Introduction

Where are all the consumer apps? Over the past few years, crypto has exhausted the speculative appetite for DeFi, NFTs, memecoins, and L2s, and failed to materially impact society. We have better, faster, stronger blockchain infrastructure, but no consumer apps to show for it. It is easy to look at a stagnant crypto industry and forget how far the space has come, how broken legacy markets are, and how big the opportunity is.

In this report, we will take a practical look at some of the most inefficient markets that exist today and draw parallels to crypto apps exploring solutions. We will unpack zkTLS and discuss why it is a major breakthrough for crypto consumer apps.

Precedence in Legacy and Crypto

There are numerous examples of inefficient markets in TradFi being exploited for progress.

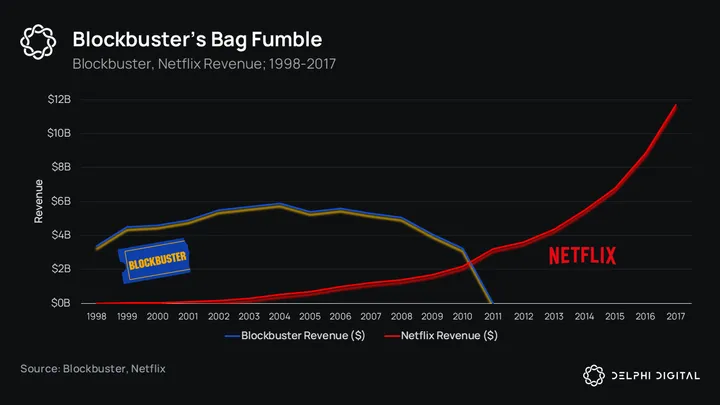

Blockbuster → Redbox → Netflix

Blockbuster reached its peak revenue of $6B in 2004. It was still generating $4B in 2009 before a rapid decline into bankruptcy in 2010. Blockbuster declined to purchase Netflix for $50M in 2000, showing a dedication to brick-and-mortar stores for media content on the cusp of the internet age. This unwillingness to adapt resulted in a rapid downfall.

Derivatives & Agriculture

Farming can be an extremely difficult industry to navigate without financial derivatives. Forward contracts for timber and agriculture can help immensely. They allow farmers to plan ahead, lock in prices for a future harvest, and secure financing.

Even within crypto, there is a concrete track record of inefficient markets being created and subsequently exploited. While crypto’s proclivity to create inefficiencies is ironic, it is encouraging how quickly solutions emerge to undermine them.

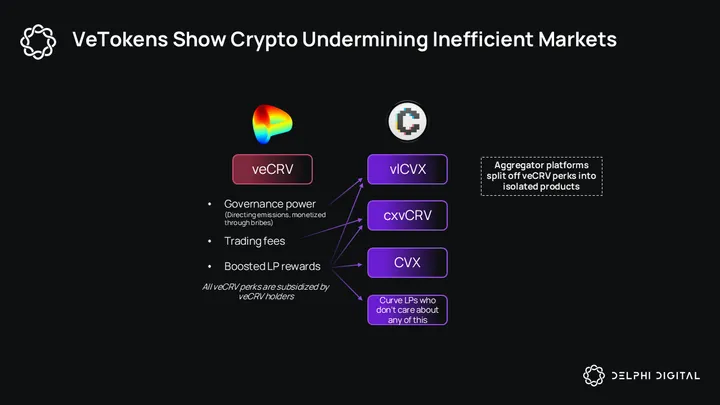

veTokens → Convex

We have extensively documented the broken ve-model, and similar projects like Radiant Capital.

Aggregators assume the liquidity burden and split off veToken perks into isolated products. Farming optimizers such as Beefy Finance programmatically dump veToken emissions, distributing them as yield to platform users. The end result is an a la carte menu for veToken perks, rendering the locking mechanism powerless, while those who do lock lose money.

Deposit caps

While it is often prudent for projects to use deposit caps and soft rollouts for safety, they ignore market forces. Real estate in oversubscribed venues (Ribbon, Eigenlayer, Aave) should be commercialized. There is an innate dollar value attached to space in the oversubscribed vault. Users who give up their spot should be able to sell it to the highest bidder.

Points programs

Since Uniswap’s canonical airdrop in 2020, airdrop sybil farmers have extracted immense amounts of value from subsequent tokens. This year, the pendulum has swung in the opposite direction, as projects farm users with vague and noncommittal points programs. Apps like Pendle have found product market fit by allowing users to speculate on the points market.

The picture of the free market is necessarily one of harmony and mutual benefit. Every inefficient and restricted market that exists today is an opportunity for crypto to infiltrate and improve society.

Gig Economy – Ride Sharing

The taxi model is extremely inefficient – rife with counterparty risk, friction, driver downtime, and unreliability. The model only works well in major cities.

Uber turned the taxi model on its head. Uber assimilated the concept of a taxi into everyday life, offering flexibility, convenience, and cost reduction for both riders and drivers. The regulatory and social controversy surrounding Uber’s rise was a testament to how disruptive the idea was.

