Zetachain Part 2: The Opportunity Ahead for Omnichain Applications

JAN 04, 2024 • 47 Min Read

App Building Opportunities

Zetachain’s ability to support smart contracts and connect to heterogeneous chains – including the Bitcoin blockchain – opens the gateway to omnichain applications.

Omnichain apps are smart contracts deployed on the EVM-compatible Zetachain. While the application logic and state of omnichain apps entirely exist on Zetachain, they have the ability to directly manage foreign assets on supported external chains (Bitcoin, Ethereum, etc.). This paves the way for some novel applications that cannot exist in other environments.

If we look at the aggregator landscape today, they’re mostly DEX venue aggregators. There isn’t a lot of aggregation happening on other kinds of DeFi primitives or across multiple chains. Take the example of the 0x API or Matcha. Matcha can allow users to aggregate liquidity from various venues in a single ecosystem — but not across ecosystems.

When trading a spot pair like ETH-USDC, this doesn’t matter; all relevant liquidity sources are on Ethereum anyway. For tokens that have portions of its supply on various chains, the current cohort of aggregators do not help users tap into all available liquidity. With derivatives, cross-chain aggregation would result in superior trade execution quality.

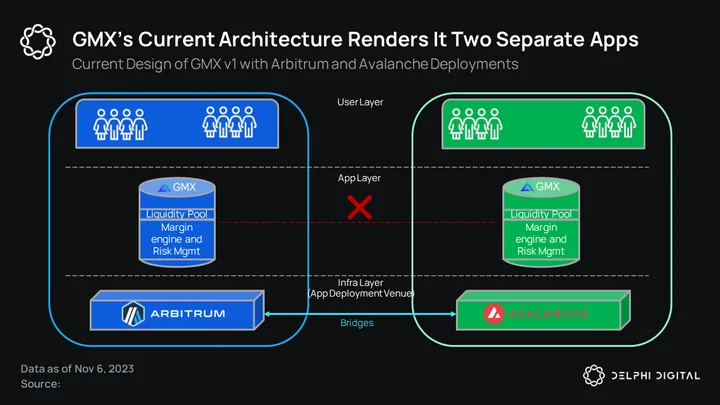

Think of a protocol like GMX that exists on both Arbitrum and Avalanche. Arbitrum is GMX’s home chain, and this deployment facilitates far more volume than the one on Avalanche. However, trading activity and token volume on Avalanche are still meaningful.

Traders on Avalanche have to make do with accessing just 15% of GMX’s global liquidity since 85% of the protocol’s AUM is on Arbitrum. There’s no way for traders on Avalanche to access this without bridging their collateral to Arbitrum and swapping some AVAX to ETH for gas.

For GMX token holders or LPs who earn GMX token rewards, liquidity on Avalanche is far less dense than liquidity on Arbitrum. This means to optimize for the best execution, GMX holders on Avalanche must bridge their tokens to Arbitrum. They cannot access the liquidity that sits on Arbitrum from Avalanche. And this is where Zetachain’s value proposition starts to take hold.

Essentially, GMX today is like two separate apps where the blockchains they are deployed on — Arbitrum and Avalanche — can bridge assets between one another, but the GMX contracts on each chain cannot communicate with each other.

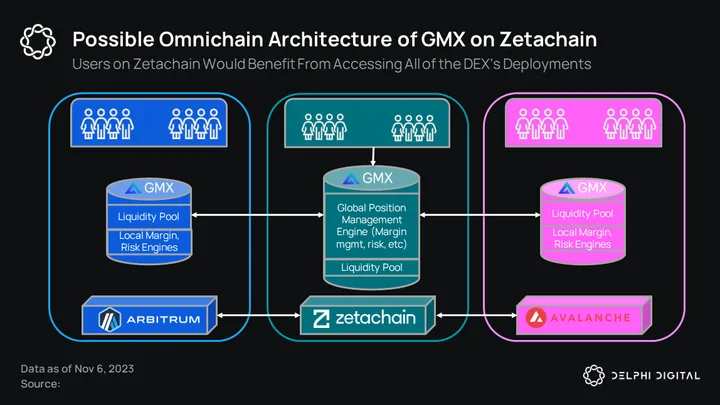

Hypothetically, if a GMX hub was deployed on Zetachain with spokes on Avalanche and Arbitrum, it would be relatively simple to work in cross-chain swaps and margin trades.

In this section of the report, we are going to explore the most essential app-building opportunities that exist for Zetachain.

Omnichain DEXs

Let’s continue our example of a hypothetical GMX hub on Zetachain with deployments on EVM chains like Arbitrum, Avalanche, and others.

The primary GMX protocol is deployed on Zetachain. This is what controls GMX’s deployments across several chains. There is a global position management layer on Zetachain that takes care of margin requirements, risk monitoring, and even executing multi-chain liquidations. On each chain, there is an instance of the DEX with different baskets of assets that LPs deposit tokens to and traders utilize for liquidity. Some assets — like BTC, ETH, USDC, and USDT — will likely exist in each chain’s basket. But there will be differences. Arbitrum’s basket would have ARB, UNI, LDO, LINK, and CRV; the Avalanche deployment would have AVAX, JOE, and QI; and the Polygon instance would have MATIC, BAL, BAND, and RPL.

Unlike the state of cross-chain deployments today, with Zetachain used as the base layer for the protocol, you could achieve liquidity interoperability between all of these different deployments. For example, a user on Zetachain could post their margin to the hub contract and have positions on all three instances of GMX. This is a core assumption to cross-chain apps on Zeta — the position management layer would sit on Zeta, therefore users who want to take advantage of GMX’s full liquidity basket have to use Zetachain.

There are two key benefits here, barring execution quality:

- The ability to split orders for an asset across various liquidity sources, similar to the MUX aggregator.

- Access to more trading pairs without having to manually bridge to all relevant chains.

The smart contract on Zetachain can directly deposit the required amount of posted margin to the relevant chain with a message for how these assets are to be utilized i.e. open a 3 ETH long position. While this process is technically achievable without Zetachain, the UX improves considerably when the user only has to:

- Interact with one chain.

- Can globally manage their position instead of managing each leg individually.

It’s difficult to conceive of Uniswap, the DEX market leader, moving its base hub from Ethereum to any other chain. But theoretically, by deploying on Zetachain and utilizing the ZRC-20 standard, users could swap in and out of any asset (on any chain), and custody said asset on whichever chain they desire.

If a user is particularly tied to Arbitrum they could, for example, do their ETH-USDT and AAVE-ETH swaps using liquidity on Ethereum without ever moving off Arbitrum directly. The assets would move from Arbitrum to Ethereum and back via Zetachain. From a cost perspective, it obviously makes more sense to custody ETH and AAVE tokens on Ethereum itself. This example is simply meant to illustrate how a chain with native smart contracts and a bridge improves the experience of accessing cross-chain liquidity.

The UX of in-built bridging and smart contracts that can interact with each other across chains is far superior to the experience of manually bridging funds around to achieve a desired end-state. And this stands to significantly improve the UX around trading on DEXs.

Consumer Aggregation Apps: Improving the On-Chain Derivatives Experience

Derivatives are likely the least composable type of asset across the on-chain spectrum. With each protocol’s derivative contracts bound by natively set margin requirements and a lack of position representation standards, it is extremely difficult to achieve composable derivatives. Composing with money markets could be a reality in a world where:

- A money market deeply understands the underlying risks and is willing to allow traders to utilize these positions for additional margin.

- The derivatives DEX gives users a position representation token (ERC-20, ERC-721, or otherwise), which is not the norm today.

However, composability across derivatives protocols — in the way someone can swap ERC-20 tokens on any Ethereum AMM — is not viable as there is no standardization.

