The Power of Algo Pools: Astroport's Passive Liquidity Solution

JUL 12, 2024 • 18 Min Read

Introduction

Astroport is a decentralized exchange (DEX), initially created to capitalize on Terra’s success, positioning itself as one of the top DEXs across every blockchain. The subsequent downturn of Terra and UST had a profound impact on Astroport.

Despite these challenges, Astroport strategically adapted through the depths of the bear market, successfully regaining traction across multiple Cosmos blockchains. Their goal is to become the largest AMM in Cosmos and eventually in the whole of crypto. Currently, Astroport has ~$31 M in TVL and achieved over $1.3B in volume since the start of 2024.

Astroport has been deployed on Terra2, Sei, Neutron, Injective, and Osmosis and is a leading DEX in the Cosmos ecosystem.

In this report, we’ll dive into what makes Astroport special and its unique strategic positioning on various Cosmos blockchains.

Astroport’s Approach to AMMs

Unlike most DEXes, which pivoted to more active forms of liquidity provision such as order books and concentrated liquidity, Astroport focused on optimizing the passive liquidity experience. The team believes passive liquidity provision is a massive and underrated opportunity that not many are considering. Despite the XYK algorithm being viewed as a poor product for passive liquidity, it is still used in Uniswap v2, Pancake Swap, and Sushi, which collectively hold $3.5B in TVL. When you see a flawed product continuing to get traction, it’s a sign that something is interesting there. The team believes that as the algorithms become more efficient, more capital will move to Automated Market Makers (AMMs).

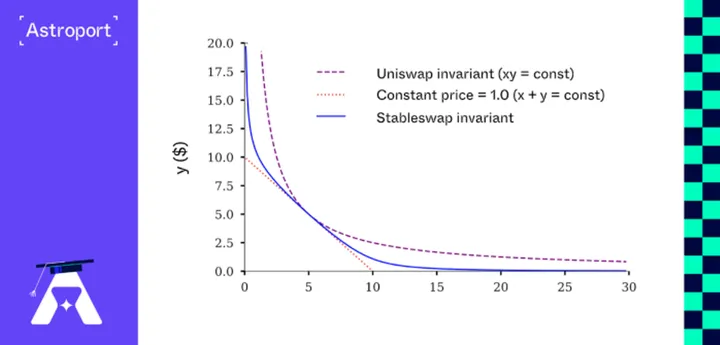

Astroport offers three main AMM designs, allowing liquidity providers to select the model that best aligns with their assets. These AMM designs are XYK, Stableswap, and PCL.

- XYK (purple dotted line): This model represents the classic constant product AMM, akin to the mechanism utilized in Uniswap v2. It is represented by the purple dotted line in the image above.

- Stableswap (blue line): The stableswap AMM design integrates elements of both constant sum AMM and constant product AMM. It uses an amplification parameter (A) that determines how close the stableswap curve should be to the constant product curve. Simply put, if A = 0, it mimics an XYK AMM curve, while higher values of A push the curve closer to a constant sum AMM.

This adjustment in A will significantly influence how assets are swapped, particularly by reducing slippage in transactions for assets that should be in close parity value, such as stablecoins and liquid staking tokens. - Passive Concentrated Liquidity (PCL) is Astroport’s flagship product, which is a concentrated version of XYK with volatility-based fees. PCL utilizes an algorithm to manage concentrated liquidity positions, as explained in the following section.

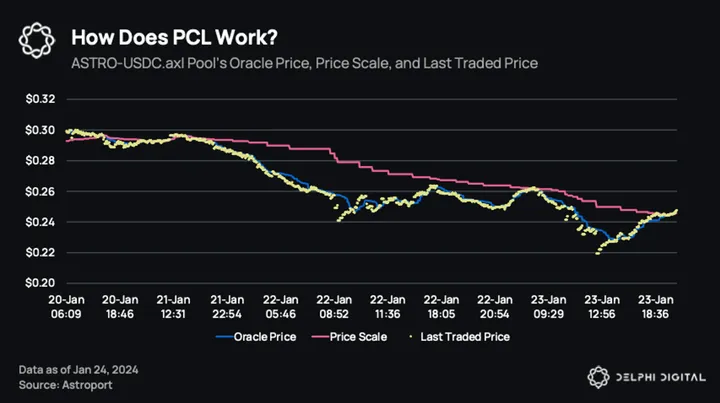

Here are some terms that are needed to understand how the PCL functions.

