Introduction

Proof-of-stake (PoS) is a consensus mechanism used in blockchains to process transactions, create new blocks, and maintain the chain’s security. In PoS, tokens are staked in order to provide security for the network. In return for staking their tokens, users are compensated with block rewards from the network and fees paid by users. To stake tokens, users have to run validator nodes. Given the technicalities involved with this, validation is typically undertaken by professional node runners.

To increase accessibility to staking and liquidity, liquid staking protocols like Lido and Rocket Pool were developed. These protocols allow users to stake their tokens with validators in exchange for a portion of the interest yield earned. Additionally, these liquid staked tokens can be easily traded on decentralized exchanges, allowing users to convert them back to unstaked tokens (e.g., from stETH to ETH).

In this report, we analyze the ETH staking market from a business and financial perspective. The end goal of this exercise is to try and ascertain these protocols’ potential for value generation.

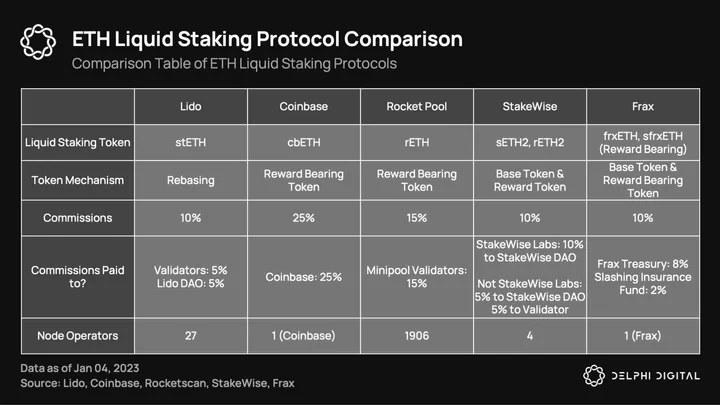

These liquid staking derivatives (LSDs) may appear similar at first glance, but they have distinct differences that set them apart. Each protocol has a unique derivative token that accrues or processes rewards differently. They also have different fee and commission structures that impact net rewards to holders.

Token Types

Rebasing Token

Rebasing tokens have an elastic total supply that can increase or decrease; the change in supply is spread proportionally across token holders. Lido’s stETH is a rebasing token, and yields earned are automatically reflected in the increased amount of stETH held. While simple for users, this can get complicated when used in DEXs, as stETH in liquidity pools also has to rebase.

Reward-Bearing Token

Reward-bearing tokens are tokens that increase their underlying value over time as rewards accrue. Unlike rebasing tokens, these do not have an elastic supply that changes frequently. Coinbase, Rocket Pool, and Frax (sfrxETH) use this token mechanism.

Base Token + Reward Token

StakeWise uses a unique model of base (sETH2) + reward token (rETH2) to segment a user’s yield and rewards, both of which are worth 1:1 with ETH staked and earned on the beacon chain. This is mainly done to help mitigate impermanent loss when providing liquidity in DEXs. However, because two liquidity pools are required, this results in segmented liquidity and potentially higher slippage.

Base Token + Reward-Bearing Token

Frax utilizes a unique model that allows users to choose between two tokens, frxETH and sfrxETH, to achieve different objectives. frxETH does not earn beacon chain yields from staked ETH, whereas sfrxETH earns all yields from staking. This means that sfrxETH earns yields from all frxETH that is not staked, increasing its yields.

There are two key advantages of this model:

- frxETH is designed to maintain parity with ETH, which makes it attractive to liquidity providers who can offer frxETH-ETH liquidity pools. Additionally, Frax owns the largest amount of protocol-owned CVX, which it can use to direct emissions and attract more liquidity. When using frxETH to provide liquidity, liquidity providers do not earn beacon chain yields from staked ETH.

- Users have the option to generate yields through liquidity provisioning or staking frxETH to sfrxETH. These yields are instead directed towards sfrxETH, which results in higher yields for sfrxETH than other liquid staking derivatives. This allows sfrxETH to achieve a “levered” yield, as the yield earned on 1 sfrxETH is greater than the yield earned on 1 staked ETH.

