Report Summary

Emerging Technology: Prediction markets are evolving into “world truth engines” that use financial incentives to reveal collective knowledge about future events, turning specialized insights into monetizable foresight.

Blockchain Advantages: Onchain prediction markets offer global participation, transparency, and composability, with market prices reflecting probabilistic outcomes of potential events.

Market Dynamics: Accuracy improves with attention and liquidity, with markets transitioning from inefficient Automated Market Makers (AMMs) to more sophisticated Order Books for deeper market depth.

Major Players: The market features two key approaches – Kalshi’s regulated, compliance-focused model targeting U.S. retail investors, and Polymarket’s crypto-native, globally-focused platform emphasizing speed and cultural relevance.

Unsolved Challenges: Critical issues include liquidity constraints, poor user discovery and experience, limited expression of user beliefs, market creation complexity, and oracle/resolution disputes.

Future Frontiers: Emerging applications include opinion markets, information markets, fantasy sports prediction, private opportunity markets, and potential governance models like futarchy.

Market Potential: The sector is estimated to have a $8–12 billion short to mid-term total addressable market, with potential to grow to $50B+ long-term, driven by intersections with sports betting, financial derivatives, and data intelligence.

Strategic Evolution: Success hinges on solving liquidity, user experience, and trust problems, with the ultimate vision of creating a decentralized, market-driven “truth machine” that can more effectively aggregate and validate collective knowledge.

Every system for discovering truth (science, journalism, capital markets) runs on incentives. Prediction markets make those incentives explicit.

If you spend as much time on crypto twitter as I do, you’ve been drowned in the noise of prediction markets (PMs). It’s been a chaotic mix of million-dollar election bets, outright speculation, and a lot of badge holders rehashing the same ideas. From the outside, it was easy to dismiss the entire category as another crypto-native casino.

I believe that is a profoundly wrong assumption.

After spending time in this rabbit hole, I’ve come to see that beneath the surface, a fundamental technological primitive is being forged. Prediction markets, in their purest form, are not about gambling; they are about monetizing verifiable knowledge. They are engines for aggregating information, challenging expert consensus, and revealing a real-time, financial truth about the future. They are, in essence, a world truth machine.

But this powerful engine is stalling. For all the hype, the industry is held back by a set of critical, unsolved problems: from creating sustainable liquidity to building a user experience that feels more like a terminal rather than a casino.

That is the purpose of this report. Together, we will dissect the core technology that powers these markets, from the incumbents to the startup disruptors. We will then confront the five most significant unsolved problems that represent the barrier between today’s reality and tomorrow’s multi-billion dollar expectations. Finally, we will look into potential solutions and the new frontier of applications that warrant our attention.

This is the deep dive I was looking for when I started. Let’s begin.

Tool for Truth (and Profit)

At its core, a prediction market is a simple and powerful concept: a market for outcome-contingent shares whose prices reflect the crowd’s estimate of each outcome’s likelihood.

This definition is the key to separating prediction markets from gambling. Gambling is about winning money from a “house” that has set odds against you. A prediction market is about monetizing verifiable knowledge. There is no house to bet against; the platform makes money from trading volume, not from your losses. This transforms the act of forecasting from a bet into a form of intellectual arbitrage.

Was there ever a field you were so knowledgeable in that you would have wagered on your insights against the consensus? For a friend, that niche is hip-hop and wrestling. What might seem like a nerdy flex is, in the era of prediction markets, a monetizable edge. This is the ultimate goal: to allow those with specialised knowledge, in any domain, to profit from their foresight.

For decades, this promise was limited by the constraints of traditional and blockchain infrastructure and regulatory hurdles. I believe the critical unlock for this new generation of prediction markets is the decision to build them onchain.

Important Question: Why Onchain?

If we can’t reliably provide a strong argument for this then we can pack up and go back to trading memecoins. It is important to answer this question especially when a platform like Kalshi proves prediction markets can function without a blockchain. In my opinion, the question isn’t about possibility, but about a philosophical and practical choice.

- Global, Permissionless Liquidity: Anyone, anywhere can participate, creating a deeper and more diverse pool of knowledge and capital. Efficient Market Hypothesis requires wide participation from a diverse set of market participants.

Case in Point: Théo, a French trader, participated with high conviction in the prediction markets for the U.S. presidential election. He proved the value of global participation, contributing to market efficiency and earning a reported $85 million profit. - Transparency & Trust: All market activity, from creation to settlement, is recorded on a public ledger, making manipulation by the platform difficult and settlement auditable. Crypto’s pseudonymous nature will lead to insider trading but with upgrades in decentralised ID and ZK verification, we have a credible path to tackling this challenge in the future.

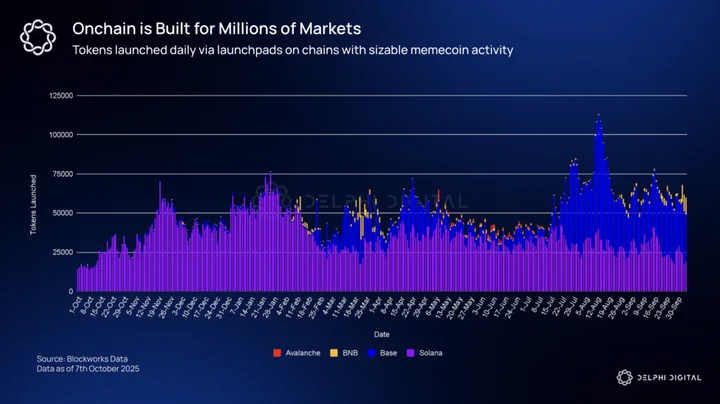

- Scalable Composability: This is the biggest unlock. Unlike traditional financial infrastructure, onchain systems are now built for both massive scale and open development. This splits into two key advantages:

- Market Breadth: Traditional exchanges are designed to serve a small universe of assets; the NYSE, for instance, lists around 2,400 companies. Crypto rails, in contrast, are battle-tested to handle a seemingly infinite supply of tokens and bootstrapping their liquidity alongside their creation. This is essential for a future where we expect millions of prediction markets on everything.

- Permissionless Building: A blockchain-based platform is not a closed product; it’s an open ecosystem. Any developer in the world can build tools and applications on top of the core market infrastructure without asking for permission. This fosters a vibrant ecosystem of add-on applications from sophisticated trading terminals to fantasy sports games.

- Market Breadth: Traditional exchanges are designed to serve a small universe of assets; the NYSE, for instance, lists around 2,400 companies. Crypto rails, in contrast, are battle-tested to handle a seemingly infinite supply of tokens and bootstrapping their liquidity alongside their creation. This is essential for a future where we expect millions of prediction markets on everything.

The Proof of Predictive Power

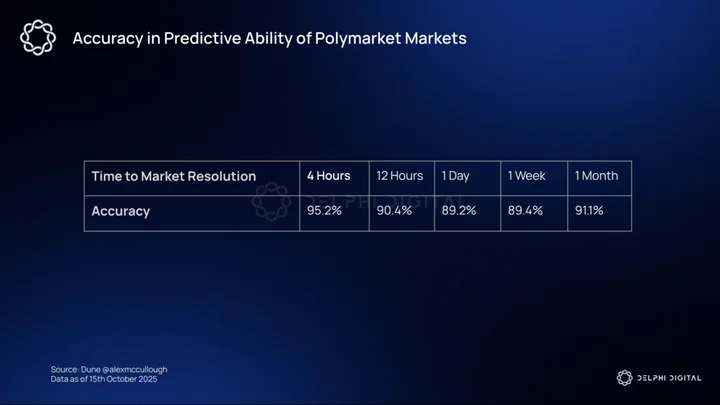

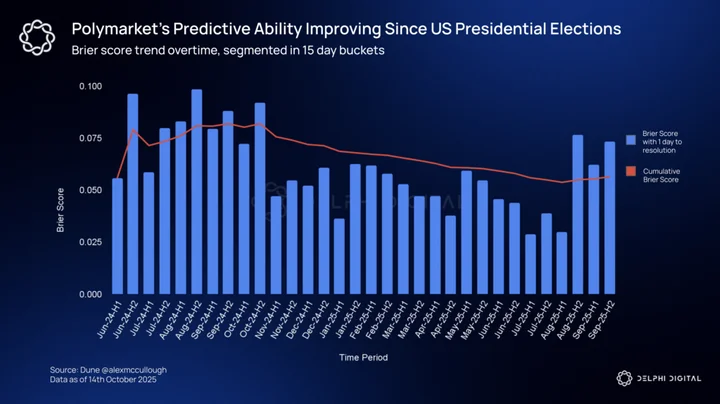

The ultimate test of a prediction market is its ability to accurately forecast the future. Simple metrics show high accuracy (Polymarket’s predictions are directionally correct over 95% of the time).

However, this accuracy does not reflect the prediction market’s precision in forecasting events. A more sophisticated measure is the Brier Score that calculates the mean squared difference between the predicted probability and the actual outcome, where a lower score (closer to 0) indicates a better prediction. H/T to Theia Research and Knower for introducing Brier scores and highlighting their importance for evaluating prediction market accuracy, respectively.