- Oracle Price (Blue Line): Exponential moving average of the pair’s price

- Price Scale (Pink Line): Where liquidity is maximally concentrated

- Last Traded Price (Yellow Dots): Last traded price that occurred within the pool.

PCL’s algorithm allows passive liquidity to adapt to market conditions, particularly in response to volatility. As the gap between the Price Scale (maximal liquidity concentration) and the Oracle Price (where liquidity is in equilibrium) widens, it indicates increased volatility. PCL pools respond by dynamically adjusting their fee structure. The wider the difference between Price Scale and Oracle Price, the higher the fees. This is akin to traditional market makers who widen bid-ask spreads in volatile markets to generate higher profits.

A key feature of PCL is “Repegging,” which enables pools to adjust their Price Scale (liquidity) with the Oracle Price. This is shown above by the gradual convergence of the Price Scale towards the Oracle Price. How does the pool decide to repeg?

The decision to repeg is contingent on a specific condition: it occurs only if the net gains from accrued fees are sufficient to offset at least half of the potential impermanent loss (IL) resulting from the repegging action. This ensures that each repegging instance partially compensates for any IL incurred, with periods of higher trading volume offering more substantial fee accruals to counterbalance realized IL. During periods of higher volume, more accrued fees can offset the realized IL.

The Power of PCL

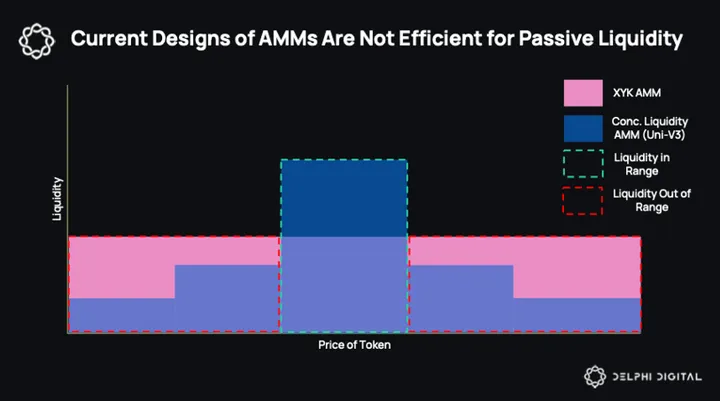

Traditional AMM models are not suitable for passive liquidity, resulting in capital inefficiency, worse trading execution, and the need for sophisticated liquidity provision strategies.

- XYK models are not capital efficient, with liquidity spread over an infinite range. The majority of liquidity is not utilized throughout its lifetime. As seen above, liquidity is spread thinly over every price point, causing trades to incur high slippage.

- Uniswap V3 introduced concentrated liquidity, which boasted higher capital efficiency with higher liquidity concentration where it was most utilized. This however, is an active process where liquidity has to “chase” the liquidity in range to be eligible for fees. This makes providing liquidity an extremely costly and sophisticated process. Furthermore, this is made worse by JIT liquidity, where MEV bots provide front-run liquidity provision for a specific trade and remove it within the same block, siphoning away fees from passive liquidity providers.

PCL’s approach of passive liquidity achieves high capital efficiency and removes the need for active management of liquidity positions. This makes concentrated liquidity provision easy for unsophisticated LPs at the expense of price range flexibility. Furthermore, PCL doesn’t just stop with AMMs, Astroport has been looking to reflect PCL’s liquidity ranges onto orderbooks, thereby capturing another source of order flow and fees for LPs.

