Report Summary

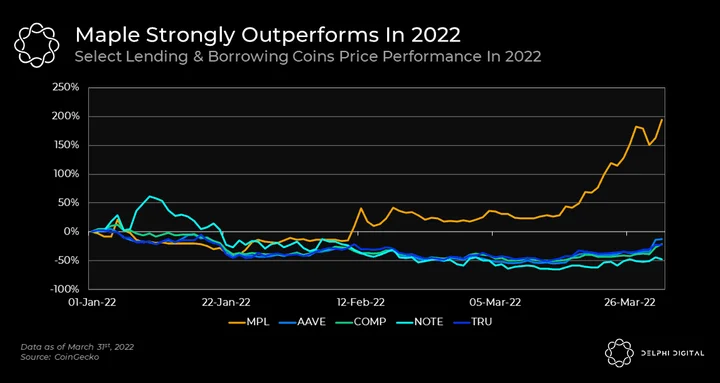

Maple Finance looks to tackle under-collateralized lending within crypto. Its growth has been impressive, funding over $580M in loans during Q1 2022 and aiming to achieve $5B in originations by the end of the year. It’s native token, MPL, has also performed extremely well, up nearly 200% since the start of the year.

Maple facilitates undercollateralized loans via its pool delegate model. These delegates are reputable trading firms such as Alameda, Maven 11, and Orthogonal Trading that manage lending pools. Delegates onboard trusted borrowers and negotiate loan terms. From here, lenders can then deposit into lending pools of their choice to earn yield and MPL token rewards.

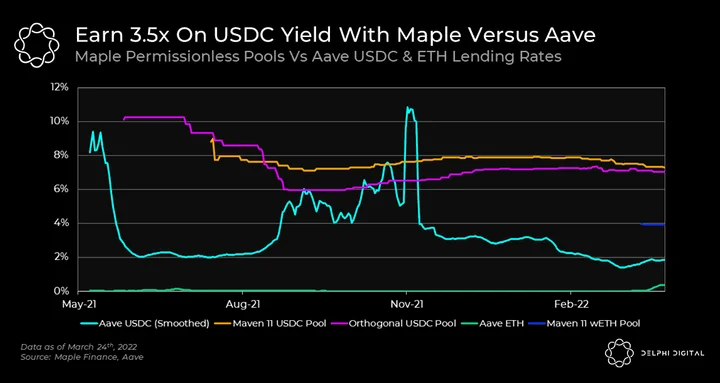

Borrowers are currently paying ~9% for USDC loans on Maple versus 3% on Aave. Although these rates are more expensive, they are stable and don’t require any capital down. This makes loans on Maple attractive for businesses that need cash to grow. Lenders can earn nearly 7% by depositing to USDC pools (+6-10% in MPL tokens) which is significantly better than Aave supply rates at 2%. These rates are sustainable and much higher than Aave but do come with added risks of potential default by borrowers.

xMPL holders directly benefit from the duration and amount of loans funded on the platform. Maple is targeting $5B in originations by the end of the year which would send ~$8.4M in earnings to xMPL holders. This represents a ~25X P/E on MPL circulating supply, and is quite reasonable considering the speed of its growth and potential to scale with the delegate model.

Introduction

Undercollateralized lending makes up less than 5% of the $50B in total value locked across crypto money markets. In traditional finance, the vast majority of credit is extended in an uncollateralized or under-collateralized fashion, allowing companies and individuals access to efficient debt financing. The lack of infrastructure surrounding these loans has acted as a massive bottleneck within the crypto economy. Maple Finance provides a solution via under-collateralized loans to approved borrowers while taking advantage of the composability and efficiency of public blockchains.

Apart from protocol growth, Maple’s token (MPL) has had a fantastic start to 2022, significantly outperforming competitors and the broader lending market.

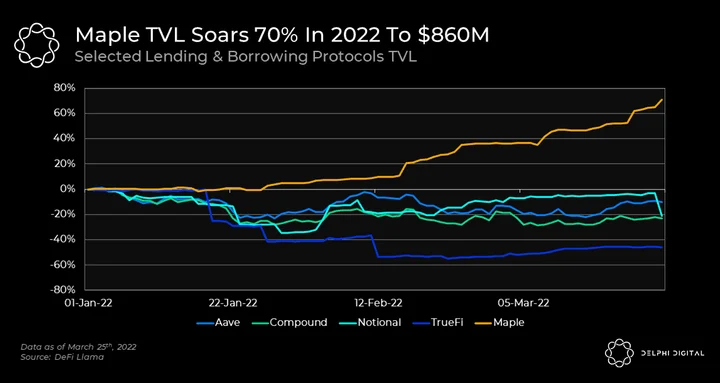

This out-performance from Maple can be attributed to its improving fundamentals versus other lending protocols. One metric we can use to illustrate this is comparing TVL between platforms. In this case, TVL makes sense as it directly relates to the number of loans these platforms can support and thus revenue that can be generated.

