Introduction

The video games industry has seen many defining genres throughout the years, but few have had as rich and impactful a history as Massively Multiplayer Online Role Playing games (MMORPGs). From the emergence of Multi-User Dungeons in the late 1970s to the MMORPG staples we know today, players have immersed themselves in these virtual worlds for decades.

A study conducted in 2005 found that more than 80% of MMORPG players spend over 6 hours gaming per week. Comparing this to the roughly 80% of non-MMORPG players who spent less than 6 hours gaming per week demonstrates the increased levels of engagement this genre typically generates.

When combined with gameplay features common in MMORPGs, such as crafting, deep player progression, and trade, these outsized levels of player engagement often translate into large and complex virtual economies. Nowhere is this more evident than in games like Second Life, Entropia Universe, and Eve Online, which have grown their virtual economies to an estimated GDP of $650M, $400M, and between $7M–$18M, respectively.

However, an engaged and highly invested player base alone is not always enough to ensure continued market growth in the current competitive landscape. Most MMORPGs are supported by a notoriously sticky fan base with high switching costs, and each new release faces large execution risks. Since the genre’s peak in the early 2010s, it has been incredibly hard for new MMORPGs to take market share from the incumbent flagship titles.

Additionally, due to the huge content scope and long development time of most MMORPGs, the costs to ship these titles are often hundreds of millions of dollars. For example, it is estimated that the development costs for Destiny, New World, Star Wars: The Old Republic, and Star Citizen (development ongoing) were $140M, $200M, $200M, and >$600M, respectively. This excludes costs associated with marketing and content updates.

Despite the inherent risks, a growing number of blockchain-powered MMORPGs are experimenting with new business models and novel player experiences in attempts to redefine the future of the genre. Although there are numerous challenges with balancing blockchain-based open economies, we remain excited by the next generation of MMORPG leveraging blockchain technology to create fully player-driven virtual worlds.

Years after Axie Infinity first brought blockchain gaming to the broader public’s attention, the number of veteran teams bringing their vast experience building MMORPGs to Web3 is at an all-time high. These teams recognize the potential value Web3 integrations can unlock and are actively testing blockchain’s superior payment rails, increased agency over player-owned assets, and improved economic transparency in games such as Metacene, MapleStory Universe, Project Awakening, and Avalon.

At the same time that there is more quality developer talent than ever before, the consumer and regulatory landscape has never been better. Asia, in particular, is fast becoming a global hub for blockchain-based MMORPG. This is thanks to a number of factors, such as progressive blockchain regulations, favorable monetization and gameplay preferences, and a pro-crypto outlook. Teams with a proven track record in China, South Korea, Japan, and South East Asia (SEA) are well positioned to capitalize on this evolving market.

This report will offer a deeper view into the MMORPG genre, explore opportunities and threats a blockchain-based approach has, and dive into one of the key case studies that will help define this genre’s future.

A Brief History of MMOs

The first significant instance of a global MMO came in the form of Multi-User Dungeons (MUDs), a new type of online game that emerged in the late 1970s. While these early iterations were purely text-based adventures that lacked the 3D environments and graphical fidelity we take for granted today, they still managed to capture the attention of a generation and offered players a new way to interact online. In fact, MUDs were so engaging that it has been reported that by as late as 1994, they accounted for as much as 10% of all global internet traffic.

The popularity of the genre – especially among younger generations that were able to convince their parents to cover the relatively expensive broadband costs – demonstrated the potential for immersive virtual worlds and attracted the knowledge and capital needed to kickstart the flywheels of growth.

Titles such as Neverwinter Nights, which launched in the early 1990s, added new depth to the player experience and helped shape the future of MMOs with the introduction of features like character creation, character progression, world persistence, and a strong focus on social interactions between players. The game’s popularity and novel distribution via AOL led to users queuing for hours and spending hundreds of dollars on internet bandwidth to access the game.

Technical innovation, much of which was pioneered by these early MMORPG developers, helped further reduce entry barriers and grow the total addressable market. The first game to showcase just how large this market would become was Ultima Online (UO), which launched in 1996 and evolved into one of the most impactful games ever made.

UO went on to establish the game subscription model and was the first game to hit over 100k subscribers. This spurred even more innovation as competition heated up at the forefront of this new form of entertainment. UO had set the stage, but it didn’t take long before a number of other successful MMORPGs emerged and further raised the bar. Notably, EverQuest, Lineage 1, MapleStory, and Final Fantasy XIV (FF14) are all considered some of history’s best MMORPGs. However, with over 7M active subscriptions (around 12M at its peak in 2011), World of Warcraft (WoW) is the most successful MMORPG to have ever been made.

