Report Summary

This report examines yield generation trends, liquidity flow, and lending dynamics in the Aptos DeFi ecosystem, highlighting the interplay between native protocols, cross-chain bridges, and stablecoin demand. Aptos is emerging as a competitive L1 for yield farming thanks to low-latency execution, low fees, and growing TVL in stable-backed strategies. The yield landscape is increasingly influenced by bridged assets, stablecoin arbitrage, and protocol-level incentive design.

Key Takeaways

1. Stablecoins Dominate Liquidity

-

Stablecoins make up a significant share of Aptos TVL, with USDC and USDT leading inflows.

-

Bridged assets (from Ethereum, Solana, BNB Chain) are fueling cross-chain yield strategies.

-

Liquidity pools pairing stables with volatile assets offer high APYs due to incentives.

2. Lending Rates & Yield Sources

-

Lending markets like Thala, Aries, and Econia are the backbone of Aptos yield generation.

-

Borrow rates on stables are low, allowing leveraged looping strategies to amplify yields.

-

Incentive APRs are a major component of net yield — without them, base rates are modest.

3. Cross-Chain Arbitrage Opportunities

-

Aptos benefits from fast finality and low fees, enabling arbitrage between L1/L2 ecosystems.

-

Bridged stablecoins are often cycled through Aptos lending pools for short-term farming before being redeployed elsewhere.

4. Protocol Design & Incentives

-

Protocols are experimenting with ve-token models to direct emissions toward specific pools.

-

Locking mechanisms for governance tokens help sustain liquidity depth but concentrate power among large holders.

-

High reliance on incentives poses sustainability risks if token rewards decline.

5. Growth Drivers

-

Expanding stablecoin liquidity and deepening lending books.

-

Continuous incentive programs to attract active capital.

-

Integrations with liquid staking derivatives (LSDs) to diversify collateral.

Conclusion

Aptos DeFi yield generation is currently incentive-driven and stablecoin-heavy, with strong cross-chain participation. While current yields are attractive, long-term sustainability will depend on building organic borrowing demand and diversified yield sources beyond incentives.

If Aptos can evolve from incentive-fueled liquidity to utility-driven capital deployment, it could become a top-tier L1 yield hub competing with Solana and Ethereum L2s.

-

Aptos: The Stablecoin Capital’s Yield Playbook

Aptos is home to over $1.3 billion in stablecoins. Most ecosystems celebrate when they hit $100 million. This concentration didn’t happen by accident.

Our previous reports explored Aptos’ technical architecture and growing ecosystem of applications. But infrastructure and applications alone don’t drive adoption, capital seeking returns does. And that’s what helped Aptos become one of the leading destinations for institutional-grade stablecoin flows.

The foundation’s approach was straightforward: support infrastructure capable of handling massive stablecoin volume at consumer-grade speeds, and composable yield opportunities would follow. Native USDC and USDT integration, sub-second finality, and negligible transaction costs created the perfect environment for yield-focused capital.

So far, things are moving in the right direction.

The yield ecosystem on Aptos has grown substantially, spanning lending, liquid staking, and concentrated liquidity. These protocols work together, enabling strategies that range from large-scale stablecoin deployment to complex multi-protocol compositions.

Two factors make this possible: technical performance and liquidity depth. Aptos’ sub-second settlement allows for frequent strategy adjustments, while over $1.3 billion in stablecoin liquidity supports institutional-size positions. Most other chains face bottlenecks in one area or the other.

The outcome is a yield ecosystem where capital stays active rather than sitting idle across wallets.

Aptos’ Most Compelling Yield Opportunities

While Aptos is home to dozens of protocols across lending, DEX, and liquid staking categories, our analysis identifies several standout opportunities based on current yield rates, protocol mechanics, and risk-adjusted returns. The following platforms represent the most attractive yield farming opportunities currently available on the network.

These protocols combine high base yields with additional incentive layers, creating compelling risk-reward profiles for different capital deployment strategies. Rates range from stable double-digit returns to triple-digit APRs, depending on asset pair volatility and leverage mechanisms.

Note: The following yield analysis reflects data captured during rolling 30-day periods throughout July and August 2025 when this analysis was conducted. All APR figures represent historical performance and are subject to ongoing fluctuation based on market conditions.

Hyperion: Organic Trading Fees Driving 200%+ APRs

Hyperion operates as Aptos’ primary CLAMM (concentrated liquidity AMM). It launched in February 2025 and has already scaled to over $128 million in TVL. The protocol’s yield structure combines trading fees from its concentrated liquidity model with additional incentive layers, creating some of the highest sustainable APRs in the Aptos ecosystem.

While Season 1 of Hyperion’s DRIP points campaign recently concluded with early contributors receiving an airdrop of 5% of $RION tokens, Season 2 is now underway following the TGE. This indicates that continued incentive programs will layer on top of the base trading fee yields, rewarding participants in the Aptos ecosystem.

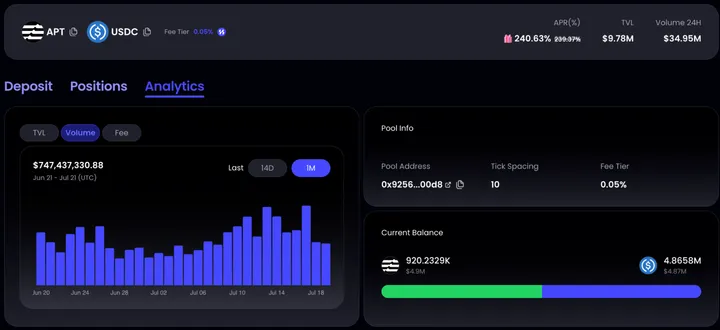

The protocol’s flagship APT-USDC pool exemplifies Hyperion’s yield potential, currently delivering a total APR of 240.63%, though yields vary with market dynamics and liquidity conditions.

