Report Summary

The “Fat Wallet” Thesis report explores how the blockchain value chain is evolving, particularly as protocols and applications are commoditized. This opens opportunities for wallets, which are close to the end-user, to capture significant value. Here are the key takeaways:

1. Thinning of Protocol and Application Layers

- Protocols, such as blockchains, are becoming commoditized due to factors like MEV redistribution, multi-chain adoption, and agentic paradigms. This results in lower switching costs and increased competition.

- Applications face commoditization due to low barriers to entry, composability, and token-based acquisition, which accelerates competition and makes it hard to build lasting moats.

2. Rise of Wallets as Value Aggregators

- Wallets, which serve as the primary front-end for users, are well-positioned to capture value. They have high switching costs due to user familiarity, brand trust, and user inertia.

- Mobile usage strengthens wallets’ positions as primary interfaces, and features like payment systems and yield management further entrench them.

3. Opportunities for Monetization

- Payment For Order Flow (PFOF): Wallets can monetize by owning user order-flow, capturing fees for facilitating transactions directly or through aggregation.

- Distribution as a Service (DaaS): By acting as a distribution channel, wallets can offer apps a pathway to users, similar to mobile app stores, potentially charging for featured placements.

- Additional Revenue Streams: Wallets can offer in-wallet payments, debit cards, and fiat on-ramps to enhance convenience and monetize user interactions.

4. Challenges and Alternatives

- Horizontally Integrated Super-Apps: Projects like Jupiter and Hyperliquid aim to create ecosystems around their services, aiming for a one-stop-shop approach, but they face hurdles like bootstrapping liquidity for each service.

- Cross-Chain Front-Ends: Platforms like Infinex aggregate apps across chains, offering a cohesive user experience and avoiding some technical challenges faced by super-apps.

5. Implications for Market Players

- Wallet providers like MetaMask and Coinbase could benefit most if they continue to innovate in user experience and accessibility. Emerging projects like Fuse, Magic Spend++, and One Balance also show promise in catering to niche markets and advanced cross-chain functionality.

The report suggests a shifting landscape where wallets may increasingly dominate due to their proximity to users, marking a potential shift from traditional blockchain value capture by protocols to more user-facing layers.

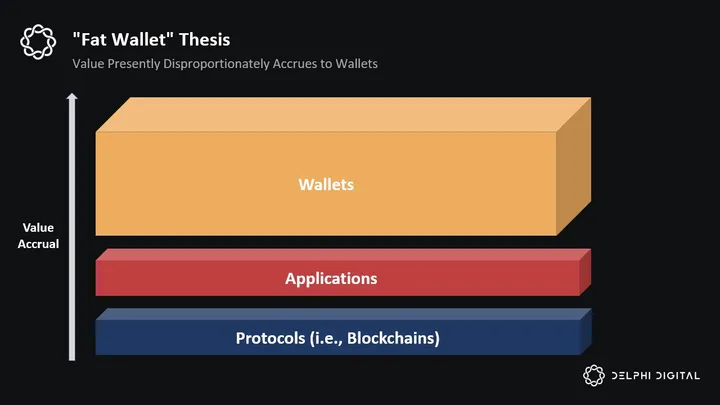

Throughout crypto’s history, there has been ongoing discourse around where value will ultimately accrue within the blockchain stack. While historically, the core contention has been between protocols and applications, there seems to be a third layer within the stack that everyone is ignoring — wallets.

The “Fat Wallet” Thesis asserts that, as protocols and applications increasingly “thin-out”, more room is being freed up for whoever owns the two most valuable resources — distribution and order-flow. Moreover, as the ultimate front-end, I believe no one is better positioned to monetize this value than wallets.

In this report we aim to accomplish four things. First, we will outline three structural trends that will continue to commoditize the protocol and application layers, leaving more room for front-ends to capture value. Subsequently, we will explore the various avenues for wallets to monetize their proximity to the end-user including payment-for-order-flow (PFOF) and selling apps Distribution as a Service (DaaS). From here, we will discuss two alternative paths — horizontally integrated super-apps and cross-chain front-ends — and why they could ultimately beat wallets in the race to owning the end user. Lastly, we will highlight the specific projects that stand to benefit from the “Fat Wallet Thesis”.

Towards “Thinner” Protocols

The question of where value will ultimately accrue within the blockchain stack can be reduced to a simple framework. For each respective layer of the crypto stack, ask yourself the following question:

If a product within this layer increases its take rate, will users leave for a cheaper alternative?

Downstream of this logic, we’re able to identify where switching costs are highest and thus who has asymmetric pricing power. Similarly, we can use this framework to identify where switching costs are lowest, and therefore which layer of the stack will become increasingly commoditized with time.

