The Year Ahead for Crypto 2025 – Full Series:

AI+DePIN

DeFi

Gaming

Infrastructure

Markets

Blockchain/acc – Time to go Fast

The industry is shifting to high throughput chains. This is not just about Solana, whose meteoric rise over the past year has led the thesis, but also alt L1s like Sui & L2s like Base who have surged in 2024, along with the numerous performant chains like Monad, HyperLiquid, Unichain, MegaETH and more all in the pipeline.

unichain is not confirmation of the appchain thesis. it is confirmation of the performant, gp chain thesis.

— ceteris (@ceterispar1bus) October 11, 2024

Users have shown that the main thing they’ve desired to use blockchains for is a good UX on a single general purpose shared state machine. There’s really no better example of this than the recent AI meta. All of the activity is on Solana and Base. Not “AI focused” L1s like TAO, NEAR, or ICP. They are happening on two general purpose chains that have only aimed to create a shared state machine that can handle a lot of activity. Narratives will come to you if you can create this.

yep.

when you create a product ppl want to use, new narratives will just come to you without being forced.https://t.co/XdnWcD4jEA

— ceteris (@ceterispar1bus) November 24, 2024

Even Ethereum has recently started to raise its gas limit with a re-focus on L1 execution and is seeing new protocols designed to speed everything up.

// thread

Introducing TOOL: Trustless Orderflow Operations LayerMaking Ethereum 12x faster with 1-second execution confirmations. No protocol changes. No L2s.

Launching MVP in Q1 2025 with support from industry leaders. pic.twitter.com/oI9OPUzjEX

— 0xprincess (@0x9212ce55) November 25, 2024

While people will debate the merits of appchains, so far we have not seen demand in practice outside of a few perp chains (Hyperliquid, dYdX), and while there are some interesting new L1s like Initia, Delta, Pod, Hyle and more that we will discuss later in the report, the next year is all about performant chains.

For some reason people believe that there can be only one high throughput blockchain, when the reality is that there will be none low throughput blockchains.

— toly 🇺🇸 (@aeyakovenko) May 4, 2024

Lastly, you should note that the chains in this section are a mix of L1/L2 and monolithic/modular. These constructions have different tradeoffs but are all trying to make the same thing: a fast shared state machine. The next sections will go over such chains.

- Solana

- High Throughput EVM: Hyperliquid, Monad, MegaETH, Unichain, Rise, Sonic, Ithaca, Nil, Berachain

- High Throughput SVM: Eclipse, Atlas, Soon, Fogo

- High Throughput MVM: Sui & Aptos

Solana – Increase Bandwidth, Reduce Latency

Solana Continues to Win

While we have grouped the other chains into EVM/SVM/MVM buckets, Solana has been the trend setter in the performant chain thesis and stands alone with a big lead over the newer competitors (most of which haven’t launched). All of Solana’s metrics experienced rapid growth in 2024, and the introduction of so many new performant chains in the pipeline, is proof that Solana has been correct.

When we wrote about Solana in the 2024 Year Ahead report it was only one month into what turned into a banner year. DEX volumes had just cracked $5B weekly, spiked to ~50% of Ethereum L1 and priority fees were just starting to see usage. Today? Not only are Solana DEX volumes now more than Ethereum L1, in November they were comparable to Ethereum and all L2s combined, and it surpassed Ethereum’s ATH DEX Volume of $118B from May 2021 (although below BSC’s $138B).

This is even more impressive when you realize every L2 runs a single centralized sequencer that doesn’t need to participate in consensus (a process that inherently degrades performance).

a perfect demonstration of solana’s engineering

in the past day, for fees:

Solana avg: 4 cents

Base avg: 10 centsSolana median: 0.2 cents

Base median: 2 centsthe catch? Base did 6.5M txns, while Solana did 92M txns

so — Solana has a 2.5x lower avg cost and a 10x lower… pic.twitter.com/RV7fUizbCM

— mert | helius.dev (@0xMert_) December 1, 2024

When compared to Ethereum volumes over the past two years, it is now on par or surpasses them monthly, and its dominance as a percentage of total DEX volume continues to climb, now accounting for nearly 1/3 of all spot trading volume on blockchains.