Current Day Landscape

Over the last 15 years, WoW has cemented itself as the market leader in the West, followed by FF14, Elder Scrolls Online, and RuneScape. They all share a similar subscription model that relies on retaining a large player base by continuously adding content and new quests. The benefits of this model are that it creates a sticky player base and a relatively reliable revenue stream that allows the developer to avoid pay-to-win (P2W) monetization models, often viewed as predatory by Western players.

However, subscription models can cap the maximum revenue potential of a game, cost a lot (in terms of maintaining a full content pipeline), and present a barrier to entry for many players in developing markets.

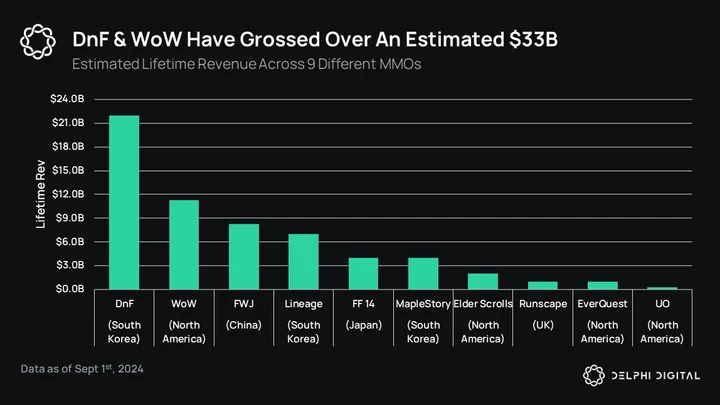

As opposed to Western MMORPGs, Eastern titles typically bet on a free-to-play approach, are often cross-platform, and come with much deeper monetization potential by design. The emphasis on grinding instead of questing, paired with the ability for players to accelerate their progression through in-game spending, has led Eastern MMORPGs to generate significantly more revenue compared to their Western competitors. For example, compared to WoW’s estimated $11.3B in lifetime revenue, Dungeon Fighter Online (DnF), a South Korean MMO, has generated approximately $22B in revenue since its launch in 2005 despite having fewer players.

Traditionally, the Western MMORPG player base in the US and Europe has largely consolidated across a few standout titles, while the Eastern landscape is arguably more fragmented. In China, WoW, DnF, and Fantasy Westward Journey (FWJ) are incredibly popular, boasting over 1 billion cumulative lifetime players. Meanwhile, South Korea has long been an MMORPG development powerhouse, seeing franchises like MapleStory reach over 100M lifetime players. Interestingly, in Japan, a market that is typically not great for MMORPGs, FF14 stands out as being the only breakout global success to have maintained a sticky domestic and international player base.

A final point should be made regarding the increasing number of cross-platform MMORPGs, especially in the East. One of the largest bottlenecks during the early days of MMORPG was the fact that it was a hardcore genre that was only really available on PCs. This materially impacted the size of the total addressable market in regions where the average household income was not high enough to own a household computer.

Despite many Asian countries getting over this monetary hurdle thanks to the proliferation of internet cafes, distribution dynamics have changed dramatically over the past decade with the advent of mobile gaming. Not only has this led to more games being released, but it has also grown the market considerably in developing regions, such as LATAM and SEA.

It should be noted that Eastern MMORPGs are better suited for mobile, in part due to user preferences and in part due to key gameplay trends. The typically more grindy core game loop is perfect for idle play, a feature common in many mobile games. Additionally, in order for MMORPG P2W monetization to work well, you need high levels of player liquidity. High-spending whales aren’t interested in spending thousands on cosmetics and powerups in barren virtual worlds. The high accessibility of mobile F2P allows studios to expand into new markets, facilitating the establishment of an invisible social hierarchy, which is the prerequisite for any whale-based economy.

Some stand-out case studies, in terms of lifetime revenue, include Lineage M (the mobile port of the hugely successful Lineage series), which has grossed almost $5B since 2017 (note that this is predominately from Eastern countries), and Fantasy Westward Journey, the China-exclusive that hit $2B in revenue two years after its launch in 2015 ($6.5B by 2019). As for more recent launches, MapleStory M, the mobile revamp of the multi-billion dollar > 20-year-old franchise, netted an estimated $55M in revenue within 35 days of its launch in China alone. The more recent launch of DnF Mobile surpassed $100M in just ten days of its China market launch ($270M within one month).

The current landscape of MMORPG is predominantly dominated by a relatively small number of decades-old IPs. The increasingly large development and marketing budgets needed to compete, combined with multi-year-long development cycles, make launching a new MMORPG a highly risky decision for a studio. For example, Amazon spent hundreds of millions on the development and launch of New World, only for it to suffer from hour-long queue times at launch and a current concurrent player count of <4k.

Fans of the MMORPG genre are becoming increasingly frustrated with the number of new releases that fall below expectations, leading to a period of almost ten years of stagnation. However, opportunities remain for studios that can leverage the best of what makes the current leading MMORPG so successful and improve upon it with novel mechanics and systems designs.