It’s worth noting that not all ETH staked to frxETH is deposited with validators. frxETH has an Algorithmic Market Operations (AMO) feature where some of the ETH deposited into frxETH is used to help maintain the frxETH-ETH peg. This can be viewed as Frax using their CVX voting power to indirectly increase the yields earned on staked ETH at the expense of beacon chain incentives. However, sfrxETH stakers can still earn more than the yield earned on 1 staked ETH, so it’s a trade-off that ultimately results in a net benefit.

Commissions

When comparing fees, Lido, StakeWise, and Frax charge the lowest commissions at 10%. Rocket Pool charges 15%, and Coinbase charges the highest at 25%. The lowest commissions benefit liquid stakers the most, as they’re able to retain more of their earned yields. Despite its relatively high commissions, Coinbase is currently the second-largest liquid staking derivative, due in part to its reputation as a trusted centralized exchange.

Node Operators

Node operators are responsible for staking ETH and running validators on behalf of depositors.

Rocket Pool has the most widely distributed operator pool, with 1,906 individual operators. They allow anyone to set up a mini-pool validator, with a minimum requirement of 16 ETH staked from the operator and another 16 ETH staked from Rocket Pool depositors.

Lido has the second largest operator pool, with 27 node operators. However, they control a significant portion of the staked ETH, raising concerns about centralization risks on the Ethereum network.

StakeWise is working towards decentralization through the launch of StakeWise v3, which will allow for permissionless node operators. StakeWise v3 was originally slated to launch in late 2022, but has since been pushed to early 2023.

Frax Finance is planning for frxETH v2, which will help decentralize frxETH. It is expected to launch closer to the ETH Shanghai upgrade in March 2023.

Liquid Staking Traction and State of the Market

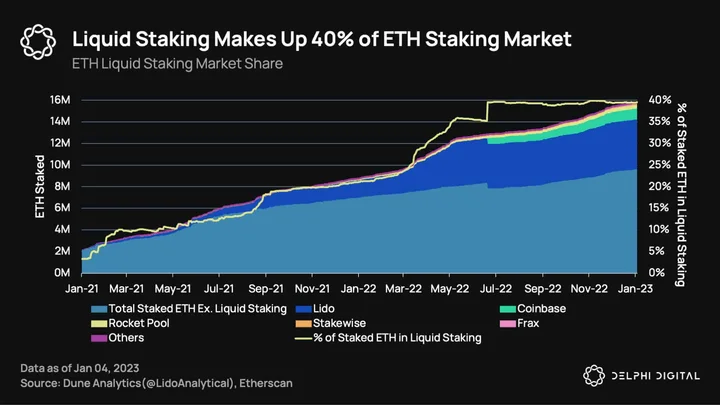

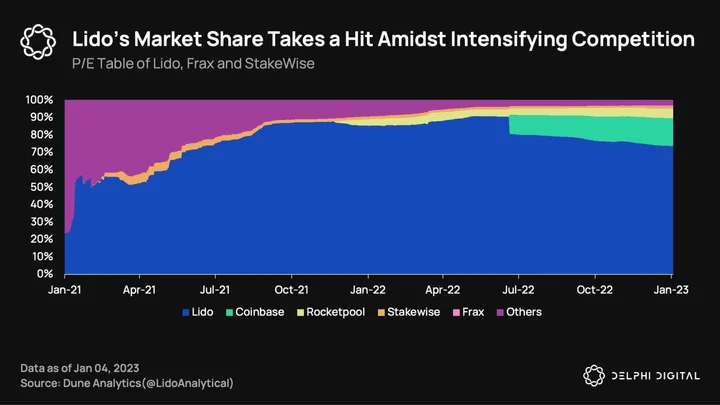

The ETH liquid staking market has grown tremendously, now capturing approximately 40% of all ETH staked. Lido is the clear leader, holding approximately 30% of staked ETH. Since the Merge, staked ETH has continued to increase along with yields. As yields have risen, so has the competition, as a significant portion of the market is still yet to be captured.

