2022 Crypto Year Ahead: Themes, Projects, and Trends We're Watching

JAN 27, 2022 • 40 Min Read

As we kick off 2022, we asked the Delphi research team to identify the themes they’re most excited about this year. Admittedly, many of these items are themes we’ve been actively publishing research on and investing in already. Still, we wanted to take this opportunity to reframe where we are, major catalysts and narratives, and the key projects we’re tracking in the new year.

Key sectors & themes we’re watching:

So without further ado, let’s dive into some of the top ideas and themes.

Note: all calculations related to pricing data and returns were conducted before last week’s market sell-off (unless otherwise specified). Our opinion on the themes and projects mentioned in this report has not changed. The latest market drawdown has provided even more attractive entry points for many of these opportunities (assuming you’ve done your own research and have built conviction in some of these names). For those interested in our latest market commentary, see here, here, here, and here.

The Scalability Wars

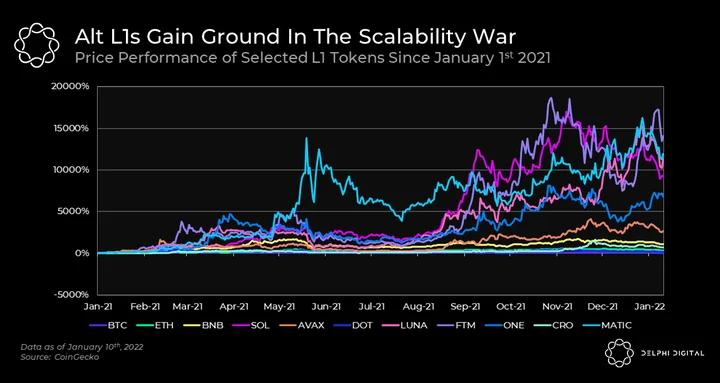

Alternative L1s were among the most dominant trends in 2021, with names like LUNA, SOL, and AVAX garnering a ton of investor attention. Meanwhile, ETH struggled to curb high transaction fees despite all the hype behind L2 solutions and the move to ETH 2.0. (For more detail, revisit our report discussing the end game of L1s and L2s.)

The “Scalability Wars” will continue to heat up as L1s battle for market share through their unique approaches to scaling throughput, reducing transaction costs, and attracting the best developer talent to their ecosystems. High fees and congestion on Ethereum will continue to push founders and developers to alternative L1s until L2 solutions become more popular (i.e., StarkNet, dYdX for trading, Immutable X for NFT minting/trading).

The latest market sell off has weighed on many of these, though we have seen names like LUNA and ATOM weather the storm better than many of their peers; their relative outperformance make them ripe contenders for further gains if and when the market does make a sustainable comeback.

NARRATIVES TO WATCH:

-

Developer Interest: Continued adoption and usage of alternative L1s is one of the most common themes our analyst team is bullish on next year, as it’s a sector we’ve been researching and publishing on for quite a while now (see our reports on AVAX, LUNA, and The L1/L2 Endgame).

-

“The recent strength of SOL, LUNA, and AVAX is notable, especially versus the ghost chain alternatives; it feels like the market is becoming more efficient. As institutions and “smart money” enter the space, these investors care more about user adoption/traction rather than promises/narratives that can drive retail. This new wave of capital is looking to invest in technologies that will capture hundreds of millions of users.” – Duncan (Twitter @Floodcapital)

-

-

Scaling Solutions: Popular L2s will get battle-tested as more applications—both financial and consumer-centric—are built, requiring low latency and lower transaction costs. Given the success of L1s over L2s, it doesn’t seem unreasonable that there will be some experimentation with L2 tokens to attract users and build communities.

-

“At this point, it’s pretty clear that tokens are the most powerful incentives for attracting attention and capital. Expect TVL across L2s to skyrocket past the current combined $5.6B as they roll out the red carpet for projects with their own fresh token incentives building natively on L2s and other dapps migrating from other chains to L2s. Two more major catalysts would be the continued support of CEX to L2 integrations to onboard retail and L2s releasing their own tokens. Similar to how many alt L1s to from 0 to 1 we can expect a similar pattern to play out on L2s as it relates to DeFi, Gaming, and NFT primitives.” – Alex G. (@Alex_Ged)

-

“Starkware, all forms of ZKrollups, and Optimistic rollups are extremely exciting. They offer a great opportunity to scale ETH. And, thanks to the reports by our own Can Gurel, I am really looking forward to modular chains like Celestia.” – Aaron (@crypto826)

-

-

Modular Blockchains & Data Availability: The rise of Rollups brought along the concept of Modular blockchains. A full-fledged blockchain is made up of three core components: execution, settlement, and consensus & data availability. Yet, a blockchain doesn’t need to perform all of these functions on its own. Instead, modular chains specialize in one or more of these components and outsource the rest to other specialized chains to achieve higher scalability. For example, a core element of the modular blockchain stack is specialized data availability chains such as Celestia which have a very high data capacity. Many rollups can make use of this capacity by choosing to dump their data to Celestia for shared security all the while focusing on scaling their execution.

