The Year Ahead for Markets 2026

DEC 11, 2025 • 71 Min Read

Report Summary

Macro Regime Shift Favors Risk Assets – Global pivot from tightening to rate cuts, fiscal deficits driving liquidity, and weak USD backdrop. Global M2 and gold at new highs historically precede BTC performance, with U.S. liquidity rebounding as QT ends and Treasury drawdowns inject capital.

Crypto Market Maturation Creates Dispersion – Markets now mirror traditional finance with high dispersion replacing broad rallies. BTC decoupled as a macro asset, while altcoins face token unlocks, weak demand, and competition—making 2026 a “stock-picker’s market.”

Structural Bids Determine Winners – Assets with ETF flows, real revenue, buybacks, or ecosystem traction (BTC, ETH, SOL, Hyperliquid) outperform. Passive speculation no longer works; fundamental demand and narrative alignment separate winners from laggards.

Competition from Exponential Tech Sectors – Speculative capital now splits between AI, robotics, energy, battery tech, and bioengineering—reducing crypto’s share of risk-on dollars and forcing crypto assets to compete on fundamentals.

On-Chain Credit Evolution – Shift from overcollateralized to undercollateralized credit using zkTLS and AI verification (3Jane). Aave dominates trustless lending, while Maple and Centrifuge scale private credit with real-world institutional traction.

RWAs Expand Beyond T-Bills – 2026 brings RWAs backed by energy infrastructure (Daylight, virtual power plants), AI compute (USDAI), and specialized corporate credit. Obex (Sky/Maker) incubates next-gen yield-bearing assets.

Corporate Chain Wars and Agent Economies – Stripe Tempo (payments) and Robinhood L2 (tokenized equities) lead verticalization over general-purpose L1s. x402 and ERC-8004 enable AI agent transactions, identity, and reputation—launching machine-to-machine crypto economies.

Institutionalization Deepens Market Structure – More crypto IPOs (Kraken, Securitize), tokens evolving into equity-like instruments for distribution (WLD), and regulated market structures cement crypto’s integration into traditional finance.

