The ETH Liquid Staking Derivative Wars

JAN 26, 2023 • 7 Min Read

🔍 The ETH Liquid Staking Derivative Wars

To stake ETH, users have to run validator nodes on Ethereum, which comes with a host of hardware and software requirements. Since it requires technical know-how, this is usually done by professionals. Apart from the blood, sweat, and tears, you also need an initial stack of 32 ETH.

Without the tech or the capital, what are Bob and Alice to do? Fear not, for they can also stake ETH by simply buying a token issued by one of the many liquid staking protocols. These protocols allow you to swap your ETH in return for a derivative token that represents staked ETH. The swapped ETH is then staked by the provider and the yield is passed on to you (minus fees).

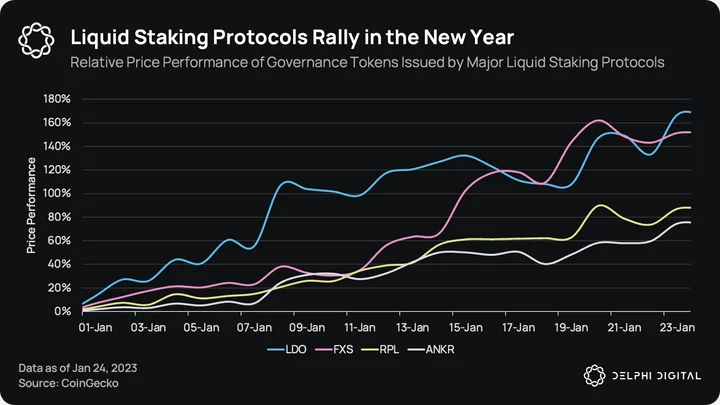

In March, Ethereum’s Shanghai upgrade will go into effect, which will also allow you to unstake the ETH (you can’t do this currently). The narrative of liquid staking is out in full force as we inch closer to the Shanghai upgrade. Since the beginning of 2023, liquid staking protocols have outperformed, with the market leader LDO gaining 167% in the past 3 weeks.

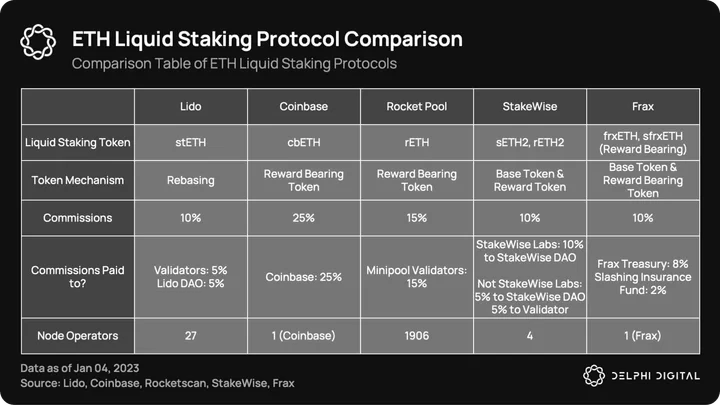

Some of the most notable protocols in this space include Lido, Coinbase, Rocket Pool, and Frax. Lido’s stETH is a rebasing token where the number of tokens held increases to reflect accumulated staking yield. Coinbase’s cbETH and Rocket Pool’s rETH is a reward-bearing token where the value of the tokens held increases to reflect accumulated staking yield. While Frax Finance’s sfrxETH is also a reward-bearing token, it is complemented by frxETH which is a stablecoin pegged to the value of ETH.

We explore these trends in further depth in our recent report on the future of ETH liquid staking, which is available for Delphi Pro members here. Here’s an edited snippet from the report:

“When comparing fees, Lido, StakeWise, and Frax charge the lowest commissions at 10%. Rocket Pool charges 15%, and Coinbase charges the highest at 25%. The lowest commissions benefit liquid stakers the most, as they’re able to retain more of their earned yields. Despite its relatively high commissions, Coinbase is currently the second-largest liquid staking derivative, due in part to its reputation as a trusted centralized exchange.