Let’s start with protocols (i.e., blockchains). In 2018, Joel Monegro laid the groundwork for why blockchains disproportionately capture value. Joel’s logic was simple. Given blockchains serve as the shared infrastructure layer for apps, switching costs are much higher at the protocol layer. In other words, even if Ethereum raised its take rate back in 2018, Uniswap can’t leave for another chain because doing so would relinquish both Uniswap’s existing user base as well as Uniswap’s composability with other Ethereum-native DeFi apps. Consequently, Uniswap is forced to remain on Ethereum, and downstream of this, users must also remain on Ethereum.

Joel’s conclusion was that while applications disproportionately captured value in Web2, the opposite will be true in Web3 — the crypto stack will be composed of “thin apps” and “fat protocols”.

While Joel’s thesis has turned out to be directionally correct thus far, a lot has changed since 2018. I would argue that there are three structural trends today that are increasingly “thinning-out” the protocol layer:

- Maturation of the MEV Supply Chain: While MEV will never be entirely eliminated, there are numerous initiatives, both at the application layer (i.e., LVR/MEV aware DEX primitives) as well as closer to the metal (encrypted mempools, TEEs, etc.), that will increasingly redistribute the amount of MEV extracted from end-users. Importantly, as the MEV supply chain continues to mature, value will increasingly climb up the MEV supply chain and asymmetrically accrue to whoever has access to the most exclusive user order-flow. As we will discuss, this implies that protocols will get thinner while front-ends and wallets get fatter.

- Multi-chain apps and chain-abstraction: Most apps today do not simply exist on one chain but rather multiple chains. In other words, apps that exist on Ethereum tend to also exist on Arbitrum and/or other L2s. We are also beginning to see more Ethereum-based DeFi apps such as Aave and MakerDAO expand to other alt-L1s such as Solana as well. As multi-chain becomes table stakes to remain competitive, the user experience across blockchains will become increasingly indistinguishable, and in turn, switching costs at the protocol layer will only get lower. Furthermore, chain-abstraction will further compress switching costs by abstracting away the bridging experience. As a result, apps will no longer remain beholden to the network effects of one chain, but instead, chains will become increasingly beholden to the distribution of front-ends.

- AI agents: In a similar vein, we seem to be heading towards a world where transactions are no longer executed by humans, but rather cross-chain agents and “solvers”. Importantly, humans and agents have structurally different incentives. Unlike humans who have subjective preferences, agents and “solvers” are programmed to principally optimize for best execution above all else. Under a chain-abstracted paradigm, intangibles such as brand or “vibes” and “alignment” will no longer be a moat. Instead, protocols will be forced to compete solely on transaction fees and liquidity. This would imply that as capturing agentic flow quickly becomes existential for blockchains to survive, chains will be forced to compress fees and incentivize liquidity to remain competitive — this should only further “thin-out” the protocol layer as a race to the bottom seems inevitable.

The net effect of the these structural trends is that both transaction fees and MEV will continue to compress, leaving more room for value capture from other layers of the stack. Coming back to our original framework, if Arbitrum meaningfully increased their take rate on transaction fees today, I expect they would in fact lose market share to other L2s such as base or L1s such as Solana supporting the same apps. This is especially true in a world where agents are routing user intents. Taken to its logical conclusion, fees will asymptotically compress to their technical limit, perhaps rendering hardware as the strongest source of defensibility for a protocol.

This brings us to the second argument from the “fat protocol” camp — moneyness. The moneyness argument hinges on two distinct ideas.

The first idea is that as long as transactions settle on the L1 (i.e., Ethereum Mainnet), users will by default have to hold ETH given gas is paid in the native token. Even within a chain-abstracted context, while users won’t hold gas tokens, agents and solvers nonetheless will. Therefore, it can be argued that ETH will remain “valuable” as a function of perpetual demand for the L1 asset.

While in theory this makes sense, this logic is reductive in practice. There is nothing stopping L2s such as Base from forcing users to pay for fees in USDC instead of ETH. From the perspective of solvers and agents, doing so would actually make sense as it would allow them to evade any directional risk associated with holding ETH inventory for gas. Holding ETH would instead only be necessary as working capital to pay for L1 blob space fees which are minimal. Therefore, in a world where attracting agentic flow dwarfs being “ETH aligned”, we could see ETH demand take a meaningful hit.

The second pillar of the moneyness argument is the idea that most assets are denominated in the L1 token and thus, trading on-chain inherently necessitates holding said token. This logic is also flawed for two reasons. First, buying ETH or SOL just to sell it for another token doesn’t necessarily foster sustainable demand. Rather, it simply increases the velocity of transactions denominated in the L1 token. Secondly, the asset that agents and solvers ultimately settle in will be deemed “money” — again, this will not be ETH but rather stablecoins.

To be clear, I’m aware this future is antithetical to the foundational tenets of crypto (i.e., censorship resistance, decentralization, etc.). However, this future implies we are no longer building solely for crypto purists. Crossing the chasm will necessitate making thoughtful compromises in the name of retail palatability. This doesn’t mean purists won’t still be able to use the L1 or the L1 won’t be used for use cases that require maximal decentralization. This simply means that the majority of users will value for UX over decentralization. The recent success of quasi-centralized projects such as Hyperliquid and TG bots clearly underscore this logic.

