Introduction

MEV (Maximal Extractable Value) has been loosely defined as the value that block proposers can permissionlessly extract by reordering, censoring, or inserting transactions.

MEV is central to Ethereum block production. As a result, today’s censorship issues are deeply intertwined with MEV research, and both will be discussed in this report. If you’d like my far more opinionated takes here, you can see my recent article.

This report is more of a factual primer focusing on:

- Overview – MEV strategies and their supply chain.

- Past – How Ethereum initially reacted to the rise of MEV and built around it.

- Present – Ethereum block production changed drastically with the Merge, and MEV was central in these design decisions.

- Future – Ethereum faces many challenges (some old, and some new post-Merge) that will need to be addressed. I cover this a bit here then plan to elaborate in the future.

If you at any point require additional background on Ethereum’s mechanics, you can see my previous report here. Some of its relevant sections have been incorporated and updated here as applicable.

Just ignore all the times where I said that centralized block production is inevitable. Whoops. Lately, I’ve been thinking it might be possible to do better.

Here’s my recent addendum to that piece on decentralized block building. It’s still unclear how this’ll shake out, but I think we’ve got a fighting chance at it.

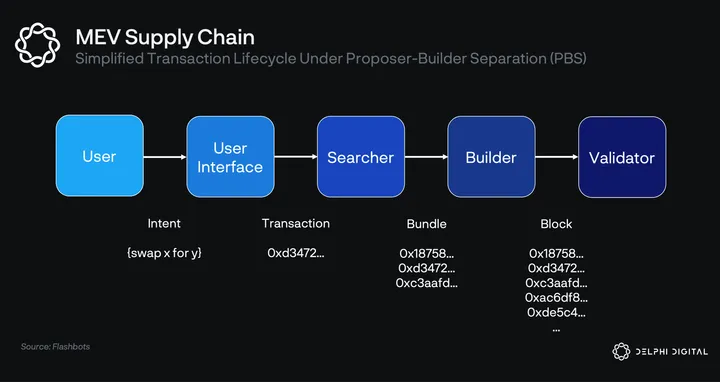

MEV Supply Chain

The oversimplified Ethereum MEV supply chain looks something like this under PBS:

- User – Express intent to enact some state transition (e.g., swap ETH → USDC).

- User Interface – UI allows the user to easily encode their intent into a transaction the blockchain can understand. This includes the whole app layer (wallet, smart contract, and dApp UI) working together to express user intent. This layer decides where to route user transactions (e.g., to the public mempool or private channels such as Flashbots Protect).

- Searcher – Run MEV strategies (e.g., arbitrage, liquidations) and submit “bundles” of their transaction preferences to builders.

- Builder – Aggregate transactions from various sources and construct a block (previously mining pool operators, but a distinct new role has been introduced post-Merge).

- Validator (Proposer) – Perform consensus duties. Proposers and builders have historically been the same logical entity by default, but PBS strips them apart.

Types of MEV

I’ll cover the major categories which encapsulate much of the value captured, but note a long-tail exists. The largest forms are becoming progressively commoditized (i.e., most profits get bid to the block producer), while the long-tail retains a higher margin for searchers.

Atomic Arbitrage

Arbitrage = Buying and selling an asset in different markets (or in derivative forms) to take advantage of differing prices.

Atomic = Entire transaction sequence successfully executes together, or they all fail together (no partial execution).

Example – A large ETH buy was just executed on SushiSwap. ETH is now $1,000 on Uniswap, but it’s $1,010 on SushiSwap. MEV searchers can submit bundles to atomically buy ETH on Uniswap and then sell it on SushiSwap until the arbitrage is closed. This benefits market efficiency without harming users, and it can provide riskless profits to extractors.

Statistical Arbitrage

Searchers can also take on risk to probabilistically capture MEV profits when conducting statistical arbitrage.

