Report Summary

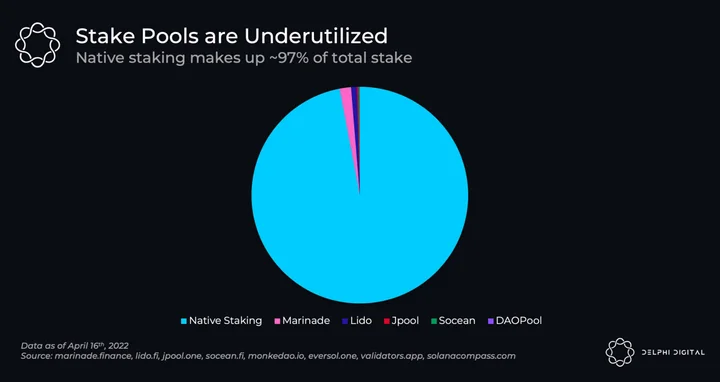

Staking on Solana generates ~$2.1B of rewards per year. Liquid staking protocols currently only capture ~3% of that, meaning there is clearly an opportunity for growth. For context, Lido alone is 28% of total stake on ETH2.0.

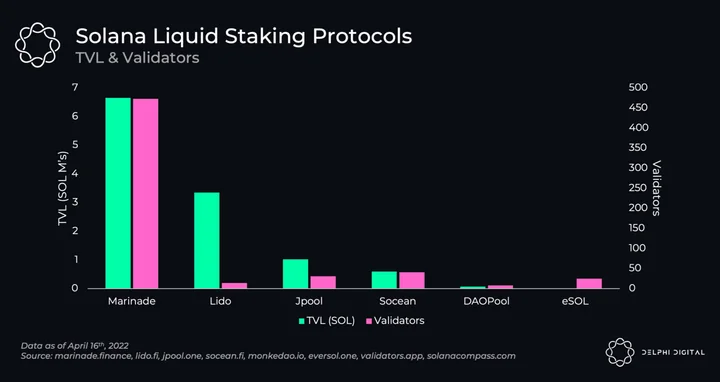

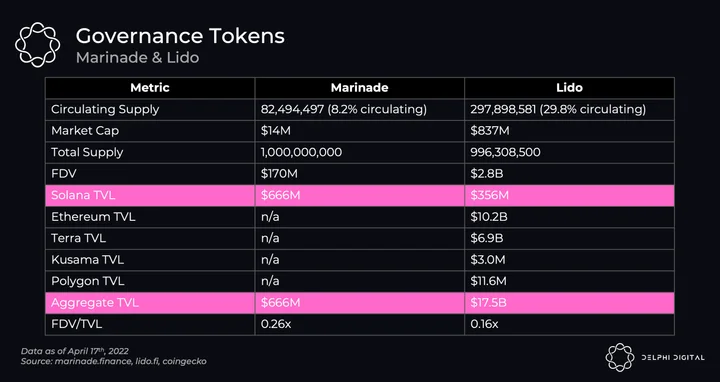

Marinade has a 57% market share, Lido 29%, and the rest combine for 14%.

All liquid staking protocols have different strategies, with Marinade focusing on decentralization, Lido on market leading validators & multi-chain, JPool the highest APY, Socean with protocol owned liquidity & Socean Streams, DAOPool with new ecosystem validators, and eSOL with the goal of funding ecosystem projects

Marinade is integrated everywhere, Lido a close second, and Socean a more distant third. Lido is the first for a cross-chain (Terra Anchor protocol) integration.

Power laws would lead us to expect a few winners in the long-term.

Introduction

Staking is one of the largest and fastest growing industries in crypto, but most staking solutions today have a glaring problem: they’re not built for DeFi.

