The Great cvxCRV Lockening, DeGods NFT Collection, DeFi Option Vaults

JUL 07, 2022 • 9 Min Read

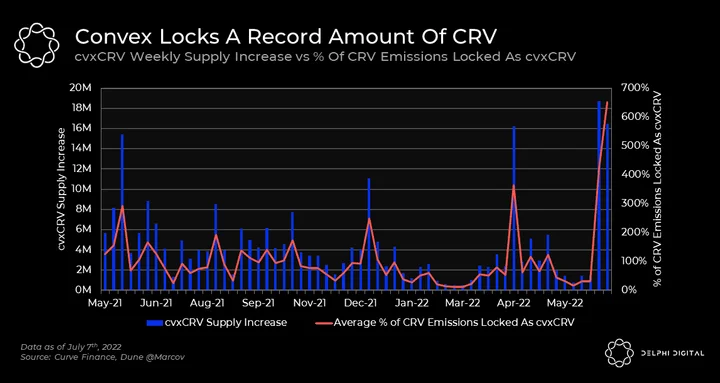

Chart of The Day: The Great cvxCRV Lockening

- Convex Finance has experienced a record-breaking period which is being dubbed the “Great Lockening.” The protocol received its largest supply increase of cvxCRV within any two-week period since its inception. Since June 27th, a whopping 35M CRV has been locked, taking the total supply of cvxCRV up to ~274M.

- This massive increase in cvxCRV supply was primarily driven by the recent proposals by Frax and Convex. Previously all the CRV farmed by Frax was being sold. Now, Frax has been admitted to the veCRV whitelist and will adhere to the following conditions:

- Lock at least 5% of CRV farmed as veCRV

- Use the remaining CRV to support the cvxCRV peg or convert it directly into cvxCRV

- Since Frax is the largest stablecoin player in the Curve ecosystem and also a massive holder of CVX, this proposal’s importance cannot be understated. Having Frax help maintain the cvxCRV peg is a huge advantage to Convex and the Curve ecosystem.

- Currently, cvxCRV is absorbing significantly more supply than is being emitted to Curve pools through gauge emissions. The percentage shown in the chart above being greater than 100% indicates that either old CRV, or CRV supply from investor and team tranches is also being locked into cvxCRV.

- The massive increase in cvxCRV supply equates to more gauge power controlled by each CVX, thus allowing Convex to direct a larger share of Curve’s future emissions. Each locked CVX now controls over 5.4 max locked veCRV, a ratio not seen since March 3rd, 2022.

- For more on Convex, you can see a previous Delphi Pro Report here.

ENS, Nina’s Super Cool World & DeGods

[Excerpt from a Delphi Insights Report]

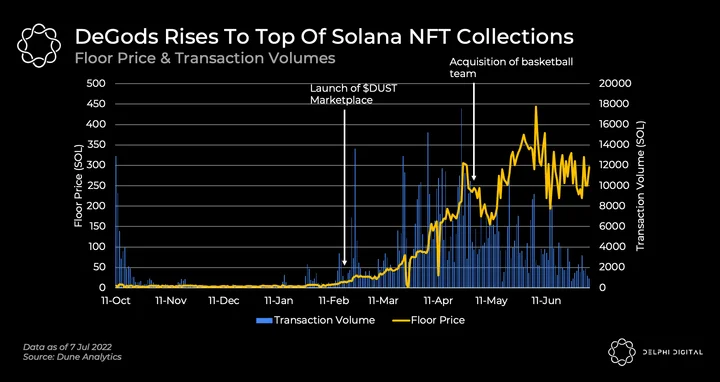

- I’ve been watching the Solana NFT ecosystem for a while now, and it has taken on a life of its own. What fascinates me is that there are a few SOL collections that have been able to maintain floor prices of 150 SOL or more (equivalent of 5+ ETH today) despite the downturn in the markets:

- DeGods (~300 SOL)

- Solana Monkey Business (~200 SOL)

- Taiyo Robotics (~150 SOL)

- Clearly, these projects have been able to build up strong communities and continue to do interesting things to sustain holder attention. Let’s dive into DeGods, the top-performing NFT collection on Solana.