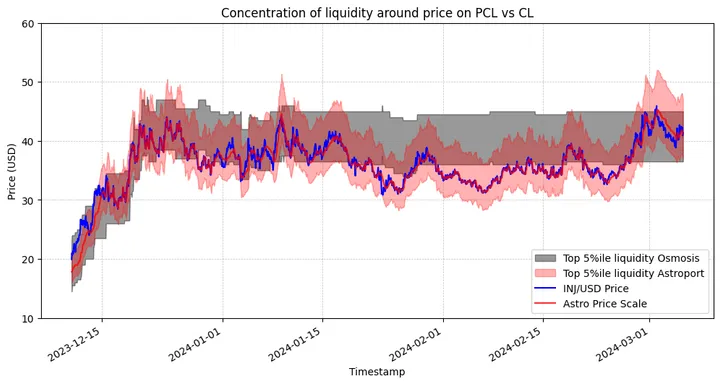

Astroport PCL vs Osmosis CL

In order to show the difference in practice, we compared liquidity concentration between Osmosis concentrated liquidity and Astroport’s PCL pool for the INJ/USD pair. As you can see, top Osmosis liquidity providers are consistently out of range for extended periods while Astroport successfully concentrates liquidity automatically around the spot price. The above graph highlights the imperfect state of liquidity concentration we see on Osmosis often, over the course of >2 months. Meanwhile, Astroport’s PCL pool still effectively re-adjusts with strong price changes, such as the move between $22 – $44.

Another advantage of the PCL design is that it collects more fees than IL losses on adjusting liquidity – the inbuilt market maker is designed to take care of that. In the situation above, the Osmosis LPs would suffer large permanent losses if they were to reconcentrate liquidity around the current price without collecting any fees to offset those losses.

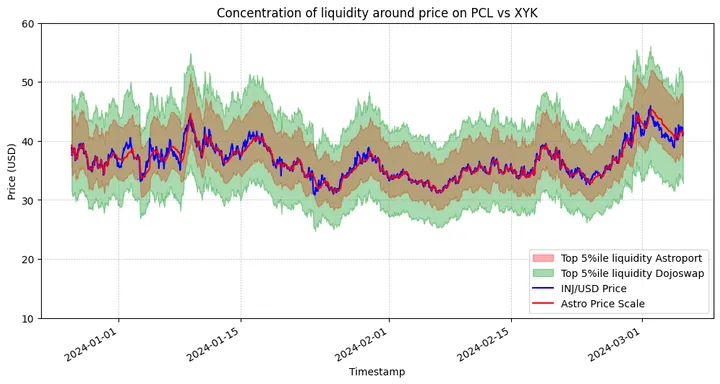

Astroport PCL vs Dojoswap XYK

When comparing Astroport’s PCL pool for the INJ/USD pair against another automated market making model (Dojoswap’s XYK pool), it highlights another large advantage of PCL. PCL pools are designed to concentrate liquidity around the current price rather than passively deploying it across the $0 to $infinity (XYK). In practice, the top 5 percentile liquidity is concentrated as shown above, much tighter than an XYK AMM.

When comparing Astroport’s PCL pool for the INJ/USD pair against another automated market making model (Dojoswap’s XYK pool), it highlights another large advantage of PCL. PCL pools are designed to concentrate liquidity around the current price rather than passively deploying it across the $0 to $infinity (XYK). In practice, the top 5 percentile liquidity is concentrated as shown above, much tighter than an XYK AMM.

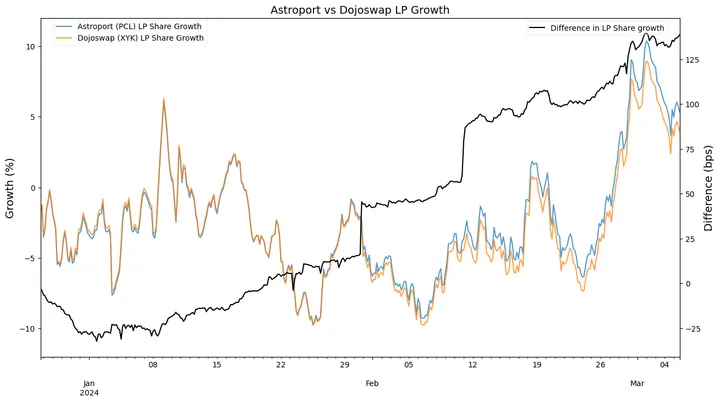

Also remember, aside from automated liquidity concentration, PCL also charges dynamic fees based on volatility, resulting in superior returns for LPs. The chart above compares the value of LP positions (worth one LP share) on PCL and XYK pools of INJ/USD. Naturally, the value of LP positions are subject to the prices of the underlying tokens and fluctuate up or down accordingly. However, over the given time period, the PCL position nearly consistently retains more value than its XYK counterpart. At the end of the analysis period, the PCL position’s growth was 1.35 percentage points higher than the XYK position’s growth. Annualized, that’s a difference of more than 7 percentage points.