While Lido remains the leader, its market share is slowly being eroded by competitors. Rocket Pool, StakeWise, and Frax are three protocols steadily gaining market share at Lido’s expense. Coinbase has also entered the competition, and now accounts for 16% of the liquid staking market. As one of the leading centralized exchanges, Coinbase has strong branding, and the ability to onboard users to staked ETH puts them in a prime position to grow.

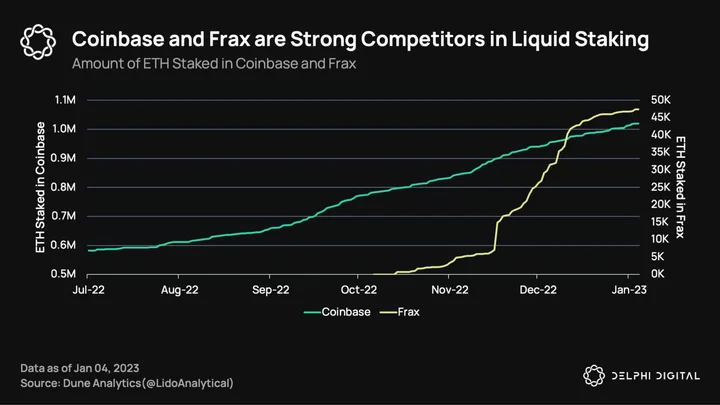

Coinbase and Frax are strong players to look out for given their astounding growth rates. ETH staked in cbETH increased Coinbase’s staked ETH from ~600k in July to ~1M as of Dec. 16th, 2022. Frax just launched their liquid staking product in October, and has seen rapid growth to ~45k staked ETH as of Dec. 16th.

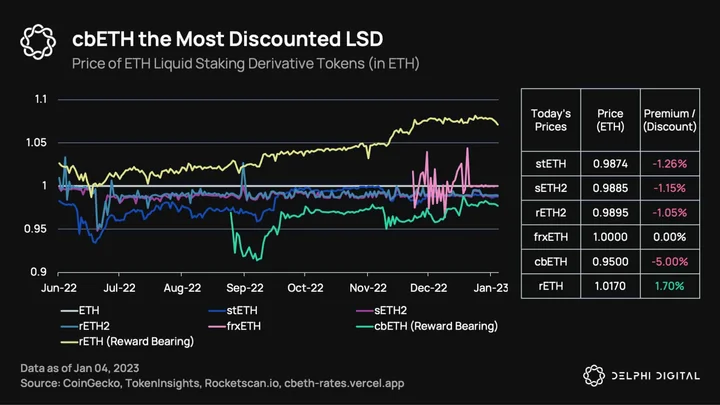

Note: Today’s prices of cbETH and rETH are normalized by their underlying ETH value, using the current price (in ETH) / underlying ETH.

Most LSDs consistently trade at a discount to their underlying value. In June, prices for all LSDs experienced a sell-off, driven by the collapse of 3AC and fears of cascading liquidations. Most have since recovered to near the peg. The current discount reflects the cost of holding LSDs, as they cannot be unstaked until the Ethereum Shanghai upgrade is completed.

Interestingly, cbETH trades at a much wider 5% discount, while rETH trades at a 1.7% premium compared to the other LSDs. The discount on cbETH could be due to CEX risks given recent events. However, if all other factors remain unchanged and you believe in Coinbase’s long-term solvency as a CEX, cbETH could be a cheaper alternative for exposure to staked ETH.

Although Rocket Pool has a widely distributed set of node operators, there is currently a lack of demand for them to run mini-pool nodes, with 5,000 ETH waiting in the deposit pool to be paired with mini-pool validators. As there aren’t enough mini-pool validators to take in the demand for deposits, this drives rETH to be trading at a 1.7% premium. Node operators can launch mini-pools to arbitrage the premium, but they must also stake a minimum of 10% of the value of the staked ETH in RPL, which impacts the profitability of this strategy. Node operators may view the arbitrage profits as a “discount” for the RPL staked.