This has, of course, led to an explosion in protocol revenue. For years the main critique against Solana was that fees were too cheap to sustain the blockchain. This was faulty logic as it ignored the convexity that fees exhibit when you create valuable state. Solana’s REV (total income from various fee sources) hit an ATH recently of >$25M in a week and is continuing to march up and to the right.

This momentum has propelled Solana to both tracking and surpassing Ethereum consistently, although recently Ethereum came back ahead (h/t to Blockworks for the data). Make sure to play around with the date ranges on these charts to get a picture of the all-time and recent change.

Also notable is that this hasn’t affected all fee paying users as it would with a global fee market. The median fee on Solana still stayed sub-cent during this period (votes, transfers, etc).

Lastly, validator income from MEV and fees surpassed income from issuance for the first time ever in November. When we published “Solana the Monolith” in May 2023 this was nearly entirely issuance. There are calls for Solana to lower issuance further in light of this— keep an eye on this SIMD. With that being said, I don’t think issuance rate matters too much (it’s just a tax on non-stakers) and would refer people to this piece by Jon Charb if you disagree.

The critique against Solana now is that this activity isn’t sustainable because it’s all memecoin trading. Listen, I get it, but this is once again adding qualifiers to any Solana metric that proves another old thesis wrong. The reality is this: Solana is the place to trade. Yes, it is dominated by memecoins now, but there is no reason why it will stay that way in the long-run, and if this is your main critique then I believe you are missing the forest for the trees. Memecoins aren’t any “less real” than other assets. The market trades what it wants to trade, and the fees paid to trade them are very real. I too hope we move past memecoins being the dominant assets traded but as of today that is just the reality, and they’ve become a good stress test for Solana.

People will also compare Solana to chains like BSC, Fantom and Polygon that gained users when Ethereum gas prices spiked last bull, and then lost them during the bear. Again, this is a flawed comparison; Solana went through an explosion in activity all while Ethereum gas prices were 1-2 gwei. They were not pushed to Solana because of high fees elsewhere. Yes, low fees are an important part of Solana, but there’s way more to it than low fees. And while you can hate memecoins, it’s not like there was another meta out there that was gaining attention. If something new comes along and Solana doesn’t capture the volume, then we can say Solana has lost ground.

If you need an example for why Solana is the place to trade, look at the recent AI meta. Agent AIXBT, an agent deployed on Base, had a significant amount of its volume traded on Solana. Solana users prefer it so much that they would rather trade a wrapped asset issued by a third party bridge (Wormhole) with much weaker security properties than use the chain where it was originally issued.

rollup roadmap:

theory – issue assets on eth l1, bridge to l2. can escape hatch back to L1 if needed

practice – issue asset on l2, trade it on another l1 through a third party PoA bridge

— ceteris (@ceterispar1bus) November 27, 2024

We saw a more extreme example of this happen when Runes on Bitcoin were going through their hype. The top traded Rune had the majority of its volume on Solana, not Bitcoin or any other chain. Bitcoin is a terrible trading chain so it makes sense price discovery would happen elsewhere, but it’s notable that it’s Solana. Solana is simply the preferred destination to trade today. Even large Ethereum NFT projects like Pudgy Penguins have chosen to launch their token on it. Solana is simply an L2 to every other chain that issues assets.

everyone looking for bitcoin l2’s don’t realize we already have one and it’s called solana pic.twitter.com/DrVxNXPhdy

— ceteris (@ceterispar1bus) April 14, 2024

The main area where Solana still lacks is stablecoin TVL and by extension, volume. This is a metric you would want to see continue to rise along with other non-meme (DePIN, RWA, DeFi, etc) volumes in the years ahead as FOREX is the largest market opportunity in the world. Also, while users prefer Solana to trade, a lot of capital still prefers to use stables and keep assets on Ethereum as it is home to most of the best DeFi applications today. While Jupiter is the best spot trading app in crypto, the rest of Solana DeFi is still well behind their Ethereum competitors. There is still a lot of room for Solana DeFi to improve, however TVL has risen steadily from a year ago and now sits #2 at ~$10B after being outside the top 10 just 1.5 years ago.

