Inside the Ecosystem: Fueling Aptos' Global Trading Engine

JUN 26, 2025 • 39 Min Read

Report Summary

Summary: Aptos Ecosystem – Delphi Report

The Delphi report provides an in-depth analysis of Aptos’ rise as a performance-first Layer 1, transitioning from raw infrastructure focus to becoming a serious contender for DeFi and trading dominance. It outlines key ecosystem trends, app performance, and the network’s roadmap to becoming the Global Trading Engine (GTE) for the onchain financial system.

Key Takeaways

1. Performance & Growth

-

Fastest L1 block times (~122 ms), thanks to upgrades like Zaptos and MoveVM optimizations.

-

TVL has surpassed $1.3B, led by increased stablecoin usage and DeFi app incentives.

-

DEX volumes and daily active addresses are rising, with trading volumes exceeding $2.9B/month.

-

Aptos is cementing its role as a DeFi-first chain, with low latency and high throughput enabling scalable, capital-intensive apps.

2. Marquee Apps Powering DeFi

-

Thala: A DeFi superapp with AMM, lending, CDP stablecoin (MOD), and liquid staking.

-

Echo Protocol: BTCFi hub with $278M+ in BTC TVL, bridging BTC to Aptos via aBTC.

-

Hyperion: Fast-rising CLMM DEX with $100M+ in daily volume; aims for superior execution.

-

Aries Markets: Top lending market with $770M in TVL; features recursive leverage, swap aggregation.

-

Echelon: Competing money market with isolated risk pools and multi-chain expansion.

-

Amnis: Liquid staking protocol with dual-token design and 170M+ APT TVL.

-

Merkle Trade: Onchain perps DEX using oracle-based execution and skew-adjusted funding.

-

emojicoin.fun: Meme launchpad for emoji-based coins, targeting native cultural engagement.

3. Promising Newcomers

-

Moar Market: Offers 15x leverage and auto-deployment of capital into yield strategies.

-

Mirage Protocol: Innovative CDP + Perps DEX hybrid using mUSD; inspired by MakerDAO and Synthetix.

-

Ekiden: Institutional-grade hybrid orderbook (off-chain matching, on-chain finality); aims to rival CEXs.

4. Payments & Stablecoins

-

Native USDT, USDC, USDe now live, enabling Aptos to serve as a stablecoin payment and settlement rail.

-

Potential to compete with Visa-scale apps—if distribution and merchant tooling challenges are solved.

5. Rise of the Global Trading Engine (GTE)

-

Aptos is building a native, composable on-chain orderbook layer—a game-changer for decentralized markets.

-

Combining DAG-based consensus (Raptr) with high throughput = ideal for CLOB-style execution.

-

The goal is to host all forms of onchain trading (perps, spot, RWAs) in a borderless 24/7 financial system.

6. Real-Time Data Layer: Shelby

-

Decentralized, monetized data storage layer co-developed by Aptos Labs + Jump.

-

Allows developers to earn from reads (not just storage fees), enabling use cases in AI, gaming, and NFTs.

-

Serves Aptos’ vision of powering not just finance, but real-time internet infrastructure.

7. Strategic Positioning

-

Aptos is executing a “build first, scale later” approach—laying groundwork with:

-

Low-latency infra

-

Secure MoveVM

-

Strong DeFi base

-

-

Lacks viral native tokens or meme culture (like Solana), but ecosystem maturity and serious apps are catching up.

Conclusion

Aptos is emerging as a serious Layer 1 designed for speed, financial infrastructure, and global trading utility. With powerful DeFi protocols, stablecoin support, and a performant tech stack, it is positioning itself to host next-gen financial apps, orderbooks, and payment rails. While liquidity and mindshare still trail Ethereum and Solana, the foundation being laid today could turn Aptos into the onchain equivalent of the Nasdaq—a Global Trading Engine for the digital economy.

-

Introduction

The success of a blockchain hinges on two key pillars: the ability for the chain to service a large number of concurrent users and the existence of applications that give users a compelling reason to use the chain.

On the first pillar, performant blockchains drove a paradigm shift in how app builders and users interact with onchain products. On the second pillar, there’s been a big shift in core approaches to ecosystem building since 2020-22 – users have come to demand more of their base layers beyond high performance.

People involved with developing and executing Ethereum’s roadmap tried to steer clear of getting involved with the app layer. This led to a much slower pathway to app development and fixing crucial issues that plagued application devs.

In our Aptos deep dive, we contrasted this to Aptos’ approach and tech stack in detail. As a blockchain, Aptos has put a serious dent into the first pillar via breakthroughs to the VM, consensus mechanism, and parallelized execution. Recently, the network recorded industry-leading L1 block times as fast as 122 milliseconds.

And as an ecosystem, Aptos has started to make headway in incubating and supporting sticky applications. But before we get into the nitty gritty of Aptos’ product layer, it’s important to understand the current state of usage and activity on the chain.

State of the Network: H1 2025

Growth on Aptos has picked up meaningfully across multiple metrics. TVL, usage, and trading volumes are all trending in the right direction as we head into the second half of 2025. While the broader ecosystem may trail the larger chains, the fundamentals are showing solid progress thanks to network upgrades and new products. Here’s a quick snapshot of how activity has evolved over the past couple of quarters:

Aptos TVL has grown significantly from the lows of last summer, climbing to a new ATH of over $1.3 bn. Much of this expansion can be attributed to increased stablecoin flows, as well as coordinated liquidity incentives across Aptos’ top protocols.

Despite consistent growth in TVL and activity, block times on Aptos have steadily improved. With a ~45% reduction in latency from 220 ms to under 125 ms today, Aptos is currently the fastest L1 measured by block time. These performance achievements reflect the ongoing upgrades made to both the MoveVM and the Move language.

While not on par with the top L1s yet, DEX volumes on Aptos have been consistently growing since the lows back in March. May marked an ATH with over $2.9 bn in monthly volume traded across Aptos-native protocols like Hyperion, Thala, and LiquidSwap.

Daily transactions have stayed in a healthy range between two and four million since the beginning of the year. A large portion of this activity takes place on key ecosystem apps such as Aries Markets, Amnis Finance, and Hyperion.

As shown on the chart, there was a significant spike in transaction volume at the end of January, coinciding with the launch of native USDC and CCTP on Aptos.