As a refresher, for a Proof-of Stake blockchain like Solana, consensus is achieved by validators running hardware and locking up SOL collateral to secure the network. In return for securing the network, validators earn ~6.5% inflationary rewards (started at 8% last year) which will be decreased at a rate of 15% YoY until a terminal rate of ~1.5%. Validators also earn transaction fees, which for now are low, but can potentially be lucrative as Solana continues to grow and the new priority-fee model is implemented. At a core protocol level, users can either stake themselves or delegate their tokens to a validator of their choice. Due to the costs & effort of running a validator (~50,000 SOL/$5M delegated stake to break-even), many users choose to delegate their SOL. While delegating SOL to a validator allows users to avoid getting diluted through inflation, it has some drawbacks, namely:

- SOL is locked and requires a cooldown period of 2-3 days

- User overhead of researching/choosing validator(s)

- Cannot use staked SOL as collateral throughout DeFi

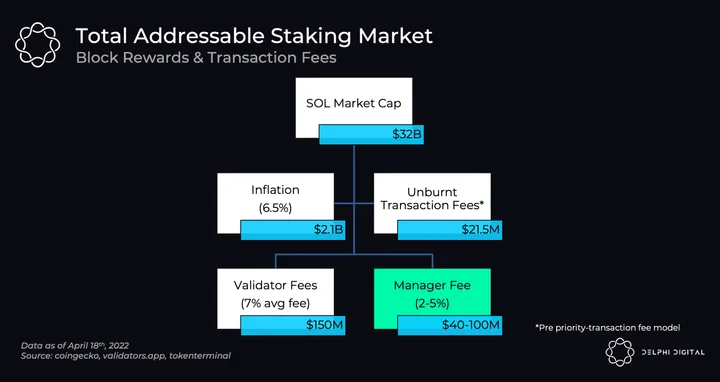

At a $32B market cap and 6.5% inflation rate, there are ~ $2.1B in rewards/year going to validators for Solana. Liquid staking protocols could extract 2-5% on those rewards through manager fees, a $40-100M revenue opportunity today.

Liquid Staking Ecosystem on Solana

Given Solana’s focus on DeFi from the outset, it was natural that liquid staking tokens would be a key area of development. So, what are liquid staking tokens? Simply put, they are a derivative token of the native asset (SOL) which earns staking rewards but is not locked-up. This allows a user to use their SOL in DeFi applications without giving up the opportunity cost of staking rewards. In an ecosystem without liquid staking, the return one must earn on the native (unstaked) asset must be greater than the rewards from staking, which can be seen as a blockchain’s native risk-free rate. For example, if a lending protocol offers a 4% yield on SOL, it does not make sense for someone to lend their SOL instead of earning 6.5% through native staking.

Along with benefits to the user, there are also benefits to the network itself. First, liquid staking tokens will delegate to numerous validators to diversify/decentralize network stake, and second, by opening up the native token as collateral it helps grow and create activity in the ecosystem which compounds over time. On Ethereum, Lido dominates the liquid staking landscape with a >85% share today. In the long run, we would expect dominant liquid staking tokens to emerge, as the more liquidity and use they have in an ecosystem, the more valuable they become. It is a reflexive flywheel effect that grows stronger the further ahead a protocol separates. However, the race on Solana is not so clear, and as a new ecosystem the position for a dominant liquid staking platform has not been decided. As of April 16th, the Solana liquid staking landscape is as follows:

At first glance of the landscape, it may look like Marinade has run away with the ecosystem. Part of this is true! Marinade is roughly double the size of Lido, by far the most decentralized with over 400 validators, and has become a staple in Solana DeFi since its launch last summer. However…

Stake pools make up a very small amount of the total stake on Solana today! For all the benefits that stake pools have, they have still not been adopted at a fast rate on Solana. As a comparison, Lido with ~$10B on ETH 2.0 is already 3% of Ethereum’s total market cap and 28% of the total stake on ETH 2.0. Liquid staking on ETH 2.0 makes up ~32% of stake, a much higher ratio than we see on Solana.

There are a few reasons for this dynamic.

- ETH 2.0 deposits opened at the end of 2020, Liquid staking on Solana launched in Summer 2021

- Staking on ETH 2.0 requires technical knowledge vs delegating on Solana. If an Ethereum user wants to earn ETH 2.0 yields they will need to run a node themselves or use a pool. On Solana it is a simple process to delegate to a validator. Ethereum does not have delegated proof of stake, but you can think of stake pools as similar to delegating stake (if the market demands something it will find a way to create it)

- ETH 2.0 staking is locked, Lido unlocks it

In addition to the above, there are some other reasons that are not specific to Solana.

