Bigger Than Binance: The $1.3B Bet on Crypto's Most Hated Business

JUL 10, 2025 • 30 Min Read

Report Summary

Summary

This detailed memo analyzes Pump.fun’s massive $1.3 billion raise, its bold goal to build a meme launchpad empire “bigger than Binance”, and how its real, durable revenue engine plus upcoming $PUMP token and buyback program might flip the “extractive” narrative that has made it crypto’s most hated yet widely used product.

Key Takeaways

1. Strong Revenue Base

-

Over $780 million in cumulative revenue since launch — real, not paper value.

-

Daily revenue still ~$1.3 million even after the January mania cooled.

-

Vertical integration (launchpad + PumpSwap AMM) lets Pump keep more fees in-house.

2. $1.3B Raise: Not Just Cash Grab

-

Funds will fuel both vertical integration (more trading features, maybe derivatives) and horizontal expansion (mainstream creator tools, livestreaming, mobile growth).

-

Potential M&A: buying Axiom to control token discovery front-end.

-

Possible CEX tie-ups or perpetual swaps to tap deep leverage markets.

3. Competitive Edge

-

Still the #1 launchpad by actual token creation and volume — despite Raydium’s LaunchLab briefly overtaking on single days.

-

Controls core trading flow: PumpSwap alone did ~$12.7B in 30-day AMM volume, catching up to Raydium’s $19.5B.

4. Token Model & Value Accrual

-

$PUMP will share protocol revenue with holders — projected 25% buyback mechanism.

-

Big airdrop (~10–12% of supply) planned for early users.

-

Valuation math: trades far cheaper on revenue multiples than peers like Jupiter and Raydium, despite superior margins and scale.

-

Peak cycle revenue could justify 2–3× upside if re-rated to peers.

5. Execution & Risk Factors

-

Market share competition is real — LaunchLab/letsbonk.fun and “aligned” alternatives are trying to chip away.

-

Revenue still cycles with memecoin market — from $134M in Jan to ~$39M in June.

-

Venture supply unlocks in future could weigh on price if not managed with smart buybacks.

-

Regulatory and legal headwinds: ongoing lawsuit about facilitating unregistered securities.

Conclusion

Pump.fun is crypto’s biggest paradox: the most hated app on Solana is also the one that prints the most real money — and now wants to share that yield with token holders. With a $1.3B war chest, proven PMF, and plans to push into mainstream creator culture and mobile-first onboarding, Pump is positioning to become the next Binance for degens — but with a memecoin twist.

If the team executes — delivering transparent buybacks, meaningful airdrops, and smart vertical + horizontal expansion — $PUMP could rally hard as the market re-rates a “hated but hyper-profitable” machine.

Biggest risk: they don’t expand fast enough to maintain dominance, or the tokenomics can’t keep up with unlocks and lawsuits.

Biggest opportunity: meme launchpads + trading as entertainment + real cash flow = the casino that always wins — and this time, maybe the users win too.-

Bigger Than Binance: How Pump.fun’s $1.3B Raise Sets Up Crypto’s Most Hated Rally

In my last memo, I broke down Pump.fun’s rise, their rollout to verticalize the stack with PumpSwap, how the launchpad landscape had evolved, and how I thought Pump was still best positioned to dominate the meme economy on Solana going forward, despite all the negative sentiment around them on crypto Twitter. I also outlined the path to a potential $PUMP token that delivers value from their new AMM – a large source of new revenue generation – back to holders, something most weren’t thinking about at the time.

With the announcement that Pump is now raising $1.3 billion at a $4 billion valuation, and planning to distribute protocol revenue to holders, there’s no better time to break down what we know about the details of the fundraise, how they could deploy this massive war chest, why they may be raising that much money, some potential risks, and of course, analyzing what $PUMP should be worth as it relates to comps, potential buybacks, and market sentiment.

The irony also couldn’t be richer. Crypto Twitter has long written Pump off as being extractive and yet, people have still used their platform religiously, without incentives. Now, Pump has the opportunity to flip the narrative that growth is slowing, using funds to propel their next phase of growth, and build something “bigger than Binance”. More importantly, they’re creating a token that is not only available to retail users in their ICO before it trades publicly, but also rewarding their early users with airdrops and a token that potentially accrues value from their lucrative business.

Pump knows they will have to introduce value accrual mechanisms for $PUMP if they want it to do well in today’s market, especially given how most crypto natives feel about them “extracting” money from the memecoin trenches. The stars could be aligned for $PUMP to perform post-TGE, but it’s up to them to execute and for the market to decide if its fundamentals and relative valuation are enough to fuel a vicious, hated rally.

The $1.3 Billion Raise: Numbers Don’t Lie

As mentioned, Pump is seeking to raise $1.3 billion through an ICO while planning to share protocol revenue with prospective token holders (whether this includes launchpad revenue, AMM revenue, or both remains unclear). You might assume that Pump seeking to raise $1.3 billion is their last move to “extract” while they can (avoiding OpenSea’s mistake of not tokenizing while pulling in ridiculous fees last cycle) or perhaps because growth is slowing as the launchpad market becomes saturated with “aligned” alternatives. Yet, the numbers tell a different story.

Since launching just over a year ago in February 2024, Pump has generated over 780 million in cumulative revenue. While fees peaked during January’s memecoin craze at over $134 million monthly, their June numbers were still extremely impressive at over $39 million. This means that between their two platforms, Pump is still generating approximately $1.3 million per day in revenue on average. However, daily revenue has trended lower in recent weeks due to increased competition, a dynamic I examined in depth in my previous report on Pump.fun and Raydium’s battle for Solana’s memecoin economy.

