This Wednesday the UMA project will list their $UMA token on Uniswap. We wanted to give our subscribers a quick rundown on UMA, as well as the liquidity impacts of listing on Uniswap. The latter portion will be tackled by Yan Liberman in tomorrow’s Delphi Daily.

The initial listing price of $UMA is set at ~$0.26, which implies a fully diluted market cap of ~$26.67mm. Notably, this is the same listing price as initial seed rounds. Only $2,000,000 of the total $100,000,000 UMA is set aside for this week’s Uniswap listing. Roughly 48.5% is held by founders and early investors, 35% is set aside for developers and UMA users, and 14.5% for future token sales.

What is UMA?

At a high level, UMA is a protocol for building “priceless” financial products.This consists of two core components: 1) the decentralized oracle (DVM) and 2) the financial contract template.

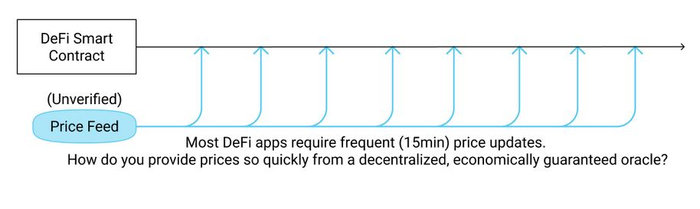

The first financial contracts that users will be able to build are priceless synthetic tokens on Ethereum. These ERC-20 tokens track external assets/information without the need for continuous on-chain price feeds. As seen by recent Defi events (SNX front-running, Maker Black Thursday, etc.), the fragility of applications are heavily due to oracle issues. ‘Priceless’ contracts mitigate this problem by incentivising counterparties to properly collateralize their positions without the need for an on-chain price feed. Liquidators can liquidate positions based on their own external price views, and oracles are only needed when liquidations are disputed.The DVM is the mechanism to ensure honest liquidations.

Rather than continuously pushing price feeds, UMA flips this design by allowing projects to pull price requests in times of price disputes.

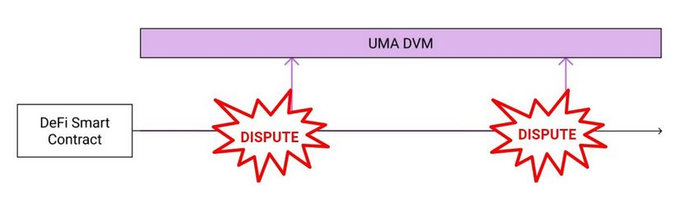

The DVM is designed to be an economically guaranteed oracle mechanism for UMA’s financial contracts.This mechanism, in short, ensures the cost-of-corruption will be greater than the profit-from-corruption. A detailed explainer can be found here.

Where does the $UMA token fit in?

$UMA is used for governance (UMA Improvement Proposals) and to vote on price requests from financial contracts (the disputed events in the above graphic). The UMAIP process can be seen here. Token holders who participate in governance AND vote with the majority receive $UMA inflationary rewards. The Foundation forgoes any rewards.

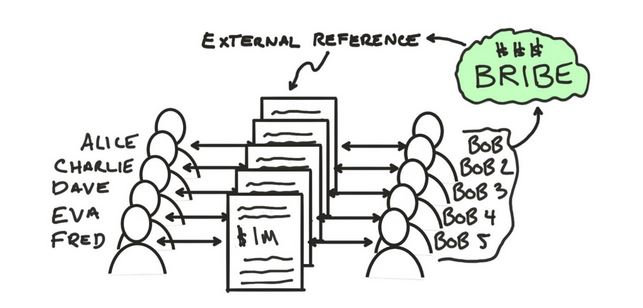

To ensure the safety and security of financial contracts, profit from corruption must be less than the cost of corruption. The costs is measured in attaining 51% of $UMA tokens to control dispute outcomes, and the profit is the total value that be extracted from UMA contracts (ie. total Dai collateral).

Scaling the UMA network (Profit from corruption, PfC) is reliant on a proportional growth in value of $UMA (cost of corruption, CoC). How does UMA plan to influence this? UMA incorporates a taxation system on financial contracts that is used to buy-back and burn $UMA. The tax is made up of two fees: 1) a regular fee that is paid periodically over the life of each contract and 2) a flat value final fee that is paid for each price request. The regular fee has more nuances, which can be found here.

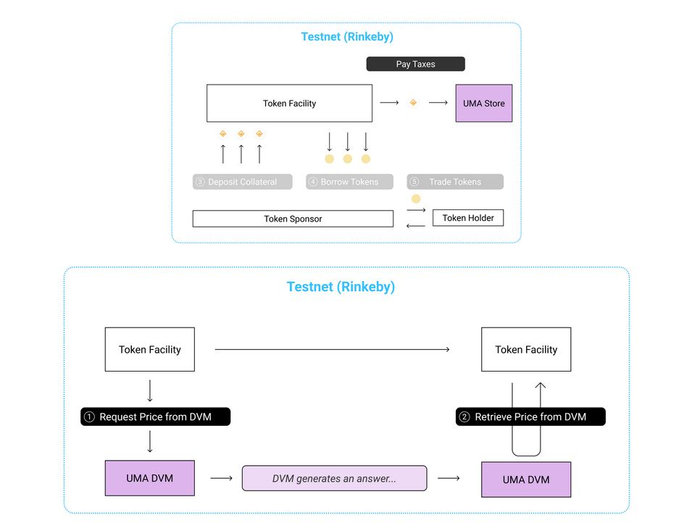

An overview of UMA’s two part design can be seen in the graphics below:

The DVM system is designed to levy the lowest fee possible to maintain that CoC > PfC as to not be rent-seeking. However, it is uncertain that a low level of taxation will necessarily lead to $UMA appreciation, and that $UMA value sufficiently grows in response to an increased demand for financial contracts (ie. a small %fee on a large financial contract does not necessarily translate to proportional UMA value accrual). Conversely, if the tax is set to high, this will detract from the value prop of creating synthetic tokens.

All in all, UMA is an exciting project that is run by a great team, and we will continue to monitor its progress. Be sure to look out for Yan’s piece on the implications of UMA listing on Uniswap tomorrow, as well as, our Oracle Thematic next month.

0 Comments