Joe’s Liquidity Book

Trader Joe recently launched v2 of its decentralized exchange (DEX), called Liquidity Book (LB). The LB design incorporates concentrated liquidity, akin to how Uniswap v3 (Uni v3) works, that enhances capital efficiency for liquidity providers (LPs) and reduces slippage for traders.

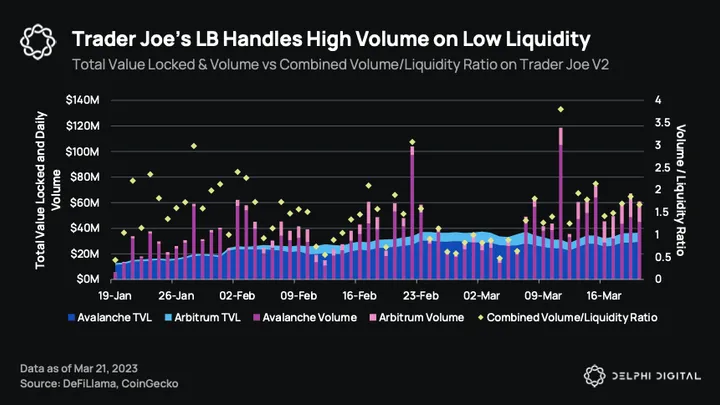

As a result, Trader Joe has been able to attract significant trading volume with minimal liquidity. LB achieved a high of $118M in daily volume with just $31.1M of TVL on March 11th, 2023, representing an impressive 3.8x volume-to-liquidity (V/L) ratio.

In this report, we will delve deeper into what Trader Joe does, the intricacies of the Liquidity Book design, how it’s different from Uniswap v3, and the potential catalysts for growth.

What Is Liquidity Book?

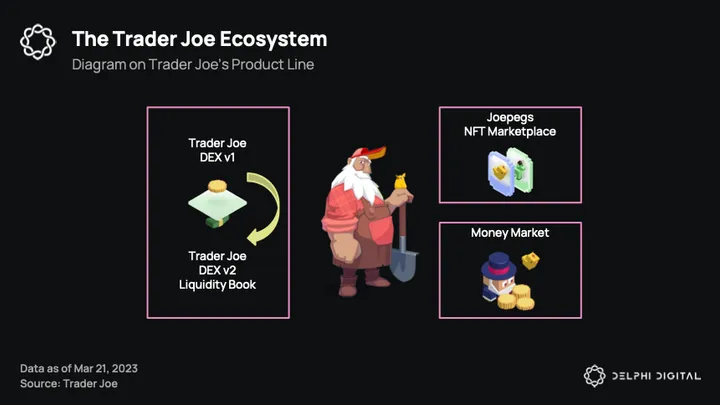

When it was launched, Trader Joe was a Uniswap v2 fork on Avalanche. Since then, they have focused on diversifying their product stack to cater to the various needs of a crypto user. Today, Trader Joe is a DEX, money market, and NFT marketplace across a number of chains.

They launched LB in an attempt to further strengthen their position in the highly competitive DEX market across three chains: Avalanche, Arbitrum, and BNB Chain.

Trader Joe’s v1 DEX is a fork of Uni v2 that utilizes the x*y=K (XYK) automated market maker (AMM) model. The drawbacks of the XYK model are well known. It uses a uniform distribution of liquidity and is not capital efficient, as liquidity pools cover prices that are unlikely to be reached. As a result, liquidity is spread thinly across the true range.

In contrast, Trader Joe’s v2 Liquidity Book is a concentrated liquidity DEX similar to Uniswap v3 but with some key differences.

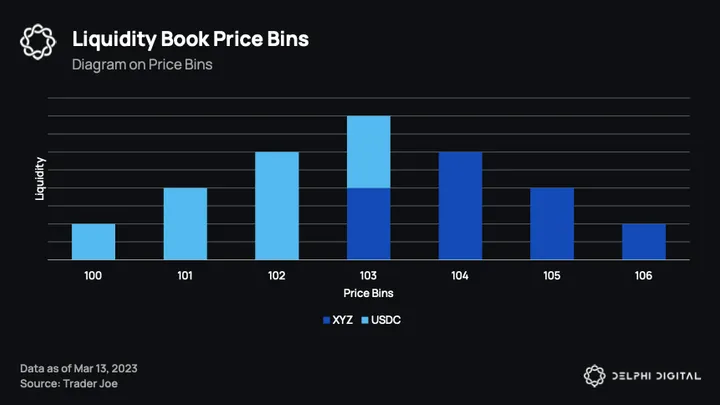

Price Bins

On LB, liquidity is allocated into discrete price bins (similar to Uni v3’s ticks), and trade occurs within the active price bin. LPs can choose the price bin range to provide liquidity and receive a proportionate share of fees generated alongside other rewards.