- Smart contract risk

- Potential tax liabilities

The first one is fairly self-explanatory. Depositing SOL to a smart contract adds a non-zero risk of a smart contract bug that native staking does not have. In fact, we have a recent example of this, an unstaking error with Marinade in March that led to the unstaking of nearly all the SOL delegated to them. Per the incident report, “On March 02, 2022 (epoch 284), a series of cascade failures in the automated scoring mechanism happened that caused almost all validators to get a score of zero, that in turn caused an emergency unstake of almost 6M SOL of Marinade stake. At no point there were funds at risk. Since no funds were at risk, we decided to address issues in our own off-chain scoring code and then to restake to more than 450 validators, as we normally would according to the delegation formula during epoch 285.” While no funds were at risk, there was a missed staking epoch that amounted to ~2.5K SOL rewards. On a positive note, it highlighted a dependency on StakeView which has been removed and an error with the emergency brake function, but still, the episode highlights how liquid staking adds risk that native staking does not have.

The second is a bit more nuanced but still relevant. With the run-up in price last year, a lot of Solana investors are sitting on large capital gains, and some jurisdictions may treat depositing SOL to a stake pool (and thus getting another token like mSOL in return) a taxable transaction. Because of this dynamic, a lot of large SOL investors have chosen not to deposit to stake pools. For all the benefits stake pools hold, the potential tax liability would outweigh them. Recently, Marinade has created a new product called “The Decentralizer” to address these two issues. This is a public good that creates no revenue for the Marinade DAO but allows users to delegate their stake to numerous validators without giving up custody of their SOL. Users (and the network) will be able to get the benefit of diversification/decentralization but will not be able to get the DeFi benefits of the liquid token mSOL.

Stake Pool Strategies

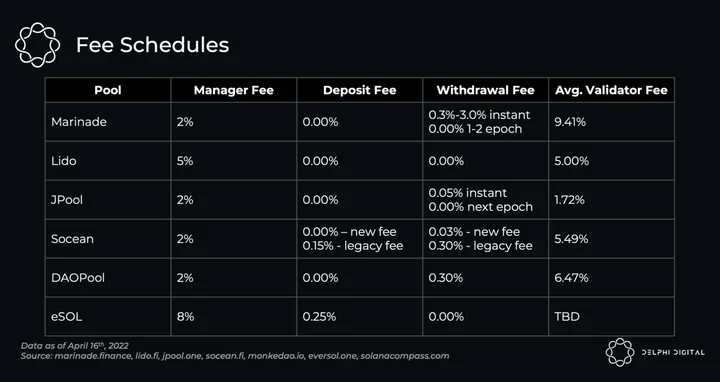

As noted above, one of the core benefits of liquid staking is to diversify validator exposure. This is beneficial to the user as they are not reliant on a single validator and risk having funds slashed due to malicious behavior (note: slashing is not yet implemented in Solana). When a user’s stake is delegated to multiple validators, the risk of loss from slashing is minimized. From an ecosystem perspective, liquid staking helps decentralize the network as user deposits are automatically spread across validators, which helps raise the Nakamoto Coefficient (number of validators that can collude to compromise the network). Each liquid staking token on Solana takes a different approach to this. Along with different stake strategies they have varying fee schedules as outlined below.

Manager Fee – fee paid on rewards, sent to DAO treasury or used for OPEX

Deposit Fee – fee paid on entire balance when depositing

Withdrawal Fee – fee paid on entire balance when withdrawing

Avg. Validator Fee – weighted average fee paid to validators on rewards

Marinade is the first liquid staking token to launch on Solana with the largest $ staked and >8x the number of validators than the next (Socean). Marinade follows a strategy outlined from the Solana Foundation to “spread the stake among the long tail of high-performance, low-commission, non-concentrated validators”. This results in Marinade not delegating to the largest validators and instead to many small to medium ones, directly improving distribution of stake in the ecosystem. Lido, in contrast, delegates to mostly well-known, large professional partners that have been vetted through a rigorous application process, the majority of which overlap with their Ethereum partners. These are some of the largest validators on Solana, including Everstake (#1 validator), Chorus One (#2), Staking Facilities (#4), Figment (#10), and more. Lido validates this stake equally across all of their validators (~150k SOL to each currently). Again, this contrasts from Marinade as, since they support small validators, delegate using a formula and vary stake with different weights. In addition, Marinade allows active stakes to be transferred to them for mSOL, and if a user delegates an active stake account from a validator in the minimum security group (largest validators that can halt network), Marinade will slowly un-delegate to other validators over a few epoch’s, depending on the size staked. Marinade and Lido control a combined 86% of stake pools, but the others are still worth highlighting as this ecosystem is new and some have recently just launched.