In summary, as switching costs across chains have never been lower, protocols have never been thinner. Furthermore, as we enter an increasingly chain-abstracted paradigm, it seems protocols will only continue to “thin-out” as they compete on tx fees and liquidity.

Towards “Thinner” Applications

Logically, this brings us to the application layer. Intuitively, one would assume that if protocols are getting “thinner”, applications must in turn get “fatter”. While some of this value will certainly get re-captured by applications, the “Fat App” thesis alone lacks nuance. The question shouldn’t be —“will apps get fatter?” — but rather — “which apps?”

When assessing value capture at the application layer, it is important to take into account three structural differences uniquely underpinning crypto apps:

- Forkability: The ability to fork apps implies that barriers to entry are implicitly lower for crypto apps

- Composability: Users have inherently lower switching costs given the interoperable nature of apps

- Token-Based Acquisition: The ability to use token incentives as an effective user acquisition tool means that the cost of acquisition (CAC) is also structurally lower for crypto apps

As I outlined in A New Framework For Understanding Moats In Crypto Market — (1) lower barriers to entry (2) lower switching costs, and (3) a structurally lower CAC — have the net effect of collectively accelerating the laws of competition for crypto apps. Consequently, it is extremely difficult to cultivate a moat and sustain market share. Kamino’s successful vampire attack is case and point.

While things like liquidity and TVL are often cited as strong sources of defensibility, both can nonetheless be subsidized by emerging competitors. This makes it extremely difficult to charge a take rate and capture value as an application. As soon as an app turns on a “fee switch”, not only are there countless other indistinguishable apps offering the same user experience, but moreover, there may even be a handful of similar apps that will actually pay users through token subsidies and points. The structural instability in the perps market reflects this phenomena.

Consequently, I would argue that the “Fat App” thesis only applies in a narrow context — it will be the handful of apps that possess some properties that cannot simply be forked nor subsidized by emerging competitors that sustainably capture value. Conversely, I expect the rest of crypto apps will get increasingly commoditized with time. If you want to dive deeper into what defensibility ultimately looks like for crypto apps, I wrote about this in detail here.

Lastly, I would argue that the rise of AI agents and solvers will have a similar effect on applications as they will on protocols. Given agents and “solvers” will principally optimize for execution quality, I expect apps will also be forced into fierce competition over attracting agentic flow. While liquidity network effects should render a winner-take-all dynamic over the long run, in the near and medium-term, I expect DeFi apps will increasingly experience a race to the bottom.

This begs the question, if both protocols and apps continue to “thin-out”, where will the majority of this value get re-aggregated?

The “Fat Wallet” Thesis

To date, the consensus thinking has been that value accrual will look fundamentally different in crypto markets. I hold the opposite view. Instead, I believe value accrual will reflect the same natural law that has governed value accrual in Web2 — whoever owns the end user disproportionately captures value.

As the canonical front-end, I believe no one is closer in proximity to the end user than wallets. There are five sub-theses supporting this logic.

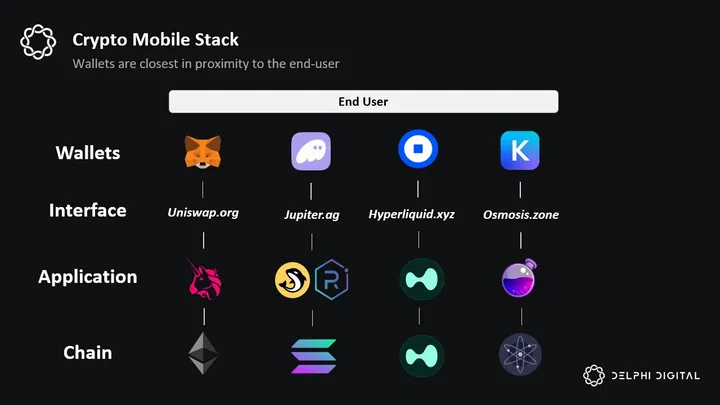

Sub-Thesis #1: Wallets Dominate The Crypto Mobile UX

A good litmus text for understanding who owns the end-user in the mobile context is to ask the following: which Web2 app do users ultimately interface with? While most users “interact” with Uniswap’s front-end to trade, they nonetheless access this front-end through their wallet application.

I would therefore argue the wallet provider is closer in proximity to the end-user. This implies that if mobile increasingly dominates the crypto UX, wallets may only continue to strengthen their relationship with the end-user as the canonical application gateway. That said, Jupiter and Infinex seem to be formidable challengers here with their respective mobile apps (more on this).

Sub-Thesis #2: Wallets are subject to high switching costs

Given users are inherently path dependent and bridging funds and moving private keys is a mental sticking point for most, wallets are subject to strong user lock-in. Moreover, given users implicitly place a high degree of trust in wallet providers, brand and “lindyness” are especially strong sources of defensibility at the wallet layer. Once again, revisiting our original question — If this respective product in the stack increases its take rate, will users leave for a cheaper alternative? — the answer seems to be uniquely “no” at the wallet layer. The fact that users willing accept a 0.875% take rate on MetaMask’s in-wallet swaps reflects this logic.

