Valuing Layer 1s - Memes, Money, or More?

APR 26, 2022 • 30 Min Read

Report Summary

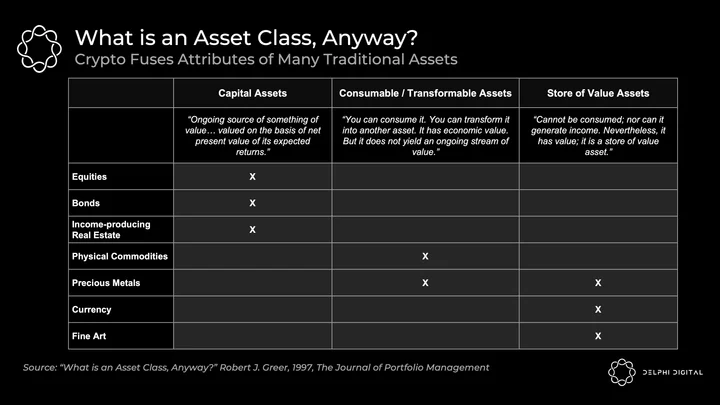

Traditional assets generally fall into one of three buckets – capital assets, consumable/transformable assets, and store of value assets. Crypto offers the unique ability to combine all three into one asset.

Meaningful revenue capture from network fees and MEV produces strong tokenomics. This directly feeds into attractive real yields for the native asset.

Long-term revenue capture must occur without hiking individual transaction fees, (i.e. scaling is needed). Monolithic blockchains appear unable to reach the scale required to capture the lion’s share of revenue.

Many-chain monolithic ecosystems such as Avalanche and Cosmos can achieve meaningful scale. However, this fragmented security approach inherently provides far less value capture back to the base asset. It will disproportionately accrue to subnets and zones, respectively.

We believe a modular stack with rollups paying rent back to the base layer could be the superior route for maximizing revenue to the L1’s native asset.

Introduction

Go grab a few bankers, and ask them how to value Apple stock. You get more or less the same answers about discounted cash flows, relevant multiples, etc. Then grab the most seasoned crypto minds around, and ask how do you value ETH? In fact, ask them why tokens have any value at all. Are cryptocurrencies really currencies? Commodities? Equities? Bonds? Mayhem ensues.

Go grab a few bankers, and ask them how to value Apple stock. You get more or less the same answers about discounted cash flows, relevant multiples, etc. Then grab the most seasoned crypto minds around, and ask how do you value ETH? In fact, ask them why tokens have any value at all. Are cryptocurrencies really currencies? Commodities? Equities? Bonds? Mayhem ensues.

Tokens fall into different buckets on that spectrum of “what the heck are these things anyway”? Some corporate valuation tools might already be quite useful for your favorite DEX. Boilerplate token rights include governance and treasury control which accrues transaction fees. Look no further than the Curve Wars for how valuable governance can be. Prioritize growth metrics for early-stage startups, and apply DCFs to more mature cash-flowing protocols. Decent logical fit.

The picture gets murkier when we introduce native L1 coins. Governance rights? Unlikely. Revenue capture for holders? Optional. In PoW networks, miners take the block rewards, transaction fees, and profit from MEV. Bitcoin and Ethereum have entirely off-chain governance. And yet, BTC and ETH have long dominated the leaderboard. These things matter, but it displays there’s a bigger picture here.

Let’s take Solana as an example where token holders directly capture network value through staking. In Anatoly’s words, Solana is a message bus. Then, aside from your proportional stake weight giving you a right to MEV, SOL is just “the thing that prevents spam in the message bus. That’s it.” Any value beyond that is unclear. So should SOL’s value just be equal to the NPV of its future expected MEV? Well then SOL’s market cap would be decimated even in the most aggressive projections.

Throughout this report, I’ll primarily use ETH and SOL for simplicity when explaining narratives. In reality, they respectively represent:

- ETH – Chains trying to capture sustainable value, as aggregate token value is important to the network’s vision

- SOL – Chains trying to minimize fees and value extracted from users, as they are agnostic to token value

I used SOL because Anatoly has been by far the most forthright and eloquent of anyone on his side of the argument which is necessary for healthy debate. I have incredible respect for this even though I’ll disagree with many of his arguments.

Why are Tokens Worth Anything?

In reasoning about fair value, Robert Greer’s 1997 paper, “What is an Asset Class, Anyway?” provides a helpful framework:

L1 cryptocurrencies can uniquely display features of all three for the first time:

Capital Assets – Sustainable Real Yield Accrues to Stakers & Holders

Call it an infinite duration bond (hi Arthur), call it a dividend stock, call it whatever you want. Yield talks. It speaks loudest amidst the backdrop of fiat’s negative real (inflation-adjusted) yield. All else equal, investors want positive real yield (e.g., staked ETH) over deeply negative (e.g., US Treasuries). Denomination matters too:

- ETH staking – future cashflows are in a deflating currency in ETH (making the real yield even more attractive)

- US Treasuries – future cashflows will be inflated away by the time you receive them

For ETH however, if you still denominate your returns in USD, then your dollar yield is exposed to ETH/USD volatility. If you denominate in ETH, you’ll happily stack your increasingly deflating asset. It’s a matter of perspective, and this is key – ETH needs to convince holders to denominate their investments in ETH (as we do in USD today).

