Note: If you’re interested in reading individual sector reports, please follow the respective links below. If you’d prefer to listen to audio versions of the reports, you may use the Listen button just above the Table of Contents on the left. The sector Year Ahead reports were originally published between December 05 – 21, 2022.

The Year Ahead for Infrastructure

Introduction: The Great Reset

This introduction was written by Co-Founder Kevin Kelly to share a few personal thoughts to prelude the full Year Ahead report. Navigate to any sector report using the Table of Contents above.

We titled this year’s report The Great Reset because we believe that’s what 2022 represented for crypto — a great reset in prices, expectations, and speculative interest all across the industry. Every major tailwind that propelled the crypto market higher from Q2 2020-Q4 2021 turned against it, resulting in one of the sharpest and quickest price drawdowns we’ve seen to date.

Bull markets are where most investors make their money, and bear markets are where you fight to preserve those gains. But long drawdowns have a silver lining in that they encourage deeper reflection, giving all of us a chance to re-evaluate what really matters and where we really want to spend our time.

‘Tis the season where everyone predicts what next year — and the years to come — will bring. For me, I spent the majority of my holiday brainpower thinking about the big picture: 1) because I’m a macro guy at heart, so I can’t help but think big picture, and 2) because I believe we could be on the cusp of a serious inflection point, one that could accelerate the trajectory of this industry and shorten the timeline for Web3 to really move the needle beyond today’s small (yet enthusiastic) user base.

Crypto has largely been a speculator’s market, and that’s still true today. But speculation isn’t inherently evil. The term “speculation” tends to carry a negative connotation. But, like most things, it sits on a spectrum. Hype and excitement drive interest, which attracts capital, which gives entrepreneurs the resources to build innovative products leveraging new technologies. Without speculation, capital wouldn’t flow to such risky ventures (and society would still be stuck in the Stone Age). In fact, I’d argue speculation is more than beneficial — it’s imperative at this stage.

The truth is there aren’t many people who are really driven to build boring products with boring use cases that offer boring returns. We need the visionaries, the hungry entrepreneurs who see the sky as their north star, not their limit. The ones who breathe life into those around them, creating waves of excitement with ripple effects that extend far beyond their own reach.

Now, not all entrepreneurs are created equal — this year we saw firsthand how an entire industry can fall victim to a select few who let ego or profits get in the way of progress and purpose. But history is littered with examples of hubris (and even outright fraud). Innovation attracts a wide array of actors — some good, some bad, some in between.

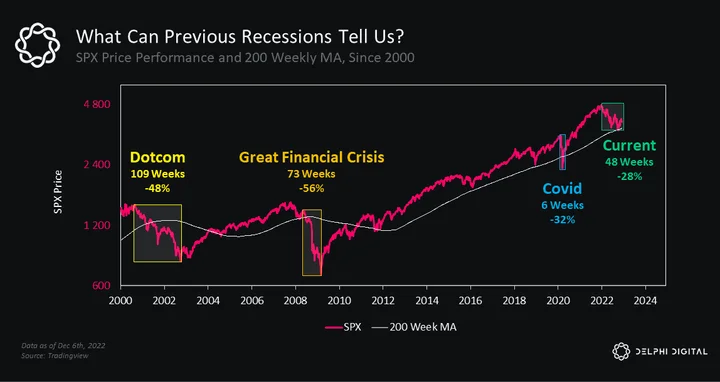

All innovation cycles start off being extremely speculative. The dotcom frenzy of the late 90s culminated in one of the most infamous market bubbles of the last century. Inflated expectations stoked higher valuations, and when market conditions turned, these 90s high-flyers were hit the hardest. Like all hype cycles, speculation got ahead of reality, and fundamentals needed time to catch up.

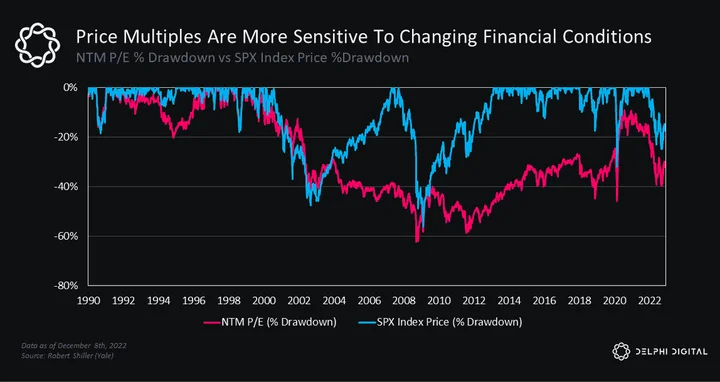

Fast forward twenty years and the tech sector is now home to many of the largest and most profitable companies in the world. But today’s corporate behemoths weren’t overnight successes. At the height of the dotcom era, Amazon’s market cap was north of $34B before it surpassed $1B in annual revenue. AMZN subsequently suffered a 94% drawdown in the depths of the dotcom crash, even as its revenue growth and market share expanded. Price multiple compression was the primary driver of the equity market’s initial decline in 2000, similar to what we just witnessed in 2022.

Crypto is facing a similar challenge, and it would be naïve to say the crypto market’s rapid valuation expansion over the last several years was driven by pure fundamentals over speculation. The question now is whether crypto is in an analogous period of dejection akin to the post-tech bubble, or if this is all just smoke and mirrors without any underlying substance.

Crypto Innovation Cycles

The crypto industry itself has gone through multiple hype cycles, each fueled by speculation on the back of new innovation triggers.

Bitcoin experienced a short-lived spike in 2013, but its true mainstream hype cycle happened in 2017. The “digital gold” narrative gained traction, as macro conditions were ripe for a new type of digitally-scarce speculative asset to thrive. Risk was in vogue, financial conditions were easing, the dollar dropped >10%, and equity volatility hit a multi-decade low as stocks kept marching higher.

The launch of the first smart contract protocol — Ethereum — drastically simplified the process for creating new crypto assets (via its standardized ERC-20 contract), laying the foundation for the ICO craze of 2017 (which also benefited from the same favorable macro backdrop).

The launch of more sophisticated DeFi protocols like Uniswap, Aave, Compound, and Synthetix made trading, lending, and borrowing crypto assets much easier than archaic alternatives, and the advent of liquidity mining (and the copycat projects that spawned from its early success) paved the way for “DeFi Summer” in 2020.

Gaming and NFTs caught fire in 2021 as attention shifted to more mainstream and consumer-friendly use cases beyond DeFi speculation. Game developers and creators alike leveraged fungible and non-fungible tokens to build new ecosystems and engagement models (some even used a combination of both). The hype behind this new wave of assets and use cases — again coupled with extremely favorable macro tailwinds — pushed crypto markets to new heights once again.

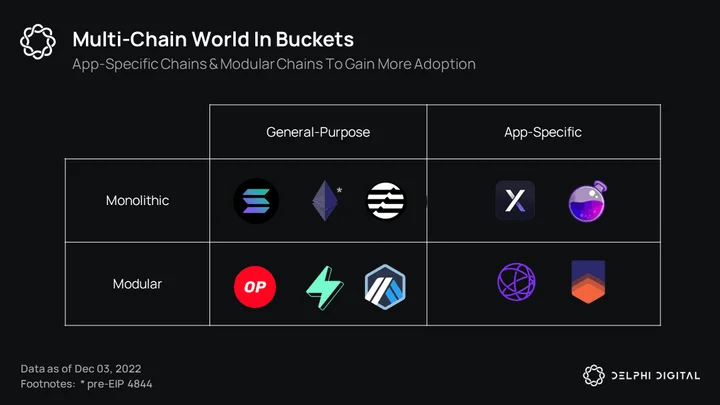

Additionally, this surge in transaction activity led to spikes in transaction costs, which accelerated the “L1 wars” narrative and sparked critical debates around the optimal blockchain architectures for different application types (you’ll find plenty of in-depth commentary on the tradeoffs between modular vs. monolithic chains in this report too, don’t worry).

The point is, each of these hype cycles brought more attention, users, and capital to the crypto ecosystem and built upon the advances made by those prior, expanding the capabilities of what’s possible with crypto/Web3 technologies.

We needed all of these innovations for different reasons. We needed highly secure protocols to facilitate open, permissionless transactions on a global scale. We needed standardization to optimize the creation of — and interaction between — digital assets that operate on top of these protocols. We needed decentralized financial applications to create more efficient, liquid markets for acquiring, selling, lending, and borrowing these new asset types. We needed non-fungible token standards to introduce more uniqueness, specificity, and customization to digital assets. And we needed to show that the design space of applicable use cases goes way beyond just trading DeFi tokens on DeFi rails with other DeFi traders.

There’s a lot we still need, too. We need more mature derivatives markets for hedging and risk management. We need standards around decentralized identity to unlock new primitives like unsecured lending and credible reputation systems. We need more UX improvements and abstraction (where appropriate). We need more regulatory clarity. We need…a lot of things.

But I believe we’re finally at a point where there are enough puzzle pieces — that can be reconfigured in enough ways to meet a wider spectrum of needs and use cases — to put us on the cusp of another, even bigger, creative explosion. One that will once again redefine what’s possible (and bring back some speculation to a market that, frankly, could use it).

We’ve all heard the rallying cry of the crypto faithful that “bear markets are where you build.” This mantra has a lot of merit — many of today’s prominent protocols and applications were built in the depths of prior downturns. In the early stages of any emergent technology, a lot of attention has to be focused on the technical aspects of what’s being built. Without that upfront investment, nothing else that could come after matters.

But building is only one side of the equation. Demand is what’s needed to maximize the value of all the sweat equity that goes into bear market building. Demand leads to more usage, which leads to faster feedback cycles, which leads to better products, which leads to more demand and more usage. And the reality is, we’re facing a demand shortage right now.

If we really want to shift the Web3 demand curve, we need to think about ways to meet the world where it is today and bring it along this journey with us. In order for us to get to this phase, we need more examples of how this technology can benefit more people beyond just leveraged speculation. Web3 products need to provide valuable utility in order for people to understand the potential applications that are possible in this new world.

That’s one reason why I’m so bullish on the long-term prospect of NFTs. Their relatability makes them uniquely positioned to attract a broader audience, which will bring in new sources of demand and buying power. The creation of new asset types will also benefit the entire crypto economy by increasing the total surface area for new participants to interact with digital assets (which I believe will be the gateway for the next wave of Web3 enthusiasts).

If we want to show the world the power of what’s being built here, we need to give the world more reasons to care. That means creating more products that more people want to engage with and getting those products in front of the very people who are most likely to find value in using them. That’s how we move the needle, at least in my view, because changing consumer behavior is a tall task without relevant and rewarding experiences to catalyze it.

That’s enough from me, now onto the good stuff. This Year Ahead report is broken down by sector and focuses on the major trends and themes our team is tracking heading into 2023.

DeFi Year Ahead

By Ashwath Balakrishnan and Jordan Yeakley, CFA

The State of DeFi and Where It’s Going

DeFi was the golden child of 2020, acting as the first true narrative of the last market cycle. Its initiation into the crypto mainstream has now endearingly gone down in history as “DeFi Summer.” Any of you who were involved in crypto at the time probably remember the sleepless nights as project after project launched to guaranteed short-term success. Yet, 99%+ of those projects probably never made it to the end of the year — or even the end of the month.

While we’ve seen groundbreaking innovations, there have been even more thoughtless clones in DeFi. The root of the issue sits between the rise of actors focused on short-term profits and the problems of user acquisition/onboarding. This is the double-edged sword of permissionless innovation.

In this report, we look to highlight some key opportunities and challenges for DeFi and spell out the reasons we remain optimistic that DeFi will thrive. But before that, let’s take a look at how the industry has fared.

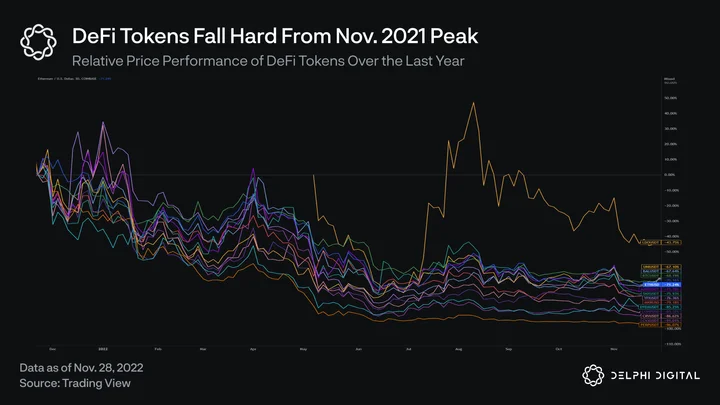

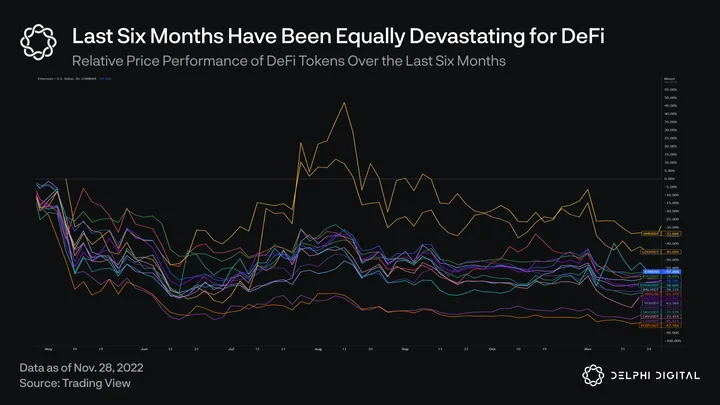

Broadly speaking, DeFi tokens have had a tumultuous year. Ethereum DeFi, which is the largest DeFi ecosystem, saw some of its highest-rated coins take a beating.