Broken down, this total APR is composed of 239.37% from trading fees and 1.26% from farming rewards. The pool operates with a 0.05% fee tier and processed $747 million in volume over the past 30 days, with a TVL of $9.78 million. This high volume-to-TVL ratio of approximately 76:1 drives the substantial fee-based returns.

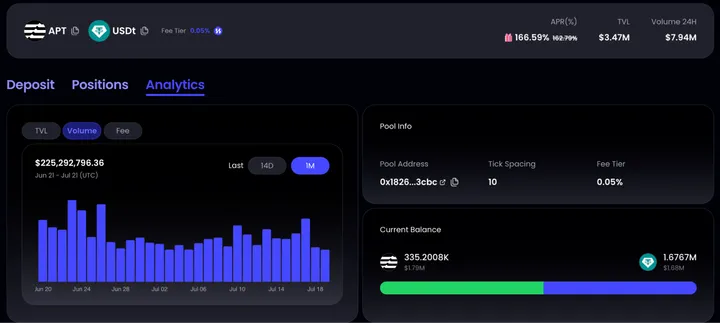

The APT-USDT pool tells a similar story. It delivers an APR of 166.59%, with 162.79% stemming from trading fees and 3.8% from farming rewards. This pool processed $225 million in volume against a TVL of just $3.47 million over the same one-month period.

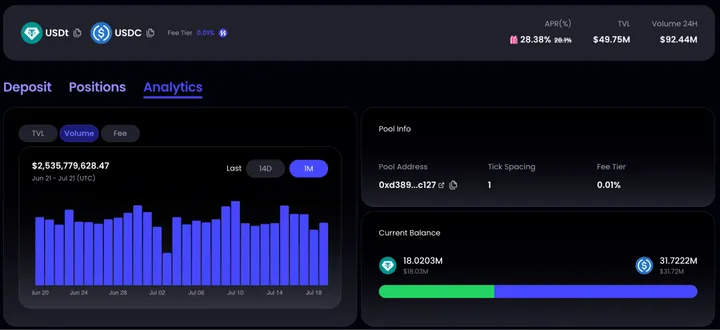

For users seeking yield without directional APT exposure, Hyperion’s USDT-USDC pool offers a compelling alternative. This stablecoin pair delivers an APR of 28.38% (28.1% from fees, 0.28% from farming rewards) with a 0.01% fee tier. The pool processed $2.54 billion in volume over 30 days against a TVL of $49.75 million.

While the APR is lower than that of APT pairs, the risk profile is fundamentally different. Liquidity providers face minimal impermanent loss risk since both assets maintain stable value. The higher TVL of $49.75 million compared to APT pools reflects this appeal to risk-averse capital seeking steady returns without volatility exposure.

Hyperion also offers Bitcoin exposure through its pools, including the APT-xBTC pool which delivers an APR of 62.32%, Echo’s aBTC-xBTC pool which generates and an APR of 23.57% APR, and Fiamma’s fiaBTC-xBTC pool which offers and APR of 41.66% APR.

Newly launched WBTC pools have also further expanded Bitcoin yield opportunities. The WBTC-USDC pool, for example, yields an APR of 229.32% with $518,450 in TVL, while the WBTC-xBTC pool offers an APR of 26.43% with $274,440 in TVL, providing both Bitcoin-stablecoin and Bitcoin-Bitcoin derivative exposure options.

These pools demonstrate Hyperion’s core value proposition: concentrated liquidity that captures organic trading fees from real volume across different risk profiles.

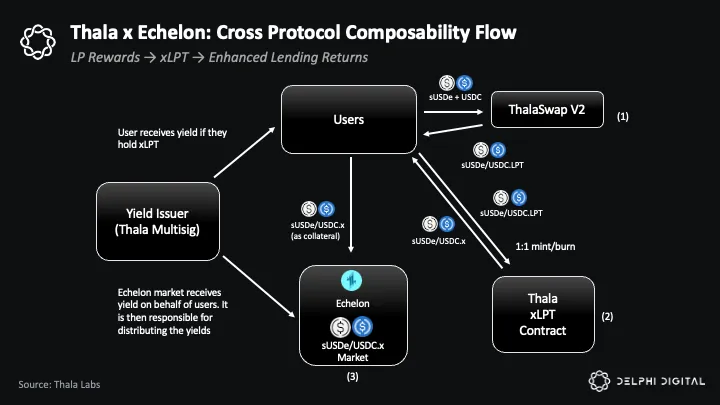

Thala: Cross-Protocol Yield Stacking via xLPT Integration

Thala operates as a multi-product DeFi platform with $148 million in TVL, offering DEX, lending, and liquid staking services. Thala’s yield structure combines swap fees and thAPT staking incentives, with veTHL lockers receiving boosted rewards.

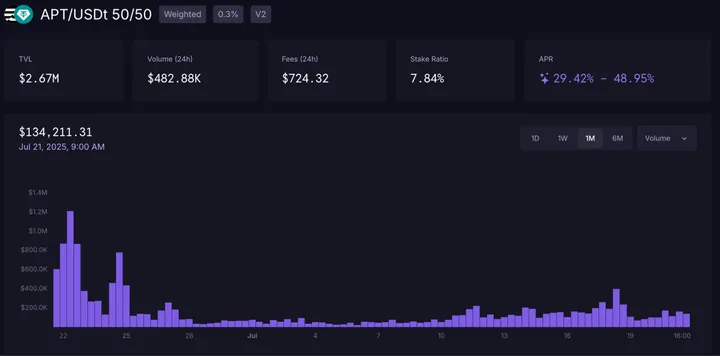

The APT-USDT pool exemplifies this approach, delivering an APR between 29.42% – 48.95% through multiple yield sources.