The competition stems from Pump’s strategic decision on March 12th to cut Raydium out of its trading flow entirely, directing all graduating tokens from its launchpad to PumpSwap, Pump’s own AMM, instead of Raydium.

This vertical integration move has paid off significantly. Since cutting Raydium out of graduated token trading, Pump has brought in an additional $108 million in total fees with PumpSwap, generating $20 million in protocol revenue since launch. June alone saw $30.5 million in total fees and $5.1 million in protocol revenue.

Note: Fees represent total collected from all sources, including LP fees (0.20%), protocol fees (0.05%) and creator fees (0.05%). Revenue represents what the protocol keeps: the 0.05% protocol fee from each trade.

This doesn’t account for creator revenue sharing, something most have failed to acknowledge when discussing Pump’s supposedly “extractive” narrative. Since revenue sharing launched in May, creators have earned over $8.1 million in cumulative fees from PumpSwap trading. Importantly, all this revenue generation has occurred while Bitcoin dominance climbed from ~58% at the start of 2025 to ~65% today, suggesting that Pump’s activity, while well off its peak, could surge again should memecoin markets heat up.

While Raydium has maintained its lead as Solana’s preeminent AMM by monthly volume, PumpSwap has effectively taken control of its graduated token trading, establishing Pump not only as crypto’s leading launchpad but also as core trading infrastructure on Solana.

PumpSwap processed $12.7 billion in AMM volume over the past 30 days compared to Raydium’s $19.5 billion, achieving 65% of the incumbent’s volume within months of launch. This represents a dramatic recapture of value that was previously flowing to Raydium, a far cry from when Raydium was passively collecting volume and fees from Pump’s ecosystem. The speed of PumpSwap’s rise demonstrates Pump’s execution capabilities and the power of owning more of the trading stack.

This success in vertical integration and sustained revenue generation, however, has also opened the door to competitive threats. While Pump has historically accounted for approximately 50% of all new fungible tokens created on Solana over the past year (even reaching over 70% at its peak), its current market share has dropped significantly to around 20% in recent days due to increased competition from Raydium’s LaunchLab, whose most popular instance letsbonk.fun, has seen explosive growth – a competitor that likely would not have emerged had Pump remained content feeding Raydium the flow for graduated token trading.

Raydium’s competitive response through LaunchLab is creating genuine disruption. On July 7th, LaunchLab processed 17,190 token launches compared to Pump’s 10,110, marking the first time any platform has surpassed Pump in daily token creation on Solana. LaunchLab also generated $143.88 million in volume versus Pump’s $32.83 million in bonding curve volume, a dramatic reversal from June 13th when Pump was processing $126.72 million daily compared to LaunchLab’s $9.11 million.

This surge has temporarily shifted the narrative from LaunchLab’s historical averages – about $8.5 million in daily volume and just 2,000 token launches per day – to breaking through $100+ million and 17,000+ launches for the first time since May. Yet this pattern mirrors May’s brief challenge that quickly faded, when LaunchLab competition first heated up and caused Pump’s token issuance dominance to fall from 60% to 30% before rebounding to over 50% within weeks. Notably, Pump’s “normal” June performance of 24,000+ daily launches and ~$120 million in daily bonding curve volume still exceeded LaunchLab’s current record numbers, suggesting the sustainability question remains whether this concentrated surge can maintain momentum.

Several factors suggest this challenge may be more temporary than transformational. The timing of LaunchLab’s resurgence, coinciding with anticipation around Pump’s $PUMP TGE, suggests strategic positioning by competitors looking to capture mindshare during a critical moment. More telling is that LaunchLab’s surge relies almost entirely on letsbonk.fun and the $BONK community (96% of launches, 99% of volume in recent record trading days), making Raydium’s challenge highly dependent on a single meme community rather than broad platform adoption.

Whether memecoins are this cycle’s NFTs and trading suddenly disappears overnight is one thing, although I find this unlikely. I would, however, argue that a successful company seeking to fundraise to grow their business should not be looked down upon and instead encouraged, especially in crypto where most projects raising massive rounds have historically had no realistic path to substantial revenue generation outside of dumping tokens on retail. They paint grand visions of how the infrastructure they’ll build will change the world despite their only users being airdrop farmers.

Pump, in many ways, represents the opposite: a proven business model with substantial revenue, real users, and demonstrated product-market fit, led by a team that’s already verticalizing their product to capture more revenue even during competitive pressure and weaker market conditions. With $780 million in proven revenue generation, Pump has earned the right to attempt to fundraise at scale. Unlike most crypto projects, they haven’t relied on token incentives or artificial flywheels to drive growth, their success stems from organic user demand and product-market fit.

The Pump team’s goal is incredibly ambitious—saying they want to create something “bigger than” Binance, bringing Pump to the masses. To do that, they’re gonna have to put that billion-plus to work, and in ways that may make us want to dream bigger…

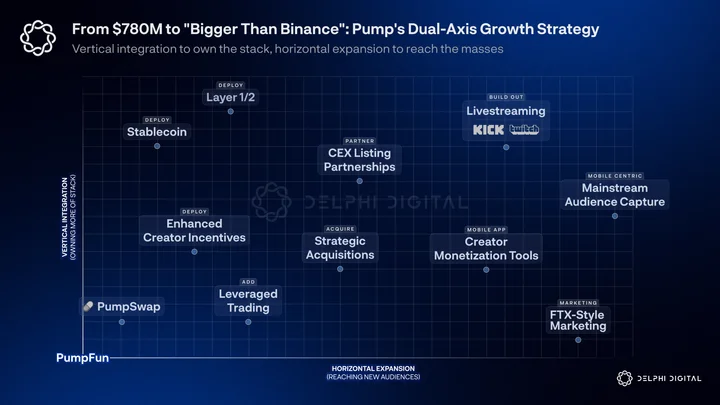

How to Spend $1.3 Billion: Vertical vs. Horizontal Expansion

Before you just write off Pump and their fundraise as an opportunistic cash grab, let’s break down how that capital could actually be deployed. After all, Pump has supposedly reinvested all of their revenue to date back into the business, and you can do a lot with a $1.3 billion dollar war chest, especially considering what they’ve already achieved with raising reportedly just a fraction of that amount initially.