For instance, the graph above indicates that the active price bin is “103.” This means that all trades will happen within that “103” price bin until liquidity is depleted in either the “XYZ” or “USDC” side. After that, the active price bin will shift upwards or downwards to the next price bin and trades will utilize liquidity from that bin. That new bin will be the new active price bin.

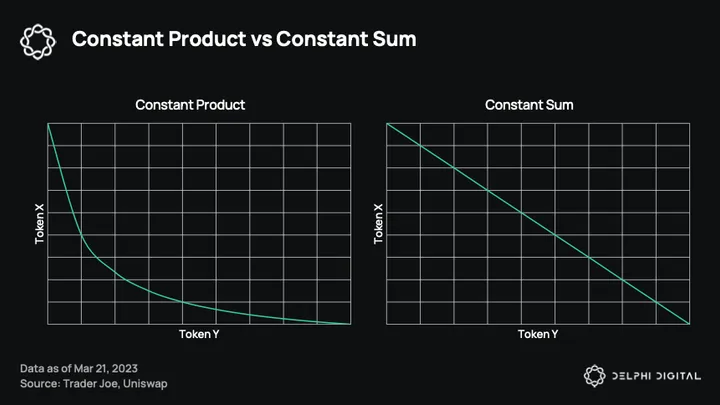

Constant Sum vs. Constant Product

Unlike Uniswap v3, which utilizes the constant product model (x*y=K) over a predetermined range determined by the LP, LB implements a constant sum model (x+y=K) within each price bin. As a result, traders enjoy zero slippage swaps if the trade occurs within the active price bins. This allows LB to have a competitive advantage over Uniswap v3 in certain scenarios, attracting higher trading volumes and thus generating more fees for LPs.

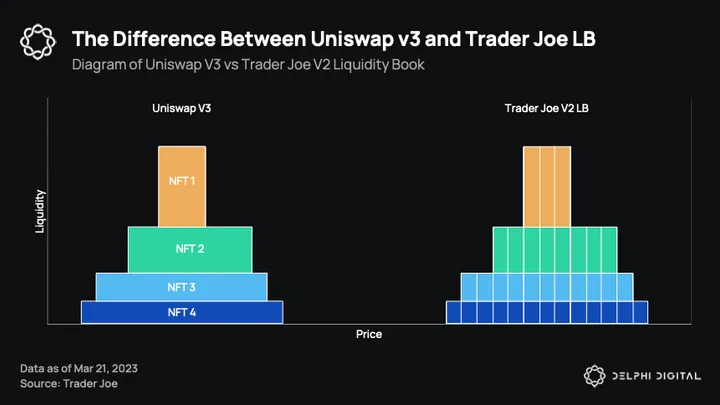

Uniswap v3 vs. Liquidity Book: Design Differences

Although both protocols employ concentrated liquidity, they differ vastly in how they aggregate liquidity. Here, we will outline the differences in their liquidity aggregation and how they impact LPs.

Uniswap v3:

- Individual liquidity positions are created as NFTs, making them inflexible. LPs have to withdraw entirely to make changes to their positions. However, it is possible to skip the NFTPositionManager module and directly provide liquidity to the pool if a developer is familiar with the Uni v3 contract, but this is unlikely for typical retail users.

- Liquidity is aggregated horizontally, with each liquidity position stacking on top of the other and having individual tick ranges for their positions.

- Liquidity is spread uniformly.

Liquidity Book:

- Liquidity positions utilize a fungible ERC-1155 token standard that gives LPs the flexibility to add or remove without exiting their positions entirely.

- Liquidity is aggregated vertically on top of individual price bins, allowing liquidity to be added in a non-uniform way.

- Liquidity spread is discretized through its segmentation of prices into different price bins. The LP has full autonomy over which price bins they want to provide liquidity in. This opens up various strategies that one can utilize.

With this, LB provides much more flexibility due to its fungible nature and provides better flexibility and experience for LPs.

Liquidity Book Fee Scales with Volatility

LB’s fee structure is distinct from Uni v3, which offers a flat base fee. LB’s swap fee comprises two components, a base fee and a variable fee that is activated based on volatility.

The base fee is a fixed fee determined by the pool creator, which ranges from 0.02% to 0.8% for current pools.

The variable fee, also called surge pricing, is calculated based on a pool’s volatility. LB implements the Volatility Accumulator (VA), a novel mechanism that monitors a pool’s volatility and adjusts the variable fee accordingly. This fee is affected by two factors: the frequency of swaps and large swaps spanning more than one price bin. The variable fee is distributed on a pro-rata basis across bins that the swaps have utilized. The unique surge pricing mimics a traditional market maker’s strategy of charging high spreads (or, in this case, fees) in a volatile market.