The past six months saw crypto as a whole get shaken up, with several key players taking large losses or blowing up entirely. Despite DeFi’s mechanisms protecting users from this fallout, DeFi tokens didn’t manage to scrape through unscathed.

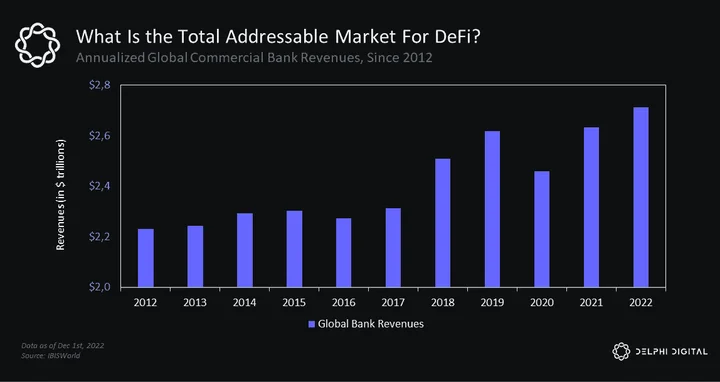

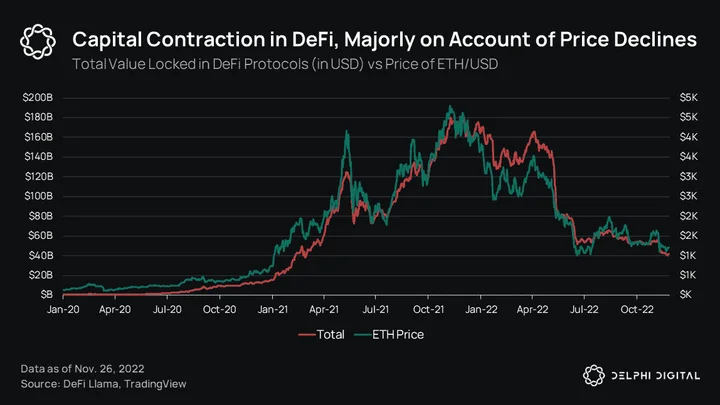

While TVL has fallen almost 75% from its peak, DeFi still accounts for a large portion of capital in on-chain products. Compared to the broader finance industry, DeFi is still a drop in the pond. The highest traction products are DEXs and money markets.

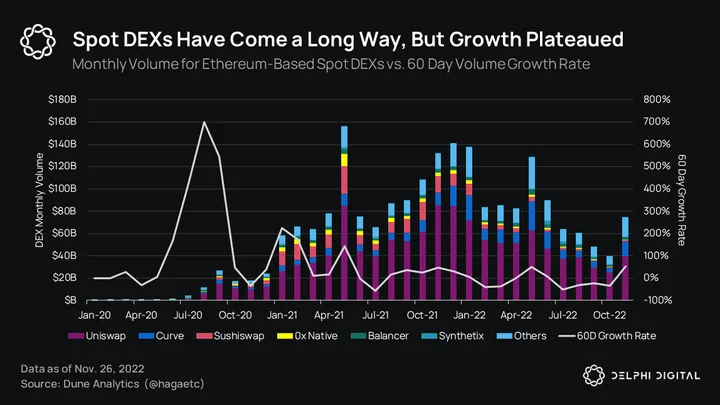

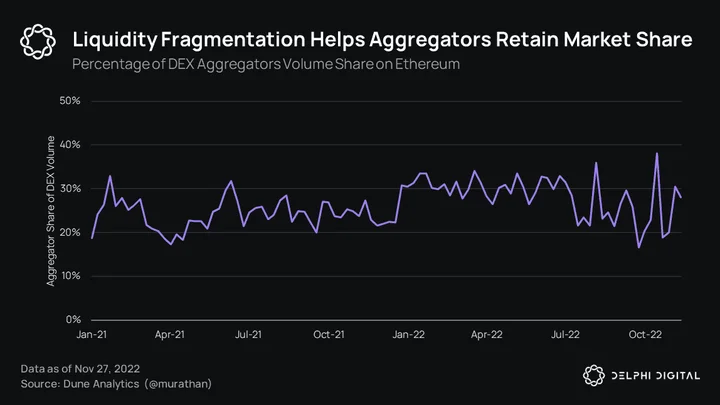

DEX volumes were on a tear in 2021. So much so that, just by looking at the above chart, you can hardly decipher how much monthly volume Ethereum DEXs did in early 2020. May 2021 was the absolute peak, followed by a temporary rise in Q4 2021. The compounded annual growth rate (CAGR) of Ethereum DEX volume from January 2020 to November 2022 is 402.4%.

Skipping to the present, we’ve had five straight months of declining DEX volume leading up to November 2022. But the hidden silver lining is that despite this massive fall from grace, DEXs on Ethereum still did about $30-40B in monthly volume — no small feat.

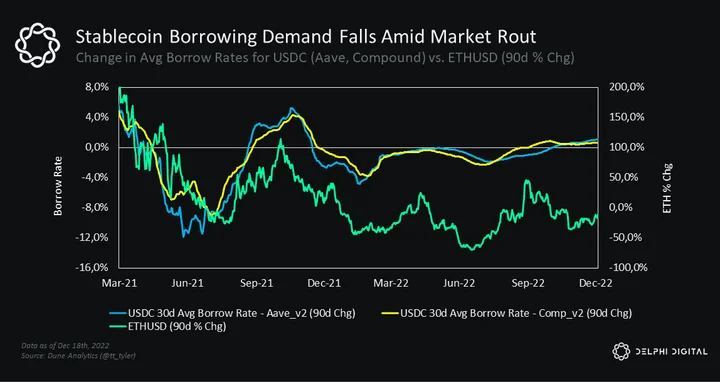

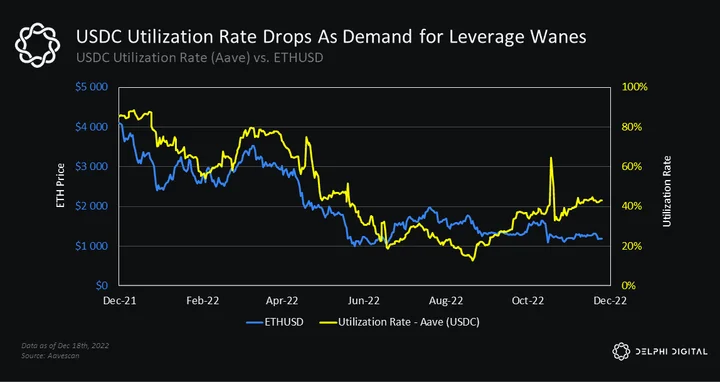

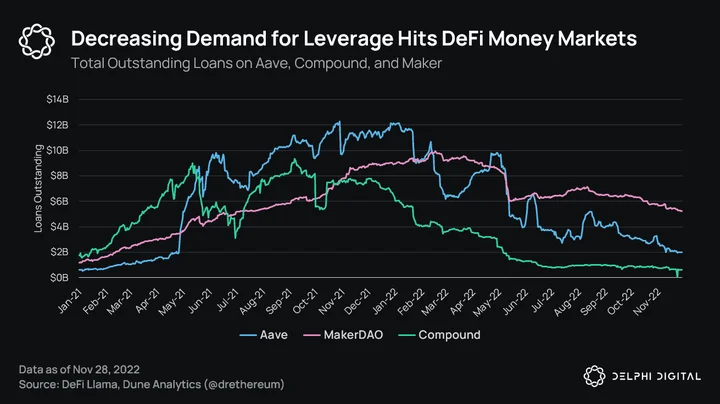

Aave, Compound, and Maker have seen incredible growth over the past three years. And yes, demand for leverage has tapered off significantly — an expected byproduct of a brutal market downturn. People just aren’t in the market for fresh DAI or obtaining leverage to yield farm and margin-long assets. But let’s not discount just how far these protocols and DeFi have come.

A concept that was once laughed at is now the reason for the lion’s share of crypto’s flows. But it’s not as though everything is rosy and perfect. DeFi has its problems.

The primary obstacles can be briefly boiled down to:

-

All DeFi products with traction are speculation-based primitives (we’ll explain why this is a necessary first step later).

-

Onboarding new users is a cumbersome process, requiring deep education.

-

Retaining users sustainably is a challenge in itself (as is the case with all new products/applications).

-

The overall UX of the space is far from ideal.

The evolution of DeFi is not something that’s going to happen over the next few months. It will be a multi-year process of painstaking innovation and building. But the end goal is arguably as righteous as they come: self-sovereign control of one’s assets/finances and the ability to scale finance into a transparent, borderless system – a system that actually seeks to enrich its users.

It’s easier than ever to be a DeFi pessimist. And if you fall into this camp, we hope to show you the other side of the coin (pun intended). In this report, we’ll highlight some key themes we believe will prove vital to the space over the next year or so — many of which are rooted in the current state of DeFi.

Pushing DeFi Forward: Themes for the Future

Theme #1: Tailwinds for DEXs — A Loss of Trust in Centralized Platforms

An overarching theme of this report revolves around users losing trust in centralized platforms — specifically with respect to crypto markets.

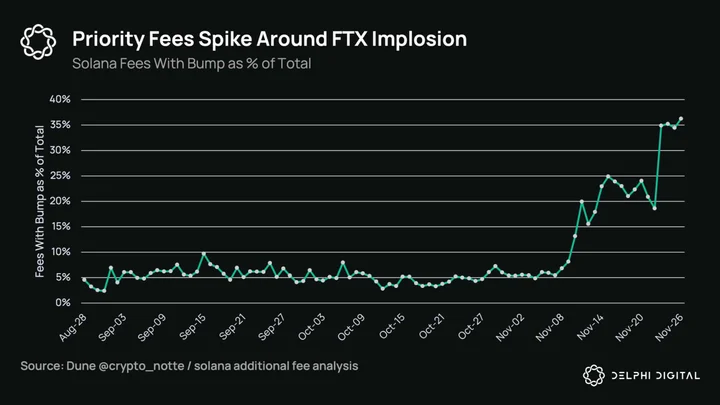

The collapse of FTX posed a systemic risk to crypto markets, and the exchange’s demise brought down a number of big players in the industry. We will continue to feel the wreckage from this event for months and years to come. But there’s a fairly obvious silver lining for decentralized counterparts.

Hayden from Uniswap cannot touch user funds sitting in Uniswap pools to buy the naming rights for an NBA team or to sponsor major sporting tournaments. Antonio from dYdX cannot touch user collateral in the platform to give his hypothetical investment fund a large loan. In short, the principles and structures of DeFi platforms do not give way to the same centralization and risks that led to the downfall of FTX, i.e., one or a few people with totalitarian control. As time goes on and the wounds from FTX heal, we believe more and more people will start to see this as well.

The underlying transparency provided by public ledger blockchains makes DeFi protocols auditable in real-time, and there are several potential paths DEXs can take over the coming years.

DEXs like Uniswap, 0x, Curve, dYdX, and GMX have stood tall in light of recent events. Seeing more crypto native participants move from centralized exchanges to self-custody could entail higher volumes on DEXs going forward. In all honesty, DEXs being a saving grace is a fairly obvious takeaway. But given the massive difference in UX between CEXs and DEXs today, it’s unlikely we will see this materialize in a big way anytime soon unless that gap narrows considerably.

There are some larger implications for DEXs on the path forward from here, specifically for how volumes shift from CEXs to DEXs. How do DEXs best position their exchange designs to capitalize on the current situation?

Take, for example, the plight of professional market makers right now. An exchange they (and everyone else) believed to be healthy and solvent ended up collapsing while many of these entities still had funds in their accounts. If FTX was doing shady things behind the scenes, the next natural question is which other exchanges are doing something similar? Perhaps market makers will now see how DEXs are the path forward for price discovery and trading in crypto.

The flipside is that these protocols are only as strong as their weakest line of code, and they run the risk of being hacked.

That aside, what is the best way to attract market makers to your DEX, assuming they start to allocate more capital toward providing liquidity on DEXs?

The most obvious answer seems to be orderbook-based DEXs like 0x, dYdX, Injective, Sei, and Zeta (among many others). Market makers are intimately familiar with orderbooks and would be more comfortable with the flexible nature of being an LP on these DEXs versus AMMs with pre-determined pricing curves.

Will a meaningful exodus of market making capital from CEXs prove to be a valuable opportunity for orderbook DEXs? Perhaps.

