Every transformative technology throughout history can be reduced to the same fundamental characteristic: they drastically reduce the marginal cost of human activity. The steam engine reduced the marginal cost of power. Cars reduced the marginal cost of travel. The internet reduced the marginal cost of information sharing. And more recently, AI is increasingly lowering the marginal cost of intelligence. Each time, costs asymptotically approach zero, new markets emerge, business models evolve, and the fabric of society is left altered.

Today, stablecoins are quietly collapsing another cost curve: the marginal cost of moving and storing value. From cross-border trade and global payments to treasury management and working capital optimization, stablecoins don’t just represent an incremental improvement to existing financial rails – they fundamentally reshape the unit economics of global commerce.

Crucially, this suggests that stablecoin adoption doesn’t hinge on purely ideological assumptions. Instead, by offering businesses a straightforward proposition – lower costs, higher margins, and new revenue streams — stablecoins are inherently aligned with the most reliable force in capitalism: the relentless pursuit of profit. According to this logic, stablecoin adoption is not something that could happen or should happen. Conversely, efficient markets suggest that stablecoin adoption will become table stakes for businesses to remain competitive.

The following manifesto will consist of three parts. First, we will outline how stablecoins can tangibly improve the bottom line of companies and why game theory implies their adoption may become a competitive necessity. From here we will lay out the bull and bear case for stablecoins and blockchains serving as the economic substrate for AI agents. Lastly, we will zoom out and entertain the competing structural incentives — from policy makers, regulators, incumbents, to foreign countries — that will inevitably drive stablecoin adoption.

Part 1: Why Stablecoin Adoption Is Inevitable

Fundamentally, stablecoins reduce costs across three vectors:

- Domestic Payments: Stablecoins represent the natural evolution of closed-loop payment networks, offering the same cost savings and yield generation benefits but on an open, interoperable infrastructure. This eliminates the traditional tradeoffs of fragmented balances, high friction, and limited merchant acceptance while preserving the economic advantages that have made closed-loop systems attractive to fintechs and larger merchants with distribution.

- Global Payments: By circumventing the complex web of intermediaries in cross-border transactions, stablecoins drastically reduce both the explicit costs of international transfers and the implicit costs of maintaining pre-funded accounts across jurisdictions. This is particularly compelling in emerging markets, where stablecoins offer both businesses and consumers a hedge against local currency instability and a way to bypass restrictive capital controls.

- AI-Enabled Commerce: Beyond traditional business use cases, stablecoins are uniquely positioned to serve as the economic substrate for the emerging AI agent economy. Their programmable nature, instant settlement, and ability to handle micro-transactions make them ideal for agent-to-agent commerce at scale.

Let’s examine each of these core vectors in detail beginning with domestic payments.

Domestic Payments: Closed-Loop Economics + Open-Loop Interoperability

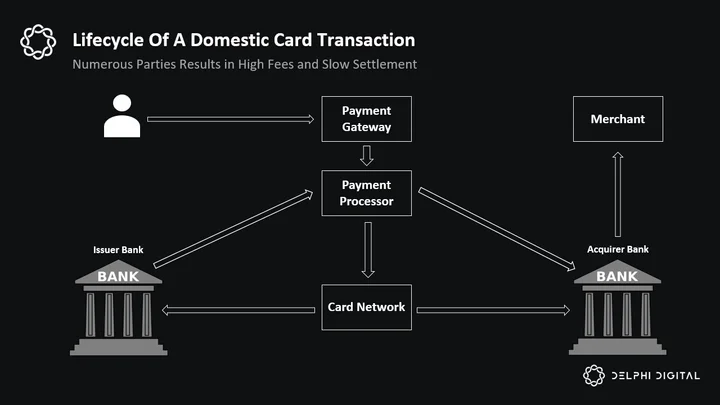

Today’s domestic payment infrastructure is expensive and slow — merchants typically pay 2-3% in fees per transaction while waiting 1-3 days for settlement. To understand why disrupting this system is challenging, we first need to understand the five key players in the domestic payments stack:

- Payment Gateways: Think of payment gateways as the online front-ends where payments are initiated. Their role is straightforward – encrypt card data and route it to processors. They typically charge monthly fees plus about 0.10% per transaction.

- Card Networks: These networks — Visa and Mastercard for example — provide the highway system connecting issuing and acquiring banks. While they don’t actually move money, they maintain the infrastructure and set operating standards. Their fees range from 0.05-0.15%.