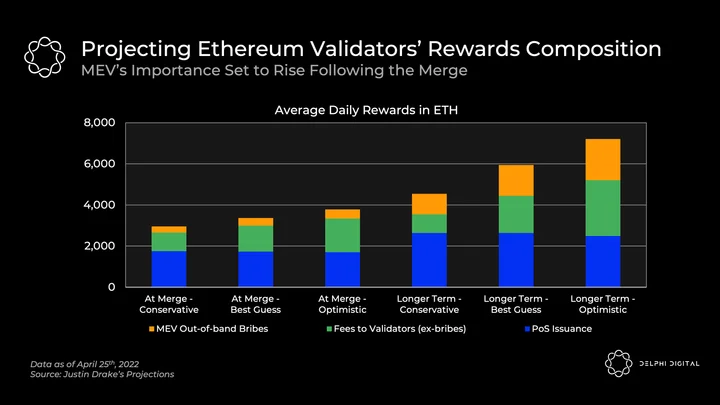

Emphasis on real yield here (as opposed to nominal). So, how do we make it sustainable too? Network activity. Staking rewards are composed of three sources:

Inflationary Block Rewards

Dialing this up will juice nominal yields, but it adds no value in proof of stake. Stakers are just picking the pockets of holders. The hype around Ethereum’s merge centers around the massive reduction in block rewards – subsidizing expensive miners is expensive and actively leaks value out of the token ecosystem entirely.

MEV

This bolsters the security budget and juices real yields. In an efficient market (with the help of projects such as Flashbots), searchers should eventually bid up to the full value of MEV as payments to validators.

Users won’t line up for sandwich attacks left and right though. Pragmatism dictates reducing exploitative MEV as much as possible then socializing the remainder (e.g., to stakers or public goods funding). Avalanche’s implementation of Snowman++ was one recent example of a protocol level change designed to reduce MEV.

For some context, Flashbots clocked Ethereum MEV in the ballpark of $500mm in 2021. From August 1st – December 31st, MEV for Ethereum, BSC, Avalanche, and Polygon respectively were at least $179.5mm, $34.79mm, $18.84mm, and $11.00mm. To be clear, these are all extreme lower bound estimates generally not even tracking major categories of MEV such as sandwich attacks, flash loans, and liquidations. The true scope remains a mystery.

Post-merge, MEV will accrue to ETH stakers rather than miners. Through Flashbots (which socializes MEV across validators), searchers can now pay for inclusion of transactions indirectly via a high gas fee, or they can set their fee to zero and offer a bribe to the miner/validator directly.

Following the merge, MEV is set to take a more important role in Ethereum than ever before as an increasingly large share of validator rewards. The below projections come from Justin Drake:

Transaction Fees

Fees accrue to stakers or burn (benefitting all holders). They directly improve overall tokenomics in either case.

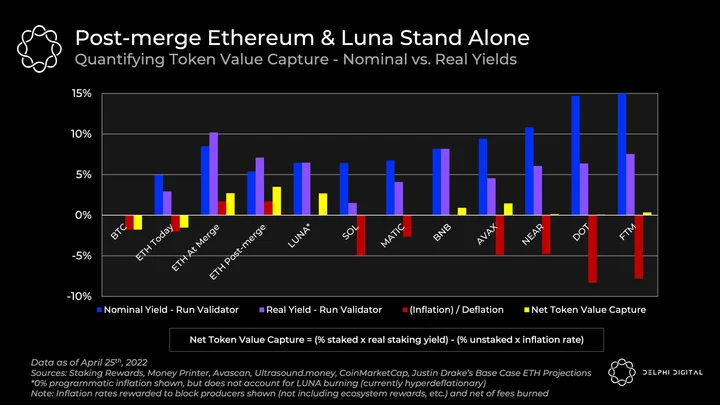

Net Token Value Capture = (% staked x real staking yield) – (% unstaked x inflation rate)

Nominal yields are headline rates, and real yields are net of inflation accounting for tokens burned.

This formula then captures the weighted average real yield across all token holders accounting for stakers and non-stakers. The first half weights the real yield of stakers. The second half weights the real yield of holders not staking (i.e., they lose inflation or gain deflation).

Real staking yields capture fees and MEV accruing to validators (only in proof of stake), as well as token burning which also benefits all holders (beneficial in both PoS and PoW).