Introduction – Why So Bearish

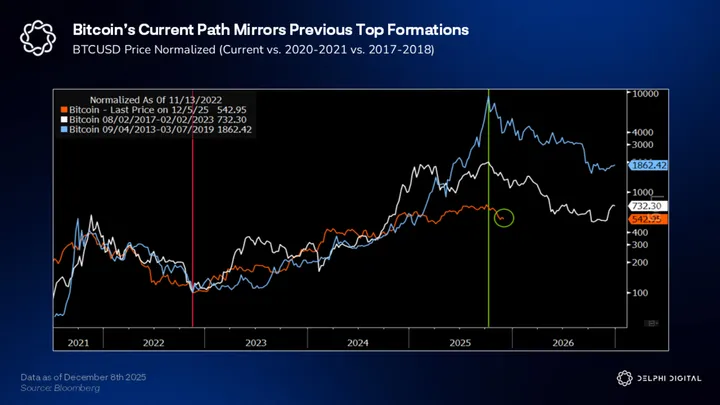

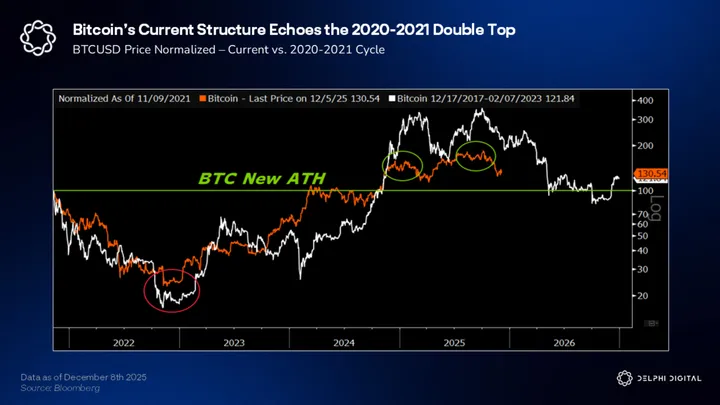

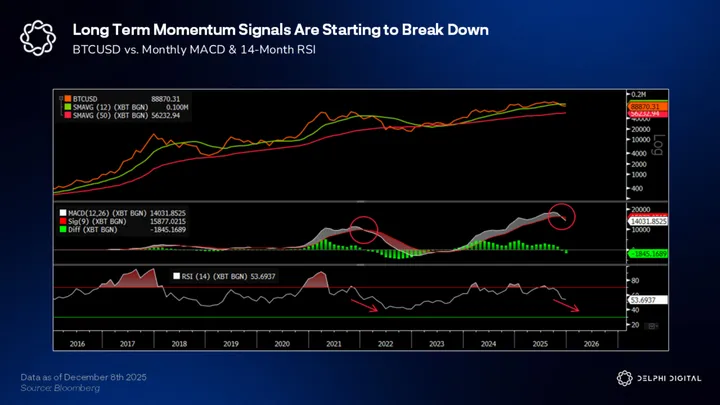

Many crypto investors have turned bearish over the last few months, claiming the top for the 4-year cycle is already behind us — and if you glance at the charts, it’s easy to see why.

BTC has closely tracked prior cycles, like 2020-2021…

Including its double peak top…

We showed this chart in our 2023 Markets Year Ahead report…

Which, if history continued to repeat, would look like this now…

With long-term momentum indicators breaking down…

It’s not that hard to see why sentiment is in the gutter, and why we’ve seen popular Crypto Fear & Greed indices continue to hit new lows in recent weeks.

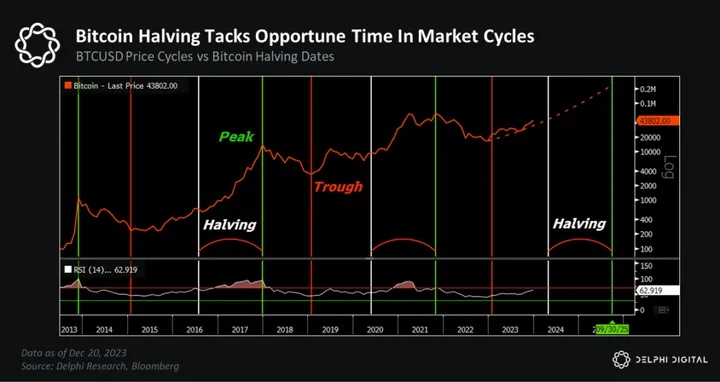

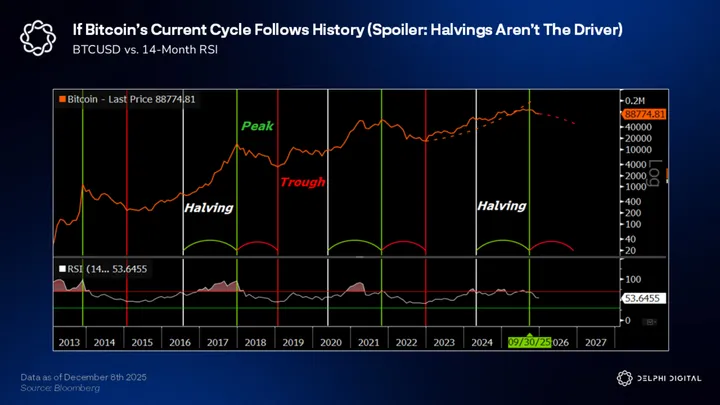

We know the historical 4-year cycle was driven by bigger macro factors like liquidity conditions though; it wasn’t just random timing.

And if those same inputs had followed similar trends to prior cycles — if global liquidity growth had topped out, the business cycle had already peaked, monetary policy was shifting from accommodative to restrictive, fiscal — we’d be the first to say it’s time to pack it up.

But that’s not what we’re seeing…

Macro Bifurcation —> Macro Convergence

The macro backdrop is transitioning from a period of bifurcation towards one of convergence as we head into 2026.

Bifurcated liquidity conditions, elevated rates, and divergent directions between monetary and fiscal authorities all appear set to turn.