Maple’s TVL has increased by 70% in 2022, now sitting at $860M. This makes Maple larger than Notional ($420M) and TrueFi ($485M), but still significantly behind Compound ($7B) and Aave ($13B). The fundamentals seem to be on the rise, so the question begs: how does Maple Finance differentiate itself in the market?

How Maple Works

Protocols like Aave and Compound require borrowers to post collateral in excess of what they are borrowing. Additionally, floating interest rates introduce risks to borrowers as interest costs are volatile and thus difficult to predict. Protocols like Notional have tried to address this with fixed-rate lending but continue to run into the same capital inefficiency hurdles that Aave and Compound face. For example, on these overcollateralized platforms, a user can put up $125 worth of ETH to borrow a maximum of $100 USDC. These solutions make sense if you want to lever up against your crypto portfolio or access partial liquidity without selling. But overcollateralized borrowing isn’t a viable option for businesses that need capital to grow.

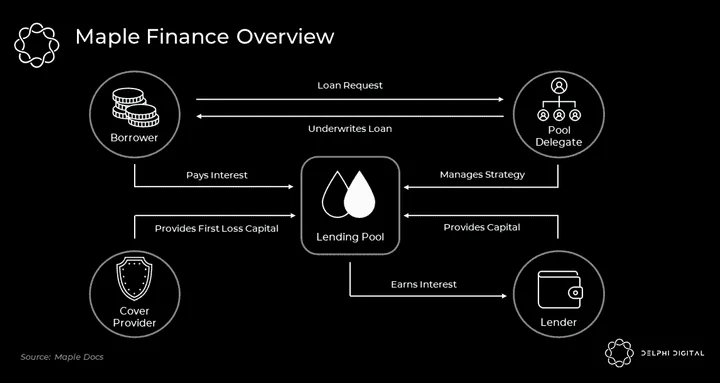

Maple provides the infrastructure to facilitate under-collateralized loans to an array of market players. Given its under-collateralized nature, the process requires additional due diligence, and a degree of centralization, versus a permissionless application like Aave. These additional trust assumptions allow for an entirely new market to be created, getting capital into the hands of businesses and filling a much-needed gap in the crypto funding landscape. The Maple ecosystem has four key participants: pool delegates, borrowers, lenders, and cover providers.

Pool delegates are reputable firms such as Alameda, Maven 11, and Orthogonal Trading that manage their own lending pools. Pool delegates can open up lending pools and provide loans to a range of borrowers that have been onboarded. It is up to the pool delegate to negotiate loan terms, perform due diligence on borrowers, and manage collateral liquidations in the event of a default.

Maple taps into lenders that want access to sustainably higher stablecoin yields. Depending on the type of pool, participants (anyone or whitelisted members) can supply liquidity to earn interest and MPL token rewards. This is where it gets interesting from a lender’s point of view. The Orthogonal Trading USDC pool is currently paying out an unincentivized 6.9% APY on USDC vs. 2% on Aave. This interest rate difference reflects the additional risk LPs take lending to under-collateralized borrowers. We will compare these rates and tradeoffs more in the next section.

After being onboarded, borrowers are able to negotiate loans with the pool delegate with a fixed interest rate and maturity. This is beneficial to borrowers as they can borrow efficiently with a predictable cost of capital.

Lastly, we have cover providers. These are users that provide “first loss capital” for lending pools in the event of a default. The cover providers are paid 10% of the interest generated by the pool to incentivize them to take on this risk.

The basic structure of Maple can be summed up by the following flow chart.

Current Users Of Maple Finance

At the moment, Maple borrowers mainly consist of crypto native market makers and trading firms. Maple is looking to expand its product offering to other crypto-oriented businesses with a high cost of capital (providing attractive yields to lenders) but strong balance sheets. Two potential categories are crypto miners and protocols/dApps. There are over 100 protocols with market caps greater than $1B. The vast majority of these projects have been funded by tokens and/or equity and very little debt. This is a massive opportunity that Maple could tap into by providing a vibrant debt market that hundreds of crypto-facing companies and protocols can use.

