Report Summary

THORChain’s volume & TVL has reached ATHs at $162M and $549M respectively with the 3 major contributing factors being (i) THORSynth Activation, (ii) Terra Integration and (iii) Cap Removal.

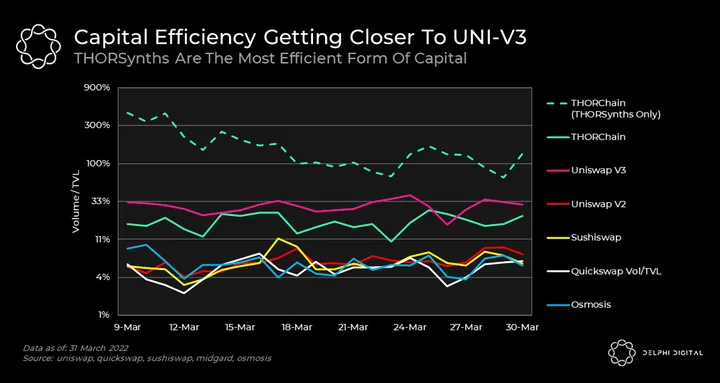

A dollar of THORSynth has generated 12x more volume than a dollar of regular LP. THORSynths are the most efficient form of capital across all AMMs including UNI-V3.

All else being equal, a pool with 16.5% synths has the potential to boost LP APY by up to 1.8x compared to a pool with no synths. The average boost becomes higher if RUNE outperforms the asset and vice versa.

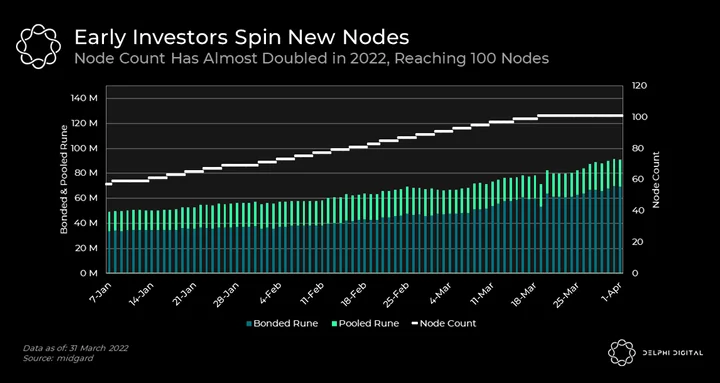

Since the beginning of the year, the node count has grown from 57 to 100 which allowed the network to safely remove the soft caps (#RAISETHECAPS). From here on, the effective cap on pools is the hard cap (bonded > pooled). Current pool size is at 40% of the hard cap limit.

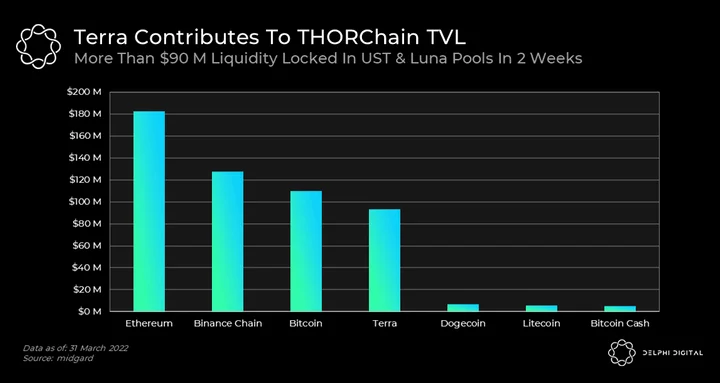

In just two weeks since it’s integration, Terra has garnered $90M of the liquidity on THORChain and currently forms 17.5% of total pooled liquidity.

Year-to-date, liquidity fees have accounted for 15% of the total protocol revenue (bonder & LP revenue) surpassing all major layer 1s with respect to unsubsidized fee generation (<1-5%)

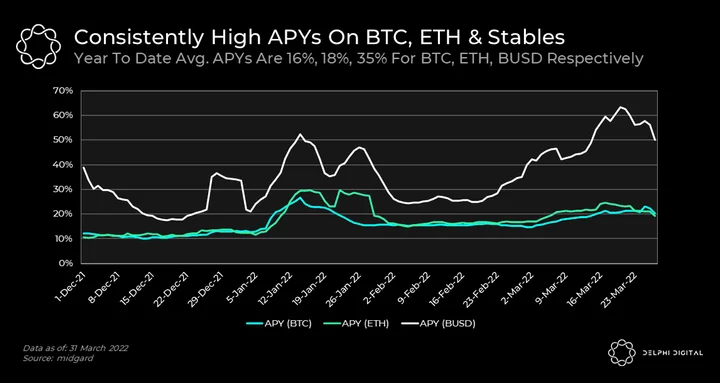

Average year-to-date APYs on BTC, ETH, BUSD pools have been 16%, 18%, and 35% respectively.