Note this doesn’t penalize high PoS inflation as is often done with simpler value capture models such as fees minus issuance. Inflationary block rewards that stay in protocol are just shifting value from holders to stakers. A higher inflation rate changes my individual opportunity cost and decision of whether or not to stake. However, it doesn’t actually say anything about value capture for the overall token itself. You’re just dialing the needle of whether to benefit stakers or other holders. It’s net neutral to value capture either way, you’re just deciding who it helps.

This is analogous to the decision of whether to burn fees or give them to validators. In this situation value is captured either way, you’re just deciding who it helps.

If you’re buying a token for a long-term investment, you will logically intend to stake it and value it as such. So a higher block reward should not directly hurt any valuation methodology. The maturation of liquid staking derivatives will also make staking even more ubiquitous. Most L1s already have the significant majority of their supply staked (ETH is currently the outlier for obvious reasons), and this should increase over time. As a thought experiment, if 100% of a token is staked, I don’t really care if the inflation rate is 5% or 10%. It’s all just moving value around and I’m breaking even.

However, this metric does capture the fact that PoW block rewards do leak out of the ecosystem from all token holders entirely. As a BTC holder, I wouldn’t actually directly care at all whether network fees are high, because I can’t capture them by staking. BTC captures no upside. The real yield of BTC will therefore always be negative at the then-current inflation rate (the staking half of the equation does not apply).

Despite not directly penalizing PoS value capture for high inflation here, I do still believe that a relatively low inflation rate is valuable for monetary stability and premium. If one of these L1s hopes to move from “speculative investment” into real “money” someday (denominate your wealth in it, medium of exchange, etc.), a high inflation rate seems untenable. Even if it doesn’t directly harm a valuation, it causes price instability and makes it difficult for users to have the asset on hand (unstaked) for spending.

It’s important to consider inflation net of burn here, especially with several of the largest L1s such as Ethereum, Avalanche, and Solana all implementing burns. While Solana burns half of all fees (other half goes to validators), it has little effect considering how minimal fees are.

Outside of Ethereum, Avalanche has been the only chain racking up meaningful fee burns. Over the past 30 days, they’re burning more than 10k AVAX per day. That’s enough to offset around 1% of inflation annually, which I netted out in the graph above.

However, note that the majority of all Avalanche activity lately has actually come from a single game Crabada which is about to move off to its own subnet, and many of its current users appear to be bots. So take the recent numbers with a grain of salt.

The C-Chain implements a mechanism similar to EIP-1559 with the base fee burned and the tip going to miners. However, their pre-burn inflation rate of 5.8% we showed for uniformity in comparison does not include other incentives which are being distributed and add to inflation in a meaningful way, such as on Aave. The picture of inflation gets murky when you account for idiosyncratic mitigating factors such as this one, which must be considered. Inflation via incentives being dished out would directly leak value away from AVAX holders, as it isn’t circulating back to the token via staking rewards.

Post-merge ETH and LUNA stand alone in capturing meaningful value. All others are nearly flat, with yields just acting as a tax moving from one pocket (holders) to another (stakers) in a sleight of hand. AVAX is next in line, but it’s important to consider the mitigating factors mentioned above.

EIP-1559 needs no introduction. The burn offsets part of today’s inflation, and will turn ETH deflationary at the merge when miner subsidies disappear. Additionally, priority fees and MEV bribes will start accruing to validators.

Right at the merge, the percent of ETH staked will likely be quite low with a very high staking yield. Then the yield will get diluted back down post-merge assuming the percentage staked rises up to around a third in the slightly longer term projection also shown.

Terra is special. LUNA has multiple sources of staking yield:

- Gas Fees – Transactions incur a small gas fee. This revenue is incredibly small for Terra.

- Stability Fee Tax – Charged on all stablecoin transactions up until January. It was capped at 1 SDT per transaction, accounting for a very small portion of revenue. It was set to a 0% tax rate with prop 172.

- Market Swaps – This is the money maker.

Terra takes a cut whenever you use the Terra Station market swap function between Terra stablecoins or between them and LUNA. (Terra Station also integrates Astroport and Terraswap where these fees don’t apply, but you’re using their respective LPs and fees as opposed to Terra’s market function.)

Fees funnel into the Oracle reward pool and are dispersed to validators (in return for reporting exchange rates). Validators then distribute these fees to delegators in the form of staking rewards over a two year period.

These fees come in one of two forms:

- Tobin Tax – Fixed % fee for swapping between Terra stablecoins, with most set at 35bps (e.g., UST → KRT)

- Spread Fee – Fee for swapping between LUNA and any Terra stablecoin. Set to a minimum of 50bps, though it can readjust higher in volatile periods to maintain stability by keeping a constant product between the Terra pool and the fiat value of the LUNA pool.

The graph above displayed LUNA’s inflation rate at 0% (there’s no inflationary block reward) for an apples to apples comparison. However, this doesn’t account for the fact that LUNA has actually been incredibly deflationary. Accounting for seignorage burn would’ve broken the graph above with massive net token value capture, and it’s difficult to compare as the deflationary rate can be volatile.

