Gary’s Protection

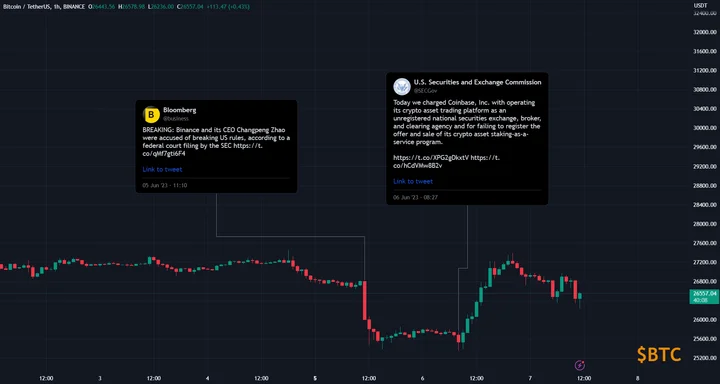

In spectacular fashion, the SEC has filed lawsuits against the two largest cryptocurrency exchanges, Binance and Coinbase, on consecutive days. Coinbase is accused of listing tokens that are unregistered securities and offering its staking program. Meanwhile, Binance (along with CZ) faces various charges like commingling customer funds and defrauding investors.

The market has quickly shaken these accusations off, with BTC now trading at roughly the same price as when the first lawsuit was announced.

Exchanges are a sensitive topic, particularly for an industry still recovering from the FTX collapse. While centralized exchanges should be subject to scrutiny, the SEC’s regulatory approach not only fails to protect investors but actually harms them.

During an appearance on NBC’s Squawk Box on the same day as the Coinbase lawsuit announcement, SEC Chairman Gary Gensler stated, “We don’t need more digital currency. We already have digital currency. It’s called the U.S. dollar. It’s called the euro. It’s called the yen. They’re all digital now.” While Chairman Gensler is entitled to his opinions, the remarks seem to reinforce the perception that the SEC is not being tech neutral in its approach to regulation.

Instead of creating clear rules for the industry to follow, the SEC has opted for regulation through enforcement, selectively punishing stakeholders acting in good faith.

Today, the Howey test is used to determine if something is an investment contract that falls under securities laws. The test originated from a landmark United States Supreme Court case called SEC v. W.J. Howey Co., decided in 1946. The case involved the Howey Company, which was selling parcels of land in a citrus grove along with service contracts for the cultivation and harvesting of the fruit. The Securities and Exchange Commission (SEC) argued that these sales constituted investment contracts and should be subject to securities regulations.

According to the Howey test, an investment contract exists when:

1. Money is invested.

2. There is a common enterprise where returns rely on others.

3. There is an expectation of profit.

4. Success primarily depends on the efforts of a third party or promoter.

For securities to be traded in the United States, they must be registered with the SEC. Therefore, if a U.S. exchange like Coinbase facilitates the trading of tokens that are actually unregistered securities, it is breaking the law. So far, the SEC has failed to provide guidelines for tokens to register as securities, as naturally it’s difficult to take a law created in 1946 for citrus groves and apply it towards permissionless public networks.

This lack of guidance has discouraged compliant behavior from industry participants. In fact, projects that have actively pursued regulatory compliance have often found themselves subjected to investigations rather than cooperation. For projects unable to afford the legal costs of an SEC investigation, it is not feasible to risk pursuing “compliance” when the path to compliance is unclear and nearly impossible.

In 2022, Coinbase held 30 meetings with the SEC in an attempt to understand the guidelines they were expected to follow. Instead of being rewarded for their proactive approach, they were met with a lawsuit. Currently, 33 countries are establishing clear guidelines for the crypto industry, while the United States lags behind.

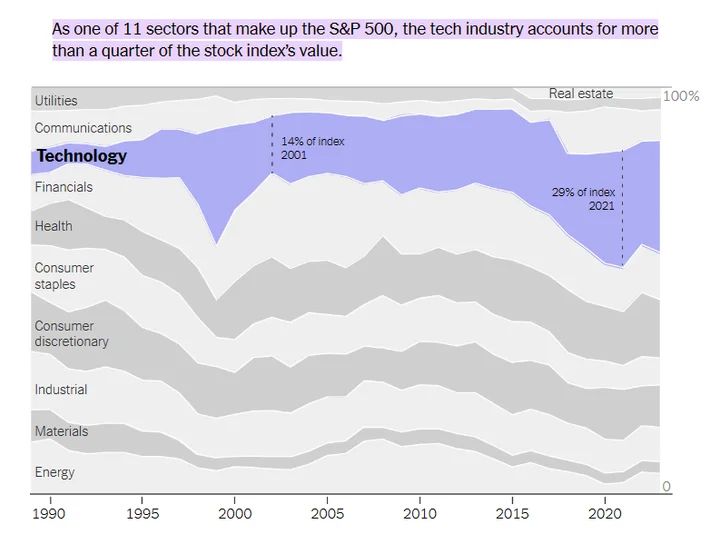

Today, the largest sector of the S&P 500 is Technology, which accounts for more than 25% of the stock index’s value (nytimes). This is due to America being the innovation capital of the world, producing 4/5 largest companies in the world over the past 50 years. America risks losing it’s innovation hub status if it continues down this path and pushes innovation offshore.

While the SEC has taken an independent stance, other entities have demonstrated their willingness to embrace crypto and maintain the country’s position as the innovation capital of the world.