Also remember, aside from automated liquidity concentration, PCL also charges dynamic fees based on volatility, resulting in superior returns for LPs. The chart above compares the value of LP positions (worth one LP share) on PCL and XYK pools of INJ/USD. Naturally, the value of LP positions are subject to the prices of the underlying tokens and fluctuate up or down accordingly. However, over the given time period, the PCL position nearly consistently retains more value than its XYK counterpart. At the end of the analysis period, the PCL position’s growth was 1.35 percentage points higher than the XYK position’s growth. Annualized, that’s a difference of more than 7 percentage points.

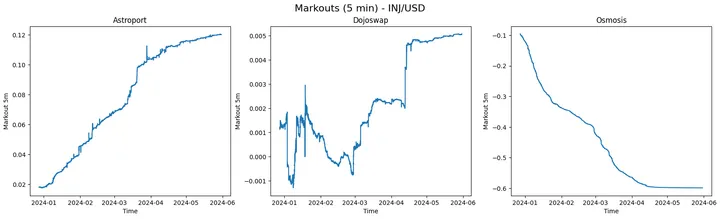

For completeness, it is also important to analyze these pools from the “markout” lens. In market making, markout is a commonly used metric to measure the effectiveness of different strategies. The formula for markout is as follows:

𝑀𝑎𝑟𝑘𝑜𝑢𝑡= ∑ 𝑑. (fair_price_post_5m − execution_price). 𝑞

Where ‘fair_price_post_5m’ is the fair price of the asset 5 mins after the trade. The direction and quantity of the trade are denoted by ‘d’ and ‘q’ respectively. Depending on whether the asset is being bought or sold, ‘d’ takes the value +1 or -1. Finally, ‘execution_price’ is the price at which the trade settles, including fees and market impact. Since the different pools being analyzed have different amounts of liquidity, it makes sense to normalize markouts by liquidity. This approach was also found to be used by Crocswap in their analysis. The results are as seen below.

Ideally, markouts should be positive and show a consistently increasing trend. Since AMMs provide liquidity at stale prices, this is usually not the case. In stark contrast to expectations and consistent with the ideal scenario, Astroport’s INJ/USD PCL pool has a positive and consistently increasing markouts trend. Dojoswap’s markouts dip in the negative, but are mostly pretty close to 0. The same pair on Osmosis’ concentrated liquidity pool has a consistently decreasing trend, completely contrary to the ideal scenario. This can be explained by the fact that Osmosis CL pools have fixed fees and provide good execution (due to concentration of liquidity) at stale prices. This design is advantageous to arbitrageurs and is at the expense of LPs.

Astroport Traction

Astroport commands most of the TVL on Neutron, Terra2 and Sei, and only lags behind on Injective. With the largest TVL, Astroport provides the deepest liquidity, which attracts order flows on those chains.

The only outlier is on Injective, where Helix is the largest DEX. As mentioned above, Astroport has been experimenting with ways to reflect PCL liquidity onto orderbooks, allowing them to tap into Helix’s orderbook flows.

Additionally, Astroport has recently deployed on Osmosis, the DEX chain of Cosmos. Naturally, with both being DEXs, Astroport and Osmosis are often in direct competition. Yet, the Osmosis DAO and their contributors both recognize the distinct value that Astroport’s PCL offering provides over Osmosis’ native active concentrated liquidity pools (which require manual adjustments) and xyk pools (least capital efficient).

Astroport vs Osmosis

When comparing Astroport to Osmosis on adoption metrics, we notice that the gap in TVL doesn’t fluctuate as much as the gap in volumes. During the first half of the last year, Astroport volume surged higher than Osmosis on certain days, despite having a lower TVL. That is not the case anymore, with Osmosis’ volumes being much higher than Astroport. As shown by the markout analysis above, and other AMM research, concentrated liquidity pools don’t have a mechanism to discriminate between informed and uninformed order flow. Therefore, it’s likely that some of Osmosis’ high volume numbers are to the detriment of LPs. In comparison, Astroport’s volumes were 12% of Osmosis’ volumes, while Astroport’s fee returns were 15% of Osmosis’ fee returns.