Daily active addresses show a similar pattern, typically ranging from around 900k to 1.2 mn daily. While down from the January peak of 1.6 mn, usage has leveled out with persistent engagement across the ecosystem.

Note: Daily active addresses refer to active interacting addresses of projects’ revenue-generating smart contracts. Active Addresses do not equate to active users, as users may create and operate multiple wallet addresses.

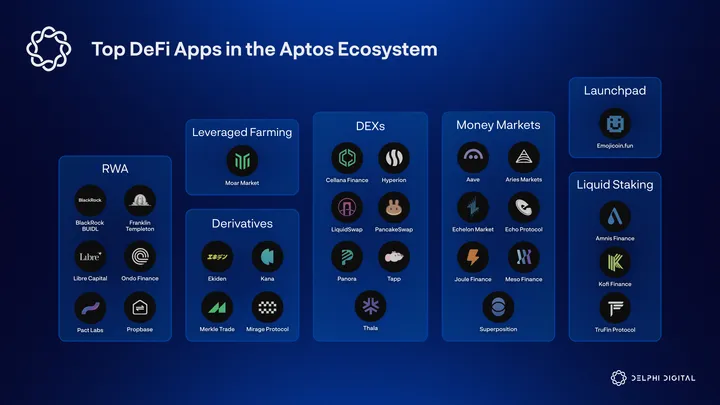

The Lay of the Land: Aptos’ Marquee Apps

As we delved deeper into the list of existing and upcoming projects on Aptos, it’s clear that the case to build on Aptos is especially reaching DeFi builders. Aptos is on the right path to becoming a DeFi hub.

A clear example of this: one of crypto’s most prestigious and battle-tested applications, Aave, is making its first non-EVM deployment on Aptos. Aave is approaching deployment in a measured way, initially launching on testnet to ensure everything runs smoothly first. The governance proposal for Aave to deploy to Aptos mainnet successfully passed this June.

The existence of a brand like Aave on Aptos is emblematic of the chain’s DeFi focus. Aave is a household name in crypto – well known and respected – boasting ~ $25 bn of TVL across its EVM deployments. Aptos, as its maiden voyage beyond the EVM sea, sends a message to the industry that it is a serious contender.

While Aave’s deployment is a loud signal, the real magic will be in Aptos’ ability to cultivate native DeFi apps that are compelling enough to make more users bridge over and actively use the chain. And this undertaking is well underway.

Thala

Thala is trying to be a DeFi superapp on Aptos and is currently the top app by cumulative and 24h revenue. The protocol has four distinct verticals: a DEX, a money market, a CDP stablecoin (called MoveDollars), and a simple liquid staking module for APT. Thala’s most successful product to date is its DEX, Thalaswap.

Thalaswap offers pool creators the ability to create weighted pools, stableswap pools, and Liquidity Bootstrapping Pools (LBPs). Thala’s documentation indicates that they are also working on enabling concentrated liquidity pools, which stand to improve liquidity efficiency. Concentrated liquidity pools would make Thala a fairly complete DEX offering.

Stablecoins and APT comprise the vast majority of volume on Thala. The top 10 pools over the past month are all stablecoin to stablecoin or APT to stablecoin pools.

Thala’s daily volume has been on a consistent upward grind over Q1/Q2 2025, following the launch of Thalaswap v2. The protocol has done over $2.3 bn in lifetime volume since ThalaSwap v2 was launched in Nov. 2024.

Thala was the top Aptos DEX until very recently, and its foray into other DeFi products hasn’t been as successful as ThalaSwap. Lending markets on Thala have a total collateral base of about $15 mn; less than 1.5 mn MoveDollars (MOD) have been issued; and about $34 mn of APT is in their liquid staking module.

One thing we have seen time and time again is how protocols that try to build a wide suite of products from the get-go – rather than devote their focus to one product – end up being a jack of all trades but a master of none.

Thala takes 50% of swap fees for protocol revenue. The protocol’s native analytics dashboard indicates about $2.2 mn of total protocol fees since its inception in April 2023. Since volume has begun to tick up, if Thala – and Aptos – are able to sustain this surge in volumes, Thala’s total fee capture should rise significantly over the course of 2025.

Thala’s continued growth as a DEX is contingent on the macro demand to trade on Aptos. The DEX on its own is not super differentiated, but it does not need to be. However, the Aptos DEX market is heating up with significant competition entering the mix. Thala’s continued growth will also be a function of its ability to attract users by providing the best execution routes.

Echo Protocol

Echo is a Bitcoin-focused liquidity & yield aggregation layer in a nutshell. Cementing its position as the go-to BTCFi hub on Aptos, Echo is aiming to replicate its success across the broader Move ecosystem. The app has steadily grown since launch and now stands as the largest protocol on Aptos by TVL, with total BTC assets nearing $278 mn on Aptos alone.

Structure-wise, Echo differs from other traditional BTC staking protocols by combining a unified and flexible vault system with a Proof-of-Reserve (PoR) guarantee. Users can deposit native BTC, BTC LSTs like LBTC, or wrapped BTC like wBTC or fBTC. Echo then locks the underlying assets and mints a composable Aptos BTC (aBTC) that can be freely used across Aptos DeFi and even bridged out to other chains.

Another standout feature is Echo’s approach to BTC yield. Once minted, Echo’s aBTC can be deployed into Echo’s Yield Layer. From lending and leveraged liquid staking to eMSTR, a flagship product that lets BTC holders boost their exposure with no risk of liquidation by using on-chain convertible notes instead of margin loans.

To boost user retention and ecosystem stickiness, Echo runs one of Aptos’ most active points programs. Users earn Echo Points – redeemable for presumably a future airdrop – by bridging, staking, lending, borrowing, or completing specific “campaigns” that offer point multipliers. For example, staking APT or using aBTC in Echo Strategies can yield up to 5x point boosts compared to standard actions.

With audited security, real-time PoR via Chainlink, and integrations with other BTC L2s like Babylon and B², Echo strives to be the default BTC liquidity and yield hub across the entire Move ecosystem.