The Future of ETH’s Liquid Staking Protocols

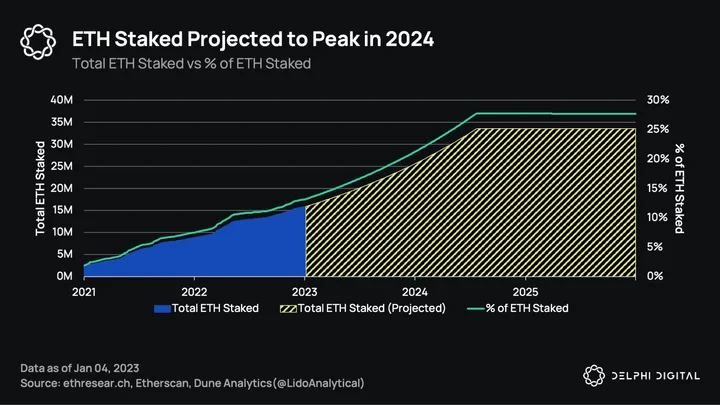

Before exploring projections, it is important to consider the potential state of ETH staking over the next three years. In 2019, Ethereum researcher Justin Drake mentioned that a target of approximately 33.5M ETH (about 27% of the total ETH supply) staked “feels about right for strong security.” A public Twitter poll in 2019 also indicated that most respondents believed that 30% of ETH would eventually be staked.

Using Justin Drake’s target for staked ETH, and considering the average daily ETH burned and projected daily ETH emissions, it is projected that approximately 33.5M ETH will be staked by April 2024.

There are, of course, concerns about the potential unstaking of ETH following the Shanghai upgrade. However, our model still projects growth in staked ETH for the following reasons:

- After the Shanghai upgrade, there will still be a queue for unstaking, and not all staked ETH will immediately become liquid. This reduces uncertainty for ETH holders considering staking because it resolves ongoing concerns about the duration of unstaking, which can lead to the mispricing of ETH LSDs.

- Once the duration of unstaking is established, ETH LSDs will be priced more accurately, as ETH redemptions enable true arbitrage. Any premium/discount will be arbitraged and converge towards the market pricing of near 1:1 with ETH.

- With more stable prices, liquidity will increase as more liquidity providers become comfortable with lower risks of a depeg.

- With higher liquidity, ETH holders will be more likely to stake, knowing they can sell their LSD back to ETH if they do not want to wait for unstaking.

- In addition, lending protocols will also start seeing ETH being borrowed for staking as arbitrageurs capture the difference between borrowing rates and staked ETH yields. This could drive more levered staked ETH positions to maximize yields and also bodes well for ETH lenders. We expect the divergence between ETH lending rates and staking rates to narrow.

Next, let’s examine how an increase in staked ETH impacts yields.

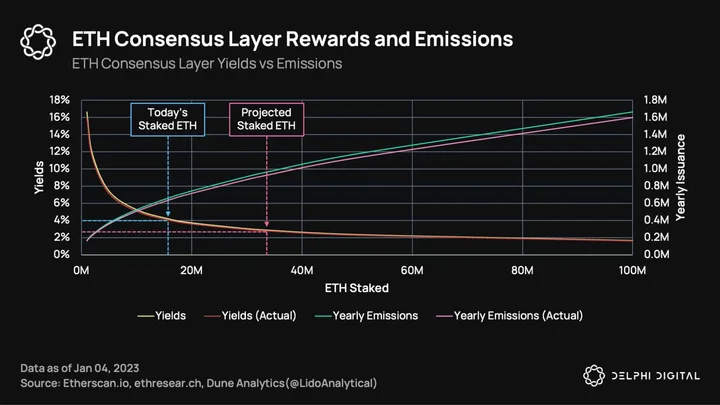

Rewards for staked ETH come from two sources — the consensus layer and the execution layer. Validators receive rewards from the consensus layer for proposing or validating blocks, attesting to their view of the chain, and participating in sync committees. The consensus-layer rewards are fixed, and emitted based on the amount of ETH staked. The following is the formula for calculating consensus layer rewards:

Yields = (c*F) / sqrt (Total Staked ETH)

Here’s what the variables are:

- c is the constant factor of ~2.6 based on the number of epochs in one year.