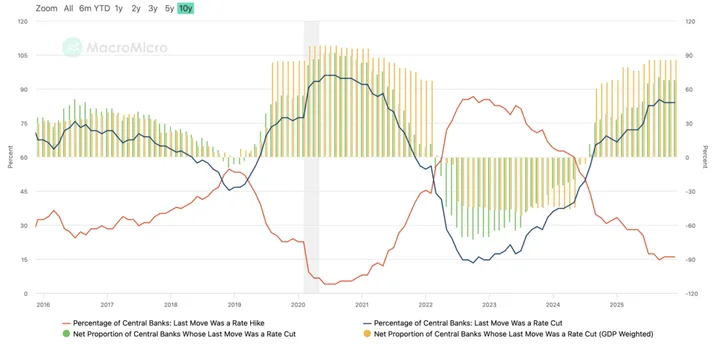

For starters, global central banks are cutting rates…not hiking them.

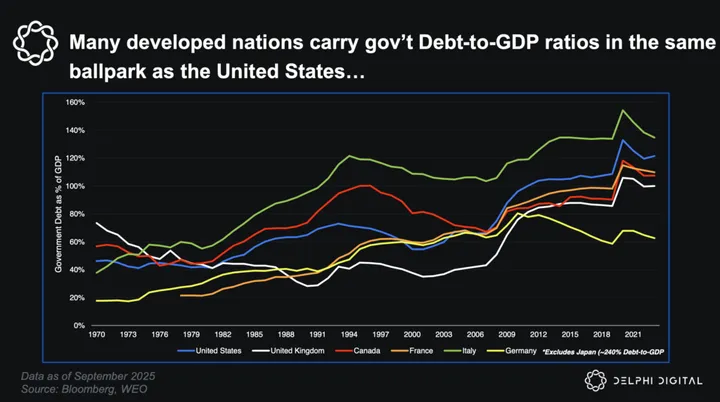

Most developed nations are running sizable fiscal deficits — this isn’t just a US-centric problem — with many staring down a similarly precarious fiscal position (see our monthly Markets Chartbooks).

Even as long-duration government bond yields surge to multi-decade highs…

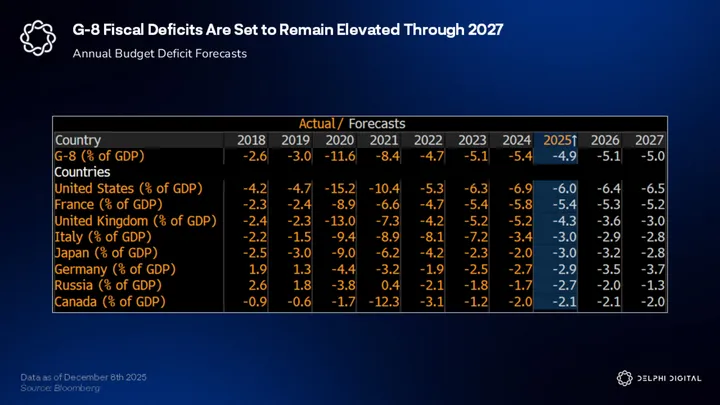

Fiscal deficits across G8 countries are expected to keep pace or rise through 2027 (at least).

More deficit spending means more debt growth, which means greater liquidity needs.

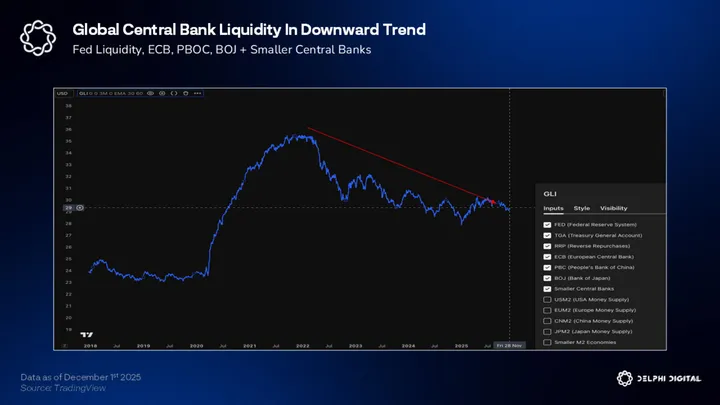

Absent the brief boost in 1H 2025 though (driven largely by a weaker USD), the Global Liquidity Index (GLI) shows the broader trend in central bank liquidity has been drifting lower.

