ENS Registrations Spike, DAO Banking, Resource Extraction In The Metaverse

JUL 05, 2022 • 10 Min Read

Anil Lulla + 3 others

Disclosure: Delphi Ventures has invested in ETH. Members of our team also hold ENS and SUSHI. These

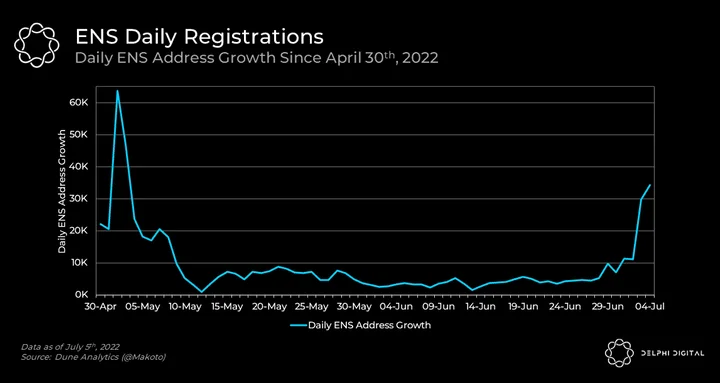

Chart of The Day: ENS Daily Registrations Spike

- Ethereum Name Service (ENS) is a decentralized domain name protocol on Ethereum. Users typically register an ENS to their crypto addresses, making it easily readable compared to the default string of alphanumeric characters.

- As every ENS address is unique, it is common for ENS holders to partake in squatting. Squatting is where a user purchases a domain and makes no use of it, instead hoping for it to gain value so they can flip it for a profit later.

- Daily ENS registrations have spiked recently, reaching over 30k new addresses on July 4th.

- The spike in registrations could likely be due to the ENS address 000.eth being bought for a record-breaking 300 ETH on OpenSea, setting off a 3-digit mania as traders try to capitalize on the hype. Additionally, ENS tops OpenSea in trading volume over the last 24 hours for the first time ever.

For more on ENS, Delphi members can read our Delphi Pro Report here.

DAO Banking: Beyond Tokens

[Excerpt from a Delphi Pro Report]

- The first major instance of a DAO financing attempt came a year ago in July 2021 when SUSHI was looking to do a strategic raise. To set the stage, SUSHI is a “community fork” of Uniswap v2. All the tokens were earned & owned by the community or from funds buying off secondary markets. In July 2021 there was a proposal SUSHI Phantom Troupe, a plan to get some VCs on board to promote & become long-term partners to SUSHI and diversify the treasury into stable assets, blue chips, and seed liquidity in markets for SUSHI’s new Kashi product. At that time, SUSHI had a treasury of ~$214M in SUSHI tokens and a protocol that was making ~$30-40M/month in swap fees. Like most protocols, however, the SUSHI emissions were far greater than income earned, and all of this income went to holders of xSUSHI, not the DAO treasury. This would be like Uber giving users Uber equity for riding with them and then paying out all the income to drivers and holders of Uber shares. You can see how this is circular and not a sustainable long-term strategy.

- Since the community wouldn’t budge on the 5bps full xSUSHI payout ratio (which was misguided even then), new strategies needed to be looked at with respect to diversifying the treasury. Side note: the fact that we tend to include native tokens in treasury assets is not really correct anyways; companies do not include unissued shares on their balance sheet, why do we include tokens there, especially when they are rather trivial to mint later in a DAO’s life (AAVE, YFI)? While none of the fundraising mechanisms proposed ended up passing for SUSHI I want to go over the two proposed by UMA because they can be useful for DAO’s to reconsider in the future.

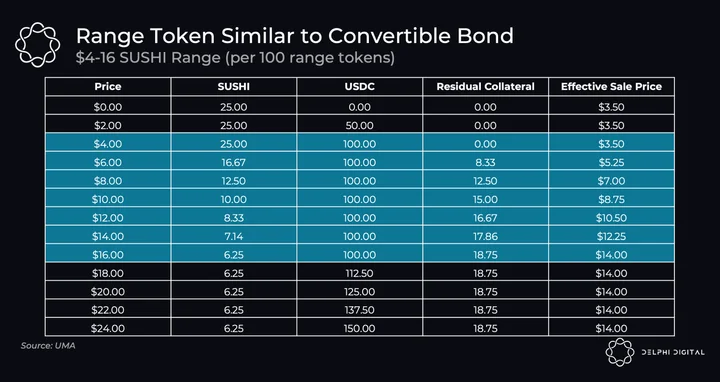

- Range Tokens: UMA’s first proposal was something called a range token, most comparable to a convertible bond (which we will go over with Porter later). Details were as follows:

- Token Name: rtSUSHI-0122

- Size: 50,000,000 rt-SUSH-0122

- Maturity: January 31, 2022

- Price: 0.875 USDC

- Total Value: 43,750,000 USDC

- Collateral: 12,500,000 $SUSHI ($100M at time)