DeFi TVL also exhibits a sort of lindy effect. The longer people have assets in DeFi protocols the longer they will trust them, less likely they are to close out CDPs (and incur taxable events), and less likely to bear the operational overhead of moving assets. People continue to point to Ethereum vs Solana’s TVL as a knock against Solana. And it’s true, Ethereum’s is much larger, but this gap continues to move in one direction. If you used this argument a year ago when Ethereum had 40x Solana’s TVL, you would have missed this moving down to 7.7x. I see no reason why this multiple doesn’t continue to decrease over the next year.

The most important question now is, how does Solana maintain this lead? If crypto is truly entering its high throughput chain era, then how will Solana fare with so many competitors coming after the king? The answer is simple, but not easy: increase bandwidth, reduce latency.

How Solana Will Keep Winning

One commonly used argument against Solana’s moat is that “there will always be a faster chain that comes along”. This is a bad argument to me, for a few reasons.

- SVM was a material improvement over EVM. Other VM’s may provide some improvements over EVM but less against SVM (specifically a parallelized VM with no token approvals).

- SVM is fastest growing alt-VM eco. Like Ethereum and EVM network effects, Solana is starting to exhibit the same. There are numerous new SVM chains we will discuss. This all creates a larger developer base.

- You can’t cheat physics. While centralized L2s with a single sequencer will be able to move faster than Solana, it is not clear if another globally distributed L1 can. With Firedancer, Anza improvements, and a ruthless dedication to IBRL, it’s hard to see Solana be outcompeted. Toly and the team have always stayed laser focused on their mission to be a globally decentralized NASDAQ; the thesis hasn’t changed.

- The ZK argument: ZK can’t speed up native consensus. Solana’s goal is to be the most performant single state machine, something ZK cannot help with.

The black pill is that if the only interop we need is sending USDC between giant state machines then ZK proving doesn’t do anything.

— Zaki ⚛️🍷 (@zmanian) November 24, 2024

With all that being said, success is by no means guaranteed. Solana is far from perfect, still has a lot of issues, and there are a lot of worthy competitors approaching.

MILLIONS of dollars in MEV are siphoned away DAILY by vpe (aka arsc), the top sandwich bot. But the worst part? This isn’t just about MEV—it’s about centralization of MEV. And it’s the greatest threat to Solana’s decentralization I’ve seen.

Solana’s volume is skyrocketing, and… pic.twitter.com/v6mlSQhtg1

— Ben ⌛ (@HypoNyms) December 10, 2024

Some key teams/initiatives for Solana are below.

Temporal

A research firm founded by ex-HFT, TradFi and MarginFi contributors (like Ben from above), Temporal looks to fix Solana’s fee markets. Their main priority is to replace swQoS with a fee based model (tl;dr is swQoS gives priority to amount of stake whereas fee market is simply fee paid). Their goal is to create a new transport layer for Solana replacing QUIC and UDP.

They recently announced Nozomi, a new fee based way to land tx’s on Solana (only pay tip if your tx is landed first). This product exploits Durable nonces to create a better priority fee mechanism. The team has a lot of experience and understands the infrastructure and nuances deeply – they are one of the main infra focused teams to watch.

Anza

While Firedancer gets the hype, the team behind Anza should not be written off or taken lightly. It’s not like the Anza team is just going through the motions and maintaining Solana’s validator client until Firedancer comes.