Prior to the Columbus-5 upgrade in late 2021, a portion of LUNA used to mint UST was sent to a community fund to finance the development of the Terra ecosystem, a portion was rewarded to validators, and the remainder was burned.

Following Columbus-5, when fresh UST is minted for LUNA, the LUNA returned to the protocol (seigniorage) is entirely burned. So for every $1 of UST minted, exactly $1 of LUNA is burned.

Note that the current LUNA staking yield also includes previously earned seignorage from the oracle reward pool (prior to Columbus-5 burning everything). This is because rewards accrue to the pool then vest to stakers non-linearly over time. Columbus-5 then reduces the staking yield over time, but realize this value is still being captured on an ongoing basis through seignorage burning (which we did not include in the graph as deflation).

LUNA is generating nearly all of its current revenue from native stablecoin market swaps. This provides an interesting takeaway for other L1s – implementing a native stablecoin mechanism internally could provide meaningful organic revenue. Note this contrasts with Near’s recently launched USN, which is managed by an independent DAO Decentral Bank.

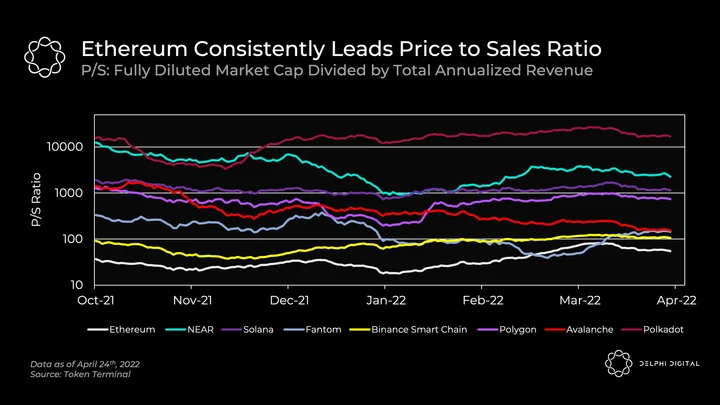

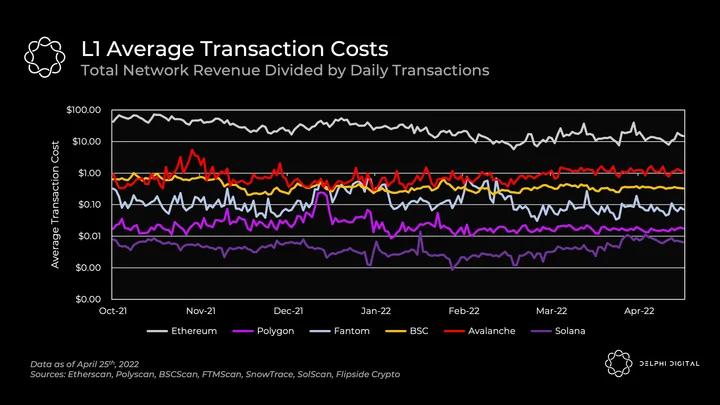

Ethereum has firmly led the pack in P/S, except for a brief period where Fantom activity spiked. BNB Chain and Fantom have otherwise come next, though at respectable levels compared to most others. The other notable contender here is Avalanche, chugging along capturing more and more revenue lately.

P/S is a helpful barometer of real demand today, but reading too much into this in isolation would provide a very incomplete picture. Growth is the other half. For example, Fantom and BNB Chain can trade at “cheap” multiples because they currently lack innovative catalysts relative to other chains here. AVAX trades higher because they have stronger growth prospects in our view, and so on. These multiples aren’t to be religiously adhered to and compared as they are in tradfi, but they’re helpful in forming a picture.

The graph below displays the dilemma chains face. Ethereum is expensive to use, Solana is cheap, and the rest fall somewhere in between. Alternate chains have gained traction primarily because they can offer much cheaper fees than Ethereum. However, they eventually need to scale throughput to capture more value without jacking up individual transaction fees (easier said than done) or they risk losing their customer base.

Consumable / Transformable Assets – Gas

Crypto as a commodity. Ethereum is an engine, and ETH keeps it humming along. Higher network activity → buy ETH to pay more gas fees.

Keep an eye on how this develops in a more modular stack with rollups, as they can allow users to pay gas in the token of their choice. Adding an L2 user would therefore increase marginal holder demand for ETH less than adding a user on the L1.

Under the hood though, rollups will still handle the conversion and pay rent back to the main chain in ETH. Ethereum will take its cut for hosting data-hungry rollups while also coordinating settlements and transfers.

This contrasts to many-chain monolithic ecosystems such as Avalanche which lack shared security and settlement. New subnets can have gas paid in the native token of their choice (not so different from rollups). However, subnets must bootstrap their own validator sets, so paid fees there will accrue to subnet validators (not Primary Network AVAX validators).