The base APR of 29.42% combines 9.89% from swap fees and 19.53% from thAPT staking rewards. Users can boost this APR to up to 48.95% through veTHL holdings. This involves locking THL tokens and/or THL-MOD LP tokens for 2-52 weeks to receive voting power that provides up to a 2x multiplier on farming rewards. The pool maintains $2.67 million in TVL with $482,880 in daily volume.

Similarly, the APT-USDC pool offers an APR of 26.14% – 45.43%, with a base yield of 26.14% (6.84% swap fees + 19.3% thAPT staking rewards) boosted to 45.43% through veTHL holdings. This pool has a higher TVL at $6.79 million but a comparable daily volume of $850,000.

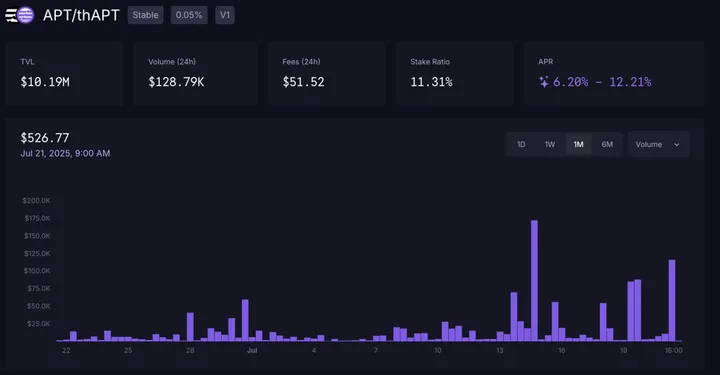

For users seeking maximum Aptos exposure, the APT-thAPT pool offers an APR of 6.20% – 12.21% by pairing native APT with Thala’s liquid staking derivative, thAPT. This stable pool generates 6.2% base APR (0.18% swap fees + 6.01% thAPT staking rewards) with potential boosts to 12.21%.

With $10.19 million in TVL and $128,800 in daily volume, this pool appeals to users wanting leveraged APT exposure without impermanent loss risk from pairing with stablecoins.

Thala’s stablecoin pools offer more conservative yields than Hyperion’s concentrated liquidity strategy, but they remain compelling nevertheless.

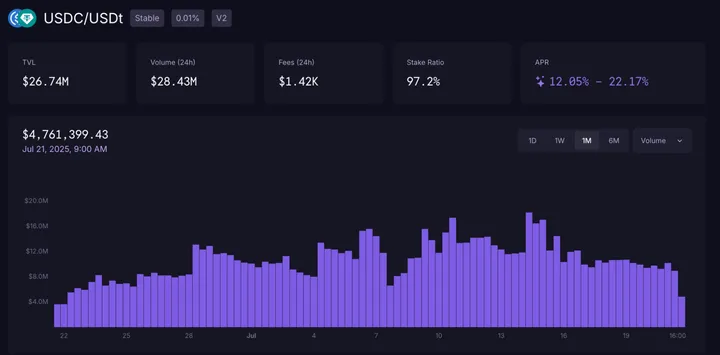

The USDC-USDT stable pool delivers an APR of 12.05% – 22.17%, combining 1.94% swap fees with 10.08% thAPT staking rewards. With $26.74 million in TVL and $28.43 million in daily volume, this represents Thala’s most liquid pool, generating $1,420 in daily fees.

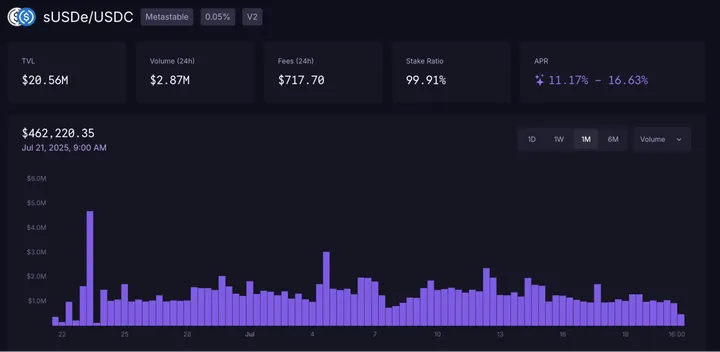

Thala’s sUSDe-USDC metastable pool offers an APR of 11.17% – 16.63% through a more complex structure: 1.27% swap fees, 4.44% from Ethena staking, and 5.44% thAPT staking rewards. This pool maintains $20.56 million in TVL with a lower daily volume of roughly $3 million, generating $718 in daily fees.

For users seeking Bitcoin yield farming opportunities, Thala offers a USDC-WBTC weighted pool delivering an APR of 64.31% – 128.44%. The pool combines 0.17% from swap fees with 64.14% in thAPT staking rewards that can be boosted to 128.44% through veTHL holdings.

Unlike Hyperion’s fee-driven model, Thala’s yields rely heavily on thAPT token incentives alongside organic swap fees. What sets Thala apart is its cross-protocol composability: staking USDC-USDT and sUSDe-USDC LP tokens generates xLPT tokens, which can be supplied on Echelon Market for additional yield layering opportunities.

Echelon Market: Lending Yields Enhanced by Ecosystem Composability

Echelon operates as a multi-chain lending protocol with $203.2 million in TVL on Aptos, positioning itself as the second-largest money market after Aries. The protocol’s yield opportunities center around supplying assets to earn interest plus additional thAPT incentives.

Echelon’s stablecoin markets demonstrate how protocol incentives can enhance base lending yields.