As a result, users are forced to use certain derivatives DEXs and commit to fragmented liquidity. This is not a new trade-off in crypto. When you choose to use a specific CEX, you’re committing to using the liquidity on that CEX. If a different CEX has deeper liquidity for the asset you want to trade, you have two options:

- Dont trade the asset

- Move your funds to the other CEX

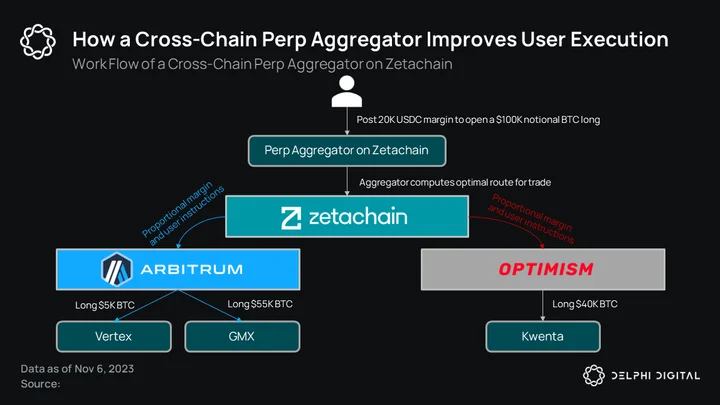

The vision for a consumer aggregation app would be to give users the experience of interacting with a single application to access liquidity from all relevant derivatives venues.

A trader who wants to long $100k notional of BTC could theoretically have this order split across several venues on different chains. If the app’s algorithm determines that the best execution for a market order is to split up the position by holding 55% on GMX, 40% on Kwenta (Synthetix), and 5% on Vertex Protocol, the user is able to access optimized execution across venues. An app like this is theoretically possible with Zetachain’s architecture.

The way this would be implemented from a smart contract level is to have deployments of this consumer app’s logic on each chain and the aggregator logic on Zetachain. Assets are withdrawn from Zetachain via the TSS address on the destination chain and are transferred to the app’s controlled contract, and the position is set up.

There are, of course, some constraints with such an app. Managing margin requirements and pricing disparities is a big one. If one venue’s price is not in line with the market, it could cause a liquidation of the position on that venue. On the one hand, splitting it up does expose traders to idiosyncratic risks like this. But another perspective would be that if your position did not have venue diversification and were instead 100% on a venue with pricing disparities, you would have a deeper loss.

Exploit risk stemming from the complexity of the contract suite is also a concern. As is the latency inherent in bridging and the inability to guarantee execution at a specific price. As a result, it seems Zetachain’s architecture is best suited for applications that aim to build out their own native liquidity on various chains. However, that doesn’t rule out the possibility of such an app existing — it just poses a few additional challenges for developers.

Lending Markets

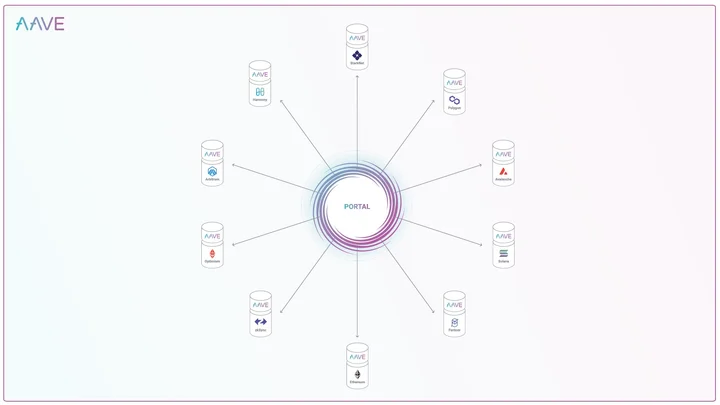

Aave v3 and the introduced Portal were the first true omnichain lending idea to hit the market, albeit it isn’t live yet. With Aave v3, users can post collateral on one supported chain and obtain a loan on a different chain. We won’t get into the specifics of how this works — that’s what the Aave documentation is for.

Radiant Capital is a live omnichain money market that operates between Arbitrum and BNB Chain. It’s an Aave v3 fork that decided to go to market rather than waiting for governance to greenlight a launch. Radiant has attracted over $500M in deposits and has over $300M in total loans outstanding at the time of writing, indicating that there is demand to use an omnichain money market — even though Radiant supports only two EVM chains.

While there is demand for the product, it’s worth noting that these numbers alone are not enough to say there is strong PMF at the moment for omnichain money markets. Radiant has a rather aggressive token incentive scheme for depositors and borrowers. Uncharacteristically high utilization ratios on the protocol suggest that a lot of the volume is users looping leverage as a token farming strategy. Token incentives play a prominent role in current product usage.

However, there is still a massive opportunity here — there’s no two ways about it.

Radiant’s system is not exactly omnichain, in the sense that the entire system is connected across the chains it supports. A loan issued on Arbitrum can be seamlessly bridged to BNB Chain, but the user still has to pay back the loan on Arbitrum. They cannot pay it back on BNB Chain.

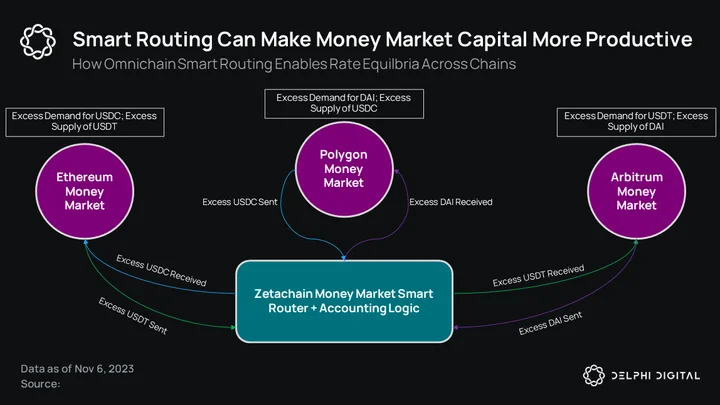

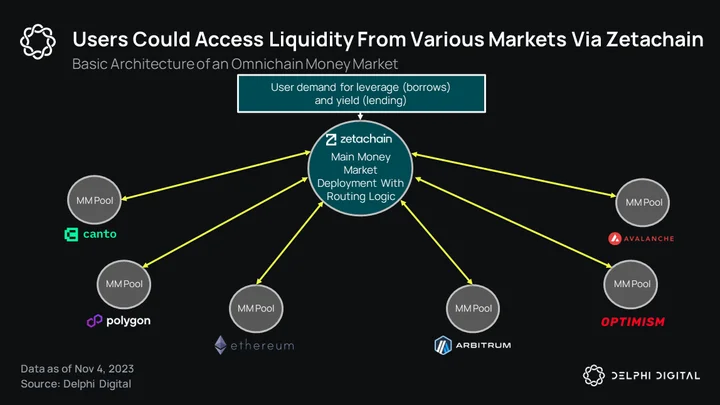

Omnichain money markets can make use of capital more efficiently. They can transport assets from one ecosystem to another as demand shifts. For example, the way Aave works today is similar to the description of GMX in the DEX section. It has independent deployments on different chains, each living in a silo. They are not yet connected in a material way. If demand to borrow USDC on Ethereum rises, there is no way for users to access the (hypothetical) hundreds of millions of USDC sitting dormant in Aave’s Polygon deployment. This is a significant cross-chain inefficiency that omnichain design can address.

In today’s environment, a user with 100 ETH on mainnet that wants leverage on Arbitrum to implement a farming strategy would have to first bridge their collateral to Arbitrum. Life becomes much easier when money market deployments of the same protocol can communicate with each other. The protocol can acknowledge collateral has been deposited on Ethereum and can sanction a loan on Arbitrum against it. The loan could also then be repaid on Arbitrum and sent to Ethereum where it is closed, thus freeing up the user’s 100 ETH.

Protocols need to tie up with bridges to become truly cross-chain in this manner. Aave and Radiant integrated with Connext and LayerZero, respectively. But even so, as mentioned earlier, Radiant only helps users bridge their loan from one chain to another — it doesn’t shift their accounting liability to another chain. There’s an opportunity to build something along these lines on Zetachain. In fact, given that Zetachain has a virtual machine — and one that is compatible with all EVM chains — several other products can be unlocked.