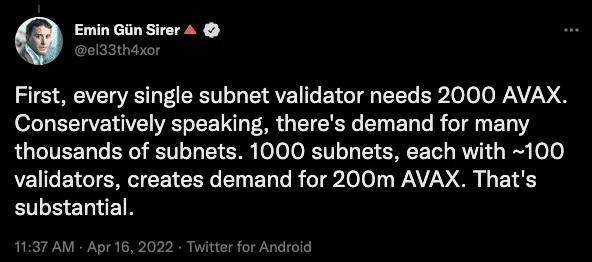

The potential benefit to AVAX would come from the fact that new subnets must validate the Primary Network by staking at least 2,000 AVAX. Here’s that bull case as recently laid out by Emin:

Firstly, thousands of subnets each with ~100 validators is not a “conservative” estimate. Even 100 subnets over any reasonable time span is a strong assumption.

100 validators per subnet directly contrasts Ava’s own docs recommending the following for subnets: “For network security and stability, we recommend 5 validators (each in a different region) for a minimal production setup. 10 validators should be enough to balance off the security, stability and future needs.” An average of 100 validators across a long tail of subnets is unrealistic.

It also assumes that every subnet validator is a completely new AVAX validator (i.e., causing 2000 AVAX new market buy pressure). In reality many will likely be existing Avalanche Primary Network stakers locked up today. Similar block producing entities across the ecosystem would be expected. As a result, no 2000 AVAX new buy pressure.

Additional staking demand from subnets will be very marginal.

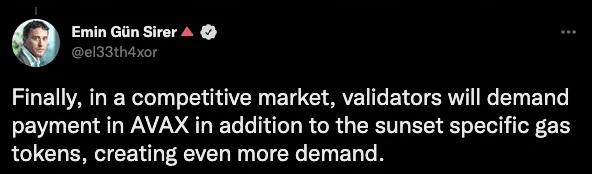

Emin also argued:

The assumption that AVAX will be “demanded” by validators on subnets seems unlikely. For example, the DFK subnet uses only JEWEL for gas. These fees are split between a burn and payment to the subnet’s validators. It is in any subnet’s self-interest to position their own token for value accrual in this way. It owes no rent back to Avalanche. At best, user-conscious subnets could allow gas to be paid in several different tokens for convenience (in which case AVAX would certainly be an option).

The biggest factor is value capture back to AVAX, and subnets fundamentally will not do this. Subnet fees accrue to its own validators. Only if subnets for some reason demanded gas to be paid in AVAX and burned it would benefit accrue directly to AVAX (which seems very unlikely).

Even in the bull case which over a long time period results in more staked AVAX, this moreso resembles the Polkadot model where DOT is locked up to secure a parachain. It never hurts to have more supply locked up, but that doesn’t make AVAX a more productive asset. Productivity comes from additional revenue capture. However, subnets will not contribute here unlike rollups.

Dankrad put out a good post last year which described why productive assets (i.e., fixed supply is not enough) are the superior form of long term store of value. This shouldn’t be hard to understand, as we already see this today. Did you want to save in gold or the S&P 500 over any long time period? The best long-term store of value needs to be better than just a sturdy rock, it’s necessary to also have meaningful value capture over the long-term.

Subnets will drive exciting innovation and activity, but the gains will disproportionately accrue to the native subnet tokens which receive the transaction fees and token burn rather than AVAX. This looks closer to what’s played out with ATOM as the Cosmos ecosystem develops vs. ETH’s role on rollups.

Of the non-Ethereum chains shown, Avalanche has the clearest roadmap to massive throughput because it splits across many chains (subnets). This similarly applies to Cosmos. However, this approach fractures security and inherently removes most of the value capture back to the main token.

Store of Value Assets – Monetary Premium

“Cryptocurrency” is often a misnomer, but sometimes it isn’t. So can our magic internet money really become money? A store of value? Medium of exchange? Look no further than ETH’s “ultrasound money” meme and you’ll see there’s at least an effort to get there.

Realize that we are building entire digital economies and countries. It makes sense then to think of their coins as real money then too.

Asset price = quantifiable utilitarian value (e.g., discounted future cashflows) +/- some arbitrary speculative or monetary premium. USD has been the global reserve asset (the highest monetary premium) so long as it’s backed by the world’s dominant economy and you could park that cash somewhere to earn yield (Treasuries).

Similarly, a cryptocurrency investor wants to see:

- Strong economy – Which L1 is facilitating the most economic activity? Where do most users want to spend their money?

- Balanced budget – Are you running at a deficit and inflating your currency away, or are you collecting enough revenue? Which ties into:

- Positive real yields – As with any country today, higher real yields attract capital inflows and strengthen currency.

USD is the go-to medium of exchange for global trade. Look no further than the petrodollar system to see the benefit to the US. It drives USD in global reserves – exporters receive dollar payments and importers need dollar reserves to purchase oil.