Lenders on Maple are in search of high but sustainable yields. Let’s dig into the pros and cons of supplying assets to Maple pools versus a protocol like Aave.

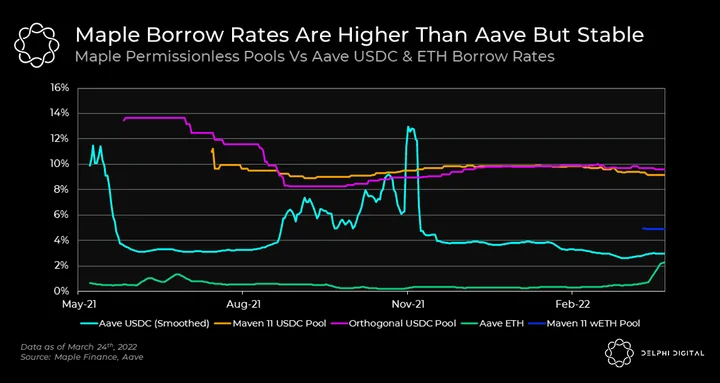

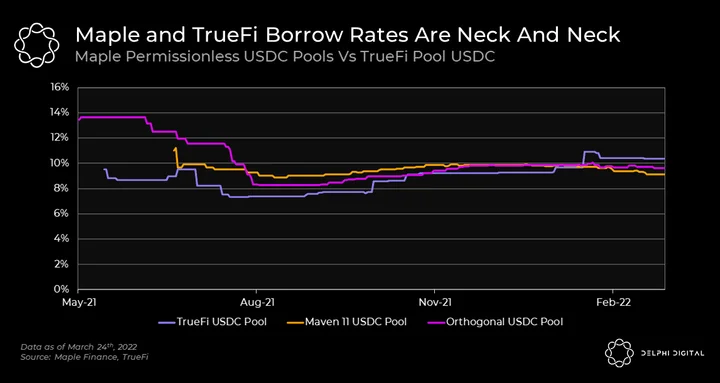

Borrowers on Maple negotiate fixed maturities (currently 30-180 days) and interest rates with pool delegates. The rates shown above are the average within each pool over time. Currently, Maple USDC pools are costlier for borrowers, sitting at just over 9% versus Aave at 3%. However, they possess some other benefits.

On Maple, most loans require no capital down, making them efficient for businesses to borrow. Compare that to Aave where borrowers must post collateral worth anywhere between 120-200% of the loan value. This is a no-go for businesses that require capital to grow.

Another critical factor is the stability of rates on Maple. Since rates are fixed at the beginning of the loan, borrowers can plan accordingly with predictable costs. Looking at the above chart, we see Aave borrowing rates spike sharply in August and November. If the cost of capital here was to double overnight, it could pose non-trivial problems for borrowers. While Aave seemingly does have a lot of downsides on the borrower side, we must take into account its decentralized and trustless nature versus Maple. This plays a much larger role when examining the risk and rewards that come with being a lender.

Lenders can currently earn nearly 3.5x more yield on Maple with rates sitting at ~7% versus Aave at 2%. With stablecoin and other delta-neutral yields coming down since mid-2021, being able to find higher – and importantly, sustainable – sources of yield has made Maple increasingly attractive for lenders.

The above rates are unincentivized but it should be noted that Maple is paying out some liquidity mining incentives to lenders for an additional 6-10% APY. This is being used to attract initial deposits while also making Maple competitive with other incentivized platforms. Over time Maple plans to wind down these incentives and allow its organic, sustainable rates to speak for themselves.

So given these higher rates available on Maple versus a platform like Aave, what are the tradeoffs you make as a lender?

As we’ve noted, Maple’s loans are under-collateralized. At its core, this means you must trust that borrowers who’ve been approved by pool delegates will not default. Each pool has different risks. Delegates outline their investment strategies and perform credit checks to calculate and approve interest rates for each borrower. Over time as Maple grows, pools can become more tailored to various investment strategies and degrees of credit risk. This allows for all sorts of lenders and borrowers to come together, making markets with varying interest rates that are dependent on perceived risks.