Prior to this announcement, Pump was already beginning to scale vertically with PumpSwap – something we’ve already seen help them maintain strong earnings even during cooler market conditions. While additional capital could help them scale further vertically, I think it’s also important, and probably overlooked, to consider just how far they could take vertical integration, and what they might accomplish from a horizontal scaling perspective.

Vertical Integration: Owning the Stack

Pump has already proven the power of vertical integration with PumpSwap, effectively doubling their potential revenue streams by controlling both token creation and trading. With $1 billion in fresh capital, they could accelerate this strategy dramatically:

- Strategic Acquisitions: Pump could target trading-adjacent protocols to fill gaps in their infrastructure. One possible target could be Axiom, which would help them own more of the front-end experience, addressing a key risk in their current business model where they don’t control token discovery and user acquisition. Axiom has already generated over $160 million in fees since its early access launch in February, putting it on pace for similar annualized revenue to Pump (~$380 million vs. Pump’s ~$780 million). This makes Axiom both an attractive acquisition target and a potential competitive threat if left independent.

- Exchange Feature Expansion: Adding perpetuals, options, and advanced trading tools to compete directly with centralized exchanges. Pump realizes they already dominate memecoin trading, but centralized exchanges remain crypto’s most lucrative businesses. With perpetual swaps potentially becoming legalized in the US, now could be the perfect time for Pump to go all-in on capturing the leverage side of degenerate crypto trading flows cementing their offering as the best of both on-chain degeneracy and the growing derivatives market.

- Infrastructure Development: While Pump could build their own stablecoin or Layer 1/2 to capture more transaction fees and improve profit margins, this seems less compelling strategically. It would be capital-intensive without exponentially growing their existing business, and they’d lose much of the distribution and liquidity advantages they currently enjoy on Solana, potentially moving them further from users rather than closer. However, building out more core infrastructure like they’ve already done with their internal AMM could be worth watching, especially if Pump executes this creatively in ways we might not anticipate today.

- Exchange Partnerships: If Pump doesn’t launch their own centralized exchange, partnering with existing exchanges could make sense strategically. They could create direct listing pipelines for graduated tokens, bringing them to CEX audiences who may be less likely to come onchain to trade. More intriguingly, they could also work towards developing a Binance Launchpool competitor or similar mechanism that rewards $PUMP holders with early access to newly bonded or listed tokens – creating a potentially powerful flywheel where projects launching on Pump get streamlined CEX listings while incentivizing people to hold $PUMP for future allocations.

Horizontal Expansion: Beyond the Crypto Native Audience

While vertical integration captures more value per user, horizontal expansion is where Pump could truly surprise markets and justify their “bigger than Binance” ambitions. The real growth opportunity lies not in converting more crypto traders, though there’s room there too, but in making token creation and trading accessible to creators, streamers, and mainstream audiences who currently view crypto as too complex or risky. With $1 billion in capital, they could execute on several fronts simultaneously:

- FTX-Style Marketing Campaigns: Pump could massively increase their marketing spending with sponsorship deals and partnerships to bring crypto trading into mainstream consciousness. Think back to how FTX executed this playbook by using portions of their $2 billion in collective fundraises for celebrity endorsements, naming rights deals, sports league sponsorships, and Super Bowl ads. This didn’t just drive user growth, it built their brand as “the most regulated crypto exchange” (obviously they didn’t deliver, but crypto became synonymous with FTX and vice versa). Pump could deploy similar capital to make memecoin trading and crypto speculation a household concept rather than a crypto-native activity.

- Livestreaming Platform Development: Pump has already leaned into livestreaming to make their user experience more engaging and will likely view this as a permanent horizontal scaling opportunity. With a large war chest, they could build out a rival platform to Kick or Stake; but instead of promoting sports betting or gambling, top streamer partnerships with creators like Kai Cenat or IShowSpeed, for example, could revolve around Pump.fun in various ways: live token launches, real-time trading, community challenges, or entirely new formats we haven’t seen yet. This could transform token creation into entertainment while onboarding new audiences who follow these creators but have never touched crypto before. The possibilities for turning memecoin culture into interactive content are vast and largely unexplored.

- Mobile-First Strategy: To the surprise of most, Pump has already rolled out a mobile app in February of this year and has over 100,000 downloads on the Android app store alone. With additional capital, they could significantly expand development here and lean into mobile-centric user acquisition, targeting mobile-native users who may be more inclined to dabble in crypto through their phones rather than desktop trading platforms or even the Telegram-based experiences that are quite popular among crypto natives today.

- Creator Economy Expansion: Building on their existing creator revenue sharing model with enhanced incentives for community building, custom launch experiences, and tools that help creators monetize their audiences through token launches. This could transform creators from occasional participants into dedicated Pump evangelists with real economic incentives.