The green shoots of ETH as a quote currency arguably arose with the ICO boom. It has proliferated further with the recent NFT boom. Whether you wanted to participate in the hottest ICO or NFT drop, you needed ETH. These effects snowball when people start to completely denominate their wealth in ETH:

However, ETH wouldn’t have the value it does today if it’s only role was as a high velocity currency that you just wanted to spend (like USD). Large US investors don’t hold actual cash, they own higher yielding dollar investments like treasuries. ETH in your wallet is the USD of the Ethereum ecosystem. Staked ETH is US treasuries, the baseline risk-free rate of the entire economy, except with more sustainable economics (i.e., deflation + real staking yield vs. inflation far outpacing incredibly low US Treasury yields).

Not to mention crypto-native unique innovations such as liquid staking tokens (e.g., stETH) let you have your cake and eat it too – liquidity, yield, and the ability to stack money legos on top.

ETH’s ability to combine monetary denomination with attractive investment qualities (deflationary + yielding) makes a great benchmark. It’s the new S&P 500 for fund managers to beat:

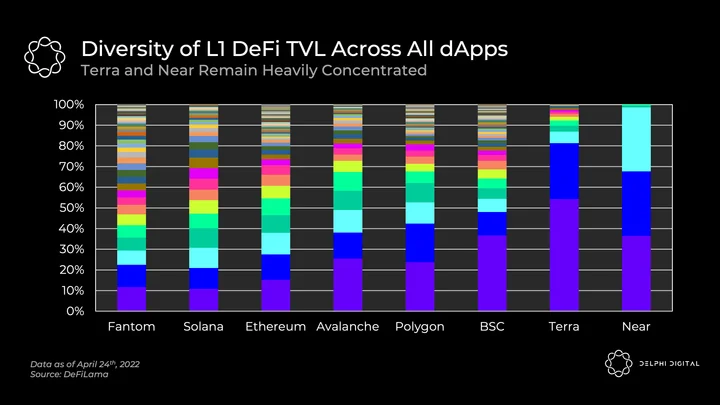

Economic diversity also adds to the stability of economic strength. Reliance on just a handful of applications brings meaningful risks. This is most notably the case for Terra and Near, though Near is still very early on in growing out its TVL:

What’s Under the Hood

If Ethereum’s scaling roadmap fails, you can talk about the burn until you’re blue in the face, but you wouldn’t want to hold ETH. If the US ran a balanced budget but its GDP tanked, USD is no longer the global reserve asset. Good tech will still drive adoption.

You can’t build a country without land and resources, and you can’t build a crypto economy without blockspace. Jacking up prices drives the incremental customer to cheaper alternatives. Growing the pie requires increasing throughput while driving down individual transaction costs. Blockspace demand is quite elastic, and it always gets chewed up. Scaling enables new use cases and attracts new users.

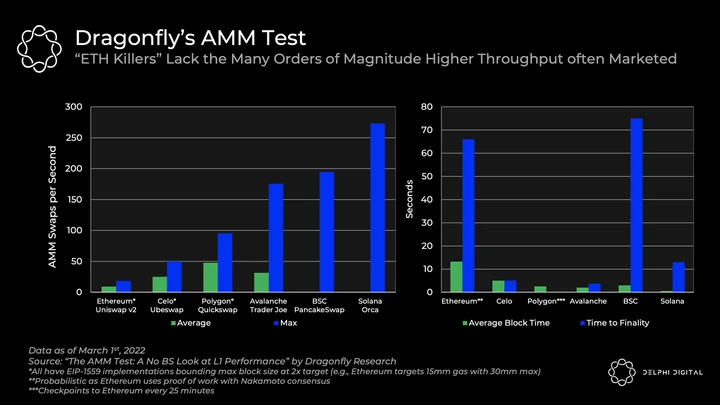

Not to rehash our recent breakdown here too much, but realized TPS (over-simplified measure of throughput) has generally ranged from low double digits (in Ethereum) to somewhere below 1,000 for Solana (excluding voting transactions). Far below the marketing numbers we’re used to seeing. Avalanche currently displays its transactional throughput as “Infinity tps (with subnets)” relative to other L1s. While theoretically true, the point is many outlandish TPS claims we see are simply not helpful or apples to apples comparisons.

Dragonfly ran a great test recently comparing max AMM swap throughput across chains as a uniform benchmark, and the results were even more tightly packed:

The delta from Ethereum is there, but it’s nowhere near the wild TPS numbers we often see marketed. Even the winner Solana only clocked in at ~273.3 trades per second. Note that Solana uses transactions for each internal consensus message unlike other chains (accounting for ~80% of its TPS).

Also, this test only taps out Solana’s single threaded execution. This doesn’t give credit to Solana’s key advantage – parallel transaction processing leveraging multiple cores. However, this is a realistic benchmark because whenever Solana does have network issues, it tends to come from a single hot market all grabbing at the same state (e.g., the Raydium IDO). At this point, throughput becomes bottlenecked by that single core execution anyway.