Analysis of Polymarket’s historical data reveals two insights:

- Accuracy Improves with Attention: The platform’s Brier Score has consistently improved over time, particularly after high-profile events like the 2024 U.S. Election brought a surge of new liquidity and participants. More attention leads to sharper, more accurate markets.

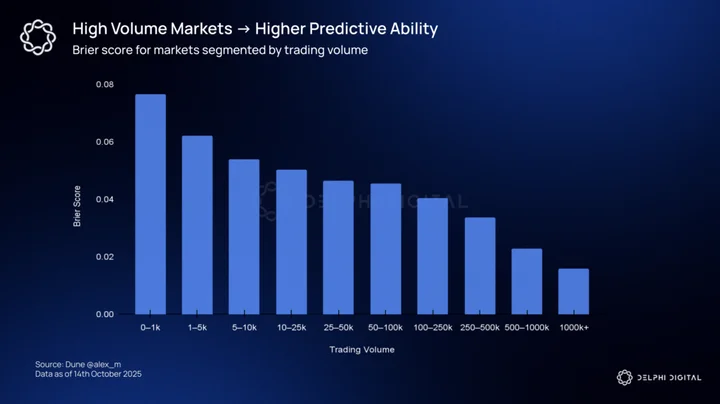

- Volume brings us closer to Truth: There is a direct and powerful correlation between a market’s trading volume and its predictive accuracy. Markets with over $10 million in volume consistently achieve the highest degree of accuracy. Liquidity doesn’t just enable trading; it powers the platform’s ability to find the truth.

The predictive power demonstrated by these scores, especially in high-volume markets, is difficult for any single individual or algorithm to replicate. It is the clearest evidence that prediction markets are not just speculative venues; they are powerful world truth engines in the making. For a deeper dive, readers can explore brier.fyi, which shows how this predictive power can vary by platform and market category, highlighting the strengths of each venue.

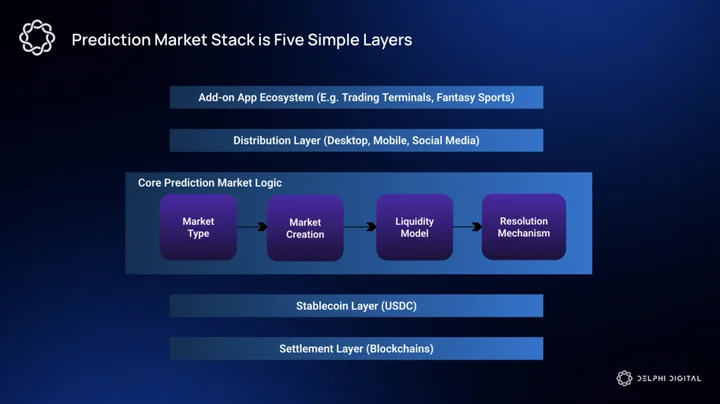

The Prediction Market Stack

To understand the current landscape, we must dissect the stack from the ground up. While platforms differ in their strategy, they all build upon a similar set of core components.

The Settlement Layer: The foundation of any onchain prediction market is the blockchain it’s built on. The requirements are straightforward: highly secure, high speed and throughput to handle rapid trading, and low transaction costs so that frequent, small-value trades remain viable. This is why most platforms are built on high-performance L1s or Layer 2 rollups.

The Stablecoin Layer: The universal collateral for onchain markets is the stablecoin, typically USDC. This provides a stable unit of accounting and is fundamental to the binary contract structure, where ‘Yes’ and ‘No’ shares must sum to $1.00. The key challenge here, especially for long-duration markets (e.g., the 2028 election), is the opportunity cost of locked capital. The evolutionary step for platforms will be integrating yield-bearing stablecoins, transforming locked funds into productive assets that can generate secondary revenue or be used to incentivize liquidity.

Kalshi already offers interest on users’ open positions and cash, Polymarket has started holding rewards offering 4% yield on open positions across 13 long duration markets. There are also startups like Robin.markets that are looking to bring yield on top of the holding rewards and extending yield to the long tail of polymarket markets.

The Core Logic: This is the engine of each prediction market. These are not minor implementation details; they are architectural decisions that dictate everything from the user’s trading experience to the platform’s capital efficiency and its ultimate position in the market.

- What types of events can be traded?

- How is liquidity provided?

- Who can create markets?

- How is truth determined?

These choices made here are the DNA of the platform. Understanding these levers is the key to understanding why the market leaders are designed the way they are, and where the opportunities lie for the next generation of applications. H/T to Baheet for sharing a framework to understand the core components of a prediction market.

Market Type

This defines the fundamental structure of the bet itself. The choice here has massive implications for user experience and liquidity.

- Binary Markets: The bread and butter of prediction markets, offering a simple “Yes” or “No” outcome. The two outcome shares are always priced to sum to $1.00 (e.g., a “Yes” share at $0.60 implies a 60% probability). Their simplicity makes them incredibly easy for users to understand and is the primary reason for their dominance. This structure also makes them highly composable, allowing them to be used as building blocks for more complex multi-outcome markets.

- Multi-Outcome Markets: For questions with more than two possible answers (e.g., “Who will win the UK election?”), platforms typically bundle several binary markets together (Labour vs. The Field, Conservative vs. The Field, etc.). While this works, it can be a clunky user experience and fragments liquidity across multiple contracts, making it a key area for future innovation.

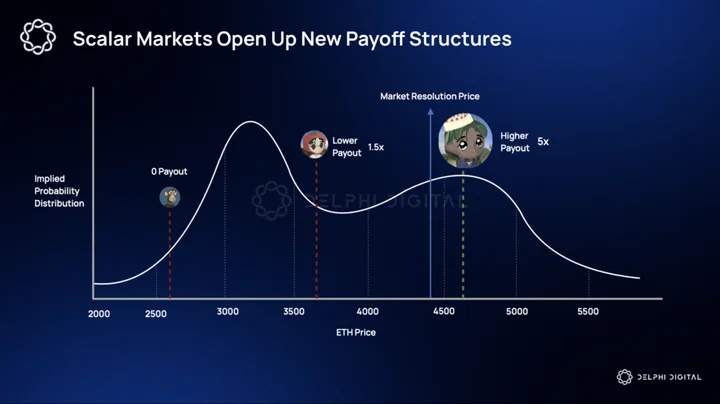

- Scalar Markets: This is an underexplored but powerful frontier. Instead of a binary outcome, scalar markets resolve on a continuous range (e.g., “What will be the total box office revenue for the new ‘Avatar’ movie in its opening weekend?”). They reward traders not just for being right, but for being more right than others. The primary challenges holding them back are user education and the difficulty of bootstrapping liquidity for a continuous range of outcomes. E.g. Trepa.io, Metaculus

Event Creation

This determines who has the power to launch new markets and represents a core philosophical choice for any platform. The industry operates on a spectrum between two poles:

- Platform-Curated: This is the model used by the current leaders, Kalshi and Polymarket. The platform’s team vets and lists all markets, ensuring they meet legal standards, have clear resolution criteria, and are likely to attract user interest. The major advantage is quality control and compliance, which builds trust and a coherent user experience. The obvious downside is limited breadth and speed; the platform becomes a bottleneck.

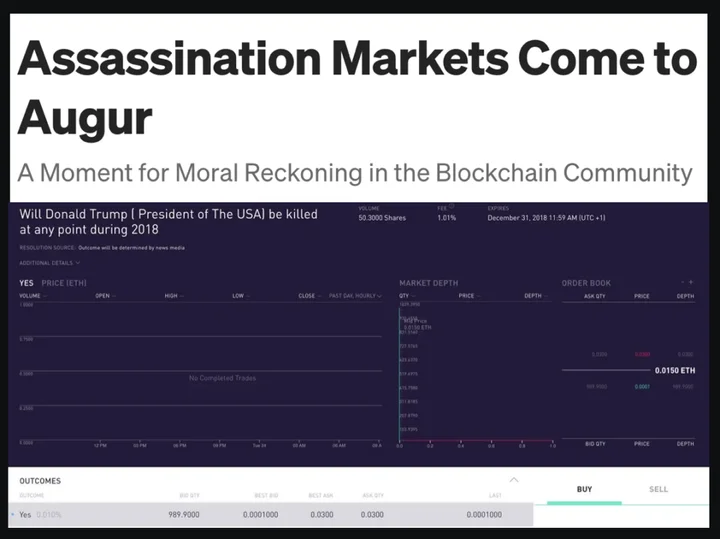

- Fully Permissionless: Pioneered by early platforms like Augur, this model allows any user to create a market for any event. The benefit is an explosion of speed and variety, allowing markets to be created on niche topics the instant they become relevant. However, this comes with significant risks: market fragmentation, low-quality or ambiguous markets, and the potential for harmful or unethical markets (like the infamous “assassination markets”) that can cause immense reputational and legal damage.

The optimal solution lies somewhere in the middle. A hybrid, community-driven model. This could involve systems where users stake their reputation and seed a portion of the liquidity while proposing markets. These markets are then vetted and further seeded by a community of curators and liquidity providers respectively, combining the speed of permissionless creation with the quality control of a curated approach.