- F is the base reward factor set by the developers to 64, which determines emissions.

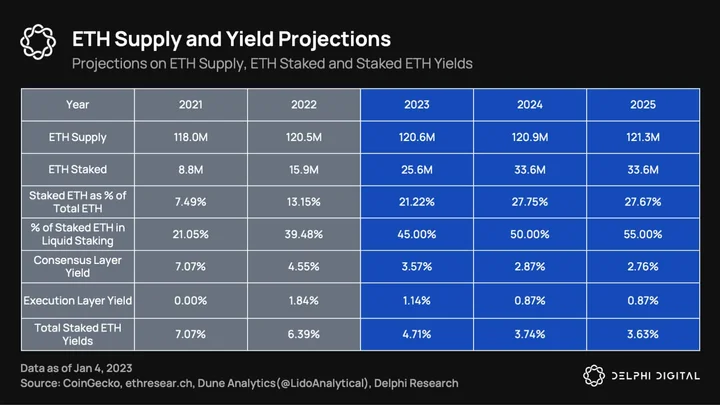

The graphic above illustrates that we are currently at approximately 15M staked ETH, resulting in validators being rewarded with a yield of around 4%. As the projected amount of staked ETH approaches ~33.5M, yields will gradually decrease to approximately 2.76%.

Using available data since the Merge, actual rewards have been slightly lower than stated, with the median and average c factors being 2.506 and 2.4997, respectively. As the average c factor has a smaller deviation from the actual issuance amount, the model will later utilize this value to calculate future yields.

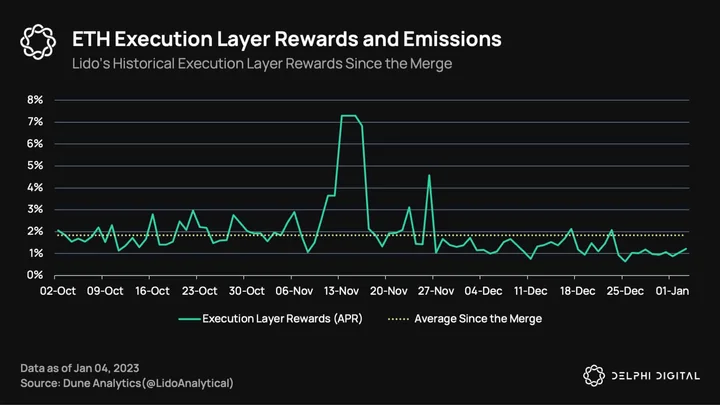

The rewards for the execution layer are variable and dependent on the level of activity on the blockchain. These rewards consist of MEV tips and transaction priority tips. In a bullish market, there are typically more transactions, which leads to higher levels of MEV and priority tips. Conversely, a bearish market results in lower levels of these rewards. Currently, daily rewards for the execution layer generally range between 1-2% APR, with an average of 1.84% APR since the Merge.

Projections on ETH and Liquid Staking Protocols

Using the above-mentioned data points, we formed a model of how ETH supply, LSD dominance, and staked ETH yields will look in the future. Let’s go through the key assumptions to understand the variables. You can view the full model used in this report here.

ETH Supply: This is the net supply change based on ETH issuance (which changes based on ETH staked as mentioned above) and the average daily ETH burned since the Merge.

ETH Staked: This is extrapolated using the average growth rate since the Merge.

Staked ETH as % of Total ETH: The projected % of ETH supply staked.