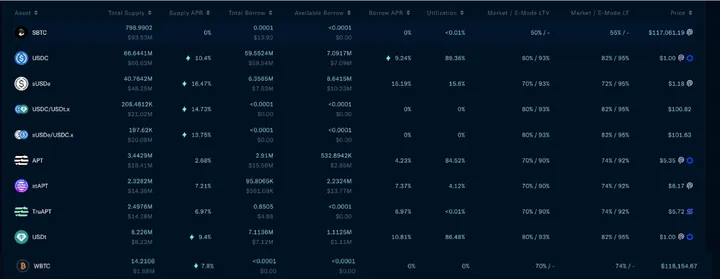

USDC suppliers, for example, earn a combined APR of 10.4%, consisting of 7.49% from lending plus 2.92% in thAPT incentives. The market shows strong utilization at 89.36% with $66.64 million supplied against $59.55 million borrowed.

USDT offers similar mechanics with an APR of 9.4% (7.01% lending + 2.39% thAPT incentives) with high utilization at 86.48%. The sUSDe market provides a higher yield with an APR of 16.47% through a three-part structure: 0.64% lending, 9.74% Ethena staking, and 6.1% APT incentives. The recently launched WBTC markets pay suppliers an APR of 7.8%, and the total supply has grown to $1.7 million since its inception.

Echelon also features OKX’s xBTC market, where suppliers earn an APR of 3.46%. Through a current campaign with OKX, users receive additional incentives when using xBTC as collateral to borrow USDC, enhancing yield opportunities for Bitcoin holders

A key differentiator for Echelon is its integration with Thala’s ecosystem. This creates a two-step yield strategy: earn DEX fees on Thala, stake the LP tokens for xLPT, then lend those xLPT tokens on Echelon for additional returns.

Users can supply xLPT tokens (generated from staking Thala’s USDC-USDT and sUSDe-USDC LP positions) directly on Echelon to earn additional yield.

The USDC/USDT.x and sUSDe/USDC.x markets show APRs of 14.73% and 13.75%, respectively. This allows users to earn lending yields on top of their existing DEX LP returns.

Liquid Staking & Restaking: APT Yield Without Lockups

Some of the popular liquid staking protocols on Aptos include Amnis Finance, Kofi Finance, and Echo Protocol. These platforms allow users to earn staking rewards on their APT while maintaining liquidity through derivative tokens that can be used across Aptos DeFi.

Amnis Finance

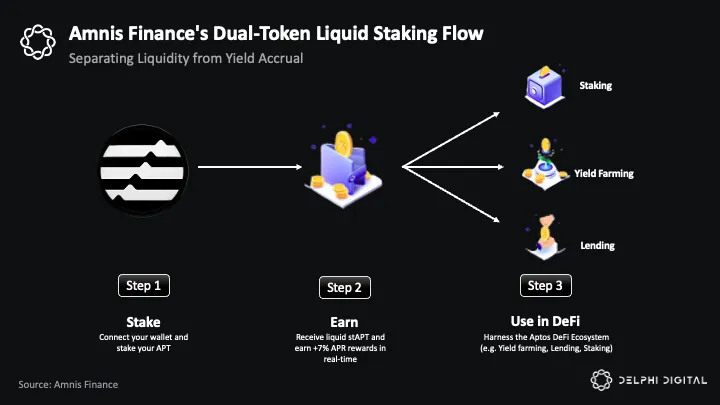

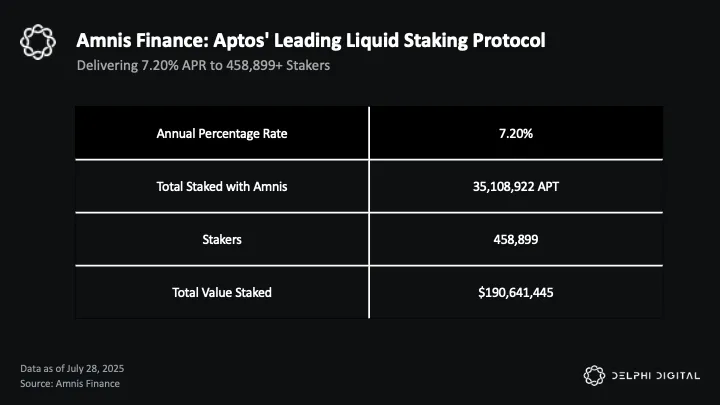

Amnis Finance operates with $183 million in TVL through a dual-token system that separates liquidity from yield accrual. Users can mint amAPT using their APT at a 1:1 ratio, then stake amAPT for stAPT to earn an APR of approximately 7.2%.

The protocol’s structure creates different utility for each token. amAPT acts as a liquid APT derivative that maintains its peg through deep liquidity pools and can be used across Aptos DeFi for lending, LP provision, and yield farming.

stAPT, on the other hand, serves as the yield-bearing vault. It earns 100% of its validator rewards plus 80% of amAPT’s validator rewards, with the remaining 20% directed to Amnis’ treasury.

This mechanism allows stAPT to capture additional yield from the broader amAPT supply beyond standard staking returns. Users can exit positions instantly through amAPT/APT liquidity pools, avoiding the standard 14-day unstaking period, while stAPT holders earn the enhanced 7.2% APR through the protocol’s validator reward allocation system.

Kofi Finance

Kofi Finance captures $32 million in TVL through a dual-token system similar to Amnis. Users can mint kAPT directly using APT at a 1:1 ratio, then stake kAPT for stkAPT to earn an APR of roughly 9.39%.

The protocol separates liquidity from yield through its token structure. kAPT serves as a liquid APT derivative pegged 1:1, tradeable across Aptos DEXs and usable as collateral in money markets. stkAPT acts as the yield-bearing asset where the exchange rate to kAPT increases daily through compounding staking rewards.

Kofi’s yield comes from Aptos’ base staking APR of 7% plus “proprietary boosted yields” that enhance returns for stkAPT holders. Users can exit positions through instant unstaking from stkAPT to kAPT, or swap through DEX partners to avoid the standard 14-day unstaking period. The protocol currently charges zero fees on its liquid staking services.

