DeFi Summer

Four years ago, DeFi “Blue-Chips” such as lending protocol AAVE and derivatives protocol Synthetix put in their all-time lows, marking the beginning of a reversal that would propel not only themselves, but an entire category of applications called “decentralized finance”.

For those of us who remember when AAVE was “ETHLend”, the notion of “DeFi” did not yet exist, and the idea of depositing your coins into another protocol seemed extremely dangerous. Spoiler alert: it was. But, in the midst of hacks, rug pulls and smart contract exploits…a category of reputable DeFi protocols emerged, noted “blue chips”.

DeFi Blue-Chips are a label only assigned to the most secure of protocols, reserved for benchmarks that newer era protocols strive towards. But, this does raise the question: How exactly does a new protocol achieve blue chip status?

It’s a tough question, but not one impossible to answer (or at least try to). There are many different ways to do this, and there is no one “correct” model to follow, but for simplicity’s sake I’m going to just use TVL as the sole metric to evaluate a protocol. TVL is one of the most straightforward metrics to use to judge the adoption of a protocol, and while no one metric should be thought of as *the metric*, TVL holds its weight pretty well on its own.

For this experiment, let’s set some ground rules. Remember, we’re trying to find the “next” DeFi blue chips, so it’s important that we knock out existing ones. Our first rule: The protocol must have been deployed in the past 2 years, or since June of 2021.

Next, we want to see some level of adoption. This generally just boils down to the TVL being above a certain number and actually increasing by a meaningful metric over a defined period. Let’s say TVL has to be above $50M and has to have increased by a minimum of 25% since the beginning of this year?

Now these two combined are probably somewhat of a good barometer for protocols worth researching, but I want to take it a step further. To ensure that these protocols are setting themselves up for success by deploying in an ecosystem that is growing, the TVL of the chain the protocol is deployed on will have to have increased by at least 50% since the beginning of the year. Also, to make sure that we’re only focusing on chains with meaningful activity, we’ll set a minimum of 500M TVL for the chain to qualify.

Thus, our metrics are:

– TVL of chain deployed on has minimum $500M TVL and increased at least 50% in 2023

– TVL of protocol is at least $50M TVL and increased at least 25% in 2023

– Created in the past 2 years

Our initial chain filter leaves us with 3 options: Arbitrum, Optimism and Solana.

By then filtering out for Deployment Date, TVL increase and TVL minimum, we’re left with only 8 protocols. Before I introduce the protocols, let me just preface them with this statement: This experiment is not meant to prove that these coins are “good”, but rather to just show an example of a systematic way to narrow focus. The beauty of these exercises is that they can (and should) be repeated, as data changes.

So, these 8 protocols could be a completely different set six months from now. Maybe we’ll have to run this experiment again at the beginning of 2024. Our 8, in order of TVL:

Now that we have our list, there’s lots of things we could try to do to distill more data. We could categorize the protocols and individually compare them to category leaders. We could pin the protocols against each other, and break down TVL, marketcaps, volumes, users, fees and any metric we could use to justify increasing our confidence.

Rather than myself trying to weigh these protocols against one another, I’ll simply choose the 3 that Delphi has written reports about this year. In 2023, Delphi published reports about Radiant, Gains Network and Trader Joe. We’ve also written about 1 other in the list, but I’ll let you do the digging to figure out which one.

Rather than trying to break these 3 protocols down, I’ll take the easy route and just leak some of our PRO research for you. Enjoy a sneak preview of Delphi Research. 👀

Radiant Capital Finds Initial Traction, But

Will It Sustain? (Published Mar 1, 2023)

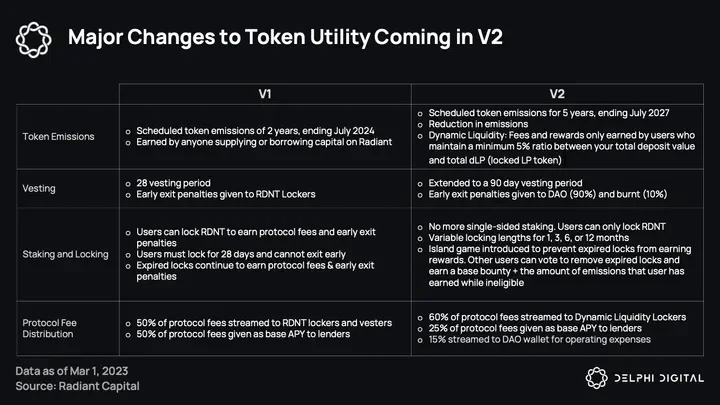

Radiant v2 is slated to launch in the coming weeks. It’s a move towards true omnichain functionality and a more balanced token economy which aims to incentivize ardent users of the protocol.