JPool is the fastest growing alternative out of the top two, having launched in late October and the #3 pool by TVL, surpassing Socean which launched in September (Socean is more integrated in the eco, however). JPool’s approach is to delegate to the lowest fee/highest APY validators with a few conditions (must be outside top 20, must have website/logo, must be active for at least 10 epoch’s). This aggressive strategy has led to JPool having the highest APY of all the stake pools. While JPool has the highest rewards, they have not been integrated into the ecosystem as of yet. Socean is the 4th largest stake pool and would be considered in the second tier along with JPool. Their strategy is similar to Marinade in that they do not delegate to the minimum security group or minimal data center security group, however choose a lower amount of validators with higher rewards/lower fees as opposed to Marinade’s focus on maximizing decentralization. They have just recently significantly cut their deposit and withdrawal fees as an attempt to gain more deposits. Low fees are a way for newer protocols to try and gain market share as it is challenging to compete with the more established, liquid protocols when starting from behind. This gives Marinade and Lido pricing power the further they separate from the rest. Socean does try to differentiate besides fees with their Socean Streams product and will be touched on later in this report.

The final two are DAOPool and eSOL. DAOPool is the most unique stake pool to launch as it was created by MonkeDAO, a DAO formed around the NFT project Solana Monkey Business. DAOPool is unique in that it only delegates and supports other NFT projects that run validators. Today, it is the least decentralized as the stake is split between 8 validators. MonkeDAO, Degen Ape Academy & Thugbirdz are the largest validators in the pool and the original three. DAOPool has gained traction due to the influence MonkeDAO has in the Solana community and going aggressive in the Saber/Sunny wars, with 27% of daoSOL in the Saber pool, becoming the third largest Saber liquid staking pool at $5M, behind Lido at $28M and Marinade at $30M. However, this is down from 98% of the supply and $19M two months ago, as the “Saber Wars” have not reached the same success as the Curve Wars on Ethereum or even the Platypus Wars on Avalanche. Due to Solana’s architecture there is more competition with AMM’s and we are seeing a lot of concentrated and even proactive ones pop up that handle more volume with less liquidity. It is likely that the market making landscape on Solana ends up much different than the EVM chains, but that is a topic outside this scope. DAOPool has started focusing outside of Saber as they look to expand, recently testing out Raydium and in discussions with Mango to become collateral in the second half of the year. DAOPool will not be the fastest grower, but is in its own niche within the Solana NFT community, and are starting to onboard new validators outside the NFT community as well. Lastly we have eSOL which is run by Everstake, the largest validator on Solana. While developed by Everstake, eSOL selects 25 validators by APY outside of the top 25 with fees <7%. They have a higher manager fee than the others which the DAO will use to invest in projects across the ecosystem. While recently new, eSOL has not gained traction yet with just $45K SOL staked, highlighting some of the challenges of being a late mover in liquid staking.

Honorable mention: aSOL is a second derivative token launched in October 2021 which takes Lido stSOL and/or Marinade mSOL to mint aSOL. It positions itself as an unbiased stake pool aggregator, the thesis being that with many stake pools, users will want a token that aggregates them all. With $750K TVL today it has not gained much traction.

