PACT Protocol: Rearchitecting Structured Credit for the Tokenized Era

DEC 08, 2025 • 32 Min Read

Report Summary

Traditional Credit Infrastructure Is Broken – Global credit markets rely on manual verification, fragmented data, and slow reconciliation, with high costs ($200k–$1M diligence fees) and delayed covenant enforcement creating months-long blind spots.

First-Gen Tokenization Failed – Early protocols (Goldfinch) only tokenized loans while keeping origination and monitoring off-chain, leading to serious failures like the Tugende default where covenant breaches went undetected for 6–9 months.

PACT Rebuilds Credit Fully On-Chain – Unlike tokenization, PACT originates, services, and enforces credit entirely on-chain using Loan NFTs containing full loan data, live schedules, and automated covenant logic for real-time reconciliation and instant enforcement.

Composable Structured Credit Stack – Loan NFTs roll into loan books → facilities → credit funds → CLOs, with borrowing-base logic, tranching, and waterfalls running natively on-chain, eliminating trustees and intermediaries.

“Farm to Table” Origination Model – Borrower loans originate directly on Aptos (not mirrored), making on-chain state the single source of truth with embedded SDKs integrating into fintech apps for native on-chain operations.

Aptos Enables Institutional-Grade Performance – Sub-second finality (130–150ms), high throughput, $1.5B stablecoin TVL ($540M from BlackRock), and Move language safety guarantees provide infrastructure required for real-time credit at scale.

Proven Market Traction – $1.9B in originations across 900k+ borrowers with institutional allocators like Tiberia Capital deploying regulated capital demonstrates the model works at real scale, not just pilots.

Structural Redesign with Real Constraints – PACT offers faster settlement, lower costs, real-time risk monitoring, and emerging market access toward onboarding the $300T debt market—but faces regulatory fragmentation, currency mismatch, and integration complexity as scaling challenges.

Note: Key technical and credit terms in italics are defined in the glossary at the end of the report.

Introduction

Global credit markets hold more than $300 trillion in outstanding debt, yet the systems behind them operate on infrastructure built decades ago. Every loan, bond, and structured product depends on a web of intermediaries, manual checks, and fragmented databases that make credit expensive, slow, and inaccessible to large parts of the world.

The inefficiencies are structural, and the risks that come with them are real. Verification happens over email, cash movements are reconciled in spreadsheets, and covenants are enforced only at quarterly reviews. Each layer adds cost and delay, while idle capital accumulates between distribution dates. As recent double-pledging cases in traditional credit have shown, fragmented oversight can create genuine exposure, not just operational friction. For smaller facilities, these bottlenecks make structured credit nearly impossible to execute efficiently.

Multiple intermediaries and manual processes create prohibitive costs for smaller facilities.

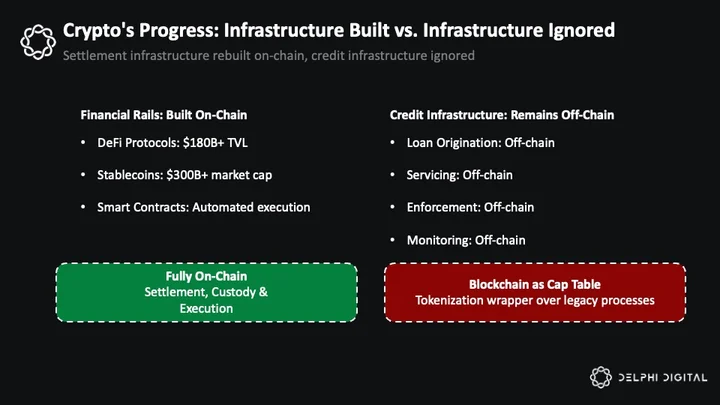

Meanwhile, crypto has already rebuilt the rails for financial settlement. DeFi protocols process billions in daily volume, stablecoins have become a $300 billion market, and smart contracts execute financial logic in real time.

Yet real-world credit remains largely untouched. Most projects have focused on tokenizing existing instruments rather than rethinking how credit itself is originated, serviced, and enforced. The result is blockchain used as a record-keeping layer rather than as actual credit infrastructure. In most implementations, it functions like a database for private credit, not the operating system that originates, services, and enforces credit on-chain.

PACT Protocol takes a different approach. Rather than using blockchain as a passive record-keeping layer, it embeds compute, data, and execution directly into the credit lifecycle. Built on Aptos, PACT provides a fully on-chain system for origination, monitoring, and enforcement where repayment flows, covenant checks, and waterfall logic execute natively. It replaces intermediaries with programmable infrastructure and turns what was once a fragmented process into a single operating system for structured credit. Where tokenization merely wrapped off-chain credit processes, PACT rebuilds those processes on-chain from the ground up.

Critically, this infrastructure extends beyond the top of the funnel. Through embedded SDKs in originator back-office systems and borrower-facing mobile apps, every participant interacts with the chain directly. Stablecoin rails connect investors, facilities, originators, and end-borrowers end-to-end, eliminating reconciliation gaps and solving the in/out cash flow problem that has limited prior on-chain credit models.

Exploring Traditional Structured Credit

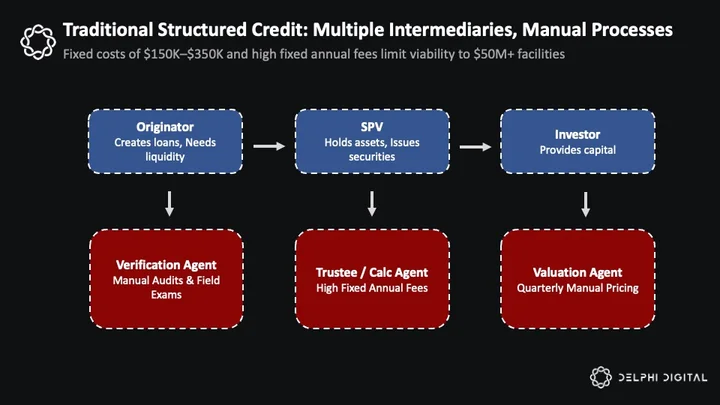

To understand how PACT differs, let’s revisit how traditional structured credit works. At its core, the system exists to connect three parties: those who originate loans (originators), those who hold them (SPVs), and those who invest in them (investors). The problem is that every step in this chain depends on manual oversight and specialized intermediaries, each adding cost and delay.