As part of the upgrade, the team will add collateral support for over 20 new assets and expand cross-chain functionality to five major chains. Ultimately, new collateral assets and markets will generate more revenue for Radiant as the demand for borrowing assets increases. To enable quicker launches on other chains, the team is prioritizing moving the ERC20 RDNT token to the LayerZero OFT (Omnichain Fungible Token) format, which has the added benefits of more seamless cross-chain fee sharing and allowing native ownership of bridging contracts rather than relying on third-party bridges.

Radiant v2 also promises a big revamp to the protocol’s token economics. For one, scheduled token emissions will be extended to five years, up from a runway of two years, thus concluding in July 2027. This will allow the protocol to bootstrap liquidity and incentivize additional user onboarding. The governance vote outlining these changes (RFP-8) also gives the Radiant DAO flexibility in allocating RDNT emissions to different chains. Vesting periods for liquidity mining rewards will be extended from 28 to 90 days, and early exit penalties will no longer be paid to stakers, but will be returned to the DAO (90%) and burned (10%). Moreover, vesting RDNT will not earn protocol fees as in v1.

Radiant is also introducing “Dynamic Liquidity.” This means that lenders and borrowers who are not staking LP tokens to the protocol will not be able to earn RDNT emissions. In order to earn RDNT emissions, users have to provide sufficient RDNT-ETH (dLP) liquidity on top of providing deposits. To be exact, their LP value has to be at least 5% of their total deposit value in order to be eligible for liquidity mining rewards. This is all part of Radiant’s plan to incentivize loyal users of the protocol instead of mercenary farm and dumpers.

While the intention of Radiant to create a sustainable rewards program is a noble one, incentives may end up being underutilized. Firstly, not every user wishes to take on the additional risk of providing an LP position on top of participating in normal money market activities. Secondly, depending on how and when the LP value is calculated, rewards may be unpredictable.

For example, if a user stakes an LP position worth 7% of their deposit, that number could easily and frequently drop below the 5% threshold due to fluctuations in the value of the LP position. This could become problematic and a source of user friction.

LP locks will also replace single-sided locking, as the protocol wants to reward users who are providing liquidity. Instead of a fixed 28-day lock, LP locking periods will be variable, allowing users with different risk profiles and liquidity needs to choose the lock period they are comfortable with. Radiant’s revenue structure will also change to allocate more borrow interest to LP stakers, reducing the portion given to lenders as APY. We will expound on this in the next section.

A summary of the major changes to RDNT’s utility coming in Radiant v2 are outlined in the table below.

Gains Network Gains Ground (Published

Feb 22, 2023)

gTrade features a synthetic model with oracle-fed prices. A single pool provides liquidity for all supported trading pairs. This is similar to how Synthetix works, but Gains Network doesn’t bother with spot synths, and targets a collateralization ratio closer to 100% (much lower than Synthetix’s c-ratio of 400%). To compensate for the additional risk of this more capital efficient approach, Gains Network features an intricate token economics design.

gTrade’s gDAI vault serves as the counterparty for trading activity, providing liquidity for all asset pairs. gDAI — and eventually other gTokens — represent a user’s ownership of DAI in the vault. The gDAI vault receives a share of trading fees, but depositors do not directly benefit from trader losses. Instead, trader losses are kept in the vault to serve as a buffer, preventing vault depositors from incurring drawdowns while safely earning trading fees. If the DAI pool becomes under-collateralized, the GNS token serves as the guarantor of last resort.

In this case, the vault is refilled by minting and selling GNS OTC, capped at 0.05% of the GNS total supply every 24 hours (18.25% per year). A percentage of all trader losses (currently 1% on Polygon, 3% on Arbitrum) are used to buy back and burn GNS. Therefore, GNS is the best way to get exposure to vault PnL.

GNS acting as the backstop for vault collateralization is similar to how MKR supports DAI loans. But just like in the case of MakerDAO, Gains Network has other incentives that shoulder the bulk of the responsibility.