Node operators are responsible for staking ETH and running validators on behalf of depositors. Rocket Pool has the most widely distributed operator pool, with 1,906 individual operators. They allow anyone to set up a mini-pool validator, with a minimum requirement of 16 ETH staked from the operator and another 16 ETH staked from Rocket Pool depositors. Lido has the second largest operator pool, with 27 node operators. However, they control a significant portion of the staked ETH, raising concerns about centralization risks on the Ethereum network.”

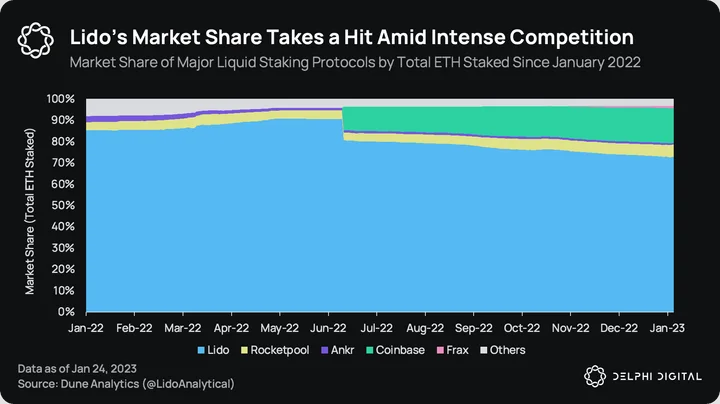

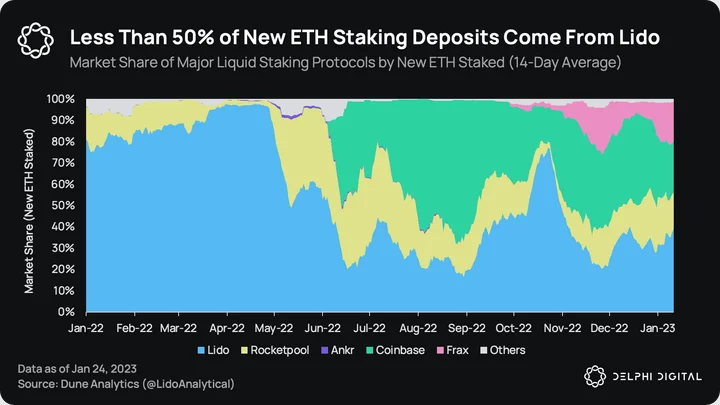

Currently, the dominant player in the war of liquid staking protocols is Lido. However, its market share has consistently declined since Coinbase’s entry into the liquid staking market in June 2022. While Lido’s market share stood at 85% in the beginning of 2022, it has since come down to 73%. And now, another entrant threatens to take even more market share from Lido… Frax Finance.

It isn’t easy to see the impact that Coinbase and Frax have had on Lido with a simple market share chart. So here’s where we see how new ETH staking deposits are being staked. Lido captured almost 80% of all new ETH staking deposits among liquid staking protocols at the beginning of 2022. Today, Lido captures less than 40% of new ETH staking deposits. On the other hand, Coinbase and Frax capture a combined 43%.

Coinbase’s growth is expected. The cbETH token is an easy-to-understand, simple reward-bearing token. The exchange business has a strong user base that can be easily onboarded to staked ETH. The company’s strong branding as a trusted centralized exchange also appeals to institutions that likely prefer to stake ETH through Coinbase. But what about Frax?