The orders of magnitude scaling required will come across many chains. This realization is already underway – Cosmos zones are gaining traction, Avalanche is bringing online new subnets, while Ethereum and Celestia are targeting rollups.

Conflicting Visions

Metrics displayed here are incredibly valuable for diagnosing the state of these networks. Short-term valuations can get out of hand though. It’s important to understand the long-term dynamics of value creation at play.

Let’s consider the two extreme approaches as case studies.

Solana’s Vision

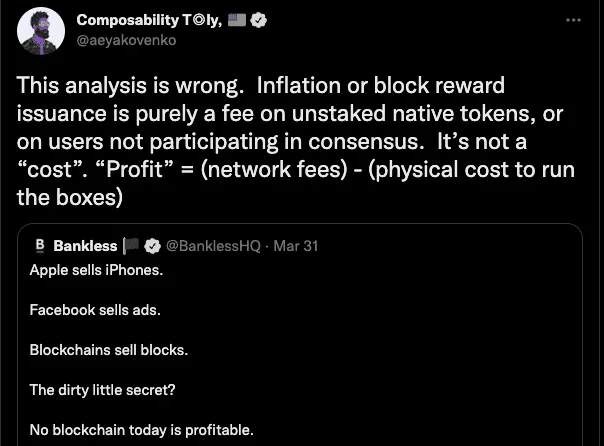

Solana’s objective is not to drive native token value. The stated value of SOL is simply the net present value of discounted future MEV cashflows.

The discount rate would settle around the risk-adjusted cost of capital for holding SOL at which point validators will stake in return for the right to capture MEV. The amount of future MEV required to back into a net present value of SOL’s current market cap would need to be sizable. You can play around with the assumptions, but in any scenario they require scaling several orders of magnitude from here.

Network transaction fees in an efficient market should then settle at validators’ operating costs, primarily:

Cumulative fees = Bandwidth cost + hardware cost + SOL voting tx fees

So effectively MEV would cover your CapEx (staking SOL), and fees need to cover your OpEx (bandwidth, hardware, and voting transactions).

Any transaction fees captured meaningfully beyond that would be viewed as extractive from users, and represent the profit to validators. In which scenario competitors should theoretically arise and undercut the network for 0 profit. It’s an admirable vision if it proves feasible to provide this service to the world at next to zero cost. But it does raise the question of value capture we’re discussing in our research here:

Ethereum’s Vision

The community makes significant effort to imbue ETH with value beyond the minimum utility. They want investors to buy, hold, and stake because it’s an incredibly attractive capital asset to hold. It’s the large liquid asset that you will safely denominate your wealth in, and its staking rewards will serve as the baseline risk-free rate of the emerging crypto economy. The key to capturing the most value is structuring attractive monetary policy (e.g., EIP-1559) to give your native asset monetary premium. That’s the endgame.

Does Token Price Matter?

Ok so we’ve settled on two models. Imbue your token with value as an attractive asset for hodlers, or run the network at bare bones costs and let the market figure out a token value. If that number is incredibly low, so be it.

But is that second approach sufficient? Does the network care about number go up? Or are the ETH maxis just sitting around jerking to the burn?

As Anatoly mentioned, you need a transaction fee as spam resistance to prevent the network from getting DOS’d. But the real reason is to maximize the staked value required to attack the network. All the other bells and whistles are optional, but the fundamental reason why all of these coins need to exist in any proof of stake system is for sybil resistance.

That’s why there’s this tricky balance with transaction fees and MEV. They are the sustainable sources of yield to token holders. If left unchecked though, they can be extractive and drive users away. You can have the most deflationary currency in the world, but it’s lipstick on a pig if nobody’s using your ghost chain.

On the flipside, you might settle trillions in value per day because everyone loves your cheap fees. But if that high value network is secured by a low dollar value of staked assets (because nobody wants to hold your monopoly money), then you’ve got an inherently unstable network vulnerable to attack. It’s possible to support the scale of today’s market caps on speculative bets for future growth, especially in the short-term. But growing into orders of magnitude greater value will mean attracting massive amounts of sticky capital.

Does the dollar amount of stake weight matter that much for security? “Security” as Solana views it is defined by the cost to destroy all replicas of the chain, because that’s truly unkillable:

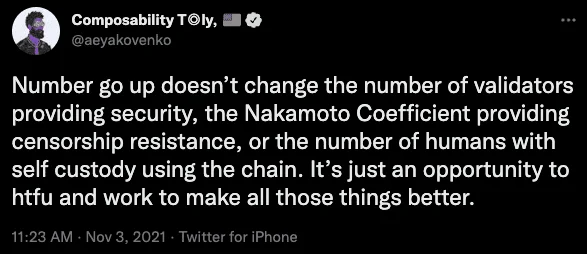

Solana’s stated goal for “decentralization” (which is important for censorship resistance and liveness) is then to maximize the Nakamoto coefficient (# of colluding validators needed to halt the network). In theory, high Nakamoto coefficient → not feasible to attack the network.