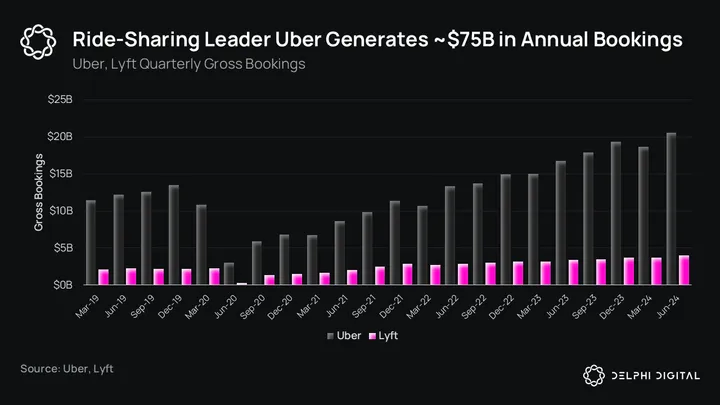

The global ride-sharing and taxi market is estimated at ~$271B in 2024. Uber’s $75B annual gross bookings support this estimate.

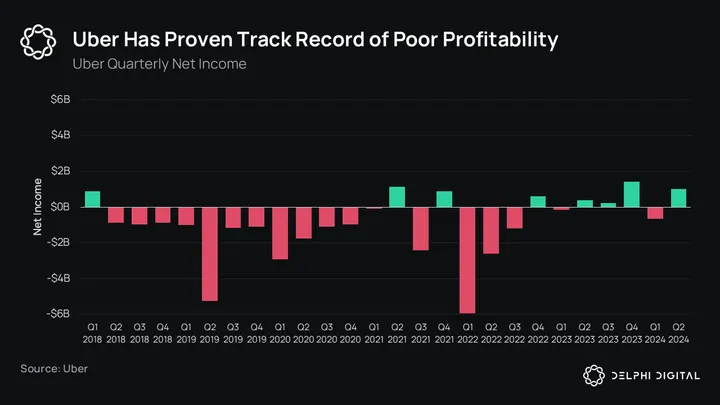

Despite the industry’s rise, Uber and other Web2 ride-sharing companies are just as vulnerable as the taxi industry was. The Uber model is a good idea with poor execution. Web2 ride-hailing, like Redbox, is the middle child of innovation.

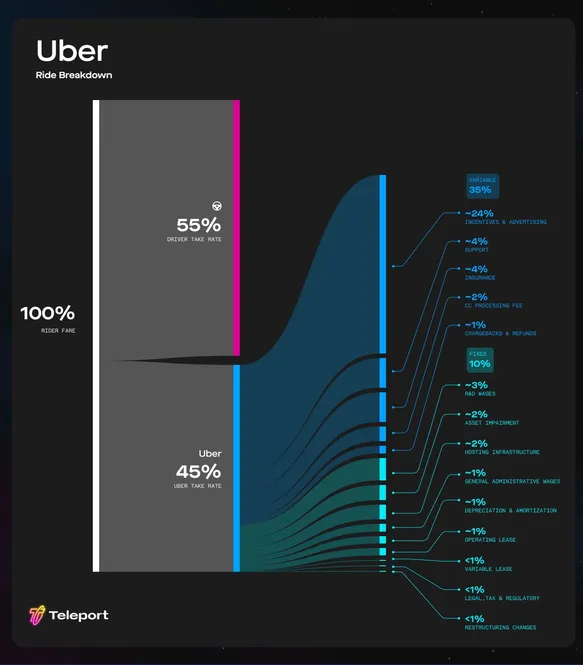

Uber and Lyft treat drivers very poorly, taking 45-50% of fares. Reported revenue as a percentage of gross bookings suggests 30%, but this is a result of shady accounting tactics such as external fees.

The 45% gross take rate goes to sustain a gluttonous, dysfunctional business that struggled mightily to make a profit. The majority of the value extracted by Uber (53% of Uber’s share, 24% of fare) goes to incentives and marketing. There are two major issues with this:

- Advertisements are unnecessary. Ride-hailing is a sticky business with established leaders who enjoy strong moats. The taxi industry never ran ads, nor did the horse carriage industry. These services exist and generate usage because people need them. Outside of the early S-curve adoption period, advertising for ride-sharing offers limited upside. Lowering costs for users and increasing wages for drivers would be a far more effective method to gain market share.

- It is unethical. Uber is simply connecting buyers and sellers of transportation. Outside of insurance, dispute resolution, reputation, price discovery, etc., it has very little responsibility. There is a strong case that Uber should be a public good. At the very least, the value Uber extracts should satisfy its fiduciary duty to shareholders and maximize value. But Uber’s marketing is its biggest variable expense cutting into potential profit. During the peak of Covid-19, when rid-sharing was at a historic low, Uber ran an expansive “No mask, no ride” ad campaign. The ROI of this ad campaign for stakeholders remains unclear. Uber’s wastefulness negatively affects drivers, riders, and shareholders.

