Report Summary

Summary of the Report: “USD.AI – Financing the Future of AI Infrastructure”

USD.AI introduces an innovative financial model aimed at solving capital inefficiencies in AI infrastructure and decentralized physical infrastructure (DePIN) financing. It leverages DeFi mechanisms—particularly recursive borrowing and synthetic dollars—to bring liquidity, scalability, and trustless lending to the historically illiquid world of physical AI hardware financing.

Key Takeaways

1. Problem: Infrastructure Finance Is Broken

-

Traditional financing models are slow, opaque, and geographically constrained.

-

Major AI/DePIN deployments (e.g., Coreweave, Stargate) expose how capital availability lags infrastructure demand.

-

There’s a massive mismatch between capital markets (investors) and money markets (infra operators).

2. Solution: USD.AI + USDai

-

USD.AI enables DePIN and AI infra operators to take collateralized, short-duration loans against hardware assets.

-

Loans use a looping mechanism, allowing borrowers to re-use capital for scaling operations.

-

USD.AI introduces USDai, a synthetic dollar backed by real-world assets like GPUs and compute units.

3. USDai Design

-

USDai is composed of Liquid Credit Tokens (LCTs) tied to hardware lending pools.

-

Issuance and trading of LCTs occur via AI Infrastructure Credit Offerings (aiCOs).

-

Like a DeFi-native bond market, USDai dynamically mints/burns based on LCT performance.

-

Structured similarly to MakerDAO meets GLP, with added hardware yield potential.

4. CALIBER Framework: Legal Enforceability

-

Uses Uniform Commercial Code (UCC Article 7) to tokenize hardware through NFTs.

-

NFTs represent real-world ownership, transferable and enforceable via bailment contracts.

-

Smart collateral design ensures legal clarity and reclaimable ownership in default scenarios.

5. QEV (Queue Extractable Value)

-

Innovative redemption mechanism for synthetic dollar stability.

-

Auction-based redemption queue aligns incentives and prevents liquidity crises.

-

Addresses common pitfalls in RWA-backed stablecoins like USDe and USD0.

6. Risk Mitigations

-

70% Loan-to-Value (LTV) ensures equity cushion.

-

Insurance funds, governance token backstop, and junior tranches mitigate tail risks.

-

Underwriting by experts (e.g., Permian Labs) ensures reliable asset valuation and oversight.

7. Use Case Impact

-

USD.AI enables DeFi users to leverage $80K into $1.3M+ in hardware through recursive loans.

-

Provides a new on-chain primitive for AI, DePIN, and real-world asset yield.

-

Borrowers gain access to capital not easily available via banks—at speed and scale.

8. Governance Token Utility

-

Token holders direct liquidity (via gauge voting) toward preferred lending pools.

-

Bribes and interest income go to token holders.

-

Serves as equity backstop during default events, similar to Aave/Maker token mechanics.

Conclusion

USD.AI is a groundbreaking fusion of DeFi, AI infrastructure, and RWAs. By introducing a synthetic dollar (USDai) backed by real, income-producing hardware, and embedding risk mitigation into legal and protocol layers, it unlocks a scalable and trustless capital formation model for physical infrastructure. If successful, USD.AI could transform how AI and DePIN networks are financed—on-chain, transparently, and globally.

-

The Flaws of Infrastructure Finance

The accelerating growth of AI brings an insatiable demand for computing resources and related infrastructure. Traditional funding models are slow, opaque, geographically limited, and ultimately not scalable.

There is a long history of financing capacity failing to keep up with hardware demand and acting as a bottleneck to growth. The shift towards ASICs for Bitcoin mining is an early example of this trend, and more recently with DePIN projects struggling to bootstrap energy, internet, and compute networks.

The disconnect between capital markets and money markets is evident in top AI infrastructure deals like the $7B Blackstone financing of Coreweave. These issues will continue to surface as DePIN and AI networks grow, as evidenced by the launch of the $500B Stargate program. Infrastructure finance is in desperate need of disruptive financing solutions.