Web3 MMOs

While there are a number of highly anticipated upcoming releases that hope to take market share away from the incumbent leaders, such as Ashes of Creation and Throne and Liberty, there is a growing subset of new entrants that are uniquely differentiated in their value proposition.

Blockchain technology has the potential to enhance the MMORPG player experience. When leveraged as a financial tool for facilitating open and transparent player-driven economies, blockchain provides superior global payment rails, increased transparency, trusted value distribution, and true player agency – facets many other MMORPGs often lack.

Over the past 24 months, a growing number of teams with rich MMORPG experience have started to venture into Web3. New entrants, such as Metacene and Avalon, join industry incumbents like MapleStory Universe (Nexon) and Project Awakening (CCP) to become pioneers in blockchain gaming. This level of commitment from experienced game developers not only supports the proposed value blockchain integrations bring but also forecasts an optimistic future for the sub-sector.

This is not to say there have not yet been any notable mentions. Big Time, for example, which started development in 2021 and was long considered one of the most highly anticipated Web3 MMORPGs, generated considerable buzz around its token launch in Q3 2023. By the end of Q1 2024, the game had grossed over $100M in in-game item sales, surpassed $230M in player-based transaction volume, and hit an all-time high (ATH) market cap of $300M.

However, a combination of unsustainable token player incentives, frequent clashes between the developer and core community, and a lack of gameplay depth at launch has led the token price and trading volume to fall 85% and 95% from ATHs, respectively. A similar story can be seen in MirM, Stella Fantasy, and Gran Saga: Unlimited, each of which shut down due to unsustainability concerns and broader market conditions.

This helps highlight just how difficult it is for an MMORPG to achieve long-term success. Importantly, adding blockchain elements only makes this more challenging as open economies make managing value extraction and economic balancing even more crucial for sustainability. A Web3 economy is unforgiving, and while enhanced community alignment can be a tremendous asset, it can quickly turn into an even bigger liability.

Building a Web3 MMORPG poses many challenges but equally offers opportunities to elevate the genre and produce the next genre-defining hit. The ability to foster a stronger sense of player ownership, better facilitate transparent value distribution, and align incentives between the developer and key stakeholders could become table stakes for the next generation of multiplayer interactive virtual worlds.

Although the lack of WoW competitors is no coincidence and implementing new tech doesn’t guarantee market share, past performance is not indicative of future success. We believe the teams with the best chance of success will be those who are deeply experienced in designing Web2 virtual economies and leverage blockchain to its full potential to produce net-new player experiences that last.

With all that said, the remainder of this report will highlight one such project. The following sections will dive deeper into MetaCene and the factors that make it an interesting case study for the potential future of blockchain-enabled MMORPGs.

Enter MetaCene

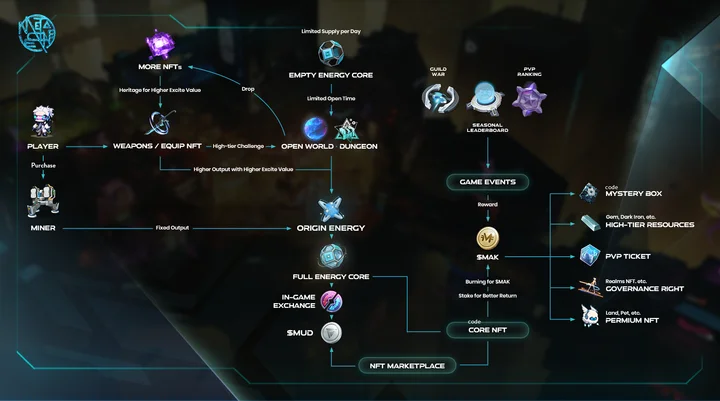

MetaCene is a Web3 MMORPG developed by industry veterans that is leveraging blockchain integrations to kickstart its growth flywheel and better align incentives between stakeholders. The game’s economy features a dual token system, which includes MUD, an uncapped supply utility token, and MAK, a capped supply governance and high-value exchange token. Additionally, many in-game items in MetaCene can be minted as NFTs and traded freely. Notably, there will also be a full Web2 experience available, and Web3 integrations will be opt-in only.

Three things stand out about MetaCene: the team behind the game, the Web3 systems and mechanics that influence the in-game economy, and the novel ServerFi system.

The Team

MetaCene’s co-founder and CEO, Alan Tan, helped shape the Chinese gaming industry during his tenure as co-founder and CTO at Shanda Interactive Entertainment and Chairman and CEO at Shanda Games. Shanda Interactive Entertainment was founded in 1999 and was one of China’s first internet gaming companies. In 2004, the company listed on the NASDAQ, raising $153M via the IPO. This was the largest IPO of a Chinese internet company in the US at the time.

Shanda got its upstart by purchasing the rights to the South Korean mega-hit The Legend of Mir 2 for the Chinese market in 2001. The company later went on to launch its first in-house developed MMORPG called World of Legend in 2003, which became a domestic breakout success that same year.