Looking at protocol fees generated through swaps, Astroport has generated an impressive $2.2M in fees over the past year. Osmosis on the other hand, has generated $10.6M. All of the protocol fees that Astroport generates goes to token stakers, while protocol swap fees that Osmosis generates are partially split between a community pool and token stakers.

Given their relative market capitalizations, ASTRO seems rather undervalued trading at ~$20M, around 6% of Osmosis’s market capitalization while generating 21% of the swap fees. As Astroport cements itself as the go-to DEX on Cosmos through multiple outposts, there is a huge catch-up potential for ASTRO.

All About ASTRO

Astroport’s native token, ASTRO, functions as an equity-like token. ASTRO, by itself, has no utility and is required to be staked into xASTRO for access to Astroport’s governance and participate in fee-sharing.

Astroport mainly generates revenue from swap fees, where the fees earned are used to purchase ASTRO and distributed to xASTRO stakers.

- Constant Product Pools charges a 0.3% fee, 2/3rds (0.2%) goes to LPs, while 1/3rd (0.1%) is distributed to xASTRO stakers.

- Stableswap Pools charges a 0.05% fee, which is split evenly between LPs and xASTRO stakers.

- PCL Pools distributes 50% of fees earned towards xASTRO stakers.

Furthermore, Terra enabled the fee-sharing module, which is distributed towards the xASTRO staking pool.

As volume rose, xASTRO’s fee earned propelled from ~$50K per week in Oct-Nov, 2023 to peaks of $293K per week as trading volume ramped up.

This is spurred by new outposts on Injective and Sei, which drove new volume. Over the past year, $2.2M of fees has been earned and distributed towards xASTRO stakers. Most of the fees have been generated from Oct 2023 to Jan 2024, amounting to $1.19M of fees earned over that period.

vxASTRO 2.0 to Restart ASTRO Wars

vxASTRO 1.0 was initially inspired by Curve’s veCRV, where locked veCRV has the voting power to direct emissions towards their intended pools. vxASTRO 2.0 will introduce a few modifications and features:

- Locking Process: ASTRO can be staked into xASTRO, then locked for vxASTRO

- Flexible Unlocking: vxASTRO will have an indefinite lock period, with users able to unlock at any time with a 2-week unlocking period

- Governance Equality: xASTRO and vxASTRO 2.0 will have the same voting power on governance proposals.

- For clarity, the initial vxASTRO 1.0 proposal had a time-based boosting for emissions and governance powers but is now removed in vxASTRO 2.0. The removal of excessive time locks and boosted governance powers reduce the centralization of Astroport.

- Emission Direction: vxASTRO will be used mainly for directing ASTRO emissions towards desired liquidity pools.

- “Tributes” Protocol: Similar to Curve’s bribes for emission voting through Votium, Astroport will have a “tributes” protocol that allows anyone to incentivize emissions to liquidity pools by paying “tributes” to voters who vote for a specific pool.

The main difference between Astro Wars and Curve Wars is that CRV demand was largely led by decentralized stablecoins where bootstrapping liquidity was key. With very few decentralized stablecoins still around participating in the Curve Wars, demand has dwindled significantly.

Astro Wars differs by having L1s compete against each other to fight for liquidity for core Cosmos assets, especially for core Cosmos L1 tokens like ATOM, TIA NTRN, INJ, SEI, etc. Assuming Astroport is the best place for passive liquidity providers, it will also be a battleground for the fight for passive liquidity in Cosmos. This could be a more sustainable long-term source of demand compared to Curve.

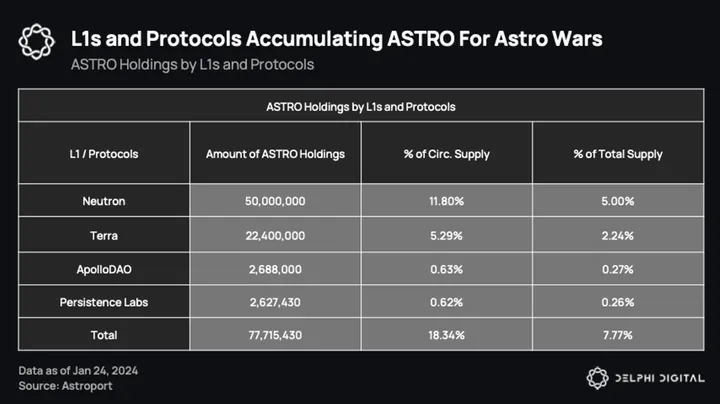

Ahead of the vxASTRO launch, several L1s and protocols have strategically accumulated ASTRO tokens, positioning themselves for participation in the upcoming ASTRO wars. Key accumulators include:

- Neutron: Acquired 50M ASTRO.