The Fed isn’t the only part of that story, but it’s a big one. The global financial system is still dominated by the marginal dollar, giving US liquidity an outsize influence, and a powerful tide when its winds shift.

Liquidity Avengers Assemble

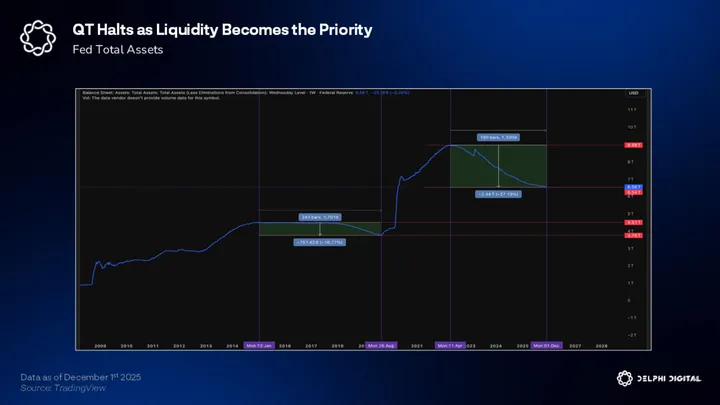

On paper, the Fed’s balance sheet has dropped ~$2.4 trillion since mid-2022, a far steeper decline than the 2017-2019 cycle (which culminated in the Sep. 2019 repo crisis that proved Fed tightening had gone too far).

Despite the headlines, the Fed hasn’t been draining all this liquidity out of the financial system, but it has become a major headwind (we’ll dive deeper into how and why this matters later on in this report).

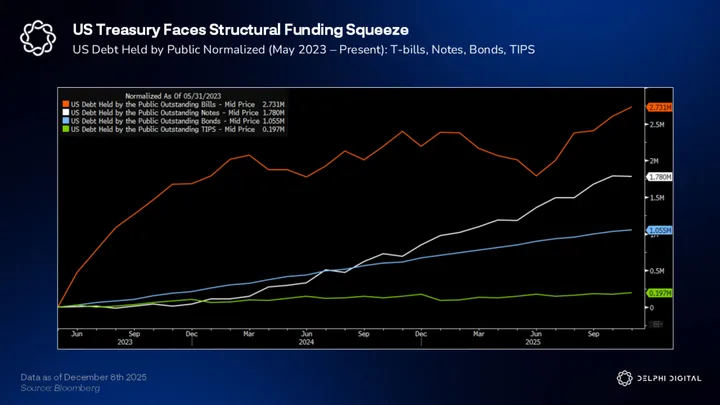

The Treasury General Account (TGA) chart shows the effects of 2025’s political and fiscal turbulence in real time. The Treasury had guided towards a TGA refill target near $850B, but the balance has surged to nearly $1 trillion (driven by a mix of precautionary issuance, the government shutdown, and administrative timing).

The TGA acts like a liquidity vacuum since every dollar sitting in the government’s checking account is a dollar not being spent or circulating in the financial system (we covered the 2025 TGA refill and its effects in more detail here).

Looking to 2026, the TGA should normalize lower, pushing liquidity back into the system. The fiscal-liquidity drain will give way to fiscal-liquidity injections.

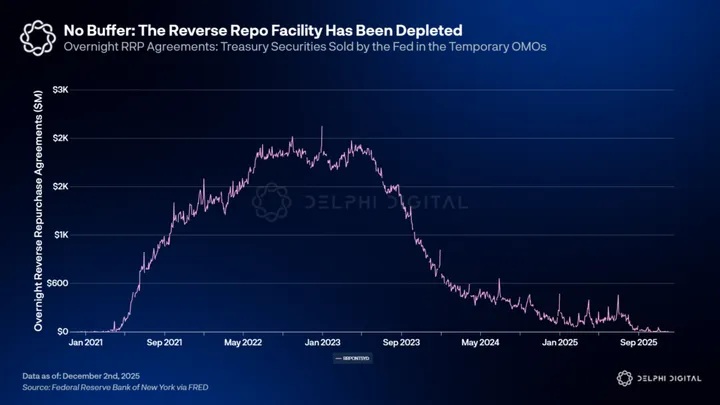

Reverse repo balances (ON RRP) have also collapsed from over $2 trillion at its peak to practically nil. Remember, during the 2023 TGA refill, the RRP cushioned the liquidity hit instead of draining bank reserves, but now that liquidity shock absorber is exhausted.