As Shanda Interactive grew its portfolio of published games, the company became a leading provider of internet cafes (becoming a games distribution leader in a nation with an estimated 2.5% household PC penetration rate). The company also innovated with early monetization models, pioneering the use of prepaid subscription cards (physical cards that dictate how long you can play a game) and later spearheading the shift to F2P in 2005 despite the pushback from shareholders (the company’s stock price by 70% after the announcement). That same year, Shanda Interactive Entertainment became the largest Chinese gaming company by market cap.

Alan became president of Shanda Group in 2008 and CEO in 2009, at which point Shanda Games accounted for almost 80% of the group’s earnings and was spun off into its own entity, IPO’ing in the US later that year and raising $1.04B (the largest US IPO of a Chinese firm that year).

Despite his past success, Alan is still passionate about making games and believes that blockchain will allow him to build the game of his dreams. To help him achieve this lofty goal, Alan has brought with him a number of his colleagues from Shanda, along with others from companies such as Snail Games, Blizzard, Perfect World, and more.

Web3 Gameplay Systems

MetaCene’s in-game economy features a number of interesting systems designed to drive value back to the most dedicated players and incentivize in-game spending. The crux of MetaCene’s long-term success will be rooted in a) how engaging these systems and mechanics are and b) how well they are balanced to maintain a healthy in-game economy.

Mining

The first standout gameplay system is the semi-idle earning mining mechanic. Early in the game, players are introduced to mining NFTs, which are used for mining ore within one of the many PvP areas.

In its original conception, ore could be synthesized into MUD. This significant token faucet acted as a great UA mechanism in the early alphas but would have eventually led to inflation. Taking Gaia Online as a case study, when the developers introduced “gold generators” in 2013 (an IAP that yielded a large amount of hard currency), it didn’t take long before the economy reached a point of hyperinflation. The value of gold, which was now a common resource, quickly plummeted, and items that used to be worth hundreds were priced in the billions!

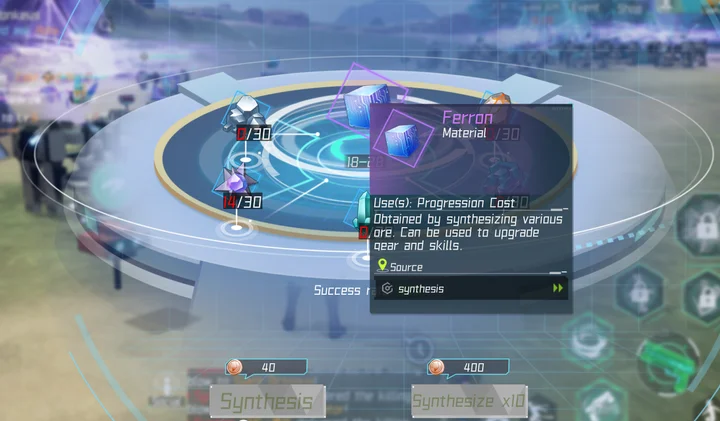

Having worked on many commonly exploited Chinese MMORPGs, the team understood the risks and removed MUD synthesis along with the release of the most recent open alpha. Currently, ore can either be traded on the marketplace for MUD or synthesized into Ferron and Origin Energy (two off-chain resources that are used for high-level equipment enhancements and generating MAK yield, respectively).

It should be further noted that this mechanic has a number of key economic levers associated with it that can be adjusted based on the game’s overall economic activity. These include ore drop rates, ore synthesis success rates, and miner durability levels. Additionally, repairing miners and boosting their efficiency with special items constitute key sinks that can be freely adjusted.

Finally, as the best mining sites are located in PvP areas, idle miners that have finished collecting ore can be hijacked by other players. This adds a level of risk management to the mining mechanic that can be leveraged in the future to add additional social mechanics and token sinks, such as guild protection, shields, or NPC bodyguards.

Despite the recent improvements, mining is still a supplementary activity that is only engaging for as long as the ROI is positive, making it a potential area for exploitation. In its current state, mining is more similar to a retention mechanism, such as a daily sign-in bonus or daily free gacha pulls. Although this has its use cases, adding more depth could better make mining a core part of the player-driven economy.

Bosses

Another key system that, during the first three alpha tests, was the primary source of player rewards was boss battles. Farming bosses is one of MetaCene’s core gameplay loops that provides players with key resources and powerful weapon and equipment NFTs (some rare items have already sold for thousands of dollars despite the relatively small player base).

Boss loot is rewarded to whoever lands the killing blow. This, combined with the fact that most bosses are located in PvP areas where Player Killing (PKing) is allowed, makes tackling bosses a high-risk, high-reward endeavor and a common area of contention amongst the current player base. This dynamic adds a key social layer, with many challenging bosses in teams, sometimes having four or more players dedicated to just defending against rival guilds or player killers (PKers). Social gameplay like this is incredibly important because it lays a foundation for a cosmetics and whale-driven economy.