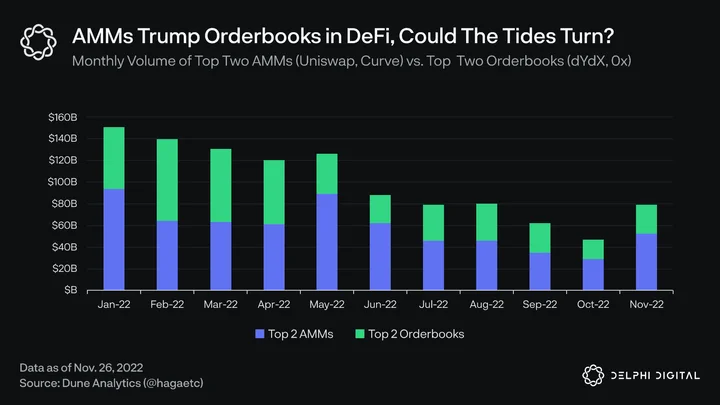

Right now, AMMs are the clear winner in the battle for DEX supremacy. And the chart above doesn’t even consider numerous other AMMs like SushiSwap, DODO, Osmosis, and Balancer that have significant liquidity and facilitate billions of dollars in cumulative volume.

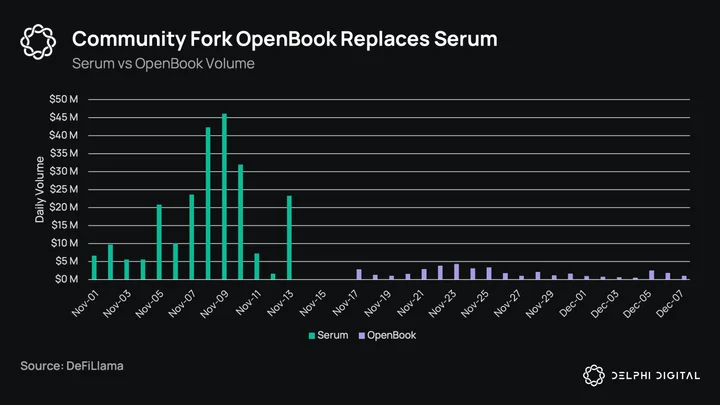

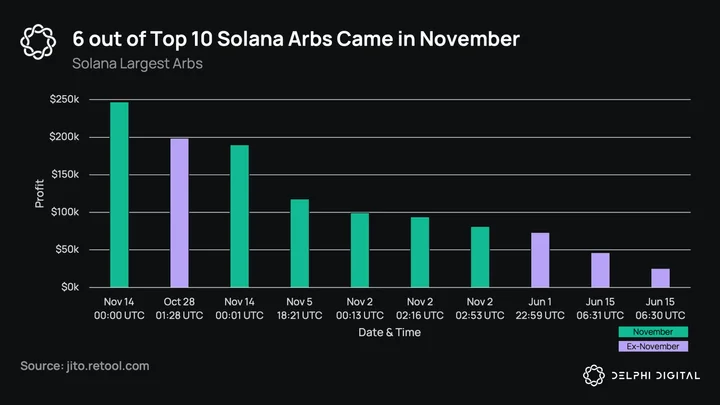

On the other hand, barring 0x and dYdX, there aren’t too many active orderbooks doing equally well. Injective and Sei (Cosmos chains) are beginning efforts to kick off volume, while Serum has all but withered away thanks to FTX. However, there is considerable hope in the Solana ecosystem over Openbook — a community-led fork of Serum.

Keep in mind, neither 0x nor dYdX run fully on-chain stacks. 0x relies on a number of market makers hosting their own orderbooks, while dYdX currently uses a centralized orderbook and matching engine.

Even just pitting two of the top AMMs against some of the only healthy orderbook DEXs shows us that AMMs have continued to gain more traction. Perhaps AMMs will continue their run of dominance and find ways to optimize for better liquidity provision.

Given the amount of volume on Uniswap v3, and the ability for LPs to configure how they deploy their liquidity thanks to concentrated liquidity, maybe more professional market makers will take the time to understand how all of this works and devote more resources to Uniswap.

It’s difficult to estimate the exact direction DEXs move in, but there’s a sizable opportunity for them to capitalize on the current situation.

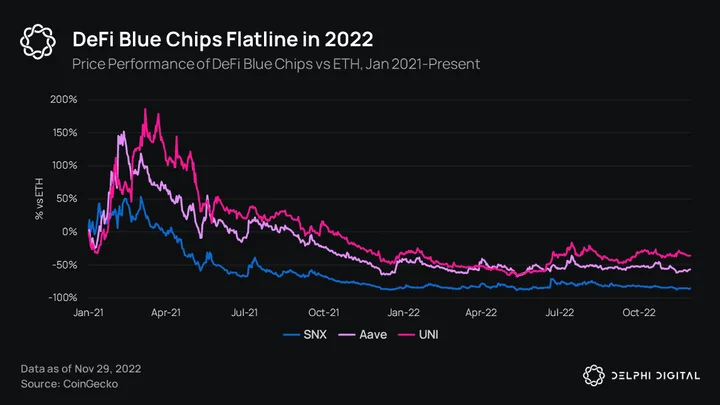

Theme #2: DeFi Blue Chips Rise From the Ashes

2022 was a brutal year for DeFi blue chips, but these projects still dominate their respective sectors. Since value will likely gravitate to the application layer over time, it seems worthwhile to explore the blue chip rebound thesis. If and when fundamentals start to actually matter, this theme will be even more salient.

Uniswap

Despite Uniswap’s tight grip on the DEX market, momentum from v3 has dried up completely. Hesitance in activating the fee switch and a cabal-like governance structure have brought the token’s utility into question. UNI has steadily declined with a lack of new tailwinds.

Uniswap has an experimental fee switch proposal currently making its way through governance. This proposal only impacts three pools and will not distribute fees to UNI holders at this time. The fee switch will likely be a lingering debate throughout 2023, but remains far off as an avenue for UNI value accrual.

Uniswap’s recent launch of its NFT marketplace aggregator marked the beginning of Uniswap’s horizontal expansion into NFTs. Such expansion could provide the UNI token with tangible utility while avoiding the slippery slope of the fee switch. Alternatively, Uniswap could grow vertically, acquiring wallet apps and building infrastructure to directly onboard users.

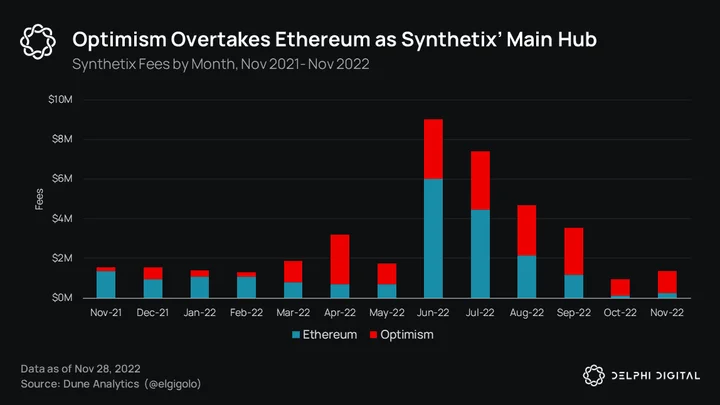

Synthetix

At a glance, Synthetix may have the most romantic use case of any OG DeFi dApp. The promise of a full-stack, permissionless derivatives platform that democratizes access to the $630T derivatives market propelled SNX to a $4B market cap in early 2021. Progress has since slowed and expectations have waned, but Synthetix has quietly been fostering a healthy ecosystem on Optimism.

The Synthetix ecosystem was a first mover for sustainable governance, liquidity mining, synthetic assets, hedged AMMs, cross-asset atomic swaps, and more. The imminent Synthetix v3 will feature a complete redesign of the protocol that will allow Synthetix to continue its leadership as a test-in-prod environment for novel DeFi concepts.

As the sole form of collateral and recipient of platform fees, SNX features the most straightforward value accrual and utility of any major DeFi token. A continued bear market coupled with DEX tailwinds could cause a flight to quality for tokens like SNX that have consistent cash flows and exciting deliverables in 2023.

Aave

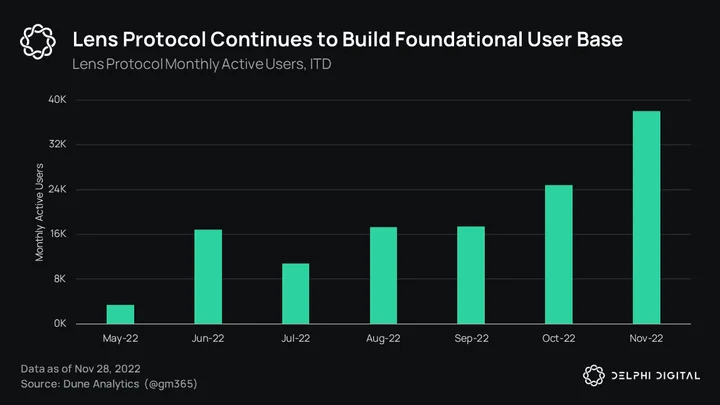

The launch of Aave v3 in March headlined an incredibly eventful year for Aave. Aave is once again taking a leadership role in pushing crypto forward, with a complete disregard for token price. The launch of its institutional DeFi platform Aave Arc, the development of decentralized stablecoin GHO, and the incubation of decentralized social graph Lens Protocol signal a focus on business development and long-term thinking.

These additions may seem insignificant at first, but they will be foundational elements in Aave’s final vision. The AAVE token has the bleakest near-term outlook of the blue chips mentioned here, but if their plans come to fruition, the token stands to benefit.

Theme #3: 0-1 Speculation Primitives

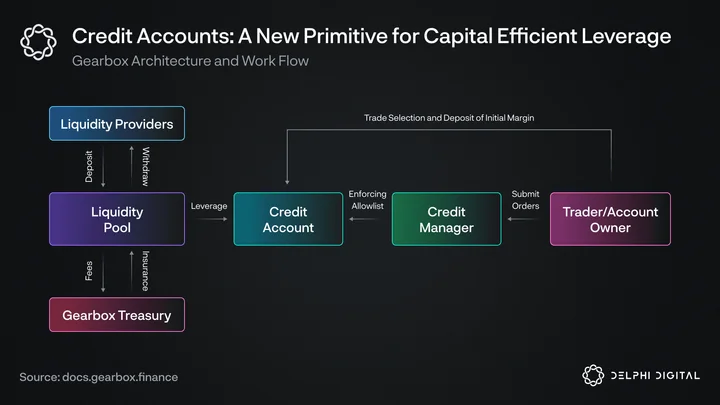

Speculation primitives have ample runway for progress in 2023. The lack of convenient, capital-efficient access to leverage has been problematic for a while now. Users are forced to utilize makeshift techniques such as recursive borrowing in order to fully capitalize on opportunities that call for spot leverage.

Gearbox allows for composable, capital-efficient leverage through its credit accounts. These credit accounts essentially act as margined leverage wallets for approved protocols. Gearbox v2 streamlines liquidations and gas costs, dramatically improving overall UX and scalability. Gearbox’s utility will exponentially grow as more protocols are whitelisted and new primitives are built. Gearbox could even allow previously infeasible applications to flourish.

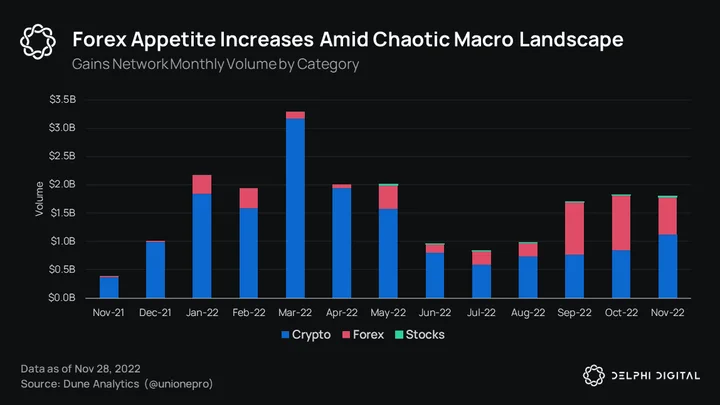

Forex is a massive market that is highly gated in traditional finance. Despite ideal conditions, attempts at bringing forex to DeFi have failed, suffering from low demand and poor design.

Given the current macro landscape, it would seem that if forex is ever going to be a thing in DeFi, it will begin to show some promise in 2023. This could occur through two approaches:

-

Synthetic assets utilizing the oracle model: Gains Network and GMX offer the easiest way to get leveraged exposure to synthetic assets. These projects have to implement creative solutions to mitigate tail risk, which are accompanied by various drawbacks. Still, this model is easy to implement and is already demonstrating the growing demand for forex in DeFi. Forex trades made up the majority of Gains Network volume in September and October. With GMX’s much larger user base and impending launch of synthetic assets, we could see forex volume explode in 2023.

-

Collateralized stablecoins pegged to various currencies: Collateralized stablecoins would benefit from composability within the broader DeFi ecosystem. Existing attempts such as Iron Bank Fixed Forex and Handle.fi have struggled due to the limited utility of spot foreign-currency exposure. The lack of convenient ramps prevent personal finance use cases, and the inaccessibility of spot leverage pushes users towards synthetic perps for trading. This is a great example of the Synthetix and Gearbox value-adds discussed above. Without liquidity pools consisting of synthetic assets, peg stability must be hard-earned through incentives and arbitrage. Oracle-fed prices for synthetic assets can shoulder this burden for forex stablecoins through liquidity pools. Gearbox’s credit accounts allow for potential utility beyond non-levered trades on Uniswap. With additional improvements in complementary dApps and on/off-ramps, this more organic avenue for on-chain forex adoption could start to gain traction.