Beyond pool delegate due diligence, there is another layer of protection for lenders called pool cover. This is the first loss capital put up by both pool delegates and cover stakers to protect lenders and earn high yields (10% of the loan interest). As an example, the Orthogonal Trading USDC pool has ~$298M worth of loans outstanding with a cover amount of $16.1M, representing a 5.42% coverage ratio. Stakers are currently earning a 16.3% unincentivized APY but can only provide cover in the form of 50:50 MPL-USDC LP positions. This severely limits flexibility for cover providers. However, Maple plans to add options for single cover staking in MPL, USDC, WBTC, and ETH in the future. We expect increased optionality in cover collateral to boost the coverage ratio across all pools.

Another factor to consider as a lender on Maple is that you must lock liquidity for a minimum of 90 days with an additional 10-day cooldown period. This, of course, is a tradeoff and can be a deterrent to those who need to move capital around quickly. But consequently, this allows Maple to have an extremely high utilization rate, as they can be sure capital will not leave without prior notice. Maple plans to change this to a shorter withdrawal period (under 2 weeks) with their V2 pool launch.

On the other hand, Aave is trustless and allows for lenders to have an extremely high degree of certainty that their loan will be repaid in full given its over-collateralized nature. Aave lenders can also deposit and withdraw liquidity at any time. At the end of the day, Maple is tackling a whole different market than Aave — businesses that need capital to grow and expand.

While we’re talking about competitors, another protocol looking to tackle the under-collateralized loan market is TrueFi.

Stacking Up Maple Finance and TrueFi

TrueFi and Maple are both under-collateralized lending platforms. Although borrow rates are similar across the platforms, their loan mechanism and underwriting process is quite different.

TrueFi performs KYC and credit checks on applying institutions, with a borrower criteria of having at least $10M in assets. From here, approved borrowers can request a loan on-chain, which is vetted and voted on by TRU stakers. If the loan is approved, borrowers can draw from TrueFi’s generalized lending pools. There are four main pools segregated by asset: BUSD, USDC, USDT, and TUSD.

In contrast, Maple uses isolated lending pools run by pool delegates which allow for two things.

The first is increased scalability. Each pool delegate is responsible for whitelisting its own borrowers, negotiating loans, and attracting lender capital. This allows for tens to hundreds of borrowers to be whitelisted relatively quickly across multiple pools versus going through one entity and subsequent community votes.

The second is increased flexibility. In TrueFi, all USDC loans happen within one lending pool, distributing risk amongst all lenders in the pool. In Maple’s model there can be many different pools for the same asset but with varying degrees of risk tolerance and expected returns. For instance, having one USDC pool that only lends out to extremely high-quality borrowers would likely be safer, but would give lenders lower yields versus a pool that lends USDC to slightly more risky borrowers. These design choices allow lenders to be more selective on where they provide capital, with the confidence that risk is isolated to each individual pool.

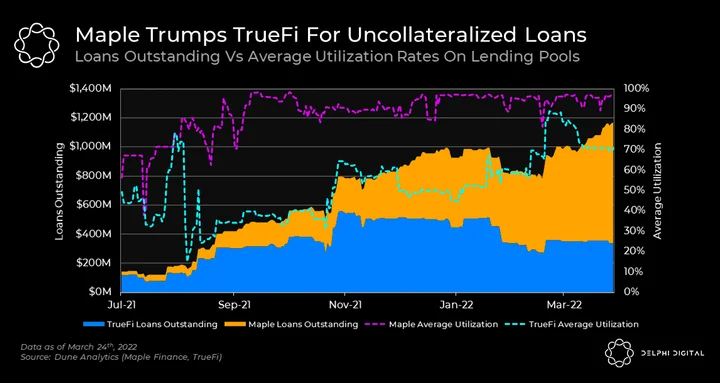

Maple’s loans outstanding have grown over 70% in 2022 with its utilization hovering above 90%. This high utilization rate versus TrueFi can be attributed to the caps that Maple has on its lending pools alongside the 90-day lock-up period. By doing this, Maple can reduce the amount of capital that is idly collecting yield while providing limited value to the protocol.

A potential problem for both Maple and TrueFi is the fact that lending yields are currently greater than borrowing costs, which opens up potential exploitation. This is a result of the cumulative lending yield consisting of organic yield and a token subsidy. Users could effectively borrow from the protocol and then lend to themselves, thus pocketing the token incentivized spread. Maple is in the process of mitigating this by slimming down or removing token incentives for lenders.

