyst for orderbook DEXs, since this is the market medium most trading shops are comfortable with. We previously published research on why decentralized orderbooks may be the end game for DeFi derivatives back in June.

It’s important to zoom out and see that this situation is not a failure of blockchains as a technology, but a single, centralized company that did not act in its customers best interest (and had the means to obfuscate their real activity behind closed doors).

Overall, we aren’t likely to ascertain the true impact of this situation for at least a few weeks, and maybe even a few months. Regulatory pressure and oversight is only going to become more contentious as a result of this week’s events. There’s a ton of speculation out there already, and the reality is we still don’t know all the facts. The best we can do is make sense of the information at hand based on pieces of info that’ll continue to be revealed from credible sources.

This does have the makings of an “ice age” moment for crypto, at least in the near term. But if anything, the news this week strengthens the case for decentralized technology. It shows us that businesses and projects existing in a transparent environment are a genuine improvement in situations like these. That’s a big positive. While the UX of crypto has a long way to go to be able to cater to the average investor or trader, the need for decentralization has never been clearer.

It’s Always Darkest Just Before the Dawn

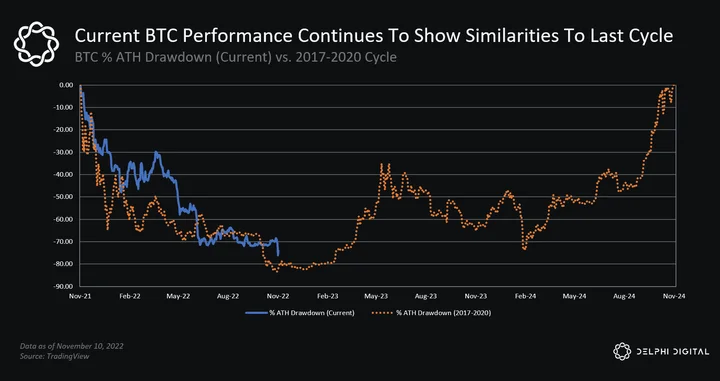

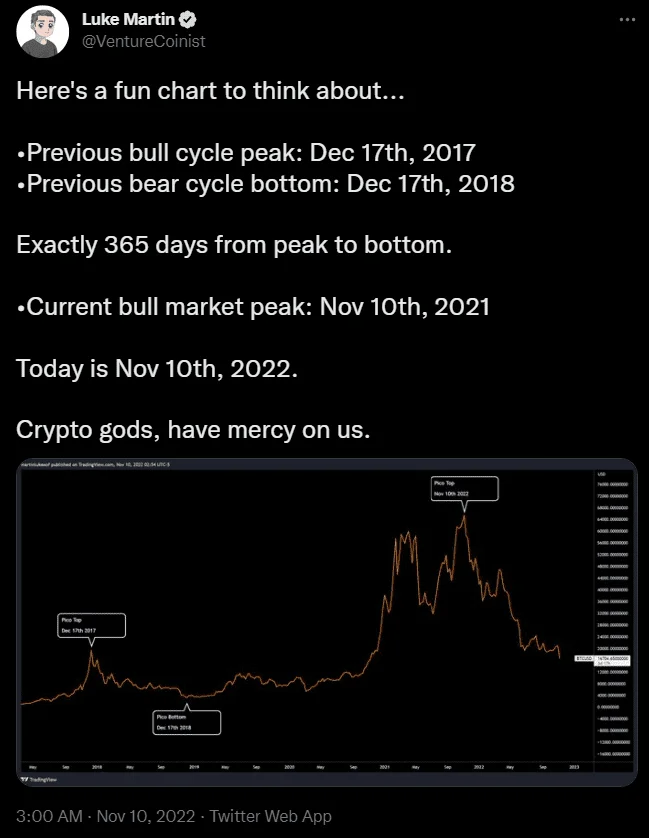

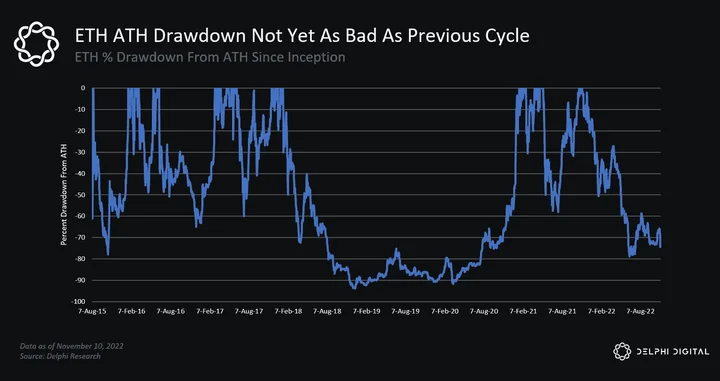

It’s not all dark and dire though. For starters, we did just witness one of the biggest left-tail events to ever hit the crypto market, and ETH still hasn’t broken below its June lows – it’s recovered back to where it traded for most of September-October.