Traditional structured credit depends on multiple intermediaries for origination, verification, and monitoring, each adding fees and friction that limit smaller facilities.

The process begins with the originator, such as a bank, fintech lender, or finance company that creates loans. These firms generate receivables but often lack the balance sheet to retain them while scaling their loan books, which requires constant equity raising that is both expensive and dilutive. To free up capital, they pledge or sell the loans into a Special Purpose Vehicle (SPV), a bankruptcy-remote entity that isolates the assets from the originator’s liabilities and enables the loans to be used as collateral to draw cash against the future receivables.

Before that transfer happens, verification agents audit the portfolio over several weeks. They review borrower documentation, confirm underwriting standards, and test collateral quality to ensure the loans exist, the details are accurate, and the assets fall within the credit box defined by the parties.

Why This System Limits Viability to Large Facilities

The costs associated with this initial due diligence involving the verification agents are highly dependent on the portfolio size and review scope. At a high level, these break down across two components: upfront due diligence fees and ongoing verification fees.

Principal Financial (PF) compiles industry data, providing a good understanding of benchmark costs. According to PF, the range for total upfront diligence fees roughly starts at $200,000 and can exceed $1m¹ with increased deal size and scope. Ongoing verification fees kick in post-close and include a monthly fee benchmarked at 1-2 bps per year¹ In addition, variable fees are charged, typically totaling $200,000 per year¹.

Once the SPV holds the assets, it issues securities backed by the loan pool and a network of intermediaries manages the structure. Trustees safeguard investor rights and enforce covenants, adding another layer of costs. While this fee is highly variable, it generally follows a declining scale² favoring large portfolios.

Calculation agents compute payment waterfalls and coverage ratios. Here, fees are typically included in the trustee fees but can be charged separately for complex waterfall calculations. Valuation agents assess collateral values quarterly, adding yet another fee layer.

Legal counsel adds further friction. Legal documentation that governs a typical structure can exceed 300 pages, requiring a high degree of expertise to structure and execute³. This translates to more upfront costs for SPV formation and an annual retainer for ongoing compliance. Depending on the jurisdiction, SPVs in securitization generally also require one or more independent directors. Annual salaries for these directors fall between $50,000 to $100,0004.

Finally, investors purchase the securities, providing capital in exchange for yield. Their confidence depends on the reporting accuracy and coordination of every intermediary along the way.

The big picture is the same across almost all fee layers: the system favors large institutional portfolios. High upfront costs and annual fees make smaller facilities uneconomical.

Beyond that, the industry is plagued by several structural drawbacks. Covenant enforcement is periodic rather than continuous. When a borrowing base calculation shows that collateral has fallen below required thresholds, the shortfall often exists for weeks before detection.

Trustees depend on monthly or quarterly reports from originators, creating long periods where facilities operate out of compliance without consequence. Cash management introduces similar lag. Loan repayments collected from borrowers sit in holding accounts until scheduled distribution dates.

Manual reconciliation is the main bottleneck. Trustees and calculation agents must verify amounts before executing transfers, leaving capital idle while investors wait for distributions. In stablecoin-based systems, this capital can flow directly to investors without currency conversion delays or cross-border settlement friction.

The cost structure compounds these delays. Trustees charge fees regardless of performance. Calculation agents, valuation agents, auditors, and legal counsel each contribute additional overhead. These costs must be absorbed by the loan portfolio, creating a minimum scale threshold that excludes smaller originators.

Scale ultimately determines viability. For microfinance lenders already operating on thin margins, this structure removes a sustainable path to profitability. And smaller or emerging market lenders are often simply priced out.

Evolution of Onchain Structured Credit: Where Prior Solutions Fell Short

The idea of bringing credit on-chain has existed since the earliest days of DeFi. Protocols like Goldfinch set out to connect traditional credit markets with blockchain infrastructure, raising hundreds of millions of dollars and originating loans to real-world borrowers. These projects represented genuine progress, but they made one critical architectural decision that limited their potential: they tokenized access to yield while leaving most of the underlying credit infrastructure off-chain.

Goldfinch pioneered asset-backed lending to emerging market borrowers, linking DeFi liquidity with fintechs and credit funds across Africa, Latin America, and Southeast Asia. The protocol employed a model of “trust through consensus,” where backers assessed the borrower’s creditworthiness and supplied first-loss capital. A senior pool then automatically diversified across approved borrower pools.

The protocol achieved significant scale, originating more than $100 million in loans. Yet the underlying architecture remained largely unchanged from traditional finance. Stablecoins are borrowed from on-chain pools, converted to fiat, and capital is then deployed to end borrowers through entirely off-chain operations. Origination, servicing, collateral monitoring, and covenant enforcement were all handled through legal agreements and manual processes. Blockchain primarily served as a fundraising and settlement layer, functioning as a more efficient cap table rather than as the foundation of a truly on-chain credit system.

The Tugende Collapse: When Tokenization Isn’t Enough

The Tugende incident illustrates why tokenization alone cannot solve the challenges of bringing credit on-chain.