Growth levers for Echo, as a protocol, are focused on a few areas:

- Cementing its position as the default BTCFi layer on other emerging Move networks like Movement and Morph

- Becoming the trusted aggregation layer for native BTC, wrapped BTC, BTC LSTs, and Bitcoin L2 assets

- Launching more structured yield products to cement its moat as the go-to BTCFi layer

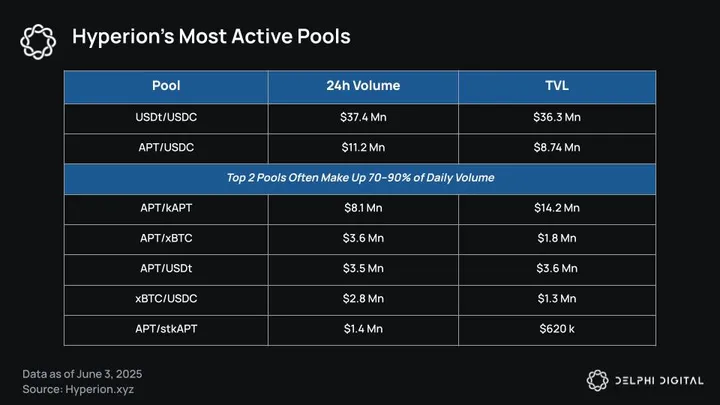

Hyperion

The newest kid on the block, Hyperion, is a concentrated liquidity AMM on Aptos. Hyperion launched in Feb. 2025. Daily volumes oscillated between $5-15 mn for the first couple of months but started to consistently settle above $20 mn per day by late April. Recently, the volume floor has been closer to $100 mn, alongside TVL climbing above $120 mn from zero in just four months – a sharp increase.

Hyperion’s burst in volume seems to have coincided with Aptos announcing that Hyperion will be part of the LFM – Aptos’ incubator for projects that are closing in on a token launch.

Initially, Hyperion was set to be a hybrid AMM-CLOB. However, with the announcement of Aptos’ native orderbook framework, Hyperion will double down on its AMM instead. Like Thala, the vast majority of volume on the DEX can be bucketed into stablecoin-to-stablecoin swaps, APT to stablecoin swaps, or APT to APT-derivative swaps.

On May 18, 2025, Hyperion did $72 mn in volume. Of this, $54.2 mn was from the USDC/USDT pool and $10.6 mn was the APT/USDC pool – a total of $65 mn or 90% of total volume. A lot of this just boils down to the sheer amount of stablecoins on Aptos.

After zeroing in on concentrated liquidity, Hyperion is basically a rendition of Uniswap v3 on Move rails. The DEX market today is no longer about building the most innovative and complex product. Raydium and PumpSwap have proved that.

The success of a DEX hinges on whether it can build loyalty by giving users superior execution. When Aptos enters its “Solana era”, where aggregators own swap customers, execution will be the only criterion that matters. That means every DEX needs to aim to provide the best ranges (for CLMMs) and deepest liquidity in order to cement their place.

Given Hyperion is currently pre-TGE, there is an implicit incentive to use the product today in the hopes of an airdrop.

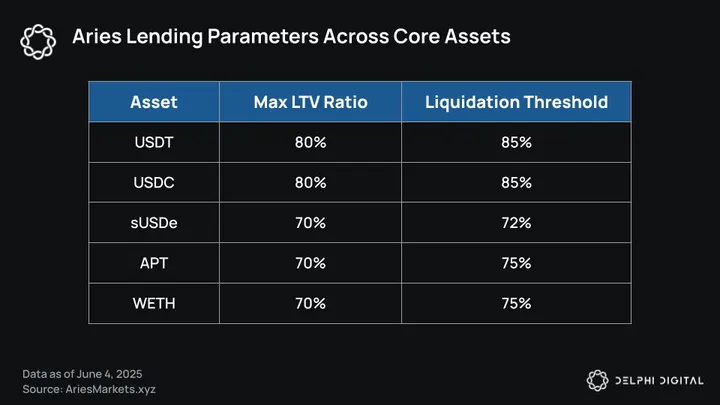

Aries Markets

Aries is not only the largest money market on Aptos, but also the second-largest protocol by TVL and one of the first dApps on the chain. The protocol has over $770 mn in deposits and over $350 mn in active loans.

As one would expect, the vast majority of lending and borrowing activity is in stablecoins. Roughly 75% of Aries’ capital supplied is in USDT, USDC, or sUSDe (Ethena’s yield-bearing semi-stablecoin). sUSDe is a much smaller market, and it’s also not a pure stablecoin like USDT and USDC. On the borrowing side, about 87% of Aries’ active loans are in USDC or USDT.

Stablecoin markets on Aries have associated incentives in APT. That means the net yield is boosted for lenders, and vice versa, the net borrowing cost is subsidized for borrowers. At the time of writing, lenders are receiving cumulative APRs of 8.88% on USDT and 9.58% on USDC. The borrowing side, however, has a net borrowing cost of 7.8% for USDT and 7.59% for USDC. All in all, this opens the gates to non-productive activity, where people deposit one stablecoin, borrow another, deposit their borrowings, and create a recursive lending strategy.

Recursive, or looped, leverage strategies are not inherently bad. They do have positive implications in that they boost pool utilization and can, in some cases, improve liquidity for a market. However, in this case, it paints a distorted picture of the appetite for leverage on Aptos. Utilization on the USDT and USDC markets currently stands at 76% and 74%, respectively. In reality, there is likely a large amount of recursive activity contributing to those higher utilization rates.

Aptos is in a nascent stage of value creation and ecosystem building. So, incentives that promote more utilization are not negative. The ultimate goal here is to have USDC/T lending rates that are not only competitive but also higher than other money markets across chains. If these incentives result in more capital being supplied on a net basis, then they are effective.

While borrower risk limits on Aries are reasonable, they are higher than more established money markets like Aave. For example, USDT on Aries has an LTV of 80% and a liquidation threshold of 85%.

Aave v3 on Ethereum mainnet has a 75% LTV and 78% liquidation threshold for USDT. Now, USDT is much more liquid on the Ethereum mainnet, but the chain itself is constrained. During liquidation cascades, the Ethereum mainnet gets clogged up much easier. Execution takes, at minimum, about 11-13 seconds (i.e., the time to propose and finalize a single Ethereum block).

Aptos is several orders of magnitude faster. Since Mar. 2025, Aptos has averaged under 140 ms per block produced. As a result, there is less concern about getting liquidations through in a timely manner. Especially given that most of the loans are stablecoin borrows against stablecoin deposits. Even as the collateral mix grows riskier, Aptos’ performance and throughput serve as a base for enabling higher risk limits than slower chains.