Advanced Yield Strategies: Multi-Protocol Compositions

We’ve covered individual yield opportunities across Aptos’ DEX, lending, and liquid staking protocols. However, sophisticated users have developed strategies that combine multiple protocols to achieve higher returns through leverage, recursive loops, and cross-protocol composability.

These strategies demonstrate how the Aptos ecosystem enables complex DeFi compositions to operate efficiently at scale. The sub-second finality and low transaction costs make frequent protocol interactions economically viable, while the integrated nature of the ecosystem allows for seamless capital flows between applications.

The following section analyzes observed multi-protocol strategies and their mechanics. These approaches typically involve higher complexity and risk compared to single-protocol farming, but they showcase the sophisticated yield optimization techniques that have emerged within Aptos’ DeFi ecosystem.

Recursive Borrowing Strategies

The most sophisticated yield strategies on Aptos involve recursive borrowing loops that leverage the spread between lending costs and farming returns.

A common recursive strategy involves supplying stablecoins on Echelon, borrowing against that collateral, and then deploying the borrowed funds into high-yield Hyperion pools.

For example, users can supply USDC on Echelon to earn an APR of ~10.24% while borrowing at 9.36%, or supply USDT, earning 7.74% while borrowing at 9.68%.Note that USDC creates a positive spread (earning more than you pay), while USDT creates a negative spread (paying more than you earn).

It’s important to note that users cannot borrow 100% of their supplied value. With LTVs typically at 80-90% for stablecoins, each recursive loop allows borrowing progressively smaller amounts, creating diminishing returns with every iteration.

The borrowed stablecoins can then be paired with APT and deployed into Hyperion pools. The APT-USDC pool currently yields an APR of 318.84%, while the APT-USDT pool offers 226.82%.

This creates a leveraged position where users earn the spread between Hyperion’s LP yields and Echelon’s borrowing costs. The net spread exceeds 300% for USDC strategies and over 200% for USDT approaches.

These strategies introduce significant APT price exposure since the borrowed funds are converted to volatile assets. Their effectiveness depends on maintaining sufficient collateral ratios to avoid liquidation, as APT price movements affect both the LP position value and the borrowing capacity on Echelon.

sUSDe-USDC Looping Strategy

A more sophisticated recursive strategy involves Ethena’s sUSDe, which offers unique yield stacking opportunities due to its underlying structure. On Echelon, sUSDe suppliers earn an APR of 16.4% while borrowing USDC costs 9.36%, creating a positive spread of approximately 7.04%.

This favorable spread enables recursive looping: supply sUSDe as collateral, borrow USDC at 9.36%, convert USDC to sUSDe, and repeat the cycle. Each iteration amplifies the position size while capturing the yield differential. The strategy benefits from sUSDe’s multi-layered yield structure – combining Ethena staking (9.74%), minimal lending demand (0.64%), and APT incentives (6.1%) on the supply side.

With 15.54% utilization on sUSDe versus 89.17% on USDC, borrowing capacity remains readily available for scaling these loops. The $8.64 million in available sUSDe borrowing capacity and $7.25 million in available USDC provide sufficient liquidity for meaningful position sizes.

The upcoming Aave deployment on Aptos could also significantly enhance this strategy’s potential. Aave, making its first non-EVM deployment on Aptos after a successful governance vote in June, brings a history of ~$25 billion in cross-chain TVL. Aave’s more mature risk parameters and potentially different interest rate curves could create additional arbitrage opportunities between the two lending protocols, particularly if Aave offers different LTV ratios or spreads for sUSDe-USDC pairs.

LST Looping Strategy

A more conservative recursive approach involves liquid staking derivatives, which offer leveraged APT exposure with reduced complexity. Users can supply stAPT on Echelon earning an APR of 7.16% while borrowing APT against it at 4.41%, creating a positive spread of 275 basis points.

This enables efficient looping: supply stAPT as collateral, borrow APT at 4.41%, stake the borrowed APT through Amnis Finance to mint additional stAPT at ~7.2% base yield, and repeat. Each cycle increases APT exposure while capturing the spread between staking yields and borrowing costs. The strategy typically generates 30-40% APR through leveraging the base staking yield.

Unlike strategies involving volatile LP positions, LST looping maintains pure APT exposure without impermanent loss risk from asset pairs. The low 4.12% utilization on stAPT also provides ample borrowing capacity for scaling positions.

This approach appeals to users seeking leveraged APT exposure while avoiding the volatility risks associated with DEX farming strategies, though it still carries liquidation risk if the APT price declines significantly.

APT-LST LP Strategies: Leveraged Staking Exposure

Liquid staking derivatives create opportunities for enhanced APT exposure through LP strategies that pair native APT with its staking derivatives. These pools allow users to maintain APT price exposure while earning trading fees and protocol incentives, effectively creating leveraged staking positions without impermanent loss risk from pairing with unrelated assets.

Hyperion and Tapp both offer APT-LST liquidity pools that cater to users seeking amplified APT exposure. Since both assets in the pair track APT’s price movement – one as native APT and the other as a yield-bearing derivative – these pools minimize impermanent loss while capturing the yield differential between staked and unstaked APT positions.

Tapp Exchange

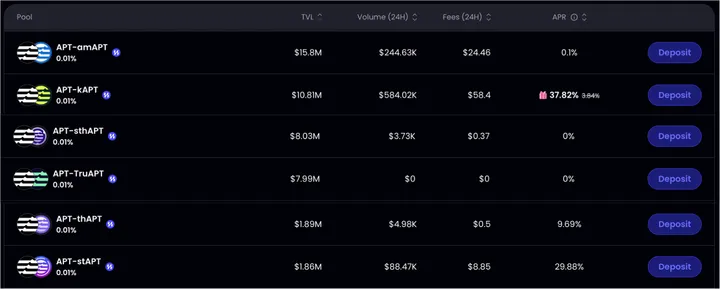

Among Tapp’s APT-LST offerings, several pools stand out for their yield potential. The APT-kAPT stable pool offers an APR of 17.45% with $1.7 million in TVL, pairing native APT with Kofi’s liquid staking derivative. For users seeking higher yields, the APT-stKAPT concentrated liquidity pool delivers an APR of 56.97% with $56,391 in TVL, though the lower TVL suggests this pool requires more active management.

