Avoiding the Real Banking Iceberg

MAR 23, 2023 • 38 Min Read

The Tip of the Iceberg

We’ve been saying for months that access to funding would be one of the biggest risks to the crypto industry this year. Never has that been more relevant than right now.

But the storyline here is bigger than crypto. It’s even bigger than the banks. This is a story about the evolution of economies, our reliance on debt, and the corner we’ve gradually backed ourselves into, leaving the best path forward a choice between two evils rather than a triumphant declaration of growth and prosperity.

Debt is the backbone of our economy, which means any disruptions to the flow of credit are disruptions to economic growth. When credit conditions tighten, it can have substantial ripple effects on everything from businesses to jobs to consumers to investors. If the US economy is an engine, credit is the oil. Without it, the car won’t run.

Aging demographics and productivity declines have pushed the US economy to become more and more reliant on debt to fuel economic growth. As the demand for debt has grown, so too has the need for more supply from those who are capable of providing it. Banks are a key provider of debt funding, and while it may seem like they have unlimited powers, their capabilities do have real limits. And those limits may be tested at a very inopportune time.

A lot of the attention so far has been on deposit outflows, and for good reason. Deposits are important — and we’ll get to why — but they aren’t the most limiting factor for bank lending and credit growth. The real key is bank capitalization.

Banks are required to maintain a certain amount of capital to serve as a buffer against any losses that may arise. When banks are profitable, they can retain some (or all) of those earnings to increase their capital base, which increases their capacity to acquire more assets or make more loans.

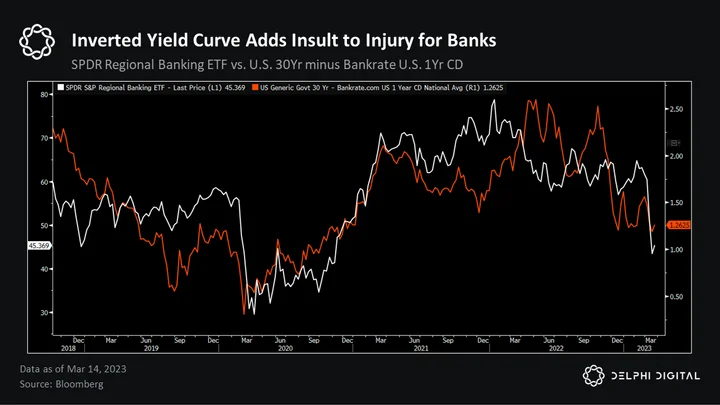

The problem now is funding costs have risen substantially and bank margins are starting to get squeezed. An inverted yield curve puts a lot of pressure on banks’ profitability, and thus their ability to grow their capital base.

Large deposit outflows only add further strain. The growing popularity of higher-yielding alternatives like MMFs has increased competition for banks to attract (and retain) deposits, leaving them in a precarious position.

If banks don’t have enough cash on hand to honor withdrawals, it forces them to source liquidity in less favorable ways. Banks may have to borrow funds at higher rates or may even be forced to sell assets, potentially exposing them to realized losses. If these losses are big enough, it will reduce a bank’s capitalization level, which means less balance sheet capacity to fund loans or extend credit. In an extreme case, losses can wipe out a bank’s capital buffer, turning a liquidity crisis into a solvency crisis.

The rapid rise in interest rates has had a negative impact on the value of longer duration assets — like investment securities and loans — which make up a vast majority of bank balance sheets (as we’ll show). If you underwrote a loan last year that pays 3% interest and now similar loans pay 5%, your loan isn’t worth as much and, if you did have to offload it, the market would require a discount to buy it.

Loans and securities makeup ~$17.5T of US commercial banks’ assets. If we do some quick math and assume higher rates equate to a 10% haircut on these assets, which implies a $1.75T loss if these were marked-to-market today.

One recent study estimates the market value of US banking system assets is $2T lower than suggested by their book value. Total equity capital for US banks is ~$2.14T, which doesn’t leave a whole lot of buffer if banks are forced to realize significant losses.

This would be an extreme scenario though, and not one we believe is very likely. But even if banks are able to avoid substantial losses by borrowing against their assets, there’s another problem caused by higher rates.

Even if we avoid a full-blown banking crisis, a lot of damage has already been done. One of the biggest downstream headwinds in our view is a material slowdown in credit growth and tighter financial conditions.

We’ve already seen financial conditions tighten dramatically since last week, and a pullback in lending now would be like attaching a ball and chain to the economy and telling it to swim.

This comes at a time when bank lending was already starting to cool off and lending standards were tightening. Since we know credit is a critical support for economic growth, an acceleration in this trend raises the odds we see a recession.

Recessions mean lower private sector profits and higher unemployment, adversely impacting a large cohort of the very people and entities banks have lent to. Loans make up a majority of commercial bank assets, so an increase in loan losses would reduce a bank’s capital (aka their “buffer”) and thus their capacity to continue lending.

That is why lending activity has to stay active because if the flow of credit dries up, economic growth will suffer. Private sector profitability will get squeezed, unemployment will rise, and demand will fall as it does in every recession. Deteriorating liquidity in the financial system is a major risk to many people, not just investors.

The risk of higher borrowing costs and the expected tightening in credit conditions could create serious vulnerabilities for many companies – and the economy as a whole – if these debts cannot be rolled over (or have to be refinanced at much higher rates). The current financial system is more of a refinancing engine that requires enough balance sheet capacity to ensure this mountain of debt can be rolled over, a topic we discussed in our “Liquidity Runs The World” report last year and again in our “Markets Year Ahead.”

In other words, the real risk of higher rates and tighter liquidity conditions isn’t that it impacts borrowing costs on new debt, but that it creates larger risks for those who need to rollover existing debts.

The Fed’s decision to raise rates another 25 bps this week made it clear they don’t see this as a real issue, at least right now. But the market is betting the Fed will have to cut rates later this year, and there’s good arguments for it.

If the Fed were to cut rates, it would have an immediate impact on funding conditions, among other benefits:

- Increase the value of their investment securities, reducing potential losses if/when banks want to offload them.

- Steepen the yield curve, which benefits banks who are in the business of borrowing short and lending long.

- Wider margins means more profitability (and/or lower losses), which strengthens bank capitalization and increases their capacity to sustain much needed lending activity.

- Make current deposit rates m

Read the full report

This report is part of Delphi Pro.

- 800+ Pro reports across every major sector

- Talk directly with our analysts

- Private community of funds and builders

Already a Pro member? Log in

0 Comments