The beauty of these horizontal programs is that Pump has the optionality to experiment across multiple initiatives simultaneously, with additional capital ready to deploy heavily into whichever programs show the strongest early traction and user growth metrics.

The potential for both horizontal growth (reaching new audiences) and continued vertical integration (owning more of the value chain) creates multiple paths to justify their ambitious valuation and growth targets. Pump’s approach, having already introduced livestreaming, likely recognizes that their next phase of growth won’t come primarily from converting more crypto-native flow (although there’s room for growth there too, especially if they build out their own centralized exchange). Instead, it’ll come from making token creation and trading accessible to creators, streamers, and mainstream audiences who currently view crypto as too complex or risky with misaligned incentives.

the moment you’ve all been waiting for$PUMP is launching through an Initial Coin Offering on Saturday, July 12th.

airdrop coming soon.

our plan is to Kill Facebook, TikTok, and Twitch. On Solana.

learn more about $PUMP and how to get involved 👇 pic.twitter.com/KApiGnvtBg

— pump.fun (@pumpdotfun) July 9, 2025

By turning memecoins into a form of social entertainment where creators are incentivized to engage their community and earning a shared portion of trading fees rather than just speculative trading, Pump could tap into markets exponentially larger than their current crypto-native user base. They’re essentially positioning to capture a slice of the online gambling and sports betting boom, sectors projected to reach market values of over $150 billion and $180 billion respectively by 2030, both growing at around 11% CAGR.

The key insight: if Pump can make token trading feel more like entertainment than fringe financial speculation on a corner of the internet, they may be able to unlock audiences who would never touch a traditional crypto exchange or wallet.

Respect the $PUMP: When $780M Revenue Meets Peak Hatred

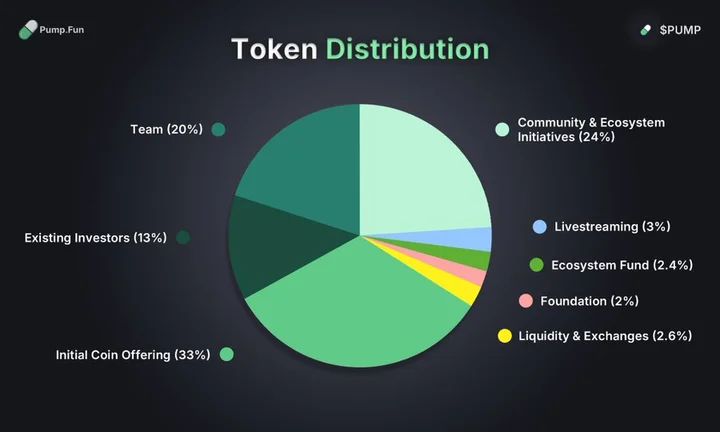

As mentioned, the Pump team knows their token must deliver real value back to holders to succeed, especially given the widespread “extractive” narrative surrounding them. Early reports suggest that they are planning to do a 25% revenue share mechanism (likely through $PUMP buybacks), decent, but nowhere near Hyperliquid’s aggressive 97% fee redistribution. As this cycle’s two largest fee generators, investors will inevitably compare the two, making $PUMP the most anticipated TGE since $HYPE. To improve sentiment, Pump is also reportedly airdropping ~10% of supply to early users, though the exact figure is not known.

Again, this $1.3 billion raise comes at a time when Pump is universally hated – despised by ETH maxis, viewed as parasitic by Solana natives, and dismissed entirely by crypto Twitter. Yet, beneath all this negativity still sits one of crypto’s most profitable businesses, generating $780 million in revenue in just over a year since launching.

In my view, the massive delta between sentiment and fundamentals, plus the growth potential from their expansion plans, creates the perfect setup for a “hated rally.” If Pump executes with a meaningful airdrop and genuine revenue sharing, they could flip the narrative overnight. The same voices who have called them extractive might suddenly realize they’ve been rewarded handsomely for their past usage while now owning a piece of the business’ future revenue, albeit indirectly.

Let’s now examine how Pump may be valued against other dominant fee-generating businesses and map out scenarios for expected token value accrual.

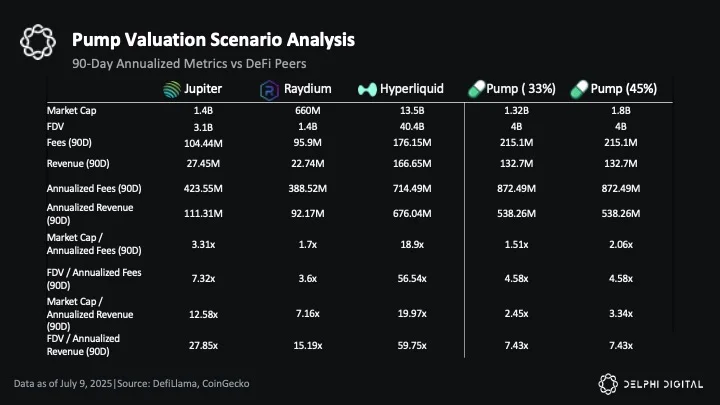

Conservative Baseline: 90-Day Valuation Multiples

When comparing Pump against DeFi blue chips using 90-day annualized figures from April through June, the numbers reveal Pump’s strong revenue generation capabilities. At $538.3 million in annualized revenue, Pump ranks as the second-highest earner, trailing only Hyperliquid’s $676.04 million but significantly outpacing Jupiter ($111.31 million) and Raydium ($92.17 million).