USD.AI Solution

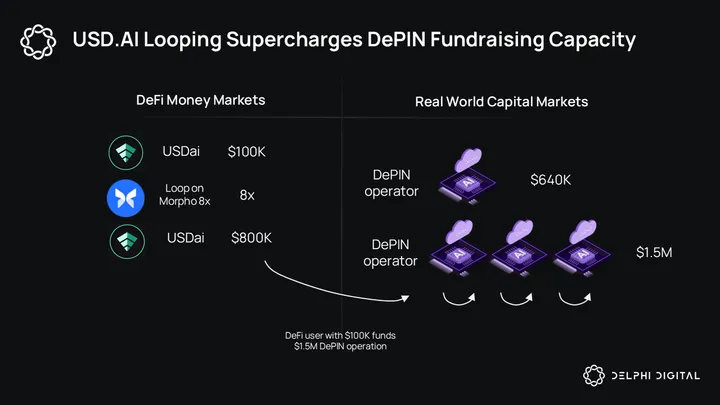

Looping has been a powerful tool for DeFi power users since DeFi Summer in 2021. By levering up through recursive borrows, users can command far greater capital than they could otherwise access, allowing for lucrative yield farming returns. As a result, demand gaps are closed more quickly, asset pegs are stronger, and the market is more efficient overall.

USD.AI provides a robust system to bring liquidity and leverage to illiquid infrastructure assets. Through its synthetic dollar, USDai, USD.AI offers a better way to scale AI hardware and DePIN mining operations by transforming illiquid assets into liquid, productive capital.

USD.AI – Looping for DePIN and AI Hardware

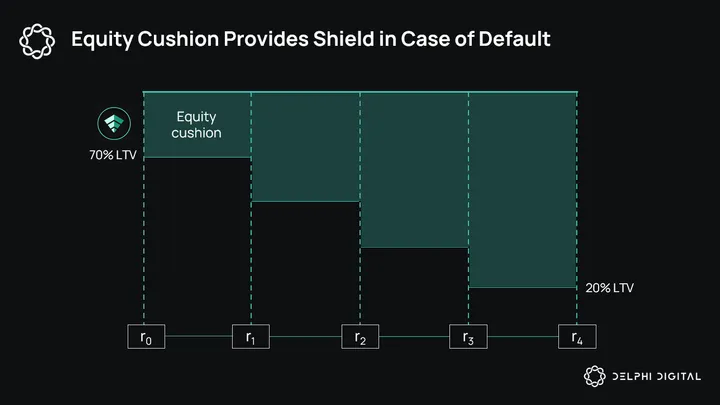

USD.AI brings the looping magic of DeFi to InfraFi. DePIN operators can collateralize hardware assets to access fixed-rate, amortizing loans. Loans are short-duration 30-day loans that automatically roll over. A 70% loan-to-value ratio gives a 30% equity cushion to lenders.

An equity cushion shields the lender from default. It is the difference between the value of a borrower’s collateral and the amount of their loan. It represents wiggle room to absorb declines in collateral value, reducing the lender’s risk of loss in case of default. A larger equity cushion increases the likelihood that a lender can recover their funds by selling the collateral if the borrower fails to repay.

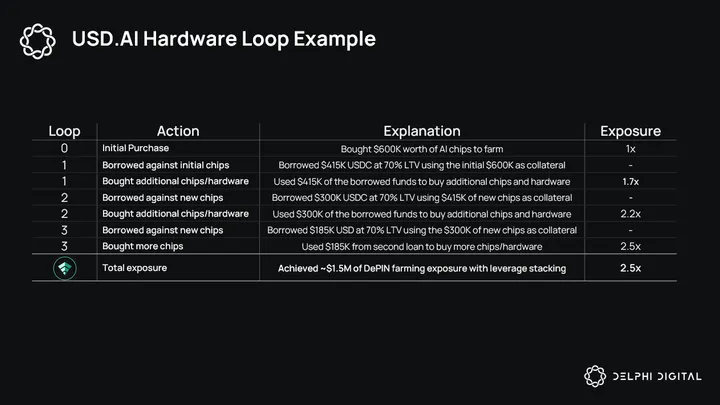

Borrowers can take their loan and lever up on hardware infra, creating the familiar looping mechanism. Vast onchain liquidity and looping makes it easier to scale industrial DePIN mining chip operations. Here is an example:

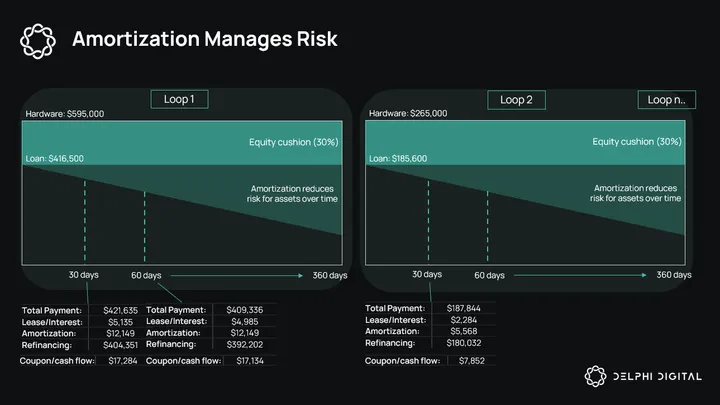

The borrower pays $595K for hardware and takes out a loan of $416.5K. At t=30, The borrower owes $5,135 in interest, and amortizes $12,149. Therefore for the second period, the refinanced loan is ~$404K, representing a 68% LTV (32% equity cushion). Amortization pays off the loan over time, growing the equity cushion and reducing default risk. Lenders are safe in the event of default so long as the value of the assets does not drop 30% below the appraised value.

Eventually, the borrower will have amortized the original loan, owning the initial cohort of hardware outright. They can then begin to pay off the subsequent loans faster or lever up on the initial hardware basket again. The USDai synthetic dollar will incorporate numerous loan arrangements like the above example under one umbrella.