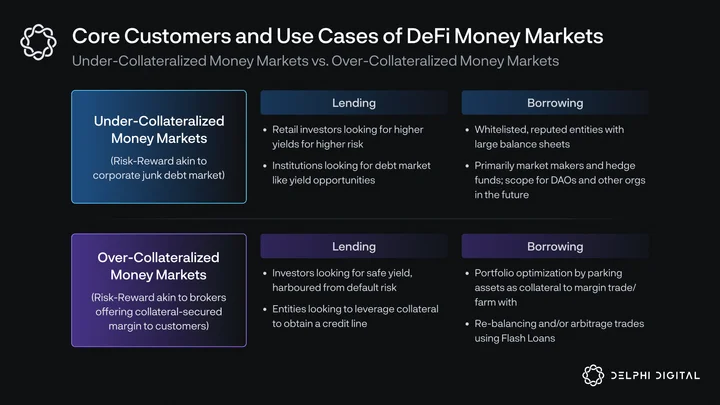

Theme #4: Undercollateralized Money Markets

We’ve written about undercollateralized money markets like Maple Finance, Clearpool, and TrueFi over the course of the year. They serve the speculation use case by funding market makers and hedge funds with accessible leverage. Unlike banks, they use on-chain holdings as a means of gauging an entity’s balance sheet health and ability to repay. Their impact on providing the market with more liquidity is evident, but projects operating in this space haven’t really found the right model yet.

As we’ve noted through our coverage of this sector, it’s no riskless endeavor for lenders. Effectively, lenders are giving out unsecured loans to market makers and hedge funds considered to be of “high stature.” Not repaying their loans is akin to burning their entire reputation in crypto. Barring insolvency and a legitimate inability to repay funds, it’s unlikely for a fund to willingly burn their reputation for a few million dollars.

However, given the frequent occurrence of tail events in crypto, the actual risk for lenders is likely higher than the perceived risk.

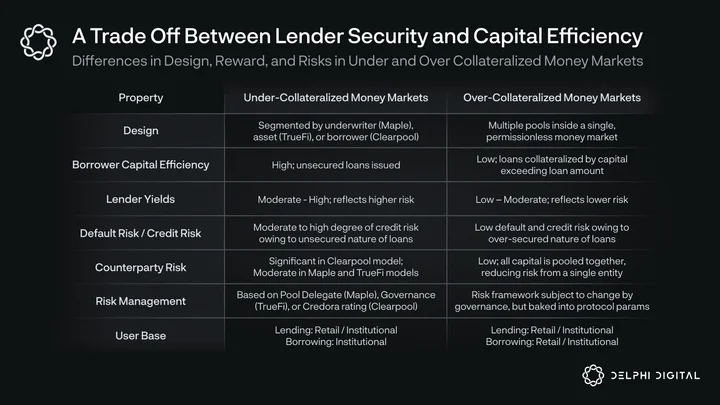

If we compare overcollateralized money markets like Aave and Compound to unsecured money markets like Maple Finance and Clearpool, there are certain types of risks that are heightened in the latter.

Default risk is the most obvious, given the unsecured nature of these loans. Counterparty and concentration risk are a close second. For example, Maple’s design is one in which a pool delegate decides who to loan lender capital to. If too much is given out to one party, lenders in that pool are exposed to greater counterparty risk. This is all the more important in the case of Clearpool, where each pool is exposed to a single borrower and therefore has higher inherent concentration risk.

In the interest of your time, we won’t delve into the designs and risks inherent to these protocols. Delphi subscribers interested in learning more about these can view our previous coverage of undercollateralized money markets, Maple Finance, and TrueFi.

For this report, the core focus is why this could turn out to be an important part of DeFi. We can all agree that liquidity is the lifeblood of a well-functioning market. When used correctly, leverage is a powerful tool. Unsecured lending remains the easiest way to unlock capital efficiency for professional investors and traders in crypto.

The core customers of unsecured money markets are market makers. They need efficient access to spot leverage to fulfill their role. It’s unlikely that traditional banks and financial institutions are going to give Wintermute, Folkvang, or GSR a large loan to market make crypto assets. But even if they did, it would be a time-consuming process marred by the bureaucracy banks are infamous for. While the evaluation process differs from protocol to protocol, on-chain undercollateralized loans are usually issued based on an on-chain balance sheet.

The other side of this coin is that if you believe banks have strong risk assessment and evaluation frameworks, it would hold true that entities that cannot get a bank loan will look to less stringent alternatives. This would be the essence of the crypto lending market — traditional finance institutions won’t give them capital, so they have to turn to crypto-native lenders. But the process of issuing loans against verifiable on-chain holdings, and monitoring the on-chain balance of an entity, could act as a mitigant by helping lenders/underwriters decide on when to take action. It’s just a matter of discovering the right business model to do all of this.

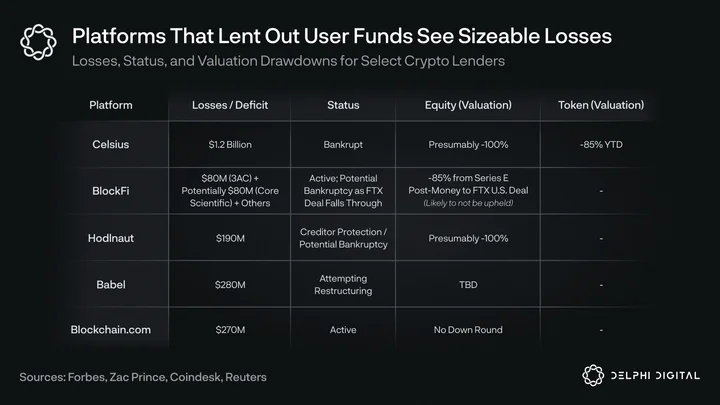

You’re probably familiar with the blow ups of institutional lenders like Celsius, BlockFi, Hodlnaut, and Babel Finance, as well as the potential ill-fate awaiting the likes of Genesis and several others. Traditional lenders run opaque operations. There’s no transparency to lenders as far as how much and to whom their money is being lent out. Capital providers to these lenders cannot evaluate concentration risk to a single borrower, and apparently they can’t rely on the lending intermediary to act with caution and diligence. Borrower concentration was what wiped out a number of lending books.

Admittedly, unsecured lending via DeFi does not fix all of this. It wouldn’t necessarily have stopped lenders from giving big loans to a single hedge fund, but it may have. Lenders could have seen a single entity getting huge loans from every platform available and started public discourse to pressurize these platforms to cut off their credit lines. Or in the case of TrueFi, which uses governance to sanction loans, token holders could’ve started voting no on further credit lines to that entity.

So maybe the music would’ve stopped earlier and caused significantly less damage.

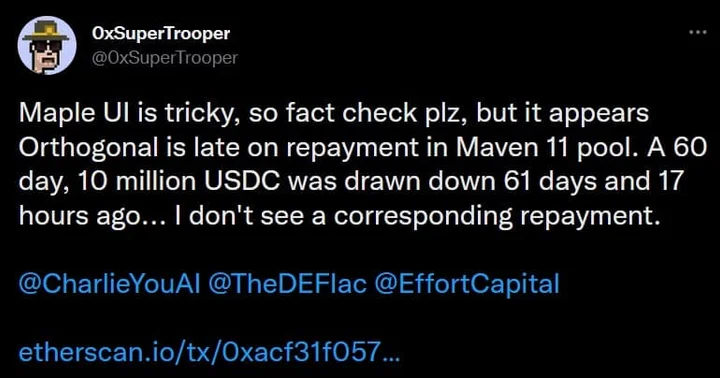

An example of this happened just this week. Last week, Auros missed a repayment of its ~$3M loan from Maple’s platform, triggering widespread concern. The situation only escalated from there.

Earlier this week, a user tweeted out how Maven11’s pool on Maple gave $30M worth of loans to Orthogonal Trading. The first of these loans was tenured for 60 days, and Orthogonal didn’t repay it. As noted, the pool delegate model Maple employs does not necessarily fix the issues that took down BlockFi and Celsius. But it does enable a transparent loanbook, which allows creditors to track ongoing concerns in real time, rather than long after things have gone wrong.

While the premise of undercollateralized lending stands to improve DeFi markets, there isn’t a ton of confidence in the models that exist today. In a nutshell: TrueFi has been using token governance to approve loan issuance (possibly changing soon), Maple affords a lot of power to pool delegates (thus centralizing loan issuance), and Clearpool has borrower-specific pools which doesn’t allow lenders to diversify their exposure.

But unsecured DeFi platforms offer the easiest way for market makers and hedge funds to obtain spot leverage. Centralized operations like BlockFi and Celsius used customer deposits to loan out capital to institutions. DeFi platforms of a similar nature also do this, except lenders can be aware of their risk profile and where their capital is being deployed. The core difference is unlocking a greater degree of transparency — and, hopefully, the ability to demand certain actions in the future.

While counterparty, concentration, and default risks will exist in any unsecured lending market, at least DeFi platforms offer an unrivaled degree of transparency. These platforms thus act as a formidable competitor to businesses like BlockFi, Nexo, Crypto.com and other institutional lending operators.

When the crypto market starts to take off again, there will be a large volume uptick for on and off-chain trading venues. Platforms that offer institutions leverage with a predictable cost of capital could prove to be an important piece of infrastructure for markets. As crypto users look to deploy capital into passive (and not risk-free) opportunities, in a time of healthy demand for leverage, unsecured on-chain lending protocols could offer prospective users competitive yields versus their centralized counterparts.

Playing devil’s advocate, it’s possible the efficiency benefits from this model are not worth the risks they entail. Maybe DeFi shouldn’t be trying to mimic TradFi, and should focus on its core goal of trustless and decentralized financial infrastructure. While unsecured credit helps indirectly enrich markets and the on-chain versions of these products enable greater loanbook transparency, decentralizing these platforms is proving to be difficult.

We recognize this is a theme with a relatively higher chance of failure, but finding the right model to balance underwriter expertise and process transparency could enable more liquid markets in DeFi.

You can find more of our thoughts on how to scale undercollateralized lending in the “Futuristic Ideas” section towards the end of this report.

Theme #5: Improving the State of Passive LP Products and Emphasizing Delta Neutrality

Uniswap v3 and the decline of SushiSwap marked the end of incentivized LP staking. LP management protocols such as Charm and Visor have done little to demystify concentrated liquidity provision for passive users. DOVs capitalized on option AMM’s inability to protect LPs, but still carry high risk over prolonged periods. Liquidity providers have been left with few options to safely chase material returns, but 2023 is bringing a new wave of DeFi projects that are catering to neglected LPs.

Lyra Finance’s Avalon update brought the first delta-hedged AMM to DeFi. The ability for an AMM to hedge its obligations has been a game changer for LPs since launch. Delta hedging is extremely difficult to implement, but more delta-neutral AMMs and sustainable yield projects are starting to emerge.

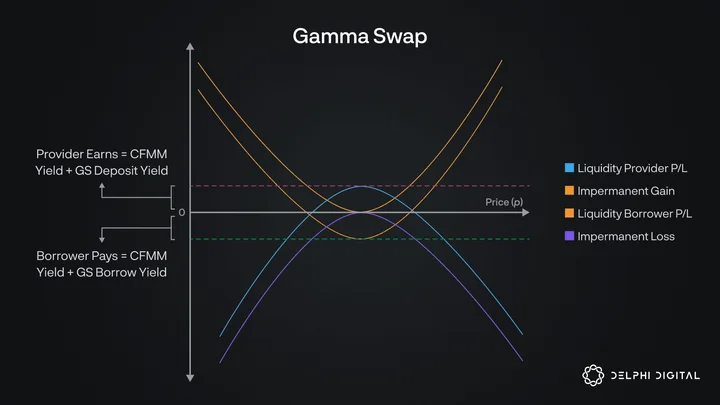

GammaSwap allows users to long volatility in order to speculate or hedge against impermanent loss. LPs on XYK AMMs are effectively long volume and short volatility. Volatility in excess of returns from trading fees results in impermanent loss. Since AMMs don’t allow the borrowing of liquidity, longing impermanent loss is not as straightforward as shorting spot tokens via money markets. GammaSwap is building a user – AMM middle layer that will allow for the manipulation of LP tokens.

Using GammaSwap, users can borrow an LP position and separate the tokens, gaining positive exposure to impermanent loss. Liquidity borrowers pay a funding rate to GammaSwap LPs, which results in a payoff structure that beats the vanilla LP position in all scenarios.

Rage Trade is attempting to address some of the prior issues with vAMMs and provide stacked yield for LPs through recycled liquidity. Rage Trade allows users to deposit LP tokens into various 80-20 vaults. 80% of the TVL remains untouched on the original platform. The remaining 20% collateralizes concentrated LP positions on a Uniswap vAMM to support Rage Trade’s ETH perpetual market. The payoff resembles the original yield plus a Uniswap v2 ETH-USDC LP position.