To learn more about TrueFi’s loan model you can read our previous report here. TrueFi has also recently launched its lending marketplace, which is very similar to Maple Finance’s current design.

Value Accrual Inside Maple

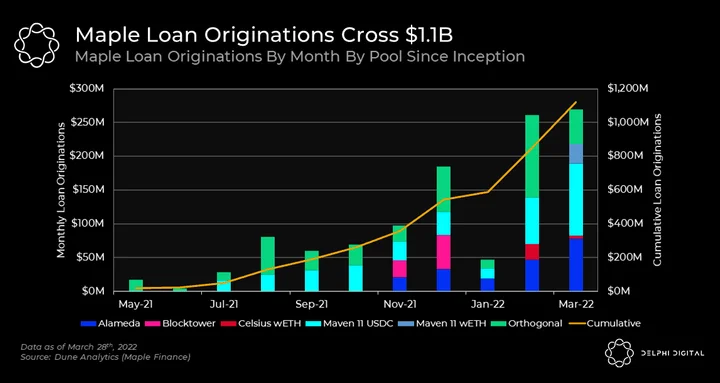

Maple has funded over $1.1B in loans since the protocol’s inception and has done ~$580M of that in the first 3 months of 2022. Assuming stable growth in loan origination, this puts Maple on track to do $2.3B in loans for 2022. However, Maple’s team has larger aspirations than that, setting out a goal of $2B by June 2022 and $5B by the end of the year.

There are origination fees of 1% (annualized) for all loans on the platform; 67% of this fee flows to the Maple treasury and 33% is paid to the pool delegate. From the treasury, 50% of these funds are used to pay for operations and 50% are used to buy back MPL and return it to xMPL stakers.

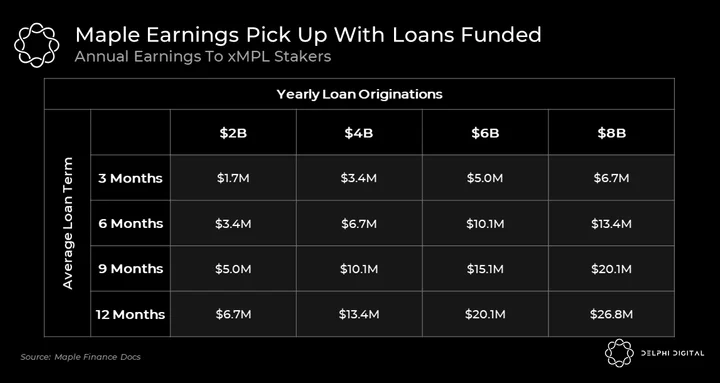

Below is a snapshot of what xMPL annual earnings could look like depending on loan originations and average duration.

If the Maple team were to hit its goal of $5B in originations for 2022 that would earn xMPL holders ~$8.4M assuming the average loan duration is 6 months. That puts the circulating P/E of MPL at ~25X, which is pretty good considering the speed of its growth and potential to scale with the delegate model. It’s important to note that the launch of xMPL will not go live until later this year.

Another very interesting development will be the launch of Maple on Solana and a secondary token called SYRUP. Maple announced its acquisition of Avari earlier this year for its expansion into the Solana ecosystem. This marks Maple as one of the first protocols to bring under-collateralized lending to Solana. The Maple treasury will hold 40% of all SYRUP and fees collected will trickle down to xMPL. The remaining SYRUP will be split between the Maple Solana treasury, the team, advisors, and potential acquisitions. You can read more about Maple on Solana here.

Maple hopes to find the same stickiness in their business model with SYRUP and Solana (pun intended).

Closing Thoughts

The market for on-chain under-collateralized loans has the potential to be massive. The Maple team has communicated its intention to onboard more pool delegates and borrowers to the platform. Starting with crypto-centric businesses like miners and protocols opens up the door to billions in potential loan originations. To date, almost all financing in crypto has been done through equity or tokens with very little use of debt instruments. Maple provides a service for these projects and companies to get access to debt capital markets in a way that was previously not available.

With V2 Pools launching soon, Maple is on the path towards liquid loan LP shares that can be traded on secondary markets. In the future, you can imagine a world where there are a variety of lending pools for specific types of borrowers and credit risk profiles. From here, you can have the loan LP tokens trading on a secondary market for all of these pools — akin to a corporate bond. This starts to look and feel very similar to traditional debt capital markets and poses a potentially massive opportunity for Maple if they can execute on their ultimate vision.

0 Comments