What makes these figures particularly noteworthy is the margin profile comparison. While Jupiter is on pace to generate $423.55 million in total fees, only $111.31 million (~25%) flows to the protocol as actual revenue, the remainder goes to liquidity providers. Similarly, Raydium would capture just $92.17 million in protocol revenue from the $388.52 million in total fees they are projected to earn. Pump’s $538.3 million represents a much higher percentage of its potential $872.49 million in total fees, creating superior unit economics where revenue growth translates more directly to protocol value rather than being diluted by external participant payments.

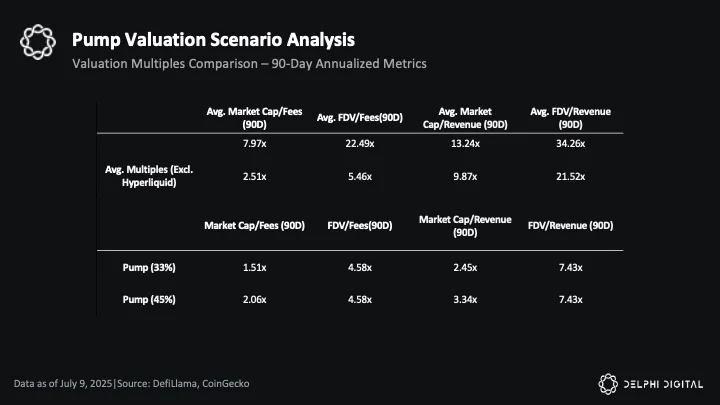

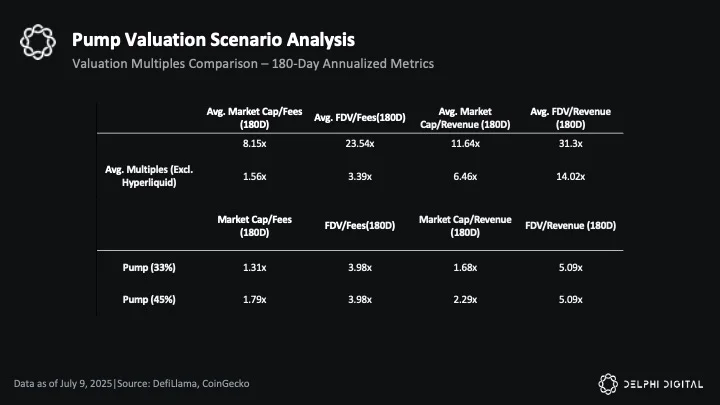

When examining Pump at its $4 billion FDV with realistic circulating supply assumptions, the valuation discount is clear. Assuming 33% circulating supply, Pump would trade at just 2.45x market cap/revenue—a dramatic discount to the peer average of 13.24x, or 9.87x excluding Hyperliquid’s outlier valuation metrics.

To put this discount in perspective: if Pump were valued like its peers at the average FDV/revenue multiple of 34.26, its $538.3 million annualized revenue would justify a $18.44 billion valuation. Even using the more conservative 21.52x average (excluding Hyperliquid), Pump would still be worth approximately $11.58 billion, representing a 190% premium to the current $4 billion ICO price. The market cap comparison shows similar undervaluation, with Pump trading at roughly one-quarter the multiple that markets assign to lower-revenue DeFi protocols.

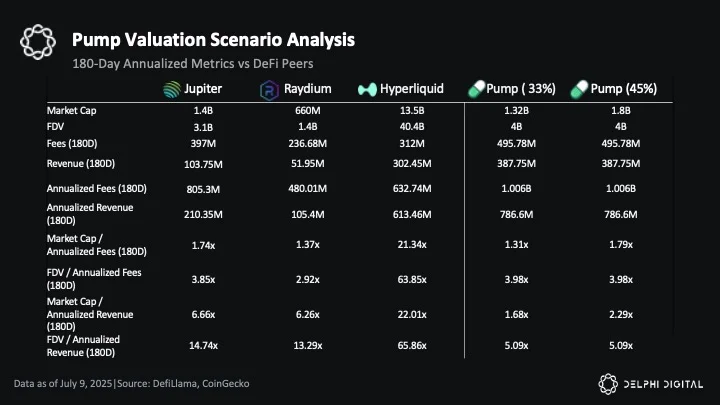

180-Day Performance: Peak Revenue Capability

It’s also worth noting that these 90-day numbers come during a stretch where Pump’s volumes don’t account for any of the January memecoin mania when they pulled in over $134 million in monthly revenue. Using this more conservative baseline actually makes the $4 billion valuation look even more attractive relative to peers. Running the numbers again using trailing 180-day revenue annualized (covering the past 6 months not including the start of July, which captures some of that January froth and assumes better market conditions), we can see just how powerful Pump can be from a revenue generation perspective during frothier market conditions.

Looking at the 180-day annualized numbers, Pump’s revenue generation outpaces even Hyperliquid, with over $786.6 million in annualized revenue compared to Hyperliquid’s $613.5 million. Using these numbers, Pump would trade at just 5.09x FDV/revenue, a significant discount to its own 7.43x FDV/revenue multiple from the trailing 90-day period. This demonstrates how much more attractive the valuation becomes when accounting for Pump’s peak performance capabilities.

While Pump is not currently earning nearly as much as it was during peak memecoin mania, the 180-day numbers represent what could be attainable again with proper deployment of their $1.3 billion war chest and a return to favorable market conditions. The valuation discount becomes even more pronounced using these metrics.

Compared to average multiples, Pump’s 5.09x FDV/revenue would be 64% cheaper than the peer average (excluding Hyperliquid) of 14.02x. If priced like peers, Pump’s FDV would be approximately $786.6 million in 180-day annualized revenue would justify an FDV or approximately $11 billion, representing a significant discount at the current $4 billion ICO price.