At the moment, Aries is the closest thing to the homepage of Aptos. The protocol’s frontend consists of access to Aries money markets, a bridging portal powered by Wormhole, and a swap aggregator that gives users the best execution in line with available swap routes.

Swap aggregation also lends another neat UX boost. Users can directly trade assets available in the money market against their collateral. For example, think of a trader who has 1,000 APT as collateral in Aries. This trader believes APT will perform well over the next few months and wants to increase exposure. Using Aries, they could of course borrow USDC against APT, take it to a DEX, and swap it for more APT. Because Aries has a swap aggregator, users could hypothetically trade borrowable USDC for APT right from the frontend.

The max leverage a user can get to farm or margin trade via Aries will always be under 2x due to the overcollateralized nature of the markets. Aries was reliant on Econia’s CLOB for its spot margin trading. As a result of Econia’s deprecation, Aries will be moving forward with the chain-level orderbook that will be built on Aptos.

Aries does not currently have a native token. If Aries TGEs, it will likely be one of the most anticipated and well-received tokens in the Aptos ecosystem.

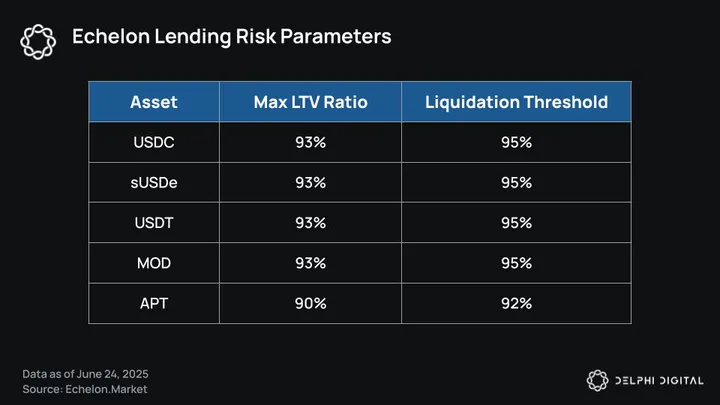

Echelon

Closely following Aries, Echelon is the second-largest money market on Aptos. Echelon has $290 mn in supplied capital and $78 mn in active loans, giving it a global utilization rate of 27% versus Aries’ rate of 62%.

Structure-wise, Echelon and Aries are not all that differentiated. They use similar risk parameters, the same interest rate slopes, and cater to the same mix of assets. Unlike Aries, Echelon is not all-in Aptos and is also deployed on Movement and its own Echelon app chain built on Initia.

One of Echelon’s main points of differentiation is its vault-accounting system. Aries uses a unified margin account, where collateralization is done on the account or address level. As a result, all of a user’s risk is lumped together. Echelon’s vault accounting system allows for isolated lending pools and thus the ability to silo specific kinds of risk/exposure. Echelon has core markets for assets like USDC, APT, and USDC; but it also has isolated markets for more volatile assets like GUI and LSD. It’s worth noting that isolated pools on Echelon have not found any meaningful traction, with less than $110k of value in the system.

When Echelon launched on Aptos mainnet in Mar. 2024, it was the first to bring the e-mode feature originally ideated by Aave. e-mode allows users to lever up at higher LTVs than otherwise allowed when they are collateralizing a loan against a pegged asset. For example, depositing APT to borrow stAPT is an action permitted in e-mode that would boost the normal LTV from 70% to 90%.

As mentioned previously, Echelon’s global utilization rate is roughly half of that of Aries. In terms of capital supplied, Echelon’s biggest markets are sBTC, USDC, and sUSDe. From a utilization perspective, the most tapped markets are APT, USDT, and USDC. It’s worth noting that while the USDC market has $69 mn supplied and $56 mn loaned, the USDT market is much smaller with $9 mn supplied and $6.77 mn borrowed. USDC and USDT are both supported with incentives in thAPT.

Echelon received a $100k grant from Thala Labs and the Aptos Ecosystem Fund, which explains why they have incentives in thAPT. The project’s roadmap also notes an intention to introduce native swapping to the Echelon front-end by implementing a white labeled instance of the Thalaswap AMM.

Growth levers for Echelon, as a protocol, are focused on a few areas:

- Becoming a brand name in the Move ecosystem, beyond just Aptos. Echelon has already deployed on Initia and Movement and will continue to double down on those chains alongside Aptos.

- Being a leader for Bitcoin assets in the Move ecosystem as BTCFi and projects associated with this narrative start to really pick up.

- Introducing modular lending primitives similar to Morpho Blue.

Amnis Finance

One of the first DeFi protocols on Aptos, Amnis Finance is a liquid staking provider with over $170 mn in TVL.

Amnis takes a somewhat different approach from Lido and Jito in the core mechanics of the liquid staking system. Instead of depositing APT and receiving a derivative token representing staked APT directly, a dual-token system is used. Users deposit APT and receive amAPT – a pure derivative of APT that aims to be pegged 1:1 to APT. Users who stake their amAPT receive stAPT, which is comparable to stETH and jtoSOL. stAPT is a representation of the principal deposited + yield earned from staking operations.

Amnis’ DAO currently takes a 7% commission on all APT staked with the protocol. For reference, Lido’s DAO on Ethereum charges about 10%. Liquid staking products tend to have two kinds of fees: a fee on withdrawing assets from the protocol and a commission on staking rewards for operating the required infrastructure. Amnis does not have a pool for quick withdrawals. However, liquidity is available against amAPT on secondary markets, allowing users to exit at a slight discount.

All in all, Amnis is a fairly simply built liquid staking provider and has done its job of enabling APT staking for regular users. The protocol launched it’s native token, Amnis, in Q4 2024.

Merkle Trade

Merkle is an onchain perpetuals DEX that uses a single-asset liquidity pool model. The platform offers a variety of tradable assets and utilizes a USDC liquidity pool as the global counterparty for all trades. This is similar to the model employed by Gains Network.

