The Looming Opportunity With Decentralized Stablecoins

AUG 17, 2023 • 30 Min Read

Introduction

Stablecoins are an integral part of crypto, with a total market capitalization of $124B. Despite the increasing adoption of DeFi, the majority of the stablecoin market is held by centralized stablecoins such as USDT and USDC.

Decentralized stablecoins are the earliest use case of DeFi. However, users increasingly opt for centralized stables like USDC and USDT due to their convenience, scalability, and adoption on CEXs. As a comparison, the top 5 centralized stablecoins hold 93.24% of the market share, and the top 5 decentralized stablecoins only account for 4.69%. Decentralized applications are only as censorship-resistant as the money that flows through them.

With a seeming lack of growth over the past year, decentralized stables are making a resurgence. Maker continues to expand the scope of DAI, while Aave and Curve have launched stablecoin ventures of their own. Will these stablecoins tip the scales back in favor of decentralized solutions?

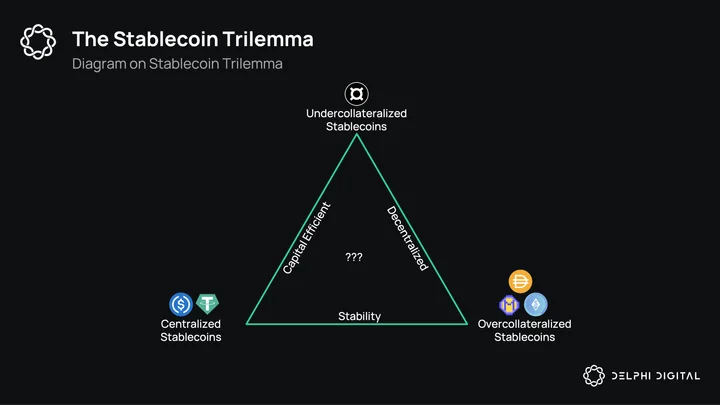

The Stablecoin Trilemma

Stablecoins aim to achieve three primary goals: stability, capital efficiency, and decentralization. Yet, the prevailing landscape shows most achieving just two. Balancing all three remains an aspirational yet elusive target.

Stablecoins aim to achieve three primary goals: stability, capital efficiency, and decentralization. Yet, the prevailing landscape shows most achieving just two. Balancing all three remains an aspirational yet elusive target.

At the heart of the stablecoin ethos is price stability. Both centralized fiat-backed and decentralized overcollateralized iterations effectively uphold their pegs. But there’s always a trade-off, with one element of the trilemma often being sidelined. The quest for a design that seamlessly integrates all three continues, but a definitive solution remains on the horizon.

Let’s now delve into the different decentralized stablecoins to assess where each initiative currently stands in the current landscape.

MakerDAO – DAI

MakerDAO is one of the largest DeFi protocols, leading DAI to be the largest decentralized stablecoin. However, they have been seeing declining usage with collateral trending down. This may be attributed to a decrease in demand for leverage, compounded by diminished opportunities for utilizing DAI in yield farming strategies.

To help kickstart demand, MakerDAO proposed the Enhanced DAI Savings Rate (EDSR) scheme, elevating the DAI Savings Rate (DSR) to an attractive 8%. This proactive measure has already begun to stimulate new demand in DAI, attracting fresh collateral into the system and possibly restarting their growth.

Furthermore, it is important to observe the upward movement in Real-World Assets (RWA) collateral within Maker. This ascent has been catalyzed by the platform’s aggressive push for multiple proposals aimed at optimizing the utilization of collateral in the PSM (Peg Stability Module) vault, which serves as the repository for the majority of its USDC holdings.

RWA Vault Analysis

RWA collateral within Maker has seen substantial growth, now comprising over half of Maker’s total collateral, amounting to ~$2.5B. This reflects Maker’s strategic deployment of DAI loans towards RWA-backed strategies, an approach explicitly designed to generate additional revenue for MakerDAO in a high-interest rate environment.

DAI loans are deployed into various fixed-income strategies, with short-term bonds accounting for the majority of the RWA collateral. This provides them with access to low-risk yield strategies through bond managers such as Monetalis and BlockTower.

To analyze the risk, we need to see where the money is deployed. By segmenting them into their various loan types, we see that Maker has a large concentration of DAI loans used in T-bills and its related products, e.g., IBTA and IB01.

However, some loans allocated are rather suboptimal given their higher risk profile. This is broken down into various ratings and internal rates of return (IRR):

- Coinbase Custody: Coinbase corporate family B2, senior debt B1 rating by Moody’s, at 2.6% IRR

- BlockTower RWA-012: Majority of loans are in BBB- and BBB loans, 4% IRR

- BlockTower RWA-013: Majority of loans are in BBB- and BBB loans, with 3rd largest exposure being A, 4% IRR

- Fortunafi: Revenue-based financing to small businesses or SaaS company, 4.5% IRR

- Harbor Trade: In default of $2.1M

These loans could expose the RWA vaults to tail-end default risks that would ultimately impact the RWA’s revenue and collateralization. It is understandable that some of the loans were provided prior to the rise of interest rates. However, at the current stage, where interest rates are at 5.5%, there is no reason to expose the protocol to unnecessary risks that do not justify their rewards.

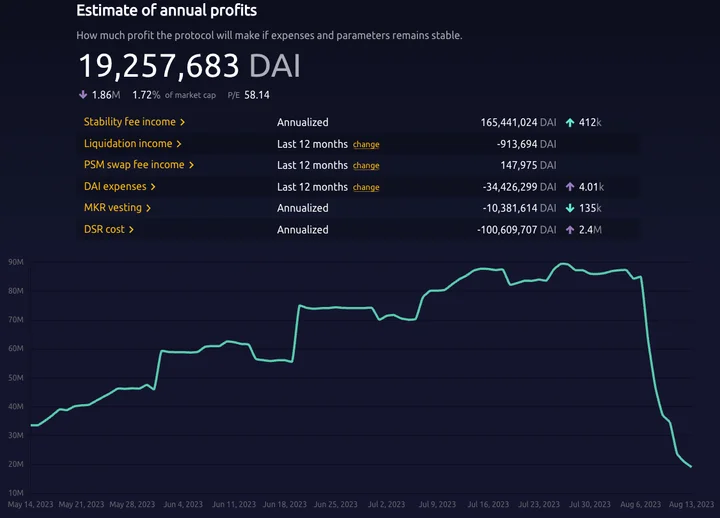

The integration of RWA has become the largest portion of Maker’s revenue and helped it increase its annualized revenue run rate to ~$150M. This will benefit MakerDAO with the build-up of a surplus buffer, but most of the revenue is currently offset by the DAI Savings Rate (DSR).

DAI Savings Rate (DSR)

The initial launch of DSR had only attracted small amounts of deposits. The recent proposal to raise the DSR from 3.19% to an Enhanced DAI Savings Rate (EDSR) of 8% was aimed at stimulating growth and demand for DAI by enhancing the attractiveness of the DSR. As a result, DAI now offers the highest yield among stablecoins, outperforming various money market yields and DEX LP returns. The implementation of EDSR has prompted a substantial inflow of DAI into the DSR, increasing the total from ~$340M to nearly $1.25B.

Source: https://makerburn.com/#/estimate

Source: https://makerburn.com/#/estimate

However, this expansion carries significant financial implications. With the DSR now set at 8%, the annual cost to Maker is projected at $101M. Consequently, this will decr

Read the full report

This report is part of Delphi Pro.

- 800+ Pro reports across every major sector

- Talk directly with our analysts

- Private community of funds and builders

Already a Pro member? Log in

0 Comments