- Terra: Secured 22.4M ASTRO. It’s unclear what the status of this ASTRO is given the recently announced TFL bankruptcy.

- Persistence Labs: Purchased approximately 2.6M ASTRO through an over-the-counter (OTC) deal.

- ApolloDAO: Accumulated ~2.7M ASTRO via open market purchases and previous holdings.

Collectively, these entities hold 18.34% of the circulating ASTRO supply, a substantial stake that underscores their commitment to participating in the ASTRO Wars and competing for ASTRO emissions.

This accumulation is a prelude to the launch of vxASTRO, which will enable L1s and protocols to direct ASTRO emissions toward their preferred liquidity pools. This capability is crucial for enhancing LP yields and bolstering liquidity for their chosen trading pairs. Moreover, by holding ASTRO, these entities demonstrate a vested interest in Astroport’s success, making them more likely to deploy liquidity on Astroport as opposed to other DEXs.

With Astroport positioning itself on four different blockchains (with more coming), demand for ASTRO will span across Cosmos ecosystems, with L1s and protocols fighting for emissions.

Will ASTRO Wars Lead to a Supply Shock?

Astroport has managed to gain a significant amount of xASTRO stakers, with ~43% of circulating ASTRO currently staked. With vxASTRO likely to come soon, most of these xASTRO could be locked, effectively reducing the actual circulating supply.

Furthermore, Astro wars can increase ASTRO demand, potentially leading to a supply-side liquidity crisis as most ASTRO are staked as vxASTRO, with little left unstaked.

The supply of ASTRO will also be rather stable as Astroport reduced ASTRO emissions to LPs. At the current emissions rate, ASTRO only inflates by ~3.2% annually.

Astroport, The Index bet on Cosmos Success

When L1 tokens perform well, a common approach to its beta would be to look into the L1’s DeFi tokens when going down the risk curve. ASTRO’s distinct advantage lies in its role as the leading liquidity hub, not just for one but for five different L1 blockchains. As Astroport continues to expand its presence across the Cosmos, the strategic significance and potential demand of ASTRO will correspondingly increase.

The remarkable growth of ASTRO prices is notably a result of its presence on multiple burgeoning L1s, particularly NTRN, SEI, INJ, LUNA, and OSMO.

In the last 8 months, ASTRO’s price escalated by ~300%, significantly outperforming the performance of NTRN, LUNA, OSMO, and INJ, which ranged between 45% – 180%. ASTRO is in an extremely favorable position to capitalize on the growth alongside L1s that Astroport has deployed.

Other Passive LPing Models

Similar to PCL and CPMM designs, some new AMM designs enable LPs to provide liquidity passively, but with added features like hyper-concentration of liquidity and orderbook integrations. Naturally, architecturally and mechanically, these designs are very different from the AMMs that are currently ubiquitous.