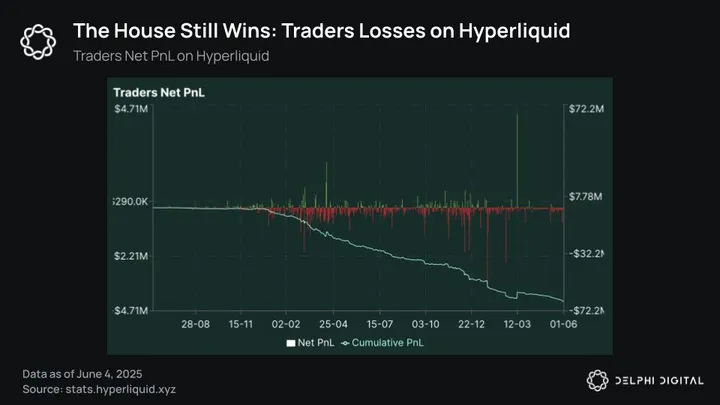

Since Merkle’s liquidity pool takes the other side of every user’s trade, it is essentially a means of betting against retail traders – a historically winning outcome. Traders on GMX, Gains, and even Hyperliquid lose money over mid-to-long periods of time. There have been concerns around the tail risk of employing such a model, but the long-standing trend of retail traders losing money has prevented these tail risks from seriously materializing.

Merkle’s supported assets include majors like BTC, ETH, and SOL; memecoins like DOGE, WIF, and TRUMP; emerging assets like VIRTUAL, WLD, and TAO; and even currency/commodity pairs like EUR/USD, USD/JPY, and XAU/USD (gold). All in all, Merkle supports 54 different tradeable pairs – which is pretty impressive. The platform uses Pyth oracles for price feeds.

Perp platforms that execute trades based on an oracle price have a long-standing problem with front-running oracle updates. GMX mitigated this by ensuring that its oracle update happens at the top of a block, and all trade executions happen after. This was implemented in the aftermath of the AVAX market front-running incident. Merkle’s approach to this problem is to split execution into two steps, using a keeper. First, a user submits their trade transaction to the smart contract. Then, a keeper bot picks up the transaction and submits it for execution against the real-time price index. This ensures necessary price feed updates happen before user trades are executed.

Merkle seeks to balance its open interest (OI) skew via its funding mechanism. Unlike orderbooks, where funding is used to bring the mark price and oracle price into equilibrium, funding on Merkle is a function of the OI skew. If there are more longs than shorts, funding will be positive and charged to longs. Shorts, however, will net receive funding payments. This is an incentive to balance out the OI for a market to try and ensure LPs are as close to delta neutral as possible.

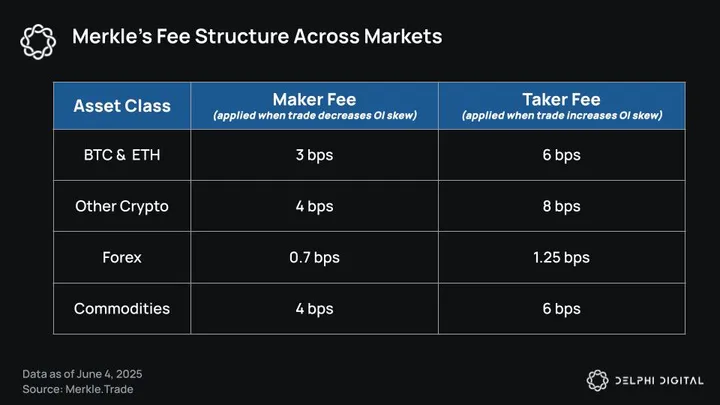

User fees for a trade are also determined by the OI skew. If a trade furthers the skew, it is subject to a higher taker fee. But if it moves against the skew, it gets a lower maker fee. For example, if the OI on the SOL market is $1 mn in longs vs $1.5 mn in shorts, those who short will pay the higher fee (taker) and those who long pay the lower fee (maker).

At the time of writing, Merkle has close to $4 mn in USDC in its core liquidity and has facilitated an average daily volume of $47 mn between Jan. 1 and May 26 – a commendable feat.

A big portion of this volume is likely arbitrageurs – and this is part of what Merkle wants to optimize for. Merkle’s funding mechanics make it more appealing for arbitrageurs to come in and bring funding to equilibrium. Rather than the funding rate being a pure function of the OI skew, i.e. skew determines the funding rate, the skew determines the velocity of change in the funding rate, i.e. how much it changes every hour. This makes the funding rate more predictable, and thus makes arbitraging rates just that much easier.

The fee structure on Merkle is fairly simple and follows a 50-30-20 split: 50% of entry/exit fees on trades go to LPs, 30% goes to a protocol fund for stakers, and 20% goes to a development silo to fund Merkle’s roadmap.

On the whole, Merkle is one of the more complete offerings on Aptos: an intuitive product, a large TAM, a mechanism design that works for both sides (LPs and traders), sensible veToken economics, and a net revenue-positive system.

emojicoin.fun

Memecoins have taken crypto by storm, but emojicoin.fun takes a different approach by introducing lighthearted yet financially serious speculations via memes on Aptos.

Emojicoin is a memecoin launchpad where every single coin from the platform is an emoji. Yes, you read that right. Instead of names like Fartcoin, Fwog, and Popcat, the coin names are either a single emoji or a string of emojis.

The core thesis is similar to Pump Fun: provide a neutral venue where creators can deploy coins and traders can trust the coins aren’t obvious rugs waiting to happen. As mentioned, emojicoins can be a single emoji or a string of emojis with the caveat that:

- The total string size should be under 10 bytes.

- Only emojis from the Unicode repository are valid.

Deployers need to pay 1 APT and provide a 1 APT refundable deposit (refunded when the coin exits bonding and is deployed on LP). It takes 1,000 APT of buy pressure to get an Emojicoin to a 4,500 APT market cap. At this point, the remaining supply of the coin along with the 1,000 APT are deployed into an XYK AMM pool. Like any bonding curve launchpad coin, buyers can pair their Emojicoin with APT and provide liquidity on the AMM.

Emojicoins are canonical, meaning there can only be one coin for a given emoji or emoji string.

The ability to craft coins according to trending ideas and narratives is limited, which means hitting the same scale as other launchpads is a tall feat. Emojicoin could, in theory, support the onset of an AI-representative memecoin like GOAT. But it’s extremely unlikely that the rigid mandate of “emojis only” will result in a similar frenzy.

The reason we wanted to surface Emojicoin is because it’s a fresh, community-centric idea that could be pivotal in bringing the chain’s community together. Aptos does not have a lot of high-quality native asset issuance. Emojicoin serves an important, but perhaps temporary, gap in the market. Emojicoin’s Arena feature, for instance, pits one coin against another for a 20 hour period. The Arena is what the Emojicoin team aptly describes as “attention warfare with real stakes”.