However, it clearly favors the most powerful players, and when coupled with MetaCene’s in-game economy and monetization, it is objectively P2W. A major challenge with this system is to balance the contrasting wants of PvE players and PKers. Due to the importance of bosses for player progression, end-game content (like guild v. guild battles), and P2E, excluding various player cohorts because they cannot compete with the game’s most powerful players will cause large amounts of player discontent and churn.

In order to better appeal to the large population of free or low-spending players and new players, a roguelike dungeon and guild boss feature (which spawns bosses in non-PvP areas) were introduced. Although this has helped provide a relatively small flow of resources to lower-level players, it has not stopped powerful players and guilds from monopolizing certain bosses located in low-level zones.

In the future, MetaCene has said they will release a new feature called World Bosses that requires large numbers of players to pool resources and spend tokens to summon. However, as it stands, bosses represent the largest faucet of NFT items in the game, with many players claiming that the generous equipment drops have led to a dramatic fall in prices on the marketplace. Although this can be viewed as a good thing for new players who want a strong loadout for minimal expense, inflation this early in the game’s lifecycle should be carefully monitored. That said, a number of levers do exist to help the developers moderate the influence this loop has on the economy, such as adjusting boss loot drop rates and respawn times.

Reactor Core

A final mention should be made for the reactor core system that went live in the most recent open alpha. Reactor cores are IAP items sold in limited quantities every day on the in-game marketplace. Players acquire origin energy from boss battles, dungeons, and ore synthesis and use it to charge their reactor core.

Once fully charged, reactor cores can be used to either unlock exclusive gameplay or be minted into an NFT. If minted, reactor cores can then be traded, sealed (staked) for a fixed time before unlocking the token rewards inside, or burned immediately to unlock a reduced amount of token rewards.

Until more details about the exclusive gameplay features unlocked by reactor cores are unveiled, this loop is the game’s core P2E system, emitting more tokens than it consumes. As such, in its current form, it is best viewed as a business expense that is being leveraged to increase UA and user engagement during the early stages of the game’s global launch.

A key challenge with reactor cores is that they are currently the primary way for players to gain exposure to MetaCene’s MAK token. As MAK has yet to launch, the more reactor cores sold represent more future token-selling pressure at TGE. To mitigate this, reactor core tokens are subject to a short cliff.

The developers will need to closely monitor how players are interacting with this system and balance token emissions in response to changes in player numbers and monetization. With this in mind, the developers will likely continue to adjust incentives to influence how players interact with reactor cores (play, mint, stake, or burn). Aside from this, there are more than nine additional levers accessible by the developers that directly affect the extent to which reactor cores can impact the token economy.

ServerFi

This brings us to MetaCene’s ServerFi system, an economic meta layer that gives key stakeholders ownership in the game’s growth. Due to the fundamental nature of multiplayer online games, as the total number of players increases, so too does the number of networking servers.

At a high level, there are two core reasons why a game will expand its server architecture. The first is so that the game can facilitate a growing number of active players without causing long queue times, major latency concerns, or game-breaking bugs to occur. For a more detailed overview of how games scale and the different server networking techniques that are commonly used, you can reference our previous report on the topic here.

The second reason is well demonstrated by a selection of games, such as WoW, GTA5, and Star Wars Galaxies, that have developed such hardcore fan bases that a network of private servers is established. These player-owned servers can offer a more customized player experience and are often maintained outside the oversight of the original developers. In the case of Star Wars Galaxies, these player-owned servers persisted long after the original game shut down, effectively passing ownership over to the players.

In addition to prolonging the lifespan of a dying game, GTA5 illustrates how private servers can breathe new life into the player base and generate non-trivial amounts of new income for the publisher. Launched in 2013, GTA5 has cemented itself as the most profitable piece of media to have ever existed, and this is largely due to its transition into a live service title and the popularity of private role-playing (RP) servers.

Due to their popularity on distribution platforms like Twitch, private RP servers serve as a key on-ramp for new players and allow third-party creators, such as NoPixel, to build sustainable businesses. The importance of private servers has not gone unnoticed by GTA5 developer Rockstar Games, who acquired modding and private server tooling company CFX.re last year, leading us to believe this form of UGC will play a crucial role in the future of GTA6.

However, for centralized Web2 games, private player-owned servers will always remain in a state of limbo, with their long-term survival entirely dependent on the IP owner. It is entirely possible that Rockstar Games could one day decide to shut down all private servers. In every case where a publisher officially permits the existence of such servers, there have been many more examples of attempts to shut them down.