Since the beginning of March, THORChain has experienced a surge in activity. By the end of the month, both volume and TVL reached a new ATH at $162M and $549M respectively. In this post, we will analyze the three recent milestones which have laid the foundation for THORChain’s recent traction. Namely, they are: the activation of THORSynths, an integration with Terra, and the removal of liquidity caps. Without further ado, let’s jump right in.![]()

![]()

MCCN Journey

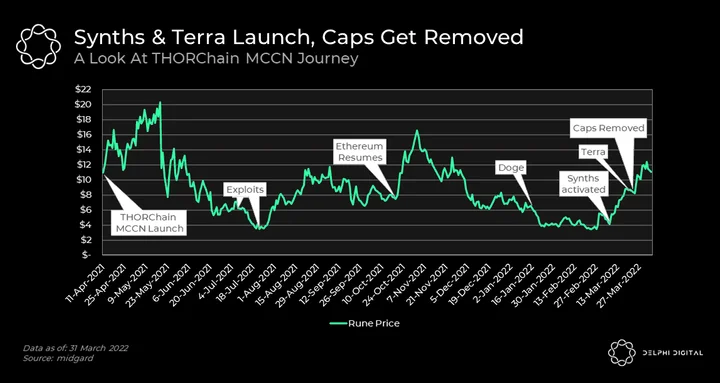

Let’s take a brief look into THORChain’s MCCN journey. MCCN refers to the “Multi-Chain Chaosnet” which precedes the full-blown Mainnet. As the name suggests, this iteration was subjected to periods of chaos. Since its launch in April, THORChain has been exposed to multiple exploits, from which it has recovered stronger than ever. THORChain LPs have been compensated for their losses via funds in the treasury, but also have been consistently enjoying lucrative yields.

The average year-to-date APYs on BTC, ETH, and BUSD pools have been 16%, 18%, and 35% respectively — which is quite strong for high-quality crypto assets.

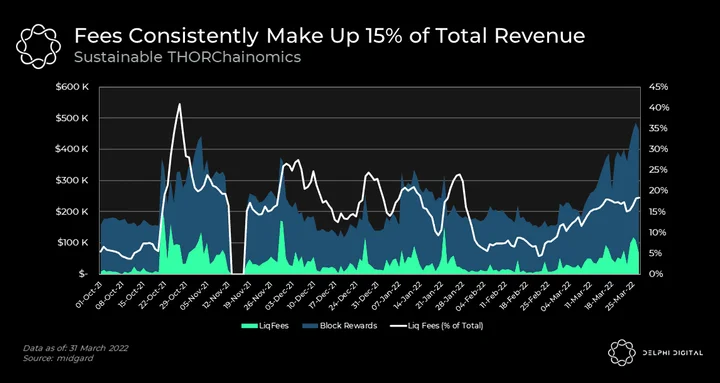

Now let’s look at the breakdown of THORChains’ revenue. On average, 15% of the revenue originated from liquidity fees generated through cross-chain swaps, and the rest was made up of block rewards. Most L1 networks typically have organic fees making up <1-5% of total revenue, putting THORChain in a pretty good position. More importantly, liquidity fees’ share of total revenue has been somewhat consistent — which is largely on account of demand for censorship-resistant, cross-chain swaps having inelastic demand.

A Refresher On Synths

Synths are a novel product that makes use of THORChain’s unique features in a highly effective way. For those who are unfamiliar with synths, we highly recommend glossing over our previous post where we covered them in depth.

As a refresher, synths are IOUs that provide one-sided price exposure to the non-RUNE asset in the pool. For example, 1 sBTC = 1 BTC — backed by liquidity in the THORChain pools. They can only be minted by depositing RUNE into the pool; the synths are also burned to withdraw RUNE from the pool. When swapping sBTC to sETH, sBTC is burned. Subsequently, RUNE withdrawn from the BTC pool is then deposited into the ETH pool to mint sETH. Thus, just like native swaps, synth swaps (or mint & burns) incur slippage and generate liquidity fees.