If we are not faster than firedancer in a year I will quit my job

— Alessandro Decina (@alessandrod) July 22, 2024

Anza recently released the Agave 2.0 client, with it some notable improvements/changes:

- Full priority fee now given to validators instead of burned

- Central scheduler now on by default. The new scheduler went live a few months back and looks to improve network jitter (full breakdown)

- A new ZK ElGamal Proof program and new syscalls

- A break from old labs client and moves Solana towards multi-client world

And it’s not like Anza isn’t focused on IBRL.

definitely nothing pic.twitter.com/SpXDllgYak

— BW (@bw_solana) December 2, 2024

And they just got talent from Ethereum.

Last week was my last week at Consensys. Today is my first day at @anza_xyz.

I’m taking my talents to Solana.

In my first 100 days, I plan on writing a spec for as much of the Solana protocol as I can get to, prioritizing fee markets and consensus implementations where I…

— Max Resnick (@MaxResnick1) December 9, 2024

Firedancer

Frankendancer went live on mainnet in September. As of now they do not have Jito support so uptake has been slow. Once that is implemented expect the number of validators running it to increase significantly. The full client is running on testnet. You can watch a live feed of Superteam Germany’s validator here: https://fd-mainnet.stakingfacilities.com/

Jito

The MEV backbone of Solana, Jito has become Solana’s most profitable protocol. All of the fee/MEV charts from above are attributable to Jito’s infrastructure. They recently released Jito Restaking which you can read more about in our Restaking report. As mentioned above, they are not yet integrated with Franken/Firedancer.

Wallet Infra

Solana’s wallet infra continues to improve with teams like Squads leading the charge. They recently introduced virtual US banks accounts, allowing users to send directly between onchain and offchain without a CEX.

Introducing virtual US bank accounts on Fuse.

Powered by @Stablecoin, your virtual bank account converts USD payments directly to USDC in your Fuse wallet.

• Accept regular bank transfers

• Skip multiple platforms & transfers

• No expensive on-ramp fees pic.twitter.com/9Qvcban8Ke— Fuse (@fusewallet) December 4, 2024

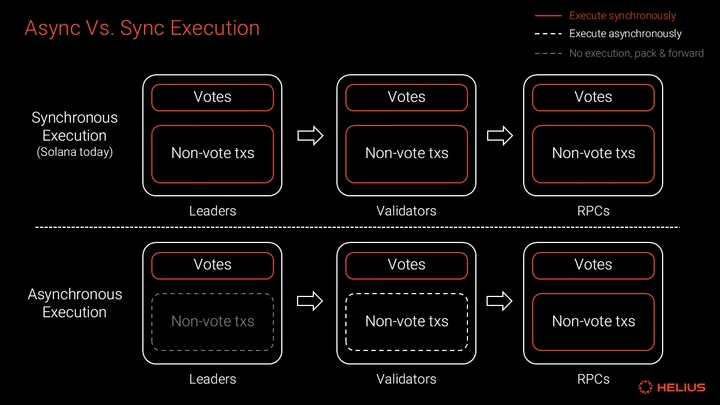

Asynchronous Execution

An ambitious challenge, async execution allows validators to create blocks without executing them. There are numerous advantages to AE like shorter block times, lower validator requirements, faster finality, a pathway to MCP (multiple concurrent proposers) and more. A good breakdown can be found here by Helius.

Mithril

Created by the Overclock Validator team, Mithril is a Solana full node client that aims to make home verifiability plausible – one of Solana’s largest critiques. They recently reached a new milestone.

New Ideas Replicated Elsewhere

One clear signal of an innovative ecosystem is when its products not only succeed but are also replicated elsewhere. The main ones that come to mind here are Pump.Fun, MetaDAO and AI Agents

- Pump.Fun gets a lot of hate for being memecoin focused but pump just gave users something they wanted with standardized regulation (stopping rug pulls). Competitors like clanker.fun and wow.xyz have launched on Base

- MetaDAO was first to launch Futarchy in prod and is now being replicated on Ethereum

- AI Agents & platforms took off on Solana & Base, not “AI focused” chains

DePIN & DeAI

More on this in the DePIN & DeAI Year Ahead report, but Solana is home to numerous DePIN networks like Helium, Hivemapper, Pipe, Dawn, and Teleport, and it’s also leading the AI agent narrative, with other infrastructure projects such as grass

Numerous SVM Stack Chains

Eclipse, Soon, Atlas, Sonic and more are all building on the SVM stack, potentially increasing SVM network effects.

