The Year Ahead for Crypto 2025 – Full Series:

AI+DePIN

DeFi

Gaming

Infrastructure

Markets

Consumer DeFi Is Almost Here

The practice of de-banking has been thrust into public discourse after Marc Andreesen’s recent appearance on the Joe Rogan Experience. It’s turning into crypto’s ‘me too’ movement, with numerous individuals, many of whom are in crypto, coming forward with their debanking stories.

DeFi has rebounded convincingly from a multi-year slumber, and the outlook is as strong as ever, with strong tech and a friendly regulatory environment ahead. But debanking is an important reminder of why we are here. DeFi hasn’t truly arrived until it offers a viable alternative to permissioned finance.

We have explored potential avenues for DeFi to make an impact in the real world in prior years, discussing opportunities with undercollateralized lending and payday loans. Heading into 2025, the bankless pipedream appears to be within reach for the first time.

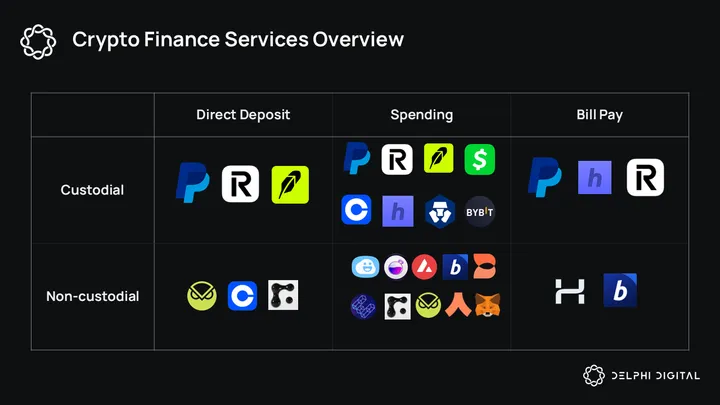

Spending

Seamless flow of everyday purchases with crypto assets is a prerequisite for this vision to emerge. Crypto debit cards have gone from a novelty to a saturated market very quickly, with numerous crypto cards hitting the market.

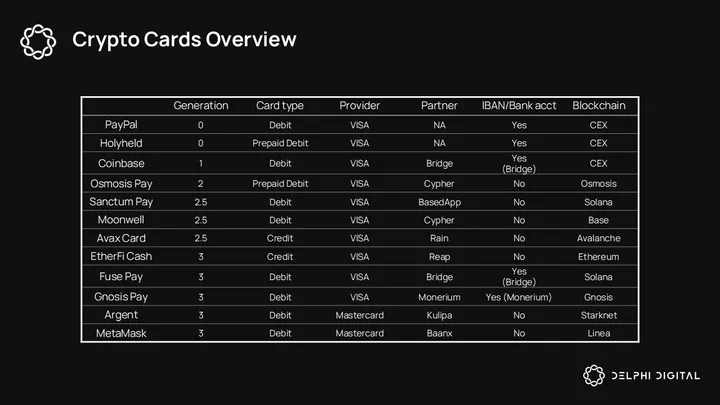

Gen 0: Custodial, prepaid, spend fiat debit cards. Converts crypto assets upon deposit (glorified offramp)

PayPal, Holyheld

Gen 1: Custodial, prepaid, spend crypto debit cards. Fiat conversion happens at payment. These are significant because they let users retain exposure to crypto assets until spending.

Coinbase, Crypto.com, Revolut, Nexo, Wirex, other CEX cards

Gen 2: Non-custodial, spend crypto prepaid debit cards. Card linked directly to a non custodial crypto wallet, but users may not have access to the private keys or be able to load an existing wallet. Crypto assets converted to fiat at the moment of purchase, but are often secluded from the rest of DeFi and require manual top-ups.

Osmosis pay, Sanctum pay, Moonwell, Avalanche

Gen 3: True self-custody, spend crypto smart contract wallet debit/credit cards. Flexible, programmable, capable of interacting with DeFi.

Gnosis Pay, Fuse Pay, Metamask card, Argent card, EtherFi

The difference between gen 2 and gen 3 cards is somewhat blurry and lies on a spectrum. Some gen 2 cards may be non-custodial, but the user may not have complete access to the private keys. Gen 2 cards often have interesting features that differentiate themselves from vanilla gen 2 cards. The real debit & credit cards offered by gen 3 enables spending on a wider range of goods and services and expands options for DeFi composability.

Loosely classifying these cards into generations has nothing to do with their UX. This exercise is about sorting what we know about their onchain capabilities and self-custodial properties. Most of the cards listed are soon to be released or slowly rolling out.