Notice that synths and native assets share the same liquidity pool. In pools loaded with synths, part of the liquidity in the pool is marked as collateral backing the synth and is owed to synth holders. The rest of the liquidity is attributed to regular LPs. This breakdown fluctuates based on RUNE’s price against paired assets.

When a synth is burned for RUNE, the amount of RUNE that can be redeemed is not necessarily the same amount deposited to mint that synth in the first place. Instead, at any point in time, synths can be redeemed for an amount of RUNE that’s equivalent to the dollar value of that synth asset — 1 sBTC can always be redeemed for 1 BTC worth of RUNE. If, during the lifecycle of a synth, RUNE’s price outperforms the non-RUNE asset in the pool, the pool (and thereby LPs) owes less RUNE to synth holders than synth holders initially deposited to the pool, and vice versa.

When a pool owes less RUNE to synth holders than their initial deposit, the surplus RUNE is captured by LPs which amplifies their APY. When it’s the opposite, the deficit owed to synth holders is initially taken out of LPs’ accrued earnings. If the deficit is higher than LPs’ earnings, the reserve backstops their loss and plugs the deficit. In the worst case, LPs can lose their accrued earnings (0% APY). However, they will never suffer a loss on their principal and can always withdraw their initial deposit for LP tokens in full. To sum up, in a pool loaded with synths, LPs no longer have a 50%-50% exposure to RUNE and the paired asset. Instead, they have asymmetrically long exposure to RUNE. They are fully exposed to upside but only partially exposed to downside.

Finally and most importantly, synth holders waive their right to fees that are generated on their collateral in the pool. Fees foregone by synth holders accrue to LPs, which amplifies their APYs irrespective of all other factors. We will evaluate the importance of this later in this post.

At initial launch, the amount of synth collateral in a particular pool is capped at 2.5% of the pool’s total liquidity. Based on this, if RUNE owed to synth holders makes up more than 2.5% of RUNE in the pool, synth minting is paused.

As of Apr. 2022, synth caps have been raised to 7.5%.

With Synths, RUNE is More Productive Than Ever

Prior to synths, one could think of THORChain as an exchange where users were forced to deposit, swap, and withdraw assets, bearing expensive gas costs each time they wanted to make a trade. With synths, users have the option to deposit and do as many trades as desired on THORChain, while also keeping the option of being able to withdraw native tokens to their chain of choice. Naturally, this is a much cheaper mode of operation and has so far attracted significant traction.

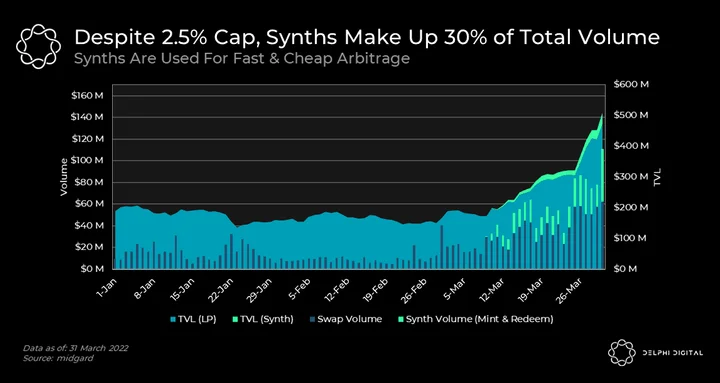

Below we take a holistic view of all pools and show how much of the pool’s liquidity and volume is attributed to synths.

Despite 2.5% caps, synth swaps (mint & burns) account for 30% of the total volume across all pools. In other words, synths have been 12x more productive in terms of generating volume compared to regular LP. This was possible because, unlike their native counterparts which live on slow and expensive external chains, synths live on the app-specific THORChain blockchain and thus can be frequently mobilized (for example, 5 second block times on THORChain vs 10 mins on Bitcoin) and cheaply transferred.

Below we compare the capital efficiency of AMMs across the board. THORChain is the second most capital-efficient AMM behind Uniswap v3. And THORSynths are the most efficient capital across all AMMs.