- Payment Processors: Think of processors like Stripe and Square as traffic managers on this highway system. They interface with merchants, handle fraud detection, and move transactions through networks. This service costs merchants 0.10-0.35%.

- Issuing Banks: Intuitively, these are the banks that issue cards to consumers. The fee structure here highlights an important nuance. For credit cards, issuing banks charge high interchange fees (1.5-2.2%). This is because they’re underwriting actual credit risk and funding credit card rewards. Conversely, debit cards, involving less risk and fewer rewards, command much lower fees (0.3-0.8%). This distinction matters – the high fees merchants complain about largely reflect credit risk, not just transaction costs.

- Acquiring Banks: These institutions hold merchant accounts and handle settlement risk, charging 0.15-0.40% for their services.

Naturally one looks at this payments lifecycle and naively assumes this model is rife with redundancy and thus ripe for disruption. Unfortunately, things are a little more nuanced than this. Each stakeholder serves essential functions that cannot simply be eliminated: gateways provide necessary security and routing, networks enable bank connectivity, processors handle fraud detection, and banks manage both credit risk and fund custody.

Naturally one looks at this payments lifecycle and naively assumes this model is rife with redundancy and thus ripe for disruption. Unfortunately, things are a little more nuanced than this. Each stakeholder serves essential functions that cannot simply be eliminated: gateways provide necessary security and routing, networks enable bank connectivity, processors handle fraud detection, and banks manage both credit risk and fund custody.

More importantly, there are structural reasons why disrupting this system has proven persistently difficult. Card networks are underpinned by entrenched two-sided network effects. Any alternative must solve for the infamous cold start problem of onboarding both issuing and acquiring banks concurrently. Perhaps most crucially, banks have strong incentives to resist change as they profit significantly from the current system’s inefficiencies, such as slow settlement times that allow them to monetize float income.

Put simply, the law of efficient markets quickly breaks down in a system subject to (1) structurally high barriers to entry and (2) stakeholders collectively incentivized to maintain the status quo.

It’s this structural impasse that led to the emergence of a clever workaround: closed-loop payment networks. Rather than attempting to disintermediate existing stakeholders directly, innovative companies have found ways to instead minimize their reliance on them.

PayPal represents the canonical example of this approach. As the pioneer of closed-loop payments at scale, PayPal strategically reduced their dependence on card networks and banks by keeping liquidity sloshing within their own closed network. When one PayPal user pays another PayPal user or merchant, no external networks or banks are needed – PayPal simply updates their internal ledger while maintaining a master account with partner banks. The money never actually moves.

This model offers two compelling advantages:

- Cost reduction by circumventing card networks and bank fees for internal transactions

- Revenue generation by investing pooled customer and merchant funds in highly liquid assets

This pattern has since been replicated by major merchants. Companies like Starbucks have created their own closed-loop networks. Instead of paying an implicit tax to card networks and banks, they incentivize consumers to use their proprietary payment networks. This allows them to both process payments internally and earn yield on customer balances. In the East, WeChat has deployed this same model at massive scale, reducing payment costs across their ecosystem of apps while generating significant investment income. While saving 1-3% on merchant fees may seem trivial, for any low-margin business, especially those that process high volumes of smaller payments, these fees can significantly impact profitability.

However, closed-loop networks nonetheless have their tradeoffs. Namely, there are three fundamental limitations that have restricted their broader adoption:

- Increased Friction: Unlike open loop systems where you simply pay with the same card linked to your bank account that you do everywhere else, closed loop systems come with the added step of uploading funds before you can pay. This added friction forces merchants to incentivize users with rewards which can quickly offset cost savings.

- Lack of Interoperability: Closed-loop systems are inherently fragmented. Consequently, my Starbucks dollars are not composable with my Chick-fila-A dollars. A customer would therefore have to withdraw funds, incur fees, wait for settlement, and re-depositing into another closed-loop system just to spend these funds. This fragmentation of balances creates additional friction and fees for both consumers and merchants.

- Limited Merchant Adoption: While large consumer businesses can leverage their scale to drive closed-loop adoption, the vast majority of longer-tail merchants lack this leverage. Few consumers are willing to download an app and pre-fund an account to save 3% at a local store. This restricts closed-loop systems to a handful of major merchants with sufficient distribution.

These limitations explain why, despite offering clear economic benefits, closed-loop networks have counterintuitively seen limited adoption beyond major merchants. For most busine

Read the full report

This report is part of Delphi Pro.

- 800+ Pro reports across every major sector

- Talk directly with our analysts

- Private community of funds and builders

Already a Pro member? Log in

0 Comments