ZK & Modularity

For the full breakdown just skip to the ZK deep dive part of this report and read “Solana the Modular” from August. The main project I wanted to highlight here is Bullet.

Check out @Tristan0x ‘s article for an inside look at how Bullet works and how it stacks up against other high-throughput L2s launching this year https://t.co/N3jNV1N394

— bullet (@bulletxyz_) November 25, 2024

The tl;dr is that Bullet is a perps appchain on Solana built using the Sovereign Labs SDK. They have a bridge to Solana and use it for DA, posting both ZK and fraud proofs to Solana. They have achieved sub 50ms latency with a target of 5ms – something you can only do with a centralized sequencer. As noted in the intro, perps dex’s are the main proven use case for appchains and so it makes sense Zeta is going with this architecture. They will be the first to try this on Solana and will be able to seamlessly tap into Solana’s native liquidity. After the success of Hyperliquid, it will be one to watch to see how they compete as Hyperliquid moves towards a general purpose L1; Bullet is VM-less, it’s just Rust.

Growing Developer Interest

Per a16z’s “State of Crypto 2024” report, Solana saw the largest jump in developer interest from 2023 to 2024 and sits at #2 in a sea of EVM chains. As we’ve said before, while Ethereum is in the lead, all of Solana’s metrics continue to go up and to the right. It’s also important to remember Ethereum launched 6 years (2014 vs 2020) before Solana.

DoubleZero

Announced on December 4th, DoubleZero is essentially trying to create a new internet for high performance blockchains (L1s and L2s). While not part of Solana itself, DZ is dubbed as “the new internet for modern distributed systems” and is built by ex-Solana Foundation employees with contributors from Firedancer and Malbec Labs. Basically, the current internet wasn’t fast enough for blockchains and so they’re trying to build a new internet. IBRL.

ETFs

While not related to network infrastructure, ETFs are a sign of institutional adoption and are a significant source of flows. There are 4 ETFs now on the table for Solana with the final decision date in August 2025. It is very possible with the new administration we will see a Solana ETF.

Job’s Not Finished

While Solana has had great momentum over the last year, and there are reasons to expect them to continue delivering, the competition is growing fast and Solana’s continued success is by no means guaranteed. The next three sections are dedicated to these competitors. As mentioned above these are a mix of L1s and L2s, and while single sequencer chains don’t compete towards being the dominant global shared state machine, they do compete for users and liquidity of various applications.

High Throughput EVM Chains

Hyperliquid, Monad, MegaETH, Unichain, Ithaca, Rise, Sonic, Nil, Berachain

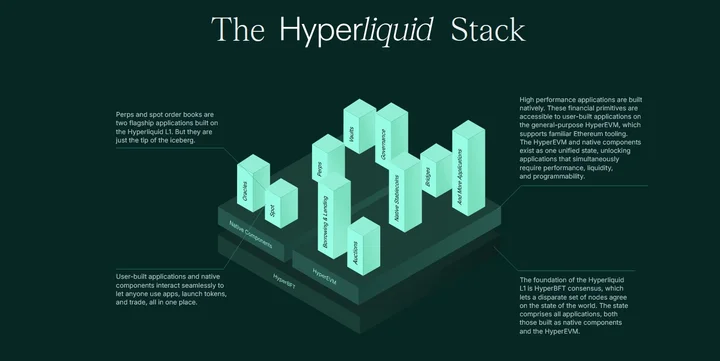

Hyperliquid (L1)

Out of the chains listed here Hyperliquid is the only one live, so it makes sense to talk about them first. Hyperliquid in its current state is not a general purpose chain, it is a perps appchain that has seen remarkable success in a competitive sector and now accounts for >50% of all perp volume. The perp landscape has seen numerous protocols take top spot like Synthetix, Perp Protocol, GMX and dYdX over the years with none have been able to maintain the lead. The competition is fierce, but that’s because the opportunity (Decentralized Binance) is so big.