- Range: $4-16/SUSHI

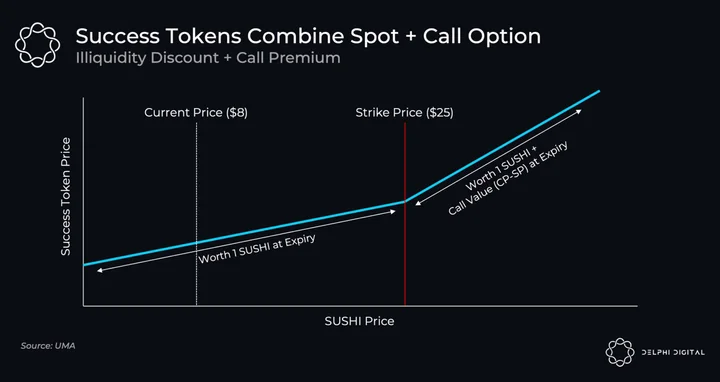

- SUSHI price at raise: $8

- The SUSHI DAO would write 50M range tokens and sell to investors at a 12.5% discount to par, raising $43.75M USDC upfront. At expiry, if SUSHI was $4-16 then range token holders would redeem for the $1 par value (similar to a zero coupon bond). If under $4 range holders would lose out, and above $16 the call option kicks in giving unlimited upside past $16

- The chart above uses range tokens bought in lots of 100. So, going over a few expiry prices:

- $2 SUSHI: holders would redeem for 25 SUSHI/100 range tokens, worth $50. The DAO will have effectively sold SUSHI at $3.50, and buyers of range tokens will have lost ~50% of principal. The 12.5M SUSHI collateral for the deal would be used in its entirety (now worth $25M).

$8 SUSHI: holders would redeem 12.5 SUSHI/100 range tokens, worth $100. Payoff is a zero-coupon bond and SUSHI DAO sold tokens effectively at $7. The DAO would keep half the SUSHI collateral, 6.25M tokens (worth $50M).

$24 SUSHI: holders would redeem 6.25 SUSHI/100 range tokens, worth $150. Payoff is a call option, with unlimited upside past $16. The DAO will have sold tokens at $14 and would have 9.375M ($225M) SUSHI collateral left. - The range token was not selected as it did not fit SUSHI’s main needs (bring on strategic partners & diversify treasury) and investors did not show interest, but it could have been utilized for bootstrapping and seeding SUSHI’s Kashi product with liquidity. Instead of incentivizing users to use Kashi by paying them SUSHI tokens, they could have issued range tokens and used protocol owned/rented liquidity instead. With a successful product leading to an increased token price, less SUSHI would be redeemed from the DAO on expiry of the range tokens than would with an outright sale today.

- With that being said, while range tokens are novel in their design, they do add a bit of complexity and do not really offer more than a convertible bond, and eventual payment is with their native token, not a borrowed asset. For a DAO that wants to retain their tokens it is more desirable to borrow in USD. From an investor’s perspective, there is also the reality that when a range token expires everyone redeems for the same underlying at the same time, which is a volatile asset. There would undoubtedly be some slippage if all range token holders wanted to liquidate their $1 worth of SUSHI for another asset at the same time (convertible bonds have this too but only on the upside). One minor benefit of range tokens over convertible bonds is on the downside risk there is no expectation to make users whole, whereas with a convertible bond there is (social and reputation damage by defaulting on a bond). While a unique DeFi design, Range tokens haven’t received much traction due to their complexity and the propensity for crypto investors to demand upside.

- Success Tokens: The second (and much more interesting) proposal from UMA was their success token. Being a community led project there was a natural apathy towards getting VC’s involved, and the original Phantom Troupe proposal had a 30% discount to the VC’s in the deal. Enter the success token. This is an illiquid token that combines one spot SUSHI + a call option to buy another SUSHI in the future at a certain price (eg $25). The pricing is essentially spot + illiquidity discount + call price. By issuing a success token, DAO’s receive funding upfront and investors are aligned to the future success of the protocol (otherwise the call option becomes worthless). This proposal did not pass because the first iteration was essentially giving away a free call option ($8 success token price @ $8 SUSHI = free call) but that doesn’t mean it can’t be reworked in the future, the right pricing just needs to be found. For example, if a token is trading @ $8 on secondary and a 2 year call with a strike of $25 is worth $3, then the success token should be offered around $11 depending on illiquidity discount. This allows a DAO to capitalize on it’s token at a premium up-front with sacrificing some upside in the future. Essentially the DAO is downside protected and investors get more upside than they would by buying spot tokens.

- Using SUSHI, they could have (hypothetically) raised ~$50M by selling 5M Success tokens @ $10 each, collateralized by 10M SUSHI in the treasury (approx 1/3 of treasury). Put into stablecoins and maybe some ETH/BTC would have given sizeable runway to finance operations in case of a prolonged bear, all while utilizing and bootstrapping their own products. Shortly after the discussion of the success token the market rebounded and all talks were ended without any action being taken. As it stands today, SUSHI is left with a treasury of 14.4M SUSHI ($14.8M) and ~$4M in SUSHIHouse (a product managed by YAM Finance).