The APT-amAPT stable pool provides an APR of 74.90% with $43,938 in TVL, pairing APT with Amnis Finance’s liquid derivative.

Hyperion

Hyperion offers similar APT-LST opportunities with different risk-return profiles. The APT-kAPT pool provides an APR of 37.82% with a substantial $10.81 million in TVL and $584,000 in daily volume, making it the most liquid APT-LST option. The APT-stAPT pool delivers an APR of 29.88% APR with $1.86 million in TVL, while the APT-thAPT pool offers an APR of 9.69% with $1.89 million in TVL.

These APT-LST pools offer a compelling middle ground for users seeking APT exposure without the complexity of managing volatile LP pairs. The yield differential between platforms – with Tapp offering APRs of up to 74% on smaller pools versus Hyperion’s 37% on larger pools – creates clear trade-offs between yield potential and liquidity depth.

Bitcoin Collateral Strategies

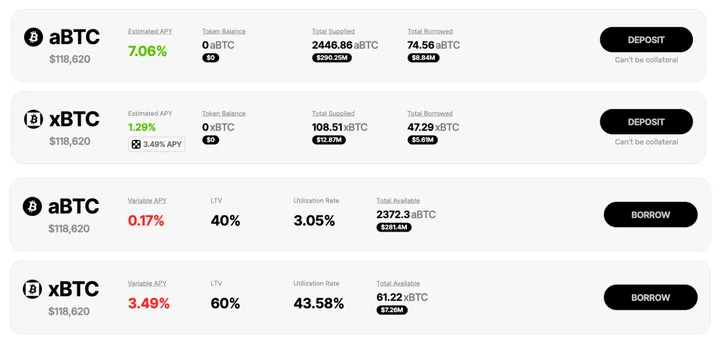

Bitcoin assets on Aptos provide unique collateral opportunities for yield farming strategies, leveraging the network’s growing BTC liquidity across multiple protocols. Users can supply various Bitcoin derivatives as collateral to borrow stablecoins or APT for deployment into higher-yielding opportunities. These include WBTC (wrapped Bitcoin backed 1:1 with native Bitcoin for cross-chain DeFi use), xBTC (OKX’s wrapped token following a 1:1 reserve mechanism), and aBTC (Echo Protocol’s liquid Bitcoin token that enables yield generation from Aptos, Bitcoin Layer 2, and Echo rewards while maintaining full DeFi composability).

Echo Protocol leads Bitcoin lending on Aptos with significant liquidity: aBTC offers an APY of 7.06% with $290.25 million in total supplied, while xBTC provides an APY of 1.29% (plus a 3.49% boost) with $12.87 million supplied.

Though collateralization is currently disabled for retail users, Echo enables it for whitelisted partners, indicating potential for institutional-scale strategies.

Aries Markets provides the primary venue for Bitcoin collateral strategies, with xBTC offering $32.9 million in lending liquidity at 62% LTV. While currently offering a deposit APR of 0%, the substantial liquidity pool enables large-scale borrowing against Bitcoin holdings.

On Echelon, WBTC suppliers can earn an APR of ~7.8% with potential for borrowing against BTC collateral at 70% LTV. The recently launched WBTC market also shows strong early adoption with $1.51 million supplied.

Meanwhile, xBTC integration is expanding across the ecosystem, with full market integration and deeper liquidity expected on Echelon soon, alongside enhanced incentives.

Additional liquidity spans the ecosystem through Hyperion’s xBTC concentrated liquidity pools, which maintain ~$4 million in total liquidity for trading and LP strategies.

Users can leverage these Bitcoin markets to borrow stablecoins or APT at attractive ratios, then deploy borrowed capital into high-yield opportunities like Hyperion’s LP pools. The combined Bitcoin lending infrastructure – over $330 million across Echo and Aries alone – positions Aptos as a significant hub for Bitcoin-collateralized DeFi strategies.

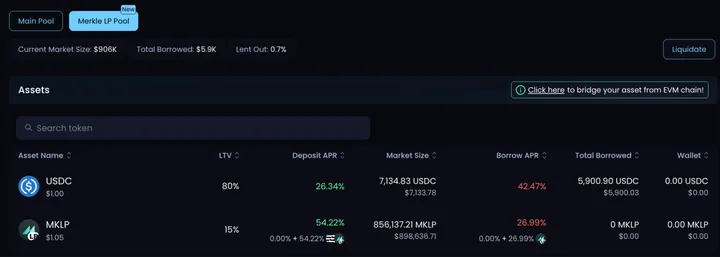

Aries x Merkle MKLP Strategy

A unique cross-protocol opportunity exists through Aries Markets’ isolated MKLP pool, which allows users to deposit Merkle Trade’s LP tokens as collateral while earning the underlying protocol yields. This strategy combines Merkle’s perpetual trading fees with leveraged position scaling through Aries’ lending infrastructure.

The mechanics involve depositing MKLP tokens to earn Merkle’s base APR of 54.22% while using them as collateral at 15% LTV on Aries. Users can then borrow USDC at an APR of 42.47% against their MKLP collateral and convert the borrowed USDC back to additional MKLP tokens, creating a recursive loop.

The strategy benefits from MKLP’s dual yield sources: earning fees from Merkle Trade’s perpetual trading activity while accessing leverage through Aries’ isolated lending pool. With $898,636 in MKLP market size and 0% current utilization, the pool offers substantial room for scaling these positions.