Ending QT now signals the Fed’s priority has shifted to liquidity stability over incremental inflation insurance. Inflation trending closer to target, a labor market that’s cooling without cracking (yet), and mild credit stress (so far) are enough to give them the green light as policymakers try to thread the needle.

Even though its not the same bazooka we saw in 2020-2021, it’s a notable shift compared to the current trend.

The Fed is a big part of that story. The global financial system is still dominated by the marginal dollar, giving US liquidity an outsize influence, and a powerful tide when its winds shift.

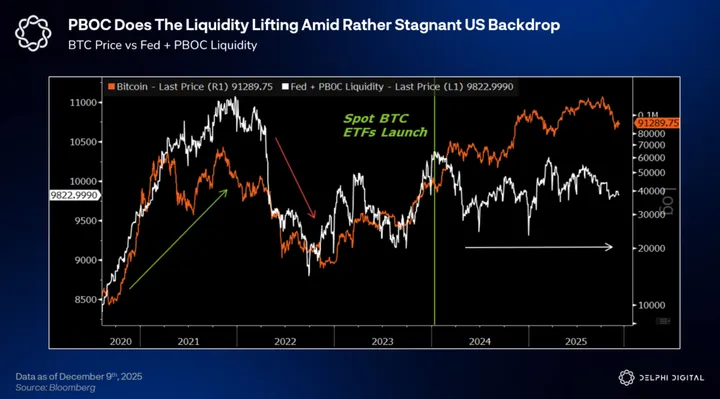

Meanwhile, China has been emerging from its own quasi-financial crisis of sorts — fighting a major real estate crisis, debt deflation, collapsing consumer and investor confidence — as the PBOC has been broadening its own liquidity support.

This has helped spark some recovery in domestic markets, like Chinese equities — and we know PBOC liquidity has been a key driver of BTC cycles too.

China has been doing much of the heavy lifting recently — as we predicted it would — despite a rather stagnant US liquidity backdrop.

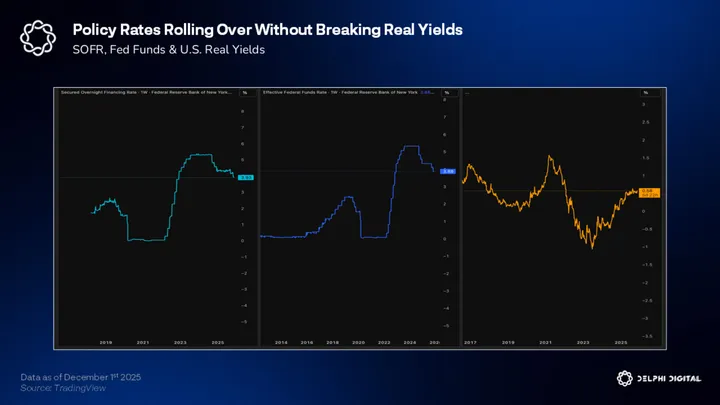

The Fed’s recent liquidity malaise will be turn more robust as “QT” officially comes to an end, the TGA starts to drawdown from its latest local top, and rate cuts follow the path of least resistance.

The Fed’s policy trajectory is clearly shifting from “restrictive and rising” to “less restrictive and declining.”

With cuts already underway, and another 25 basis point cut likely in December, the forward curve is pricing at least 3 more cuts through 2026, putting the Fed funds rate in the low 3s by EOY 2026.

The Fed is easing, but doing so without triggering a collapse in real rates, which signals a controlled transition rather than a panic pivot.