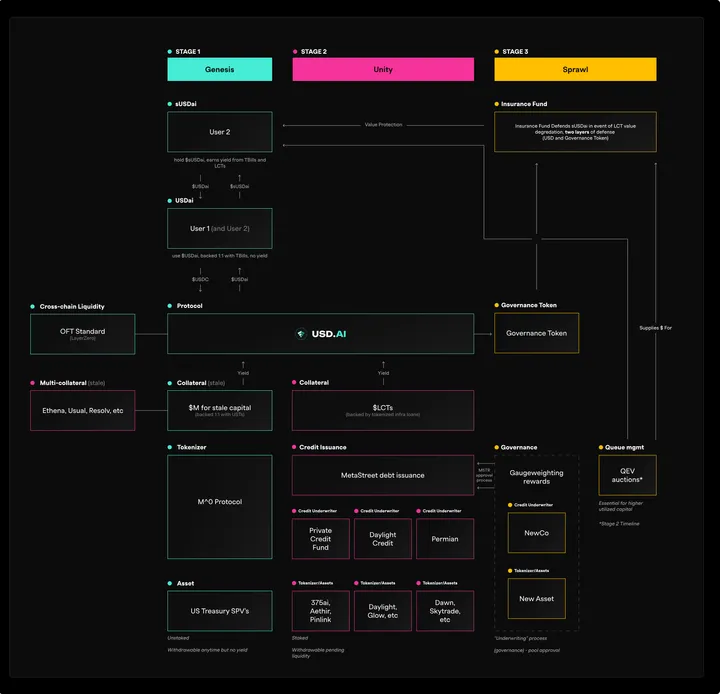

USDai Deep Dive

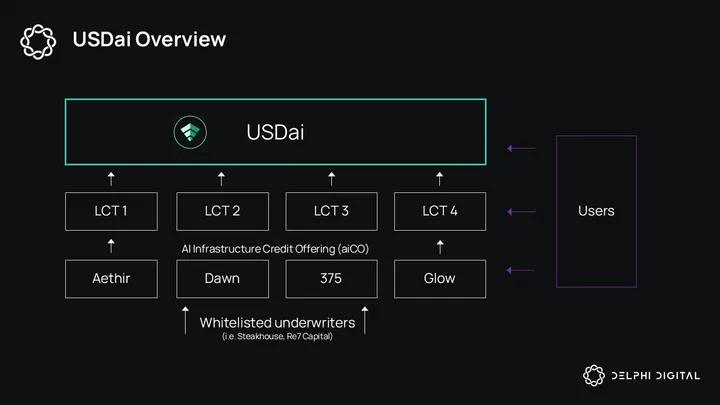

USDai is a synthetic dollar backed by loans against AI hardware, compute, and DePIN assets. Users can deposit capital in specific hardware lending vaults to have control over their backing and return, or they can get passive exposure to the complete business through USDai.

USDai is made up of Liquid Credit Tokens (LCTs), which are issued from hardware-backed lending pools (e.g., Aethir RK3588/USDC, 70% LTV). These LCTs are introduced through AI Infrastructure Credit Offerings (aiCOs), the initial issuance and trading events for specific lending pools provided by an appraiser & underwriter. USDai dynamically mints and burns tokens based on the value of aggregated LCTs, creating a scalable, credit-backed synthetic dollar.

USDai can be thought of as a high-yield bond index, with each loan being individual tradable bonds. Its crypto-native analogue is GLP/HLP, but with LCT tokens of different hardware loans as the collateral backing.

A more detailed overview of USDai’s inner workings can be found below. USD.AI employs a modular underwriting system to ensure the model can support various hardware sectors without sacrificing scalability or quality. The underwriting will follow an investment banking-like style, in which whitelisted underwriters oversee specialized sectors.

Permian Labs will be the sole underwriter at launch, specializing in compute assets. As USDai grows, additional underwriters will be onboarded to support Solar/Energy (Glow, Daylight), Internet (Dawn), Airspace (SkyTrade), and other emerging hardware intensive businesses. This model is similar to the Morpho lending structure, which sees whitelisted entities such as Steakhouse Financial and Re7 Capital curate markets for users.

Roadmap

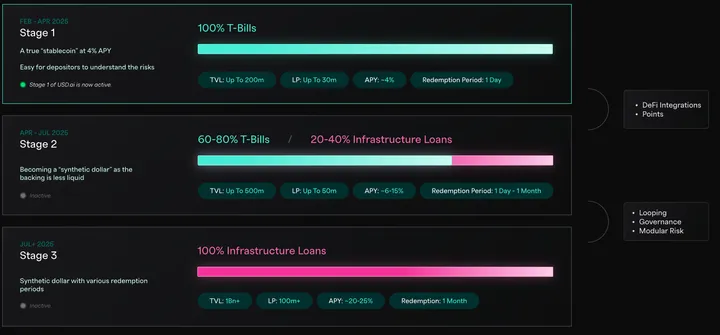

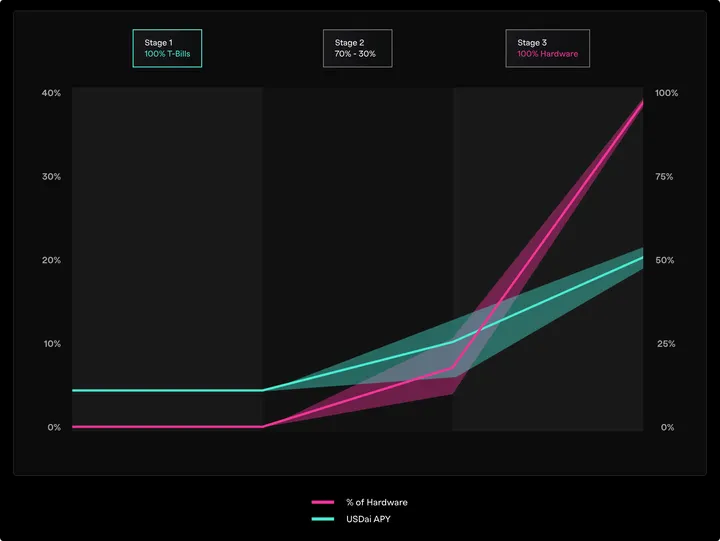

Initially, USDai will be made up of T-bills powered by M^0. M^0 is rearchitecting the stablecoin stack from the bottom up, offering a credibly neutral settlement layer for any application to mint and redeem “M,” a fully fungible stablecoin overcollateralized by treasuries. For more on M^0, check out our Alpha Feed post.