Holyheld

Holyheld has become CT’s favorite crypto card and most popular by top up volume. While Holyheld works with any non-custodial wallet, the card itself is custodial and spends fiat EUR. It also comes with a native IBAN. When a user tops up their card, they are sending money to an EUR account with Holyheld that conducts their eventual payment, which is not viewable onchain. For this reason, Holyheld is technically classified as a gen 0 card, as it is essentially a crypto offramp solution that requires frequent top ups.

There is little improvement of Holyheld over sending money to a PayPal account and converting to USD. The user flow of sending USDC to Coinbase and swiping a Coinbase debit to pay with USDC is likely superior. PayPal and Coinbase also offer native yield of 4-5% for idle cash.

What Holyheld does well is make top-up/offramp user flow incredibly smooth. Holyheld supports over 1000 cryptocurrencies on numerous blockchains. Top-ups are gasless and take less than a minute. If a user has a passkey, they do not even need a wallet. Holyheld recently breached $2M in weekly top ups, demonstrating the demand for this type of product with a strong UX.

Holyheld’s current offering will struggle to remain competitive as more polished, self custodial solutions that live within DeFi continue to emerge. Holyheld’s antidote for this is the Blockchain Reconciliation and Remittance Record (BRRR protocol), for which they recently raised funding.

Gnosis Pay

Gnosis Pay kicked off 3rd gen cards when they unveiled the first non-custodial debit card at EthCC 2023. Gnosis Pay allows users to turn their Safe wallet into a non custodial bank account, complete with a Monerium issued IBAN and the capability of making SEPA transfers directly from the user’s blockchain address.

Gnosis Pay is a single signer Gnosis Safe wallet controlled by the user’s EOA. Gnosis Pay Safe has 2 custom modules, a roles module and a delay module. The roles module configures basic parameters such as tokens used and daily spending limit. The delay module ensures that all non-card transactions (i.e. sending funds to another address) are subject to a 3 minute delay. This delay enables best practices security and prevents double spending, but prevents the user from using the Gnosis Pay Safe within DeFi, requiring regular top-ups like other cards. Gnosis Pay is available on Gnosis and supports EURe and GBPe. For more on Gnosis Pay, see our EthCC report.

Zeal, a smart wallet on top of Gnosis, offers a web app and additional features to improve the UX. Zeal enables auto top-ups to a user’s Gnosis Pay Safe, allowing them to earn yield with sDAI and sell for EURe when the spending balance falls below a specified threshold. Eventually, we will see more creative DeFi integrations built with this type of logic. Users will soon be able to transfer from smart wallet to any IBAN, enabling rent and other bill payments.

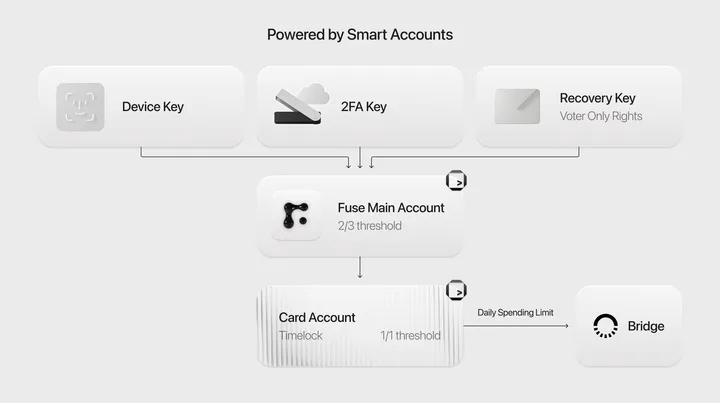

Fuse Pay

Fuse Wallet is a smart wallet built on Squads protocol on Solana. Fuse has an integration with Drift for yield and will soon incorporate Jupiter for swaps. Fuse Pay also has a partnership with Bridge, offering direct deposits and spending from self-custody. Fuse Pay and Gnosis Pay do not have “top ups” in the sense that users are transferring crypto to a foreign account. Users are transferring funds to a carveout within their smart wallet/Safe and retaining full custody. Direct deposit is currently available in the US, and the Fuse Pay card will launch soon.

EtherFi Cash & Avalanche Card

EtherFi Cash and Avalanche cards mimic credit cards buy allowing users to spend their crypto assets or borrow against them from onchain liquidity pools. These cards support LSTs like sAVAX and eETH, and allow users to pay down debt with yield generated. The Avalanche card will start out with its own liquidity pools, and EtherFi will use a special Cash pool on Aave. Interest rates will be determined by the utilization rate model. EtherFi will give users a passkey for seamless control over their smart contract wallet, and will build out integrations with various DeFi apps.

Exactly finance is a lending protocol on Optimism that allows anyone to turn their Gen 2 card into a credit card like experience through their dApp. The architecture is similar to EtherFi and Avalanche, but sits on top of Exactly Finance pools.