Liquid Staking in DeFi

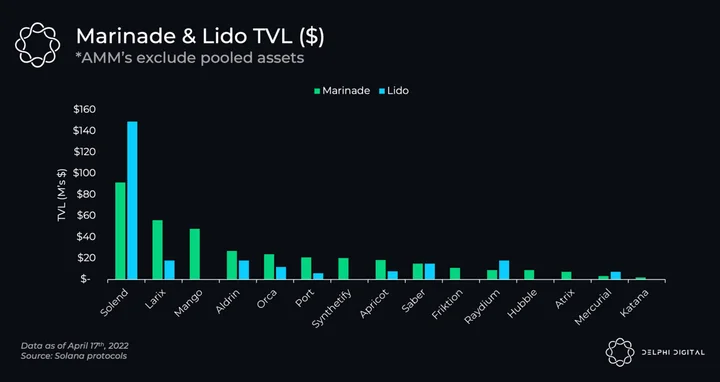

Most important besides stake pool strategy & fees (and arguably most important) is how well integrated a stake pool token is within DeFi. As stake pools are capital efficient derivatives of the underlying, if one were to just hold it in their wallet they would not see much of a difference compared to self-delegating outside of diversification. Liquidity and composability are the other main selling features to users, and more liquidity begets more liquidity. As the first main liquid staking token launched (and native to Solana), mSOL (Marinade) has the most DeFi integrations in the ecosystem, being onboarded to every major lending & AMM platform, plus option vaults, derivative platforms, and the only one accepted as collateral to mint USDH, a relatively new over-collateralized stablecoin by Hubble. Note that the chart above only includes material and/or incentivized pools for AMM’s (Saber, Raydium, Orca, Atrix, Aldrin). As they are permissionless a pool could be created at any time. Protocols that use the tokens as collateral (the main use-case of liquid staking) have a more diligent onboarding process.

Lido is in a similar spot to Marinade, albeit with a few less integrations so far. Moving forward, one would expect Lido’s stSOL to continue being onboarded at a pace similar to Marinade’s mSOL due to its reputation across crypto and having key Solana partners like Alameda Research and Jump Crypto as investors. One notable protocol to highlight for Lido is Anchor, a protocol on a different blockchain, Terra. Anchor has already onboarded Lido for bLUNA and bETH, and stLUNA is used in the Terra ecosystem on protocols like Astroport and Mars. Recently, a proposal has been made to onboard bSOL to Anchor which will use Lido to bridge SOL from Solana to Terra through the Portal/Wormhole bridge, a Jump Crypto incubation. Integrations like this highlight that while Marinade may be the most liquid and first to integrate on Solana, Lido’s multi-chain strategy opens up more possibilities due to their relations with other chains.

Analyzing the top protocols, it becomes clear the level of preference mSOL has in the Solana ecosystem, with Lido a close second. The other protocols have been left out of the chart above due to their size at this stage, although it should be noted that scnSOL (Socean) has the third most integrations, with $12M on Solend and $4M on Orca. Liquidity pools are of utmost importance when underwriting collateral and is one of the main reasons mSOL and stSOL are accepted virtually everywhere. mSOL has a few more integrations than stSOL like Mango, Synthetify and Hubble, but are for the most part both integrated into the major protocols, which cannot be said the same for others. Over time if the other stake pools keep growing they should be onboarded to more, but Marinade and Lido have large head starts. This lead allows them to compound faster, being preferred collateral for protocols to onboard as they are deemed less risky due to their liquidity, lindyness and larger holder base.

As stated prior, Socean is the third most integrated token in the ecosystem. They are taking a different approach to liquidity than the others as they have not been paying for liquidity (Marinade incentivizes use with MNDE, Lido with LDO) but rather take a protocol owned liquidity approach popularized by OlympusDAO and have created a separate product for the ecosystem to use, Socean Streams. The Socean Streams product launched on February 14th, a product not just for Socean, but one used for other protocols across the Solana ecosystem. Streams allows ecosystem partners to sell locked/vesting tokens to raise capital. Early partners have been UXD Protocol, Port Finance, Atlas DEX, and a few others which have used streams to raise $0.5M in the first two months. UXD used streams to acquire SBR to incentivize their Saber pool, Atlas DEX used streams to have their airdrop unlock linearly over 6 months, and Port Finance used it to purchase protocol owned liquidity. Streams is unique in that it allows protocols to sell their tokens to more long-term oriented partners than your typical IDO and are flexible in what the protocol wants to use it for. Continued usage of Streams will get Socean goodwill across the ecosystem and build a larger partner base, potentially leading to more integrations in the future. While Socean is behind Lido and Marinade today, the continued adoption of Streams and their upcoming IDO could be a catalyst to close that gap and make them a more serious contender in the ecosystem.