-

The ETH Merge: How could we forget arguably the most important milestone in Ethereum’s history, marking the shift from PoW to PoS? This long-awaited event should not be overlooked, but it has flown under the radar since there’s no hard deadline set for the merge. Public estimates target late Q2 at best, but you can follow along here for updates. Here are a few post-Merge consequences from an investor’s lens:

-

ETH Staking Yields: Post EIP-1559, ETH fees have been split into two components: the base fee and tip. (The base fee is burnt, and the tip goes to miners.) After the merge, the tip portion of the fees will go to validators/stakers. This tip revenue alongside block inflation going to stakers will turn ETH into a positively yielding asset.

-

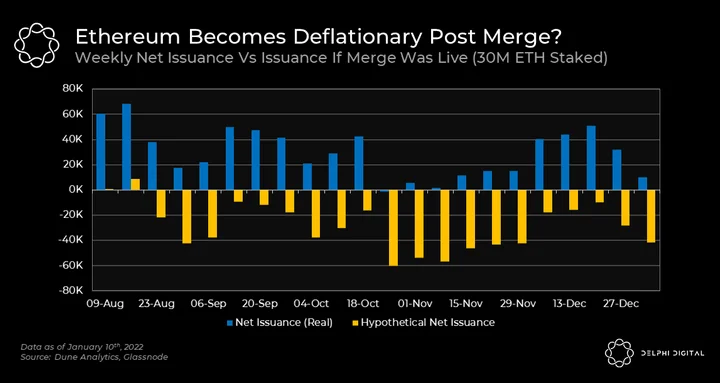

Net Deflationary Asset: Since EIP-1559 went live in August, ETH has had one net deflationary week. If we retroactively show the merge being live at 30M ETH staked, ETH would have been deflationary every week since August 23rd. Currently, the ETH 2.0 deposit contract only holds ~9M ETH, so 30M is quite conservative. But we feel this is a solid medium-to-long term figure to use while projecting ETH issuance. With 30M ETH staked, issuance is slashed from the ~13,400 a day to ~2,700.

-

- Institutional Capital Inflows: The second most liquid crypto asset—now with a more sustainable monetary policy—that also offers higher yields in a low yield macro environment adds another layer of upside for institutional investors. Coupled with the shift to a “greener” and more energy-efficient model, we expect to see more capital inflows targeting ETH in the coming months.

-

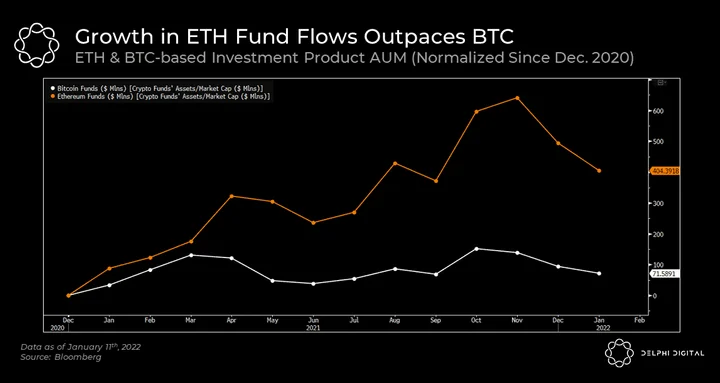

Notably, institutional capital flows have started to broaden outside of BTC and ETH as more TradFi investors fall down the proverbial crypto rabbit hole. This is likely to benefit larger liquid alternative L1s in the top 10-20 coins, as most institutions are unlikely to dabble in smaller, less liquid names. The increasing accessibility of crypto assets beyond BTC and ETH will help accelerate institutional capital flows into these smaller yet prominent names.

-

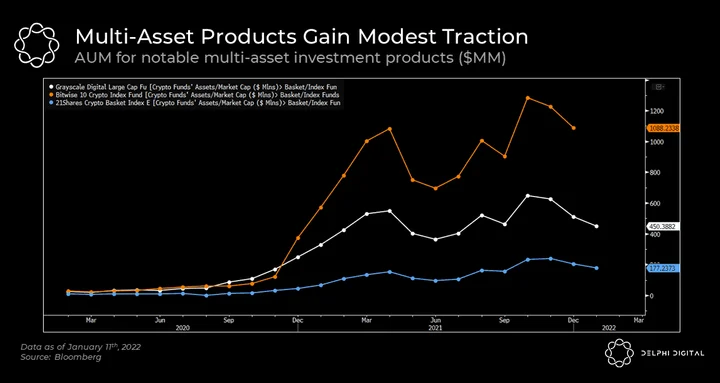

Multi-asset investment products haven’t seen a ton of demand yet, with their total AUM at ~$4.2 billion versus $35 billion for BTC-based products alone. Notable providers include Grayscale, Bitwise, and 21 Shares.

-

-

-

S

-

Read the full report

This report is part of Delphi Pro.

- 800+ Pro reports across every major sector

- Talk directly with our analysts

- Private community of funds and builders

Already a Pro member? Log in

0 Comments