Argent & Metamask

The vast majority of non-custodial crypto cards are prepaid debit cards that require frequent top ups. These cards vary in the degree to which they are able to obfuscate this process from the user flow and curate unique experiences (mimicking credit cards, offering savings yield). Custodial CEX cards are wallet-linked and convenient, but come with shady history and account closure concerns.

Argent and Metamask have introduced new cards that enable users to spend crypto directly from their main wallets. These cards eliminate the need to continuously top up prepaid cards, reducing UX friction and addressing the time-value cost of capital often associated with prepaid or carveout solutions. In order to minimize time value opportunity cost, users must increase mental maintenance overhead. This innovation provides users with seamless access to DeFi and greater financial freedom.

Argent & Metamask’s card setups could introduce additional risk, as the user is trusting the card partner with a greater surface area of their portfolio. If these cards are able to mitigate security concerns and work as advertised, we likely see the birth of Gen 4 in 2025. It is worth noting that many of the more advanced Gen 3 cards also have this capability. There is no technical reason Fuse and Gnosis Pay cannot offer this; the delay module is all that prevents preventing Gnosis Pay users from swapping memecoins to EURe in the checkout line before purchasing a burrito.

A user is likely not going to hold their main stash on a mobile wallet they use to interface with their Metamask card. Therefore, additional UX wrappers are necessary for both Gen 3 and Gen 4 to truly unlock the next level experience.

Crypto Banking Services

Crypto cards are making great progress, but for users to fully immerse themselves in DeFi, banking features such as direct deposit and bill pay are necessary.

PayPal

PayPal offers users a modern Web2 fintech payments platform with a direct deposit option. PayPal has ventured into crypto over the past few years, offering the ability to buy, sell, and transfer a small selection of crypto assets. Its crypto presence revolves around its stablecoin, PYUSD, available on Solana and Ethereum.

PayPal offers a virtual debit card that can spend from a PayPal account balance or pull from users’ other banking cards. It does not allow users to spend crypto or PYUSD yet, which creates additional steps for those who wish to offramp through PYUSD for spending. PayPal also allows users to use their virtual bank account and routing number for payments, resulting in an e-check option that can pay bills including rent, car payment, utilities, credit card bills, etc.

PayPal is currently the most comprehensive solution available. It can do everything: spending, bills, rent, direct deposit, yield, etc. Venmo ‘s growing traction as a payment option makes the setup even more attractive.

Other Crypto-Friendly Fintechs: Robinhood, Cash App, Revolut

Robinhood, Cash App, and Revolut are examples of other crypto-friendly fintechs that offer similar feature sets to PayPal: the ability to purchase and transfer crypto assets, direct deposit, and a custodial debit card for spending, although most of these lack a bill pay feature. Revolut offers bill pay, and Robinhood offered it until the feature was sunset in June-24.

For now, these options lack some of the more CEX-heavy features but offer a comprehensive experience on the legacy finance side. They have the ability to onboard a wide range of users as they do not come with as many lifestyle adjustments, and they have signaled intentions of growing their presence in crypto. Revolut has launched Revolut X, a standalone cryptocurrency exchange, and there are rumors that Revolut and Robinhood are building stablecoins of their own.

Coinbase

Coinbase offers a suite of features that mimic traditional banking. It offers direct deposit to a Coinbase account and a high yield (5%) on idle USDC stored in the account. The Coinbase debit card allows users to spend with USDC or USD, a strong differentiator from other options. A user could send USDC to Coinbase and pay with their debit card once the transaction is registered, without any extra steps.

More recently, Coinbase has bootstrapped strong user activity on Base, and shipped increased integrations with Coinbase Wallet and Smart Wallet:

- Coinbase Onramp partnership with ApplePay

- Partnership with Bridge to bring direct deposit on-chain to Coinbase wallet on Base

- Expanded the USDC high yield program from Coinbase accounts to any USDC balances held on Base.

Other CEXs Dabbling in Banking: Crypto.com, Bybit, Nexo

There are a variety of other CEXs with popular debit cards that allow users to receive direct deposit to their accounts. These have been the most popular crypto cards over the past few years, offering impressive perks, loyalty rewards, and in Nexo’s case, a credit card. Like Coinbase, they do not allow users to repurpose their direct deposit bank information to pay bills. These solutions are ideal for crypto-natives, but they may struggle to compete with the Fintechs that add CEX features. For this reason, Coinbase’s onchain migration appears to be a very smart move.