Liquidity Model

This is the engine that matches buyers and sellers. The industry’s evolution here tells a clear story of a technology finding a fit.

- Automated Market Makers (AMMs): Early crypto-native platforms heavily relied on AMMs, often using algorithms like the Logarithmic Market Scoring Rule (LMSR). AMMs were revolutionary for DeFi because they solved the cold start problem, guaranteeing liquidity was always available. However, in prediction markets, they proved to be capital inefficient and one of the tokens in the pool is bound to go to zero eventually. Liquidity providers face the risk of permanent loss.

- Central Limit Order Book (CLOB): This is the model used by every traditional financial exchange, and it has become a consensus choice for modern prediction markets. A CLOB directly matches buy and sell orders, and doesn’t require a pool of passive, locked capital. One of the key turning points had been Polymarket’s migration from an AMM to an order book.

Platforms like Kalshi utilize a new approach, centering on a CLOB but supported by an internal trading arm and third-party professional market makers to ensure robust liquidity.

Outcome Resolution (Oracles)

This is the trust layer. When the event is over, how is “the truth” determined and the market settled? This is a critical point of failure and a key area of differentiation.

- Human-Reviewed: Kalshi, as a regulated entity, relies on a markets team that reviews event outcomes to ensure they align with the market’s specific criteria. This allows for nuanced interpretation of complex events but is slower and centralized.

- Automated Data Feeds: For purely quantitative markets (e.g., “Will BTC close above $70k on Tuesday?”), resolution can be handled automatically by pulling data from a trusted, high-quality API. This is the fastest and most objective method but is only suitable for a limited set of data-driven events.

- Decentralized Oracles: This is the crypto-native solution, used by Polymarket, relying on UMA’s Optimistic Oracle. A proposed outcome is put forth, and there is a challenge period during which any user can dispute it by posting a bond. This system is censorship-resistant and flexible but can be slower and, in rare situations, has led to contested resolutions that have damaged user trust.

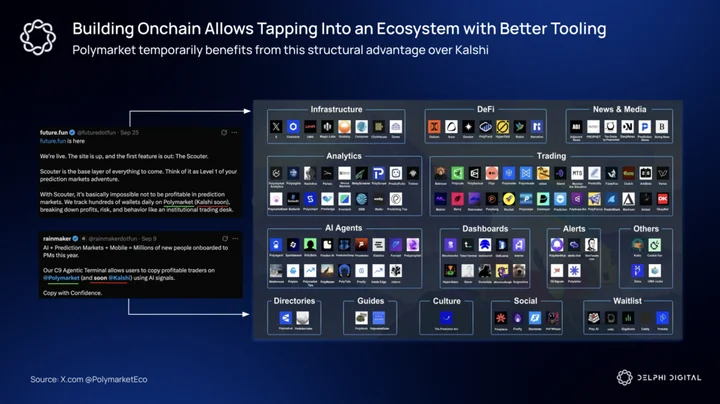

These foundational layers of settlement, collateral, and core logic form the powerful but invisible engine of the prediction market. While the complete stack also includes how these markets are distributed to users and the ecosystem of add-on applications they enable, those layers are where the unsolved problems and future opportunities lie.

We will intentionally defer a deep dive into those layers to later in the report. For now, we must first look at how the industry’s current giants have mastered the foundational engine we’ve just described. Let’s turn to the titans: Kalshi and Polymarket.

Majors and Moats – Kalshi vs. Polymarket

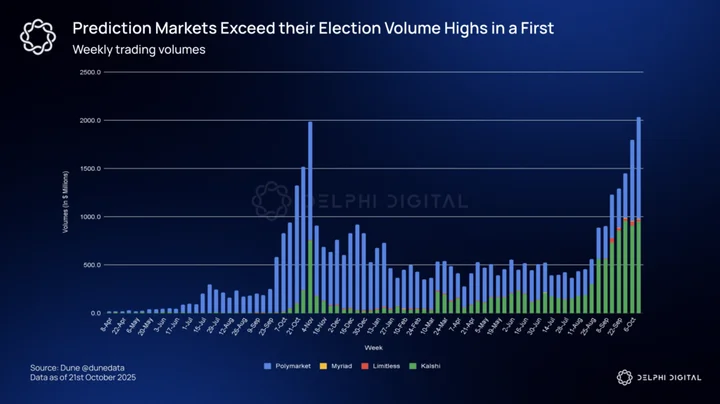

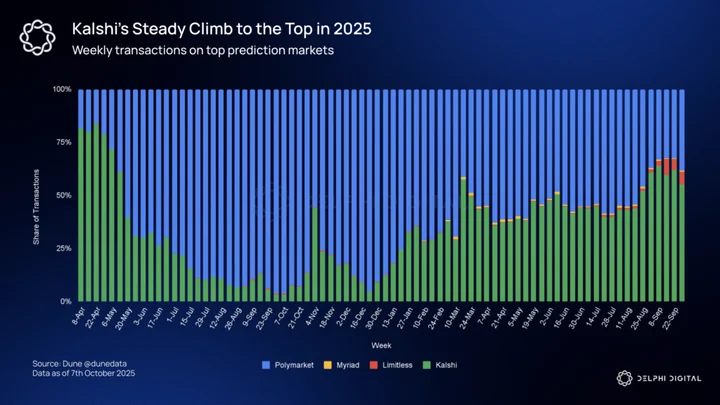

With a shared technological foundation, the competition between the two market leaders, who collectively command over 98% of the market share, has moved beyond the stack. The real battle is now one of high-level strategy, regulatory moats, and establishing a lead via new distribution channels.

Just to put things into perspective, the next nearest competitor Limitless does less than 10% of the volume of each of the leaders. While Myriad is the next biggest player in the generalised prediction market category, it ends up further back generating <1% of the leader volumes.

Kalshi

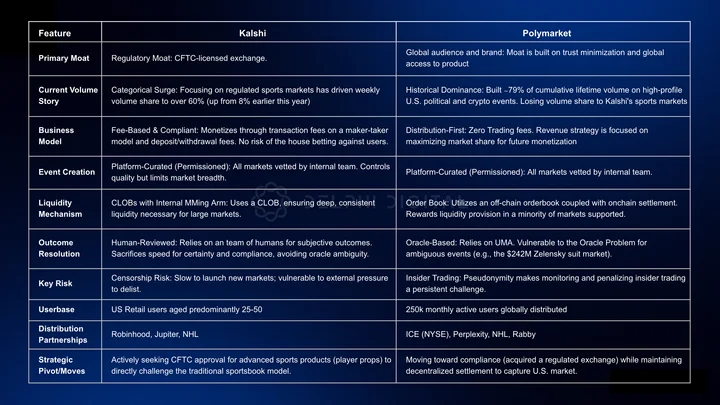

Kalshi’s strategy is to win by playing the long game of compliance and legitimacy. Their defining feature had been their status as a CFTC-licensed Designated Contract Market (DCM), a regulatory moat that took years of painstaking legal work to achieve. This is not just a license; it is their core strategic weapon.

- Go-to-Market & Moat: Kalshi’s regulatory status unlocks a user base that is untouchable by offshore competitors: mainstream US retail investors. Their moat is reinforced by key partnerships, most notably their integration with Robinhood, which gives them direct access to a massive, pre-existing pool of retail capital. Their plan is to become the “S&P 500 of events”

- Target Audience & Market Focus: Kalshi’s product is tailored for a demographic that values security and regulatory oversight, primarily US-based middle aged retail investors. Their market selection reflects this, focusing on verifiable, data-driven event contracts such as:

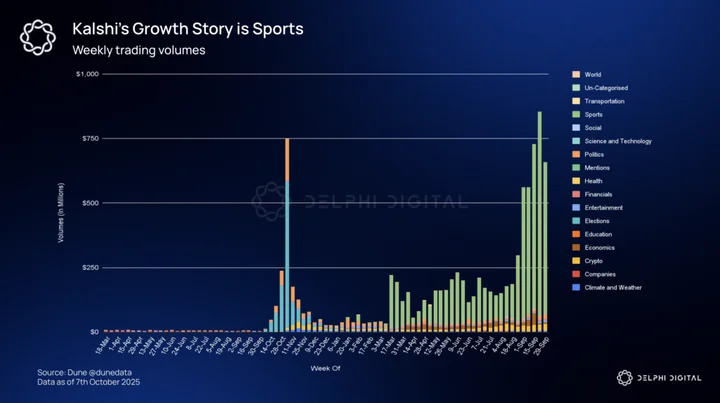

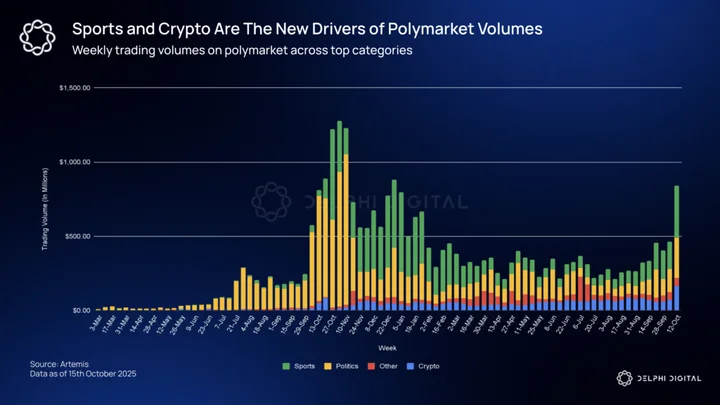

- Sports Markets: The US Sports betting industry is huge and is already feeling the pressure from Kalshi’s entry into the market.