- Introduction: DeGods is self-described as a “deflationary collection of degenerates, punks, and misfits. Gods of the metaverse & masters of our universe,” and it launched in October 2021. Since then, the team has found ways to growth hack their way to the top, which can provide valuable lessons for other NFT projects.

- The concept of staking NFTs to earn fungible tokens is not new, yet many projects have done this only to generate useless & valueless tokens. DeGods implemented $DUST, the utility token within the DeGod ecosystem, which still holds value today (0.035 SOL /$DUST, or approximately $1.40). $DUST can only be earned by staking: DeGods can be staked to earn $DUST (10/day per DeGod). 1000 $DUST is required to mutate a DeGod into a DeadGod, which can be staked to earn 30 $ DUST/day per DeadGod. 97% of DeGods have already been mutated into DeadGods and approximately 96% of NFTs are staked.

- $DUST can be utilized to purchase raffle tickets for allowlists and bid on 1/1 auction items on their private marketplace.

- DeGods acquired the Killer 3s, a professional American 3-on-3 basketball team that plays in BIG3 (a league whose teams feature former NBA players and international players). Ownership includes IP & commercial rights, streaming rights, DeGods brand placements, and directing high-level team strategy. BIG3 season playoffs pull in ~500,000 TV views every weekend.

- The typical owner of a DeGod is a Solana NFT degen. Based on the art and branding thus far, it has a grungy, anti-establishment type of vibe that bears some similarities to skate culture and would appeal to that type of niche audience rather than a mainstream brand.

- The long thesis for DeGods stems from 2 main things:

- That the Solana & the Solana NFT ecosystem will flourish and grow. Current data (e.g. developer growth, transaction volumes) supports this. SOL is down 85% from its ATH price today and has a lot of room to grow over the long term.

- The belief that DeGods will continue to remain the leading NFT collection on Solana. This is much more difficult to predict.

- If we take floor price as a proxy for demand and execution capabilities, DeGods is the current king of Solana NFT collections. The next nearest collection is Solana Monkey Business, sitting at just under 200 SOL floor.

- The typical owner of a DeGod is a Solana NFT degen. Based on the art and branding thus far, it has a grungy, anti-establishment type of vibe that bears some similarities to skate culture and would appeal to that type of niche audience rather than a mainstream brand.

- The purchase of a basketball team shows that the team can make bold decisions and explore untested waters. It is an attempt to bridge the project beyond the crypto community. How many NFT projects can say they own something as real as a sports team? Very few. Yet, after the attention dies off (e.g. when the current season ends), it remains to be seen if the team has the expertise to properly run a professional basketball team and grow the value of its investment.

- For more information, Delphi members can see the full Delphi Insights Report here.

The Inner Workings of DeFi Option Vaults (DOVs)

[Excerpt from a Delphi Pro Report]

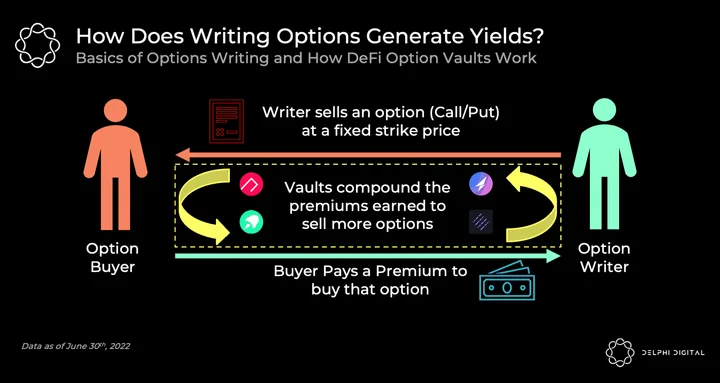

- Decentralized Option Vaults (DOVs) are a relatively new product in the world of DeFi. These vaults offer users the potential to earn yield in a way that differs from the standard token emissions on liquidity mining that we typically see. In essence, DOVs help users sell options in an automated fashion, allowing them to *potentially* earn a real return via the premiums.

- The basic concept behind DOVs is nothing new to the world of finance. In TradFi, these are called “structured products”, and they’re essentially a method of asset management that involves combining several instruments into a single financial product, thus creating new payoff curves.