Sub-Thesis #3: Wallets Meet Users Where They’re At

Crypto apps are financial by nature. Unlike Web2, almost every on-chain transaction is some form of a financial transaction. Consequently, the account layer is deeply fundamental to crypto users. Additionally, there are a handful of features uniquely synergetic with the wallet layer — payments, native yield on idle user deposits, automated portfolio management, and other consumer use cases such as crypto debit cards. Fuse seems to be leading the way here with features such as Fuse Earn and Fuse Pay which allows users to spend their wallet balance in the real world with a Visa debit card.

Announcing Fuse Pay

A virtual @Visa card that enables everyday, real-world spending of stablecoins directly from your Fuse wallet.

Learn more ↓ pic.twitter.com/p2UGOPJuoR

— Fuse (@fusewallet) September 20, 2024

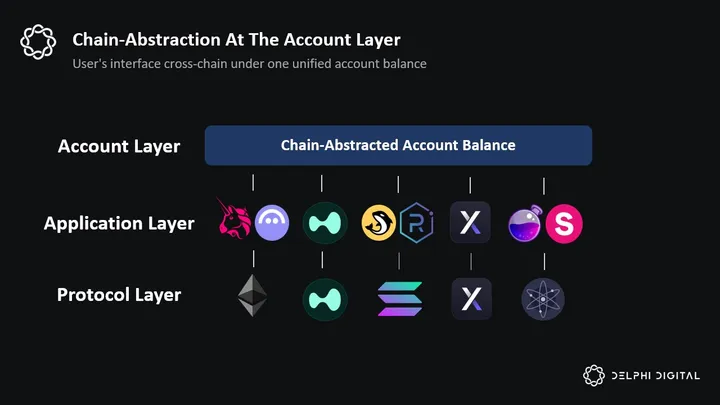

Sub-Thesis #4: Chain-Abstraction

While chain-abstraction is a technically thorny issue, one of the more compelling solutions is addressing chain-abstraction at the wallet layer. The idea that I can access any application across any chain from the comfort of a single account balance seems especially intuitive.

Projects such as Console, Initia, Magic Account, Polaris, Particle, and Coinbase’s smart wallet are all building toward this vision. One Balance is also taking a similar account-centric approach, but not simply because of the UX benefits. By locking the “state” of a user’s account instead of the chain itself, “credible accounts” enable users to benefit from the settlement times on destination chains while circumventing security concerns around double-spend issues. Going forward, I expect more teams will meet users where they are at and explore chain-abstraction at the wallet layer.

Sub-Thesis #5: Unique synergies with AI

Lastly, there seem to be three obvious opportunities for AI augmentation at the wallet layer. First, low hanging fruit here seems to be integrating AI agents to handle the execution of cross-chain transactions on the back-end. Importantly, while I expect agents to increasingly commoditize the rest of the blockchain stack, users will nonetheless need to permission agents to ultimately execute transactions on their behalf. This would imply the wallet layer is best positioned to become the canonical front-end for AI agents. Another opportunity for integrating AI at the account layer could include automated staking and yield farming strategies. Projects such as Dawn AI are building adjacent to this.

Additionally, given wallets ultimately own user data, there also seems to be an opportunity to created a curated user experience through harnessing the power of LLMs. This can also raise switching costs for users by providing a personalized UX only possible on that respective wallet. While harnessing user data feels antithetical to crypto’s foundational tenets, this is something wallet providers such as MetaMask are already doing behind the scenes.

Now that we have laid out “why” wallets will increasingly own the end-user relationship, let’s explore “how” they will ultimately monetize their relationship with the end-user.

Opportunities for Monetization

Payment For Order Flow (PFOF)

The first opportunity for wallets to monetize is by owning user order-flow. While the MEV supply-chain will continue to evolve, one thing will increasingly hold true — value disproportionately accrues to whoever has the most exclusive access to order-flow.

In other words, all the ongoing initiatives to redistribute MEV — both at the application layer (e.g. LVR-aware DEXs etc) as well as closer to the metal (e.g. encrypted mempools, TEEs, etc) — will disproportionately benefit whoever is the originator of that orderflow.

The reason is simple. Anyone downstream of order-flow origination will increasingly lose pricing power as the MEV supply chain matures while the originator of order-flow (i.e., front-ends) increasingly gain bargaining power. Said differently, the only stakeholder that can increase their take rate without losing market share will be the order-flow originators themselves.

Let’s first explore who these front-ends are today and subsequently speculate on how this market structure may change going forward.