Your Nakamoto coefficient could be a trillion though, but if their cumulative stake is $1 I could overtake them myself. Extreme example, but you get the point. Number of validators in isolation means very little, especially if you assume that a large attacker disguises itself behind many entities as would logically be expected. A high Nakamoto coefficient helps defend against an attacker corrupting many distributed nodes, but it does nothing to prevent an economic attack. In this respect, Solana’s goal of maximizing the Nakamoto coefficient appears at odds with the indifference regarding token value capture, as one without the other is insufficient.

This is particularly concerning because Solana is ill-equipped to deal with this attack. Anyone can fully validate Solana, but that requires meaningful capital and effort that the 99% of users will never be able to do. Networks such as Ethereum or Celestia with a religious adherence to allowing everyday users to rest behind near full node security (with low capital and hardware requirements) are far more capable of dealing with and recovering from a 51% attack. Cryptographic assurances are always preferred to cryptoeconomic ones. If all your light clients know not to accept the invalid chain being attacked, you greatly mitigate the damage that can be done.

Anatoly often argues that Solana is optimized for “stopping the first strike in a nuclear war” (by maximizing the Nakamoto coefficient and real time censorship resistance to prevent a majority attack), and Ethereum is optimized for “picking up the pieces” after. However, an insurmountable staked value is just as important as the Nakamoto coefficient to prevent the strike.

The argument here may come down to the fact that even at a relatively lower market cap, taking over the network would be difficult to make personally profitable. It seems unlikely that someone would try to spend tens of billions of dollars to attack a blockchain in the hope of making a quick buck and getting away with it. It would more likely be a state actor acting maliciously to take down a globally important network for low economic cost relative to the damage inflicted. At this point, it may come down to a fundamentally different view with the community:

Anatoly has been clear “If you’re not in trouble with the US, Europe, or China it doesn’t matter, nothing else matters. If you are in trouble with one of those, nothing will help you. So this is why I’m not worried about those attacks. I just don’t care.”

So if the only attack that a massive market cap is protecting you from is a state actor, why bother? Just acknowledge that threat exists, then ignore it and build the best damn machine you can. Solana is working to do just that.

If we really are building the future of France on top of these networks though, I want the strongest assurances possible. Even against a state actor. It seems irresponsible to build a systemically important network for the global economy that an adversarial government could easily attack. You don’t have to look around too hard to realize that economic and cyber warfare are increasingly the preferred methods of offense. These systems must be designed in such a way to make these attacks cost in the many trillions of dollars so as to be infeasible. If number go up helps to protect that, then so be it!

This security argument alone also ignores the moral argument and overall need for a robust base layer asset in this new digital world, especially with BTC’s potential shortcomings. This is an argument for another day, but an important role that I believe in and many in the crypto community clearly want as well.

Showdown – Modular v. Monolithic Value Capture

ETH needs to grow rapidly in relation to the network value because it secures the whole thing.

Tying back to many-chain monolithic systems, it becomes clear why a massive token price is simply not required. AVAX’s price will not as directly benefit from the growth of its subnet ecosystem, but it doesn’t really need to. Their vision from its fundamental design does not provide shared security. There is no need for the price of the largest asset in a many-chain independently secured monolithic system to track the growth of the surrounding ecosystem.

Monolithic chains are inherently at a disadvantage for fee capture because they are capped at:

Fees = Throughput x $ users will pay for individual transactions

Modular data availability, consensus, and settlement layers (such as Ethereum) by design will capture far more value. They are capped at:

Fees = Throughput x $ users will pay for aggregated transactions

This is the key point for future fee revenue projections.

A rollup would pay Ethereum a massive fee in a single transaction to secure an entire rollup block of potentially thousands of individual transactions compared to what a single user would be willing to pay for a swap on the Avalanche C-Chain for example. Additionally, it is technologically feasible to securely scale a data availability layer (such as Celestia’s or Ethereum’s designs) orders of magnitude further than a monolithic chain. You’ve now maximized both parts of the equation compared to a monolithic chain.

The one important negative externality of rollups on the base layer asset to note is MEV extraction. Individual users will likely all leave the Ethereum L1 eventually. As this happens, MEV capture will progressively shift to rollup block producers. However, this shift will naturally coincide with rollup fees paid back to the L1 ramping up massively. Pure data availability and consensus layers such as Celestia and Polygon Avail from the start will not capture MEV as they have no enshrined execution, and thus will rely on fees alone.

If Layer 1 crypto economies hope to reach the scale of massive global importance, then sustainable value capture is critical to their long run health.

The most secure modular base layers (data availability, consensus, and settlement) by design will capture the most value of any single chain because they can scale the furthest and their blockspace is the most valuable.

0 Comments