Given how quickly narratives and capital flows can shift in crypto, it wouldn’t be a complete surprise to see a few coins on the platform break out with anomalous volumes and attention.

Early Projects Spotlight

The projects in the section above have been on Aptos’ mainnet for a considerable amount of time.

For relatively new projects or those that haven’t been deployed to mainnet yet, it’s difficult to gauge what’s real and what isn’t. But a few projects from this nascent category caught our attention: Moar Markets, Mirage Protocol, and Ekiden.

Moar Market

Moar Market is a pure-play leverage primitive on Aptos. Users can borrow up to 15x against their collateral, deploying both the loan and the collateral into yield-bearing strategies or for margin trading.

The overall structure and target market are similar to Joule on Aptos and Gearbox on the EVM. Credit primitives where the collateral can be productively deployed, and a more optimistic approach to liquidations, are required to push the needle of what’s possible with onchain leverage.

Moar has its core money markets and also its own strategies. Lenders in the money market give out loans to borrowers who then deploy them into strategies. Currently, a couple of strategies on the Moar frontend include:

- APT-USDC 50/50 LP on Hyperion’s 0.05% pool. Max APY of 630% and a base APY of 170% against a 10.56% borrow rate. A max leverage of 4x is applicable. The strategy takes APT or USDC collateral, borrows the remaining necessary APT and USDC, and deploys it into Hyperion’s concentrated liquidity pool. Users can pick an aggressive range (+/-5%), a conservative range (+/-10%), or the full range (lower APY, but less risk).

- USDT-USDC 50/50 LP on Hyperion’s 0.01% pool. Max APY of 160% and a base APY of 28% against an 8.7% borrow rate. A max leverage of 9x is applicable. The strategy takes USDT or USDC collateral, borrows the remaining necessary USDT/C, and deploys it into Hyperion’s concentrated liquidity pool. Since there is much lower volatility risk, the aggressive range option is +/- 0.01% (1 basis point) and the conservative option is +/- 0.1% (10 bps). Full range is also an option, but wouldn’t make much sense.

Moar has a distinct advantage over the competition for margin trading. Unlike Aries, whose spot margin trading capabilities are limited to under 2x, Moar is able to support a higher degree of leverage – and do so safely.

To understand why it can safely allow for higher leverage margin trading, we can look at the example of Gearbox, which has found a fair degree of traction on Ethereum. Given Ethereum’s infrastructural constraints, high leverage margin trading on Gearbox has always been a bit of a pipe dream. 11-13 second block times meant that liquidations couldn’t happen at the required speed. As a result, Gearbox’s core focus stayed with leveraged strategies.

Aptos’ block times, performance, and ability to support extremely quick liquidations as prices change mean that credit primitives like Moar and Joule are not tied to the same constraints. And as a result, there is a larger opportunity to support 2-5x spot margin trading – even for volatile assets.

Mirage Protocol

Of all the protocols we have looked at on Aptos, Mirage might just be the most exciting in terms of vision and roadmap.

Mirage is the marriage between a CDP-stablecoin protocol and a perps DEX. Users can mint Mirage’s native stablecoin – mUSD – as an overcollateralized debt obligation against USDC, APT, and hopefully other high-quality collateral in the future. At this point, it starts to resemble MakerDAO more than anything else.

But Mirage also has a perpetuals DEX. And this is what helps the stablecoin’s utility really come to life. mUSD is the margin asset to trade Mirage’s perps. The core liquidity model for perps is a virtual price liquidity pool, similar to GMX or Merkle. And the approach to fees and slippage (maker/taker depending on whether it contributes to or reduces skew) is also similar.

However, the liquidity pool is structured very differently. Rather than having LPs come and deposit assets to form the global counterparty to all trades, Mirage’s mUSD minters are essentially the liquidity pool. As trader PNL grows, mUSD minters (or LPs) will see their debt grow.

Those familiar with Synthetix will see the similarities in the model. SNX stakers can mint sUSD against their SNX and cumulatively form the “global debt pool”. If traders win trades, the debt pool rises and impacts stakers on a pro-rata basis. If traders net lose on the platform, the global debt pool shrinks.

In a nutshell, users deposit collateral and mint mUSD. They can then sell it, farm with it, or trade Mirage perps with it. It is in the best interest of mUSD minters to do something that generates a yield to offset any potential increases in their proportional debt levels. However, the protocol gives them an extra boost. A portion of the fees generated from trading activity on the perps DEX is used to pay down the debt of LPs. This introduces a self-repaying loan model that can encourage people to become mUSD minters.

One of the biggest differences to Mirage’s model is the exclusive use of exogenous collateral for CDPs. Synthetix allowed those who held the native SNX token to mint stablecoins against it. The use of endogenous collateral (assets issued by the same protocol) has become a strong anti-signal in recent times.

Mirage’s token, MIRA, isn’t live yet but is mentioned in detail in the protocol’s documentation. The token will employ a veToken model with lock times ranging from 6 months to 3 years. 10% of protocol fees will be used in a buyback and burn program. veMIRA holders will earn a fixed portion of emissions. Keep in mind, Mirage as a protocol is still very early, so all of this could be subject to change.

To sum it up, Mirage is one of the more exciting pieces of mechanism design on Aptos and the Move ecosystem. If the team can execute on the vision well, it will create a flywheel that tackles two of crypto’s highest PMF uses: perpetuals and stablecoins.

Ekiden

Ekiden is a new hybrid orderbook exchange being built on Aptos, designed to meet the requirements of both high-frequency traders and institutional players. Its infrastructure design combines an off-chain CLOB with secure on-chain finality, giving traders high-speed execution alongside transparent, trustless settlement.

Ekiden’s is expected to launch on mainnet in the next couple of months. For now, Ekiden has a private waitlist that users can register for. The focus at launch will be on perpetual markets, with spot trading to follow later on. Notably, they are offering a 0% maker fee to attract early liquidity providers and market makers, though this may change over time.

A key differentiator for Ekiden is its execution speed. By leveraging Aptos’ technical design and batching system, Ekiden targets a trade execution time under only 20 milliseconds – very competitive with CEXs and much faster than most other DEXs.