The CFTC has stated that several digital assets are commodities rather than securities, as emphasized by CFTC Chairman Benham just yesterday, highlighting the potential for financial inclusion enabled by crypto. Recently, members of the U.S. Congress introduced new legislation to establish a pathway for a token to transition from being a security to being a commodity.

The U.S. government demonstrates support for crypto across its various branches, and there is backing from nearly every corporate sector within the country. Implementing common sense regulations will pave the way for the U.S. to maintain its position as the global capital of innovation. One individual’s claim that “We don’t need more digital currency” will cause significantly more harm to the U.S. than it ever will on this permissionless global technology.

In the Coinbase suit, the SEC alleged 13 seemingly random cryptocurrencies as securities. A lack of guidance and respect for the industry not only hurts good actors, but rewards bad actors for being able to blend in with the sea of projects that want to comply but don’t know how. The SEC has positioned itself not as a protector of investors, but rather as an enabler of such bad actors as SBF. Scare tactics are being used, such as a request that assets held by Binance.US should be frozen. Binance.US will likely shut down shortly as a result of these actions.

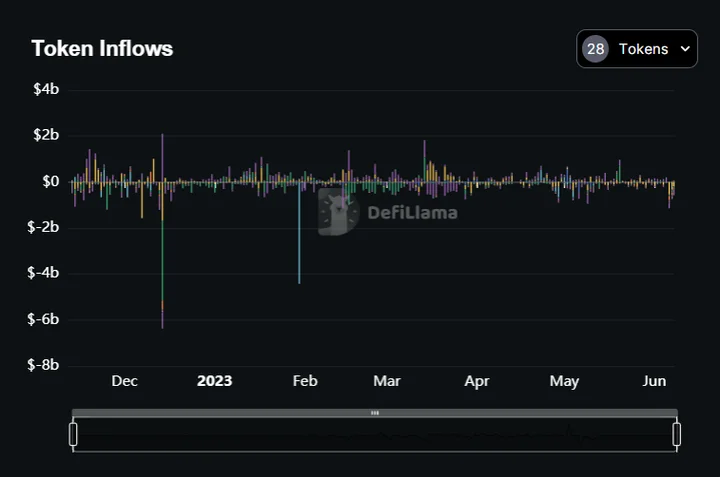

However, the lack of customer withdrawals (shown for Binance by DefiLlama above) despite these enforcement actions reflect a market that seems to have dismissed the SEC, signaling an agency that is losing credibility by the day.

Gabriel Shapiro and Sarah Brennan, General Counsels of Delphi Labs and Delphi Ventures, recently published a series of policy papers proposing a regulatory framework that embraces transparency, disintermediation, and decentralization.

A key point highlighted in these papers illustrates how current regulatory stances can inadvertently promote unchecked monopolization in the industry. The authors dive into how regulatory burdens should fall on the subset of large and systemically important market actors that are most likely to cause, and most able to improve, risk factors across the ecosystem. You can read the full paper here.

While responsibility should scale with power, a lack of guidance de-correlates the two and harms investors rather than protect them. As it stands, the industry needs to shield itself from Gary’s protection.

👩🏫 AMA with Delphi Ventures GC, Sarah Brennan

Q1. Is a statement like “We don’t need more digital currency.” unprecedented from an SEC chairman?

I think that was a slip from prepared talking points at a minimum. The standard talking points are that the SEC is merit neutral – the SEC should be merit neutral. This statement is a break from that where a policy determination is being made.

Q2. How do you see the Binance and Coinbase lawsuits playing out?

I think they will both be very long and expensive fights that require significant resources from all parties involved. It is hard to say how these play out – practically, I think Binance likely exits the US and I think we have a chance of legislation that might help Coinbase’s outlook to stay in the US market. On the registration front, it is a tough situation for Coinbase. They are being accused of failing to register while at the same time such registration is not currently possible in the US in the digital asset space.

Q3. How long do you think it will take to pass sensible crypto regulation in the U.S.? And are there any proposals in particular that have caught your eye?

I think we have a shot right now with the Digital Asset Market Structure bill that was released recently in discussion draft. It would go along way to give regulatory certainty around token issuances. There is work to do on the draft to make it viable and it needs bipartisan support to have legs. But even if it doesn’t pass, it could very well form the basis for eventual legislation within the next 2-5 years and then there will be years of regulatory rulemaking that would follow. This would need to be supplemented but it could form the cornerstone for regulation and we are starting to have sensible conversations on use cases for blockchain and broader sets of appropriate regulations, including the FTC’s role in policing fraud. I think we have some positive momentum right now but this is hard to get right, bipartisan support is not guaranteed and time will tell.

😭 Meme of the Week

📖 Delphi Reads (Alpha Feed Unlocked)

As mobile gaming grew its share of the global games industry, the free-to-play business was booming. Following a model of onboarding first and monetization later via in-app purchases, F2P quickly carried the industry to new all-time highs. Brian sheds light on Web3’s Implications for Multi-Billion Dollar In-Game Item Economies.

We saw a 66% increase in total funding amount and a 240% increase in the number of deals announced in May compared to April. That being said, total Web3 game investments are still down by 37% compared to February. Joseph provides insight towards VC gaming funding in 2023.

As a new contender in the NFT lending realm, Blend achieved a remarkable feat by capturing 77% of the total NFT borrowing volume market share and facilitating over 31.8k loans totaling $466M in volume since launch. YH provides perspective into Blend being the new leader in NFT Lending.

0 Comments