- The core use case of DOVs is automating the process of writing options on behalf of depositors. DOVs mainly have two strategies – 1) writing Covered Calls and 2) Cash-Secured Puts. To put it simply, it’s just selling options and earning the premiums paid by buyers (i.e., selling real risk).

- For covered calls, depositors own risk assets like ETH, SOL, AVAX, AAVE, and others. For cash-secured puts, users are required to deposit stablecoins. A covered call is a strategy where one is long a spot asset and sells out-of-the-money calls against it to generate cash flow. On the other hand, a cash-secured put is a strategy where one holds stablecoin/cash and sells out-of-the-money puts against it.

- DOVs sell out-of-the-money options as the goal is to minimize the risk of the option expiring in-the-money. If the options expire without any worth, depositors keep the premiums earned (to their benefit). This strategy utilizes the short time frame to earn premiums from theta decay – the phenomenon of an option losing value over time.

- These protocols help depositors sell options to market makers through an auction process that determines the price. Once the options are sold, the premiums gained are then redeposited back into the vault and compounded to sell more options in the next cycle. The options sold by DOVs usually expire weekly (every Friday), with some protocols offering bi-weekly and monthly expiries.

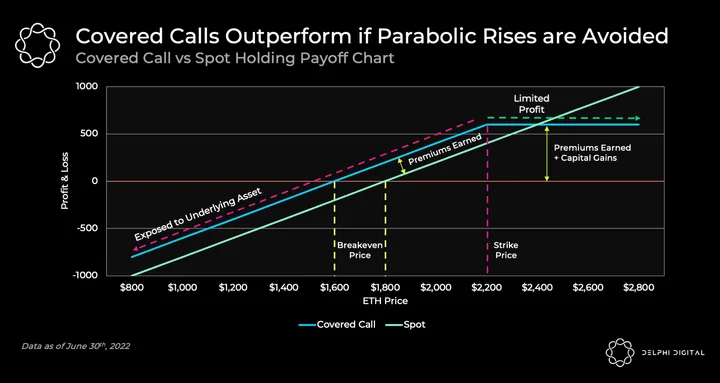

- Note: The chart above is only for illustrative purposes. The numbers are not representative of the actual potential PnL that could happen.

- Recall that writing a covered call is a two-part strategy: a long on a spot asset (e.g. holding ETH) and selling call options (e.g. writing an ETH call) of the same asset to earn premiums from option buyers. Covered calls are partially hedged when the calls go in-the-money, as the long spot position continues benefiting from higher prices while the short call position loses more value as prices go up.

- Looking at the payoff graphic above, selling covered calls always gives you higher returns than holding spot if the option doesn’t go above strike price, (i.e. as long as it doesn’t expire in-the-money). But this is a highly idealistic scenario, as no strategy can have a 100% hit rate.

- These are the risks you undertake when writing covered calls:

- To be collateralized for writing a covered call, you will need to own the underlying asset. Therefore, the option writer is exposed to the underlying asset’s price movement. Generally, these vaults are geared towards people who already own the underlying asset.

- If the underlying asset rises in price at a parabolic rate and goes in-the-money, option holders will exercise the call option to buy the asset at expiry. As an option writer, you are essentially setting a limit sell order at the assigned strike price, reducing your profitability in such a scenario.

- The maximum loss for a covered call writer is calculated as the price paid for underlying asset minus premiums received.

- For more information, Delphi members can see the full Delphi Pro Report here.

Notable Tweets

How a Fake Job Offer Led to $540 Million in Stolen Funds

Scoop! How a fake job offer took down the world’s most popular crypto game

— Ryan Weeks (@RyanJamesWeeks) July 6, 2022

Nexo In Talks to Acquire Vauld

In a consolidation effort aimed at the betterment of the space, as well as the strengthening of our presence in Southeast Asia, we’ve entered exclusive talks with @VauldOfficial for the full acquisition of the Singapore-based company.

— Nexo (@Nexo) July 5, 2022

Ethereum Completes Second Successful Test of the Merge

Sepolia Testnet the second of three testnet merge successfully happened today.

The next one is Gorli in a few weeks, then Mining will be gone for good on Ethereum with activation on Mainnet.

— Marc “Aavechan.lens” Zeller 👻 💜 (@lemiscateNEXO) July 6, 2022

0 Comments