During this phase, users can deposit stablecoins and mint USDai. This initial phase will allow USD.AI to build up a strong base of liquidity, preparing it to service flurries of hardware lending demand without being bottlenecked by sporadic borrower-side growth early on.

USDai can be staked for sUSDai, the yield bearing synthetic dollar that will receive T-bill yield and eventually hardware loan yield.

As USDai grows, its backing will become increasingly composed of hardware loans. During the 2nd phase, USDai will generate ~6-15% APY, and have 1 day – 1 month redemption intervals.

In the terminal phase, as USDai approaches 100% hardware backing, yield will surge to over 20%, but liquidity will be strained. The monthly interest & amortization payments will be the only surface area available for direct redemption. USD.AI has designed a creative solution to handle redemptions in phase 3.

Queue Extractable Value (QEV)

Redemption is a challenge for synthetic dollar-type projects with less liquid collateral backing, like USDai, USDe (Ethena), and USD0++ (Usual Money). The typical solution is to throw token incentives at LPs to ensure strong liquidity on AMMs. This method was insufficient in the recent Usual Money depeg.

USD.AI will address this issue by confronting the underlying problem- inefficient pricing of liquidity. Queues are everywhere IRL and in crypto. DeFi has arbitrage, capped deposits, rigid rules around redemption and interest rate pricing, etc. USD.AI embraces the market dynamics at play similarly to Flashbots’ MEV-Boost.

QEV integrates an auction-based prioritization mechanism directly into the system. A transparent and demand-driven market determines queue positioning, preventing opaque or unfair liquidity bottlenecks. QEV enables a system where redemption costs shift dynamically based on liquidity conditions, preventing forced liquidations and chaotic exits on secondary markets.

QEV will become more relevant as USDai becomes more hardware-backed in stage 3. Liquidity pools will remain the primary method of entry and exit for USDai, and QEV will offer a supplemental market based mechanism for pricing liquidity.

How it works

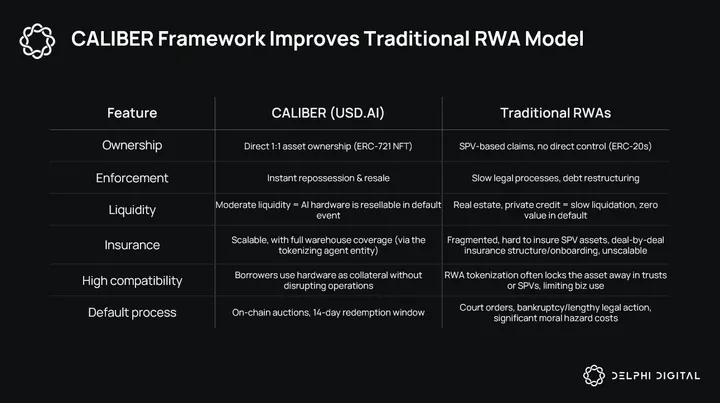

Outside of T-bill products, RWA models often struggle with tokenizing physical assets. Centrifuge, Goldfinch, MakerDAO, etc often use SPV-based ownership, with weak enforcement and inefficient risk management. Onchain participants have little insight into the inner workings of the legal processes and must place a significant amount of trust in the protocol operators.