MetaCene’s ServerFi and Realms system is designed to utilize all the benefits private servers present while mitigating against centralization concerns. As the game’s player base grows and more servers are added, the most engaged players will have the ability to acquire Realm NFTs. Realms will represent fractionalized ownership over these servers, unlocking various tools and features to lower the technical barriers for UGC-inclined holders and offering governance, exclusive rights, and a share in the revenue generated from the corresponding server.

MetaCene will also allow a single entity (this could be a single whale or guild) to acquire the majority ownership of select servers. This will open up new possibilities for third parties to develop UGC within the MetaCene ecosystem and leverage the ServerFi blockchain rails to gate, monetize, and grow these player-owned worlds.

The ServerFi system can be viewed as an engagement mechanic that creates a positive feedback loop between in-player activity and shared upside in the game’s success. However, it is important that MetaCene introduces measures to mitigate against behaviors such as passive participation and excessive speculation. This is what ultimately led to the rise and fall of Land NFTs in circa 2021.

Additionally, in the absence of a reputation system that is tied to ownership, it is very easy for the capital-rich to effectively colonize worlds to the detriment of the player experience. Other challenges occur when player accounts and assets are allowed to travel freely between different server worlds. This can increase player interactions and trading velocity, but the unavoidable nuances in player behavior can produce arbitrage opportunities that can quickly destroy an in-game economy.

It should also be noted that although the ownership of Realms is verifiably decentralized, for as long as the underlying server architecture and IP are in the custody of a centralized entity, many of the previously mentioned risks inherent in Web2 games will remain. Additionally, gaming server architecture is notoriously complex and expensive to maintain. It requires constant adjustment between both bare metal and cloud-based servers. NFTs, on the other hand, are relatively rigid in their design. A sufficient number of levers will be required to account for bad actors, falling player numbers (no game is up only), passive speculators, and a host of other key considerations.

MetaCene’s Growth So Far

MetaCene has so far completed three private alpha tests and is currently in open alpha before having its global launch in September 2024. Allowing users to test the game early and often can be hugely beneficial in increasing the chances of a successful launch. Not only does it allow for bugs and exploits to be identified and dealt with early on, but it can also provide valuable insights into expected player behavior and benchmark key growth metrics.

In the interest of this report, Metacene has shared data with Delphi Creative from these early playtests so that we can ground the analysis and allow for some broad assumptions to be made on the game’s performance post-global launch.

The most recent playtest started on July 28th, successfully reactivating previous playtesters and onboarding new players with numerous incentives totaling the equivalent of $3M in prizes. It should be noted that the majority of these rewards are being distributed via two different leaderboard prize pools, each with a focus on increasing active engagement, retention, and playtime. After just under one month of the playtest going live, participants have completed 5.4M in-game missions, defeated 629k bosses, had 46,655 PvP battles, and created over 200 new guilds.

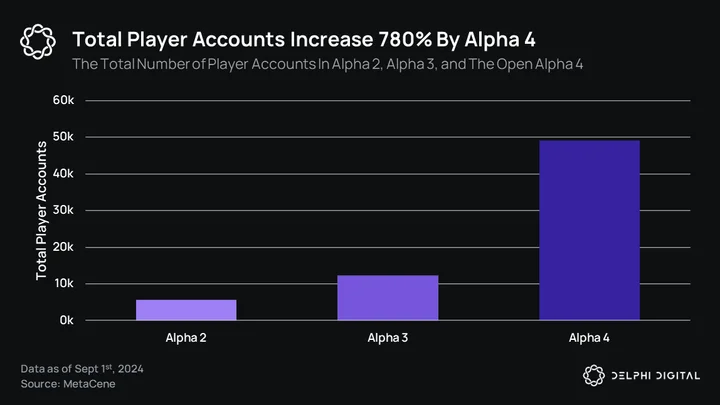

In terms of the total number of unique player accounts, MetaCenes reports an increase of almost 780% from Alpha 2 to the current open alpha, which sits at just under 50,000 accounts. This represents an average of 6.6k DAU, as tracked by MetaCene, and an average of 1.5k daily unique active wallets (DUAW), as reported by DappRadar.