Marinade & Lido Valuations

While TVL is an overused and usually poor valuation metric in crypto (for an AMM we don’t want to know TVL, but Volume/TVL, or even just Volume), it is the most important one for liquid staking. The #1 goal for liquid staking protocols is to grow TVL and become ingrained throughout the ecosystem as fast (and safely) as possible. The winners here will have a substantial revenue stream to extract value from. As highlighted at the beginning of this report, there are approximately $2.1B of capturable fees on Solana today, of which only $60M (3%) are being captured by liquid staking protocols.

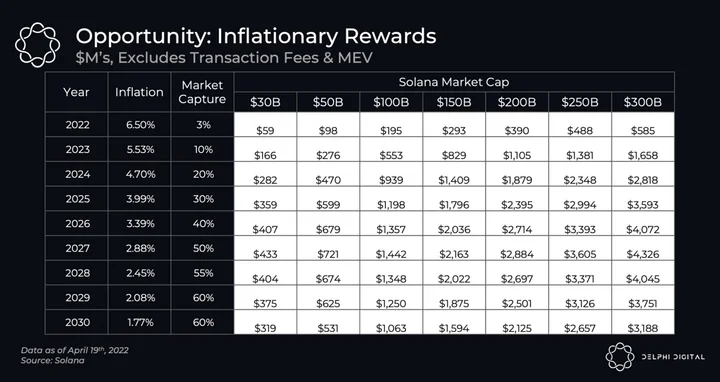

If we isolate inflationary rewards the potential revenue opportunity for these protocols is in the multi-billions assuming 1) their market capture increases, and 2) Solana continues to grow. Earning a 2-5% manager fee on $2B rewards (the total approximate rewards on Solana today) would be $40-100M in annual income. In addition to inflation, validators earn transaction fees and MEV. Today, Solana’s annualized transaction fee revenue that is unburnt (Solana burns 50% of fees) is ~$22M. Under development is a priority-transaction fee model that will allow for increased fees on high demand accounts. This fee market will look a bit different than what we typically see. For comparison, the way Ethereum’s fee market works is that fees for everyone increase evenly. Solana will be taking a different approach, targeting specific apps. This would be like increasing fees for OpenSea users but not Uniswap users. Once the new fee market is launched it will open the doors to MEV. In the long-run, most income for validators will not be from token inflation but rather transaction fees and MEV. Due to this upcoming fee market change and the unknowns that surround it, it is not appropriate to try and estimate potential fee income for validators at this time, but will be a major component over the coming years. While Solana still aims to be cheap for most users, the new fee market and MEV that comes with it could become lucrative.

To finish off it is worth highlighting what Marinade has done for their governance token. As of April 4th, in order to vote in the DAO you will need a Marinade “Chef” NFT. 3,333 limited edition Octopus NFT’s were made available for mint (~2,000 left today). Once the limited editions are sold out users will be able to mint regular editions which are uncapped. These require locking the governance token MNDE for 30 days and come in 5 levels plus rarities. Outside of rarities that could change values, the NFT’s will always be able to be redeemed for the MNDE backing them with a 30 day cooldown, or sold on NFT marketplaces. It’s a combination of a governance token, a vote-locked (ve) token, and an NFT.

Final Thoughts

Liquid staking protocols are a vital building block/lego of Proof-of-Stake networks. Over time, we would expect a winner-take-most outcome with a few protocols obtaining all of the liquidity. There is a significant flywheel effect as liquidity compounds for these protocols as they become more integrated (“lego-fied”) in the ecosystem and are used as intertwined blocks. Once protocols start composing with and building on top of each other it is nearly impossible to remove the glue. These tokens have their own lindy effect and are hard to overcome once a lead has been built.

Marinade is the clear leader in the Solana ecosystem today with Lido second, but it is still early as only 3% of the TAM has been captured. Socean, JPool, and more recently DAOPool and eSOL are all coming with unique strategies that may allow them to gain market share in the coming year, but it will be an uphill battle trying to catch up to the lead Marinade and Lido have built.

0 Comments