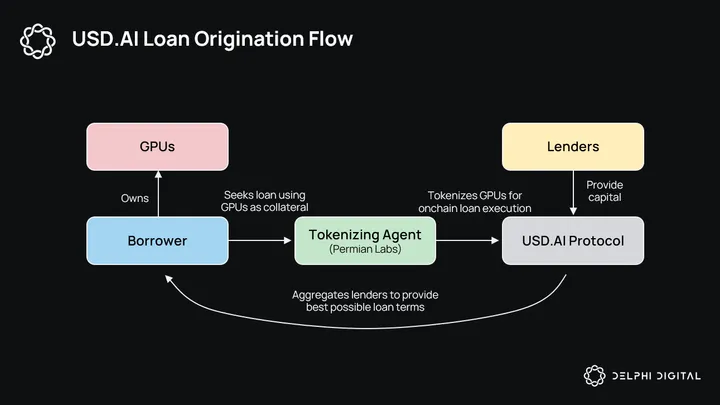

USD.AI introduces CALIBER (Collateralized Asset Ledger: Insurance, Bailment, Evaluation, and Redemption) a new offchain/onchain framework utilizing Uniform Commercial Code (UCC Section 7). **It enables direct asset ownership, enforceable redemption, and integrated insurance for DePIN hardware. Lets unpack the entire flow.

Tokenization & Bailment – The tokenization and bailment process is similar to a sale & leaseback. The borrower sells GPUs to the Tokenizing Agent, who tokenizes ownership of the GPUs with NFTs in accordance with the Uniform Commercial Code Article 7. These NFTs represent real-world, enforceable ownership of the assets moving forward. Legal ownership is passed to the NFT holder as the holder of the “electronic copy of record”, basically a digital deed. the bailment contract stipulates the holder of the electronic copy of record is the “bailor” and can reclaim the underlying asset

The tokenization process involves a rigorous diligence process, including proof of insurance, physical site visit, and lien insurance.

The Borrower and Tokenizing Agent enter into a bailment agreement granting the borrower the right to operate and profit from the GPUs on behalf of the legal owner (the Tokenizing Agent, holder of the NFT). As part of the bailment agreement, the NFT is transferred back to the borrower, who can then post the NFT as collateral to access debt proceeds onchain.

Underwriting – The borrower pledges NFTs to the lending pool, which allows them to borrow $ from the pool. The service provider values the assets and maintains the valuation oracle. The service provider has signed an agreement with the tokenizing agent and is responsible for repossession in the event of default, and charges a fee to the pool for their services.

Loan Execution – The borrower is free to borrow directly from the protocol, using the NFT as collateral. The borrower must make payments every 30 days to keep their loan current according to the terms (e.g., 15% APR, 3-5 year principal amortization).

Default – In the event of default, the mobile chip NFTs are sold onchain in an auction. Auction proceeds are returned to the pool, allowing lenders to get their money.

The CALIBER framework clarifies much of the gray area involved in other RWA models.

Summary of Risks and Mitigants

USDai is fully collateralized and has comprehensive risk mitigants, but is similar to more traditional RWA models and institutional lending projects in its need to solve for various offchain trust assumptions. Here is a complete overview of challenges and solutions:

Preventing default:

- Onboarding Diligence – Thorough vetting of counterparties’ financial status and compliance requirements before participation.

- Bailment contract – Clear legal structure secures asset ownership and collateral rights throughout the financing period.

- Modular underwriting – Comprehensive system including asset appraisal, default handling, and flexible amortization options. 3-10% administration fee ensures underwriters’ interests align with platform success.

- Amortization – Regular principal repayment schedule reduces exposure over time, with first successful implementation complete.

- Tax optimization – **Sale & leaseback structure offers tax efficiency while maintaining regulatory compliance (esp. in USA).

Preventing loss, given default:

- Equity cushion – 70% Loan-to-Value (LTV) ratio provides a safety margin against asset value fluctuations and default risks.

- Onchain auction – Built-in safeguards include auction repurchase guarantees

- Insurance fund – Dedicated insurance vehicle provides protection against unexpected losses, strengthening system stability.

- Governance token backstop – Token functions as ultimate risk buffer in case of major depeg, similar to Aave and Maker models.