% of Staked ETH in Liquid Staking: This measures the total market share of LSDs, which have grown rapidly from 21% in 2021 to 39.5% in 2022. In our model, we took a conservative route of reducing the growth to ~5% annually.

Consensus-Layer Rewards: As mentioned above, yields decline as more ETH is staked.

Execution-Layer Rewards: The current conditions in ETH represent a conservative scenario in prolonged bearish/stagnant markets. The rewards here are calculated using the average daily execution-layer reward diluted by increasing ETH staked.

Total Staked ETH Rewards: Sum of consensus-layer rewards and execution-layer rewards.

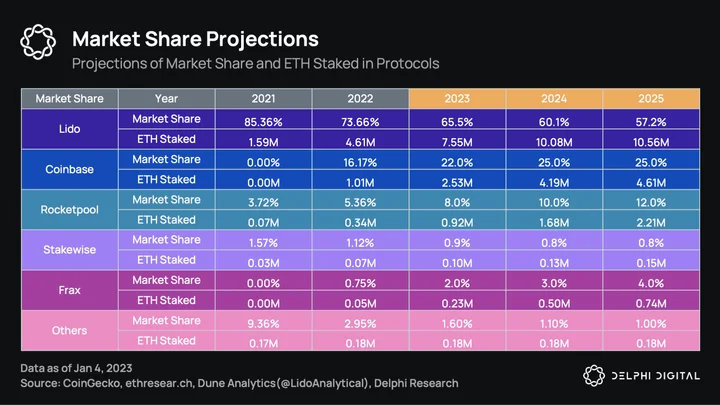

The model further breaks down the key ETH LSD protocols/companies. We predict that Lido will continue to grow, but as Coinbase and smaller protocols enter the market, they will gradually chip away at Lido’s total market share. Having said that, Lido is still likely to be the market leader when it comes to liquid staking. Coinbase’s growth is expected, as they have a strong user base from their exchange business. They have seen particularly strong growth, capturing a significant 16% market share shortly after launching in June 2022. Institutions, in particular, will likely find more solace staking with Coinbase as opposed to decentralized protocols, at least in the near future.

Rocket Pool is likely to continue growing as the second-leading ETH LSD protocol. It must continue attracting mini-pool stakers beyond its node operators to arbitrage the rETH premium.

StakeWise has struggled to increase its market share over the past year. Its slow growth will likely result in a decline in market share over time. This projection does not consider their upcoming v3 and osETH launch, as there is insufficient data to determine whether they will gain traction.

Frax’s frxETH has shown strong growth since its launch. Frax has sizable CVX voting power to incentivize deep liquidity and an AMO mechanism that helps maintain the frxETH peg, giving it an advantage over other LSD protocols. Furthermore, sfrxETH is one of, if not the, highest yielding ETH-staking derivative, which acts as a natural incentive for users to consider Frax.

Other protocols have not seen growth and are expected to remain stagnant, according to the projections.

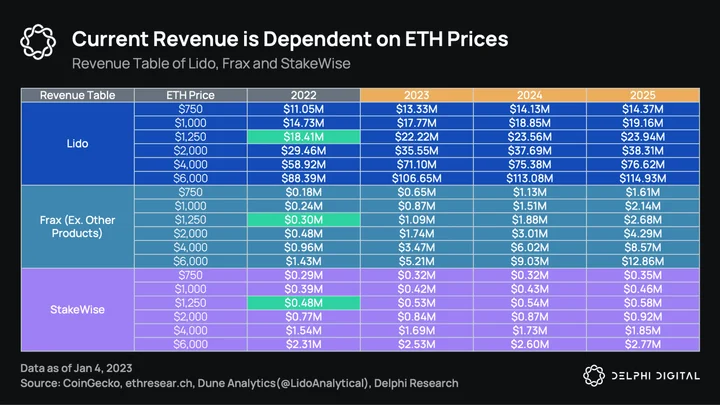

As Lido, StakeWise, and Frax are the three protocols that collect fees on rewards earned from deposited staked ETH to their DAOs, let’s examine their revenue and P/S multiples.