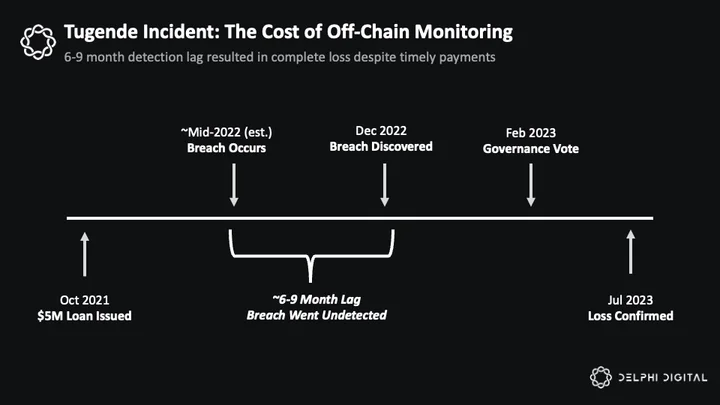

In October 2021, Goldfinch extended a $5 million loan to Tugende Kenya, a motorcycle financing company. The facility was secured by off-chain collateral, including cash, inventory, and loan receivables, and contained standard covenants such as a loan-to-value ratio below 80 percent and minimum tangible net worth requirements. Tugende made every interest payment on time. By traditional metrics, the loan appeared to be performing.

Goldfinch’s $5M Tugende facility collapsed after a six- to nine-month covenant breach went undetected due to off-chain monitoring and delayed reporting

In December 2022, during a routine quarterly review, Goldfinch discovered that Tugende Kenya had made an unauthorized $1.9 million intercompany loan to its struggling Ugandan affiliate months earlier. The transaction breached multiple covenants but went undetected because monitoring relied on periodic reports rather than real-time visibility.

By the time the violation surfaced, capital had been diverted, the loan portfolio had deteriorated, and contagion from the Ugandan affiliate had spread. Despite appointing a global law firm and months of restructuring negotiations, the facility ultimately resulted in a complete write-down of the $5 million principal.

The issue was not credit quality or borrower intent. Tugende had a decade of operational history, strong institutional backing from Toyota’s venture arm and the US Development Finance Corporation, and a genuine interest in resolving the breach. The unauthorized intercompany transfer represented misuse of funds that violated covenants, but quarterly reporting meant the violation went undetected for months. The failure to detect this fraud was architectural. Legal enforcement required lengthy, expensive remediation with no guarantee of recovery.

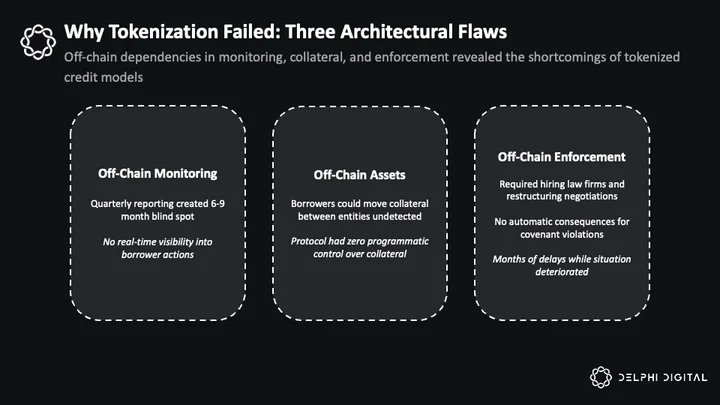

Why tokenization failed: three architectural flaws that allowed fraud to go undetected. Off-chain monitoring, assets, and enforcement left critical risks unresolved.

The blockchain recorded payments to protocol investors but had no insight into how borrowers used the capital or whether they complied with covenants. Without fully on-chain data, payment flows, and enforcement logic working together, tokenization reduced risk only at the fundraising layer. Yet, the core credit functions remained exposed to traditional inefficiencies.

PACT’s Approach to Rebuilding Structured Credit On-Chain

PACT’s approach diverges from tokenization-first protocols in one crucial way: the entire collateral chain originates directly on-chain, from individual microloans up through structured facilities, rather than tokenizing company-level debentures after the fact. This architectural decision reshapes every layer of the system, enabling capabilities that tokenization wrappers cannot replicate.

Importantly, automation in PACT does not replace credit judgment. Fund managers still select originators, set underwriting standards, and design facility structures. The protocol’s role is to enforce those decisions with consistent, code-driven execution, not to assume discretion. This distinction is critical for institutional allocators who require clear separation between underwriting and automated settlement.

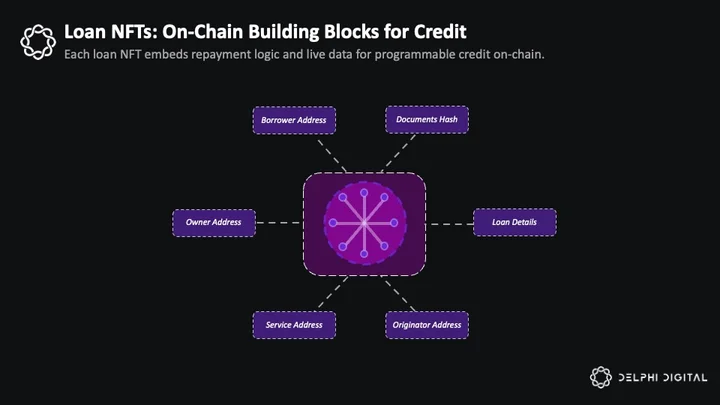

Loan NFTs: Programmable Credit Primitives

At the base layer, each loan in PACT is minted as a non-fungible token (NFT) with embedded logic and live metadata. Every loan NFT carries a unique public identifier, similar to a CUSIP in traditional markets, along with borrower data, repayment schedules, collateral details, and performance metrics.