- Junior Tranche – Vault managers will be required to participate in a junior tranche, for “skin in the game”

Given these mitigants, how can lenders get burned? When would a borrower be incentivized to default? This comprehensive framework leaves few scenarios to exploit. One potential scenario could see a loan taken out against state-of-the-art chips right before a new chip comes out, dramatically repricing the old chips below the equity buffer. If the borrower has not yet used debt proceeds to purchase more of the original chips, it may make sense for the borrower to default. In this case, the borrower has amortized some of their loan via monthly coupons, requiring the drop in value to be increasingly steeper to result in a loss as time passes. The farther away from loan origination, the more likely that the borrower has already levered up on the same chips and is stuck with them. In a way, the borrow rate is a deep OTM put option premium for each hardware device. The underwriter will also be aware of potential new hardware releases and consider this factor throughout the underwriting process.

USD.AI has developed a comprehensive set of mitigants to address its trust assumptions and unique problem set. QEV is a particularly encouraging tool to mitigate liquidity issues as USDai’s backing matures. Still, peg stability will be a long-term risk for such an illiquid and unprecedented project. Even liquid, fully onchain pegged assets (LSTs, treasury-backed stables) have endured extreme stress tests due to the highly leveraged looping meta. The post-default onchain NFT auction’s timeliness and demand depth have not yet been demonstrated. While it is unlikely borrowers will ever be incentivized to default, unforeseen events in the chip space, black swan events, or human error in the underwriting process could result in extreme pressure on an already illiquid backing. A major unwinding event could test the appetite for the defaulted hardware auction process, spooking holders of the already illiquid USDai. However, the risk of a death spiral seems negligible as a significant de-peg has no direct impact on hardware borrowers’ operations. Adequate diversification should be able to contain tail risk in the core business.

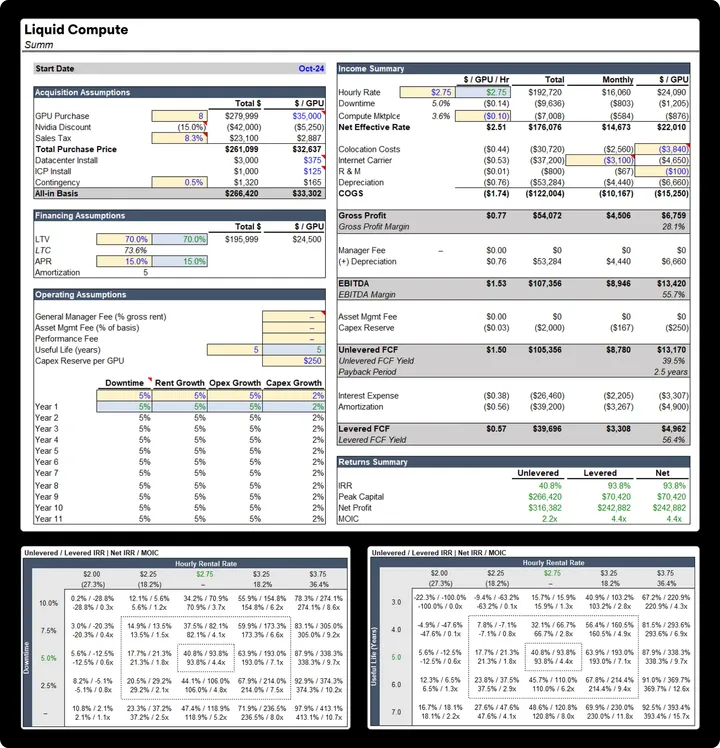

Value Proposition for Borrowers

A common question surrounding USD.AI and similar products like Ondo, Maple, etc is why there is such an appetite for high-interest rate loans on the borrower side. The answer is leverage. It can be difficult for crypto-adjacent entities to get loans from banks in a reliable and timely manner. DeFi simplifies this process and offers leverage on the underlying business. Even with relatively high interest rates, seamless access to leverage reliably juices returns for operators.

The following model examines the cost structure of a Neocloud GPU operator that wants to borrow against 1 cluster of 8 H100 GPUs.

The key takeaway from the model is that a levered strategy yields an IRR of 93.8% and a multiple on invested capital (MOIC) of 4.4x, double the figures of the unlevered position of 40.6% IRR and 2.2x MOIC.