- Political & Governmental Outcomes: Congressional votes, bill passages.

- Key Performance: While historically trailing Polymarket in total volume, Kalshi’s growth has been steady and consistent. With the surge in sports related markets they had briefly taken over the lead in trading volumes.

Polymarket

Polymarket’s strategy has been built on the core tenets of crypto: global accessibility and permissionless innovation. By operating onchain and outside of direct US jurisdiction, they have built a powerful moat based on being the most culturally relevant prediction market in the world.

- Go-to-Market & Moat: Polymarket’s moat is its brand. It is the default venue for high-stakes, global events and has captured the mindshare of the crypto-native and politically-obsessed users. They need to build speed as a competitive advantage; by spinning up markets on a breaking news story in minutes, capturing the narrative and liquidity before a regulated competitor could even draft the contract terms.

- Target Audience & Market Focus: Polymarket caters to a global, crypto-savvy user base. These are power users who are comfortable with self-custody wallets and value the platform’s censorship resistance. Their market focus is on grabbing global headlines and serving the insane appetite of the terminally online degen.

- High-Stakes Politics: US Presidential Election, international elections, and political appointments.

- Financial Metrics and Events: ETF approvals, token price targets, earnings targets.

- Key Performance: Polymarket is the undisputed leader in trading volume, often facilitating tens of millions of dollars on single markets. Beyond volume, their key metric is their predictive accuracy. By aggregating a vast, global pool of information, their markets have demonstrated a remarkable ability to forecast events, from election outcomes to ETF approvals, often outperforming traditional polls and pundits.

Another race between prediction markets will be in generating higher volumes per unit of open interest. Platforms like Limitless and Myriad, in their infancy, have targeted markets like price prediction markets (that look like 0DTE options) leading to higher volumes and activity. It will be important to monitor how such activity rates evolve as these platforms diversify into more categories.

The rivalry might have started as a clash of philosophies but increasingly looks like both platforms are converging across most design decisions and the fight from here on out will be around distribution and solving user pain points.

The Five Unsolved Problems

Despite the technological convergence and the billions in volume, the prediction market industry is still a fraction of its potential size. A gauntlet of five fundamental challenges holds it back. Solving these problems is the goalpost for the next generation of builders, and the platform that cracks them could dominate the future of the market.

The Liquidity Problem

Liquidity is the lifeblood of any market, and its absence is the single most significant factor holding prediction markets back. The core issue is a vicious, self-reinforcing cycle where:

- A new or niche market starts with low liquidity.

- A trader who wants to participate faces bad execution, high slippage, and the inability to fill a large order without drastically moving the price.

- This poor experience deters more traders from participating, keeping trading volume low.

- Low volume means the market’s odds are less accurate and less reliable as a source of information, which in turn deters potential liquidity providers who see no active, profitable market to support.

- This leads back to step 1, the market remains illiquid.

This is the classic chicken-and-egg problem. You need high volume to attract deep liquidity, but you also need deep liquidity to support it. This “liquidity paradox” is why the long tail of interesting, niche markets on most platforms are ghost towns, even if the headline markets are active.

It’s difficult to break the cycle because the liquidity providers have to lock up their capital in a market for an unspecified duration, often for weeks, with no secondary yield. Polymarket already runs an incentive program that rewards market makers providing liquidity on selected markets. Choosing the right set of markets to incentivize and a well designed liquidity bootstrapping mechanism will be critical in growing the long tail of markets.

The Discovery & UX Problem

The current user experience for finding and engaging with markets is too vanilla. Platforms are often just a long, contextless list of questions. For a user to participate, they must already know what they’re looking for. This is a massive barrier to entry. New users aren’t greeted with markets tailored to their interests or expertise. There is no personalization layer, no curation, and no effective way to navigate the thousands of potential markets. This discovery failure makes the platforms feel inaccessible and limits their appeal to a small core of power users.

The Expression Problem (Parlays & Leverage)

The current binary market structure is a blunt instrument. While simple to understand, it severely limits the confidence a trader can express in their own beliefs. This ultimately forces users to lock up far more money than necessary to represent their true convictions. This challenge breaks down into two core missing pieces:

Leverage

Adding leverage to binary prediction markets is not as simple as converting the polymarket book into a Perp DEX product. PMs resolve in a zero-sum way i.e. each share is ultimately worth either $1 or $0, making volatility and inventory risks far more severe. With annualized volatility exceeding 1,500%, these markets are already extreme without leverage.

Unlike tokens that can rebound after dips, PM outcomes are final. A leveraged trader’s position is highly path-dependent: volatility and delays to resolution increase the odds of liquidation. Even if the trader is directionally correct, leverage can wipe them out before settlement.

We also need to consider two factors about liquidity

- Most PMs function with far less liquidity than token pools and

- Liquidity in PMs dries up as probabilities move toward extremes.

Both of these make leveraged positions fragile, since thin order books are easier to manipulate. A large trader could deliberately swing prices to extremes to trigger liquidations, then profit from the rebound. For market makers, leverage multiplies an already tricky problem of participating in prediction markets: one side of the market is guaranteed to settle at $0. Managing such inventory risk in a leveraged environment is uncharted territory, which is why existing platforms have stuck to spot-only trading.

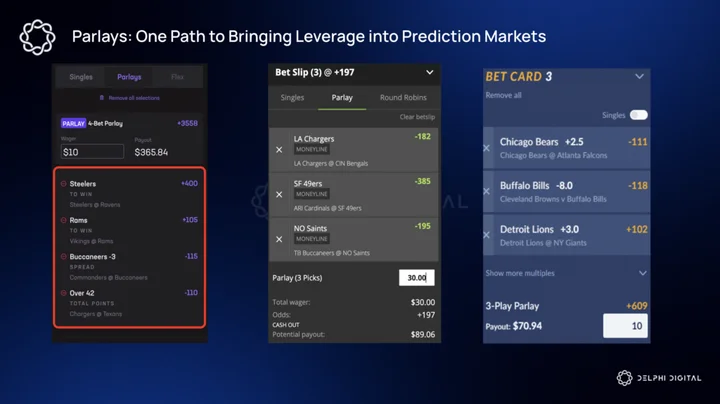

Many researchers suggest borrowing a page from the playbook of sportsbooks to give users the taste of leverage that they desire in the form of parlays.

Lack of Combinatorial Markets (Parlays)

Sportsbooks operate like a Risk Insurer. A sportsbook like FanDuel or DraftKings can offer a 12-leg parlay at enormous odds because they operate as a single counterparty i.e the house. They manage a giant, diversified book of risk. They don’t need to pre-fund every ticket’s maximum payout. They manage their net exposure across millions of bets, knowing that contradictory outcomes (e.g., one parlay has the Lakers winning, another has the Warriors winning) cancel each other out.

Prediction Markets operate like an Escrow Agent. They must fully collateralize every contract the moment it is traded. If a position could pay out $20,000, that $20,000 in cash equivalent must be locked in escrow immediately. This is a core requirement for maintaining a trustless, solvent platform, but it is brutally capital-inefficient. The prediction market is an escrow agent, locking cash for every possible outcome.

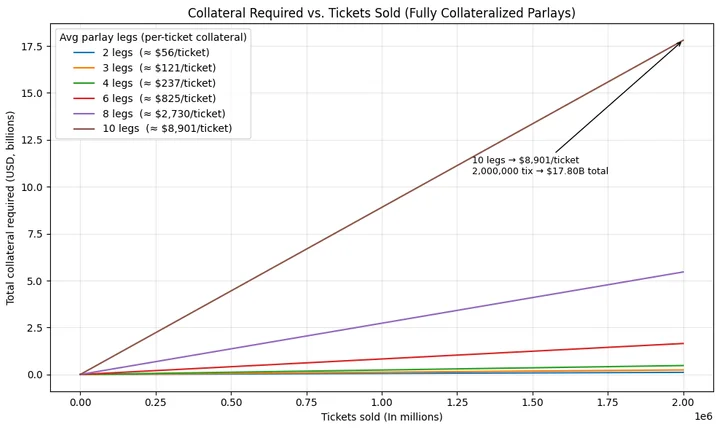

This simple difference means the parlay math for a prediction market blows up terrifyingly fast:

- Long-Tail Payouts: A simple $5 parlay at +100,000 odds would force the counterparty (a market maker or another user) to instantly lock up $5,000 in collateral.

- High Ticket Volume: Even a fraction of a standard sportsbook’s demand of parlay tickets in a single day would require market makers to lock up hundreds of millions of dollars just to collateralize these long-shot bets.