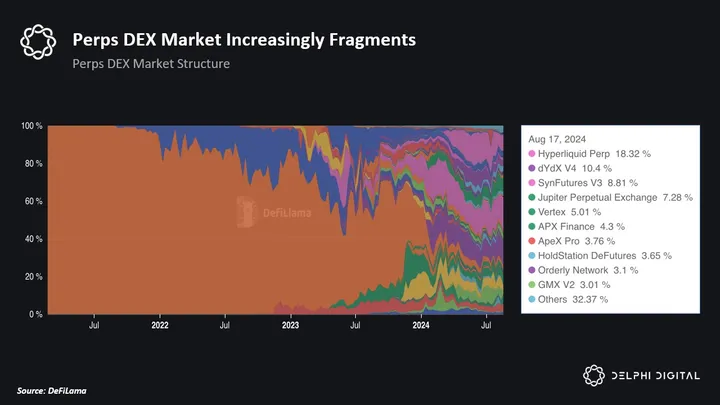

Despite historically dominating the order-flow market, DEX front-ends are increasingly losing market share to three alternative front-ends:

- Solver Models: These front-ends are agnostic to where liquidity is sourced from. In other words, solvers can either fill user intents through multiple on-chain DEXs, directly through private market maker inventory, or a combination of both. The leading solver models today are CowSwap and 1inch Fusion.

- Telegram Bots: These front-ends offer two main services: (1) enabling users to conveniently trade tokens from the comfort of their Telegram interface and (2) token “sniping” or allowing users to buy a token launch in its initial block. As I see it, TG bots represent v1 of agentic front-ends. Some of the current leaders in the TG bot space include Banana Gun and Maestro.

- Wallet Swaps: Wallet swaps enable users to trade tokens from the convenience of their wallet front-end without needing to interface with apps. While most wallet swaps are currently routed through a third-party aggregator (e.g. 1inch), other wallets are exploring integrating their own solver networks to improve execution (e.g. Shogun). The leading wallet swap providers today are OKX wallet and Meta Mask Swaps.

While on the surface it appears that solver models are increasingly dominating the order-flow market, it is essential to note that not all order-flow is created equal. There are two distinct kinds of order-flow: (1) fee sensitive flow and (2) fee insensitive flow.

Generally, solver models and aggregators disproportionately dominate “fee sensitive” flow. Given these users are trading in 100k+ size, execution matters to them. These traders won’t accept even 10 bps in excess fees. Accordingly, “fee sensitive” traders are the least valuable customer segment. Despite owning the majority of the front-end market by volume, these front-ends generate far less value per $1 traded.

Conversely, wallet swaps and TG bots own the most valuable user base — “fee insensitive” traders. Instead of paying for execution, these traders are paying for convenience. Accordingly, paying 50 bps on a trade is irrelevant to these users, especially when they’re expecting a binary outcome of either 100x or zero. Consequently, TG bots and wallet swaps produce far more revenue per $1 of volume swapped.

Now that we have laid out the current state of the order-flow market, let’s speculate on how things will change, specifically as on-chain activity becomes increasingly cross-chain. Going forward, I expect three trends will continue to play out:

- Order-flow becomes increasingly valuable: As more stakeholders (i.e., solvers, ai agents etc) are added to the MEV supply-chain in a chain-abstracted context, this will only further underscore the value of exclusive order-flow. Moreover, as I alluded to earlier, the countless ongoing initiatives to redistribute MEV will also result in more value re-captured by front-ends. In other words, the maturation of the MEV supply chain will inherently result in “thinner protocols” and “fatter front-ends” as orderflow becomes all that matters.

- DEXs become back-ends: The ultimate winners of this first trend will be whoever owns the end-user as the ultimate front-end, specifically “fee-insensitive” users. While DEXs are currently the leaders here, this may continue to change, especially as more cross-chain front-ends emerge. The top two contenders here in my eyes are chain-abstracted wallets and alternative front-ends such as Infinex.

- TG bots maintain their stranglehold on their respective market: Lastly, I expect TG bots will continue to serve their respective market segment of retail traders looking for non-linear payouts from the comfort of their Telegram interface. While this is certainly a more narrow market, it is nonetheless a valuable customer base.

Lastly, one interesting project that stands out in the context of wallets and order-flow is DFlow. Dflow enables Solana wallets and apps to effectively “sell” their non-toxic order-flow to liquidity providers on both order-books such as Phoenix as well as AMMs. Given DFlow order-flow is non-toxic retail flow (i.e., not CEX/DEX arb), LPs can theoretically quote traders with tighter spreads (in the context of AMMs this is done by adjusting fees dynamically).

This model can both give users better net execution, thus freeing up more room for wallets and apps to charge a take rate and capture value. DFlow uniquely makes sense integrated at the wallet layer given wallet order-flow is non-toxic by nature.

Distribution as a Service

This brings us to the second opportunity for wallets to monetize their proximity to the end user — Distribution as a Service (DaaS).

Downstream of serving as the canonical front-end through which users interface on-chain, apps are ultimately at the whim of the distribution of wallet providers, specifically within the mobile context. Furthermore, I expect wallets will only gain more leverage over apps as most new users onboard via wallets as the primary on-chain gateway. The commoditization of DeFi apps will concurrently put more power into the hands of wallets as we discussed early.