However, this discount is most apparent when examining circulating market cap, which represents the true tradable float. Assuming 33% circulating supply, Pump would trade at just 1.68x market cap/revenue, far below the peer average of 6.46x, excluding Hyperliquid. If trading at a similar market cap/revenue multiple, it would justify approximately $5.1 billion in market cap, or a $15 billion+ FDV.

Interestingly, from a fees perspective, Pump trades roughly in line with peers: 1.31x market cap/fees versus the average (excluding Hyperliquid) of 1.56x, and 3.98x FDV/fees versus the 3.39x average. This suggests the $4 billion valuation may be correctly pricing Pump’s fee generation capability, but overlooking its superior take rate and higher-margin business model on a revenue basis compared to peers.

Token Value Accrual: Buyback Mechanics and Earnings Multiples

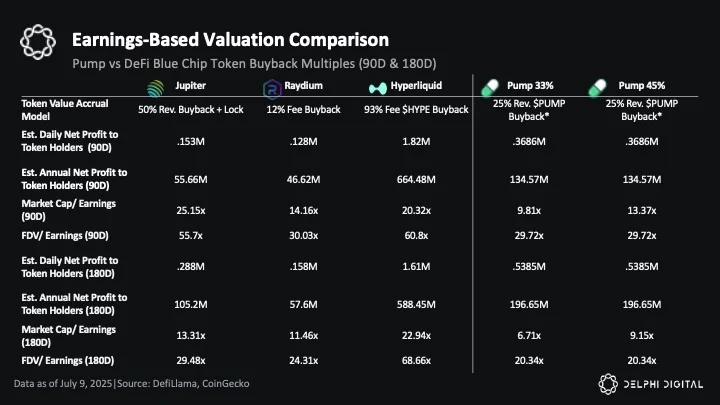

While analyzing annualized fee and revenue multiples is helpful, what really matters for token investors going forward is how much value ultimately accrues to protocol tokens. Jupiter, Raydium, and Hyperliquid all tie value back to their tokens, albeit at different ratios. Jupiter uses 50% of its revenue for buying back and locking $JUP, Raydium uses 12% of fees (not revenue) to buy back $RAY, while Hyperliquid uses 93% of fees to buy back $HYPE.

Using trailing 90-day numbers, $HYPE holders receive an estimated $1.82 million in daily buying pressure from Hyperliquid’s assistance fund, or $664.5 million annually. Jupiter contributes $0.153 million daily ($55.7 million annually) while Raydium provides $0.128 million daily ($46.6 million annually).

Assuming Pump commits to using 25% of their current revenue from both launchpad and AMM operations, token holders would receive $0.369 million in daily $PUMP buying pressure, or $134.6 million annually. This is meaningfully more than Jupiter and Raydium’s estimated net profit to token holders, but still well below Hyperliquid’s.

While Hyperliquid’s high buyback percentage explains part of its premium valuation, another factor is business consistency. Hyperliquid’s revenue has been resilient, with 180-day numbers actually slightly lower than 90-day ones ($588.5 million vs $664.5 million annual net profit to holders), demonstrating stable fundamentals.

In contrast, using 180-day estimates, Pump, Raydium, and Jupiter would have much higher annualized and daily net profits flowing to token holders, directly correlated to their higher revenue during peak periods. This creates more reflexive buyback dynamics; when business conditions improve, token holder returns increase dramatically, but the inverse is also true during market downturns.

But there’s more at play when evaluating potential valuation frameworks and explaining the stark multiple differences across protocols, especially with Hyperliquid. Where Hyperliquid trades at 68.66x FDV/earnings versus Jupiter’s 29.48x or Raydium’s 24.31x has other explanations beyond pure earnings distribution.

Hyperliquid lacks venture investors entirely. While it trades at $13.5 billion circulating versus $40.5 billion fully diluted, investors are comfortable knowing the team’s 23.8% allocation is locked and the 38.9% reserved for future emissions has no venture investors waiting to dump supply. Their user-friendly tokenomics (including allocating 31% of initial supply to early users) has built significant community goodwill, contributing to their valuation premium.

In contrast, Pump will have venture investors who, while vested at launch, will presumably look to realize gains as their supply unlocks. Additionally, Pump faces the opposite goodwill factor that benefits Hyperliquid: widespread negative sentiment and the “extractive” narrative that could weigh on valuations regardless of fundamentals. Both Raydium and Jupiter still have over half their total supplies waiting to unlock, creating ongoing sell pressure and market uncertainty. Jupiter’s premium to Raydium partly reflects recent strategic moves: they burned over 3 billion $JUP in November (30% of total supply) while rolling out their 50% revenue buybacks and an acquisition spree, including Moonshot, signaling future growth potential.

Raydium, meanwhile, was dealt a significant blow when Pump launched PumpSwap, cutting off a core volume driver in graduated token trading. While Raydium has attempted to compete by launching LaunchLab as a direct challenger to Pump’s launchpad business, with instances like letsbonk.fun generating temporary volume spikes, these efforts have failed to meaningfully dent Pump’s dominance until more recently.

Still, on an FDV/earnings basis at $4 billion, Pump is priced at 29.72x (90-day), a multiple that is nearly identical to Raydium’s 30.03x, which could be mispriced given Pump’s superior positioning throughout the past year. Pump will also operate with much greater strength and optionality, especially with a fresh $1.3 billion-dollar war chest and proven ability to adapt offerings strategically.