A key theme for these emerging projects is that they deliver concrete improvements over the status quo. LPs are still exposed to impermanent loss and drawdowns, but receive supplemental income by powering innovative new products.

Theme #6: The Rebirth of UX Aggregators: A Front End for DeFi

The current state of DeFi’s — or rather, crypto’s — UX is far from ideal. Right now, the general process flow is as follows: plugging a piece of hardware into your computer, using a browser extension to control the flow of funds, and visiting an array of different websites to conduct one’s activity. Traditional tech UX designers lost a piece of their soul reading that.

Using crypto is hard. And the harder it stays, the thicker the wall between this industry and mainstream adoption.

Zooming in on financial services, what exactly does the UX of traditional finance look like? It differs from person to person. But typically, you would have one app for your brokerage (investments), one or a few banking apps, one or a few payments apps (Apple Pay/Google Pay), and maybe an aggregator of sorts to help consolidate information and pay off multiple credit card bills from a single interface. At most, the average person probably has 4-5 financial apps they use to get everything done.

But why is this the case? Well, different banks operate upon their own infrastructure and do a great job of gatekeeping features. Aggregation apps can only aggregate certain feature sets like credit card payments. For most things, you have to use a bank’s website/app. Or even worse — visit a branch.

DeFi sits upon a few transparent infrastructure legos. Ethereum, Solana, Avalanche, and Arbitrum are a few examples of those base layers. These networks are home to non-custodial networks, where the highest degree of custody you would be subjected to is smart contract custody. And even in that case, every user has control over when they can deposit/withdraw funds.

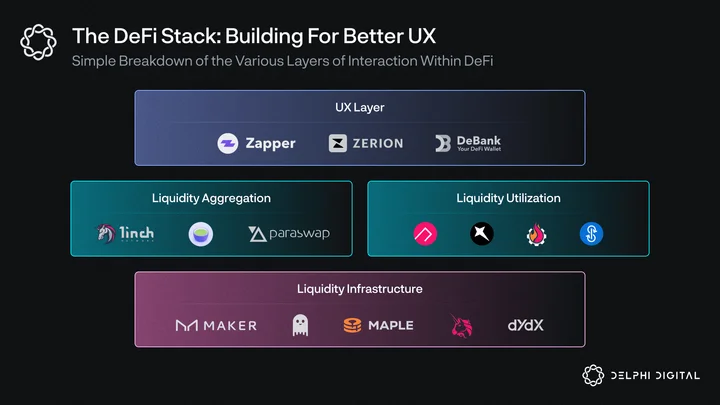

Because of this, we don’t need to live in a future where users have to go to the Uniswap front end to access swaps, or the Aave front end to find yield for their idle assets. We have the ability to create UX aggregators that act as a unified front end for all of DeFi.

First of all, unlike banks and brokerages, there usually is no single app crypto users visit. If you want to buy Apple stock, it doesn’t really matter if you use a Charles Schwab brokerage account or a TD Ameritrade account. Either way, your order still goes to the NYSE orderbook. However, in DeFi, there is no central trading venue. There are hundreds, if not thousands, of DEXs with liquidity to trade assets on. Depending on your trade size, you will find different execution prices for a token you want to purchase on Uniswap, Curve, 0x, Bancor, SushiSwap, etc.

Liquidity aggregators fix this. Protocols like Matcha, 1inch, and ParaSwap pull quotes from a variety of DEXs in order to find users the best execution price. A rational user would visit one of these liquidity aggregators rather than visiting different front ends to find the right quote or being loyal to a single trading venue.

As explained in the introduction, DEXs have seen the greatest degree of product-market fit thus far. And thus, DEX aggregators have been successful. In the future, as DeFi grows, we expect to see liquidity aggregation expand further than DEXs. Aggregators for borrowing, lending (or yield in general), options, perpetual swaps, and other products are bound to pop up. The large number of protocols facilitating each of these activities necessitates this.

But wait, if we have liquidity aggregators specific to each sector of DeFi, does that mean users will have to visit different aggregator front ends for each of their needs? Who’s going to aggregate aggregation?

UX aggregators sit atop all these liquidity aggregators, joining all their features into a unified interface. Imagine visiting a single front end, connecting your wallets, and being able to instantly find the best venues for: a specific swap, yield-bearing opportunities, borrowing rates, execution for perpetual futures, the cheapest option premiums (or most expensive for prospective sellers), and more.

Even for power users, UX aggregators offer a dramatic step forward in the ease of using these applications. Products like this don’t necessarily cater to new users unfamiliar with the space — a concept we’ll touch on later in this report. Considering users will still have to use hardware wallets and browser wallet extensions, the core customers for pure UX aggregators are people who already know how to use these things. But making life easier for the current cohort of users is not something to be taken lightly. Every step towards improving DeFi’s ease of use is a welcomed step.

For newer crypto users who use their own wallets to trade, UX aggregators offer some cool benefits. For starters, access is limited to protocols deemed to be “safe” from rug risk. Zapper is unlikely to integrate some new farm spitting out a 4-digit APY with a high risk of the team pulling off a rug. More savvy users who understand the risks of these farms will have no qualms occasionally visiting a new front end to indulge their inner degen. However, since the entire experience is non-custodial, there is a large degree of autonomy. For example, one could still swap into high-risk tokens using a UX or liquidity aggregator by overriding the warning that pops up. You get warned, and that’s it. Nobody stops you from doing anything.

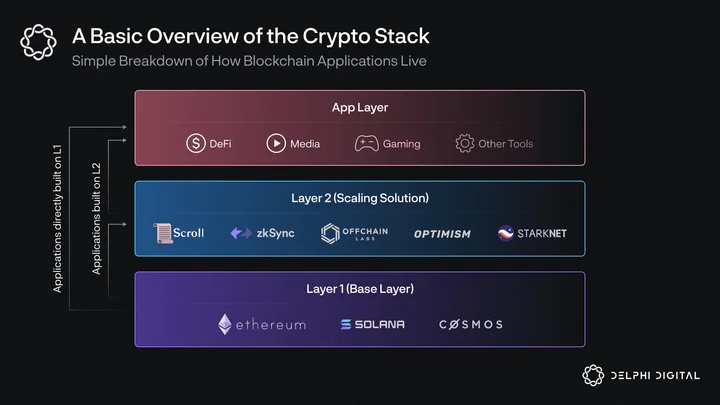

With different aggregation layers, the DeFi stack looks something like the above graphic. Rather than thinking about Uniswap, Aave, 0x, and other protocols as consumer dApps, we believe it is more accurate to term them “liquidity infrastructure.” The main point of these dApps is to house liquidity and help users get efficient execution for their activities. Their core customers should be considered liquidity providers rather than traders. Catering to traders/investors and discerning the best trading venues is the job of liquidity aggregators.

Importantly, this hierarchy also means that UX aggregators will own the customers, as they are the layers with which users interact. Now, this may prompt one to think these are great businesses to own, but monetization is not that simple.

This isn’t Web2 where Facebook can bombard users with advertisements. There are already tons of UX aggregators like Zapper, Zerion, and DeBank, and given that a user owns their information via their on-chain addresses, switching costs are incredibly low. If one UX aggregator attempts to monetize via advertisement — something frowned upon by most crypto proponents — the cost of moving to a different UX aggregator is negligible to the user.

Overall, we believe UX aggregators are primed to become the primary user-facing layer in DeFi. The timeline to this happening is dependent upon when they introduce the kind of feature sets consumers want. Zapper, Zerion, and DeBank already enjoy fairly deep user bases given the number of active on-chain users. Now, it’s just a matter of figuring out a novel monetization mechanism that doesn’t infringe on usability.

Theme #7: Ditching veTokens for More Sustainable Alternatives

VeTokenomics burst onto the scene with Curve’s yield farming frenzy at the tail end of DeFi Summer. The ensuing Curve wars fortified Curve’s position as DeFi’s liquidity moat. Today, dozens of other projects are starting to embrace veToken designs. There is now over $10B TVL in projects that have implemented or plan to implement some form of veTokenomics.

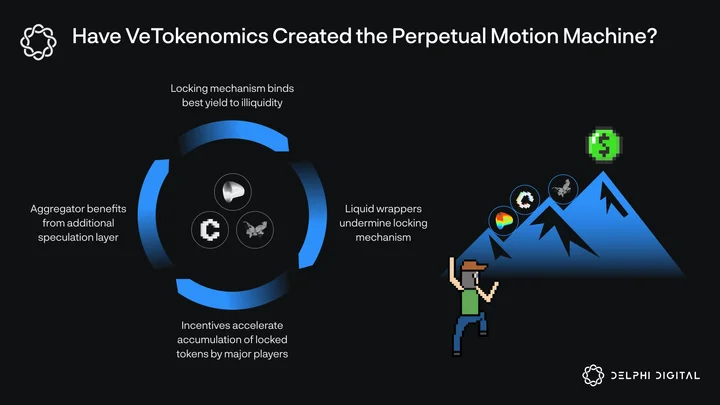

At their core, veTokens are creating market inefficiencies (binding illiquidity to optimal yield) that are intended to relieve sell pressure from aggressive liquidity-mining programs.

Typically, mature veToken structures such as CRV, CVX, FRAX, and BAL result in around 50% of token supply being locked – an undeniable benefit for token holders. When applicable, steep emissions elegantly charge a funding rate to token holders that provide no value to the project. Theoretically, long-term thinking by ve-lockers drives additional value. This benefit breaks down as individual users are outdone by aggregators which further separate incentives.

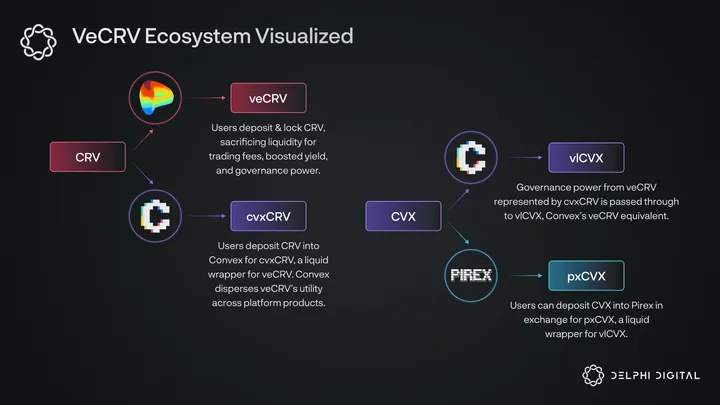

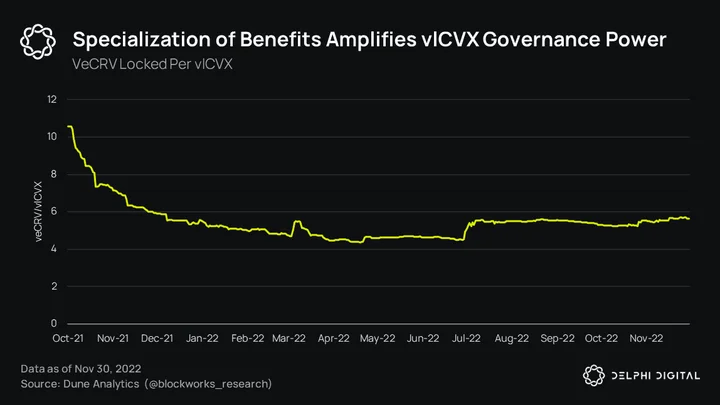

Once veCRV was launched, Convex created a liquid wrapper called cvxCRV. Convex allowed users to stake their Curve LP tokens to enjoy boosted yields without the veCRV commitment. This accelerated Convex’s accumulation of veCRV, as individual users tended to avoid the unnecessary sunk cost. Users who locked CVX for 16 weeks in exchange for vlCVX controlled the gauge votes of Convex’s veCRV and avoided the linear decay. This separation of veCRV’s utility allows vlCVX to wield massive voting power, with 1 vlCVX controlling over 5 veCRV. Individual veCRV holders are diluted, with veCRV’s utility spread too thin by comparison.

Since Convex requires users to lock CVX for vlCVX to steer gauge voting and earn bribes, the need for an additional liquid wrapper is born. Redacted Cartel’s Pirex creates liquid wrappers for locked-token schemes such as vlCVX. Pirex allows for the auto-compounding of rewards and the tokenization of future voting events. It will soon incorporate GMX along with – ironically – its native revenue-locked BTRFLY.

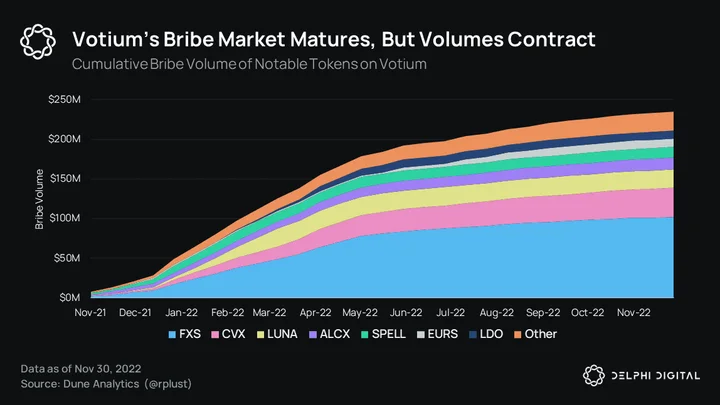

Bribe markets such as Votium and Redacted Cartel’s aptly named Hidden Hand allow users to sell governance votes for money. With the market for veTokens set to skyrocket in 2023, the market for voting boutiques undermining these designs in favor of equilibrium could benefit tremendously. Votium currently dominates the market for Convex, with over $200M in cumulative bribes paid on the platform.