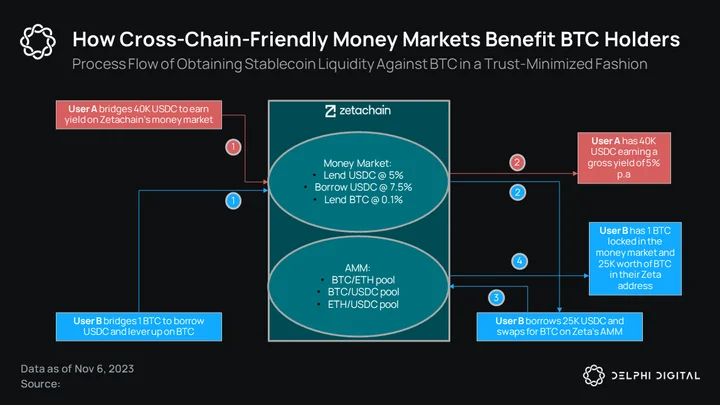

The Bitcoin faithful have a few options when trying to access leverage against their holdings: use an illiquid product like Sovryn on Rootstock, wrap their Bitcoin and send it to Ethereum (centrally custodied by BitGo), or deposit it on THORChain and obtain a loan against it. Zetachain enables a similar path to THORChain with validator-controlled, decentralized custody in a TSS address. But as a smart contract platform that can attract app builders and have a wider suite of products, it could prove to be more appealing than borrowing on THORChain.

BTC holders can also access liquidity in the form of USDC and USDT, owing to Zetachain’s ability to draw liquidity from larger ecosystems like Ethereum, Arbitrum, Polygon, Optimism, etc. Holders can verify the existence and safe custody of their BTC by monitoring Zetachain’s TSS address.

Hardline Bitcoiners probably wouldn’t use any lending products anyway. But an omnichain money market built on Zetachain would provide the opportunity to do so for larger holders who would prefer to make their BTC productive without the liquidity woes of Sovryn, minimal subsequent functionality of the loan with THORChain, and counterparty risk/centralization of WBTC or CEXs.

Omnichain Yield Products

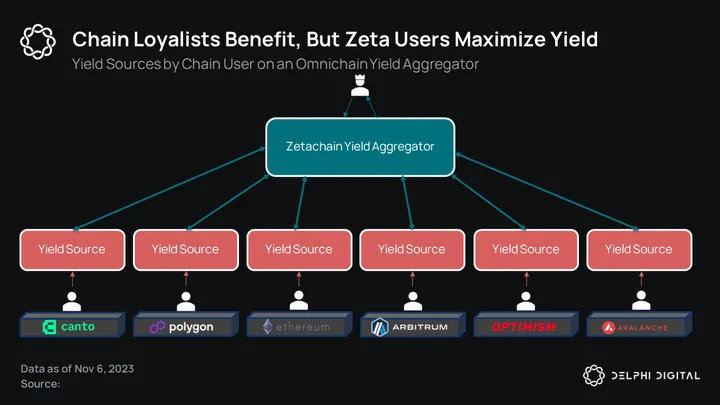

The potential of omnichain yield products is perhaps the most fascinating opportunity for Zetachain. In an age where everyone is in search of yield, Zetachain’s architecture allows for products to hyper-optimize for the best yield — albeit not without constraints.

In a world where app deployments on different chains can communicate with each other, it’s possible to build a smart yield aggregation engine that taps into the best yield sources across the universe of compatible chains.

Think about an app that takes in USDC deposits on Zeta and deploys them across Aave (Ethereum, Polygon, Arbitrum, Optimism), Venus (BSC), Compound (Ethereum), and Radiant (BSC, Arbitrum). The smart contract suite, across chains, can communicate with each other to ensure optimal capital allocation for yield. So, from a UX standpoint, you would just need to deposit your asset of choice into a Zetachain smart contract — and the rest is on autopilot.

The overall strategy can differ, but it would likely be managed by an off-chain algorithm that takes the net yield and the types of risk presented by each venue into account. Funds in a single strategy, say USDT, would have to run a risk check for every venue with a corresponding USDT market. Some critical criteria to evaluate could be:

- Technical risk — the probability of an exploit or getting funds locked (qualitative in nature).

- Financial risk — innate risk profile of underlying strategy, probability of principal erosion

- Liquidity risk — the level of pool utilization and efficiency of liquidations.

- Counterparty risk — the degree of exposure to a particular counterparty or set of entities.

- Concentration risk — a large portion of user assets shouldn’t be deployed to a specific venue unless the risk-adjusted yield deems it worthy.

- Saturation/capacity of strategy — how much money can be deposited into this market without materially lowering the yield on offer or risking locked funds due to high utilization rates?

A strategy that deploys capital to overcollateralized money markets would not have much financial risk or counterparty risk. But If a strategy deploys capital to a mix of yield-bearing opportunities like GLP on GMX, Uniswap v3 USDC-USDT LP, and put-selling vaults denominated in stablecoins, then the risk assessment becomes all the more imperative.

The entire tech stack of such an app would be highly complex. Which, in the open-source world, also means that it would be more vulnerable to bugs and thus exploits. However, the UX that such an app could provide is enticing. And if it weren’t for the fear of exploits that has gripped the crypto world, I would be confident enough to say that something like this would have immediate PMF.

Tangent: To reach a large-scale audience, crypto apps need to be able to do complex things without pushing that burden onto users. That means it’s easy to use and does a lot of things behind the scenes. Naturally, this translates into a complex back-end framework. So this is something we’re just going to have work through in order to make decentralized products appealing to larger audiences.

Another critical decision with an app like this is to decide who can create strategies and how they’re created. A set number of strategies that each have a mandate is ideal from a cost-benefit perspective. If the risk assessment process is handled by an off-chain algorithm, you could theoretically have a handful of automated strategies with varying risk levels and add new potential venues to each strategy as they fit in.

By having a small number of strategies per asset (each offering different risk/reward profiles), instead of user-deployed strategies, hitting economies of scale is much simpler. Simply put, less vaults and more AUM in each vault translates into lower rebalancing costs for users. This is because the gas to move between protocols and bridge between chains is shared across a larger cohort. Allowing users to granularize their strategies would give them a meaningful UX benefit but at the expense of higher per-user costs, thus making it more viable as an ad-hoc feature for the crypto wealthy.

P2P Financial Infra Layer

OTC markets in crypto are reasonably vibrant. They’re also very unstructured and relatively opaque. Unlike a lit orderbook, it’s difficult to visualize all of the demand and supply on the OTC market. But things are like this for a reason. Large buyers and sellers don’t want to publicize their intent to “move size” on an asset. Despite this, many OTC desks and dealers run semi-public Telegram/Discord channels that list a lot of their flow — specifically on equity, token warrants, and large tranches of liquid tokens.

Peer-to-pool trading is in the norm in DeFi and on-chain finance, but peer-to-peer facilitators are starting to take off. Morpho is a P2P money market that’s seen significant growth recently. And most NFT lending volume is done via P2P loans. An easy framework to think of this is along the same lines as Blur Blend, Arcade, or Morpho — but without being limited to available liquidity on a specific chain.

Now, I’m not saying this is the sexiest use of Zetachain’s omnichain capabilities, but it is a fresh idea that could become very important. An infra layer that accepts orders for any instrument and helps enforce terms/covenants can become the base for more accessible and transparent OTC activity across the on-chain universe.

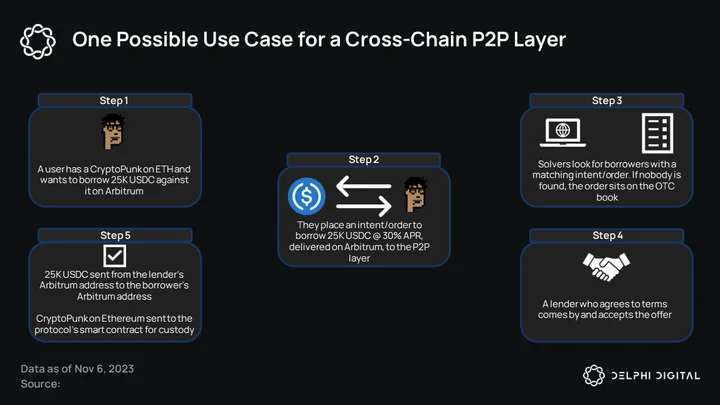

So how exactly would this work? Users interact with a front-end app where they can either choose to execute close to the prevailing market price (work flow similar to an RFQ) or set a limit price for their order. The order’s parameters include the chain the order is originated on, the desired destination chain, and the address on said chain. Once the order is placed, user funds move into a designated escrow address for a solver network to be able to access once they find an optimal route.