Lifinity

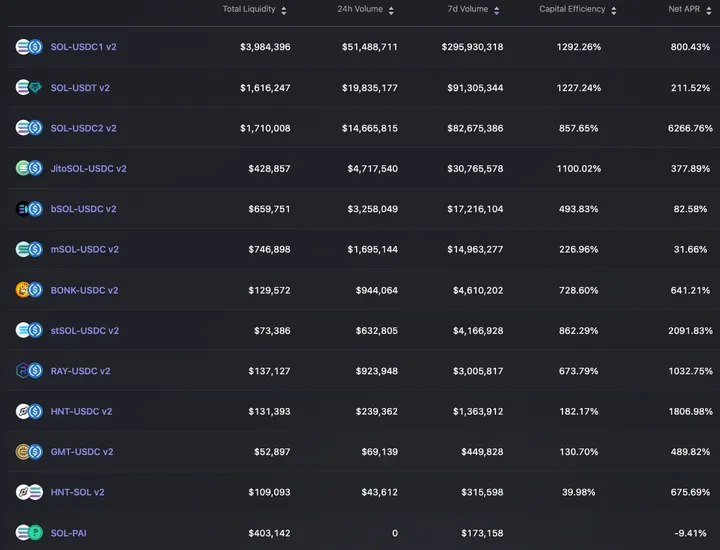

Lifinity allows passive liquidity provision, while still affording the greater returns of active liquidity management. They very accurately describe their DEX as a “proactive market maker”. Lifinity enables the passive liquidity experience and great returns by using their closed-source market making algorithm in the backend. Top pools on Lifinity are SOL or SOL derivatives paired with stables, BONK, RAY, etc., as shown below.

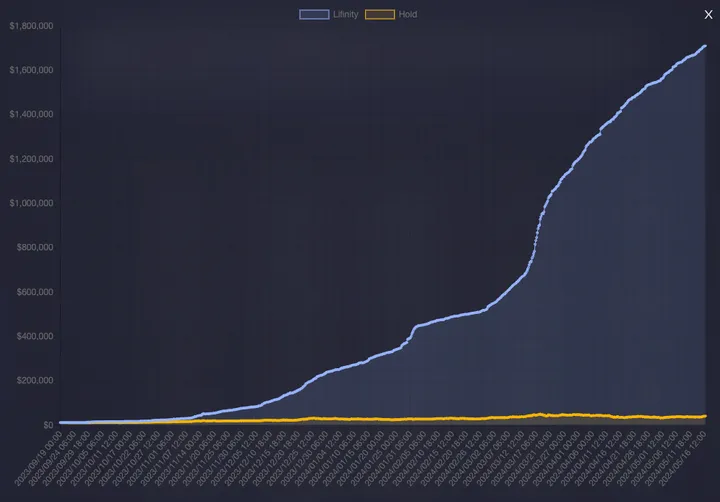

While walled gardens are typically looked down upon in crypto, Lifinity cannot come close to offering triple and quadruple digit APRs without having alpha, and naturally, they’’re secretive about it. That said, a key reason behind Lifinity’s success is avoiding toxic order flow with the help of oracles to price assets in the pool. To give a quick refresher on toxic order flow in the context of AMMs, this refers to the losses incurred by LPs by providing liquidity at stale prices to arbitrageurs – also known as IL and LVR. To give context on LP returns on Lifinity, the following stats on the Lifinity frontend compare Lifinity’s returns compared to a 50/50 portfolio held from September 2023 for the pair listed “SOL-USDC2 – v2”. A “hold” portfolio would have returned an impressive 334% from start to peak, but Lifinity made an astronomical 14769% in the same time frame.

While walled gardens are typically looked down upon in crypto, Lifinity cannot come close to offering triple and quadruple digit APRs without having alpha, and naturally, they’’re secretive about it. That said, a key reason behind Lifinity’s success is avoiding toxic order flow with the help of oracles to price assets in the pool. To give a quick refresher on toxic order flow in the context of AMMs, this refers to the losses incurred by LPs by providing liquidity at stale prices to arbitrageurs – also known as IL and LVR. To give context on LP returns on Lifinity, the following stats on the Lifinity frontend compare Lifinity’s returns compared to a 50/50 portfolio held from September 2023 for the pair listed “SOL-USDC2 – v2”. A “hold” portfolio would have returned an impressive 334% from start to peak, but Lifinity made an astronomical 14769% in the same time frame.

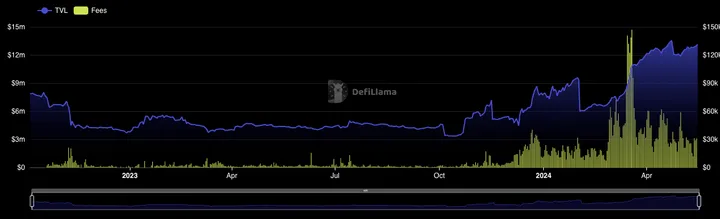

This superior performance is reflected at a protocol level, with annualized fee revenues standing at ~$11.78m for a TVL of $13.13m (source and more charts on DefiLlama)