During Votium’s early rounds, bribers were able to steer over $5 in CRV emissions per $1 spent on bribing. This situation is particularly convenient for projects like Frax, who own a significant amount of CRV and CVX while using bribes to direct emissions towards their pools. vlCVX ownership offers a rebate for bribe expenses, as Frax essentially pays themselves. Emissions per $1 spent on bribes are now around $1.40, and will likely settle at or below $1.

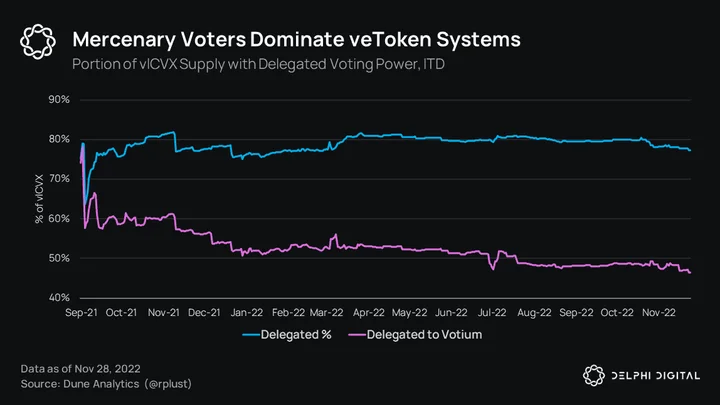

While emissions per dollar decrease, the portion of mercenary voters will likely remain stable or increase. vlCVX delegation has remained steady at around 80% since inception. Users don’t lock veTokens to govern, they lock to earn monetary benefit. This is further supported by the mere ~18% of veCRV holders who have voted in Curve governance. Votium’s decreasing market share is likely more a result of the miserable bribe-claiming UX rather than a declining appetite for bribes. Pirex’s collaboration with Llama Airforce solves this issue with uCVX, which auto-compounds earnings into pxCVX.

As additional aggregation layers continue to emerge, users will opt for the outermost layer rather than deciphering the convoluted mess of unlock schedules and who controls who. Frax-like ownership at the metagovernance layer will be less practical, as NAV will be made up of unrelated businesses. Bribe markets will resemble native token dumping as a service as the increasingly transactional shadow market is relegated to the back end. As we are already starting to see with sustainable yield and principal-protected products, the market will squeeze everything it can out of these high FDV gauge tokens to support compressed yields.

The veToken design was purpose-built for Curve’s business. It works as well as it ever will for Curve. Now, projects are implementing veTokenomics as a levered liquidity-mining program without any concrete objectives or KPIs. Like pool 2s, Ohm forks, and LUNA clones, the manic copycat phase of adoption tends to exhaust the market appetite for tokenomics fads. What is left is strictly the fundamentals. With veTokens, the fundamentals are just multiple layers of red tape propping up on-chain Feudalism.

VeTokenomics aren’t inherently bad, they’re just pointless. There’s so much more to crypto than token unlock schedules. The rise of veTokens is a symptom of the widespread lethargy in DeFi over the past year. Market inefficiencies will inevitably be undermined and abstracted away from view. All roads eventually lead to a laissez-faire approach. In the meantime, there is a lot of value to be extracted while inching towards this equilibrium. Playing this narrative correctly could be incredibly lucrative.

What Surprised Us

Surprise #1: Underwhelming Derivatives Traction

dYdX had a breakout year in 2021, finding strong footing on the back of its StarkEx validum network and a much-anticipated token launch. In the first 10 months of 2022, dYdX facilitated a whopping $419B of perpetuals volume. While that’s still much lower than the likes of FTX and Binance, it’s still commendable.

Sadly, dYdX is the only obvious example of getting on-chain derivatives markets right. Other models of perpetuals from the likes of Perpetual Protocol, Drift, MCDEX, and others were far from successful. A lot of projects aimed to incorporate the virtual liquidity model, owing to the ease of setting up a market and the ability to bootstrap without tangible liquidity.

We’ve noted the massive shortcoming of this model in a previous report shining light on decentralized perpetuals at large. And while a few of us at Delphi believe this style of liquidity structuring is done and dusted, we’re still seeing projects pursue the virtual AMM (vAMM) model.

Apart from new names like Rage Trade, there isn’t much design-level innovation happening with decentralized perpetuals. Because of this, a few of us on the Delphi DeFi team have begun to suspect that on-chain orderbooks will see strong traction.

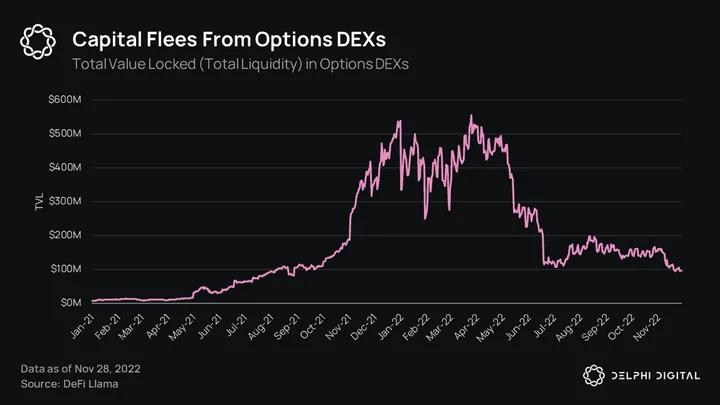

Options were another standout on the year — but not for good reasons. We’ve been chasing DeFi options for nearly two years now, with very little results to justify the capital, resources, and effort put into these endeavors. As someone keeping a close eye on the space, it seems as though AMMs were the wrong solution to the options liquidity problem.

Upon discovering Zeta Markets and the high-throughput environment of Solana, it was tough not to be convinced that orderbooks were the path forward. Liquidity was flexible and priced at what individual actors deemed a fair value to be — unlike AMMs where pricing was forced. The optimal path forward seemed to be a native volatility surface on the DEX and some form of Black-Scholes pricing to ascertain the fair value of an option. Moreover, most options DEXs did not truly understand their customers.

Until Zeta, no options exchange offered futures contracts with expiries matching all options contracts. Futures are essential to options dealers in order to hedge their positions. Without futures, trading operations would have to be fragmented, with one leg of the trade on the option DEX and the other leg on FTX or another venue with delta-one products.

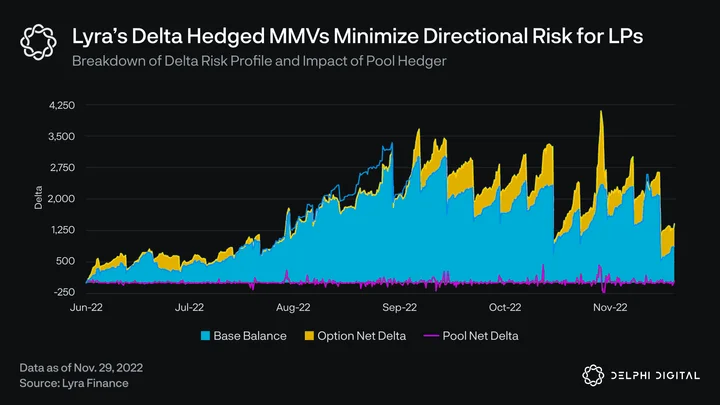

Our thoughts on the feasibility of options AMMs were challenged when our analyst, Jordan, published a fantastic piece of research on Lyra. In a nutshell, Lyra has created vaults that offer a delta-neutral experience for liquidity providers. That means that hoarding delta and hoping price moves in your favor is no longer how DeFi options LPs have to make money. Instead, they can simply extract spreads and fees with minimal delta risk, i.e., no additional exposure to price movements.

Lyra has some drawbacks, the most prominent of which is its reliance on Synthetix for hedge liquidity and Synthetix’s inherent limitations on liquidity (limited by the size of the debt pool). But otherwise, it was the first time I had seen a truly sustainable approach to creating AMM-based options that didn’t leave LPs for dead.

Towards the end of 2022, we’ve seen the design space for on-chain derivatives take a necessary step forward. There are a handful of projects creating handy experiments that could end up being the future of DeFi derivatives. Rage Trade introduces a unique liquidity provision mechanism for perpetuals — one that allows LPs to deposit existing LP tokens to compound yield. Their 80-20 liquidity split also stands to possibly offset impermanent loss, but that remains to be seen in practice.

Overall, though 2022 was a mostly dreadful year for DeFi derivatives (and DeFi as a whole), we’re seeing a lot more cool designs get put into practice and battle-tested. While we’re at the mercy of the market, we expect a lot more of the same product innovation in 2023, if not actual traction and an expanding user base.

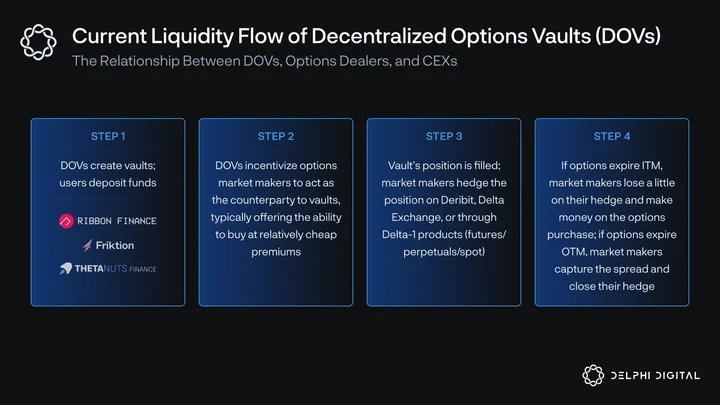

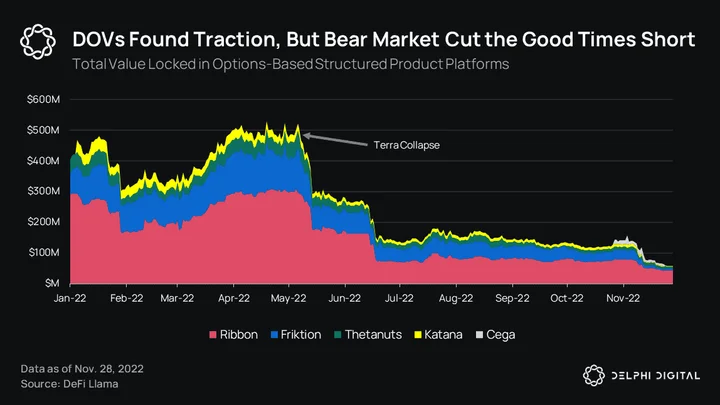

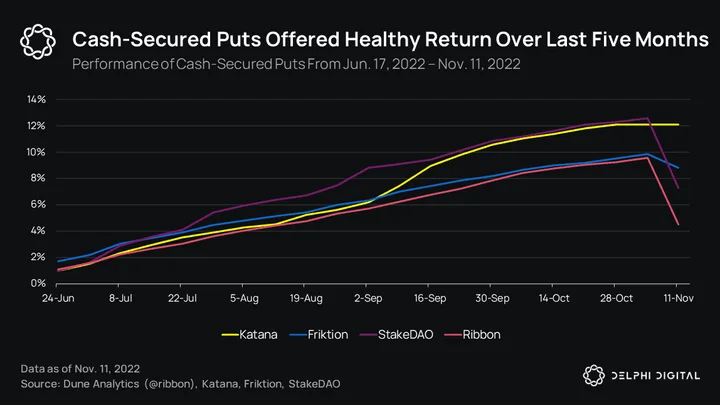

Surprise #2: Saturation of the Structured Products Space

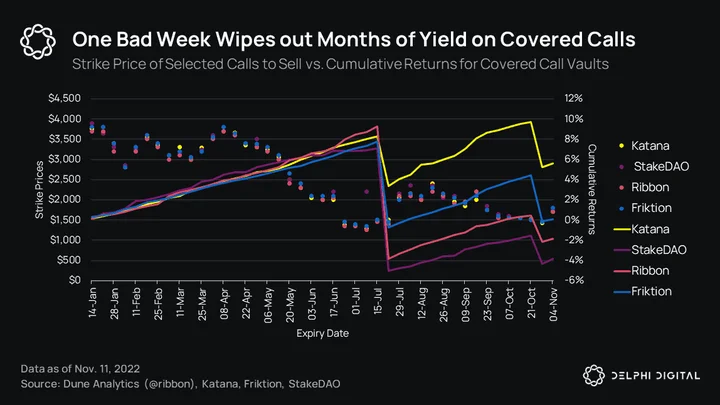

When Ribbon Finance launched in Q2 2021, it was a revelation. Every budding finance nerd knew of structured products and how they were gatekept for wealthy investors in TradFi. Ribbon broke the locks off the gate by introducing systematic option-selling vaults as an on-chain primitive. This meant the strategy was completely transparent. The first two strategies were simple: covered calls (sell calls against the underlying spot asset as collateral) and protected puts (sell puts against stablecoin collateral).