When a borrower makes a payment, the NFT updates instantly to reflect the new principal balance, accrued interest, and payment history. The payment flows directly to whoever holds the loan NFT – whether an individual investor, a loan book aggregating multiple loans, or a facility that has pooled the loan as collateral. If a payment is late, delinquency status changes automatically.

Fee triggers, covenant breaches, and amortization adjustments execute through smart-contract logic without manual intervention. The NFT enforces the loan’s terms directly and prevents unauthorized modification.

Visualization of a loan NFT’s on-chain data structure, linking borrower, servicer, and originator information to enforce terms programmatically.

This design improves transparency and efficiency while reducing risk meaningfully by enabling four core properties essential for composable credit markets:

- Uniqueness: Each loan maintains its own identity and attributes for granular tracking at the asset level. This prevents double pledging. A loan NFT can only be held by one entity at a time, ensuring collateral isn’t used in multiple facilities simultaneously.

- Transferability: Loans can move between whitelisted wallets while preserving all associated rights and obligations. The payment routing automatically follows ownership – whoever holds the NFT receives the cash flows, functioning like a plumbing network that routes money to the current sink (owner) without manual intervention.

- Real-time reconciliation: Payments are updated against amortization schedules immediately rather than through end-of-month processes. This enables daily borrowing base checks, daily waterfall runs, and real-time covenant monitoring at the facility level, rather than monthly or quarterly snapshots.

- Composability: Loan NFTs serve as building blocks that can be combined into higher-order financial structures without losing their individual characteristics.

From Loans to Structured Products: The Composable Stack

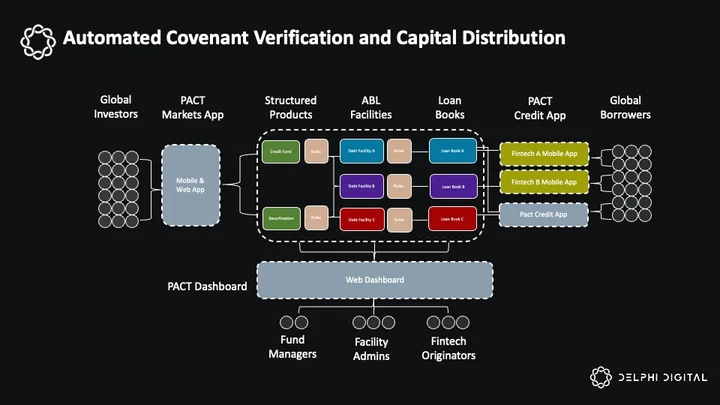

The loan NFT primitive enables PACT to construct the entire structured credit stack on-chain. These programmable loan NFTs form the foundation for PACT’s full on-chain structured credit stack.

Loan books aggregate multiple NFTs and track collective repayment flows, functioning as on-chain loan portfolios. Initially owned by the fintech originators who created the underlying loans, individual loans from these books (or entire loan books) can then be pledged as collateral to credit facilities that implement borrowing-base logic, concentration limits, eligibility criteria, and payment waterfalls entirely through code.

In traditional finance, an asset-backed lending facility relies on manual oversight. A calculation agent reviews portfolios monthly or quarterly to determine which loans qualify as eligible collateral and whether the facility remains within covenant limits. Breaches or deterioration often go unnoticed for weeks.

In PACT’s model, these same rules execute automatically. When a fintech originator requests a draw from their facility, the contract evaluates each loan NFT against the facility’s eligibility criteria in real time. Loans that breach limits or underperform are excluded immediately. If the remaining collateral cannot support the requested draw, the transaction fails on-chain.

PACT’s ecosystem illustrates how capital flows from global investors through structured products, facilities, and loan books to end borrowers via fintech apps.

PACT’s Fully On-Chain Credit Infrastructure

The facility tokens representing these debt facilities can be aggregated into credit funds and collateralized loan obligations (CLOs) with multiple tranches, each carrying distinct seniority and payment rights. Facilities themselves are also tranched. All have at minimum an equity tranche (originator) and senior tranche (capital provider), with some including additional junior slices.

Senior tranche holders receive distributions before junior investors, enforced automatically by the waterfall logic in PACT’s smart contracts. Capital calls, distributions, and covenant checks execute without trustees, calculation agents, or manual intermediaries. The entire structured credit stack functions as composable code rather than a web of legal agreements.

Onchain-Native: Farm to Table RWAs

The difference between tokenizing existing loans and originating loans directly on-chain may sound trivial, but it is operationally decisive. Tokenization treats the blockchain as a registry for assets that already exist elsewhere. Loans are still created, serviced, and enforced through traditional systems, with tokens representing economic claims on securities created 2-3 levels away from the underlying loans.

PACT’s model reverses this. When a borrower receives a loan through a fintech partner integrated with PACT, the loan originates as an NFT on Aptos. The borrower’s documentation is stored in a UETA-compliant vault, with access tied to on-chain ownership. Repayment schedules, interest calculations, and payment distributions are encoded directly in smart contracts from the start. There is no off-chain loan being mirrored on-chain. The on-chain NFT is the loan itself.

This is what PACT calls “farm to table RWAs”, assets that are native to blockchain infrastructure rather than ported onto it. Because loans originate and operate entirely on-chain, there is no reconciliation gap between blockchain state and off-chain records. When a borrower makes a payment, the transaction updates the NFT in real time, triggers waterfall distributions, and adjusts covenant metrics automatically. PACT does not require oracles to verify off-chain events because every event occurs on-chain from origination through repayment.

Embedded Compliance and Identity

Operating a permissionless credit protocol introduces clear regulatory challenges. PACT handles enforcement at the smart-contract level, but compliance itself is not embedded in the protocol. Instead, it is addressed through off-chain tooling built on top of PACT by ecosystem contributors, including Pact Labs, which builds apps, wallets, SDKs, and dashboards that let participants meet KYC, whitelisting, and operational requirements when needed. The protocol’s contracts remain public, transparent, and tamper-proof, while identity checks and monitoring occur through external systems that integrate with PACT rather than existing inside it.