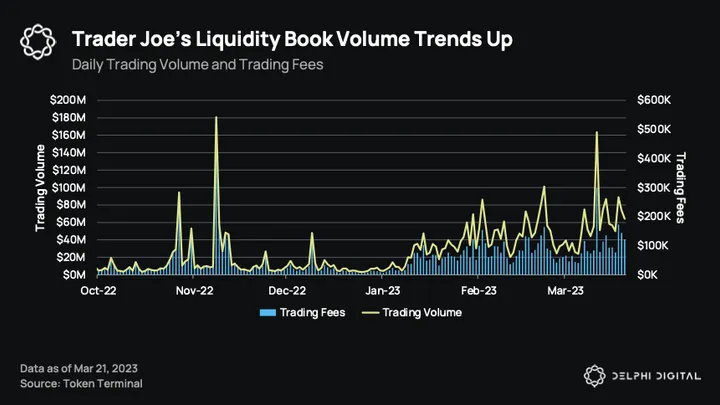

Performance Metrics

Note: This includes volume from Trader Joe v1, which is why volume differs from the first chart, which only accounts for Trader Joe v2 LB’s volume.

As they move towards the concentrated liquidity DEX model, they’ve started to attract more volume and generate more fees. Since LB’s launch and their expansion to Arbitrum, their volume started trending up, hitting highs of $100M in daily volume on March 11th, 2023 after being stagnant at the end of 2022. This reignited volume led to them generating $6.08M in fees for LPs year-to-date.

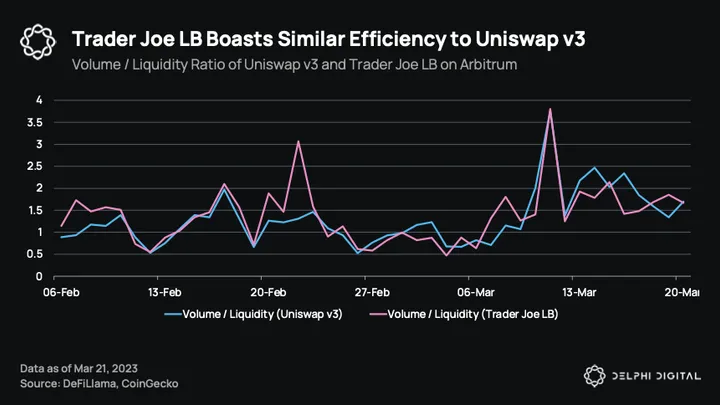

Using the V/L ratio to measure liquidity utilization performance, we see that both DEXs closely track each other. This suggests that Uni v3 and LB perform similarly well, and LPs can expect comparable utilization — and thus fees — on either DEX.

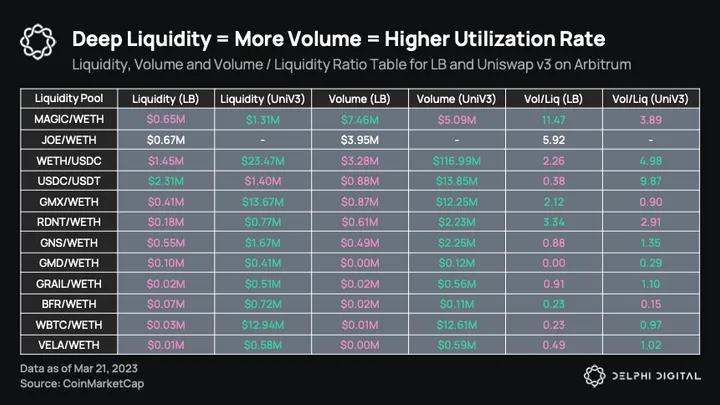

Deeper liquidity often translates into higher trading volumes due to better execution. LB acts in a similar fashion even though it has a different mechanism. There is only one edge case, where the MAGIC/WETH pool has lower liquidity but more volume than Uni v3.

The main difference here is that selected pools actually have better utilization as measured by their V/L ratio. The three main pools to highlight are MAGIC/WETH, RDNT/WETH, and GMX/WETH, all of which produced higher V/L ratios than their Uni v3 counterparts. This could have been the result of their LB rewards program, where LPs are rewarded based on how much fees they generate against each other. This incentivizes LPs to provide liquidity in narrow bin ranges to accrue the most fees.