By the end of 2021, there were probably over 20 teams that had raised capital to build on-chain structured products. In hindsight, all of us should have seen this coming. It was a lucrative thing to do. Build some strategies, incentivize market makers to give your users the liquidity they need, and rake it in via management/performance fees. Of course, all of this is assuming the project was able to attract depositor capital.

To expand on the “incentivize market makers” point from above, all of these platforms basically rent liquidity from Deribit. Since on-chain options haven’t taken off, structured products create deals with market makers to get the liquidity they need. Market makers will, for example, buy calls from Ribbon depositors at a certain price, then sell an equivalent amount of calls with the same specs (expiry, strike) to hedge. By doing this, they capture a spread — essentially the difference in the price they buy from Ribbon at and sell on Deribit.

We got on-chain options-based structured products before on-chain options, which is peculiar to say the least. This makes the saturation even more surprising.

While these products enjoyed capital inflows going into Q2 2022, this began to reverse. It wasn’t just a tapering off, but a large outflow of capital alongside principal erosion in USD terms as crypto assets got beaten down. Soon, the amount of capital managed by these products had fallen by anywhere from 60-90%.

It seems counterintuitive for yield-bearing products to see a deterioration in capital managed as crypto asset prices and lending yields took a hit, right? Selling options to generate yield was probably the only way left to generate returns in crypto. But there is another side to the story — the side of tail risk.

Selling options is not free money. Far from it. In fact, some of the most experienced and knowledgeable options traders think selling options is overrated from a yield-generation perspective. Many use the old analogy of it being akin to picking up pennies in front of a steamroller. In this context, the steamroller is the notion of tail risk — which is far too common in crypto.

One bad week can erase months of steady gains. Look no further than the performance of covered calls. This is precisely the kind of tail risk selling options entails.

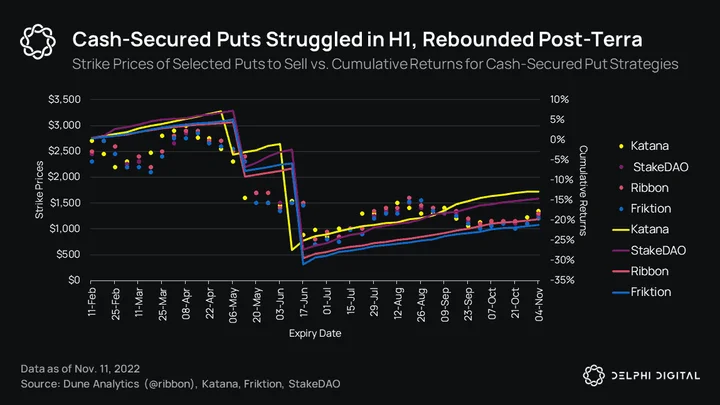

But if you think about it logically, it does make sense that we saw mass outflows in the aftermath of market-wide contagion driven by the Terra and 3AC collapses. But on the flipside, once this tail risk had played out and the market had quieted down a bit, these vaults likely showed a healthy return, since the “black swan” had played out and price stagnation started to settle in.

And that’s exactly what we saw. Cash-secured puts fared well from late June into November, until FTX threw a wrench in the market’s plans.

Overall, what was surprising was the sheer number of projects building on-chain structured products. Realistically, the industry probably wasn’t ready for this. The concept of portfolio construction is still a bit of a reach in crypto. And structured products are not a place to park all your idle assets, but rather a piece of the puzzle that is optimal portfolio construction.

We’ve seen projects like Cega pop up that introduced complex yield-generation strategies (via options) to the DeFi market. I know this may come off very Gensler-esque, but are these products truly suitable for retail investors? Just because you can, doesn’t necessarily mean you should. A covered call is simple and easy to grasp. You just need a basic understanding of options.

But when you bring fixed coupon notes, barrier options, and other exotics into the equation, it becomes a lot more complex for the average user to follow.

Real yield is a very important narrative, because we all know relying on token incentives doesn’t lead to long-term favorable outcomes. At the same time, these real yields come with their own set of very real risks, and those who treat them like an Aave money market pool may unfortunately have to learn about these risks the hard way.

Futuristic Ideas

Idea #1: Envisioning a Consumer-Grade DeFi Experience

In the section on unified UX layers for DeFi, we described a tool that allows users to retain full custody of their assets while improving the experience of directly interacting with DeFi protocols. This kind of setup is ideal for power users who are comfortable with the trade-offs for self-custody. But in order to allow the average Joe to get comfortable with DeFi, we need something slightly more custodial and risk-tuned.

The idea is pretty simple — but there is a big and obvious caveat. Imagine a Robinhood-esque app plugging into different DeFi protocols, simply providing some degree of custody and facilitating user interactions with underlying liquidity. Revisit the graphic in the UX aggregation section that visualizes the DeFi stack. Instead of a simple UX aggregator at the top, we slip a centralized solution in there. Yes, it does need to be a somewhat centralized solution. Ideally, the setup is semi-centralized, with a multisig wallet where the platform holds 1/3 keys and the user holds 2/3 keys.

Perhaps users start off with the platform having custody of their assets and slowly move towards a more self-custodial model. Initially, they can rely on the platform and gradually learn about self-custody, what it entails, and why it matters.

In this case, the application is just a unified front end with risk-limitation features. Given the number of scams in crypto and the inability of new participants to separate the wheat from the chaff, this should be a welcome feature. It could have only certain DeFi protocols and actions enabled on the platform, cutting off access to the numerous honeypots and scams that exist in the space. It could also have some additional value-add features baked in; maybe an anti-liquidation mechanism like DeFi Saver and stop-losses for spot positions (unwind position if market price hits a certain price threshold).

Given this platform would be structured akin to a centralized exchange, it would (ideally) be regulated and have access to banking services, thus enabling the flow of funds from fiat in a bank account to stablecoins in the user’s wallet. Really, the custody fallback if a user loses one of their keys and the rails to move from fiat to crypto would create a much cleaner user experience for those looking to start tinkering with DeFi and crypto at large.

What are some examples of what a user on this platform could do?

-

Simple swaps via DEX aggregators.

-

Staking ETH via Lido/Rocket Pool.

-

Access to automated liquidity-provisioning services.

-

Relatively safe yields and access to low leverage using Aave/Compound.

-

Higher and riskier yields using Yearn, Ribbon, Maple Finance, TrueFi, etc.

-

Maybe even perpetuals trading on dYdX for users in accepted jurisdictions.

At this point, every reader of this report is aware of what happened with FTX. This event has caused a lot of uncertainty with how centralized platforms manage user funds. BlockFi was an industry darling targeting an IPO earlier this year, and now it’s bankrupt. So how can users trust a platform like this, where some or all funds are custodied by the platform?

Well, realistically, it boils down to finding a profitable business model without having to rely on customer funds the way platforms like BlockFi and Celsius did. The platform’s job is simply to custody funds and facilitate the usage of decentralized applications/infrastructure.

Employing a management fee in the range of 0.2-0.5% based on funds held would be one driver of revenue. Slapping a small markup on transaction fees would be a potential second source of revenue. Another interesting idea could be implementing a freemium model, where free users have to custody with the platform (giving them more custody-centric fees) and paying a subscription would enable users to use the multisig where they hold 2/3 keys and the platform holds 1/3 keys.

Whatever the exact model, it’s important that they act as custodians like Coinbase and Anchorage (hopefully) do and not touch customer funds. As mentioned before, their job is to do two simple things: custody some/all assets and facilitate interactions with decentralized tech.

Regulation creates a big question mark over the viability of such a business, and we’re not going to act like we know how this would be perceived by global financial regulators. Nevertheless, a platform like this could prove to be a major boon for crypto usage, enabling less financially and tech-savvy users to start exploring the space at their own pace.

The eventual goal of this would be to help people learn about the importance of decentralization, self-custody, and censorship-resistance firsthand. Hopefully, this would pave the path for more people to directly interact with decentralized software.

Idea #2: How to Scale Undercollateralized Lending

DeFi has built most of the primitives that are currently possible. We have protocols that facilitate whitelisted undercollateralized lending. But if DeFi is ever going to truly rival traditional finance, we will have to tackle mass-scale undercollateralized loans eventually. Such a system may seem several years away, but it isn’t as far-fetched as it seems. Self-sovereign identity and Sybil resistant primitives hold the key to unlocking this. From there, we can begin to construct an undercollateralized lending system that onboards crypto’s next billion users.

We have three crucial objectives:

-

Sybil resistance: An individual cannot beat us more than once.

-

Incentives, game theory, and crypto-native recourse: The proportion of individuals that choose to hurt us will be below a sustainable threshold.

-

System architecture: An individual cannot beat us too badly.

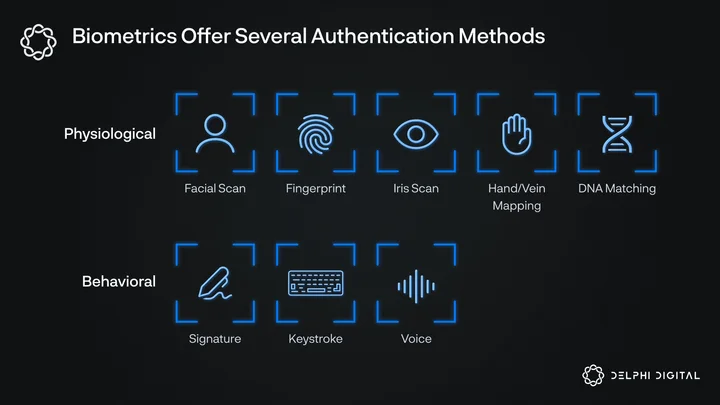

Utilizing decentralized identifiers and verifiable credentials to improve crypto’s Sybil resistance is paramount to building any undercollateralized lending ecosystem. Let’s take a look at some potential methods.

Biometric Authentication

Biometric authentication is highly accurate, scalable, and versatile. Biometrics offer permanent, portable authentication that traditional passwords cannot provide. Biometrics can utilize numerous physical and behavioral features to verify identity with a high degree of confidence.

Biometrics are gaining major traction in Web2 with governments and the private sector alike. Understandably, there is growing pushback towards the use of biometrics. Skeptics cite dystopian scenarios and the honeypot risk associated with storing large amounts of sensitive data in centralized databases. Additionally, industry-leading biometric authentication products such as Apple’s FaceID have been exploited under lab conditions. Despite a high degree of accuracy, the rare instances where a malicious actor succeeds are far more detrimental than other authentication methods. Once an attacker fools the authentication system, there is little to prevent them from scaling their attack with numerous fake identities.

Whether we like it or not, biometrics have arrived and will continue to entrench themselves in our phones, airports, and cities. Crypto has the potential to implement biometric authentication far more effectively than in Web2. Biometric templates can be locally encrypted into hash functions that are then shared, allowing the user’s biometric data to remain private.

Social Graphs — Webs of Trust

Social graph analysis is easier to fool in one instance than biometrics, but offers strong resistance to large-scale attacks. Compromising an entire social graph would take an enormous amount of time, capital, and coordination.

Biometrics and social graphs will likely co-anchor the winning identity solution. They both scale effortlessly and cover each others’ weaknesses. Homomorphic encryption and zero-knowledge proofs can allow the user to retain sovereignty over their data. Given transparent and cryptographically verifiable trust assumptions, users will likely be willing to offer more revealing info that they would normally shield from Web2 giants.

Turing Tests — Pseudonym Parties

Turing tests involve using CAPTCHAs to separate humans from bots. These tests are difficult for a computer to solve while being simple for a human. Turing tests are very effective at discerning humans from bots, but less effective at preventing a human from imitating several humans.

Pseudonym parties involve various forms of periodic IRL meetups. Pseudonym parties are perhaps the most-ironclad proof of personhood method, since humans cannot be in two places at once. Pseudonym parties offer poor scalability though, due to the increasing difficulty of in-person meetups as the network grows.

Existing solutions often incorporate elements of both pseudonym parties and Turing tests. These methods could be used to complement an already-formidable identity system, but cannot be solely relied upon.

Summary

Existing on-chain implementations of these methods are promising. For now though, these projects have failed to generate users due to their unambitious goals. Focusing identity solutions around DAO tooling just adds overhead to widespread governance apathy. Focusing on pie in the sky solutions like UBI only serves to undermine the legitimacy of the project. Refocusing efforts towards more relevant experiments such as accountability for anonymous developers, high-profile NFT launches, and undercollateralized loans could allow these projects to gain traction in 2023. Aggregating these identity methods into a multifactor authentication solution like Gitcoin passport could help accelerate the growth of these projects and streamline their integration with prominent dApps.

Incentives, Game Theory, and Crypto-Native Recourse

In traditional finance, loans are secured by the guarantee of recourse. This recourse is given in two ways:

-

Gating of financial privileges via credit scoring. The threat of being locked out deters malicious behavior.

-

Punishment and/or repossession of assets. This threat is backed by the state’s monopoly on force.

There are a number of tools at our disposal to select good borrowers, incentivize good behavior, and make delinquency as unpleasant as possible.