![]()

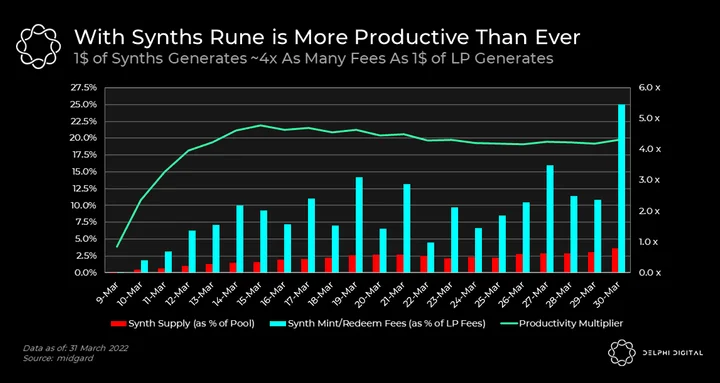

Next, we zoom in on fees. With synths, pools not only generate liquidity fees from native swaps but also synth swaps (mint & burns). Below we see how much of the total liquidity fees generated in the pool have originated from synth swaps.

We divide this figure by the collateral share for synths in pools to compare the capital efficiency of synths to regular LPs. We notice that a dollar of synths has so far managed to generate ~4x more liquidity fees than a dollar of LP capital; a unit of measurement coined as the “productivity multiplier”.

Note that slippage on synth swaps is artificially halved by doubling the virtual depth of the pool. While this parameterization contributes to the high utilization ratio (volume / TVL), it results in lower fees per volume which justifies why synths generated ~4x more fees, while doing ~12x more volume.

Synth caps are planned to be gradually raised and eventually be kept fixed at 16.6%. Assuming a productivity multiplier of 4x, a pool with 16.6% synths will generate (=16.6%*4+1-16.6%) 1.5x more fees than a pool without synths.

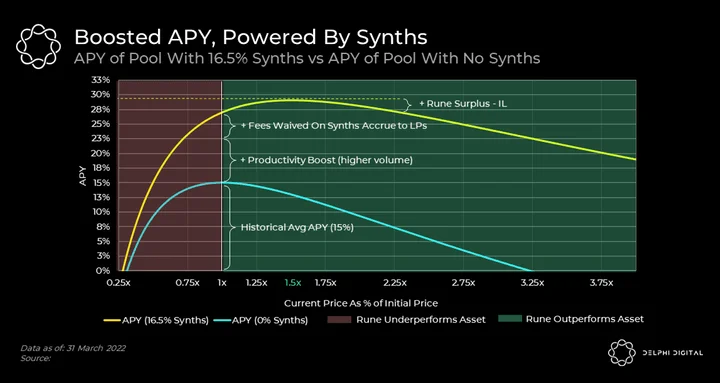

Crucially, LPs will be capturing *all* of these fees (recall that synth holders waive their rights to fees) even though they only have contributed to (1-16.6%) = 83% of the pool’s TVL. All else being equal, this will amplify their APY by (1.5/0.83) 1.8x.

If during the LPs’ stay in the pool, RUNE outperforms the paired asset in price, the pool will owe less RUNE to synth holders than they initially deposited. Thus *in addition,* to 1.8x amplified earnings, LPs will also get to capture a part of the RUNE deposited as synth collateral — which, if higher than IL, will further boost yields.

All of this can be visualized on the above chart where we compare the APYs of a pool loaded with 16.5% synths to that of a pool without synths. The X-axis shows RUNE’s price change relative to its paired asset in the pool. For the sake of simplicity, the pool can hypothetically be a RUNE<>BUSD pool. For illustrative purposes, we also assume that all synth minting and LP deposits occurred at the same time and haven’t been withdrawn since.

If the pool without synths has 15% APY (THORChain’s year to date average), then a pool with 16.5% synths amplifies this APY by 1.8x to make it 27%. In addition to this, LPs in synthetically loaded pools no longer have symmetrical exposure (50% Rune-50%Asset) but instead take on a levered long position on RUNE. As such, if Rune were to appreciate in price by 1.5x, LPs would also experience an increase in their LP value because the RUNE surplus they would capture on synths collateral would exceed their IL due to price divergence. This would further boost their APY to nearly 30%. This is what makes synths so special.