The Token Economic Model

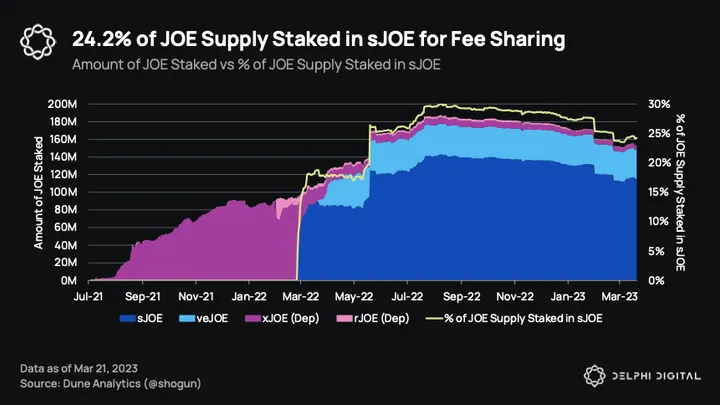

Note: xJOE and rJOE have been depreciated.

The JOE token accrues value in multiple ways, but we’re focusing on two of their active JOE staking products, veJOE and sJOE.

veJOE allows stakers to boost JOE LP rewards in various boosted pools. The boosted pool yields are an additional yield earned on top of the pool and are distributed on a pro-rata basis based on the amount of veJOE staked. This is exclusively on Avalanche.

sJOE, previously xJOE, offers fee sharing for JOE stakers. A percentage of swap fees is deducted from every swap and used to purchase a stablecoin which is distributed on a pro-rata basis to sJOE stakers. sJOE will be available on all available chains, but earnings accruing to sJOE are siloed on each chain. From the graphic above, JOE in various staking products has been decreasing slowly. sJOE holds the majority share, with 24.2% of the total supply being staked.

Fee sharing for sJOE on LB is not live yet. Fee sharing will first be available on BNB Chain alongside its deployment of LB. Fee sharing on Arbitrum and Avalanche will await the launch of LB v2.1. However, the percentage of fees earned from swaps is yet to be decided, with a maximum of 25% given to sJOE stakers.

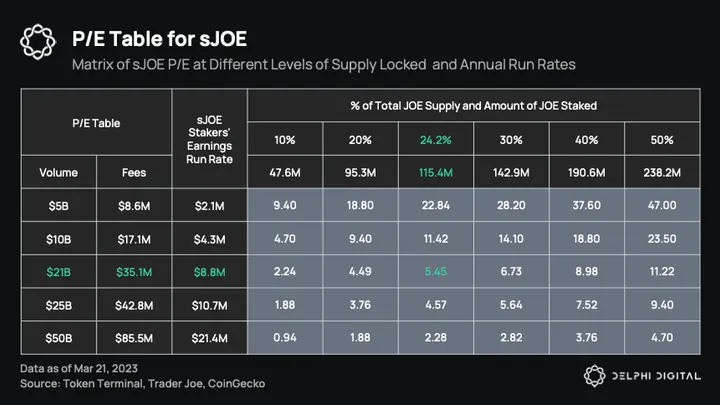

P/E Table for sJOE

Note: The volume and fees are calculated using 30D average annualized data. The fee percentage is set at a 30D average fee of 0.1675% across all pools. sJOE staker earnings assume a 25% max protocol fee on total swap fees. The P/E uses a JOE price of $0.413008 with an FDV of $196M.

The LB is currently allowing LB LPs to earn the full portion of fees. With Trader Joe’s v2 fee sharing aiming to go live in Q1 2023, let’s take a look at what its potential earnings and valuation could be.

The 30D annualized volume is at a run rate of $21B, with potential fees of $35.1M attributed to LPs and sJOE. Assuming the maximum 25% of fees being attributed to sJOE stakers, sJOE could potentially be earning $8.8M in stablecoins. At current staking rates of 24.2% of total supply, sJOE is valued at a price-to-earnings (P/E) ratio of 5.45. However, we expect staking rates to increase once sJOE and fee sharing are live across all supported chains. At a 50% supply staking rate, sJOE is valued at a P/E of 11.22.

Conclusion

Trader Joe’s LB introduced a novel innovation that created an alternative model of concentrated liquidity and provides more flexibility for LPs. Its unique implementation of a constant sum invariant within each price bin allows traders to enjoy zero-slippage swaps, unlike other constant product AMM DEXs.

However, the expiration of Uni v3’s license on April 1st, 2023, will create competition in the concentrated liquidity DEX space. Multiple forks and new liquidity mining programs may attract LPs and yield farmers, leading to competition for both liquidity and volume.

Nonetheless, Trader Joe is expected to gain momentum on multiple upcoming tailwinds. Trader Joe’s LB v2.1 will include “Auto-Pools,” an automated liquidity management product for LB, limit orders, permissionless pools, and sJOE fee sharing. Auto-Pools will attract more passive LPs that want to farm or earn fees; fee sharing will attract more demand for sJOE staking, and permissionless pools will allow any asset to be traded on the DEX, generating more demand. These value-added services give Trader Joe an edge over its competitors and could potentially be what’s needed to push them forward even more.

Special thanks to Jose Villacrez for designing the cover image for this report and to Ashwath Balakrishnan and Brian McRae for editing.

0 Comments