Securitization and tranching will be crucial in the manipulation and repackaging of risk into more palatable chunks. The social graph will supercharge predictive analytics and allow for highly creative slicing of risk buckets. Alpha hunting and on-chain sleuthing will grow to encompass finding mispriced risk factors based on demographics, lifestyles, geographic locations, behaviors, etc.

Auctioning off bad debt via junk bonds is a logical continuation of the subordinate tranche, and marries the onboarding of higher risk appetites with a much-needed sink for distressed debt. Buying junk bonds would represent an extremely asymmetric bet on the long-term viability of the system as a whole. If the system is successful, it becomes more entrenched in society, costing users more to leave. Paying off bad debt to rejoin the system becomes a bigger priority and is cheaper than the investment necessary to forge a new identity. Scouring the social graph for mispriced junk bonds deemed likely to be paid off would become an incredibly lucrative and extravagant enterprise.

Doxxing: The threat of doxxing is one of the few crypto-native recourse options we have at our disposal. Doxxing the user to the owner of junk bonds after X days and/or doxxing to the public after X days serves to increase the attractiveness of the junk bonds.

Permissioned expenditure: Setting constraints on how borrowers spend protocol funds can increase transparency and predictability. Through a partnership with Web2 fintechs or the creation of a proprietary, permissioned stablecoin, borrowed funds could be directed to stickier goods such as car payments or mortgages, rather than consumables. This would result in a more concrete paper trail, leaving the door open for further recourse as the ecosystem matures.

This option comes with costs, however, as the lending activity would remain isolated from broader DeFi, sacrificing the composability and second-order innovation possible with a more permissionless system.

System Architecture

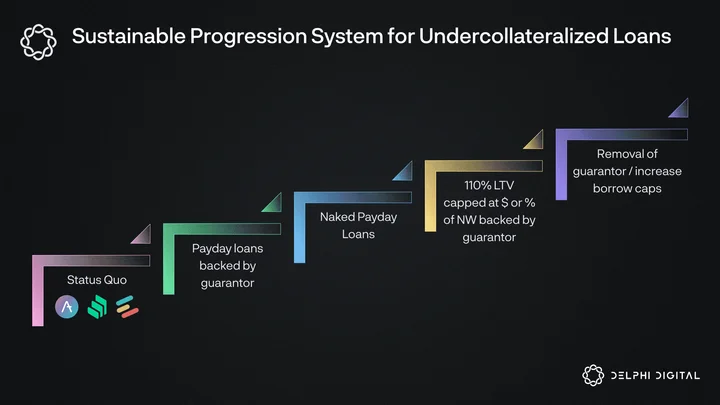

Users progress through a tier-based system, gradually earning a longer leash as the protocol allows itself to become more vulnerable to default. This stepped-program will stagger the progression of user cohorts, allowing a beta test-like diagnosis of any weak points.

As seen above, the progression system would look like this:

-

Status quo on Aave/Compound/Euler.

-

Payday loans:

-

Due to the low time-lag of payday loans, they would carry relatively low risk. Coinbase supports direct deposit and has made strides towards this type of infrastructure.

-

Experimentation with payroll custody is currently limited to prepaid debit cards. More progress needs to be made here.

-

Payday loans could be amortized by payment streams via Sablier/Superfluid. This would dramatically lower borrowing costs, providing a credit card-like experience for those with no access to credit.

-

Low probability of default allows capital-efficient use of credit delegation for guarantors. Aave’s seldom-used credit delegation feature that was introduced in v2 would find product market fit.

-

-

110% LTV capped at $ or % of net worth with guarantor.

-

Removal of guarantor, progressively increasing LTV and borrow caps.

By the time a user reaches the latter tiers, they would be strong power users. They would have likely paid hundreds of dollars in interest over a few years, lowering the protocol’s loss given a default. Prominent lending platforms such as Aave, Compound, and Euler will implement their own flavors of this system, using a variety of levers to taper progression.

Why does this all matter?

Overcollateralized (or secured) lending has dominated DeFi to-date. Yet overcollateralized lending is inherently prohibitive for those who don’t already have access to ample capital. If you need $100 to borrow $50, then secured lending only benefits those who already have $100. Those seeking a $50 loan to invest in productive uses (like starting or expanding a business, for example) are out of luck. Unsecured lending aims to increase accessibility to funding to creditworthy borrowers with lower capital requirements.

Access to financing and credit is a core tenant of every major developed economy. Efficient markets for lending and borrowing increase capital efficiency and allow excess capital to flow to more productive use cases. The problem is unsecured lending requires a large degree of trust, much more than secured lending because these types of loans are often undercollateralized (or uncollateralized in the case of some personal loans). The difficulty is determining a borrower’s “creditworthiness” in a model that relies more heavily on trust rather than their ability to pledge adequate collateral.

Unsecured lending, when operating properly, has several benefits. Although the risk of undercollateralized loans is higher, they can also generate higher returns for lenders to compensate for said risk. It also enables more opportunities for credit creation, which increases an economy’s money supply and the number of viable investment opportunities that can be funded. The expansion and contraction of credit has tremendous impacts on economic growth and business cycles, and the crypto economy is no different.

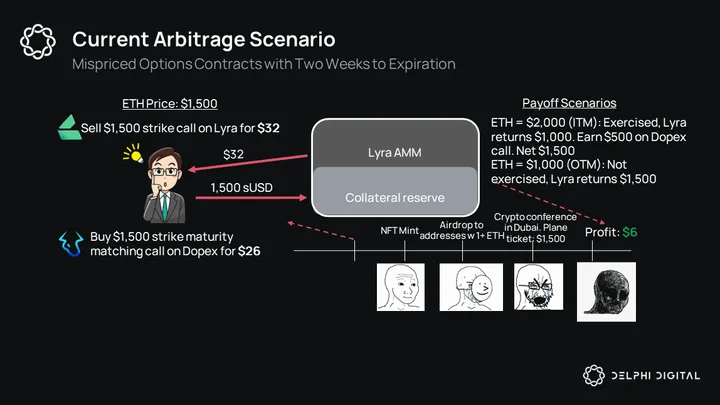

Idea #3: The Advent of True On-Chain Arbitrage

Arbitrage is crucial to the health of any financial ecosystem. It keeps prices tight and fair for all participants. In traditional finance, a simple arbitrage opportunity may look something like this:

-

Sell an overpriced derivatives contract.

-

Borrow cash to construct an offsetting basket of securities.

-

Calculate profit X, borrow X net of interest to get paid today.

The limited capital burden and ability to earn profit instantly leads to efficiently priced and liquid derivative markets. Arbitrage opportunities that remain are hard to find and only offer a few basis points of profit. This is a testament to how important arbitrageurs are to efficient markets.

Without the ability to borrow uncollateralized, on-chain arbitrage in crypto is very cumbersome. For now, it takes place in 2 forms:

-

Flash loans.

-

Buy low/sell high, hold to maturity. Capital is tied up for the duration of the contract, and profit is realized at maturity.

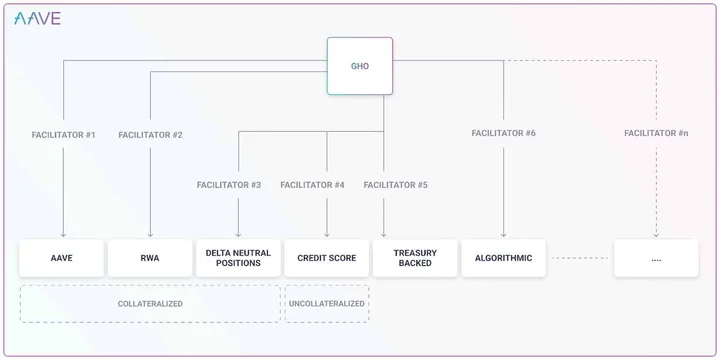

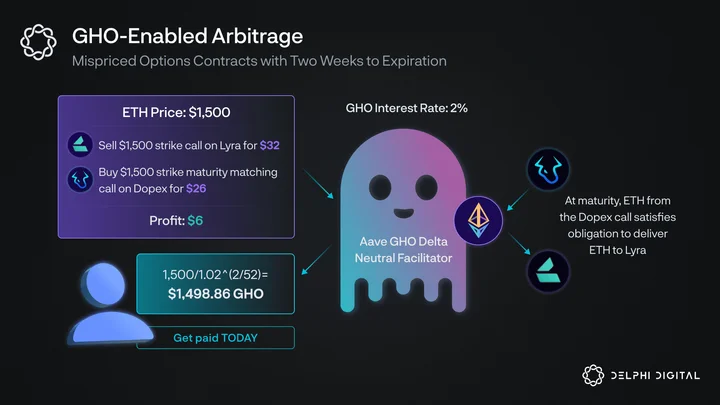

Aave’s GHO stable coin is very promising. One overlooked aspect of its potential is facilitator #3: delta-neutral positions. There are some exciting possibilities for this in the future. Aave’s portal feature and incredibly deep liquidity are ideal for facilitating the settlement of multi-currency cross-chain offsetting derivatives contracts. The synergies between Aave’s lending business and crypto’s immature derivatives markets are tantalizing.

Today, typical arbitrage for crypto options may look something like the above. Buy low, sell high, hold to maturity. This is inefficient due to the collateral required to short an option. For arbitrage purposes, options must be fully collateralized. Otherwise, the setup is exposed to the price action of the underlying and no longer offers risk-free profit.

By deploying a borrowing module on top of options AMMs or a derivative-backed stablecoin on top of lending protocols, on-chain arbitrage can start to resemble the real deal. A user purchases offsetting derivatives contracts, earning profit on the mispriced premiums immediately. The user then deposits the contracts into the lending platform’s arbitrage module to free up collateral, net of interest costs.

An obvious flaw with this idea is that for higher strike prices and longer maturities, interest costs will severely eat into profit, rendering the method impractical. Lending reserves would quickly be tied up collateralizing delta-neutral derivatives baskets, which would be a deal breaker for the lending platform. To account for this, options AMMs could whitelist lending protocols that have adequate procedures to have uncollateralized options or more generous liquidation procedures for partially collateralized positions. Alternatively, improvements could be made at the contract level to allow options to be collateralized by other derivatives contracts.

The options protocols are getting the most value from this arrangement, so it is in their interest to create a palatable situation for the lending platforms. Options platforms would receive much more efficient pricing and liquidity, likely making significant headway in their battle against CEXs. The lending protocol would gain utility for its idle reserves and product-market fit for its stablecoin (without expensive liquidity-mining programs).

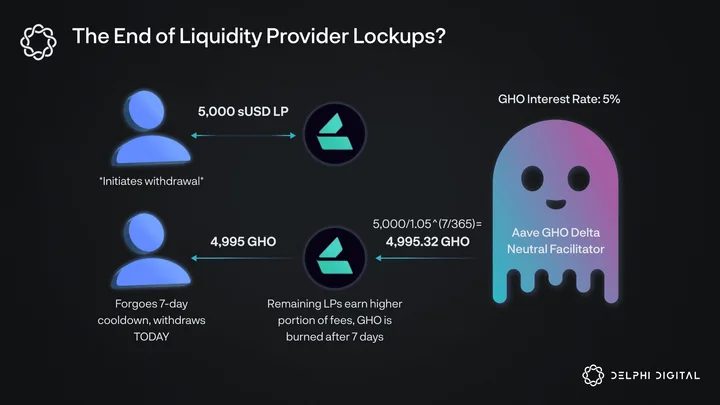

AMMs could use GHO in other ways, too. Say the protocol wants a user to wait 7 days to withdraw funds. The pool is adequately delta hedged, so it mints 5,000 GHO and lets the user withdraw 5,000 GHO less a borrowing fee for 7 days. In 7 days, the protocol converts an equivalent amount of pool reserves to GHO, which is then burned. The pro rata earnings of that 5,000 GHO go to the safety module or the rest of the pool’s LPs in exchange for assuming disproportionate risk.

One can’t help but wonder, could this put Deribit in DeFi’s crosshairs? Deribit’s settlement currency and non-fungibility of positions are the only things preventing a $10B vampire attack for the ages. Still, the potential synergies of a borrowing module on top of a delta-neutral stablecoin facilitator are fascinating to explore. On-chain derivatives are starting to simmer heading into 2023.

Conclusion

We could talk about several other themes that we believe will shape the industry. At the top of our minds: the need for payment rails, better on and off-ramps for crypto <> fiat, the emergence of DeFi app-chains, the implications of applications owning their infra layer, and many others. Additionally, the DeFi bull case and how resilient it’s been in light of recent market carnage is top of mind.

We chose to focus on a few key themes based on DeFi’s historical usage patterns and what is necessary to fully construct the base building blocks.

There’s a lot to be excited about. DeFi stands on the precipice of some of the greatest opportunities (and challenges) the financial industry has seen. We believe that decentralizing the financial system and creating permissionless access to an array of financial products will prove to be key endeavors over the next decade. Regulation poses the most obvious of challenges – especially given the importance of U.S. regulators’ stances and the prevalence of lobbies who have a vested interest in squashing DeFi.

As investors, researchers, and builders, our job is to exercise cautious optimism and find a way forward for products we believe can change the world. The themes we’ve outlined in this report will prove vital in attracting users to DeFi by improving the general state of the industry.