As product depth and liquidity increase on the platform, Ekiden could position itself as the go-to platform for both leveraged perps and spot trading on Aptos. The goal is to capture trading flow that would otherwise remain on CEXs or other DEXs, offering a seamless trading experience within the Move ecosystem.

That said, with the project still gated behind a waitlist and its token economics yet to be disclosed, Ekiden remains a very early-stage bet. It has the potential to become a top trading venue on Aptos, but the proof is in the pudding. Before a performant trading experience is live on mainnet, it’s too early to call. The next few months should reveal whether the Ekiden team can deliver on its ambitious roadmap.

Emerging Opportunities on Aptos

The Aptos tech stack boasts all-around performance measures, the MoveVM offers developers a much more secure base to build their ideas on, and there are a variety of UX-centric tech features (outlined in our previous Aptos report) that seek to make using the chain butter smooth for users.

While in theory, Aptos’ technology could comfortably support a wide range of sectors and ideas, we believe there are a few core narratives that are of utmost importance in Aptos’ aspirations to become the premier DeFi chain.

Payments

Native USDT launched on Aptos in Q3 2024, followed by native USDC and Circle’s Cross Chain Transfer Protocol (CCTP) in Jan. 2025. Ethena’s stablecoin, USDe, also came on board in Feb., bringing fully on-chain and delta-neutral stabelcoin yields to the ecosystem. USDT currently comprises nearly 70% of all stablecoins on Aptos. With all of the stablecoin giants offering native support and Aptos’ tech merits, there is an opportunity to conjure up a perfect storm in the payments and RWA issuance landscape.

Payments are one of the biggest onchain use cases that just haven’t materialized in the desired way yet. Scale and tech stack have been one problem, but blockchains have made significant progress in overcoming that hurdle. The second problem, and more important one, has been the ability to create distribution at the same scale as FinTechs like Venmo, PayPal, and others. The closest thing to crypto’s PayPal is Coinbase Commerce, and even that serves a small cut of online merchants.

In the past, payments were tough because even the scale required to process transactions from a few hundred thousand users was not viable. The core opportunity for Aptos in payments comes down to the tech stack’s ability to handle the load from a successful payments app.

From that perspective, it is an obvious opportunity.

However, nailing distribution is a completely different ball game. For starters, users should be able to seamlessly spend their stablecoins. And that comes from significant business development and growth efforts focused on merchants. The payments platform itself needs to feel seamless and “not like crypto”. This requires an app that powers payments with stablecoins but does not saddle users with the baggage of holding native tokens for gas or needing a CEX to offramp.

Nailing payments will require a few key items:

- Strong support from the foundation is needed in building the app and making sure the complexities are abstracted to the highest possible degree.

- Leadership that understands the nitty gritty of cracking distribution in the traditional payments space.

- A compelling pitch for prospective merchants and a ridiculously simple path to enable stablecoin payments for them. This includes not only the ease of receiving stablecoins, but also the ease of off-ramping them or spending them for OpEx.

- A clever use of tokens and incentivization in order to first target onchain residents. It’s clear now that onchain apps first have to convince existing cohorts to use their app before expecting fresh onboardings into the user journey.

- Functional feature sets like payroll management, off-ramping options, yield accounts, and other things that can nudge folks to take their paychecks in stablecoins.

There are a handful of networks today that can support both Visa’s required throughput and also have the two most popular stablecoins natively available on the chain – and Aptos is one of those few.

Payments seem like an easy sector on the surface, but the combination of the complexity required on the backend to make things intuitive and the BizDev/sales required to make things functional for users (merchant onboarding, feature sets, etc.) makes it one of the more challenging yet rewarding use cases for crypto.

Aptos’ Next Chapter: The Rise of the Global Trading Engine

Aptos has emerged with a distinct orientation: while consumer and gaming apps are present, the ecosystem is clearly coalescing around high-frequency, capital-intensive financial applications. That focus is now materializing into a unified product vision: a native orderbook layer and execution environment purpose-built for modern markets, making Aptos the Global Trading Engine (GTE).

The native orderbook layer is based on a framework-level Central Limit Order Book (CLOB) design. With complete on-chain matching, this CLOB enforces transparency and fairness. The days of market makers covertly providing preferential order flow to contracted entities are over.

Composable in nature, this CLOB will act as the connective tissue supporting Aptos’ ecosystem with peak performance. Aptos has already achieved leading L1 block times with Zaptos and will soon fully integrate Raptr, a new consensus protocol. Combining the high throughput of DAG-based approaches with the low latency of leader-based architecture, Raptr stands to supercharge Aptos’ capabilities.

Together with Aptos’ targeted ecosystem initiatives, such as the $200 mn commitment for grants and investments for ecosystem builders, optimizations for new trading primitives, and performance upgrades, the stage is set to turn Aptos into the GTE.

If the world does fully move on-chain, every form of value transfer in the financial system will be transformed. This future requires blockchain rails that accommodate tomorrow’s demand, where all assets (stocks, treasuries, real estate, private credit, and more) are tradable on-chain, capital markets operate 24/7 without borders or intermediaries, and anyone, anywhere, can instantly and securely participate in financial activities. Here, Aptos is one of the few networks strategically positioned to fulfill the GTE vision – contingent on sustained and increasing adoption of its DeFi ecosystem.

Over the years, we have witnessed several attempts to do this with varying degrees of success. Sei went to market with this vision, though it didn’t pan out as expected. Hyperliquid went from a centrally run orderbook/matching engine with settlement on Arbitrum to an L1 with an embedded orderbook. These two represent opposite sides of the spectrum.

Hyperliquid’s GTM was to really focus on perp traders. And once they established themselves as a competitive venue for traders, they began executing on their L1 vision with HyperEVM. Sei tried to weave the whole thing together at once – before building trust with traders, market makers, and other relevant market participants.

Aptos sits rather uniquely in the middle of the spectrum. It’s a trusted and scalable L1 that can reliably handle the order load from liquid perps and spot trading; it has native USDC/USDT for margin; and it’s already home to $1 bn+ of stablecoins.

As Aptos’ ecosystem builds towards its grander vision of becoming the Global Trading Engine, we expect spot books to be developed first over other instruments. From a volume perspective, going perpetuals first would make sense. But as a new feature being integrated into a blockchain, there is a strong case to be made that the logical flow is to build spot liquidity and then derivatives.

