The Future of On-Chain Liquidity

SEP 14, 2023 • 31 Min Read

Introduction

Despite the adoption of Automated Market Makers (AMMs) in the DeFi space, numerous problems persist. Liquidity providers(LPs) enter the market with the expectation of earning fees by effectively acting as the “house.” However, the inherent design of Constant Function AMMs (CFAMMs), combined with the passive nature of liquidity provision, leaves users vulnerable to Maximum Extractable Value (MEV) exploits and impermanent losses (or re-balancing induced losses).

The susceptibility of CFAMMs to MEV attacks is particularly pronounced, with Uniswap v2 being a notable target for MEV attacks. The static nature of liquidity within CFAMMs creates opportunities for MEV searchers to perform CEX-DEX arbitrages due to stale prices.

Furthermore, the prevalence of sandwich attacks is a concerning issue. These attacks involve MEV bots front-running and back-running user orders, capitalizing on the price slippage set by the user during the transaction. One infamous example, “jaredfromsubway.eth,” has managed to amass approximately 4.7K ETH in net profits through the execution of MEV attack strategies.

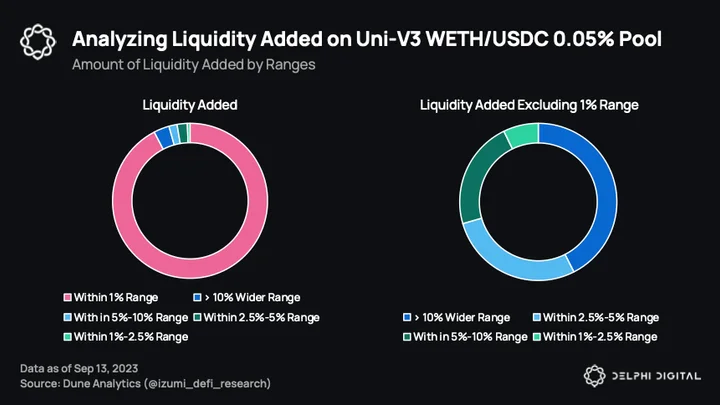

Delving into Uniswap v3 liquidity for WETH/USDC 0.05% fee pool, a distinct pattern emerges. The majority of liquidity providers prefer to operate within the 1% price range to optimize for fee. However, after removing most of the Just-in-Time (JIT) liquidity within the 1% range, a more equitable distribution of LPs becomes apparent. This underscores the substantial impact of JIT liquidity on LPs, as it selectively contributes liquidity when it is financially advantageous, thereby diluting the fees that passive LPs would have otherwise earned.

Consequently, LPs in Uniswap v3 navigate a nuanced risk landscape, encompassing not only the potential for leveraged impermanent loss (IL) but also the risk of fee loss due to the presence of JIT liquidity. These factors affect the value proposition to provide liquidity on Uniswap v3.

These issues make the current designs of AMMs tough to adopt and toxic. The sheer dominance of AMMs is a byproduct of it being the simplest DEX design to implement on a blockchain. It’s clear to us that the DEX market is in the midst of a “status-quo overhaul”.

In this report, we seek to highlight certain developments that we believe will stand out in the DEX market. Namely, how AMMs might evolve, new-age orderbooks, and DEX aggregation. They all tie into each other and will be vital to the future of on-chain liquidity.

Uniswap v4

Uniswap v4 was announced in May and was largely well received at first. The introduction of concentrated liquidity in Uniswap v3 was a 0 to 1 moment for AMMs, but the design proved difficult to build upon and was still prohibitively opinionated.

Uniswap v4 introduces hooks, which shift away from the rigid structure of v3 towards an extremely wide open v4. Uniswap v3 offers unprecedented gas efficiency due to the use of a Singleton contract, significantly simplifying the design under the hood. Transaction costs on Uniswap v4 are expected to be only slightly higher than an ERC-20 token transfer, which will have numerous downstream improvements for swappers and LPs alike.

The biggest new problem with Uniswap v4 will be routing. Routing is already difficult, with over 200k pools, three protocol versions, and 8+ blockchain deployments. The high degree of expressiveness allowed by hooks and the much easier developer experience are likely to compound this problem by an order of magnitude.

UniswapX and The Ensuing Routing Problem

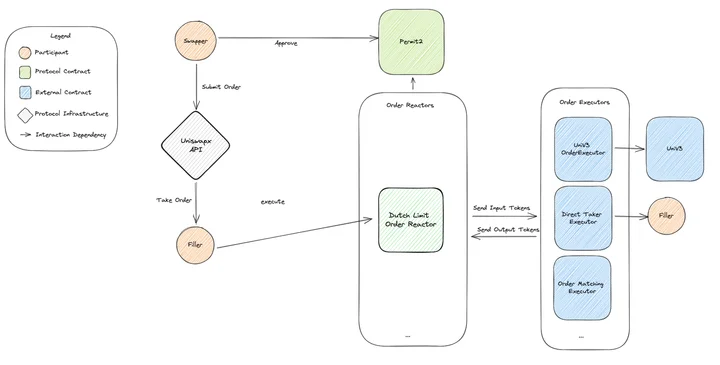

Routing on Uniswap v4 will be very difficult. To address this issue, Uniswap unveiled Uniswap X at EthCC.

While the gas savings and custom pools of Uniswap v4 will offer vast improvements to LPs, UniswapX is a routing protocol designed to take full advantage of v4s vast ecosystem of hooks and liquidity to offer CEX-level trade execution. Like Aori and Cowswap (later in this report), UniswapX utilizes an intent-based trading architecture, where off-chain fillers/solvers compete to settle taker volume.

UniswapX uses a form of Dutch auction it calls a Dutch order. The decaying nature of Dutch orders creates a competitive market among fillers to offer best execution for traders while keeping a small profit for themselves. Fillers are incentivized to fill an order as quickly as they can while still being profitable. If a filler is too greedy, they risk losing the order to another filler willing to take a smaller profit.

Liquidity to settle trades can be sourced from on-chain liquidity venues like Uniswap or other DEXs, off-chain liquidity, or from other UniswapX orders. Dutch auctions benefit from the same trading benefits as batch auctions.

-

Better prices by aggregating liquidity sources

-

Gas-free swapping

-

Protection against MEV

-

No cost for failed transactions

-

Gas-free cross-chain swaps

UniswapX includes an optional RFQ system on top. The RFQ system allows an order to specify a filler that receives the exclusive right to fill the order for a brief duration before the order is opened up for any filler to execute. These fillers can only win a quote if they guarantee improved trade execution over Uniswap v3 or v2 liquidity pools. During this period, other fillers can still ‘win’ the order by improving on the exclusive filler’s quote beyond a threshold. The exacts of said threshold are unknown as of now.

In theory, the RFQ system incentivizes fillers to offer their best price out of the gate in order to win the order, speeding up the entire process and imp

Read the full report

This report is part of Delphi Pro.

- 800+ Pro reports across every major sector

- Talk directly with our analysts

- Private community of funds and builders

Already a Pro member? Log in

0 Comments