While the borrowing cost of 42.47% appears high relative to the 54.22% MKLP yield, the leveraged nature of the strategy can amplify the net spread through multiple iterations. The isolated pool structure also ensures MKLP-specific risks don’t affect other positions on Aries, providing controlled exposure to this specialized yield farming approach.

Risks and Considerations

The advanced yield strategies outlined above demonstrate sophisticated protocol interactions that have emerged within Aptos’ DeFi ecosystem. However, these multi-protocol compositions introduce several risk factors that users should understand before deploying any capital.

Liquidation Risk

Leveraged strategies involving borrowing against collateral face liquidation risk if asset prices move unfavorably. Recursive borrowing strategies that convert stablecoins to APT for Hyperion LP positions are particularly exposed to APT price volatility. A significant APT price decline can trigger liquidation cascades where both the LP position value and borrowing capacity deteriorate simultaneously.

LST looping strategies, while more conservative, still carry liquidation risk if APT prices fall substantially relative to borrowed amounts. The tight spreads that make these strategies viable can quickly turn negative during market stress, requiring active position management.

Smart Contract and Protocol Risk

Multi-protocol strategies increase exposure to smart contract vulnerabilities across multiple applications. Users deploying capital across Echelon, Hyperion, and other protocols simultaneously face compounded smart contract risk. Additionally, protocol changes – such as interest rate adjustments, fee modifications, or incentive program alterations – can impact strategy profitability without warning.

The integration risks between protocols, while minimized by Aptos’ technical architecture, still exist. Cross-protocol strategies depend on continued interoperability and liquidity availability across multiple venues.

Market and Liquidity Risks

High-yield strategies often depend on specific market conditions and liquidity availability. The substantial APRs observed in Hyperion pools reflect current trading volumes and fee generation, which can fluctuate significantly based on market activity and user behavior.

Impermanent loss in volatile LP pairs, while discussed as minimal in APT-LST strategies, can still occur if the price relationship between paired assets diverges from expected correlations.

These risk considerations highlight the importance of understanding both individual protocol mechanics and the compounded risks inherent in multi-protocol yield strategies.

Yield Volatility and Performance Disclaimers

The APR figures and yield opportunities discussed throughout this analysis are based on historical rolling 30-day data captured during our research conducted in July and August 2025.

These yields represent past performance during specific observation periods and fluctuate continuously based on trading volumes, liquidity provision levels, protocol incentive changes, and broader market conditions.

Users should not expect these rates to remain constant or view them as guaranteed returns. Actual yields experienced may vary significantly from the historical figures presented, and all yield farming strategies carry the risk of lower-than-expected returns or potential losses.

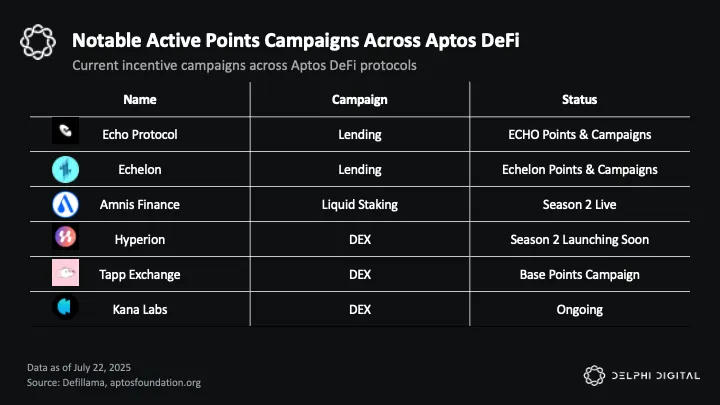

Points Programs and Additional Incentives

The yield opportunities and strategies we’ve analyzed represent one important dimension for users navigating Aptos’ DeFi ecosystem. However, many protocols also implement additional incentive mechanisms worth understanding, as they layer reward programs on top of their base yield generation.

Beyond direct yields, several established protocols operate active points campaigns. These programs reward user engagement through lending, trading, and providing liquidity, creating additional value streams parallel to core yield offerings.

The following active campaigns demonstrate how protocols structure additional incentives to complement their base yield offerings:

Echo Protocol operates comprehensive points campaigns alongside its Bitcoin liquidity aggregation services. Users earn ECHO points through various protocol interactions, including bridging, staking, lending, and utilizing aBTC across Aptos DeFi strategies. The protocol runs targeted campaigns with point multipliers, offering up to 5x boosts for specific activities like deploying aBTC in yield strategies.

Echelon Market launched Season 2 of its points campaign following Season 1’s conclusion on March 9. Season 1 distributed 60 billion points across $160 million in TVL to over 60,000 wallets. The lending protocol offers enhanced earning rates of 2 points per $1 lent and 4 points per $1 borrowed for assets like sUSDe, USDC, and USDT, with an additional 10% referral bonus. Echelon also runs bi-weekly campaigns with boosted multipliers, currently featuring 2.5x rewards on major stablecoins.

Amnis Finance launched Season 2 of its points program following the $AMI TGE in March. The campaign allocates 1% of AMI supply for distribution based on points accrued during the season. Users earn points by staking APT through Amnis, utilizing amAPT/stAPT tokens across Aptos DeFi protocols, and referring new users to the platform.

Hyperion recently concluded Season 1 with the $RION token launch on July 15 and has since launched Season 2. The current campaign features boosted APRs across pools through DRIP incentives. Season 1’s conclusion with an actual token distribution provides a concrete example of how points campaigns can translate into token allocations.

Tapp Exchange rolled out its ongoing “Base Points” reward system to continuously reward liquidity providers and traders. The DEX awards 10 points per $100 in TVL per day for liquidity provision and 4 points per $0.01 in trading fees. Points accumulate continuously rather than through seasonal campaigns.