The last bear market also bottomed in a violent drawdown just before Christmas in 2018. Almost right on cue, we saw a nasty selloff that pushed BTC to a new cycle low nearly exactly one year since its peak.

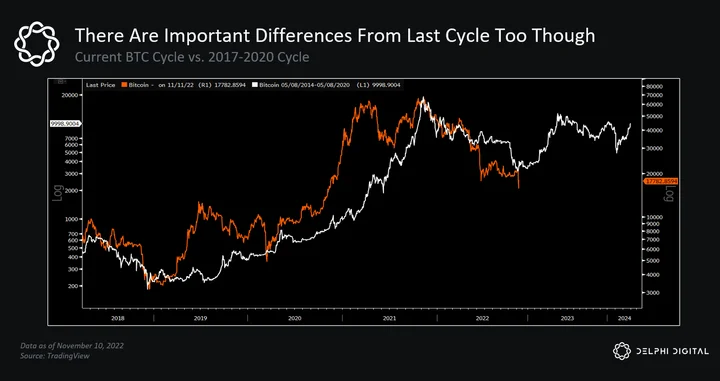

There are important differences between then and now, but the timing of peaks and troughs has been noticeably similar.

During a week like this, we could also use a dose of hopium too.

During a week like this, we could also use a dose of hopium too.

ETH’s drawdown hasn’t been as severe this time around either – last cycle it fell ~93% from peak to trough. Given the improvements in ETH’s supply-side fundamentals, it’s hard to imagine history repeating itself.

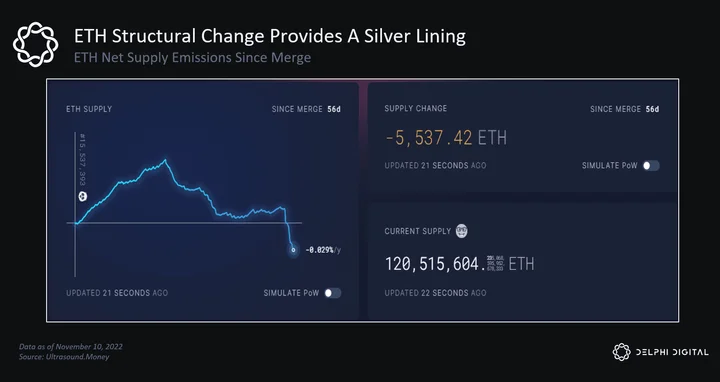

Speaking of which, one silver lining amid this week’s chaos is that ETH’s net supply emissions since the Merge finally turned negative, largely driven by the increase in transaction activity (which obviously came at a cost).

Speaking of which, one silver lining amid this week’s chaos is that ETH’s net supply emissions since the Merge finally turned negative, largely driven by the increase in transaction activity (which obviously came at a cost).

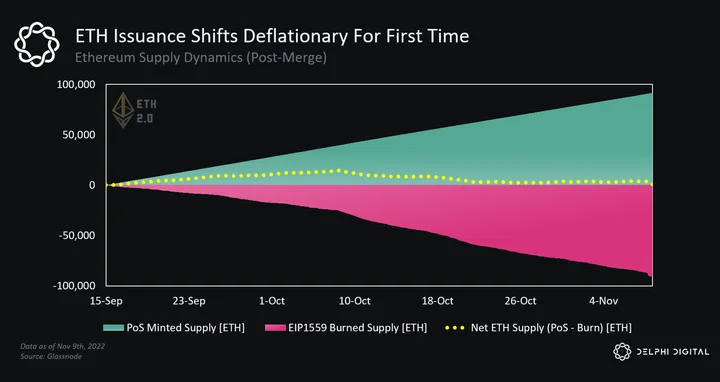

The panic derived from the FTX fallout caused a sharp increase in gas fees over the past few days. Since Nov. 8, the average ETH gas fee has been 53 GWEI, which has resulted in ~5.3k ETH burned per day. This was the ultimate reason behind ETH’s recent shift to issuance becoming deflationary. The chart below displays the progressive amount of ETH minted and burned since the Merge, with the yellow dotted line noting the net issuance.