Zetachain nodes, or even a more specific network of solvers for this app, can fulfill the trade by moving assets to the user’s specified address on the destination chain. The fulfillment transaction is recorded on Zetachain and includes a memo with full order details — origination chain, destination chain, order parameters, etc. As the order is fulfilled, Zetachain’s TSS address on the origination chain transfers to assets to the entity that fulfilled the order. This can be done periodically in batches to reduce settlement costs.

A mechanism like this would work for a variety of use cases and instruments. For someone who has a CryptoPunk on Ethereum and wants a loan to yield farm on Arbitrum, things can get messy. You have to hop on to P2P NFT lending platform, find a counterparty willing to lend to you, and then bridge those funds to Arbitrum. What if you could instead send your intent to use your Punk as collateral on Ethereum to receive a loan (at specified terms) on Arbitrum?

The process changes slightly depending on the kind of instrument being used. In the example illustrated in the above graphic, the system would transfer the user’s NFT to a smart contract for escrow/custody until the loan is repaid (goes back to original owner) or defaulted on (goes to the lender).

For the most part, this would be desirable for asset swaps and P2P loan agreements — perhaps not so much for paper instruments like SAFEs given the legal overhang. It’s a simple product that has the potential to facilitate a significant amount of volume in the right market conditions. Think of it as a pervasive P2P financial layer powered by a solver network to help match orders from internal and external sources.

Other Relevant Ideas

The opportunities described here are by no means an exhaustive list of the kinds of applications Zetachain can help foster. Instead, it’s a handful of ideas that we believe are the most obvious and important for the network to seize. There are other primitives and user-facing applications that could be built on Zetachain to take advantage of its cross-chain infra:

- Cross-domain identity primitives with the ability to port/connect a user’s identity across chains

- A Bitcoin-centric social graph like New Bitcoin City

- A truly cross-chain NFT marketplace that aggregates listings and offers the ability to atomically settle in any Zetachain supported asset

- A decentralized stablecoin with issuance, asset-backing, and atomic transfers across multiple supported chains

- A liquidation prevention service on top of an omnichain money market

- Cross-chain friendly credit accounts, similar to the Gearbox Protocol.

Bitcoin DeFi and the Opportunity for Zetachain

DeFi was the first large-scale success of Ethereum’s smart contract capability and brought a whole new use case to Ethereum. Ethereum’s DeFi ecosystem has lending apps, exchanges, derivatives, and more. Bitcoin doesn’t have Ethereum capabilities around smart contracts, so Bitcoin DeFi generally requires other chains.

When looking at DeFi on Bitcoin, we focus on three projects: Rootstock, Stacks, and THORChain. While Rootstock and Stacks support general-purpose smart contracts are Bitcoin-focused DeFi, THORChain, built with Cosmos-SDK, is an application-specific chain that is Bitcoin-friendly.

As the most popular and highest market cap cryptocurrency, there is much potential in BTC-friendly DeFi ecosystems. Most BTC sits idle in wallets. Any attempt to turn that into productive capital is a huge boost for the overall crypto-economy.

The Current State of Bitcoin DeFi: App Ecosystem

Both Stacks and Rootstock (RSK) attempt to recreate Ethereum’s DeFi successes by connecting with Bitcoin via a custom bridge and encouraging builders to deploy apps on their smart contract-compatible chain.

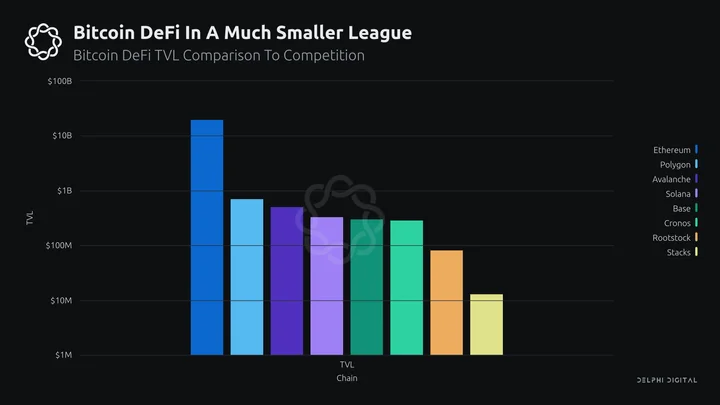

Bitcoin-focused DeFi is tiny compared to most ecosystems – let alone Ethereum. THORChain alone is larger than Stacks and RSK combined at $130M TVL. Ethereums TVL sits near $20B, Solana at around $330M, Polygon at $700M, and even the much younger Base at $301M. Despite projects like Stacks and RSK plugging into the most well-known chain in crypto, together, they barely account for $100M in assets. Their lack of adoption begs the question: why aren’t Bitcoiners using them, and what lessons can we learn from their struggles?

Rootstock – $81.73M TVL

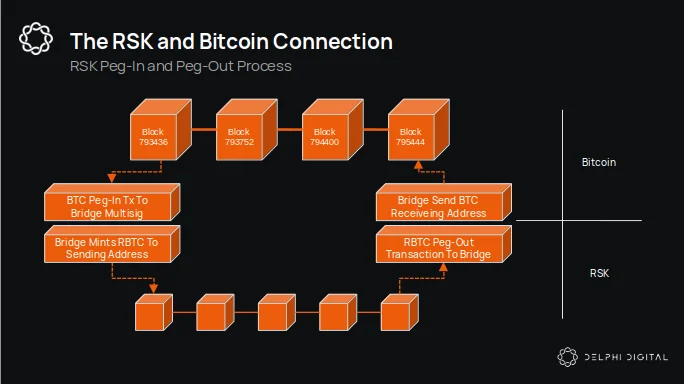

Rootstock (RSK) is a smart contract Bitcoin sidechain. Users transfer BTC to the chain, which then becomes RBTC, the native gas asset of the Rootstock chain. RSK uses merge mining with Bitcoin, meaning it inherits some level of Bitcoin security. RSK also has a much lower block time compared to BTC at around 34 seconds.

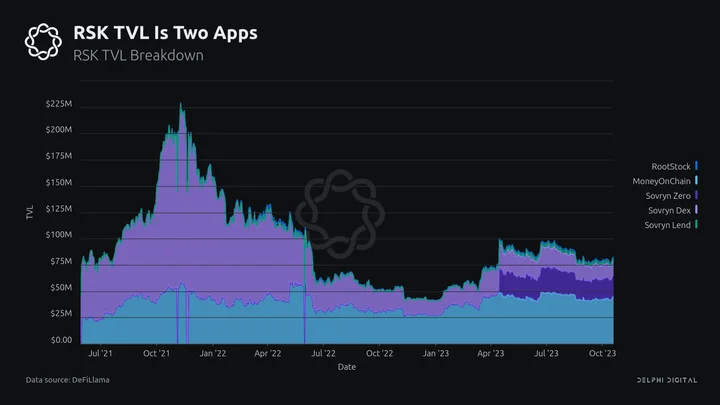

RSK is a fork of GETH, and it’s compatible with the EVM as it has its RSKVM. As RSK is EVM compatible, ETH wallets like Metamask work with it, although the UX of transferring BTC over is relatively clunky. 98% of RSK’s TVL is in two apps: Money On Chain and Sovryn.

“Money on Chain” accounts for over half of RSK’s TVL and is a CDP stablecoin platform that uses BTC as collateral. They use numerous tokens for their app:

- MOC for governance and staking.

- BPro, a leveraged Bitcoin token with passive income.

- DoC is a Bitcoin-based stablecoin.

