Introduction

Mobile is the dominant global gaming platform. The proliferation of fast wireless internet and comparatively low hardware costs are key factors that are driving widespread adoption. It has been reported that in 2022, consumers spent an average of five hours per day on their mobile devices. That represents one-third of all waking hours and a 3% increase from the year before. Aside from “everything apps” like WeChat, LINE, and maybe one day X, mobile gaming is a leading factor in why humans are spending an increasingly long time on mobile devices.

The most recent estimates state that by the end of 2023, there will be a total of 3.38B gamers, and this number will grow 12% to reach 3.79B by 2026 (representing a CAGR of 4.3% from 2021 to 2026). Out of those 3.38B, more than 80% are expected to engage with mobile gaming content in some form. Furthermore, >50% of gaming’s $184.4B in global revenue in 2022 came from the mobile market segment. Despite the challenges, this figure is expected to grow by $400M by the end of 2023 and surpass $100B by 2026 (from an estimated global total of $212.4B).

Mobile game downloads reached 90B in 2022 (35% of the global total) and have remained relatively stable after an initial boost thanks to COVID lockdowns. Mobile gaming revenues, on the other hand, declined for the first time in history in Q1 2021. Since then, revenues have continued to fall for five consecutive quarters. Apple remains the most profitable hardware of choice, accounting for 62% of total in-game spend, and has also demonstrated its resilience over Android, with revenue falling 4% against Android’s 16%. Additionally, there are more than 1.5M mobile games available across the Apple and Google app stores. Operators in this increasingly competitive market are feeling more pressure than ever before to explore alternative genre mixes, novel monetization models, and new forms of distribution. This report will put forward the bull case for blockchain games taking a mobile-first approach, outline the opportunities and challenges in implementing this new technology, and highlight some of our key areas and projects of interest.Why Web3 Mobile

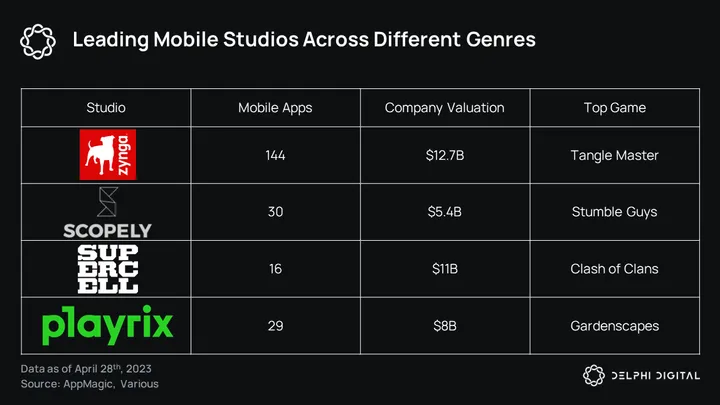

The two most often-cited reasons for the slowdown in mobile gaming’s meteoric rise and slight retrace from its all-time highs are the post-pandemic normalization of key metrics and the arguably more impactful privacy changes made across mobile’s two most prominent platforms. Without going too deep into the weeds, the changes to Apple’s Identifier for Advertisers (IDFA) and Google’s Advertising ID (GAID) made it more challenging for mobile businesses to effectively collect and analyze user data in order to optimize user acquisition (UA), retention, and revenue per download (RpD). To put things into perspective, in 2022, total mobile ad spend reached $336B (a 13.8% increase from the year before). These changes were a mighty blow for certain mobile gaming genres, where data analytics are critical for scale and profitability. Although hypercasual was the hardest hit by these changes, all genres have been impacted to a certain extent. Total consumer spend has dropped by 3% YoY to $124B, a reported 40% of mobile companies reported losses post-IDFA, and 75% of these businesses said that the losses put their businesses at risk. Privacy changes are just one example of why the cost-per-installs (CPI) is increasing and the lifetime value (LTV) of mobile players is declining. The chances of building a breakout success have decreased, and the incumbent giants have a clear advantage in this increasingly hostile environment, with titles like Scopely’s Monopoly Go! spending an estimated $2.5M per day on UA! As consolidation continues and valuations increase, how can indies compete?

Privacy changes are just one example of why the cost-per-installs (CPI) is increasing and the lifetime value (LTV) of mobile players is declining. The chances of building a breakout success have decreased, and the incumbent giants have a clear advantage in this increasingly hostile environment, with titles like Scopely’s Monopoly Go! spending an estimated $2.5M per day on UA! As consolidation continues and valuations increase, how can indies compete?

We are now observing a new trend in mobile gaming, with several genre-specific developers attempting to increase the depth of their monetization models. There is a clear move away from ad revenue-only strategies and a larger emphasis being placed on boosting retention and increasing consumer spend on in-app purchases (IAPs). We believe blockchain technology, if implemented in the right way, can have a meaningful impact on these initiatives.

Mobile gamers are inherently more accustomed to many of the monetization practices that share a lot of synergies with blockchain technology. After pioneering the F2P model in the early 2010s, in-game spending now represents approximately 97% of global mobile revenue. Outside of hybridcasual, 66% of top-performing mid-core mobile games implemented gacha mechanics, and a reported 73% of global revenues came from loot boxes. Both features have strong synergies with blockchain integration, as do many of the abundant forms of pay-to-win (P2W) mechanics prolific throughout the mobile segment.

In addition to the wide design overlap between blockchain and mobile games, they also target very similar users. North America is widely accepted as one of the top-spending mobile gaming markets (outside of China) and is also considered the international hub for a lot of Web3 activity. Furthermore, established markets such as South Korea and Japan have some of the highest levels of mobile adoption, and emerging markets in South America and Asia, such as Brazil, India, and the Philippines, have shown rapid growth in blockchain adoption. All of these regions should be considered top markets of interest, and games with localized go-to-market strategies stand to benefit the most.

Finally, both Apple and Google have recently taken steps to reduce the regulatory restrictions on blockchain-based applications for their respective mobile platforms. As such, the opportunities for teams to target new well-adjusted markets or increase player LTV via strategic blockchain integrations have never been more significant.

Obstacles to Adoption

Mobile gaming, by and large, is gate-kept by Apple’s App Store and the Google Play Store. Despite many core tenets of blockchain gaming pointing toward a decentralized future where power is taken away from the central powers, games currently still require centralized servers and distribution to scale (in stark contrast to the approach made by fully on-chain games and autonomous worlds). As outlined in our Primer for Web3 Distribution and The G

Read the full report

This report is part of Delphi Pro.

- 800+ Pro reports across every major sector

- Talk directly with our analysts

- Private community of funds and builders

Already a Pro member? Log in

0 Comments