The panic derived from the FTX fallout caused a sharp increase in gas fees over the past few days. Since Nov. 8, the average ETH gas fee has been 53 GWEI, which has resulted in ~5.3k ETH burned per day. This was the ultimate reason behind ETH’s recent shift to issuance becoming deflationary. The chart below displays the progressive amount of ETH minted and burned since the Merge, with the yellow dotted line noting the net issuance.

The post-Merge deflationary narrative matters very little in the face of a prolonged bear market, but it’ll take on a life of its own during the next bull run. Narratives matter more when price is trending up, and ETH has one of the strongest narratives of any asset at its back.

The post-Merge deflationary narrative matters very little in the face of a prolonged bear market, but it’ll take on a life of its own during the next bull run. Narratives matter more when price is trending up, and ETH has one of the strongest narratives of any asset at its back.

Closing Thoughts

If you’re looking for curated links to additional content our team put together, you can skip to the final section of the report below.

Kevin here – I wanted to share a couple personal thoughts on this situation before signing off for the week. The last few days have easily been some of the worst I’ve experienced since starting my crypto tenure. I think one of the reasons it’s all so painful – aside from the obvious financial hurt – is everyone just feels duped. SBF was someone our industry put on the highest of pedestals. Before this week, some would’ve gone so far as to argue he earned his place on the Mt. Rushmore of crypto pioneers.

I won’t speak for others (though I know some probably felt the same way) when I say I wanted FTX to thrive. I’m a big believer in the power of decentralized platforms – if I wasn’t I’d be off doing something else. But it’s possible for the two to co-exist, at least until we have better UX for decentralized peers. FTX was also more than just another centralized exchange. SBF was praised as a visionary by many outside of crypto, which in turn helped bring more credibility back to the industry itself.

I admit I cheered as the company went from startup challenger to mainstream incumbent. I smiled when I saw the FTX logo on a major league umpire’s uniform. I even chuckled at their Super Bowl commercials (which turns out Larry David wasn’t actually wrong after all). I bought into the narrative SBF was selling because I wanted it to be true.

The Narrative Machine at its finest.

The events that transpired this week are still difficult to come to terms with. When the news first broke, my jaw dropped. I wanted it to be a fake headline because, if it wasn’t, the blast radius from the fallout was going to be epic. And I didn’t know where that contagion would end (and truthfully I still don’t). Even if there’s a peaceful resolution at the end of the road, the psychological damage won’t fade away nearly as quickly.

FTX, Alameda, and SBF seemed to be at the center of nearly every major turning point in crypto markets this year. When the market started spiraling in what looked like a liquidity crisis back in May/June, as rumors started flying about other major crypto firms that were caught in the crossfire, SBF was out in front making deals left and right for companies on the brink of insolvency. The news helped calm some nerves, which in turn stemmed some of the bleeding. One could argue this was instrumental in ensuring the market bottom wasn’t retested, at least at the time. So the fact that this all turned out to be just smoke and mirrors blindsided all of us, and we all have the right to be on edge.

This week’s events will stay with us for a while, but I don’t think it’ll be the death of us. Some believe FTX’s now infamous collapse will push the space back several years. I don’t subscribe to that view. Yes, there are going to be a lot more headlines and a lot more information coming to light over the coming weeks (and even months). But crypto has too much momentum at this point – the train left the station a while ago. The collapse of one person’s empire isn’t enough to deal a death blow to everything this industry has built.

Jason made a comment earlier this week about main character syndrome and how it’s been an early warning sign for adverse events this year. We saw it leading up to the Terra/LUNA crash, and now we’ve seen it with the rise and fall of SBF.

Maybe Harvey Dent was onto something…and maybe the night really is darkest just before the dawn…

Additional Reading

Kyle (lookin for vc / data analyst internship) on Twitter

In FTX Bankruptcy, Startup Stakes Could Be Sold Off Fast

Exclusive: Behind FTX’s fall, battling billionaires and a failed bid to save crypto

Which crypto companies have exposure to FTX?

Crypto Market Structure Changes

NFT Startups Reportedly Not Affected by FTX Blowup

Serum Update and Post Mortem

0 Comments