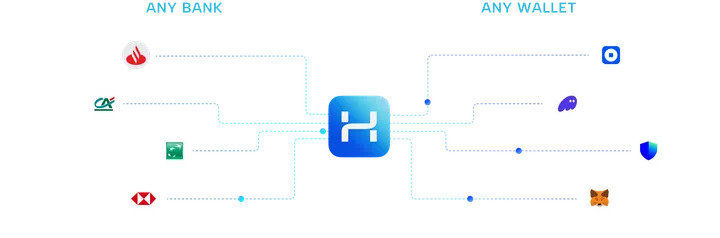

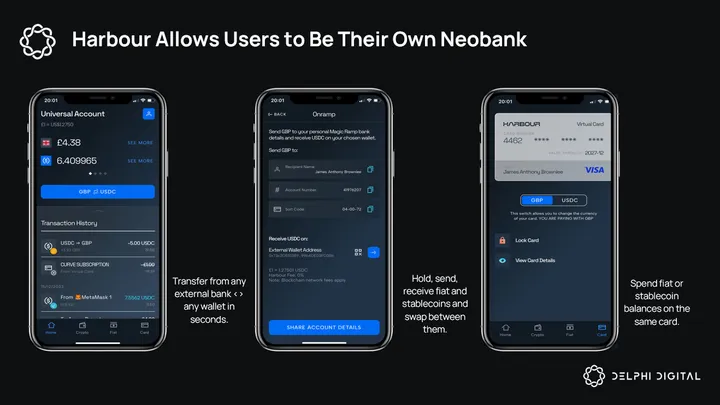

Harbour

Harbour is a promising project that can help many of the different products discussed here work together more closely. It’s flagship product, Magic Ramp, is a competitor to Moonpay, offering far cheaper onramp costs (0.5% vs. 1-4.5%).

In cooperation with their banking partner, Harbour issues real bank accounts and ties them to onchain addresses. It has the logic and liquidity on top to seamlessly convert offchain money to onchain money and vice versa.

Users can send USDC to Harbour, convert to GBP, using local payment rails to send it to their bank account. Harbour supports IBAN and will soon offer direct deposit. It is live in Europe with plans to expand to the US and other regions soon.

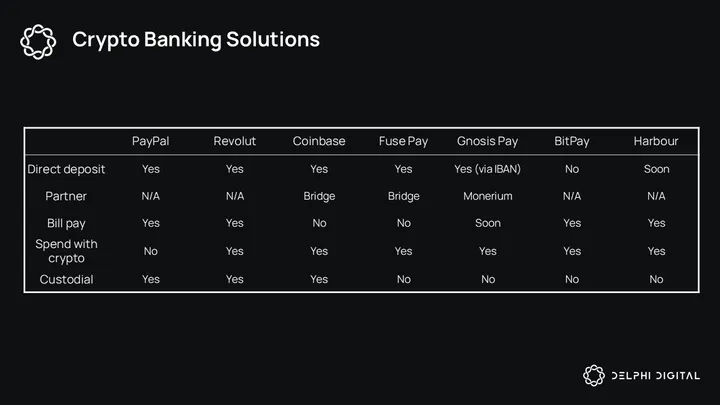

PayPal, Harbour and BitPay offer differentiation through bill pay. PayPal offers the full stack of banking services, but is in a custodial account.

BitPay: Non-custodial wallet for storing and spending crypto. No direct deposit, but offers bill pay in select US States. Only one to offer US bill pay from non-custodial wallet.

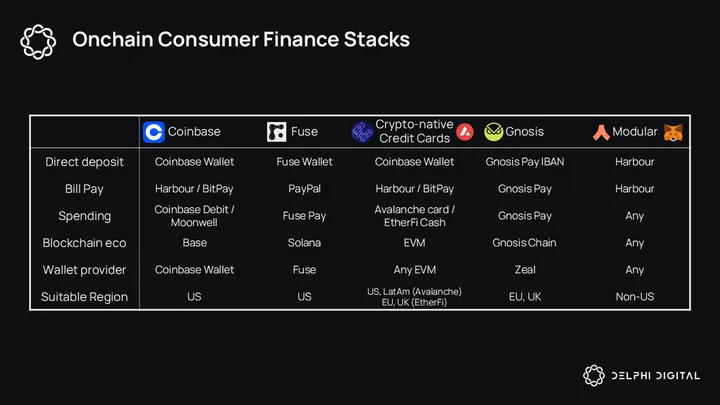

End-to-End Crypto Banking Stacks

Combining various crypto cards and banking services allows for a variety of personal finance DeFi stacks to emerge. The UX may be clunky for now, but for those determined to do so, conducting finances end-to-end in crypto is possible.

As the leaders on the banking side, PayPal and Coinbase anchor most personal finance DeFi stacks. PayPal o

Read the full report

This report is part of Delphi Pro.

- 800+ Pro reports across every major sector

- Talk directly with our analysts

- Private community of funds and builders

Already a Pro member? Log in

0 Comments