Accordingly, in a similar way that Apple has monetized IOS, wallets seem well positioned to reach exclusive deals with apps in return for providing distribution. For example, wallet providers could build-out their own app-store and charge apps with some revenue sharing agreement. While MetaMask is not currently monetizing their “snaps” feature, I expect they will at some point given they have inherently strong bargaining power.

In a similar vein, wallet providers could also steer users towards specific apps in return for some shared economics. The advantage this approach has over traditional advertising is that users can seamlessly make purchases and interface with apps all from the comfort of their wallet. Coinbase already seems to be exploring a similar path with “featured” app and in-wallet “quests”.

As attention becomes the most valuable resource in the crypto economy, we could see a shift in demand from “Block Space” to “Wallet Space”.

Additional Opportunities

Lastly, there are a handful of other notable opportunities for wallets to monetize their proximity to the end-user:

- In-Wallet Payments and Debit Cards: Payments are often cited as a “killer use case” for crypto given the instantaneous settlement times that blockchains provide. While we have yet to see a crypto payment app reach escape velocity, this feature seems especially intuitive if integrated at the wallet layer. Once again, by meeting users where they are (i.e., at the account layer), wallets are well-positioned to either reach exclusive partnerships with existing payment apps or possibly build out their payment feature within the wallet. Similarly, as alluded to earlier, wallets could also build out their own debit cards and thus allow users to spend their crypto in the “real world”. Both could represent meaningful revenue streams at scale while simultaneously raising switching costs.

- On and Off-Ramp: Another lucrative crypto business is providing users with the ability to on and off-ramp into fiat. Once again, as the canonical gateway, wallets are also well positioned to reach exclusive deals here with on/off-ramp service providers.

- Yield Farming as a Service: Wallets can provide users with lucrative yields on idle deposits in return for a small fee. This feature can also be enhanced with the use of AI agents.

The Race To Owning The End User

Thus far, we have strictly laid out the bull case for why wallets will disproportionately capture value. Let’s now lay out the bear case.

While it is clear to me that the crypto user experience will increasingly reflect one unified front-end from which users can perform any on-chain action, it is less obvious what this front-end will ultimately look like. Although wallets seem to have a clear head start in the “race to owning the end user”, there are two additional paths that seem to be converging on a similar vision as a unified front-end — horizontally integrated super-apps and cross-chain front-ends.

Path #1: Horizontally Integrated Super-Apps

These are apps that use an initial product as a wedge to integrate an ecosystem of adjacent apps. The goal with this approach is to become a fully integrated one-stop-shop of native applications unified under one front-end. Importantly, given this super-app approach is built on the same chain, the user experience is unconstrained by the technical complexities of synchronizing state across multiple chains. While this may sound like a trivial nuance, these technical pain points add additional latency, costs, and security implications that could meaningfully hinder the user experience. Another underappreciated advantage of this approach is that it more efficiently and securely enables cross-margin which is inherently limited under a multi-chain approach.

Some projects that seem to be pursuing this super-app approach are the following:

- Jupiter: Jupiter has used their spot aggregator as an initial wedge to subsequently build out their own launch pad, LST, and native perps DEX, which is now the fourth largest perps platform across all chains at time of writing. Jupiter also recently announced plans to integrate their own solver model/RFQ product and mobile app with built-in on-ramping. The latter clearly signals an attempt to get closer in proximity to the end user by becoming the ultimate Solana front-end. Given Jupiter already has a strong relationship with the end-user through their aggregator product, I see them as a formidable challenger in the race to owning the end-user in the Solana ecosystem.

It’s never been easier to trade on Solana, with Jupiter Mobile.

Zero Platform Fees, Built-in On-ramp.

Best Mobile Swap experience on Solana. pic.twitter.com/gczPglBNUD

— Jupiter 🪐 (@JupiterExchange) October 8, 2024

- Drift: By using their novel perps DEX model — dynamic AMM + decentralized central limit order book + just-in-time (JIT) liquidity — as an initial wedge, Drift has also since expanded to offering a host of synergistic products including spot trading, lending, pre-launch futures, synthetic derivatives and more recently an in-house prediction market. Importantly, given each of these features exist under one super-app, Drift is able to seamlessly offer cross-margin. This killer-feature is much harder to integrate under cross-chain front-ends.

- Hyperliquid: The Hyperliquid team has done an incredible job building out one of the most intuitive perps trading experiences. Today Hyperliquid is the leading perps DEX by trading volume at 27% market share. Hyperliquid has also recently integrated their own spot DEX. I would not be surprised if in the near-future the team uses their current market positioning to ship adjacent products such as a lending arm and perhaps a prediction market.