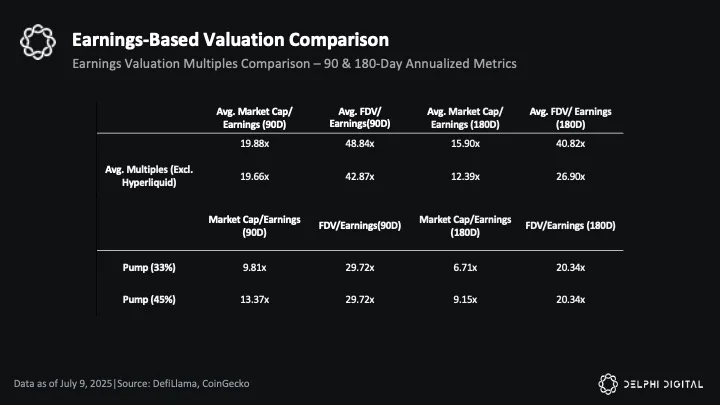

The math on a market cap basis is even more compelling. Currently, based on its 90-day annualized earnings of $134.6 million, we can analyze two float scenarios. The first is a 33% float from the ICO ($1.32B market cap), giving it a 9.81x market cap/earnings multiple. The second is a 45% float ($1.8B market cap), assuming the initial 33% is joined by a 12% airdrop (half of the community allocation); this scenario results in a 13.37x multiple.

A simple rerating to the peer average of 19.66x (90-day, excluding Hyperliquid) would justify an approximate $2.65 billion market cap. This implies an FDV of $8.03 billion (a 101% upside) at the 33% float, or an FDV of $5.89 billion (a 47% upside) at the 45% float.

Even a more conservative move to match Raydium’s 14.16x multiple would generate an approximate $1.91 billion market cap. This would, in turn, imply an FDV of $5.79 billion representing 45% upside with the smaller float, or an FDV of $4.24 billion representing 6% upside with the larger one.

This also assumes only multiple expansion to current peer levels, without factoring in potential revenue growth from their two billion-dollar deployment or the superior unit economics Pump has already demonstrated. The setup suggests meaningful upside potential purely from valuation normalization, before considering the operational improvements that fresh capital could enable.

Once vesting and airdrop schedules are more clearly defined, the market will better assess how future supply affects Pump’s float and potential rerating. Our analysis modeled a sizable 12% airdrop, but the team could opt for a smaller initial distribution. A more conservative airdrop would result in an even lower initial float than the 45% modeled, further amplifying supply constraints.

If investor unlocks also don’t begin for 12 months post-ICO, the combination of large daily buying pressure, a genuinely scarce initial float, and a potential sentiment reversal (driven by an airdrop and users finally being able to share in Pump’s profitability) could create the ideal conditions for significant multiple expansion and price discovery, at least in the short run.

Challenges Ahead: Assessing Pump’s Key Risk Factors

Having outlined potential deployment strategies for Pump’s billion-dollar war chest and established valuation frameworks suggesting $PUMP could be worth significantly more than its $4 billion ICO price, it’s important to assess the key risks that could prevent this rerating from occurring. While my thesis centers on near-term launch dynamics and supply-demand imbalances, particularly around sentiment reversal potential, several structural challenges could undermine the investment case.

Launchpad Wars: Can Pump Maintain Dominance Against “Aligned” Alternatives?

The most obvious challenge ahead, and the one on everyone’s mind in crypto, is whether Pump will be able to retain control of the launchpad market amid increasing competition, especially from those presenting themselves as more “aligned.” These competitors, namely LaunchLab and the letsbonk.fun instance, have used fees to buyback and burn their native tokens ($RAY and $BONK) while leveraging the Solana-native and cult-like community of BONK, a token born from Solana’s ashes during its airdrop post-FTX collapse. Meanwhile, Pump has been labeled as parasitic to Solana, with critics arguing they extract value from the ecosystem through their large Solana deposits to Kraken (presumably to be market sold for USDC).

Yet, as outlined, Pump will be using protocol revenue to buyback $PUMP, creating a flywheel where more trading directly benefits holders. Additionally, an airdrop to early users, especially one as large as Pump’s tokenomics allow (we estimated 12%, which would exceed $480 million assuming Pump remains at a $4 billion FDV), would be enormous. This doesn’t account for the incentive programs Pump could run to encourage and reward platform usage with their expanded war chest.

That said, Pump appears to be targeting an inherently different market than its competitors. While Raydium’s LaunchLab and its popular letsbonk.fun instance feel more niche and crypto-native (clearly emphasizing driving volume and attempting to steal mindshare ahead of the $PUMP TGE), it has still struggled to meaningfully challenge Pump for sustained periods. Jupiter’s JUP Studio and Moonshot’s “Create” feature have also failed to meaningfully dent Pump’s dominance or even scale to the volumes that LaunchLab has achieved, albeit briefly. While Believe stands out by targeting early-stage web2 companies fundraising onchain as part of the internet capital markets narrative, focused on web2 business fundraising rather than pure-meme speculation, volumes are nowhere close to what meme trading generates and represents a fundamentally different market segment than what Pump has dominated.

Time will tell whether all of these launchpads can coexist, but based on Pump’s scaling plans and fresh $1.3 billion in capital, Pump should be able to not only reclaim dominance in current memecoin markets but also expand into future ones where they’re attempting to grow the pie. Ultimately, onchain degenerates and serial token deployers will go where the most volume and incentives are, and Pump will undoubtedly be that place in the coming quarters if the team continues to execute and deploy their fundraise effectively.

