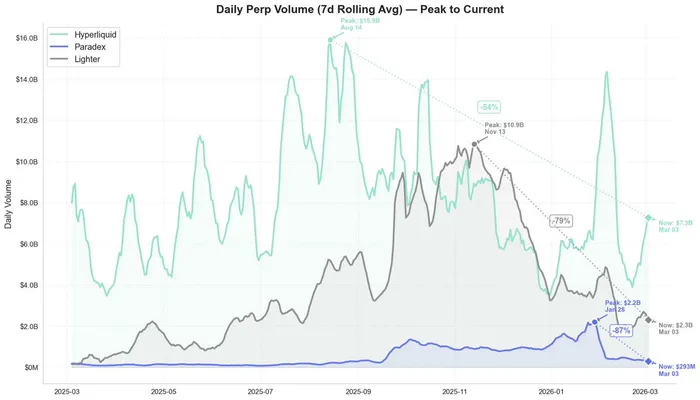

The last few months have been a rough rollercoaster for Paradex. They went from doing over $3B in daily volumes to now settling at ~$300 million. They have caught an incredible amount of FUD, none of which really fazed me.

Let’s touch on the first piece of FUD that everyone will talk about which is the decrease in volumes.

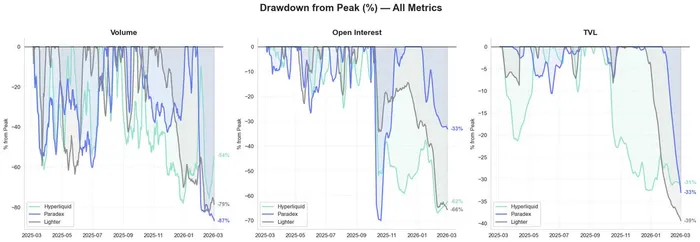

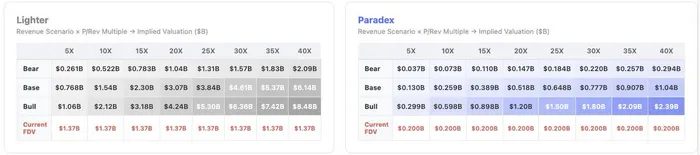

Here are a few charts that will help you think through this.

The end result is a 30-90% drawdown from their peak across metrics which is roughly in line with the two major onchain perp DEXs. So while the headline might say “Paradex volumes are down -87%”, net net, not as bad across various metrics.

The next common pushback will be: “Well no one will want to hold the second or third best perp DEX token as just owning the market leader tends to be the best bet.”

While this is generally speaking true I don’t hate the idea of owning a token where the entire @tradeparadigm team is building the product, trading at an attractive valuation (hopefully), while dated options and paradigm’s RFQ integration is just around the corner. This, “dated options and paradigm’s RFQ integration”, in my opinion, should be their go-to-market (GTM) strategy. Their GTM to-date has largely been leaning on zero fees and privacy. While I do believe that fees will compress and privacy does matter, “paradex = options and paradigm’s RFQ onchain” is a much simpler and idiotproof GTM.

This GTM push towards privacy and zero fees instead of options has actually been my biggest frustration thus far. I have had many conversations with the team about this. They are incredibly sharp and arguably the “smartest” perp team in the market today (so I am likely wrong here) but I have strongly felt that their biggest selling point was the paradigm options and RFQ integration. I guess, at the end of the day it’s a founder/team bet anyways, but I would like to see their GTM strategy pivot to, “paradex = options and paradigm’s RFQ onchain.”

BUT, maybe I am wrong, and the zero fees + privacy is the optimal GTM strategy and the token rips and is listed on Upbit and goes to Valhalla.

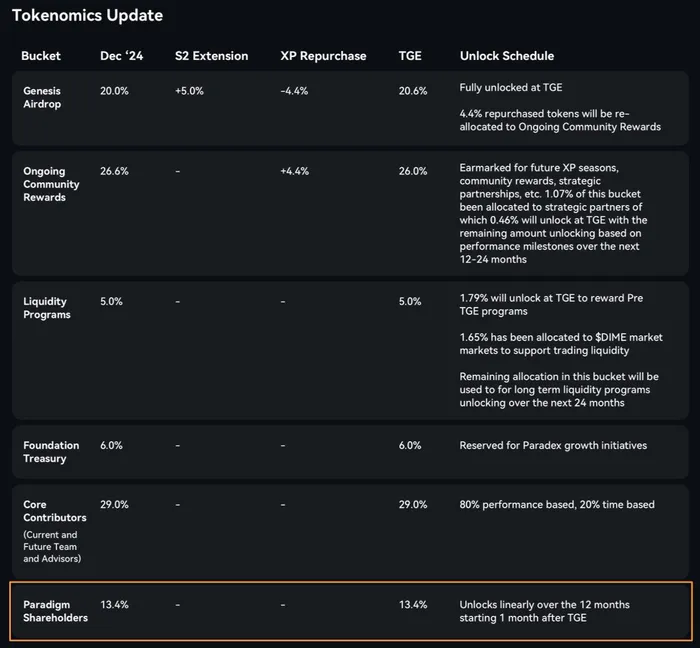

Maybe the last piece of FUD you will hear is the Paradigm Investor unlocks starting 1m after TGE and vesting over 12m.