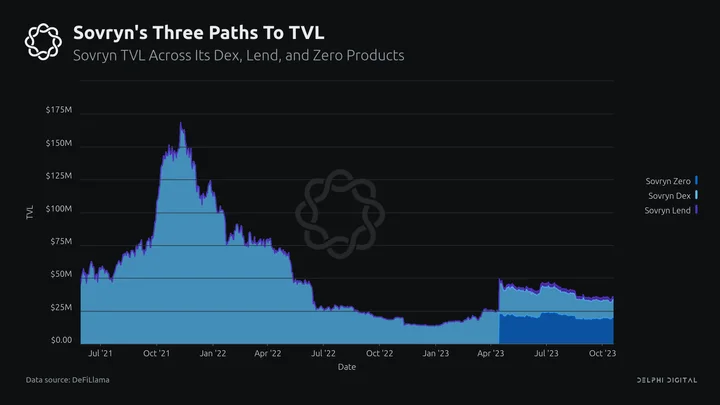

Sovryn accounts for close to $50M in TVL. Like Money on Chain, Sovryn aims to do a lot. There is a DEX, a lending product, and Sovryn Zero. SOV is their governance token.

- Sovryn Zero allows 0% interest loans on Bitcoin and its Bitcoin-backed stablecoin, ZUSD.

- Sovryn DEX is an AMM platform for spot (CLOB), margin, and simple swap trading on RSK. The TVL of the DEX sits at $13.67M despite the Sovryn DEX being the main DEX of the ecosystem, like other DEX’s. Sovryn issues SOV as rewards for LPs in their DEX. From their app, there are only 12 active pools at the [moment](https://alpha.sovryn.app/yield-farm?_gl=1*11embla*_ga*MTMxMzcxODIyMy4xNjk3NTc3MTE5*_ga_JLNF5Q0CP9*MTY5NzU3NzExOC4xLjEuMTY5NzU3NzU1NS4yMC4wLjA.).

- The lending product also allows users to lend their assets, like RBTC, to earn returns. Sovryn will enable users to borrow five assets: BPro, DOC, XUSD, RBTC, and DLLR.

These two apps account for almost all the TVL and activity on RSK. Unfortunately, compared to their competitors on other L1s, their activity is minuscule.

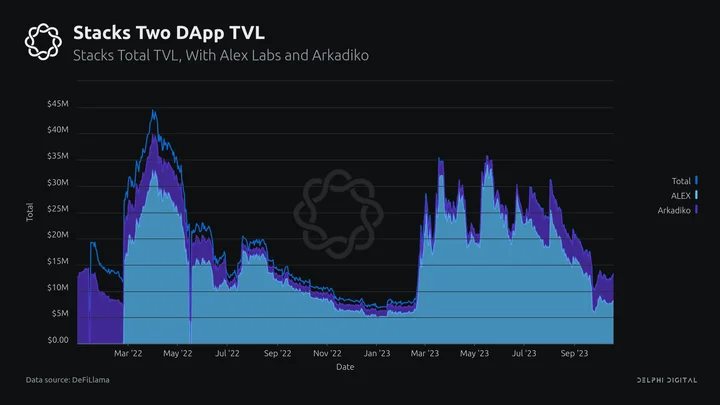

Stacks – $12.9M TVL

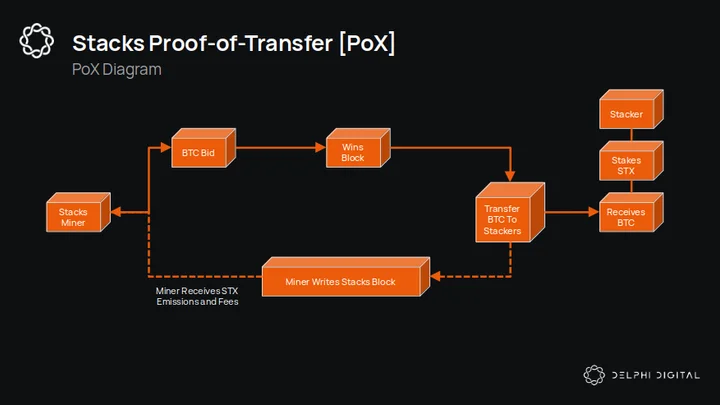

Unlike RSK, Stacks is not EVM compatible and has its own programming language Clarity, which is relatively unpopular. Stacks has a novel consensus method called Proof of Transfer [PoX] and it’s own (non-BTC backed) gas token STX.

In PoX, miners bid BTC to earn the chance to write Stack blocks. Miners who write a block receive STX block rewards and transaction fees. PoX then sends the miner’s BTC bid to users who stake STX tokens – allowing for some passive BTC income. Like RSK, most Stacks activity is again dominated by two apps: Alex and Arkadiko.

Alex Labs is a foundation dedicated to building DeFi on Stacks governed by their token ALEX. Their current product is an AMM DEX that allows for simple asset swaps of Stack-based tokens. However, like Sovryn and Money On Chain, there are other features:

- BRC-20 CLOB – Alex has hopped on the inscription technology by building a simple order book DEX for BRC-20 tokens. BRC-20’s on this DEX trade against sUSDT.

- Farm – Alex Labs Farm product is a yield optimizer for their DEX. It allows users to add liquidity to certain pools to earn ALEX rewards.

- Stake – users can stake ALEX tokens to earn additional rewards.

- Lottery – users can enter the ALEX lottery to win ALEX and other rewards like Stacks NFTs. Based on the documentation, the lottery is only for a limited time.

- Bridge – Alex provides users with a limited bridge to and from Stacks. The bridge connects Stacks to BSC Mainnet and Ethereum.

- Launchpad – Finally, Alex also has a project launchpad. To get access to their Launchpad, users just earn APower through staking or yield farming.

- APower is a nontransferrable token that gives users access to the Launchpad.

Arkadiko is a protocol where users can collateralize their assets to mint a stablecoin called USDA. Additionally, the app has a built-in AMM DEX for simple swaps.

THORChain and The Notion of Bitcoin-Friendly DeFi

Unlike RSK and Stacks, we cannot consider THORChain to be Bitcoin-centric DeFi, as the chain’s capital base and core utility is not solely focused on Bitcoin and BTC. THORChain is a bridge-app-chain that enables native swaps between a variety of chains — like Bitcoin, Ethereum, Avalanche, BNB Chain, and many others.

The difference between Bitcoin-friendly and Bitcoin-focused is fairly obvious. One has a philosophical goal of only trying to promote Bitcoin and BTC-denominated activity — the other is trying to integrate the promise of BTC as an asset with the functionality of other chains. RSK and Stacks have attempted to build an ecosystem for the ardent Bitcoiners who have a stern disdain for virtually all other public blockchains. THORChain has built a system that enables a variety of assets — including BTC — to be swapped or made productive through liquidity provisioning (AMM LP or lending). From each chain’s capital base and core usage metrics, it’s painfully obvious which philosophy makes the most sense.

The core premise of THORChain is native swaps, with the recent addition of synthetic assets and a lending product as well. THORChain accounts for the vast majority of BTC held by external chains.

THORChain has been on a roll in 2023, hitting an ATH in daily swap volume with the trend looking to continue. Earlier in November, THORChain facilitated more weekly volume than Curve Finance. The introduction of synths has given the DEX’s volume a huge boost and is roughly on par with native asset swap volume. This has also resulted in an increase in the number of addresses/users interacting with THORChain.

The overall number of swaps facilitated by the network has roughly doubled since the beginning of the year. The average number of unique addresses using THORChain per day has nearly tripled from ~ under 1K per day in Jan. 2023 to slightly over 3K now.

THORChain has the made the process of providing liquidity slightly easier with its Saver product. Not everyone wants to buy RUNE, provide asset-RUNE liquidity, and bear the risks that come with that. Single-sided LPing with built in protection from LVR or impermanent loss enables those sensitive to divergence losses, common with AMM LPing, to capitalize their assets with lower risk of losing principal exposure. That doesn’t mean there isn’t no risk; depositing funds into the Saver pool is akin to lending your assets to the network. There is risk of principal erosion, but to a meaningfully lesser degree than LPing in an asset-RUNE pool.

There is arguably no community or group of investors as sensitive to divergence loss and as averse to dual-side LPing as BTC investors. And along those lines, the expected result is that the majority of capital in the Saver product is in the form of BTC.

THORChain has made strides that have cemented it as the epicenter of what is considered Bitcoin DeFi today. However, the scope of products that can be built natively on THORChain are somewhat limited by the lack of a native VM and the inability to deploy smart contracts.

Challenges in Bitcoin DeFi

Of course, the question remains: why have the current Bitcoin offerings failed to attract many users? The apps have tokens and incentives; they are generally secure and have a comparable UX/UI to Ethereum-based projects. And yet, users are not showing up to use these apps.