Different participants access the system through different interfaces depending on their role. Some end investors use the PACT Wallet, which requires KYC verification through an external compliance partner. Managers access a web dashboard, originators integrate via SDK, and borrowers interact through originator mobile apps. Once KYC-verified through their respective interface, the wallet address is added to a global whitelist maintained on-chain.

The whitelisting structure is hierarchical. Originators can whitelist end borrowers, managers can whitelist investors and originators, and PACT Labs can whitelist managers, originators, and investors. The structured credit contracts (such as facility contracts) that hold loan NFTs are also whitelisted, enabling them to receive and manage collateral.

Smart contracts then enforce compliance directly. Loan NFTs, facility tokens, and fund shares can only be transferred between whitelisted addresses. Any attempt to send assets to an unauthorized wallet fails automatically.

In practice, this compliance model is anchored by deep technical integration at the originator level. PACT’s SDK is embedded directly into partners’ back-office systems and Android mobile apps, allowing borrower actions, repayments, draw requests, and loan signatures to be initiated and signed on-chain at the source. Every borrower receives an on-chain stablecoin wallet, and all servicing flows pass through these wallets, ensuring that origination, collections, and covenant checks reference the same on-chain state without manual reconciliation. This removes the “garbage in/garbage out” problem common in hybrid systems where protocols depend on delayed or trusted off-chain reporting.

This restriction is built into the protocol itself, enforced by the Aptos validator network, not enforced by PACT Labs or any off-chain administrator. Even if a user bypassed the interface, transfers to non-compliant wallets would be rejected by the underlying contracts.

Real-Time Visibility and Automated Execution

The combination of on-chain origination, programmable NFTs, and automated enforcement enables two key capabilities: real-time transparency and continuous execution of complex credit logic.

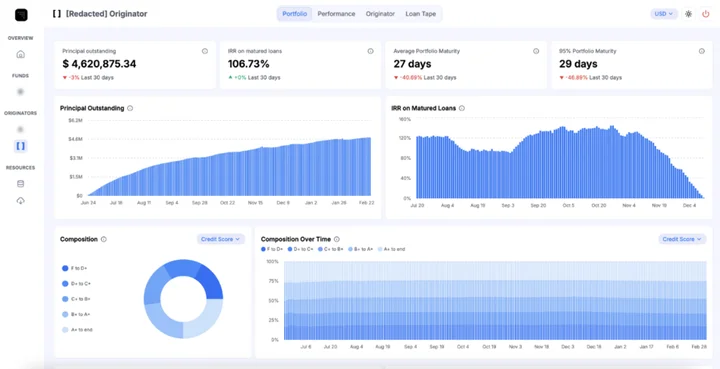

Example of Pact’s on-chain analytics dashboard used by fund and facility managers to monitor live repayment, maturity, and covenant metrics across active facilities.

Every loan’s state is visible on-chain at any time. Fund managers and facility administrators can query live performance data such as repayment schedules, covenant ratios, delinquency rates, and coverage metrics without waiting for monthly reports. Because the blockchain is public, anyone can independently audit this data by examining past payment history, verifying loan terms, and comparing reported metrics to on-chain reality. This transparency is possible in traditional ABL software, but the key difference is that PACT’s on-chain infrastructure enables external verification rather than requiring trust in a single data provider.

Execution also happens automatically. If a facility’s aggregate loan-to-value ratio breaches a covenant threshold, the smart contract can restrict new draws, increase interest rates, or trigger prepayments according to predefined terms. When borrower payments arrive, the protocol executes the waterfall instantly, allocating funds to senior tranches, reserve accounts, and equity holders in the correct order without manual calculation or distribution steps.

Each stage of Pact’s lending stack validates collateral and covenant compliance in real time, with stablecoins flowing through the entire system.

Automation does not eliminate human judgment in credit origination or structuring. Fund managers still choose which originators to finance and how to design facilities, but once those parameters are encoded in smart contracts, execution occurs automatically with consistent, code-enforced execution instead of human discretion.

Aptos: Infrastructure for Institutional-Grade Credit

Scaling On-Chain Credit: Institutional Demand Meets Infrastructure Limits

PACT’s growth shows that this model operates at institutional scale. The protocol has facilitated $1.9 billion in total loan originations, with $669 million currently outstanding across more than 900,000 total borrowers.

Active borrowers (those who made a payment in the last month) range between 150,000 to 250,000. Loan volume has nearly doubled in 2025, driven by institutional capital deployment through Tiberia and expanding fintech integrations in emerging markets.

PACT has originated 1.9B dollars in loans on-chain, doubling volumes in 2025 as institutional deployment and fintech integrations expand.

Sustaining this level of throughput and real-time processing requires an execution environment built for institutional scale.

PACT’s architecture makes specific technical demands that narrow the field of viable blockchain platforms. Real-time covenant enforcement across thousands of loans, instant waterfall distributions, and continuous collateral verification require sustained high throughput without degradation under load. Sub-second finality is not a luxury when borrowers expect instant settlement and facility draws need immediate execution. At scale, technical reliability becomes critical to operations.

From Scale to Execution: Why PACT Chose Aptos

Aptos delivers on these requirements through architectural choices outlined in our earlier infrastructure report. Its pipelined design parallelizes consensus, execution, storage, and certification, optimizing the processing stack rather than just transaction execution. The result is consistent sub-second finality and block times around 130-150 milliseconds, even under the variable loads typical of credit operations.