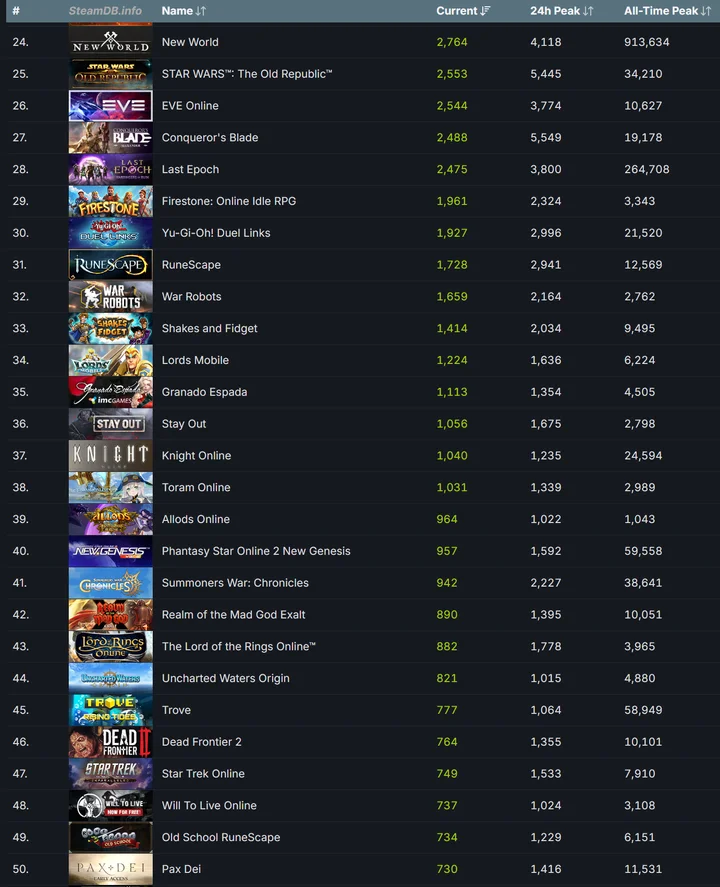

It should be noted that it is likely that neither metric completely omits bot accounts. That said, the lower end of this range still places MetaCene at roughly the 40th rank in terms of most played MMORPGs on Steam according to SteamDB (~20th if accounting for the higher end of the range in DAU). This does not account for the fact that MetaCene is still in early access.

For some perspective, out of the more than 64k games on Steam, only 930 (the top 1.5% of games) made over $1M in revenue, and only 157 made more than $10M. MetaCene’s current Steam ranking as an early access title is a testament to the power of blockchain incentives as a UA mechanism, and it will be interesting to see how this metric changes post-global launch when spending on traditional UA channels starts to scale.

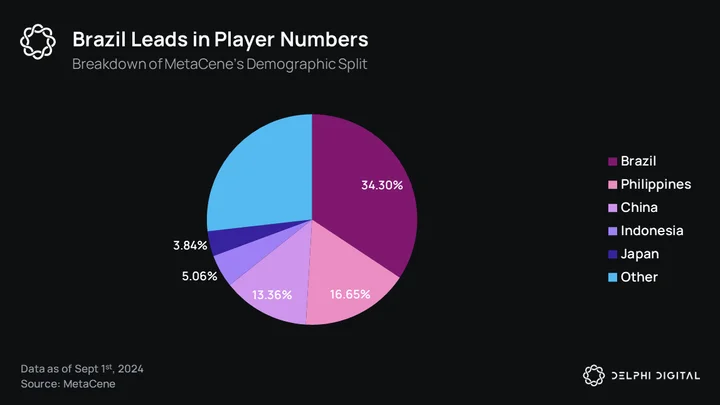

MetaCene’s early player base is currently divided into five core demographics: Brazil (34%), Philippines (17%), China (13%), Indonesia (5%), and Japan (4%), along with several other regions (namely South Korean, Vietnam, Singapore, and North America). Note that this split has remained relatively constant throughout all playtests.

Despite there being no data on paid UA, the consistent growth across all playtests suggests product-market fit in the outlined geographical regions. Although not a definitive indicator, this is typically one of a handful of metrics that suggest paid UA will effectively scale the player base in target regions. If the team wishes to scale in regions not outlined in the above chart, then more UA tests will be necessary.

Importantly, it is evident that the majority of MetaCene’s current player base is located in T3 developing markets. This is to be expected of almost all games that have a P2E element with little to no high-cost barriers to entry. Encouragingly, the presence of Chinese and Japanese users highlights an opportunity for deeper monetization, provided the team can effectively convert these players into spenders.

On the topic of monetization, MetaCene currently boasts a 24% conversion rate from F2P to paying players, which is meaningfully higher than the genre average of 5%-15%. This is an encouraging metric to see in an early-access F2P game and indicative of many Web3 games. Granted, during the early stages of the game’s release, when player incentives are still high and dependent on a minimal amount of spend, a high conversion rate is expected. A percentage of these paying users are only doing so in order to increase their earnings and maintain a positive ROI.