Kana Labs operates an ongoing rewards program featuring both referral mechanics and transaction-based points earning. The commission-based referral system provides bonuses and early access perks to top-performing affiliates. Additionally, users earn reward points for every transaction on Kana Labs, contributing to a Season 2 program where points can be redeemed for KANA tokens and other benefits.

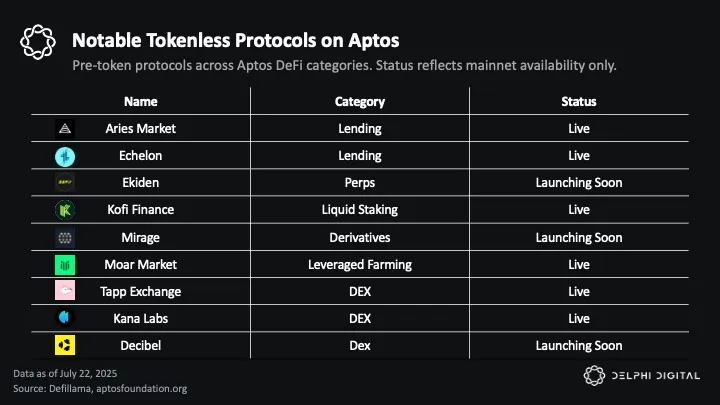

Notable Tokenless Protocols

Beyond the established protocols generating yields and running incentive campaigns, Aptos is home to several notable projects that have yet to launch native tokens. Some of these protocols are actively running the points campaigns outlined in the previous section. These protocols span various DeFi categories and represent different stages of development and adoption.

While the timing and structure of potential future tokenizations remain entirely at the discretion of individual protocol teams, these pre-token protocols have attracted user attention as part of Aptos’ developing landscape. Historically, when DeFi protocols introduced tokens, early users were often included in distribution mechanisms.

Understanding which protocols operate without tokens provides useful context for the ecosystem’s current state and development trajectory. It also sheds light on user behaviors around pre-token protocol engagement.

The following protocols represent notable tokenless projects across key DeFi categories:

Aries Market is Aptos’ largest lending protocol offering borrowing and lending services across major assets, including APT, USDC, USDT, and Bitcoin derivatives, with over $350 million in TVL. The protocol has been live since Aptos’ early days and serves as the ecosystem’s primary money market infrastructure. The protocol’s established position makes it one of the most anticipated potential launches in the ecosystem.

Echelon operates as one of Aptos’ largest lending protocols with over $110 million in TVL. As mentioned in the previous section, the protocol is currently running Season 2 of its points campaign with enhanced earning rates and bi-weekly multiplier campaigns.

Ekiden is a hybrid orderbook exchange built on Aptos, combining off-chain CLOB infrastructure with on-chain settlement to target both high-frequency traders and institutional users. The platform focuses on perpetual markets with sub-20 millisecond execution speeds and plans to offer 0% maker fees at launch. Ekiden currently operates in private testnet with public testnet expected next month, followed by mainnet deployment.

Kofi Finance is a liquid staking protocol offering boosted yields through MEV revenue sharing and leveraged liquid staking vaults. Users stake APT to receive kAPT tokens, which can be further staked for stkAPT to earn enhanced rewards and used across the Aptos DeFi ecosystem.

Mirage Protocol combines CDP stablecoin issuance with perpetual trading, allowing users to mint mUSD stablecoins against collateral for trading perpetuals on an integrated DEX. The protocol remains in development with mainnet deployment expected soon. Plans include a MIRA token using a veToken model.

Moar Market provides leveraged trading and yield farming with up to 15x leverage, offering money markets and structured strategies that deploy capital across protocols like Hyperion. The protocol remains in development with mainnet deployment anticipated soon.

Tapp Exchange operates as a DEX on Aptos offering various liquidity pools and trading pairs. As mentioned in the previous section, the protocol recently launched its ongoing “Base Points” reward system with continuous point accumulation for liquidity providers and traders.

Decibel is a fully on-chain trading engine that unifies spot, perpetuals, and margin into one programmable platform. Developed by the Decibel Foundation in collaboration with Aptos Labs, the protocol features 100% on-chain order matching with cross-margin multi-collateral accounts and X-Chain funding capabilities. Decibel is currently live on Devnet.

Conclusion: Aptos’ Yield Landscape in Practice

As outlined in our previous report “Inside the Ecosystem: Fueling Aptos’ Global Trading Engine,” the differentiating factor for blockchains today lies in the applications and opportunities available to users. This is what drives real adoption and engagement.

Aptos is developing in this direction. The ecosystem features a substantial DeFi landscape with compelling opportunities across lending, trading, and liquid staking protocols. Users can access a range of strategies: from conservative APRs of 10-16% on stablecoin yields to sophisticated leveraged strategies exceeding 200%. Technical infrastructure and deep stablecoin liquidity combine to enable multi-protocol compositions. Speed and low costs are table stakes, but meaningful institutional strategies require both technical performance and liquidity depth.

The ecosystem also shows institutional interest. Aave’s decision to make its first non-EVM deployment on Aptos represents credibility for the platform’s DeFi capabilities. The recent addition of WBTC support and growing Bitcoin-related DeFi infrastructure, combined with targeted incentives across lending markets, demonstrates coordinated efforts to capture diversified liquidity flows.

These developments help explain why Aptos has emerged as a stablecoin hub, holding over $1.3 billion in native USDC and USDT.

For users on Aptos, opportunities vary by strategy and risk appetite. Conservative capital can earn steady stablecoin yields while accumulating points from established pre-token protocols. More aggressive farmers can chase higher APRs on Hyperion pools or capitalize on Bitcoin DeFi incentives as that infrastructure develops. The ecosystem supports both institutional-scale strategies and active farming approaches at meaningful scale.

0 Comments