Fundraise Execution and Historical Precedent

The next most immediate risk, albeit unlikely, would be Pump’s inability to fill the entire $1.3 billion raise, split between an ~$710 million private sale and ~$590 million public offering, which would signal weak institutional confidence despite seemingly strong fundamentals and could spook potential investors. The pace of the public sale will be telling, a quick fill would suggest strong underlying demand and positive launch dynamics, while a slow or incomplete public sale would raise concerns about whether they’ve exhausted their marginal buyer base. Beyond the funding implications, failure to complete the raise may also indicate that market sentiment around Pump is too entrenched to flip; that the community’s hatred runs too deep to allow for fundamental reevaluation, regardless of the underlying business metrics. While a generous airdrop and committed buyback program could help shift this dynamic as mentioned earlier, the sentiment risk remains significant.

Historically, massive crypto raises have also not resulted in strong long-term outcomes, falling into two distinct categories. The first includes projects with legitimate, revenue-generating businesses that were highly cyclical, companies that had real operations and strong fundamentals during favorable conditions. However, most were riding unsustainable trends where additional capital for horizontal scaling or user acquisition couldn’t solve the underlying cyclical nature of their businesses. The second category encompasses hyped infrastructure projects that raised massive amounts on grand visions but lacked realistic paths to sustainable profitability, burning through capital while chasing theoretical use cases.

Pump sits closer to the first category: they have a real, profitable business, but one that’s inherently tied to market cycles. While they’ve shown surprising resilience despite the weaker altcoin market since January, growth has still stalled. Even with the additional revenue capture from PumpSwap, Pump’s June revenue of $39 million was down ~70% from its January peak of $134 million, demonstrating that their revenue remains closely tied to memecoin market cycles and overall crypto sentiment, even as they maintain category leadership.

Execution Risk on Ambitious Scaling Plans

Beyond market dependency, there’s significant execution risk. The $1.3 billion war chest provides assurance they can survive an extended market downturn, but successfully rolling out the previously mentioned vertical and horizontal scaling initiatives is far from guaranteed. Building sticky, long-term revenue growth and user acquisition, especially targeting mainstream audiences, presents fundamentally different challenges than the viral 0-to-$780 million revenue growth they’ve achieved over the past year, let alone retaining their current revenue metrics which, as mentioned, remain closely tied to memecoin market cycles and broader crypto sentiment.

Supply Dynamics and Long-Term Token Pressure

From a token perspective, Pump faces venture and early investor unlock schedules that projects like Hyperliquid avoid, giving them less flexibility around buyback generosity and long-term supply control. While the low float and potentially high revenue allocation to $PUMP buybacks could initially help with price discovery and early success, the longer-term outlook is more uncertain. With both a growing circulating supply and potentially slowing revenue, the dynamics could become reflexively negative.

Regulatory and Legal Headwinds

Finally, while the regulatory landscape under the current administration has been more crypto-friendly, Pump’s casino-esque mechanics make them a natural target for regulatory scrutiny. The platform already faces a proposed class action lawsuit alleging they generated substantial profits helping users create tokens that constitute unregistered securities, violating federal securities laws. Getting tied up in lawsuits and facing regulatory scrutiny (especially as they seek to bring Pump to the masses outside the crypto-native bubble) would create massive headwinds with a public audience that remains skeptical about crypto adoption following FTX’s collapse.

The Contrarian Setup: Maximum Pessimism Meets Proven Profitability

The consensus view is clear: everyone hates Pump, assumes this fundraise is their last chance to “extract” before the business deteriorates, and believes their best days are behind them. Yet, as we broke down, the numbers tell a fundamentally different story.

Contrary to the narrative of extraction and decline, Pump has demonstrated remarkable resilience and strategic foresight. While revenue declined from January’s $134 million peak to June’s $39 million, they simultaneously launched PumpSwap to capture previously lost value, generating an additional $20 million in protocol revenue in just months. This vertical integration during a market downturn shows a team executing strategically rather than simply riding momentum.

Our valuation analysis also supports this contrarian view. At $4 billion FDV, $PUMP trades at a steep discount to comparable protocols, creating what appears to be a significant mispricing. With immediate token unlocks for ICO participants while a large portion of supply remains locked due to investor vesting schedules, potentially substantial buyback pressure, and a massive disconnect between fundamentals and sentiment, the setup for potential re-rating and initial price discovery is compelling. Importantly, at the $4 billion ICO price, no participants will have meaningful paper gains looking to dump, creating cleaner price discovery dynamics in the early trading window.

Most crypto natives debated whether Circle was even worth $5B before its IPO. Today it trades at $45B+ as the de facto public market play on stablecoins. Pump could follow a similar path, not through an IPO, but as the crypto-native way for funds to get meme economy exposure without picking individual tokens or sitting on DEXScreener all day. Sometimes owning the casino beats trying to beat it.

That said, the risks and challenges ahead are substantial. Retaining business strength in a potentially prolonged weak market while simultaneously expanding beyond crypto natives to mainstream audiences presents execution challenges that could derail the growth story. Regulatory scrutiny and competitive pressures add additional uncertainty, as do longer-term supply dynamics and limited flexibility around buyback commitments given they have previous investors and aren’t bootstrapped like Hyperliquid.

However, Pump has, in my view, earned the right to attempt their ambitious transformation. With $780 million in proven revenue generation, a potentially $2 billion post-raise war chest, and a track record of successful execution under pressure from competent competitors, they’ve positioned themselves to capitalize on what could be their next phase of growth.

For investors willing to bet against consensus, the combination of strong fundamentals, attractive valuation, and maximum pessimism creates what may be one of the cycle’s most compelling contrarian TGEs.

0 Comments