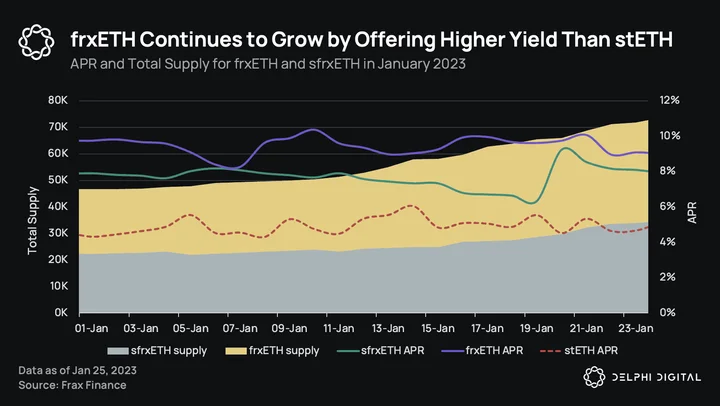

Users can deposit 1 ETH and mint 1 frxETH. Users can stake frxETH to get sfrxETH. While frxETH is a stablecoin pegged to ETH, sfrxETH is a liquid staking token that accrues value from staking rewards. Users can also provide liquidity to frxETH pairs on Curve and earn trading fees and token rewards. The ETH deposited to mint frxETH is staked with validators with 90% of the rewards flowing back to sfrxETH holders. Rewards are deposited back in the vault, allowing sfrxETH holders to redeem more frxETH than originally staked.

During the month of January, the total supply of frxETH has increased 58% while the total supply of sfrxETH has increased by 55%. Currently, there are 73.6K frxETH tokens but there are only 34.6K sfrxETH tokens. This allows sfrxETH holders to earn enhanced staking rewards sourced from ETH deposited by other users as well. These are users who have minted frxETH but haven’t staked for sfrxETH.

Currently, sfrxETH holders are earning an APR of 7.92% from all ETH staked with validators while frxETH holders are earning an APR of 8.95% from trading fees and token rewards. We expect these APRs to stay in a small range as capital flows to the more attractive option. On the other hand, stETH issued by Lido is currently earning an APR of 5.11%, making it clear why users might prefer Frax over Lido.

📅 This Week in Delphi Research

Heads or Thales: Exploring the Potential of Positional Parimutuel Markets

As Vitalik said in a blog post, prediction markets remain some of the lowest-hanging fruit for crypto disruption. In this deep dive, Jordan examines the major flaws in the current models and various innovations in the space. Specifically, he takes a closer look at Thales and attempts to forecast volume growth. Will you find this report to be a fascinating read? We predict yes.

LTC Shows Relative Strength Amid Market Chaos

LTC is scheduled for a havlening in August 2023. Historically, the token has rallied more than 6x in the run-up before the event. In this market note, Priyansh digs into the technical data to construct a top-down view of the market and points out the key levels for resistance and support over various time frames.

From 1 to 100: What the Future Holds for DEXs

Trust in CEXs is evaporating at a rapid pace as the dominos from the FTX collapse keep falling. Can DEXs take over the scene by leveraging the pangs of betrayal in the hearts of traders? In yet another report, Priyansh peers into his crystal ball and attempts to build a bull, bear, and base case for the growth of DEXs – the fastest-growing on-chain product.

📖 Delphi Reads

Co-founder of Reflexer, the protocol that issues the decentralized RAI stablecoin, Ameen Soleimani writes a tweet thread saying that it was a mistake to only accept ETH as collateral to mint RAI. While this allowed the stablecoin to reduce censorship risk and centralization, it also limited its ability to scale. Read the tweet thread here and reactions of the RAI community here. Back in August 2022, there was also some talk of introducing a multi-collateral version of RAI. Read more about that here.

Index Coop just launched the Diversified Staked ETH Index, which is composed of 44% Rocket Pool’s rETH, 30% Lido’s stETH, and 26% StakeWise’s sETH2. This diversifies your staked ETH across 3 liquid staking protocols. Notable exclusions include Coinbase’s cbETH (high fees, short track record) and Frax’s sfrxETH (short track record). Read more here.

Co-founder of Solana Labs, Anatoly appeared on the Superteam Podcast for a Solana vs. Ethereum debate with Toghrul, researcher at Scroll zkEVM. With Solana seeing somewhat of a resurgence in the new year, it might still be worth keeping tabs on the project. Watch the video here.

🔥 Meme of the Week

Last week, the Department of Justice announced an enforcement action that triggered some PTSD amongst market participants who have just been through a rough year. It was all anti-climatic when the action turned out to be against Bitzlato, a small Russian exchange. The action feels more like posturing than anything serious, as most of the significant fraud that the DoJ was supposed to protect against has already dealt damage to retail users.

Meme via @DoomPosting.

0 Comments