Aptos processes ~$55B in monthly stablecoin volume across more than 100M transactions, peaking near $68B in mid-2025. Sustained throughput at this scale demonstrates platform readiness for real-time credit settlement.

The network’s performance is most visible in its stablecoin settlement layer. Aptos now routinely processes over $55 billion in monthly stablecoin volume across more than 100 million transactions. This is sustained, real-world capacity that mirrors the settlement activity credit markets demand. When multiple fintechs initiate facility draws or thousands of repayments occur simultaneously, performance remains stable because the infrastructure already handles comparable transaction loads daily.

Aptos hosts $1.5B in stablecoin TVL, including $540M in BlackRock’s BUIDL fund, anchoring institutional liquidity for credit protocols.

Aptos provides the liquidity base that credit markets need to scale. Its stablecoin ecosystem holds over $1.5 billion in TVL across native USDC and USDT pools, allowing instant settlement without the security trade-offs of bridged assets. Native issuance means these stablecoins are minted and redeemed directly on Aptos. This helps ensure deep, reliable liquidity for institutional applications.

Roughly $540 million of that capital sits in BlackRock’s BUIDL fund, a tokenized money market fund backed by U.S. Treasuries and repo agreements. BlackRock’s presence signals confidence in Aptos’s technical reliability and regulatory posture, establishing it as one of the few blockchains ready to host institutional-grade settlement rails.

The technical stack reinforces that positioning. Move, Aptos’s programming language, enforces strict safety guarantees at the base layer. Assets are treated as unique primitives that can’t be duplicated or destroyed, a design choice that eliminates entire categories of smart contract risk. For PACT, that means complex waterfall logic, borrowing base calculations, and covenant enforcement can execute on-chain with the precision required for institutional lending.

This combination of speed, safety, and credibility is attracting serious players. Franklin Templeton’s tokenized funds, Apollo’s private credit products, and Aptos Ascend (developed with Microsoft, Brevan Howard, and SK Telecom) all demonstrate the network’s readiness for regulated finance. For managers like Tiberia Capital, which allocates hundreds of millions toward emerging market credit, infrastructure credibility directly informs allocation decisions.

Together, Aptos’s throughput, design, and institutional validation make it a credible foundation for structured credit and a pathway to eventually bring parts of the $300 trillion debt market on-chain.

Evaluating Competing Models in On-Chain Credit

Earlier, we outlined how traditional structured credit relies on manual processes, intermediaries, and delayed reconciliation while featuring countless cost layers that make small facilities uneconomical. Blockchain technology, in theory, should eliminate these bottlenecks. Yet despite years of experimentation, most attempts to bring credit on-chain have replicated the same inefficiencies rather than resolving them.

The on-chain credit market has seen multiple approaches trying to merge traditional finance with blockchain infrastructure. Each made incremental progress, but none rebuilt the system from first principles. By understanding where these efforts stalled, we can clarify why PACT represents a structural, not cosmetic, redesign.

The Tokenization Wrapper Problem

Most on-chain credit platforms function as refinancing layers rather than native lending systems. Goldfinch and Centrifuge exemplify this model by tokenizing existing off-chain debt and connecting it to DeFi liquidity. But the underlying origination, servicing, and enforcement remain dependent on traditional intermediaries.

Goldfinch has focused on institutional borrowers in emerging markets, syndicating loans above $1 million through tokenized pools. In practice, the protocol refinances debentures rather than enabling on-chain native lending capacity. Monitoring and enforcement occur through periodic reviews rather than automated systems.

The Tugende default illustrated the cost of this architecture. Covenant breaches went undetected for six to nine months, ultimately resulting in a $5 million write-off despite the borrower making timely payments. This was not an operational mistake but an architectural failure since fraud went undetected for months. Without rebuilding the monitoring and enforcement stack, tokenization simply recreates TradFi’s latency and opacity on-chain.

Regulatory friction compounded the issue. Goldfinch’s FIDU token faced SEC scrutiny for potential securities violations, creating uncertainty that weighed on protocol activity and token performance. Together, these constraints exposed the limits of tokenizing existing credit structures without redesigning them.

Centrifuge has taken a similar approach, enabling asset originators to refinance portfolios through DeFi. The platform has achieved institutional adoption but continues to rely on off-chain origination and servicing. Risk management, compliance, and borrower operations all remain external to the blockchain, limiting scalability and real-world impact. In recent years, Centrifuge has shifted its focus toward other RWA categories such as T-bills, where its architecture has proven most sustainable.

The Market Mismatch Problem

Figure Technologies demonstrates another limitation, targeting markets where blockchain creates marginal improvement. The company applies distributed ledger infrastructure to US home equity loans, a mature market already saturated with capital, automation, and regulation.

Blockchain primarily serves as a record-keeping enhancement here. The result is an efficiency upgrade rather than a change in how risk is monitored or enforced. Origination, servicing, and securitization remain conventional. While Figure’s regulatory standing and transaction volume validate blockchain’s feasibility, they do not strictly demonstrate blockchain’s necessity.

Maple Finance reveals a different form of constraint. The protocol provides unsecured, pool-based lending to crypto-native institutions like trading firms and market makers and has facilitated meaningful on-chain volume. But Maple’s model depends on off-chain underwriting and monitoring performed by Pool Delegates, with borrower diligence, collateral checks, and covenant oversight happening outside the protocol. “Real-time monitoring” is operational rather than on-chain, requiring trust in Maple’s team rather than automated enforcement.

As a result, Maple is effective for its intended institutional borrower segment but is not designed for asset-level collateral verification or structured credit use cases that require on-chain lifecycle management.