Picking the Right Approach and Building Useful Liquidity

The biggest issue with Bitcoin DeFi today boils down to two problems: creating liquidity against BTC and focusing on the right kind of users. Hardcore Bitcoiners care deeply about security, to the extent that they are happy with the opportunity cost of productizing their BTC for the security of cold storage. This group of investors can be considered cypherpunks, who do not care about things like asset efficiency.

The average BTC investor doesn’t strongly align with cypherpunk ethos. BTC’s standing as a macro asset opened the door to investors who recognize both the value proposition of BTC as a censorship-resistant store of value, the upside of productizing ones assets, and the functionality of turing complete chains.

Today, a peak into ecosystems trying to build for hardcore Bitcoiners reveals an obvious lack of PMF. The vast majority of these people do not accept the trade-offs that come along with re-capitalizing their BTC — side chains, sovereign chains with bridges, and giving up self-custody of native BTC.

The amount of BTC on exchanges is proof enough that the real opportunity exists outside of self-custody hardos. Users (BTC holders) will flock to where to where liquidity is. And it is only a certain kind of user that will do so. Attempting to build liquidity but target the wrong user is a common recipe for disaster. And this disastrous approach aligns with what Rootstock and Stacks have pursued. Giving users the ability to borrow a stablecoin with miniscule liquidity and volume on a chain that is “Bitcoin aligned” neither caters to the cypherpunk nor the average investor.

For the most part, the target of any ecosystem trying to be BTC-friendly should be to nip at the trove of BTC sitting on CEXs. It’s impossible to target the entire portion, given BTC liquidity will always (and should) be strong on CEXs. However, it is possible to create trust-minimized experiences to allow users to do things like borrow against their holdings and use it as collateral to trade derivatives, amongst other things.

The success of WBTC and THORChain highlights a strong point – you may not be able to convince the hardcore cypherpunks, but there are reasonable BTC investors who are looking for avenues to make their capital more productive. Ideally, this should be the target cohort for alternative ecosystems looking to be Bitcoin-friendly.

Product Building So Far

One of the dynamics we see in Bitcoin-focused DeFi is that the protocols go broad. They do not try to build one thing well and grow it, instead they have launched a single app that has a basic AMM, money market, and stablecoin.

Three of the four apps highlighted in the previous section have their own AMM; two of the four provide lending and borrowing; and three of the four apps have their own native stablecoin. Throwing a bunch of products out in the market without any real focus isn’t a sound approach — leaving aside the notion of these chains seeming to misunderstand who their user is.

This approach seems to stem from the notion that there is no Bitcoin-centric DeFi ecosystem to rival Ethereum’s, and thus there is an opportunity to build all the things that exist on Ethereum. However, Ethereum’s DeFi ecosystem has actual user demand. The builders on Stacks and Rootstock don’t seem to understand that Bitcoin alignment is fruitless, as they user group they aim to cater to doesn’t want to do anything with their Bitcoin — and the user group they should be catering to are off on other chains that have deeper stablecoin liquidity, more willing users, and more functional runtime environments.

The track record of protocols that quickly spread themselves into numerous different products is not excellent. The most cited example of this in crypto is Sushiswap. Sushiswap was originally a “community-owned” Uniswap clone. But soon, they attempted to expand into NFTs, lending, and margin trading — without first scaling the DEX into a product that could compete without a boat load of incentives.

After leadership woes, Sushiswap is a shadow of its former self and has been surpassed by its competition that focused on perfecting one product first.

Opportunities in Bitcoin DeFi

The bad news is that Bitcoin DeFi is struggling due to various factors. The good news is that there is a huge vacuum for other more determined teams and protocols to capitalize on.

Building For the Right Users

The hardline Bitcoiners do not want to productize their holdings. They have minimal interest in doing anything with their BTC, besides perhaps using the BTC as collateral — to buy more BTC. In the end, it’s reasonable to assume this cohort of users actually trusts centralized businesses like Binance and the erstwhile BlockFi more than chains like Ethereum. And as such, they are likely not the right user to target.

Your average BTC investor who holds their coins on CEX to do things with their capital is likely the ideal target user. They align with the notion of not letting all of their capital sit idle. This cohort of users are more likely to be open to trying new chains and on-chain products. As illustrated earlier in this section, close to 10% of BTC’s supply sits on CEXs. While a large chunk of that is likely market makers, whose core business operations involve having BTC on various CEXs, there are also some users — retail and institutional — who would be open to more decentralized alternatives.

When lending platforms like BlockFi and Celsius were able to amass large swathes of BTC from retail users, surely their is a market for this business model to exist on-chain with the ability to conduct public financial audits.

Ordinals: Assessing the Ecosystem and What Lies Ahead

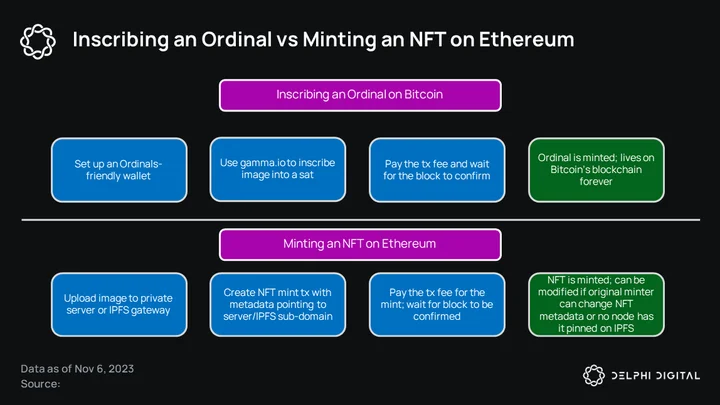

Ordinals are a recent entrant into the crypto zeitgeist. The ELI5 of Ordinals is that they’re NFTs on Bitcoin. Essentially, they are just representations of data stored in the Bitcoin blockchain. An Ordinal could be a text file, image, video, sound, or anything else. The biggest benefit Ordinals bring to the table is that their data is stored on-chain.

On Ethereum, most NFT metadata just points you to a centralized server where the associated multimedia file is stored. This means the owner of said server could just change what it is in the directory and change what the NFT represents. Ordinals do not suffer from this problem — instead, they introduce new problems.

Ordinals can, in theory, be up to 4MB in size since that is the block size limit on Bitcoin. The entire corresponding file/data associated with the Ordinal is stored on-chain. That means large video files or extremely high-resolution images aren’t suited for Ordinals. The cost of publishing data and inscribing an Ordinal on Bitcoin isn’t cheap either — relative to Ethereum, and especially Polygon and Solana.

By now, it should be clear that certain kinds of Ordinals make the most sense. A mass-produced profile picture NFT collection probably shouldn’t be launching on Ordinals. The cost to minters/users outweighs the marginal benefit of censorship-resistant avatars.

The best kinds of Ordinals are things that benefit from immutability and censorship resistance. A great example of this is this publishing platform that inscribes articles/essays into Ordinals. Even here, not just any essay would make sense as an Ordinal.

- Marketing copy for a project? Nope.

- A community manifesto for developers in crypto? Yes.

- An article on something relevant happening in the world that could be subject to hindsight revisions? Yes.

- A list of exercises for people looking to grow their rear delts? Definitely not.

An underlying theme to our value proposition for Ordinals is that things that genuinely benefit from the properties they enable will be true winners—high-end art, tokenized luxury items, critical pieces of literature, etc. An example of a tasteful way to utilize Ordinals was the Asprey-Buggati NFT. The limited edition NFT collection boasted tiers ranging from $10K to $200K. For a value with such a high perceived financial value, Ordinals make sense because people sinking in that kind of cash can be assured that their purchase is permanent and not modifiable ex-post.

With a fair idea of what Ordinals are and where they can be useful, let’s dig deeper into some outstanding problems and theorize on solutions to bridge the gap between reality and vision.

The Current State of Ordinals

Playing around with Ordinals does not functionally look too different from NFTs on Ethereum or Solana. In fact, the most used Ordinal marketplace is Magic Eden, which has its roots in Solana NFT trading. You use an Ordinal friendly wallet, like Unisat or Xverse wallet. Load it with BTC, and now you can buy stuff on Magic Eden or any other marketplace.