Market Positioning

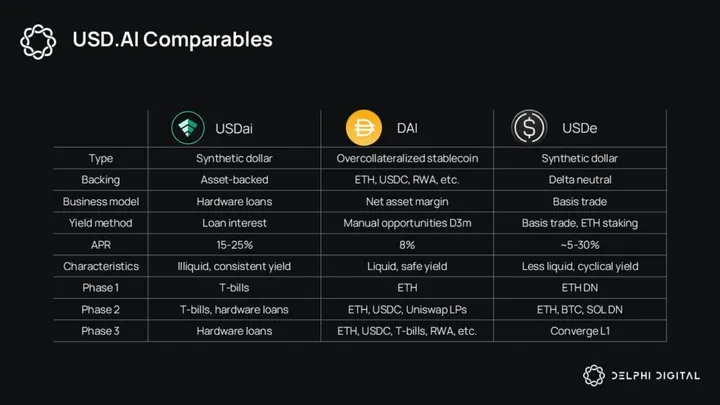

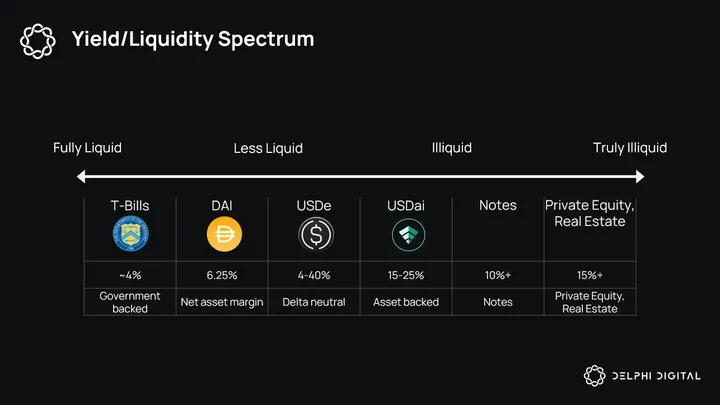

USDai is most comparable to DAI and USDe. DAI was initially backed solely by ETH, before transitioning to USDC backing and eventually RWA backing. USDai and USDe share the synthetic dollar model, with a less liquid but more lucrative back-end business powering the onchain yield engines.

USDai, DAI, and USDe have various tradeoffs concerning yield and liquidity. USDai brings a very unique profile to the yield spectrum. On the low end, T-bills are highly liquid and generate around 4%. Maker/Sky’s net asset margin business generates 6-7% while retaining strong liquidity. USDe is a bit less liquid, with redemption periods several hours and unstaking cooldowns of several days. USDe also exhibits highly cyclical returns that can reach over 40% in bull market and 0-5% in a downturn.

USDai’s redemption period extends to 30 days and is limited by its income, but QEV will alleviate much of this traffic. Once USDai becomes predominantly asset-backed, it will generate a consistent ~20% yield and be relatively insulated from market cycles. sUSDai offers a compelling return without venturing into the truly illiquid yields, like market maker loans or private equity.

Governance Token

USD.AI will have a governance token that benefits from organic cash flows and real utility. The governance token will have a gauge-weighted mechanic that directs passive debt to different hardware pools. DePIN projects will be able to bribe USD.AI token holders to direct liquidity towards their business. This may prove a more viable option than rigid token emissions that have become the norm for DePIN growth incentivization.

The governance token will serve as an equity backstop in case of default, and therefore has a strong claim to the cash flows it receives. The governance token will receive bribes and and share of interest income, while directing debt and insuring solvency.

Conclusion

USD.AI harnesses the power of DeFi to bring scalability and efficiency to DePIN capital formation. DeFi’s global liquidity and onchain creativity can allow a DeFi user with $80K USDai to loop on Morpho and finance a ~$1.3M DePIN mining operation.

The harmonious marriage of capital markets and money markets has not yet been seen to this degree in finance. USD.AI offers exposure to RWA, DePIN, and AI, and onboards yet another source of impressive, organic yield to DeFi.

0 Comments