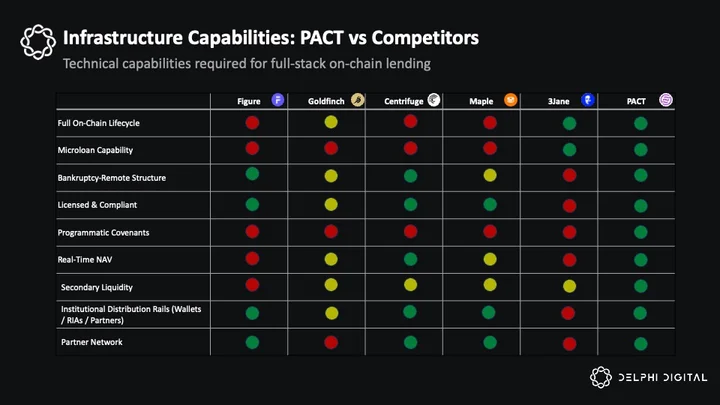

The Architecture Advantage: Why PACT Scales

PACT combines four elements that no competitor has yet replicated: full-stack on-chain infrastructure, real transparency, an emerging market focus, and comprehensive compliance frameworks. Together, these pillars allow PACT to operate as a self-contained credit system rather than a tokenization layer built on top of traditional infrastructure.

Infrastructure Depth

Infrastructure depth matters because it enables operations competitors cannot copy. When Goldfinch’s quarterly reporting created long detection lags for covenant breaches, the issue wasn’t just diligence, it was architectural. Tokenizing existing credit without rebuilding the monitoring and enforcement stack means inheriting the same limitations that make traditional finance slow and opaque.

PACT’s automated disbursement rules, automated waterfall execution, collection account segregation, and instant cash sweeps remove these frictions by keeping the entire credit lifecycle on-chain from origination through repayment.

Comparison of technical capabilities across leading credit protocols. PACT demonstrates the broadest implementation coverage, spanning microloan servicing, real-time NAV tracking, and programmable covenant management.

This full-stack approach extends to collateral verification, waterfall distributions, and secondary market liquidity. When a borrower makes a payment, the system immediately updates loan NFT metadata, recalculates facility-level metrics, executes waterfall logic across multiple tranches, and reflects changes in tokenized positions. Competitors using blockchain for syndication only can’t achieve this operational tempo because the underlying assets and their associated cash flows remain off-chain.

This architecture extends beyond repayment logic to collateral verification, waterfall distributions, and secondary market liquidity. When originators add new loans to a facility, the system verifies eligibility against borrowing base criteria, checks concentration limits, and updates available capacity automatically. When payments arrive, the protocol executes waterfall logic across tranches, routes cash to collection accounts, and triggers sweeps to investors based on facility terms. Actions that competitors relying on off-chain processes cannot mirror.

Market Focus

Emerging market microloans represent the segment where blockchain creates the greatest impact. Figure’s US home equity market has limited improvement potential from decentralized infrastructure. PACT’s $50 average loan size serving 900,000+ unbanked individuals addresses populations where traditional banking infrastructure either doesn’t exist or operates with prohibitive economics.

The technology enables access rather than marginally improving existing processes. Stablecoins reduce the cost and delay of moving capital across lenders, originators, and servicing partners, which lowers the all-in cost of running credit facilities. By reducing these system-level frictions, PACT can extend small-ticket credit at terms that are economically viable. Programmatic compliance reduces intermediary overhead, and on-chain monitoring keeps facilities within covenants in real time.

Compliance and Execution

Compliance defines what can actually scale. Goldfinch’s ongoing SEC considerations highlight how regulatory gaps cap growth. PACT addresses these challenges through licensed partners like Berkeley Square Finance Group (BSFG) and Tiberia Capital, combined with bankruptcy-remote structures that legally map token ownership to creditor claims. This framework gives institutional investors the clarity and protection required for real capital deployment.

Execution turns that framework into practice. BSFG supplies originators across Asia, Africa, and the Middle East, while Tiberia Capital is deploying $100 million toward a $300 million target through the protocol.

Together, these elements make PACT less a lending protocol and more a functioning credit network, one that combines compliant capital, automated enforcement, and real-world distribution under a unified on-chain infrastructure.

Structural Risks and Practical Constraints

PACT’s infrastructure fixes many of the glaring issues in structured credit, but scaling a $300 trillion market on-chain introduces challenges that go well beyond smart design choices.

Regulation remains the biggest variable. Credit frameworks differ across jurisdictions and most were not designed with blockchain in mind. PACT mitigates this by working with local entities that handle jurisdiction-specific compliance. This includes Berkeley Square Finance Group (BSFG), which operates as a global and local merchant bank, but the heavier lift comes from the fintech originators who hold the licenses needed to lend in each geography. Protocol-level KYC and whitelisting support this foundation, but global expansion still requires continuous adaptation to local securities, lending, and consumer-protection rules. What is compliant today may require reconfiguration tomorrow.

The fact that institutions like BlackRock and Franklin Templeton already operate on Aptos provides some precedent, but credit markets attract far closer scrutiny than tokenized treasuries.

Broader investor access also presents a paradox. Opening private credit to non-institutional participants sounds democratizing, yet accredited investor rules and suitability requirements exist for good reason. Credit can be complex and illiquid, and a Nigerian microfinance pool behaves nothing like U.S. corporate debt. PACT will need to balance accessibility with the guardrails regulators expect.

Currency remains another friction point. Stablecoins work well for dollar-denominated deals, but most emerging market lenders and borrowers operate in local currencies. A fintech in Lagos issuing Naira loans must constantly manage conversions and exposure to U.S. dollar volatility. Real-time settlement helps with timing risk but doesn’t solve the underlying mismatch between dollar funding and local revenue streams.

Smart contract and infrastructure risk cannot be ignored, either. Even with Move’s resource safety model and formal verification, complex multi-tranche waterfalls introduce edge cases. As PACT scales past $1.9 billion in originations, small probabilities translate into material outcomes. Network downtime could also disrupt instant payments. While Aptos has shown stability, blockchain rails are still young compared to legacy systems built for decades of uptime.

