Report Summary

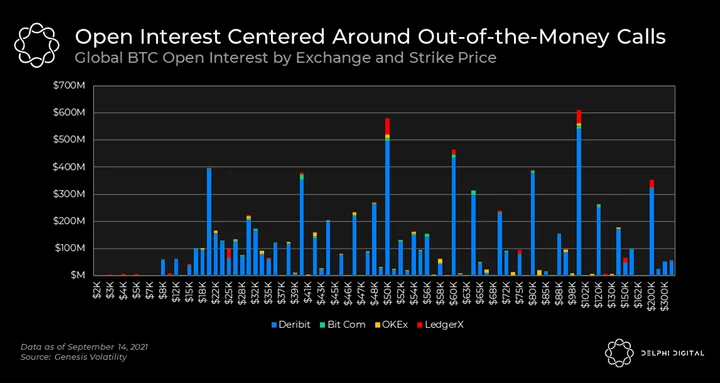

Looking at the global open interest (every exchange, every contract, every strike price), we see a concentration of capital at $50K, $60K, $80K, and $100K. This doesn’t necessarily infer bullish sentiment, as for every ape buying an out-of-the-money call, there’s a seller who believes the option will expire worthless. The same goes for the “anti-apes” buying out-of-the-money puts at $20K and $40K.

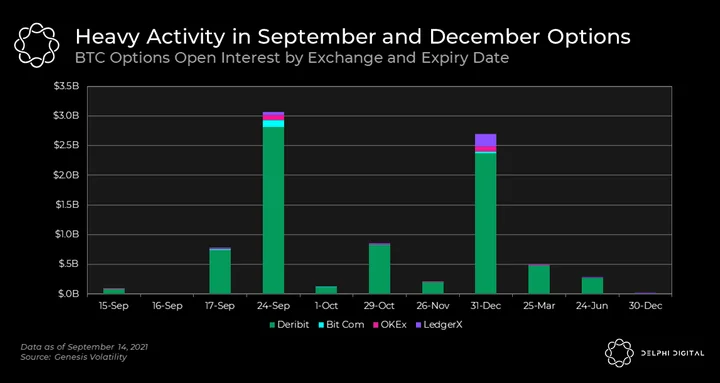

BTC options open interest is heavily skewed towards the Sep. 24 expiry and the Dec. 31 expiry. Both of these are quarter-end option expiries, which tend to see the most interest. Given this quarter’s options are set to expire in 10 days, higher than normal volatility (compared to the last couple of months) is to be expected.

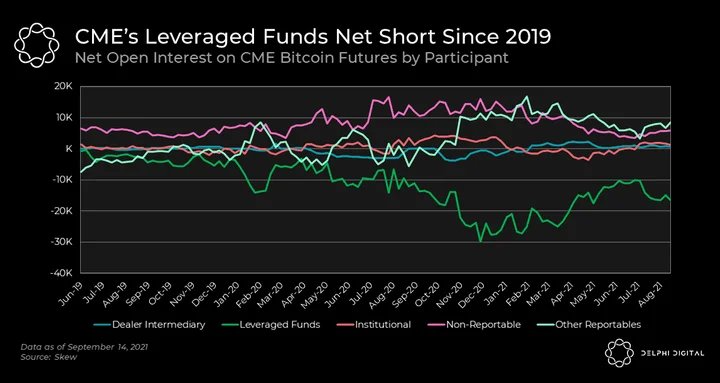

Pivoting to the futures market, leveraged funds trading on CME are net short BTC per CME’s weekly Commitment of Traders report. But this doesn’t really tell us the whole story. The net open interest for these funds hit their lowest level of -30K BTC in Dec. 2020 — just before BTC embarked on it’s journey from $10K to $65K. But net open interest was never positive, peaking at -10K BTC in July.

The likely scenario here is that these funds are long BTC on the spot market and hedging their position by shorting futures. In doing so, they earn a basis yield from the difference between the spot price and futures price (which is almost always higher than spot). So when net OI for leveraged funds climbed between Jan. 2021 and June. 2021, the logical explanation seems to be that they were taking profit on their spot BTC and unwinding their shorts to make sure they didn’t have naked short exposure.

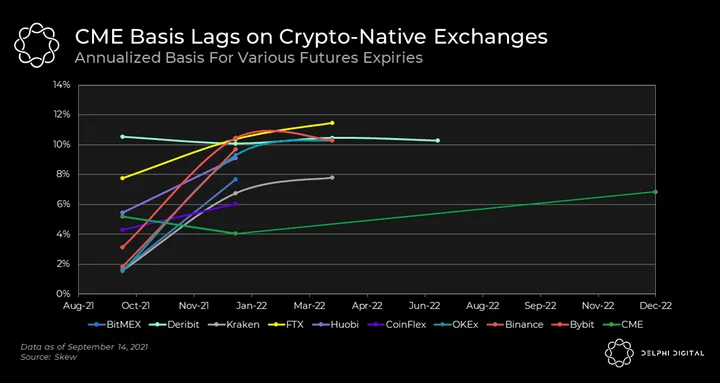

We can somewhat confirm the above thesis by looking at annualized basis for various futures expiries across exchanges. CME’s traders are institutions, and thus more prudent. Seeing a 5-10% basis opportunity is extremely attractive to them. On the flipside, most traders on Binance or FTX are trying to increase their long exposure to BTC. As a result, we see a relatively lower basis on CME, as basis extraction is the crowded trade on the exchange.