Actual activity on Ordinals saw a significant spike between May and Sept 2023, averaging over 200K inscribed sats per day over that period. While most of October was tranquil and led many to believe this was just a short-term narrative, things began to pick up going into the end of the month.

There was a growing narrative that Ordinals would be able to battle Bitcoin’s economic crisis, where the split of block rewards over transaction fees in miner revenue was highly skewed towards block rewards. Ordinals offered a new lease on life to the network’s economics, offering the ability for something widely care of to be traded back and forth, thus generating more fee revenues.

As you can see from the chart above, fees spiked to a massive level of over 200 BTC per day for an extremely short period. [insert commentary on ordinals fees/total btc fees]

The vast majority of inscriptions are text, which alludes to them being BRC-20 tokens. While less than 10% of all Ordinals mimic NFTs, those are the ones drawing in the most attention and trading volume.

The top five Ordinals collections on MagicEden, as of Nov. 2023, are Bitcoin Frogs, ABC, Ordinal Maxi Biz (OMB), bitmap, and ORC-Cash. We’ve discussed some of this in our previous Delphi Pro coverage, so here’s a brief overview:

- Bitcoin Frogs is a PFP collection of 10,000 pixelated frogs.

- ABC is a PFP collection of 7,900 avatars in the style of a children’s drawing.

- Ordinal Maxi Biz, borrowing its name from Solana Monkey Business (SMBs), is a PFP collection of 2,100 avatars that resemble the broad frame of crypto punks but with a hand-drawn aesthetic rather than pixels.

- Bitmap is a unique implementation of the inscription process built on top of Ordinal theory. Bitmaps represent entire blocks on Bitcoin that users can “claim” and inscribe on top of. Some analogize it to “owning real estate in the Bitcoin blockchain”.

- OSH, or ORC-Cash, is a BRC-20 token that tokenizes mint inscriptions themselves. It’s analogized to be akin to cash bills with a serial number.

From the top five, it’s only the bottom two that are actually intriguing and pushing the needle. This does bring up a point that PFPs seem to be in high demand across ecosystems, irrespective of minting costs. Ordinal-based PFPs aren’t going to be wiped out. There is probably demand from Bitcoiners to adopt something akin to what their counterparts on other chains bear across their social media accounts. However, there are also technological elements that could make the idea of PFP Ordinals more feasible.

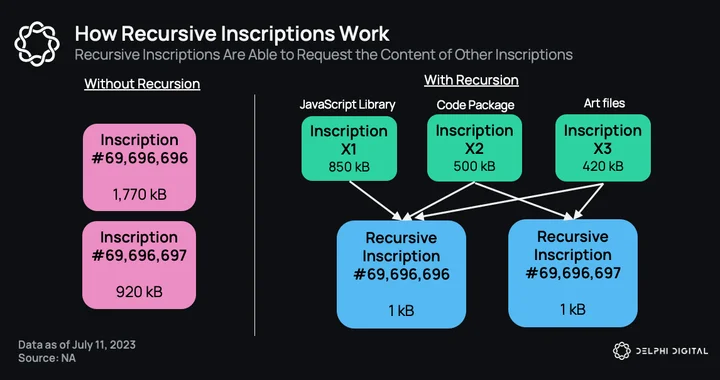

Recursion, with respect to Ordinals, is the process of citing an existing inscription in a new inscription. For example, if you wanted to inscribe a collage of four images on a sat, the normal process would include uploading all four images to Bitcoin and inscribing that data on the sat. However, if each of those four images already exists as an Ordinal, the new inscription would just have to reference the four previous inscriptions. This saves the minter time and money as the new storage requirement is lower, but most importantly, it’s a means of overcoming the 4MB bottleneck previously mentioned.

In our Delphi Pro report titled “The Huge Cultural Opportunity for Ordinals”, our team noted the salient features recursion brings to Ordinals:

- Recursion solves the maximum file size bottleneck for inscriptions, which is typically 400kB but technically up to 4MB. A complex digital artifact can be built out over several inscriptions, with the main inscription referencing other side inscriptions.

- Recursion allows code libraries to be built out over time as inscriptions. Others can then reference these inscriptions for use, in a similar model to open-source software development. Popular libraries like p5.js and Three.js have been inscribed and are available for everyone to use.

- Recursion reduces the cost of inscriptions, especially for collections. Repetitive code can be inscribed separately and less data is needed for each inscription.

- Recursion enables inscriptions to be composable.

Directly quoting the report: “A 10,000 PFP collection no longer requires inscribing 10,000 separate JPG files. Instead, you can inscribe the 200 traits and then make 10,000 more inscriptions that request traits programmatically and render the image.”

Challenges for Ordinals

Ordinals are a new form of on-chain creative expression. They’re still far behind NFTs — as we know them — in terms of a user base, traction, and functional products. There is potential here, precisely because of how it lives natively on Bitcoin — and the subsequent lack of exciting things in Bitcoin. However, there are some key challenges we believe they have to overcome before we can forecast the ecosystem’s future with any certainty.

The UX Challenge: Missing Puzzle Pieces

This is a problem not just for Ordinals, but crypto at large. Ordinals did suffer from UX that lags the status quo in crypto, however, the tooling around inscribing has signficantly improved in recent months. Services like Magic Eden and Gamma abstract much of the complexity out of process.

Discoverability of new collections is another problem that Magic Eden has recently addressed to a degree, but this still hasn’t really been solved. The TL;DR is that it’s challenging to locate all relevant Ordinals on a single platform. Since there is marketplace fragmentation, listings are also scattered across these platforms.

There are still a lot of other things to account for. For example, trading NFTs as a speculator is very easy on Ethereum. This comes down to the fact that block times are 13 seconds, and you only have to wait for a single block (most of the time) for your transaction to be confirmed. Once the block with the NFT trade is finalized, the trader can do as they please with their NFT — put it up for a loan, list it at a higher price, or maybe even stake the NFT.

Those opportunities do not exist with Ordinals yet. And yes, Ordinals are barely a year old so it will take some time for things to be built around it. However, Bitcoin’s 10 minute block times inherently disincentivize a robust trading ecosystem. Whether you like it or not, speculation is a prime reason why NFTs on Ethereum and Solana have deep liquidity. And Bitcoin’s block times could be a major hindrance to not just the trading of Ordinals, but the emergence of a robust suite of products built around it. But, as always, it isn’t completely hopeless. We are starting to see early signs of new products supporting Ordinals; but we cannot determine how successful these products can be.

Liquidium is a new platform offering P2P BTC loans against Ordinals — similar to the ecosystem of P2P lending built on top of the Ethereum NFT market. However, if you were to scan through recent P2P loans made against NFTs on Blur Blend or Arcade, you would notice that most of them are made against established NFTs: CryptoPunks, BoredApes, Doodle, Milady’s, etc.

Now, in the grand scheme of things, are there even established Ordinals? One could argue that rare sats are the only real market for this, because they have perceived historical value. But at this point, there are no definitive arguments you make for a why a specific Ordinal collection is worth lending against. And this gives way to our next challenge.

Incentivizing Creators and Accessing Better Liquidity

A large part of the Bitcoin community isn’t exactly in favor of the whole Ordinals movement. There was a mini culture war that erupted when Ordinals started to gain some attention. And so, as a result, there is no demand to trade and use Ordinals from a lot of Bitcoin-natives.

The existing community of on-chain creatives is firmly rooted in Ethereum, Solana, and Polygon for the most part. These are chains with thriving NFT ecosystems and healthy liquidity metrics. Ethereum dominates in the “blue chip NFT” realm. Most on-chain entities willing to shell out serious money for on-chain art do so on Ethereum. Even though the unit economics of minting large scale collections on Ethereum is much higher than Solana or Polygon, Ethereum still reigns supreme even in this realm.

Liquidity from willing collectors is essential to create a thriving marketplace for creatives. And whether this can exist on Bitcoin remains to be seen. In essence, developers of Ordinals and its ancillary ecosystem of marketplaces and tooling need to think deeply about how they can market their solutions to creators and collectors. Ethereum and Solana team have their work cut out for them because they both have the ability to run native applications, and thus creating a healthy marketplace is a lot simpler. With a healthy market, there can be a balance between the demand to collect and the supply of art.