- Disproportionate Scaling: Each additional longshot leg added to a parlay multiplies the required collateral, not linearly, but exponentially.

Forcing market makers to dedicate their capital to backing these highly improbable, long-tail bets is a catastrophic drain on liquidity. It starves the core spot markets of the liquidity they need to function.

Permissionless Market Creation Problem

The industry is caught between two flawed models for creating new markets: the slow, centralized curation of the major platforms, and the chaotic, anything-goes permissionless model. I believe neither of these approaches is the ideal end state that we should be striving for.

The core issue is that relevance has a half-life. The most explosive, high-volume trading opportunities often emerge from breaking news and cultural moments. By the time a centralized platform vets and lists a market, the initial wave of interest has often passed.

A market on ”Will the academy rescind Will Smith’s Oscar for Slapping Chris Rock?” would have generated immense volume in the three to four hours immediately following the event, when the question was plastered across social media. A rigid listing process makes capturing this spontaneous, explosive interest difficult to say the least.

This is the promise of a permissionless listing system: the ability to create markets at the speed of culture, much like memecoins are spun up on platforms like on pump in immediate response to world events. However, this permissionless ideal consistently runs into three major challenges:

- Semantic Fragmentation: If ten different users create ten slightly different versions of the same question, liquidity is split into ten useless pools with none of them garnering trading volume.

- The Liquidity Cold Start: A newly created market has zero liquidity, leading to the “chicken-and-egg” problem in its most extreme form.

- Quality Control: Without a vetting mechanism, the platform is flooded with low-quality, ambiguous markets that destroy user trust.

These problems will persist but the team solving this will have unlocked a massive new category of markets. They need to build a system that is as fast as pump.fun but has the built-in guardrails to prevent fragmentation and ensure a baseline of quality and liquidity.

The Oracle and Resolution Problem

A prediction market is fundamentally a contract on a future truth. The entire system collapses if users do not have absolute faith in the mechanism that determines that truth. The Oracle is therefore the most critical and vulnerable piece of the entire stack. This isn’t just a technical challenge; it is a crisis of trust, with polymarket’s current approach showing major flaws.

Polymarket uses UMA’s optimistic oracle, which is designed to be censorship-resistant and capable of resolving any subjective question. In practice, however, this system has been brittle. Ambiguously worded markets have led to highly controversial resolutions. A clear case study of this oracle problem is the infamous Zelensky Suit incident. A Polymarket market, which attracted hundreds of millions of dollars in volume, asked a simple question: “Will Zelensky wear a suit before July?”

The market’s ambiguity became a crisis when, in late June, Zelensky attended a NATO summit wearing a formal black blazer and matching pants—a significant departure from his usual military attire.

- The Yes side argued that media outlets widely reported it as a “suit” and that it met the technical definition (a jacket and trousers cut from the same cloth).

- The No side argued it was a stylized, non-traditional jacket, worn without a tie, and that Polymarket’s oracle (UMA) had previously resolved “No” for a near-identical outfit.

The market was disputed and escalated to UMA’s token-based voting system. This is where the system’s brittle economic design was exposed. The value of the bet (hundreds of millions) was vastly larger than the cost to corrupt the vote, leading to widespread accusations that UMA whales could place a massive bet on Polymarket and then use their disproportionate voting power to force their desired outcome. Such incidents leave many users feeling the decision making process is unfair.

Kalshi, as a centralized entity, has built a sound resolution system that has scaled successfully till date. Their approach utilises well defined rules at market creation and an independent 3rd party information source. At the same time, it allows for human nuance, which is essential for interpreting edge cases. However, this creates a centralized point of attack and becomes resource intensive as the number of markets multiply from here.

Voided Markets Problem

As sports markets becoming an ever increasing part of prediction markets we have another problem that compounds the infuriating user experience: the voided market. This is prevalent in the high-volume sports category but also applicable when a market’s terms are deemed too ambiguous.

When a key condition isn’t met (like a specific player not participating in a game), the market is simply canceled and all capital is to be returned. But how would a platform return all capital in a simple situation like:

- A trader, let’s call her Alice, buys a “YES” contract for a NBA team’s win from another trader, Bob for $40.

- Alice then sells that same contract to a third trader, Charlie, for $60, making a profit of $20. Alice withdraws her $20 profit from the exchange.

- The game is then canceled, and the exchange decides to “void” the market. The platform has to now return back $120 but holds only $100 in reserves

This is a deeply frustrating and unproductive outcome for everyone (except Alice). It represents a failure in the market creation process and punishes traders who spent time and capital participating in good faith.

The Solution Space

After looking at the absolute dominance of Kalshi and Polymarket and the scale of their treasuries, a natural question arises: Is there any room for smaller players to exist?

Initially, I struggled to answer this question myself, but the answer is yes, and new players are the most likely source of the breakthroughs the industry needs. The Five Unsolved Problems are not just challenges; they are a roadmap. They are the alpha. The opportunity for the next generation of builders is in attacking these foundational problems directly.

The incumbents are locked into their respective models, leaving the future wide open. This section will serve as a playbook for the insurgents, outlining some potential solutions for the problems we’ve discussed.

The Liquidity Problem

Since most platforms are opting for a orderbook based liquidity model, I’ll make suggestions to improve liquidity for such a setup. Polymarket already employs a system with rewards allocated individually for each market spending over $10.5Mn, whereas Kalshi has spent over $9M to date.

Before the 2024 US election, Polymarket took a risk and decided to give away >$50k per day to its MMs ($1.7 per $100 in volume)

Today, they give $0.025 per $100

Polymarket has burned ~$10M. And in doing so, made prediction markets healthy with rebates close to perp exchanges pic.twitter.com/ppUFQ4O4zB

— defiance (@defiance_cr) August 31, 2025

I want to propose a system that rewards the quality, placement, and persistence of capital. This is how you break the paradox and build a market deep enough to support institutional volume. This system has three core layers:

Layer 1: Quality-Weighted Maker Rebates

The foundational layer must be an always-on system that rewards the quality of a quote, not just its existence. Platforms can pay a rebate that scales based on the metrics that genuinely improve the trading experience.

- Time-at-Best (how long a quote is the best offer),

- Quoted Size (depth)

- Spread Tightness.

This is the most direct way to reduce slippage and sharpen price discovery. For a regulated exchange like Kalshi, this offers simple, auditable transparency. For Polymarket, it’s a verifiable, onchain mechanism to align rewards with value delivered, mirroring the proven tiered systems of top exchanges like Binance.

Layer 2: Cross-Market Reward Tiers

To prevent market makers from only servicing the most popular, high-volume markets, the platform must bundle risk and rewards. Under a Franchise Tier system, market makers can only unlock the top-tier rewards by committing to maintain target liquidity across a diversified, pre-approved universe of markets, including the long tail. By linking a maker’s ultimate profitability to their service across a basket of disparate markets, the platform can direct liquidity towards markets they believe will drive volume in the future.

Layer 3: Surge Multipliers & Batch Auctions

The final layer is to ensure liquidity is present when it is needed most: during peak volatility.

- Surge Multipliers: Around scheduled catalyst events (a CPI report, a political debate), the platform activates time-boxed multipliers (e.g., 3-5x) on maker rebates. This is a powerful economic signal that strategically concentrates capital at the point of high user demand.

- Frequent Batch Auctions (FBA): To protect market makers from being on the receiving end of toxic flow by high-frequency traders during these volatile windows, the platform can temporarily switch to Frequent Batch Auctions. By collecting and matching orders at a single price every few seconds, FBAs neutralise microsecond speed advantages and create a fairer environment, encouraging market makers to provide deeper liquidity during critical moments.

The Discovery and UX Problem

Here we need to unbundle the interface from the core protocol. The future of the user experience is not a single frontend, but different tools that cater to the entire user spectrum. This breaks down into two key opportunities:

The Curation Layer

The goal for mass adoption is to transform the user experience from a financial terminal into a personalised, engaging feed. Prediction markets must adopt the data-driven personalisation techniques perfected by social media and e-commerce.

The Spotify Model: The user onboarding could be inspired from spotify’s onboarding. Instead of a generic list, the platform should surface markets based on a user’s explicit interests (tags they follow), location, social graph, and past trading history. If a user primarily engages with esports and pop-culture markets, those markets should dominate their home screen, not a generic fed rate hike market.

Social trading tools are also an interesting category to watch out for as they allow users to participate in prediction markets they discover on social media and messaging apps where users already spend time discussing these topics. E.g. Polycule (Telegram), FliprBot, PrediBot (Twitter), Competi (Discord).

Contextual Integration will become more critical as the sector matures. The platform that identifies user preferences and intelligently recommends relevant markets will see a dramatic increase in engagement and trading volume.

The Power-User Layer

For the professional and power-user segment, discovery is less of a problem than data density and execution speed. A massive opportunity exists to build “The Terminal” for prediction markets. The parallels to memecoin trading are clear: first came the launchpads (pump.fun), then came tools to improve access (telegram bots like BananaGun), and finally came the professional trading terminals (gmgn, Axiom) that became indispensable for active traders.