- Ethena: As first and foremost a synthetic dollar, Ethena is coming from a different starting point to building out a super-app ecosystem. However, given Ethena already disproportionately provides flow to perps exchanges through USDe, it seems relatively low lift for them to provide this flow to emerging exchanges in return for some economics. Moreover, if the Ethena team was to support an ecosystem of additional apps such as lending and spot trading, the advantage these USDe-centric apps would have is a structurally lower cost of capital given USDe is inherently yield bearing. Since writing about this in August, the Ethena team has clearly signaled that they are in fact pursuing this approach.

The temp check vote in favour of Ethereal’s potential integration with Ethena has passed, and the Ethena Network roadmap begins

sENA and rsENA holders begin earning rewards for @etherealdex now

More details below ⬇️ pic.twitter.com/mQIQSAVitK

— Ethena Labs (@ethena_labs) October 3, 2024

While at scale this super-app approach is certainly more defensible than pure front-ends, it is worth noting some tradeoffs.

First, these apps are forced to bootstrap each adjacent product from scratch. In other words, unlike aggregators and wallets who can flexibly plug into existing apps according to what users want, super-apps must undergo the infamous liquidity bootstrapping phase to each respective app. While this process is certainly easier as adjacent products can serve as synergistic extensions to the initial product, this approach nonetheless implies taking on existing incumbents. This is especially difficult given incumbents have a much more narrow product focus.

As I mentioned in A New Framework For Identity Moats In Crypto Markets, when code is a commodity and liquidity can be subsidized, constantly shipping and improving existing products is arguably the only way to grow and maintain market share. Horizontally integrated super-app are at an inherent disadvantage here. Consequently, while there are a handful of teams I would certainly not bet against here, the super-app approach will certainly face headwinds in the race to owning the end user.

To be clear however, while these apps may not win the race to owning the end-user, I still expect they will continue to capture meaningfully value. Each of these apps are both (1) leaders in their respective verticals and (2) spearheaded by elite teams. As long as scope creep doesn’t get the best of them and they continue to improve their existing product, I expect these apps will remain market leaders. They may just evolve into more back-end liquidity layers for alternative front-ends who ultimately own the end-user.

Path #2: Cross-Chain Front-Ends

This brings us to the second path in the race to owning the end user — cross-chain front-ends. Instead of building out the applications themselves, this approach aims to be more of a cross-chain application aggregator of sorts. However, where this approach differs from the wallet-centric approach is that it is more of a traditional application. Thus, this front-end will likely abstract the account layer through a more Web2 onboarding experience. While these projects won’t be able to meet users where they’re at to the same degree as existing wallets, the onboarding experience will likely be a lot smoother and familiar to non-crypto users.

Another advantage of this approach relative to super-apps is that you immediately transcend the liquidity cold start problem by plugging into existing apps. This allows these front-ends to remain flexible and integrate emerging apps according to what users want at that time — all while keeping operating expenses to a minimum. One killer feature here could include allowing users to farm multiple airdrops from the comfort of this unified front-end.

It is also worth noting that given these projects will support apps across multiple chains, they will rely on some back-end infrastructure such as intent-based bridges, AI agents, or more generalized chain-abstraction solutions such as NEAR’s chain signatures or Anoma’s universal intent machine (UIM) for non EVM chains.

The leading project taking this approach is Infinex. By serving as a front-end aggregator of numerous apps across both EVM chains and Solana, Infinex aims to offer a CEX-like experience while preserving principles such as non-custody, trustlessness, and permissionlessness. Infinex will also secure user accounts with Passkeys, thus evading the UX pain points associated with seed phrases.

Infinex will initially offer spot trading and staking with plans to integrate perps, options, lending, margin trading, yield farming, as well as a fiat on-ramping feature. While it is still early, I expect Infinex will continue to garner hype leading up to their official launch. Moreover, as someone who has been building in crypto for a while, Kain is also not someone to bet against.

I believe both Infinex and Jupiter are perhaps the top two non-wallet contenders in the race to owning the end-user.

Implications of the “Fat Wallet” Thesis

In summary, the “Fat Wallet” thesis posits that as protocols and applications increasingly “thin out”, wallets and other front-ends are best positioned to re-capture this value by owning the two most scarce and valuable resources — user attention and order-flow.

Before concluding, let’s quickly outline who some of the biggest beneficiaries of the “Fat Wallet” Thesis are today, and will be going forward. Intuitively, given the high switching costs at the wallet layer, existing incumbents are well-positioned to maintain their market dominance.

However, MetaMask’s slow motion decline since 2023 reflects the fact that switching costs alone are not a sustainable moat. MetaMask’s UX has been long criticized as being unintuitive, especially for new users. Moreover, exchanges such as Coinbase, OKX, and Bitget have an inherent advantage over MetaMask by owning the top of the distribution funnel. Most users who start buying majors and subsequently want trade longer-tail tokens intuitively view exchange-owned wallets as the logical choice.

Just tested Coinbase Smart Wallet for the first time. This is an absolute game changer.

Went from no wallet (no extension) to minting an NFT in 20 seconds. All while signing securely with Touch ID.