After several years of poor earnings, Uber has strung together several profitable quarters. Interestingly, this coincides with a drop in reported revenue as a % of gross bookings and growing public awareness of algorithmic wage discrimination. Uber appears to offer drivers different prices for the same rides, even after controlling for confounding variables. There is a gray area around the legality of this practice. Uber drivers are legally classified as contractors but do not have pricing power. Even with algorithmic wage discrimination and misleading reporting practices, Uber is barely profitable.

Teleport

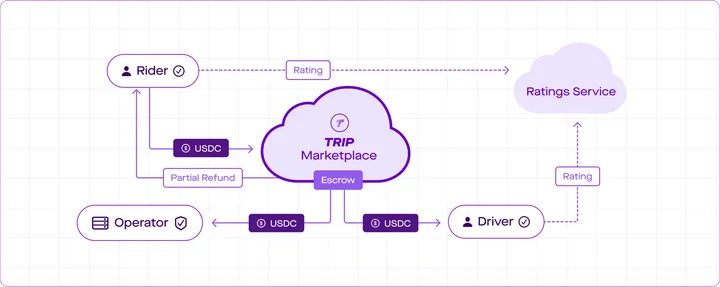

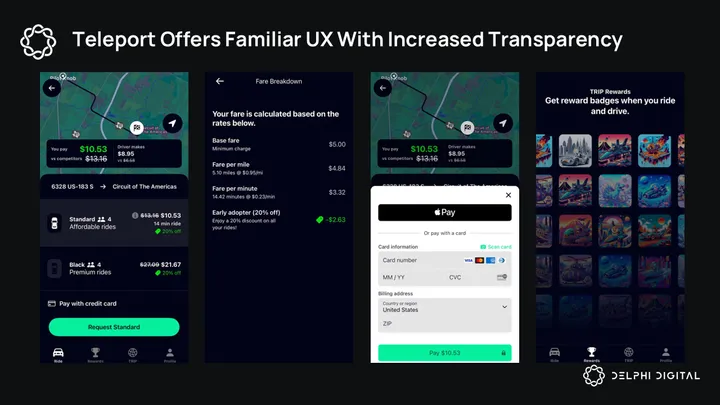

Teleport replaces bloated Web2 intermediaries with a decentralized marketplace called the TRIP ride-share protocol. TRIP is built on Solana and is available on the iOS app store.

Teleport guts the legacy structure for a minimalist model with few entities:

- Drivers and riders

- Operators – handle the regulatory and operational requirements of providing rideshare service.

- TRIP marketplace – DAO-governed smart contracts that offer coordination and consensus services to the network. Help the network remain neutral and fair without relying on centralized authority.

- Ambassadors – help the TRIP Marketplace overcome supply/demand imbalances by recruiting additional drivers and riders.

- Verifiers – onboarding facilitators. Inspect driver licenses, perform car inspections, conduct background checks and verify phone numbers.

- Auditors – confirming legal and operational eligibility of verifiers and operators

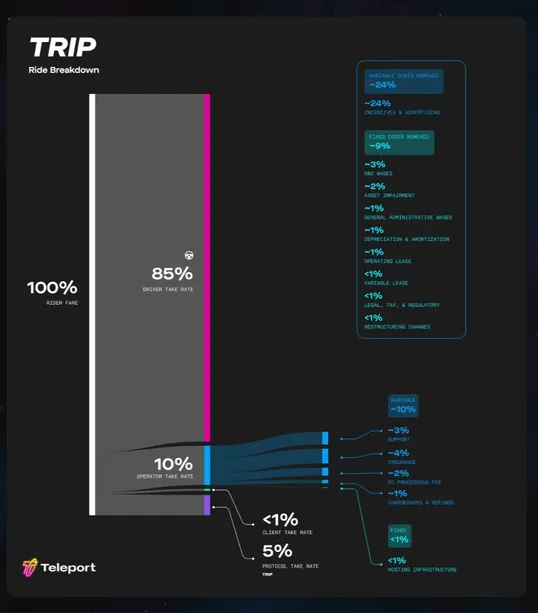

Teleport eliminates advertising and unnecessary fixed costs such as R&D wages. The TRIP protocol passes on cost savings to drivers and riders and incentivizes them to recruit new users. A complete analysis of cost structure differences can be found in Teleport’s Ridesharing Econ 101.

TRIP Miles are points allocated to network participants in accordance to their contributions to the network. They can be redeemed for TRIP rewards, which are represented as NFTs on Solana. The NFTs are classified into 41 tiers, with higher tiers often possessing unique attributes. The NFTs are meant to represent one’s contribution to the network. When Teleport releases a token, there could be some interesting dynamics between TRIP miles, NFTs, and revenue share.

Compared to Uber and Lyft, Teleport is a major improvement for drivers:

- Paid better – 85% driver take rate vs ~55% on incumbent marketplaces.

- Paid instantly – Drivers can opt-in to be paid instantly with USDC. Uber and Lyft have a payment delay unless certain criteria are met, and follow a traditional paycheck structure.

- Far

Read the full report

This report is part of Delphi Pro.

- 800+ Pro reports across every major sector

- Talk directly with our analysts

- Private community of funds and builders

Already a Pro member? Log in

0 Comments