Royalties are basically non-existent with Ordinals. Financial incentives in this regard naturally push creators toward existing NFT platforms with enforceable royalties over Ordinals. Ordzaar is the first platform to bring royalties to Ordinals, but major marketplaces will also have to play a role in enforcing codified royalties.

Ordinals builders have to figure out the right incentives to bring creators over to their ecosystem. This primarily comprises business development and bolstering awareness of Ordinals value proposition. In addition, the Ordinals ecosystem also needs to tap into the liquidity on ecosystems like Ethereum in order to grow.

Finding the Sweet Spot of Where Ordinals Trump NFTs

While Ordinals are not the same as NFTs, they have similar properties. Ordinals too aren’t fungible in the sense that they are interchangeable. Ordinals are inscribed on sats (or satoshis) which is the smallest unit of BTC. And BTC is fungible, so if you ignore the Ordinal, sats are entirely fungible. This divergence of fungibility on the different layers of a sat is precisely why you cannot use any Bitcoin wallet to own Ordinals — you need a wallet with sat control that can enable you to not spend the inscribed sat.

Right now, the NFT landscape is dominated by various forms of art — primarily visual. While there are other use cases like registries and certificate issuance (like POAP), the key market that exists today is creative in nature. The big question for the Ordinals ecosystem is whether to go down a similar path or focus on other endeavors.

(Chart on NFT volume by type of NFT)

Take, for instance, the idea of tokenizing a rare 1-of-1 piece of digital art. With Ethereum, the artwork likely lives on an IPFS sub-domain, and the NFT’s metadata simply points you to said IPFS link where the artwork lives. The person who uploaded the artwork could change what that IPFS sub-domain hosts, or unpin the art so it slowly isn’t stored on any client. If you were to buy a $69M NFT, something like this happening probably would enrage the purchaser.

However, with an Ordinal, this scenario simply isn’t possible. As mentioned earlier, all files inscribed into an Ordinal are stored in the Bitcoin blockchain. The artwork actually exists on-chain and is tied to a specific sat. Nobody can reverse this.

With this in mind which of the following would you place more trust in: an NFT on Ethereum that represents ownership of a real-world asset to the NFT holder, or an Ordinal of the same? The point we’re trying to make here is that Ordinals do some things — verifiable ownership and immutability — much better than NFTs.

The easiest path to adoption would be to mimic the Ethereum NFT ecosystem and hope to usher in more creators and liquidity. The untrodden path of leaning into what Ordinals enable best would help cement a unique value proposition.

Opportunities For Zetachain

The challenges faced by the Ordinals ecosystem are not a death sentence. Ordinals bring something to the table that NFTs, as we know them, have failed to provide. However, there are some unique challenges with equally unique opportunities for Ordinals.

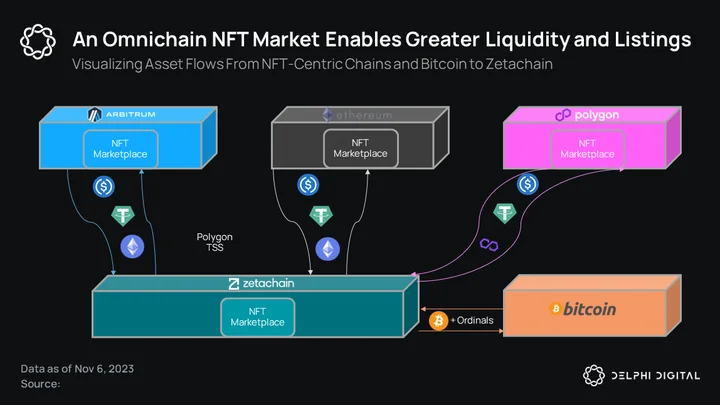

Solving for Liquidity: An Interconnected Marketplace for Ordinals

One of the easiest way to get creators to use Ordinals is to jumpstart liquidity into the ecosystem. If Ordinals are thinly traded, there’s little to no incentive for creators to use Ordinals over Ethereum or Solana. But bridging in liquidity, which leads to higher trading volume, presents an organic incentive for creators.

User can wrap their BTC on Zetachain by sending it to the network’s TSS address jointly controlled by validators. Suppose Zetachain’s TSS can implement sat control and allow users to send their inscribed sats to the network and have them show up as wrapped Ordinals. In that case, there’s a possible solution to the existing liquidity draught.

In essence, since Zetachain can enable users to bridge over their ETH and stablecoins as well as BTC and Ordinals, there’s an opportunity to create a more liquidity-dense marketplace for Ordinals that isn’t limited to just BTC.

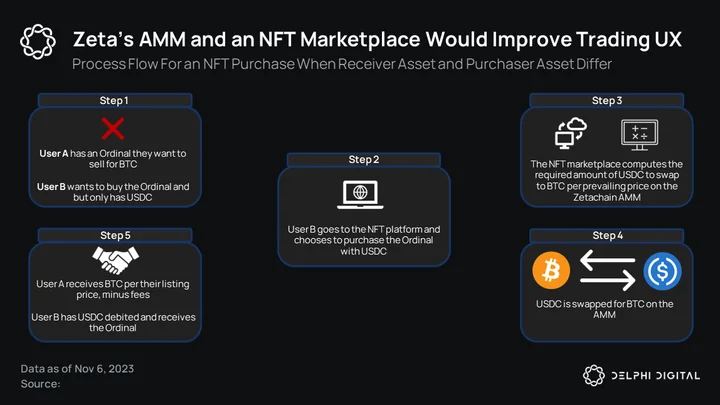

Zetachain’s ability to have both a DEX and NFT marketplace could enable an extra layer of UX improvement. If somebody lists their Ordinal on Zeta’s marketplace opting to set their listing price and receive their payout in BTC, the marketplace could integrate with an AMM to atomically swap the purchaser’s asset for BTC.

The process flow would look like the graphic below.

Assuming both buyers and sellers of Ordinals are flexible to receive/pay whatever asset they want, the swapping process is only required when the asset used to purchase the Ordinal and the asset the seller wants differ. Zetachain’s native liquidity pools can also help facilitate this.

But how do Ordinals benefit from such a marketplace? For starters, a lot more potential liquidity. Collectors sitting on ETH and stablecoins can buy creative works fairly easily; they only have to bridge their assets to Zetachain. The current scenario would either be sending their assets to a CEX to buy BTC, then setting up an Ordinals-friendly BTC wallet, and finally purchasing the asset, or swapping ETH for BTC on THORChain and receiving it to an Ordinals-friendly wallet. The UX with Zetachain seems much cleaner, as an EVM user wouldn’t need to use multiple wallets or swap assets back and forth manually.

Making the UX of purchasing an Ordinal easier makes it more viable to grow liquidity and volume numbers. This, in turn, serves as a key incentive for more creators to come into Ordinals after which even more collectors will watch the ecosystem with interest. If you layer in the ability to set royalties on collection or single inscription programatically, then the playing field starts to look a lot more level.

It’s critical to note that the viability of this is dependent on the ability to Zetachain’s TSS address to differentiate Ordinal sats from ordinary sats. Since sats are fungible, there would need to be a system that ties a specific sat (or wrapped Ordinal) to a specific user.

Grow Liquidity, Grow Relevance, Enable More Primitives

Step one in the Ordinals opportunity is to build the robust marketplace described above. As that happens, more and more collections within Ordinals will gain relevance. Subesquently, as specific collections become valuable, a market for ancillary primitives to make the Ordinals productive will begin to emerge.

The reason why Blur Blend does so much volume is because there are willing lenders against specific NFT collections on Ethereum. The most significant missing piece in recreating this for Ordinals is the relevance of the underlying assets and, consequently, the willingness of lenders to give loans against these assets.

In the situation of a loan default, NFT lenders receive the underlying NFT. Lenders in this realm have to make their peace with that. And only if that the worst-case is palatable is the risk of lending against NFTs acceptable.

Assuming all of this plays out, we could see an “NFT-Fi” ecosystem get built out. Zetachain could host the app layer for this, given smart contracts would be required to build out these primitives.

0 Comments