This superior performance is reflected at a protocol level, with annualized fee revenues standing at ~$11.78m for a TVL of $13.13m (source and more charts on DefiLlama)

Elixir

With orderbook DEXs becoming popular, Elixir saw a problem and an opportunity. Orderbook exchanges, CEX or DEX, rely on market makers to provide liquidity to takers. For large cap tokens with high liquidity, market makers are naturally incentivized to participate because there is a constant demand for liquidity. For mid caps and especially low caps, the incentive for market makers to get involved is not always clear, which results in market making firms requiring an extra fee for their services. This could be in the form of tokens, cash, with vesting schedules, and other terms and conditions. Naturally, this requires a fair bit of administrative work and legal help as well. This is the problem that Elixir is created to solve; the problem of liquidity provision on orderbook DEXs. As of today, LPs can deposit liquidity to orderbook DEXs like Bluefin, Vertex, and RabbitX.

The liquidity supplied through Elixir is deployed on the orderbook DEX based on the popular Avellaneda & Stoikov market making algorithm. This market making algorithm is described as the orderbook equivalent of Uniswap V2’s CPMM (XYK AMM) since it has a very similar risk/return profile. This algorithm takes into account many parameters, such as current price, current and target inventory, volatility, orderbook density, etc., to come up with the optimal reserve price (reference price to which bid-ask spread is added) and magnitude of the bid-ask spread.

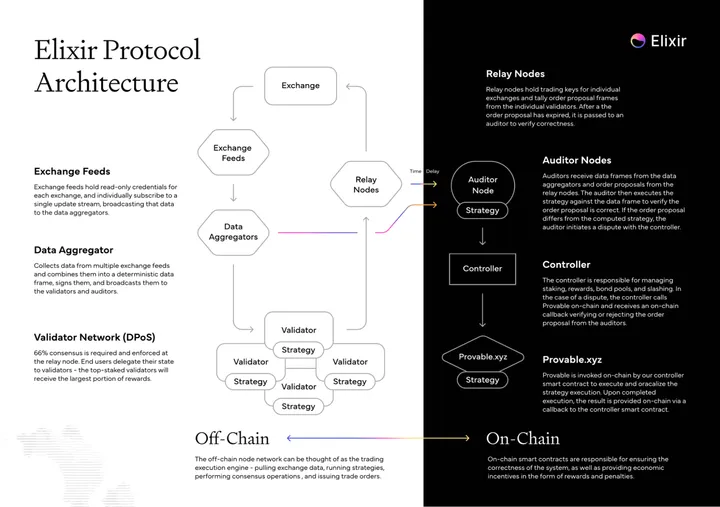

In order to be trustless and decentralized, they employ a network of data aggregators, validators, auditors, etc. to ingest live orderbooks and supply liquidity in a secure way. The network uses DPoS to reach consensus on blocks. The architecture is illustrated by the following infographic.

Conclusion

Astroport’s resurgence following Terra’s collapse exemplifies remarkable resilience and adaptability. Their strategic decision to establish a presence on multiple Cosmos blockchains has progressively positioned it as a central liquidity hub. With their PCL AMM, they can attract capital-efficient passive liquidity and compete effectively against Osmosis with lower TVL.

vxASTRO will be a key tailwind, restarting Astro Wars and creating a strong demand for ASTRO. vxASTRO will be required to vote for emissions to incentivize and attract deep liquidity. If an L1 or a protocol wants to leverage Astroport for deep liquidity, they must acquire ASTRO. This can be done through open market purchases, OTC deals, or token swaps with Astroport.

With Astro Wars, demand for ASTRO will be a key indicator to look out for once the flywheel kickstart. If the demand for liquidity on Astroport is high, it could lead to a supply shock on ASTRO as L1s and protocols fight for vote emissions. Furthermore, Astroport’s “Tributes” protocol will generate an additional income stream for its emission voters.

Astroport’s strategic maneuvers extend beyond liquidity provision; it is poised to become an index bet on various L1s where outposts are deployed. Through token swap agreements, various L1s can acquire stakes in ASTRO tokens, having vested interest in Astroport’s success. Such agreements solidify Astroport’s position within these ecosystems and elevate the entry barriers for potential competitors, further cementing its role as a dominant DEX where it is deployed.

0 Comments