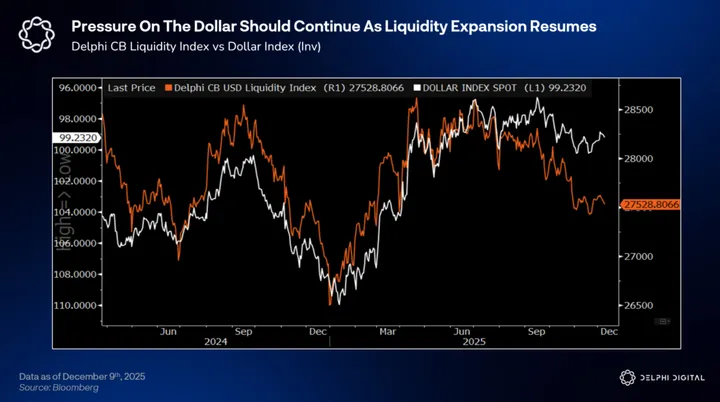

Lower rates, massive deficit spending, and more liquidity unlocks should keep pressure on the dollar too, allowing global liquidity to inflect higher.

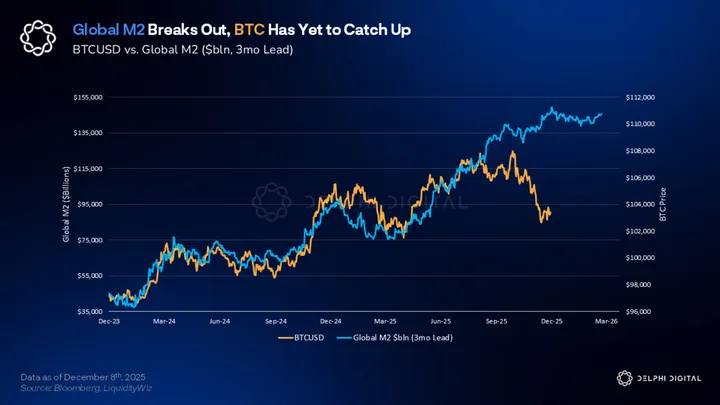

Global M2 is already breaking to new highs.

Gold has broken out already too, reinforcing the currency debasement trend is intact.

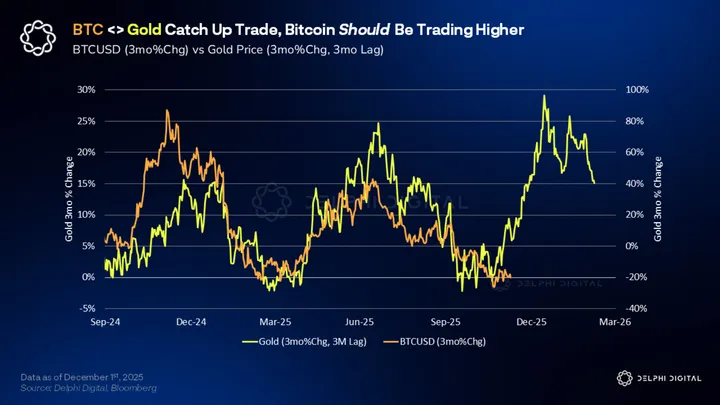

And if gold and global M2 typically lead BTC by ~3-4 months…

Then BTC should be trading higher.

Gold’s Structural Demand, Debasement Trend Shines

At the start of the year, we called gold “one of the best charts to watch” because it was “sending a signal of what’s likely to come.”

It was trading at $2,700/oz before its price surged >60% over the next 9 months.