The case for perpetuals first, however, is the current state of asset issuance on Aptos. There aren’t many interesting spot assets to trade. There are barely any natively issued, non-pegged assets on the chain trading at a market cap of over $10 mn.

The vast majority (85%+) of trading volume on the chain’s DEXs comes from USDC, USDT, and APT. Aptos is a young chain, and it takes time for projects to mature and attract significant flows to their tokens from investors. So while this is happening gradually in the background, perps provide a strong reason for traders and users to keep their capital on the chain.

Hyperliquid’s success spawned apps like Lootbase – a crypto-native version of Robinhood entirely powered by Hyperliquid’s orderbook. Aptos’ GTE should strive for similar second-order effects. With the right oracle infra, this app could theoretically offer perps on equities, commodities, and other assets that aren’t issued on blockchains. A trading app that feels like Robinhood but trades on Aptos GTE could find PMF very quickly.

And that’s down to one simple reason. An honest look at today’s onchain environment aggressively confirms the notion that people primarily want to trade assets.

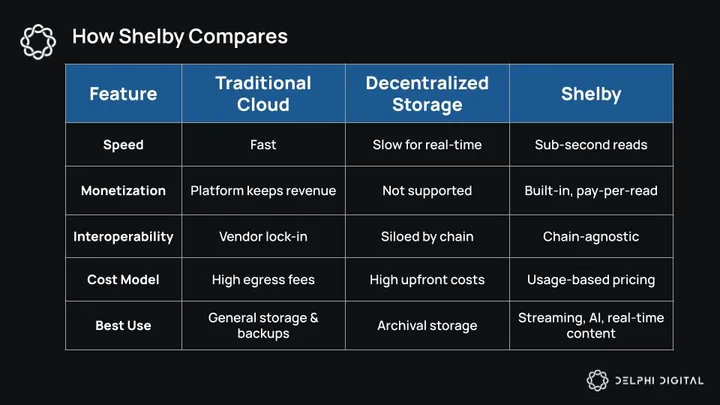

Shelby

Perhaps one of the most notable infrastructure developments in the Aptos ecosystem is Shelby – a cloud-grade, decentralized hot storage protocol co-developed by Aptos Labs and Jump Crypto. As Aptos advances its Global Trading Engine framework – aimed at enabling always-on, on-chain capital markets – Shelby introduces an additional layer to the stack: infrastructure for on-chain value creation and data delivery.

Shelby aims to fill one of the most persistent gaps in the Web3 cloud stack. Most decentralized storage is optimized for cold archival use: slow, static, and disconnected from monetization. As a result, many Web3 projects rely on centralized clouds, exposing them to opaque pricing, shifting terms, and long-term platform risk.

Instead of simply holding data, Shelby actively monetizes stored data through incentivized reads and rapid access. This design turns any file into a live revenue stream. Unlocking use cases from pay-per-view media, AI outputs, or gaming assets, this is a big step up from the cold storage model most builders are familiar with. Developers and providers can now earn from usage rather than worrying about just covering storage costs.

Shelby uses Aptos as its first settlement layer, relying on the high throughput and fast finality to coordinate reads, writes, and payments with low latency. Importantly, Shelby’s chain-agnostic design means it can ultimately serve data across multiple blockchains and not just Aptos, widening its impact.

It treats data as an economic asset: accessible in real time, priced per access, and compatible across applications. This approach introduces a new monetization layer within decentralized infrastructure, enabling value to be derived not only from trading and payments, but from data usage itself.

Shelby is currently in private waitlist mode, with early partners like Story Protocol and Metaplex exploring how to use it for data-heavy apps. This adds another piece to Aptos’ ability to serve both the financial internet and the real-time data economy.

The Path to Mainstream Success

In the bid to build a successful ecosystem, there are two boxes that need to be ticked from a product perspective:

- Build the primitives, products, and experiences that users want today. Focus on the portion of the market that has proven demand and market-fit today.

- Set the stage for founders to build next-gen products. Think about and focus on what users will want months to years down the line.

As of today, the Aptos ecosystem has made significant progress on the first item. The core primitives for DeFi have been built, and apps building on top of these primitives are starting to pop up. Stage 1 is done; stage 2 of this plan involves driving more capital (liquidity) and usage (volume) to these products.

Ethereum and Solana’s success as Layer 1s also underscores the value of building early traction with both on-chain capital owners and CEX infrastructure – an area where Aptos is still gaining ground. Ethereum has now cemented its place as the backbone of onchain finance. Even if it does not see the same level of activity as 2020-22, it’s still the largest chain by capital base. This has proven to be vital because it helped Ethereum become the main bridge between onchain capital owners and CEXs. As a result, the chain is now entrenched with both users and exchanges.

But how was Ethereum able to do this? It all boils down to one simple fact: Ethereum had the assets that users wanted to own and trade. The chain’s app layer boom led to several native tokens on the chain becoming the crypto equivalent of a household brand name; Uniswap, Aave, and Maker, among others. Ethereum became the primary issuance hub for stablecoins. Tether, which previously relied on the Omni sidechain, started doing most of its issuance across Ethereum and Tron.

Solana has a completely different story but the same outcome. Profuse asset issuance, albeit of a much lower quality, led to Solana dominating mindshare with the pure trader class. Traders chase every trend, narrative, and swing that can generate attention. Solana has ⅙ of Ethereum’s TVL but slightly exceeds it in daily DEX volume.

What Aptos is missing today are assets people genuinely want to hold and trade. Product tokens require catalysts and genuine fundamentals in order to generate volume. And while a lot of DeFi platforms on Aptos are putting up healthy numbers, there’s still something missing to get investors excited. To their credit, the Aptos Foundation does recognize this. And it’s reflected in its recent announcement of the LFM, a TGE track for Aptos ecosystem projects.

Building an ecosystem is a marathon, not a sprint. While that means success can take time, it also means that the skyscrapers of tomorrow are only possible if the foundations laid today are strong. And there is ample evidence from what we see in the ecosystem today that Aptos is largely moving in the right direction.

Overall, Aptos has set the stage with an extremely performant tech stack. The ecosystem and capital base are growing and showing glimmers of potential viral products. While there’s a long way to go in establishing itself as a top ecosystem by activity and mindshare, Aptos is cementing itself as a true contender in the bid for DeFi supremacy.

0 Comments