Finally, adoption itself is non-trivial. Convincing fintechs to integrate new infrastructure means navigating real operational costs: embedding SDKs, retraining teams, adjusting reporting, and managing privacy concerns. Some lenders will hesitate to expose repayment data on-chain, even in permissioned environments. Transparency strengthens risk oversight but reduces the opacity that traditional credit markets often depend on.

None of these risks are unique to PACT. They’re inherent to moving traditional finance on-chain. Early traction proves there’s real utility, but scaling from $2 billion to $2 trillion will test whether the model can withstand the regulatory, technical, and cultural pressures that come with mainstream adoption.

Conclusion: Toward an On-Chain Credit System

Structured credit continues to rely on infrastructure built for a different era. Manual verification, quarterly reporting, and intermediaries are costly and time-consuming, making smaller facilities economically unviable. These friction points have historically excluded emerging market borrowers, not because of credit risk alone, but because the operating model was never designed to serve them.

But any shift to on-chain credit must confront the operational risks that have undermined prior attempts, identity fraud, unverifiable collateral, and reliance on off-chain monitoring.

Early blockchain credit protocols recognized these inefficiencies but largely treated the problem as one of representation. Loans originated off-chain, tokenized for fundraising, and operated through traditional systems. The result was improved access to capital but limited improvement in transparency or operational control. The collapse of Goldfinch’s Tugende facility, despite flawless payment history, shows the limits of models where risk monitoring and collateral validation remain off-chain, even when repayments appear perfect on-chain.

PACT’s model differs by rebuilding credit processes directly on-chain. Loans originate as programmable NFTs, covenants execute at the protocol level, and waterfall distributions settle automatically. The design reduces latency, enables real-time monitoring, and removes layers of administrative overhead. Downstream, PACT’s greater transparency eliminates some of the traditional blind spots improving risk mitigation. It represents a shift from tokenizing financial assets to engineering financial infrastructure.

And to date, PACT has been able to scale quickly. PACT has originated $1.9 billion in loans across more than 900,000 borrowers, with institutional managers like Tiberia Capital already deploying regulated capital through the platform. Proof that on-chain credit can work within existing regulatory frameworks and reach real borrowers in emerging markets.

Rebuilding credit infrastructure on-chain is not a solved problem. Regulatory fragmentation, currency mismatches, and adoption barriers will continue to test the model. But PACT’s progress illustrates a credible path forward: one where blockchain moves beyond representation to participation in real financial operations. If the goal is to make credit markets more transparent, efficient, and accessible, the groundwork now exists to evaluate that possibility in practice rather than theory.

Glossary

- Borrowing base: The portion of a loan portfolio that qualifies as eligible collateral after applying haircuts, concentration limits, and eligibility criteria.

- Covenant: A contractual test or condition, such as minimum equity, maximum delinquency, or loan-to-value thresholds, that a borrower or facility must maintain.

- Facility: A committed pool of capital that an originator can draw against, governed by borrowing-base rules and covenant tests.

- Microfinance / Microloans: Small loans, often under a few hundred dollars, provided to underbanked or unbanked borrowers in emerging markets.

- Move: Aptos’s smart-contract language that treats assets as resources that cannot be accidentally duplicated or destroyed.

- Native USDC / USDT: Stablecoins issued directly on Aptos by Circle or Tether rather than bridged from another network. Native issuance enables mint/redeem on Aptos and reduces bridge-related risk.

- Net Asset Value (NAV): The value of a portfolio’s assets minus its liabilities. In credit, NAV reflects the real-time value of the underlying loan pool.

- Non-fungible token (NFT): A unique on-chain asset with its own identifier and metadata. In PACT, each loan NFT represents a specific loan and its repayment status.

- Originator: A lender (bank, fintech, finance company) that issues loans before pledging or selling them into a structured facility.

- Real-World Asset (RWA): A tokenized claim on an off-chain or real-economy asset, such as loans, invoices, real estate, or Treasury bills.

- Stablecoin: A digital token pegged to a reference asset (usually USD). Used for settlement, collateral, and cash management in on-chain credit systems.

- Special Purpose Vehicle (SPV): A bankruptcy-remote legal entity that holds loan assets and issues securities backed by those assets, separating investor claims from the originator’s balance sheet.

- Structured credit: A segment of credit markets where pools of loans or receivables are packaged into securities with defined cash-flow rules, covenants, and tranching.

- Tokenization: Creating on-chain tokens that represent claims on existing assets or cash flows, without necessarily moving origination or servicing on-chain.

- Total Value Locked (TVL): The total value of assets deposited in a protocol or network, often used as a proxy for liquidity and adoption.

- Tranche: A slice of a structured credit deal with its own risk, return, and payment priority. Senior tranches get paid first; junior tranches take losses first and earn higher returns.

- UETA-Compliant Vault: A digital storage system that satisfies the requirements of the U.S. Uniform Electronic Transactions Act (UETA), which allows electronic records and signatures to be treated as legally valid. In PACT’s system, the borrower’s loan documents are stored in a UETA-compliant vault so that the on-chain NFT has a legally recognized link to the underlying loan paperwork.

- Waterfall: The predefined order in which cash flows from borrowers are distributed to fees, reserves, senior tranches, and then junior or equity tranches.

Footnotes:

1Financial Principal, What is a Verification Agent?, Debt Facility & Securitization

2The Tax Advisor, Trustee Compensation: Proceed With Caution

3Guggenheim Investments, Understanding Collateralized Loan Obligations (CLOs)

4Lexology, In brief: securitisation transactions in USA, Cadwalader Wickersham & Taft LLP

0 Comments