To be honest, I don’t love this as it will be heavy sell pressure on the token for the first 12-months. This is quite a quick unlock and increases the total float by a good bit over the first year. I don’t really have an anecdote here. However, I can say that the team is incredibly aligned with their community. I have talked at length about how Hyperliquid created a cult by (1) making their users rich and by (2) being hyper-aligned with their users and token holders from day one. Paradex will have the opportunity to make their users rich over the coming months and they have the opportunity to maximally align with their community, which it seems like they are doing. Paradex has done something new here by buying back XP tokens pre TGE.

This gives me confidence that they will act in such a way that is in the best interest of their users and token holders.

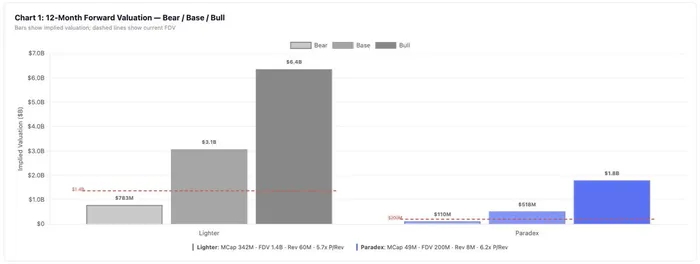

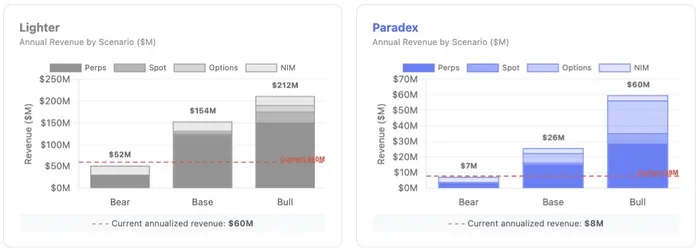

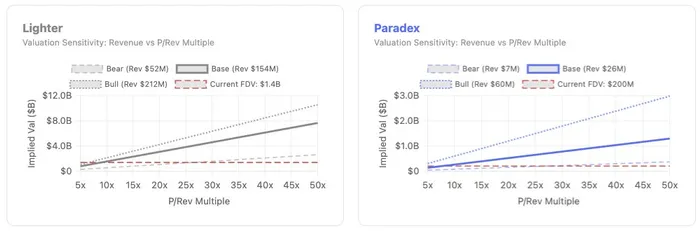

Revenues & Valuation

I won’t go into great detail on Paradex’s microstructure, because I have discussed this at length, but I still think RPI will give them pricing power on the fee side of things with MMs so I expect their effective take rate to go up and is applied in my bull scenario below.

Regarding revenues and valuations, it only feels appropriate to look at it in context of Paradex’s two biggest onchain competitors in @HyperliquidX and @Lighter_xyz.

One of the bigger issues for Lighter and Paradex from a revenue standpoint is that their effective take rate is so low. Now obviously this is, for both teams, one of their big selling points: “zero fees.” However, they sacrifice revenues in doing so. Therefore, it takes a lot more volume for them to generate the type of revenues we have become accustomed to from Hyperliquid. So for simplicity (and y-axis scaling) I’ll just show Lighter and Paradex.

I am estimating that $DIME will TGE around a $200M FDV. I will update after TGE.

In my model, a lot of Paradex’s success is tied to the success of options (my own opinion), while also having meaningful pricing power on their perps offering due to RPI. I believe options will be the product that brings in and attracts more volume/users than they would get otherwise. These users will stay due to robust unified margin across spot, perps, options, and prediction markets. This puts a lot of execution risk on options. If their options product doesn’t hit the mark, $DIME is somewhat hard to justify at $200M FDV regardless of what multiple you put on it given how competitive and cult-like perps have become.

Telling Your Story Before Those Short Your Token Do

One thing I hear consistently from funds is that investor relations (IR) in crypto is rough. Lighter and Pump both get this feedback a lot. I think this is largely because their tokens are pretty much down only but also because communication and transparency from the team is subpar. And Paradex won’t be immune to this public market scrutiny either. Investors want to understand your (Paradex) story. They want to know where you’re going, what you’re building toward, and why it matters. You don’t need to give away the playbook or share anything that crosses a line. But if you’re not telling people the broad strokes, someone else is going to tell the story for you, and it’s usually someone who is short your token.

Regulatory Picture

The CFTC has signaled that regulated perpetual futures are coming to the U.S. within the next month or so. Hyperliquid is already in DC. @jchervinsky is running @HyperliquidPC backed by $29M in HYPE, explicitly working on a DeFi derivatives framework. Lighter is US-based. Both of them are positioning for a world where onshore perps are legal and institutional capital has a compliant on-ramp, which I believe will happen this year.

Paradex doesn’t have a U.S. presence that I’m aware of. Being late to the US regulatory conversation will put you at a disadvantage, even though it might save you some money. Sure, they could just focus on Asia, which is a massive market, but not having a presence in the US will hurt.

The valuation isn’t expensive on an absolute basis or relative to peers (24x P/Rev on a FDV basis and if we move towards $125M FDV it feels cheap), the product roadmap makes sense, and Paradigm’s involvement on the options and RFQ side is a structural edge that no other perp DEX has. But the thesis requires two things to go right: options need to work, and the team needs to figure out their US strategy before the window closes. If both of those happen, this is an attractive bet but if neither of the above come to fruition, the current FDV will be seen as a nice exit for farmers.

Disclaimer: I hold $DIME.