For MakerDAO, users are incentivized to mint DAI when it is above peg and to pay off their CDPs when DAI trades below peg. Gains Network mimics this successful dynamic by offering gDAI vault depositors time and collateralization-based incentives. Users can earn up to a maximum 5% discount on their deposits if the vault has a c-ratio below 100% and they lock for a year. Discounts are offered up to a collateralization ratio of 150% and for time locks of as little as 2 weeks. These incentives help to increase the stickiness of vault deposits and increase the likelihood of additional deposits when the vault is in need.

Trader Joe’s Novel Take on Concentrated

Liquidity (Published March 23, 2023)

When it was launched, Trader Joe was a Uniswap v2 fork on Avalanche. Since then, they have focused on diversifying their product stack to cater to the various needs of a crypto user. Today, Trader Joe is a DEX, money market, and NFT marketplace across a number of chains.

They launched LB in an attempt to further strengthen their position in the highly competitive DEX market across three chains: Avalanche, Arbitrum, and BNB Chain.

Trader Joe’s v1 DEX is a fork of Uni v2 that utilizes the x*y=K (XYK) automated market maker (AMM) model. The drawbacks of the XYK model are well known. It uses a uniform distribution of liquidity and is not capital efficient, as liquidity pools cover prices that are unlikely to be reached. As a result, liquidity is spread thinly across the true range.

In contrast, Trader Joe’s v2 Liquidity Book is a concentrated liquidity DEX similar to Uniswap v3 but with some key differences.

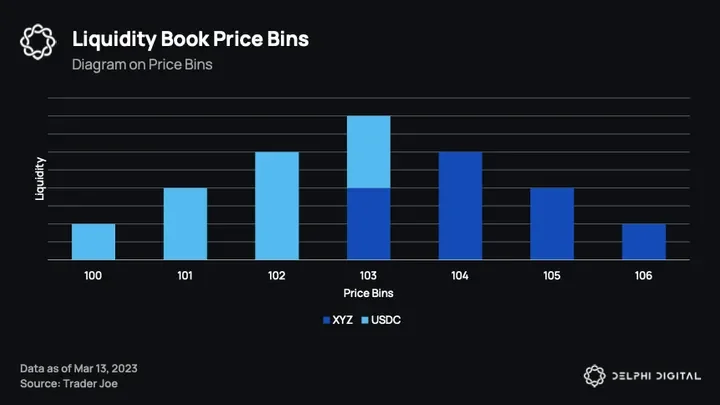

On LB, liquidity is allocated into discrete price bins (similar to Uni v3’s ticks), and trade occurs within the active price bin. LPs can choose the price bin range to provide liquidity and receive a proportionate share of fees generated alongside other rewards.

For instance, the graph above indicates that the active price bin is “103.” This means that all trades will happen within that “103” price bin until liquidity is depleted in either the “XYZ” or “USDC” side. After that, the active price bin will shift upwards or downwards to the next price bin and trades will utilize liquidity from that bin. That new bin will be the new active price bin.

Hey there, just checking in. If you’ve made it this far, and want to keep reading, we’ve unlocked the Trader Joe report for you. If you’re serious about success in the crypto industry, you need access to high quality information. With Delphi on your side, you’ll have access to the same high-quality research and analysis that the pros use. Enjoy this unlocked report, to get a taste of what your crypto process could evolve into.

😭 Meme of the Week

📖 Delphi Reads (Alpha Feed Unlocked)

Cancun Upgrade Incoming, EIP-4844 to Benefit L2s

The Shanghai upgrade provided significant benefits to Liquid Staking Derivatives (LSDs) and mitigated the uncertain duration risks for stakers.

The forthcoming Cancun upgrade will introduce EIP-4844, a crucial enhancement designed to boost the scalability of L2 solutions.

TradFi Entrants and Power Dynamic Shifts

No one can miss the surge in news around traditional market institutions making loud new crypto plays — from BlackRock, Deutsche Bank, Schwab, Citadel Securities, to Fidelity.

For me, it is less news in and of itself — I fully expect these players to be wherever there is the potential for money to be made. What is more interesting to me is the calculus behind these moves as well as the potential implications.

Delphi Roundup | June 28th

Dive into an electrifying Bull vs. Bear episode where we tackle the seismic impact of BlackRock’s prospective Bitcoin ETF on BTC’s resurgence past the 30k mark.

Amid SEC filings against Coinbase, its chosen custodian, we’ll explore what this development means for the industry in our Market Matters segment.

0 Comments