Price Action Backed Fundamentals

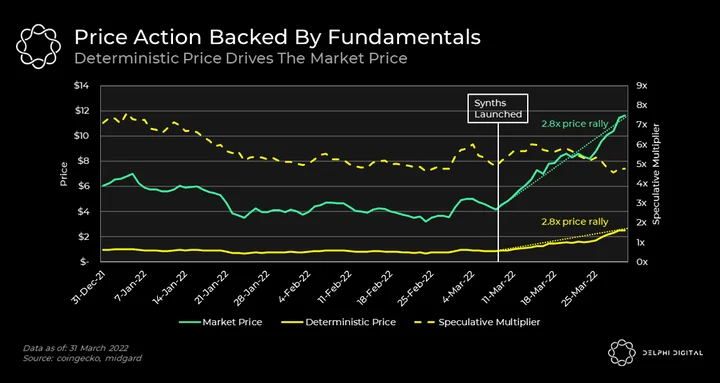

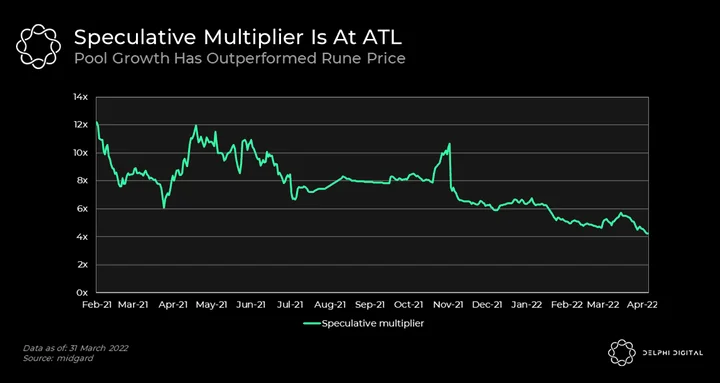

The synth launch has kickstarted a price rally for RUNE. Since the initial launch of synths on Mar. 9, RUNE price has appreciated by 2.8x. This price-performance has been completely matched with the deterministic RUNE price which also increased 2.8x during the same period.

As a refresher, deterministic price (3 * Non-RUNE assets in the pools/RUNE’s circulating supply) measures RUNE’s “fair” value based on fundamentals i.e. pool growth.

By dividing market price by deterministic price, one can calculate RUNE’s “speculative multiplier”.

Since market price and deterministic price both appreciated by 2.8x, by the end of the three week price rally, the speculative multiplier returned back to its original value at 5x. This shows that the price action of RUNE wasn’t purely hype-based, but also reflected fundamentals.

Indeed at 5x, the speculative multiplier is at its all time low. Based on this measure, RUNE seems undervalued despite the recent price rally.

Fun fact: The aforementioned productivity multiplier dampens the speculative multiplier even further and can be taken into account in future calculations.

Besides synths, two major factors have contributed to pool growth and thereby caused the speculative multiplier to drop: Terra’s integration and the removal of pool caps.

Terra Integration

In two weeks since its integration, Terra has contributed over $90M to THORChain’s TVL, which currently represents 17.5% of total pooled liquidity.

![]()

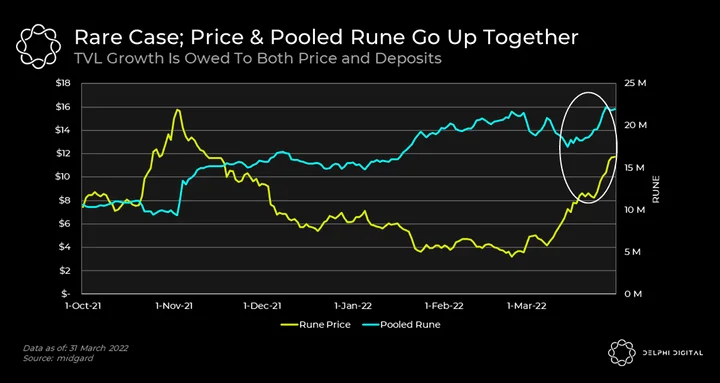

This has caused a rare case where an increase in the price of RUNE coincided with an increase in the amount of RUNE in pools.

Such integrations form new supply sinks for RUNE, creating scarcity in free floating supply as people voluntarily lock RUNE into pools. The pool growth is then accompanied by bond growth.