These terminals, which can integrate with multiple underlying platforms (Polymarket, Kalshi, etc.), can justify charging fees by offering a suite of indispensable features:

- Market Aggregation & Order Routing: A single interface to view odds across all major platforms and route trades to the venue with the best price and lowest fees. E.g. TradeFox, Flipr, Stand

- AI Assisted Market and Opportunity Discovery: Utilizing AI to augment and improve a trader’s decision making process E.g. Polyfactual, Polymtrade, Polysights or utilizing agents to help users passively participate in prediction markets E.g. Polytrader, Billy Bets, Rainmaker

- Real-Time News & Data Integration: A live feed of news, social media sentiment, and economic data integrated directly alongside the relevant markets and their impact on a trader’s open positions. E.g. Verso Trading, BetMoar, fireplacegg

- Onchain Intelligence: Tools for tracking the flow of smart money, identifying large wallet movements, and analyzing the positions of top traders. E.g. Hashdive, Polymarket Analytics, Polyburg, Polyscope.

- Advanced Risk Management and Order Types: Tools that allow users to model complex scenarios and utilize order types such as TWAPs and trailing stop losses for professional traders. E.g. TradeFox

- 3rd Party Leverage: Offering leverage on selective high volume markets with their custom liquidation engines. E.g. Flipr

This is the category with the highest concentration of new PM startups. By splitting the user experience into these two paths: a personalized feed for the 99% and a data-dense, professional terminal for the 1%, the UX problem is likely to be solved first.

The Expression Problem

Teams like TradeFox are already working towards introducing leverage in prediction markets. Instead let’s discuss how parlays can be scaled in prediction markets. One of the approaches suggested by researchers combines a proposed HIP-4 with a RFQ/JIT based system that allows counterparties to compete in an auction to price parlays based on the underlying event markets. This method however does not address the escrowed collateral problem.

Parlays on HIP-4

In this post @rajivpoc @kratikl_ @0xkrane and @noops_eth provide a framework on how to build

parlays using HIP-4 pic.twitter.com/gz1V7SRhZG— bedlam research (@bedlamresearch) September 26, 2025

I believe the answer is not a one shot solution, but an upgrade that methodically de-risks parlay underwriting.

Phase 1: Constrain the Design Space

The first step is to treat parlays not as a feature for everyone to create, but as a specialized, high-risk product underwritten by professionals.

- Dedicated Counterparties: Instead of allowing any user to underwrite a complex parlay, the platform must initially rely on a select group of professional Market Makers (MMs). These MMs have the sophistication to price and hedge the complex, combinatorial risks that grow exponentially with each added leg.

- DeFi Opportunity – Parlay Vaults: A crypto-native platform like Polymarket could innovate here by introducing ERC-4626 Parlay Vaults. Users could deposit capital into these vaults to earn real yield, generated from collecting the risk premium on these low-likelihood tickets (For reference: parlays accounted for 70% of all NFL and NBA bets placed on FanDuel). The vaults themselves would be managed by MMs, not requiring them to lock up more capital and allowing the LPs to underwrite the risk.

- Strict Market Constraints: The “pick-your-own-legs” model is too risky initially. Platforms must offer a limited, curated menu of pre-approved markets for parlay inclusion. This is exactly the approach Kalshi is taking by initially offering only same-game parlays. Furthermore, the Time-to-Resolution (TTR) must be kept low. This allows MMs to turn over their capital rapidly.

Phase 2: Introduce a Simple Net Margin System (NMS)

Pivot from Escrow to Net Risk: The NMS shifts from requiring collateral for every possible payout to requiring only margin for the maximum net loss based on the MM’s entire book. The system would need to be able to identify mutually exclusive outcomes (e.g., Lakers win & Warriors win in a LAL-GSW game) cannot both happen, freeing up the capital that would otherwise be locked against impossible scenarios.

This dramatically improves capital efficiency, allowing MMs to underwrite more tickets and use their freed-up capital to provide liquidity elsewhere on the platform.

Phase 3: Correlation-Aware Risk Engine

A basic Net Margin System is a good start, but it’s not paranoid enough for real-world chaos. The final step is to upgrade it to handle sudden shocks.

Jump Risk Problem: A market maker’s book might seem balanced, but a single piece of news (e.g. star player’s injury into a game) can instantly change all the relationships between bets. This is “Jump Risk,” where a seemingly safe, diversified position suddenly becomes a massive, directional bet.

The risk engine must constantly run automated stress tests against these worst-case scenarios. Requiring Market makers to hold enough extra collateral to survive these simulated shocks. This ensures they are always prepared for a sudden crisis, protecting the platform and its users. Successfully building this infrastructure doesn’t just replicate the sportsbook experience; it can surpass it as the odds offered via prediction markets can very realistically be better than sports books (no need to charge Vig).

Polymarkets “Nothing Ever Happens” markets are another fun experiment that are structured as inverse parlays where missing out on every leg of the market leads to the market resolving to yes.

Permissionless Market Creation

This is the problem statement that piques my interest the most and we have quite a few independent solutions being explored. As an early stage startup it becomes ever more challenging to attract professional market makers or active traders to improve market depth by placing limit orders on the CLOB. Hence we see the recurring element of AMM adjacent designs for user generated markets.

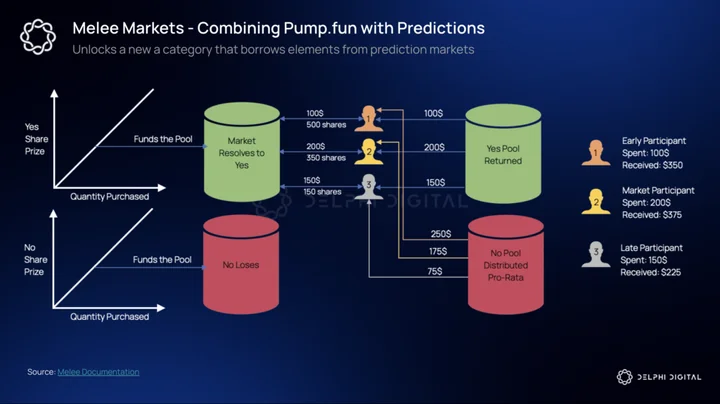

Melee borrows a bit of inspiration from the pump.fun model to bootstrapping new prediction markets by removing the need for centralized market makers or liquidity providers. Instead of relying on an orderbook or AMM with prices capped between $0–$1, each outcome in a Melee market has its own bonding curve. By doing so Melee is not limited to just binary markets but can support up to 32 outcomes for each market.

When participants buy shares in an outcome along a bonding curve, their deposits are added to that outcome’s pool. This has a few important externalities. By selling these outcomes along a bonding curve, there arises an incentive for traders to participate in buying outcomes as early as possible (sniping and acquiring outcome tokens for cheap).

To avoid these snipers/early participants from dumping tokens on unsuspecting users who wish to participate into a prediction market, Melee doesn’t allow sale of outcome tokens until market resolution. Upon resolution, the winning side first receives its initial stake back, and then the remainder of tokens (USDC) held in all losing outcome pools are distributed proportionally among winning shareholders.

What works in this design?

- Design is made to appeal to a crypto native audience. The earlier someone buys, the lower their entry price on the bonding curve, and therefore the greater their potential percentage return. It’s an elegant incentive structure that mirrors the memecoin-like payoff that many users have been looking for in prediction markets.

- Markets can be deployed instantly, with no requirement for a counterparty, team, or governance gatekeeping the process. Liquidity grows naturally as participants buy into outcomes, and no one can pull liquidity once the market begins.

- Design is not limited to pure play prediction markets and can be extended to build opinion markets with quick resolution.

What are the challenges to adoption?

- However, the design does trade off flexibility. Like most parimutuel systems, all liquidity is locked until resolution. There’s no secondary market to exit a position or hedge mid market. This can push away many traders who do not wish to hold positions till the resolution of each market.

- As these markets become popular the only way to reduce the probability of an outcome (A) is to purchase an ever increasing amount of outcome (B). If the market keeps flipping odds between outcomes it becomes very costly to bring the odds inline with the real probabilities. At scale these markets are likely to deviate from the real probabilities of event occurrence.

Overall, Melee’s model is a direct path toward fully permissionless prediction markets that rewards conviction, early participation, and expands beyond the binary market model.

XO Market takes an equally innovative approach, building on top of the foundational Logarithmic Market Scoring Rule (LMSR) used in earliest attempts at prediction markets.

How does it work?