The protocols here earn fees on rewards that then accrue towards their DAOs. Here are the fees they charge:

- Lido: 5%

- Frax: 8%

- StakeWise: 10% if the node operators are StakeWise Labs and 5% if they’re not. This results in a weighted average of ~8.5% for StakeWise.

The table above shows the potential revenue for each protocol at various ETH price levels. The cells highlighted in green indicate the current revenue of each protocol based on their current ETH LSD market share. Our projections for 2023-2025 are based on the previous two models of staked ETH amount, the percentage of staked ETH in liquid staking, and the respective market share of each protocol. Multiple price levels have been included to illustrate the potential impact of different ETH price scenarios on the revenue of these protocols. Please note that these calculations are based solely on the protocols’ ETH liquid staking products and do not consider other offerings.

Currently, the annual run rates for Lido, Frax, and StakeWise are $18.41M, $0.3M, and $0.48M, respectively. As the revenue of LSDs is tied to ETH prices, fluctuations in prices can significantly affect these metrics, both positively and negatively.

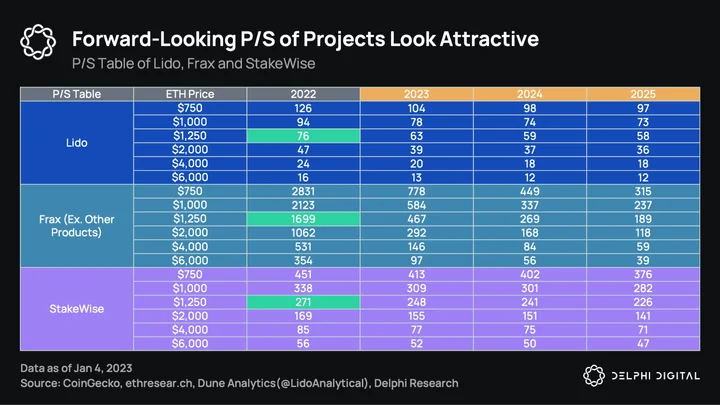

The table above displays the fully diluted price-to-sales (P/S) ratios of the protocols based on ETH prices. Despite having the largest fully diluted value (FDV), Lido’s strong market share position has made it a highly profitable business, resulting in the most attractive P/S multiple. At the time of our 2021 report on Lido, its P/S ratio was 610x, which has declined significantly to 76x over the past year.

Frax and StakeWise have larger P/S ratios even with lower FDVs, due to their smaller market share and corresponding lower revenue.

Conclusion

ETH staking derivatives are a simple business model that has generated millions in revenue for protocols like Lido. However, ETH LSDs are becoming increasingly competitive as Coinbase and new protocols like Frax eat into Lido’s market dominance. The total addressable market for ETH LSDs is definitely not fully tapped, with the amount of staked ETH projected to double over the next two years. Smaller liquid staking protocols could face problems due to liquidity issues that make it hard for stakers to exit pre-unstaking. Frax stands in a unique spot due to their CVX stronghold, which already makes frxETH the LSD with the second deepest liquidity.

Furthermore, there are still uncertainties surrounding execution-layer yields resulting from roll-ups. This can dampen MEV and transaction priority tips, which affects execution-layer yields and hence lowers revenue to liquid staking protocols.

As revenue is directly correlated with ETH prices, liquid staking protocols can be seen as a levered bet on ETH as they gain a stronger market share over staked ETH. The unstaking that is bound to happen should not be seen as a negative for ETH, but rather as a positive for liquid staking protocols, as it will reduce the uncertainty surrounding LSDs today.

The ETH liquid staking market continues to thrive in the midst of uncertainty. ETH liquid staking protocols are akin to a levered bet on the Ethereum network itself, and are likely to further cement their PMF over the coming years.

Special thanks to Abe Weiskorn for designing the cover image for this report and to Ashwath Balakrishnan and Brian McRae for editing.

0 Comments