- The failed SUSHI raise is worthwhile to look back on, not necessarily because they needed to raise from VC’s, but because their entire success was 100% reliant on SUSHI’s price. Paying for LPs (users) and paying for contributors using the same currency while the treasury accumulates no profits and all liquidity is rented. This is a challenge for any DAO to survive in an adversarial environment. They had a chance to diversify away, cut emissions and own some of their own liquidity by leveraging other tools but did not. In fairness, there were not many options available at the time to do so, but the point remains.

- Most projects have learned by now that financing everything by issuing/printing tokens is not a sustainable path, and options have started coming to market to address this.

- For more information, Delphi members can see the full Delphi Pro Report here.

BreederDAO: Resource Extraction In The Metaverse

[Excerpt from a Delphi Pro Report]

- BREED is the native token of BreederDAO. It will have several functions, including governance, potential rights to BreederDAO revenue in the future, staking rewards, and weighted preferential access to BreederDAO IBO’s (more on these below).

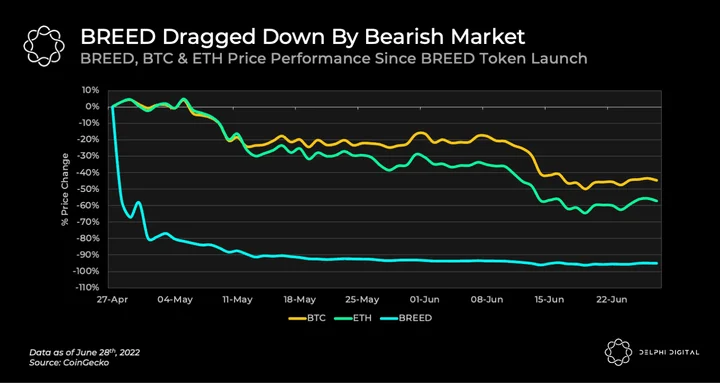

- BREED was launched at an unfortunate time in the market as you can see in the chart above. Even though larger assets such as BTC and ETH are down significantly, it’s clear that BREED has fared worse. It should be noted that most tokens in this sector are also down 80-90% from their highs as well.

- BreederDAO can be seen as a long term play on the growth of play-to-earn gaming. In our previous report Dawn Of The Guilds, we framed Yield Guild Games as an index bet on play-to-earn gaming. This is based on guilds like YGG being diversified across a multitude of games. In a way, DAOs that service guilds such as YGG are akin to an index bet on guilds. Betting on an individual game means trying to pick the winning game. Betting on a guild is effectively a bet on the basket of games the guild participates in. Betting on BreederDAO is an additional layer of abstraction away from picking the winning game and instead becomes a bet on a basket of guilds that the DAO partners with. With $512M raised by guilds last year, there is substantial opportunity for specialized DAOs like BreederDAO.

- Whilst we think we have a long way to go in terms of settling on the optimal model for earning mechanics in games, it’s pretty clear that the play-to-earn sector has inertia for the foreseeable future. This bodes well for play-to-earn guilds, which in turn bodes well for guild servicing DAOs like BreederDAO.

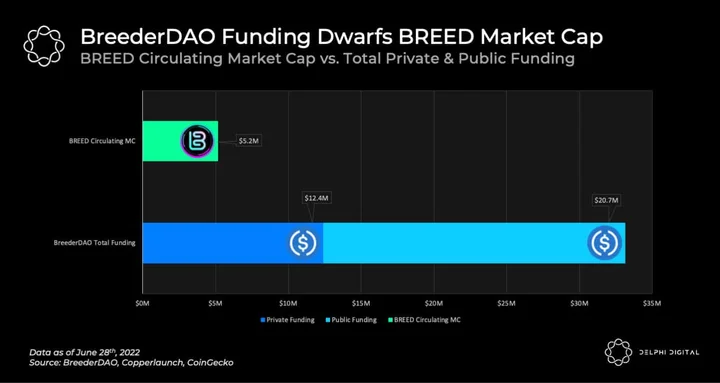

- The chart above contrasts the current value of BREED’s circulating market cap with BreederDAO’s total private and public funds raised. If you believe games with an earning component aren’t going to disappear overnight, BREED could be worth looking at. However, if play-to-earn fails to become sustainable over time, it won’t bode well for projects like BreederDAO whose survival depends on the success of the category.

- For more, Delphi members can see the full Delphi Pro report here.

Notable Tweets

Vauld Suspends Services

JUST IN: Vauld suspends trading, deposits, and withdrawals, citing current “market conditions.”

—

Watcher.Guru (@WatcherGuru) July 4, 2022

Largest Bitcoin Exchange Outflow

Largest #bitcoin exchange outflow on record.

Probably nothing…

— Lark Davis (@TheCryptoLark) July 5, 2022

Ethereum vs. Solana NFT Volume

NFT volume 🖼

Ethereum (left) vs Solana (right)

— Alex Svanevik🐧 (@ASvanevik) July 4, 2022

Anil Lulla + 3 others

0 Comments