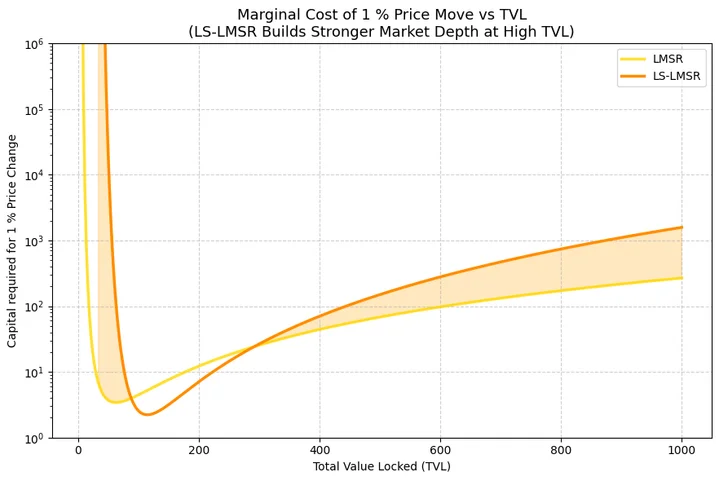

Any user can create a market, but they must provide an initial liquidity seed. This solves the cold start problem and also reduces the risk of spam markets. The market then runs on a Liquidity-Sensitive variation of LMSR (LS-LMSR), where the market’s depth and efficiency automatically increase as more TVL is locked into the liquidity pool. Calculating the capital needed to move the prediction market odds shows us how liquidity depth can be successfully enhanced by pivoting to LS-LMSR over the original LMSR design.

Additionally market creators earn a small fee on every trade, incentivising them to create high-quality, popular markets. For resolution, it uses a multi-layered system: an AI-oracle provides an initial proposal, which is followed by a challenge period and, if necessary, a final verdict from a decentralised court of staked human jurors.

What works in this design?

- Baseline Liquidity & Aligned Incentives: Every market is liquid from block one. The creator fee and capital requirements directly align the interests of the creator with the health and popularity of the market they’ve built.

- Robustness: The LS-LMSR ensures that popular markets attracting liquidity become highly efficient to trade, while the multi-layered resolution system gives it the speed of AI with the fairness of human oversight.

What are the challenges?

- The Toxic Flow Problem Near Expiry: The LS-LMSR model is designed to deepen liquidity as more capital enters. However, as a market nears resolution, the information becomes clearer, and the incoming order flow becomes increasingly toxic to LPs (e.g., betting on an NBA game in the final minutes). The AMM, in its current form, isn’t designed to protect LPs from these near-certain losses.

The Next Steps?

The solution space is still nascent, with other teams like Buzzing, PMX also tackling the problem. The PMX model, for example, utilizes an interesting AMM coupled with an arbitrage bot. In its current form, its “lossless” liquidity model creates an illusion of market depth that results in poor execution, high costs for the trader.

I believe the most promising path forward lies in synthesis of elements across designs. One of the solutions can combine the incentivized, creator-driven model of XO Market with the risk management of Paradigm’s proposed dynamic pm-AMM. This would introduce time-based liquidity decay, a mechanism to protect LPs from the inevitable toxic flow as a market nears expiry.

— (@DaftaryNeel) July 14, 2025

The Oracle Problem

While a critical problem, the oracle challenge may be less of a standalone startup opportunity and more of a fundamental piece of infrastructure that all future platforms must perfect. The future of resolutions is a multi-layered stack:

- Automation Layer (For Speed & Efficiency): The base layer leverages Verifiable AI (from protocols like Allora Network, Mira or Talus Labs) to automate the resolution of most markets that are straightforward. The AI scans trusted data feeds and instantly proposes an outcome. To prevent spam, any user challenging the AI must post a financial bond, which is forfeited if their challenge fails.

AI Oracles present a promising approach to automated truth verification of information.

We tested their use in 1,660 high-stakes prediction markets on @Polymarket, realizing an 89% accuracy in outcomes.

Dive deeper into the approach & results 👇https://t.co/RJzXUXPeRU

— Chainlink (@chainlink) March 21, 2025

- Expertise Layer (For Dispute Resolution): For complex or subjective disputes, a layer of human oversight will always be essential. An ideal system moves beyond the capital-based voting and instead uses reputation-based juries, where voting power is tied to a juror’s onchain reputation score (earned through past, accurate decisions, leveraging protocols like Ethos Network) and combine it with token voting. This is to ensure that decisions are made by those with proven expertise, not the largest bag.

- Security Layer: For the highest-value markets, the ultimate source of truth must be cryptographically secure. This can be achieved via a Multi-Oracle Consensus from independent data providers (Chainlink, Pyth, and Redstone). To provide a tamper-proof audit trail and verify the integrity of the entire process, Zero-Knowledge Proofs (via services like Succinct Labs) could be used. This provides mathematical certainty that the resolution is both accurate and honestly reported.

New Frontier

The future of prediction markets will not be a single, monolithic platform, but a vibrant ecosystem of adjacent applications. These are standalone product categories that leverage the core mechanics of prediction markets – incentivized forecasting, information aggregation, and skin-in-the-game to create entirely new experiences. Here are five such frontiers:

Opinion Markets: Meta Prediction Markets

Opinion markets are a fascinating twist on the classic model. Instead of betting on a factual outcome, participants bet on what the crowd will believe. For example, “Will over 70% of participants bet yes on this market?”

These markets can have an incredibly fast resolution loop. The market can settle in hours or days, based solely on its own internal dynamics, removing the need for slow external oracles. It also creates a powerful social meta-game, rewarding players who can accurately predict collective psychology, not just objective facts.

This model is perfect for monetizing cultural influence. Platforms like Melee Markets, Fact Machine, vPop.wtf (scalar opinion markets) and Opinions.fun are aiming to allow influencers and communities to create viral markets on subjective, trending topics, turning social capital into a direct economic engine.

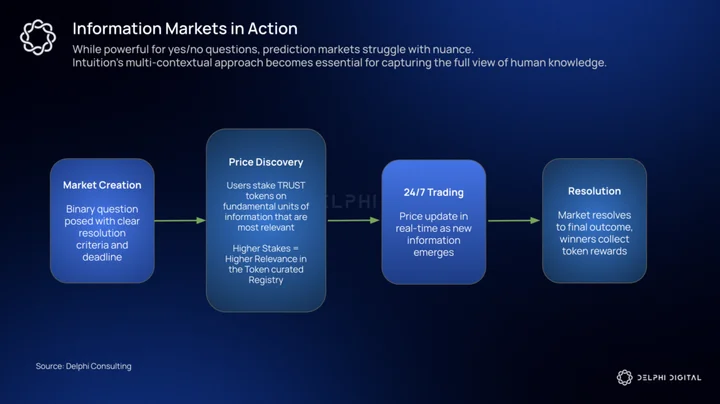

Information Markets: Curating a Knowledge Graph

Prediction markets are great for converging on a single, binary truth (“Yes or No”). But most questions are far more complex. This limitation creates an opportunity for Information Markets, which are designed to curate and validate such data.

These markets use staking mechanics not to predict an outcome, but to validate pieces of information and their relationships to each other. Users are rewarded for staking on data that the broader community deems useful or accurate.

This shifts the goal from predicting a single future event to collaboratively building a graph of collective knowledge. It’s a new primitive for decentralised data curation and token curated registries, with projects like Intuition Protocol pioneering the mechanism.

Fantasy Sports

I’ll make an attempt to position fantasy sports in a new light. I think of fantasy sports games as a high-cadence, recurring prediction markets with proven potential (It is a $25Bn industry). In games like Football.fun (FDF), users are essentially playing a series of weekly prediction markets wherein the performance of their assembled team is measured against other players. The goal is still to predict the best playing players for the week subject to constraints like budget caps.

This model is inherently attractive because:

- Tournaments typically can be run once or twice a week, translating to repetitive markets that drive sustained volume and engagement.

- It allows users to monetize their deep, niche knowledge of a sport, moving beyond simple bets into combinatorial predictions (e.g., predicting the collective performance of a squad of players).

Platforms like FDF have a structural advantage over both traditional fantasy leagues and physical collectible based games. The underlying assets are tradable and represent a prediction of a player’s in game value. This divorces the game’s economy from the slow, inelastic supply constraints of physical items (gacha boxes). The digital ecosystem can be tweaked to adjust player supply, contract costs, or prize pools to serve a massive and rapidly growing user base in a way physical-first systems never could.

Private Prediction Markets: Opportunity Markets

Opportunity markets is another primitive proposed by the Paradigm team that adapts the mechanics of prediction markets to solve a distinct problem – connecting institutions to a network of early, valuable information. They function as private, decentralised scouting programs, transforming external insights into business signals.

In this model, a Sponsor (e.g., a VC firm, music label, or corporate R&D arm) provides all the liquidity for a specific, highly niche market (e.g., “Will we invest in Startup Y this year?”). Participants in these markets act as Scouts, and are incentivized to participate in the market. As Scouts with high conviction buy “YES” shares, the rising market price becomes a proprietary data-aggregated signal that the Sponsor must (re)investigate the opportunity.

These private markets utilize TEEs and delayed issuance of outcome tokens to solve two key problems that plague public markets:

- Overcomes the free-rider problem by ensuring the valuable price signal remains visible only to the sponsor.

- Solves the long-tail liquidity issue by making the sponsor interested in the signal the permanent market maker.