This is how we bring mass retail onchain, huge kudos to the Coinbase team. pic.twitter.com/3BL9gaxNbT

— cygaar (@0xCygaar) May 24, 2024

Furthermore, the launch of Coinbase’s smart wallet will make this process increasingly seamless. Users will be able to spin up a wallet without the need for a browser extension or app. Instead, given smart wallets are smart accounts deployed on Base, passkeys will be used to abstract traditional UX pain points associated with seed phrases. Additionally, users will be able to transact on-chain using their Coinbase exchange account balance, thus abstracting the complexities of sending funds to a wallet address.

Given (1) Coinbase already owns the top of the distribution funnel and (2) it will be inherently difficult to compete with their UX, I expect Coinbase may be the primarily beneficiary of the “Fat Wallet” Thesis. Jesse Pollak also recently announced that he is now leading the Coinbase Wallet team, signaling that the wallet layer is a core focus for Coinbase.

hey everyone – some news: in addition to leading the @base team, i’ll be stepping up to lead @coinbasewallet and joining the @coinbase exec team.

i’m really excited to take on this new mandate and to accelerate our mission of bringing a billion people and a million builders…

— jesse.base.eth (@jessepollak) September 30, 2024

While Coinbase and other exchanges are well-positioned in growing their respective user bases, there are a handful of emerging projects that I nonetheless remain excited about:

- One Balance: Spearheaded by former Flashbots co-founder Stephane Gosselin, One Balance is building “credible accounts” for apps and wallets to enable users to interact cross-chain all from one unified account balance.

- Fuse: One of the leading wallets in the Solana ecosystem, Fuse is building out novel features such as Fuse Earn and Fuse Pay which allows users to spend their wallet balance in the real world with a Visa debit card.

- Magic Spend++: In collaboration with Coinbase and Socket, Magic Spend ++ allows users to trade assets cross-chain all from the comfort of their Magic Spend account.

- Polaris: Built by the Osmosis team, Polaris is a Cosmos-native wallet that enables users to swap assets across numerous chains through one unified wallet balance.

- NEAR: Chain-signatures built by the NEAR team allow users to securely interact across multiple chains; wallets leveraging chain signatures include SWEAT Wallet and HOT Protocol’s native Hot Wallet built as a Telegram mini-app.

- Consumer-Centric Chains: Instead of catering to the end-user as a front-end, consumer-centric chain such as Abstract and Xion are taking a qualitatively different approach by tailoring their value prop to applications; these chains enable apps to retain their proximity to the end user by effectively providing “chain-abstraction” and “account-abstraction” as a service.

Importantly, given high switching costs will likely continue to insulate existing incumbents, these emerging projects will need employ effective go-to-market (GTM) strategies to gain market share. While still a nascent area of focus, there are a handful of GTM ideas that could be interesting:

- Incentive Campaigns: By incentivizing users through points, token airdrops or attractive yields on idle deposits, emerging wallets can more effectively acquire users. Wallet, a Telegram native wallet provider, has been offering initial users 50% APY on up to 3000 in USDT deposits. Spending more on incentive campaigns can be uniquely justified at the wallet layer given wallet users tend to have structurally higher LTVs relative to apps.

- Web Proofs: Given the aforementioned incentives can be easily gamed, one creative solution to more effectively allocate incentives is by using Web Proofs. By heavily incentivizing users who can prove they have moved their assets from MetaMask or some other wallet provider, emerging wallets can more effectively acquire users.

- Niche Focus: By targeting an initial user bases (e.g., memecoin traders, DeFi power users, NFT collectors, etc) wallet providers can use this as a wedge to subsequently expand their offerings. Mobile memecoin trading seems like the most obvious GTM strategy here.

- Blinks: Instead of trying to bring non-crypto users to crypto, emerging wallets can instead meet potential users where they are at with blinks. This could be especially effective if accompanied with any of the aforementioned economic incentives as well as a smooth onboarding experience.

- TG Native-Wallets: Similarly, emerging wallets can cater to users by offering Telegram-native wallets. TG bots provide an obvious proof of concept for the effectiveness of this approach. I remain excited about the idea of a TG bot that allows users to preform additional functionalities beyond trading shitcoins.

- Social Integration: Social network effects tend to be the strongest form of network effects. Consequently by integrating some social element, wallets can cultivate a stronger relationship with the end user while also raising switching costs.

Looking Ahead

Crypto markets are quietly undergoing a shift. Despite historically capturing the majority of value in the crypto stack, I believe the protocol layer will continue to “thin-out”. Counterintuitively I do not believe it will be applications that re-capture this value, but rather front-ends who ultimately own the end user.

While wallets have a clear head-start in the race to owning the end-user, I remain excited about the prospects of alternative front-ends such as Infinex and Jupiter as formidable challengers.

As more investors and builders realize the importance of owning user attention and order-flow, I expect the we will continue to see the race to owning the end-user heat up.

0 Comments