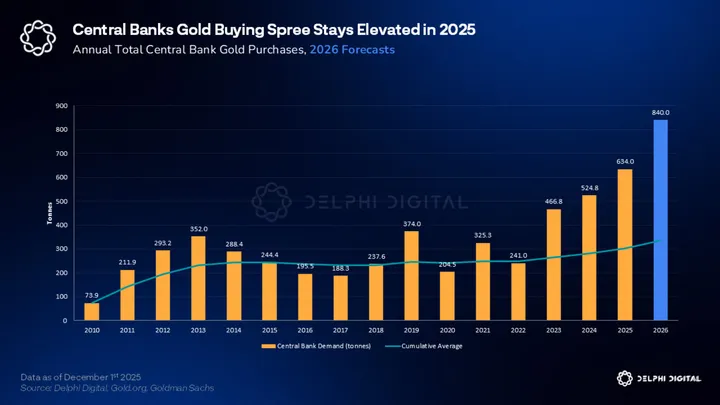

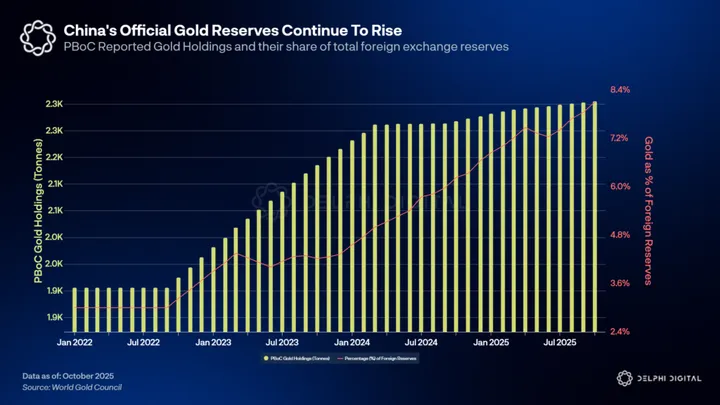

Heading into 2026, gold still has one of the strongest structural demand tailwinds behind it. The message from central banks is clear — they want assets that sit outside political systems, outside sanction regimes, and outside the vulnerabilities of dollar liquidity cycles.

Central banks purchased more than 600 tonnes of gold in 2025, a trend we expect to continue into 2026. Goldman Sachs forecasts central bank gold buying will average 70 tonnes per month throughout 2026 or roughly 840 tones by H2.

This follows the record prints of 2023 and 2024, when buying exceeded the highs seen after the GFC. When gold’s price jumps to new highs, we typically see central banks stop buying or sell some of their holdings.

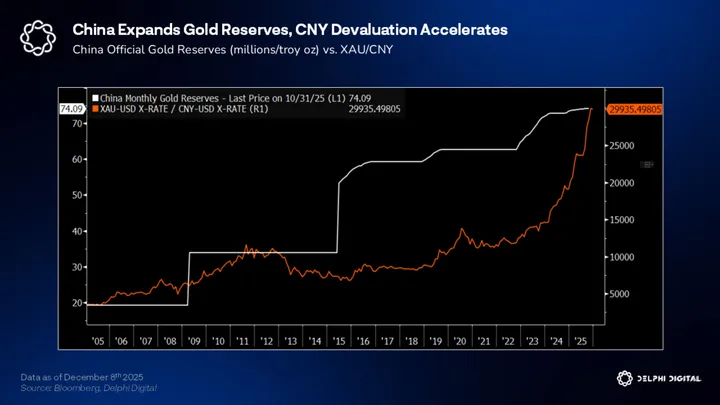

But we’ve seen continued aggressive buying despite this huge price run up, and gold is a big China story right now.

The PBOC has been one of the largest and most consistent buyers in the world, and this is just what we see in official data — its total gold holdings are much likely higher when off balance sheet or shadow reserves are accounted for.

There’s a bigger trend at play here too. If China really wanted to accelerate de-dollarization, buying gold then devaluing the yuan against it would be a sensible move. Accumulate a bunch of gold reserves, force its price to run up much higher, and then push to settle more trade in yuan (which is now backed by much more valuable gold reserves). If they buy enough gold, and price runs high enough, it could even be used to recapitalize some of their debt.

This is another trend worth watching.

If that’s the strategy, and China remains one of the most important marginal buyers in the gold market, the underlying demand trend can remain intact even if Western investor flows remain uneven (not to mention other smaller countries who’ve been buying recently too).

