Introduction

Exactly one year ago, we wrote about how credit markets for NFTs were developing and why they would be an important step forward for NFTs to mature into a proper, investable asset class. Since then, several new protocols have been launched, and the landscape has shifted significantly.

It’s a good time to take stock of where we are now and how things have changed.

A Quick Recap

NFT finance is an umbrella term that represents the apps and infrastructure that enable greater financialization of NFTs — often mimicking what is available in the traditional finance world and DeFi. The number of startups that are building in this sector has exploded, as evidenced by this infographic from Upshot circa July 2023.

Outside of marketplaces or exchanges, there are two verticals in NFT finance we are watching closely because they have the greatest potential for growth. These are:

-

NFT Lending (credit markets)

-

Derivatives (perps & options)

In traditional markets, derivatives trading volume has consistently outpaced spot trading volume. Similarly, NFT derivatives allow traders to gain greater capital efficiency and flexibility than simply holding spot NFTs, as well as the ability to hedge. They also allow more efficient price discovery outside of spot NFT markets. Perps make NFT collections more accessible to people since they can obtain exposure to an expensive collection without having to own an entire NFT (e.g CryptoPunks). One consequence is that it could lead to an erosion in the scarcity value for some of these collections.

While we expect derivatives to be an important aspect of NFT finance, lending is the current opportunity that is starting to find traction. Our focus for this report will be on NFT lending protocols. We sifted through the entire landscape to try and highlight where the opportunities (and risks) are and which protocols are worth paying attention to.

Let’s face it; NFTs are illiquid assets. While they can hold significant value, converting that value into liquidity can be a slow and cumbersome process. NFT lending disrupts the status quo. Owners can unlock liquidity quickly and efficiently by collateralizing their NFTs. And this is crucial when you think of NFTs as a part of an investment portfolio.

Opportunities & Risks

We’ll kick this report off by highlighting the main opportunities in NFT finance today, which include:

-

Earning above-market yields as a lender. Typical APRs in this space range from 10-30%, outperforming more traditional DeFi offerings such as Aave’s 2.2% or Lido’s 3.7% liquid staking. This disparity partially arises from the inherent illiquidity of NFTs and the general lack of widespread understanding of the asset class. Savvy lenders can mitigate some risk through portfolio diversification, focusing on high-quality NFTs or utilizing aggregator platforms like Spice Finance.

-

Airdrop farming. With the impending token launches by several NFT lending protocols, airdrop farming presents an additional layer of yield opportunity. We expect these tokens to be distributed equitably among both lenders and borrowers based on their platform activity. Airdrops can essentially amplify lending yields or subsidize borrowing costs, making the market even more enticing for both parties.

NFT lending is not without its risks. Yields are high, but for a reason:

-

Loan defaults have more serious consequences for lenders compared to staking ETH on Lido or lending USDC on Compound. Lenders will need to directly handle the NFT collateral, including selling it to recover part or all of their principal.

-

Collateral risk. NFTs can be volatile assets. If the value of an NFT used as collateral plummets drastically, surpassing the loan’s value, lenders could find themselves in a precarious situation. In extreme scenarios, this could result in a complete loss of principal for the lender.

-

Protocol & smart contract risk. This is especially pertinent for P2Pool protocols, which have to be designed in a robust manner and have not been battle-tested during periods of extreme volatility yet.

Market Size & Growth Opportunity

How do we estimate the scale of the opportunity with NFT lending?

We begin by looking at the number of unique users across major NFT lending platforms on Ethereum. The number of users continues to grow steadily, having picked up significantly since mid-2022.

However, the absolute number of users who have taken out a loan on NFT lending protocols is still tiny (11,757). This is even more stark when you compare this to the broader NFT space.

-

OpenSea had its lowest count of monthly active users since July 2021, and that is still 12x more than the number of people who have ever used an NFT lending protocol.

-

There are 6 – 8K daily traders on OpenSea. In contrast, there are ~700 daily borrowers across all NFT lending platforms on Ethereum.

Looking at loan origination volumes, the data was heavily skewed by the entrance of Blend. Excluding Blend, loan volumes hover at approximately $2.8M/week. This represents <5% of NFT trading volumes.

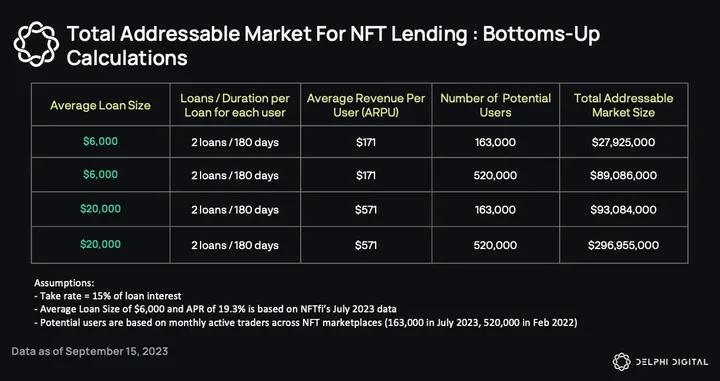

TAM Calculations

We will attempt to quantify the total addressable market for NFT lending.

Top-down approach:

At present, the NFT lending sector carries an outstanding debt totaling $82.9M spread across 11 NFT lending platforms. This is the amount of debt that is earning interest for lenders at various interest rates.

When we juxtapose this with one of the leading DeFi lending platforms today, Aave, which currently boasts an outstanding debt of $2.4B, it becomes evident how minuscule the NFT lending landscape is when compared to the broader crypto space (just 3%). Considering the wide design space and potential inherent in NFTs, it’s not difficult to imagine a future where this figure grows substantially.

Bottom-up approach:

To gauge the potential for growth in the NFT lending market, it’s crucial to start with some current metrics. Utilizing July 2023 data from NFTfi as a representative sample, the average loan size stands at approximately $6,000 with an average annual percentage rate (APR) of 19.3%. When you break this down, it results in loan interest of $96.5 for every 30-day loan period for an average loan.

To gauge the potential for growth in the NFT lending market, it’s crucial to start with some current metrics. Utilizing July 2023 data from NFTfi as a representative sample, the average loan size stands at approximately $6,000 with an average annual percentage rate (APR) of 19.3%. When you break this down, it results in loan interest of $96.5 for every 30-day loan period for an average loan.

Let’s assume:

-

The take rate for a protocol is 15% of loan interest. The current fee landscape varies, with NFTfi charging 5% while BendDAO charges 30% today.

-

A typical borrower takes out 2 loans with a total duration of 180 days each in their lifetime.

This results in an average revenue per user = $171

The number of monthly active traders on NFT marketplaces, standing at 163,000 as of July 2023, serves as a good proxy for the total addressable market (TAM) for NFT loans. By these metrics, the current TAM is a modest $27,925,000.

Key Levers for Growth

Let’s explore some scenarios that could

Read the full report

This report is part of Delphi Pro.

- 800+ Pro reports across every major sector

- Talk directly with our analysts

- Private community of funds and builders

Already a Pro member? Log in

0 Comments