THORChain Has Permanently #RAISEDTHECAPS

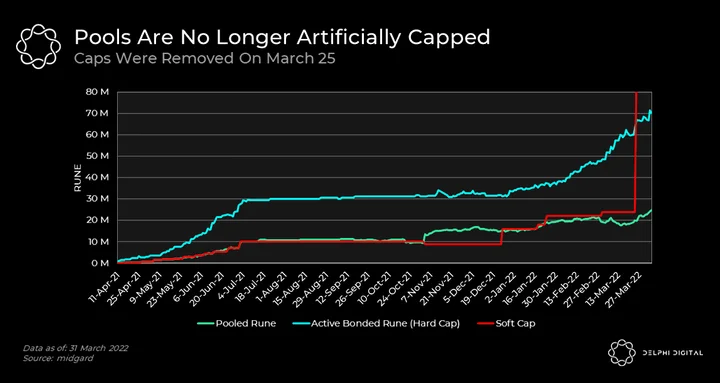

On the day of the Terra integration, the long overdue liquidity caps were completely removed which marked a new milestone for THORChain.

Based on THORChain’s economic security model, THORChain nodes must bond in more value than they are securing in pools. This is a hard cap baked into THORChain’s codebase.

Notice that when the hard cap is reached, new deposits to the pool are paused. However, this mechanism cannot and does not address the potential case where pools outgrow bonds due to price movements of RUNE relative to non-RUNE assets. Since pools are always 50% RUNE and 50% asset, and bonds are 100% RUNE, if RUNE underperforms paired assets, pool value can exceed bonded value, even though deposits to pools are paused. Similarly, the hard cap doesn’t address the edge case where nodes, for whatever reason, unbond large chunks of RUNE in a short period of time.

These cases are addressed by the Incentive Pendulum which splits block rewards & fees between bonders and pools. When pools outgrow bonds, the pendulum directs rewards to bonders which incentivizes them to bond in more RUNE and vice versa. However, ultimately this reward mechanism is effective to the extent that market agents act on it. Importantly, even though anyone can contribute to pools, only tech-savvy, high-net-worth individuals can run nodes. Thus, bond growth via incentives is always a slower process than making pools grow. By purely relying on Pendulum and hard caps, THORChain may at times temporarily operate at an unsafe (Bonded RUNE < Pooled RUNE) state until market forces push it back to an optimal or overbonded state (Bonded RUNE >= Pooled RUNE).

Particularly in the early days, this has been a serious challenge. This is why, as a precaution in addition to the hard cap, THORChain devs have been artificially capping pools by a soft cap (implied in #RAISETHECAPS). The soft cap allowed devs to quickly set limits on pool growth to give nodes enough time to increase their bonds. The obvious downside of soft caps was that they have almost always become a resistance against organic pool growth. This can be seen on the chart above.

Since the beginning of the year, important steps have been taken to alleviate the mentioned risks and lay the foundation for a healthy network where soft caps would no longer be needed.

First, early investors of RUNE have agreed to spin new nodes in return for getting their vested RUNE earlier. This was followed by the “Pooled Nodes mechanism” which has been recently activated. Under Pooled Nodes, a group of friends who can’t individually afford the minimum RUNE bond requirement can team together and run a THORChain node. Pooled nodes currently make up 25% of the total nodes in the network. Both of these improvements open THORChain node participation to a wider audience. Since the beginning of the year, the node count has grown from 57 to 100. With 100 nodes the network is in a much healthier position as bonds can grow rather quickly to accompany spikes in pool growth through wider market competition.

These steps have allowed THORChain to comfortably remove soft caps on pools. With the removal of soft caps, the network is now out in the wild and its growth potential is fully unleashed!

Importantly, besides improving the security of the network, more nodes create upward pressure on RUNE price as they remove RUNE out of the free-floating supply to bond in.

Productive vs Speculative Rune

With that in mind, we can now take a holistic view of RUNE supply.

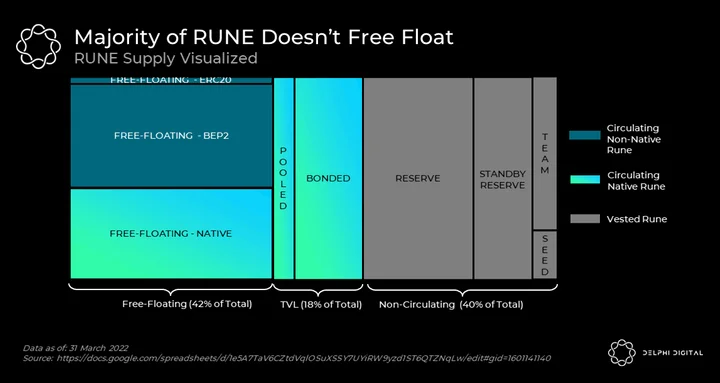

RUNE has a max cap of 500M tokens. 40% of this total supply (200 M RUNE) is non-circulating — formed of vested seed/team allocations and reserves.