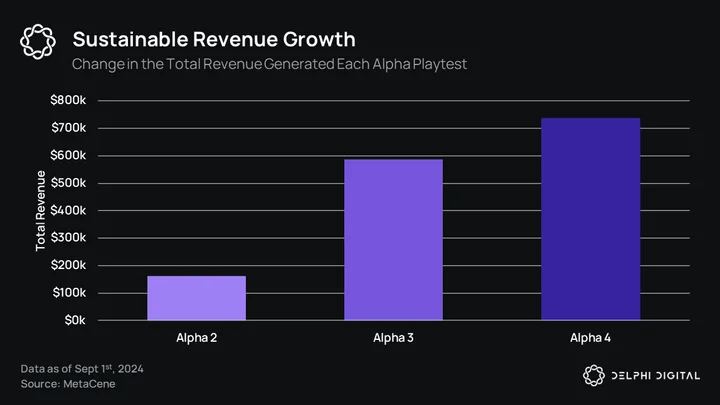

That said, MetaCene successfully scaled monetization to a monthly average revenue per user (ARPU) of $48 and a monthly average revenue per paying user (ARPPU) of $177 during alpha 3. These metrics have since normalized to $15 and $64, respectively, in the latest playtest but are still an estimated 3-5x higher than many of the leading Web2 incumbents. Stepping back, this equates to MetaCene generating a total of $737,295 in revenue within less than one month of the latest playtest going live, representing a 26% increase from alpha test 3 and a 356% increase from alpha test 2 – not accounting for any new monetization that has been added over time.

One of the largest areas of consumer spending is reactor cores, which, as previously stated, represent an inflationary token sink. However, based on anecdotal evidence from playtesters and the current price of MUD, we estimate no more than $100k in correlated token emissions pre-MAK TGE (note that this will change after MAK TGE, with current reactor core emission estimated at $230k). Under the assumption that the remaining 53% of revenue is a true sink (there may be some indirect inflationary pressure from power leveling) and discounting the numerous inflationary UA incentives currently live, MetaCene has verified its monetization model and come close to finding the equilibrium between inflationary incentives and deflationary player spending.

The true test will be in the team’s ability to grow its revenues relative to the inflationary incentives to a point where the 30% token buy-back mechanism (subject to change) will have a meaningful impact on MAK stakeholders.

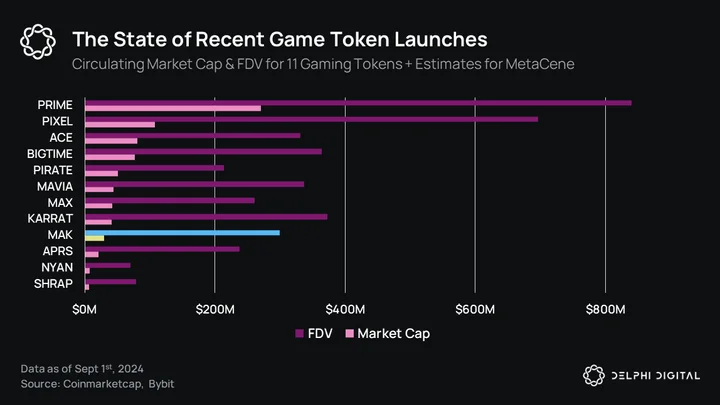

It should be noted that on August 23rd, MAK trading was enabled on the Bybit Pre-Market. The opening price (taken 30 minutes after the first sale) was $0.43, and at the time of writing, MAK is currently trading at $0.245. With a total supply of 1B tokens, this represents an FDV of $430M and $245M, respectively.

Based on current pre-market prices and roughly 10% of the total supply unlocked at TGE, we estimate that MAK will launch somewhere between a $20M and $40M market cap. For perspective, the market caps for the most notable recent gaming launches are displayed in the above graph.

Closing Comments

Metacene is anticipated to be one of the most promising Web3 MMORPGs to launch in 2024. Backed by an experienced team that has helped push MMORPG boundaries in one of the world’s largest gaming markets, there are few projects that are as well positioned to deliver engaging blockchain-based incentive and economic game designs. The growth in key performance metrics from playtest to playtest is encouraging, and the proven monetization strategy at this early stage is a great starting point for the team to further scale.

As with any Web3 game, the true challenge comes after TGE. If it is not already obvious, many of MetaCene’s current gameplay systems, such as mining, bosses, and reactor cores, are designed to incentivize UA, engagement, and retention. MetaCene is leveraging blockchain incentives to bootstrap the foundation for a F2P whale-based economy to be established.

As previously mentioned, it is well-studied throughout many Eastern MMOs that a vibrant virtual world with dynamic social systems and P2W monetization is often a prerequisite for this to occur. Where MetaCene differs is that they are also leveraging decentralized blockchain primitives to provide players with increased agency over their assets and co-ownership in both the virtual worlds they inhabit and the company’s future success. It is undeniable that many of these gameplay systems will place inflationary pressure on the in-game economy for as long as the game lacks a substantial whale base to either soak up token emissions or balance them out with increased spending.

Fortunately, unlike many other Web3 games, MetaCene is already live and in the hands of players around the world, providing the team with highly valuable in-game data, numerous economic levers, and a collection of token sinks live from day one. Our hope is that the team can apply what they learned from these early playtests and remain agile in adjusting the levers needed to balance an open gaming economy.

Regardless of how it performs post-TGE, MetaCene represents a great case study for game developers who wish to leverage blockchain technology in ways that meaningfully influence the player experience and better align incentives.

0 Comments