Market Update

After a few days of pain, the market is bouncing again. BTC and ETH are finding strength, but what’s more surprising is today’s biggest winners are DeFi blue chips. DeFi coins have seen muted price action for months now, and a strong trend could catch several who ditched the sector.

Apes Gonna Ape

- Looking at the global open interest (every exchange, every contract, every strike price), we see a concentration of capital at $50K, $60K, $80K, and $100K. This doesn’t necessarily infer bullish sentiment, as for every ape buying an out-of-the-money call, there’s a seller who believes the option will expire worthless. The same goes for the “anti-apes” buying out-of-the-money puts at $20K and $40K.

- There’s a prevailing notion in crypto that the strike with the most open interest is where “max pain” is for options sellers. (In other words, the strike with the most OI is where sellers are most exposed to selling calls that expire in the money, which can have unlimited downside.) But max pain is not a real conceptual construct with the options market, given most option sellers are hedged. For the futures market, however, key liquidation levels for longs and shorts can be considered areas of “max pain.”

September’s Options Action

- BTC options open interest is heavily skewed towards the Sep. 24 expiry and the Dec. 31 expiry. Both of these are quarter-end option expiries, which tend to see the most interest. Given this quarter’s options are set to expire in 10 days, higher than normal volatility (compared to the last couple of months) is to be expected.

- Through Paradigm’s order flow data, we’ve seen a good amount of Sep-Dec calendar call spreads over the last couple of weeks. This means people are selling September calls and buying December calls. The idea of this trade is to create slightly longer-term exposure to BTC while subsidizing the trader’s cost basis by selling options (and earning a premium). Typically, one would sell an near-term option they believe will expire worthless and buy a long-term options they think will give them outsized returns.

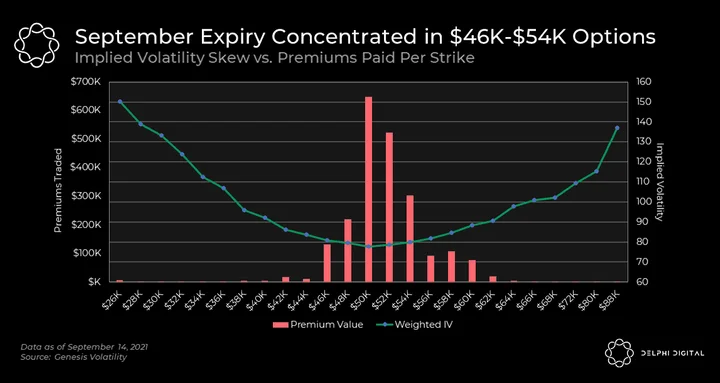

- Within the September expiry, most activity is concentrated between $46K and $54K. The implied volatility skew is fairly balanced despite a lack of activity on the tails (extremely out-of-the-money options). Speculators within this expiry seem to believe that a move to $48-50K is imminent within the next 10 days.

Is CME Really Net Short?

- Pivoting to the futures market, leveraged funds trading on CME are net short BTC per CME’s weekly Commitment of Traders report. But this doesn’t really tell us the whole story. The net open interest for these funds hit their lowest level of -30K BTC in Dec. 2020 — just before BTC embarked on its journey from $10K to $65K. But net open interest was never positive, peaking at -10K BTC in July.

- The likely scenario here is that these funds are long BTC on the spot market and hedging their position by shorting futures. In doing so, they earn a basis yield from the difference between the spot price and futures price (which is almost always higher than spot). So when net OI for leveraged funds climbed between Jan. 2021 and June. 2021, the logical explanation seems to be that they were taking profit on their spot BTC and unwinding their shorts to make sure they didn’t have naked short exposure.

- So in a way, the net OI for leveraged funds going down again could be a sign that they’re buying BTC spot again and adding hedges to protect that position and guarantee a yield.

- We can somewhat confirm the above thesis by looking at annualized basis for various futures expiries across exchanges. CME’s traders are institutions, and thus more prudent. Seeing a 5-10% basis opportunity is extremely attractive to them. On the flip side, most traders on Binance or FTX are trying to increase their long exposure to BTC. As a result, we see a relatively lower basis on CME, as basis extraction is the crowded trade on the exchange.

- Crypto-native exchanges have a perma-bid from apes when the market is moving. There aren’t a ton of funds and traders playing the basis extraction game, so basis trade yield is much higher as demand for long futures outpaces demand to short them. If funds trading on CME could trade on Binance, Kraken, FTX, and other crypto-native exchanges, we would see better efficiency in the market as they pounce on the opportunity to lock in a higher basis yield.

Notable Tweets

Another day, another stress test for crypto

Not a good day for Blockchains.

– Solana is currently down.

– Arbitrum went down, came back up, went down again.

– Someone tried a 550 bock reorg attack with fake PoW on Ethereum, managed to fool some nethermind nodes.— Mudit Gupta (@Mudit__Gupta) September 14, 2021

DeFi’s time to shine?

Staring hopefully is a foolproof strategy.

Bluechip redemption arc imminent just as L1 narrative momentum momentarily begins to fade and VCs start desperately playing their usual games in jpeg land. https://t.co/NK4vj21EyU pic.twitter.com/MdVgYXnVyB

— Hsaka (@HsakaTrades) September 14, 2021

A thesis on ETH going forward

There are several things leading up to an extraordinary supply shock for $ETH

It’s getting to the point where it doesn’t even matter who sells, there is simply too much demand for block space on Ethereum

Let’s discuss! ?

— croissant (@CroissantEth) September 13, 2021

0 Comments