Example – ETH is trading at different prices on an Ethereum L1 DEX and a rollup DEX. Searchers could submit arbitrage transactions across these domains, but they run the risk that one trade executes while the other leg does not. They no longer capture a riskless profit from a sequence of transactions executing atomically. However, you can turn this specific cross-domain stat arb into (riskless) atomic arb if you control block production across domains.

Liquidity Sniping

This is another specific example of probabilistic MEV capture. Extractors who are willing and able to effectively manage risk across position sizing and timing will outcompete here.

Liquidity sniping entails purchasing some asset immediately after it’s listed in a DEX pair and liquidity is added. The sniper then offloads the position over an extended period of time, warehousing risk in the interim. In normal conditions, the asset price will rise significantly from its initial listing price. However, this isn’t guaranteed – the sniper is taking inventory risk as they offload it.

Frontrunning

Trades create a price impact – that’s why you set some slippage tolerance of where you’re willing to be filled. However, this opens up the ability to frontrun your trade.

Example – I want to buy 10 ETH for $10,000, but I set my slippage tolerance to 2%. Searchers can see this in the mempool, then swoop in and take that liquidity in front of me, causing me to execute at my worst price and getting only 9.8 ETH.

Generalized Frontrunning

This is the attack popularized in Ethereum is a Dark Forest. Generalized frontrunners can scan the public mempool for any transaction, simulate it with their own wallet address swapped in, then frontrun the original transaction with their own if it’s profitable. This reaches far beyond just simple DEX trading.

Backrunning

Intuitively, it’s the opposite of frontrunning.

Example – After I executed that trade earlier of $10,000 for 9.8 ETH, the price of ETH on that exchange is now ~$1,020. However, the global market price of ETH is still sitting at $1,000. Someone can profit by closing this gap – selling ETH right behind me at a premium until the gap has been closed back to $1,000.

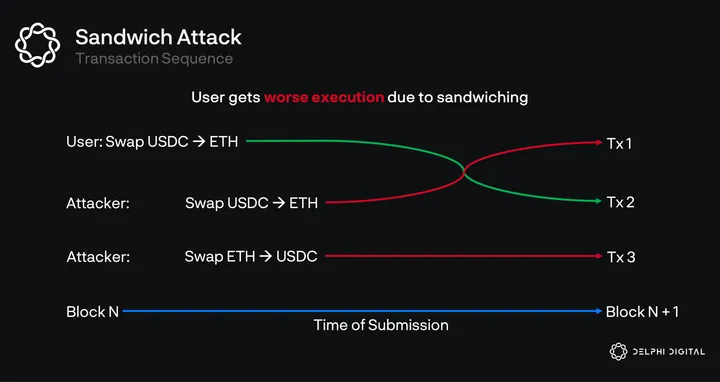

Frontrun + Backrun = Sandwich

Upon seeing a large trade order in the mempool, searchers could submit a bundle including (1) their frontrun tx, (2) the target tx, then (3) a backrun tx. They scoop up liquidity, allow the target to push up the price, then immediately sell it at a markup.

Liquidations

Open market participants are needed to liquidate under-collateralized loans. This helps to ensure a properly functioning DeFi market.

Example – User borrowed USDC against their ETH on Aave, but the price of ETH has since fallen. The borrower is now under-collateralized (i.e., USDC value is approaching the value of their ETH collateral, and is below the protocol’s collateral requirements). Anyone is able to liquidate this loan – they can pay off the USDC loan as quickly as possible, claim the ETH collateral, and sell it. Well-designed protocols can auction off the right to liquidate this position. The loan is closed, keeping the protocol solvent, and the liquidator earns a profit.

Just-in-Time (“JIT”) Liquidity

TLDR if you’re unfamiliar with Uniswap v3’s concentrated liquidity – LPs provide liquidity over a specific price ra

Read the full report

This report is part of Delphi Pro.

- 800+ Pro reports across every major sector

- Talk directly with our analysts

- Private community of funds and builders

Already a Pro member? Log in

0 Comments