Why are they in this section then if they’re an appchain? Because they are moving to create a general purpose high throughout EVM L1. However, we should categorize it correctly today. It is not a decentralized perps exchange, it is a centralized, permissioned chain run by the team’s 4 co-located validators in Tokyo. They are aiming to transition to a decentralized, open source L1, but that is not what they are today.

BTW I have no issue with such products/services existing, I am even open to the idea that ‘CeDeFi’ or ‘onchain CeFi’ could be better/more sustainable than DeFi (and market seems to be telling us that), but things should be properly labeled. . .

— _gabrielShapir0 (@lex_node) December 1, 2024

With that being said, they have done something rare in launching a new protocol without any funding and enriching a community of diehard supporters. They are kind of building backwards but now have a massive valuation to fund their vision. Hyperliquid is a good example of an appchain being successful and wanting more; wanting to become their own gp chain.

many such cases https://t.co/tpS4LBJGR9 pic.twitter.com/NZm9wtV40M

— Jon Charbonneau 🇺🇸 (@jon_charb) January 27, 2024

The challenge for Hyperliquid now will be how they transition to a decentralized L1 with a globally distributed validator set, all while maintaining the same UX that got them so many diehard users. If you talk to any power user of Hyperliquid they will tell you that it is the best trading experience in the market. Maintaining this experience will be harder as they decentralize and by extension network latency increases. They now have a testnet with more validators outside of the team run ones.

Hyperliquid created their own consensus mechanism HyperBFT after pivoting from Tendermint in earlier days. Internal testing with co-located validators shows an end-to-end latency median of 0.2 seconds and 99th percentile at 0.9 seconds. How this performs with a larger, globally distributed validator set is TBD.

Hyperliquid created their own consensus mechanism HyperBFT after pivoting from Tendermint in earlier days. Internal testing with co-located validators shows an end-to-end latency median of 0.2 seconds and 99th percentile at 0.9 seconds. How this performs with a larger, globally distributed validator set is TBD.

Their EVM solution is unique and will be different than others on this list. Hyperliquid’s perps and spot order books are all built in Rust and will continue to be isolated to their own environment. The EVM is being added as a generalized VM on top. The native VM is permissioned and tailored to their app, the EVM is permissionless and open to all. The challenge in having two distinct VMs is fragmenting liquidity between the two and getting them to work together seamlessly; the benefit is that EVM congestion shouldn’t impact perps performance.

There’s no question Hyperliquid has been a resounding success to date, and their go to market with a 30% community airdrop gives them a strong & dedicated user/holder base moving forward. L1s are never community owned, especially in the post-ICO era. There are significant technical hurdles to pass, but they now have a massive valuation and there are a lot of catalysts/narratives like leading perp dex, leading high throughput EVM chain, and best L1 distribution to help them get there.

There is the other question as to if Hyperliquid should even try to decentralize meaningfully. Their product is good because it’s centralized, and users don’t seem to care, not only with Hyperliquid but also L2s governed by multisigs. It’s not clear if the drawback of decentralization is actually worth the degradation in performance, especially as we transition to Trump’s America.

A lot of people will point to Hyperliquid’s airdrop as a successful way to launch a new protocol, but the reality is that they built something users just really wanted to use. You can’t airdrop your way to success. Make s

Read the full report

This report is part of Delphi Pro.

- 800+ Pro reports across every major sector

- Talk directly with our analysts

- Private community of funds and builders

Already a Pro member? Log in

0 Comments