As a refresher, the reserve emits block rewards, ILP payments and, in extreme cases, may compensate network participants for their losses. At present, the reserve is in a strong position by holding $2B worth of tokens.

30% of the circulating supply is voluntarily locked in bonds & pools. Bonded & pooled RUNE is productive as it is used for swaps and security respectively. When RUNE gets locked in pools and/or bonded, it generates scarcity in free-floating supply.

The rest is free-floating RUNE. Here, 115M of the token is formed of non-native (BEP2, ERC20) RUNE. Given that these tokens can’t participate in bonds and/or pools they can’t provide useful work for the THORChain network. Thus they can be deemed as the most speculative portion of RUNE. BEP and ERC20 RUNE can be voluntarily upgraded to native RUNE. Once upgraded they can’t be converted back. Thus, the high rate of upgrades is a good sign that signals commitment and potentially increased productivity.

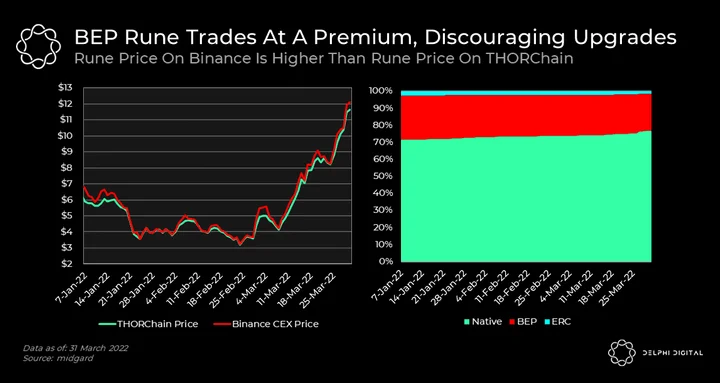

However, the pace of upgrades has been somewhat slower than one may have expected, especially considering significant milestones such as THORSynth’s launch, Terra integration, and soft cap removal.

Surprisingly, BEP RUNE on Binance trades at a premium compared to native RUNE, which discourages upgrades. We think there are two key reasons for this.

- Unlike Binance CEX, THORChain forces users to use wallets that are integrated with THORChain. Admittedly, this makes THORChain less accessible to the average user compared to Binance CEX which offers a much easier UX for onboarding. This will be improved as more wallets get integrated into THORChain.

- Post exploits, the THORChain blockchain halted for a considerable time. Even after the blockchain resumed, trading on-chain remained partially/fully paused for weeks/months. This caused an undesirable effect where native RUNE holders couldn’t move their RUNE while BEP/ERC RUNE holders were able to quickly sell their RUNE on external markets and hedge their risks at will. We think this mobility contributes to the premium that BEP RUNE trades at.

Things To Look Out For

THORChain’s 2022 roadmap is not short of new features and milestones. Here is a short summary of exciting improvements that are expected to be implemented by EOY.

- More chains: Haven (privacy algo stablecoin chain), Monero, Cosmos Hub, Avalanche, L2s, and many others are amongst chains that will be integrated in the near future. With each chain integration, we will likely see the amount of RUNE in pools going up along with the RUNE price, making the rare case we’ve witnessed on Terra integration not so rare.

- More wallets: In order to interact with THORChain one must use a wallet/UI that has been integrated to THORChain. Thus wallet integrations are a crucial prerequisite for THORChain’s success. Wallet integrations will be a top priority for devs in 2022 and we expect all major wallets to eventually integrate with THORChain.

- DEX aggregators: Integrations with DEX aggregators will route swaps through THORChain enabling users to swap exotic tokens cross-chain: ex. ERC20Token -> ETH -> RUNE -> LUNA -> exotic CRW-20 token. With these integrations, THORChain will be making use of not only top-tier assets but also long-tail assets, which may increase volumes significantly.

- THORFi: The next biggest milestone on THORChain’s journey is THORFi which will introduce a number of novel products including no liquidation lending/borrowing, and single-sided fixed yields (ie. earn BTC on BTC). The design of THORFi is out of the scope of this report but those interested can take a sneak peek here. We are very excited about the THORFi products that are currently being worked on.

As more chains, wallets, and products get added, THORChain will grow stronger and be more prepared than ever for the Mainnet launch.

0 Comments