Read More: Opportunity Markets

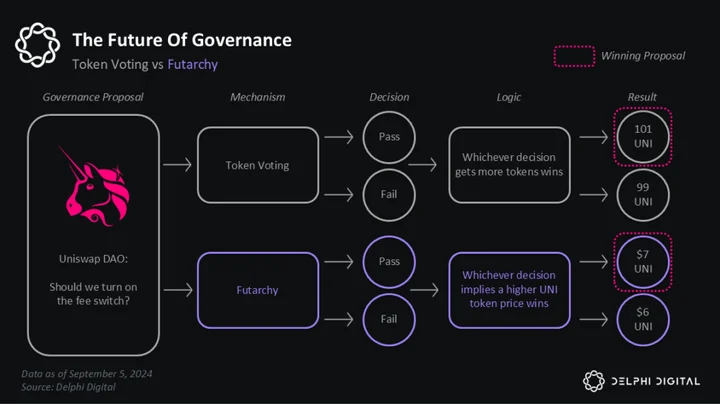

Futarchy

Futarchy is a governance model that delegates policy decisions to the intelligence of a market. The core idea is: “Vote on values, but bet on beliefs.”

A DAO or community needs to first agree on a goal (e.g., “maximize user growth”). When a new proposal is made, two conditional prediction markets are created: one for the outcome if the proposal passes, and one for if it fails. The proposal is automatically adopted if the market predicts it will lead to a better outcome for the stated goal.

This transformation of governance from a subjective popularity contest into an objective, information-driven exercise has gotten crypto people excited about DAO governance for the first time in years. It forces participants to put capital behind their beliefs, surfacing informed insights and making it more likely that the organization achieves its goals.

Read More: Markets will save the World

And the best part is that we’re not just limited to these applications. Teams have started to build Prediction market based news platforms (Boringnews), lending markets for PM positions (Gondor), Setting up prediction market funds (Polyfund). And this layer of applications will keep on expanding.

Sizing the Prediction Market Category

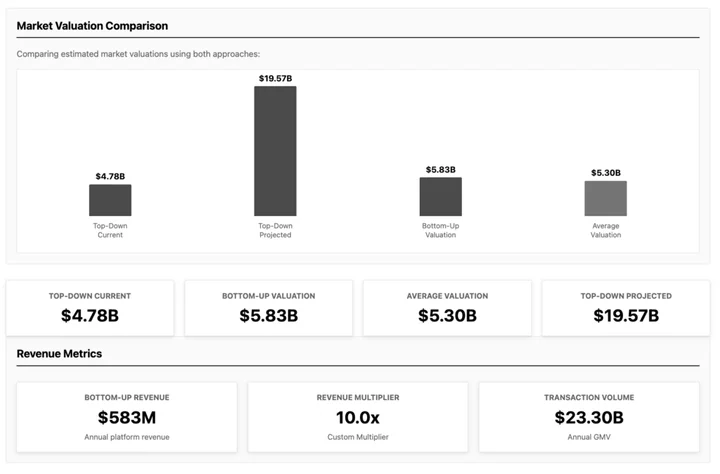

To truly grasp the scale of the prediction market opportunity, a single comparison is insufficient. The category is a hybrid, blending elements of financial markets, gambling and alternative data providers. We’re using a dual methodology to create a range of estimates for the Total Addressable Market (TAM).

The Top-Down Analysis

The first approach is to view prediction markets as a disruptive competitor, poised to capture a share of massive, adjacent markets where similar economic behaviors already exist. We identify established proxy markets and estimate a realistic capture rate achievable in the near future. The core formula is straightforward:

Market Size = Proxy Market Size × Capture Rate × Regulatory Accessibility

The potential pools of capital are immense. They range from the most direct competitor, the $203 billion global sports betting market, the $127 billion online gambling market, and even aspirational targets like the $450 billion retail financial instruments and $82 billion market research industries.

The Bottom-Up Analysis

The second approach builds the market size from the most fundamental unit: the user. We identify distinct user archetypes, estimate their population and annual spending, calculate the total platform revenue, and then apply a valuation multiple from a comparable industry. The user base is not a monolith, but a mosaic of key groups: high-volume financial traders, the massive pool of sports bettors, politics enthusiasts, and high-value professional forecasters.

The Final Estimate

Using both methods provides a crucial reality check. The Top-Down approach grounds our estimate in the reality of existing markets, while the Bottom-Up approach is grounded in plausible user behavior.

We estimate the market size using grounded expectations about emerging user behaviour and the ability of prediction market platforms to compete with existing industries. Based on this, we estimate short to medium term market opportunity in the $8 billion to $12 billion range.

Some readers might disagree with my assumptions and are free to utilize the tool (Prediction Markets Market Sizing) to calculate the opportunity size inline with their own expectations.

Comparing this grounded estimate to recent private market activity is insightful. With the recent Polymarket fundraise at $9 billion and a Kalshi round at $5 billion, it’s clear that investors are pricing in a much more optimistic growth scenario. These combined valuations, which are almost double the low end of my estimate, suggests a strong belief in a rapid clearance of regulatory obstacles and an explosive growth in user volumes.

In the grand scheme of things, I do believe the category will grow to over $50-80 Billion. The key difference in our theses is simply the time horizon it will take to reach that monumental scale.

Reality Check with Risks

This deep dive would be incomplete without confronting the substantial risks that could cap the industry well below multi-billion-dollar juggernaut expectations. The bull case is compelling, but we face a few challenges.

Regulatory Flip Flop

The bull case assumes a clear path to regulatory clarity. The bear case is that the industry can be trapped in a cage of legal ambiguity and targeted restrictions.

- Permission can Always Become Prohibition: The CFTC’s proposal to ban election betting is a key example. It signals that even if a product finds a market, regulators can challenge its very existence overnight. Legal victories, like Kalshi’s, are temporary truces in a battle that can be restarted with any new administration or rule change.

- Unsolvable Problem of Insider Trading: For mainstream users, rampant insider trading is a dealbreaker. If the perception of a rigged game takes hold, it will permanently poison the well for organic, retail adoption, regardless of the technology’s potential.

The other day a student asked me about the prevalence of insider trading in prediction markets. I now have an answer. pic.twitter.com/CpYLCstLw5

— Jason Furman (@jasonfurman) October 10, 2025

There are counterarguments by the permabulls that the possible occurrence of insider trading is a feature and not a bug as it allows the private information a way to enter into public domain in the quickest manner. I disagree completely with that framing as healthy markets function with the right toxicity ratio, or ratio of retail to smart traders. In a world where insider trading is rampant your toxic flow increases and retail participation dips simultaneously.

Liquidity Troubles Persist

The bull case relies on new solutions and incentives to solve or at least patch the liquidity problem. The bear case argues that thin, fragmented liquidity is a permanent structural feature, not a bug to be fixed.

Unlike a single, deep market for BTC or ETH, prediction markets inherently splinter liquidity across thousands of short-lived contracts. The proposed solutions for sustainable liquidity may not be enough to overcome this constant churn and fragmentation. This structural thinness could deter serious institutional capital, leaving the industry perpetually reliant on a smaller pool of retail flow and capping its ultimate size.

The Adoption Chasm

The bull case believes better UX can bring prediction markets to the masses. The bear case argues that the chasm between the product and a mainstream audience is a psychological one, not a design one.

- A Niche Product for a Niche Mindset: The “marketification of everything” may only ever appeal to the terminally online degens. For the vast majority, the idea of trading shares in outcomes may not be as appealing and familiar as buying equities.

- Incumbents Fight Back: Sportsbooks like DraftKings already own a major segment of casual bettors and will push to maintain their market share by pressing on their advantages. For serious hedging, corporations will almost always prefer the legal certainty of regulated derivatives. Prediction markets risk being squeezed from both ends i.e complex for the masses, and not suitable for the institutions, leaving them trapped in a small middle ground.

Conclusion

This report began by framing prediction markets not as a niche betting tool, but as a primitive for aggregating information and discovering truth. We’ve seen the data that proves their remarkable predictive power, but also confronted the formidable challenges and problems that keep them from reaching their full potential.

The journey through these problems reveals a clear truth: the challenges themselves are a map for the next generation of builders. The solutions, from architecting sustainable liquidity and multi-layered oracles to finally cracking the code on parlays, are the shifts that will unlock more growth that the investors in Polymarket and Kalshi are most definitely pricing in with the recent multi-billion dollar valuation rounds. In turn, this foundation will spawn a new frontier of adjacent applications, from engaging consumer games to powerful trading tools.

One of the most surprising takeaways from this deep dive was my own evolving view on the need for a native platform token. Initially skeptical, I now see it as a critical piece of the puzzle. A well-designed token can make a difference across many verticals of operations. It is a tool for –

- securing the protocol (acting as oracle collateral and dispute bonds)

- powering the ecosystem (funding liquidity and tooling incentives),

- enabling entirely new products like the parlay vaults we discussed

- Lever to drive volumes via trading rewards

$BTC$ETH$BNB$SOL$POLY 🤔 https://t.co/HmMobU6nBh

— Shayne Coplan 🦅 (@shayne_coplan) October 8, 2025

It can be a complete game-changer for accelerating the platform’s flywheel. Hoping that the Polymarket token is this and much more.

The ultimate vision is to build the world truth engine. The road is long, and the risks are real. But the promise of a world where the instant, probabilistic judgment of the market is an indispensable tool for decision-making is too significant to ignore. The shift to an information economy powered by prediction markets feels, in the long run, inevitable.

0 Comments