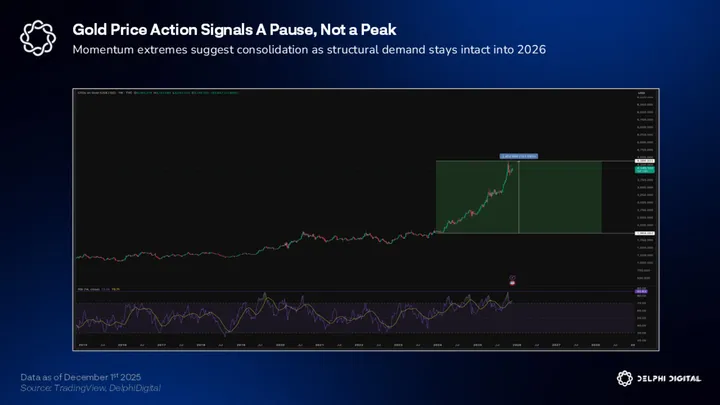

Gold’s Price Action Signals a Pause, Not a Peak

Gold logged one of its strongest moves on recent record, rising more than 120% since the start of 2024. Gold’s weekly chart RSI also hit an extreme reading >85, touching levels we’ve only seen a handful of times in modern history (monthly RSI is tracking early 1970s levels).

No chart goes up in a straight line forever, and all signs points to slowing momentum in the near term, often giving way to a period of sideways consolidation and a healthy reset before more potential upside continuation (assuming demand remains supportive).

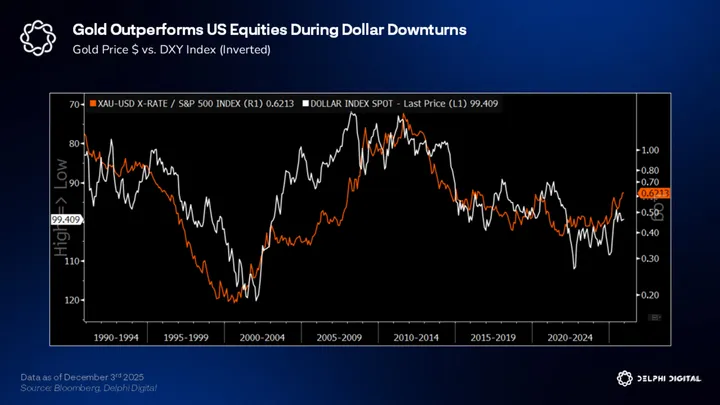

Gold tends to outperform equities during extended periods of DXY weakness too.

After consolidating the gains from an unusually strong year, the longer-term trend should reassert itself. The next leg higher depends less on speculation and more on the same steady forces such as official-sector accumulation, weaker dollar, and the “debasement trade” maintaining mindshare.

Gold prices have been speaking volumes this year and remain one of the clearest signals that the currency debasement trend is accelerating. We have been pounding the table on this for a long while (example reports here and here) and the market is finally catching up.

Markets may not get the firehose of liquidity like in 2020, but the setup is there for a cleaner, more predictable easing rhythm where major CB policies begin to converge as deficit spending fuels greater debt monetization.

This tends to favor duration, large caps / growth equities, gold, BTC and digital assets with real structural demand behind them. Productive growth assets tied to real economic activity and debasement-sensitive assets can both do well.

Revisions to restrictive banking regulations will relieve balance sheet pressures, opening more liquidity valves to support funding markets, more shock absorbers for new UST issuance, and more stabilizers for the Treasury financing cycle as public debts are monetized via the banking system.

The shift from persistent tightening to progressive liquidity augmentation is upon us.

Monetary inflation will continue, and fiscal dominance is behind the wheel.

And here’s why…

Glass Houses — UST Liquidity Fragility

Liquidity is like a phantom — when you need it most, it disappears.

The flash crash of October 10th showed how many crypto asset valuations are being propped up by a handful of MMs, and in times of extreme stress these valuations mean little if liquidity isn’t there to support them.

This isn’t just a crypto phenomenon though.

The world’s most important securities market — US Treasuries — also faces challenges with its financial plumbing, and it’s a lot more fragile than it appears on the surface.

Bessent’s Impossible Dilemma

The US is running a $1.5-2T fiscal deficit per year. That means the US Treasury needs the market to absorb multi-trillion dollars of net new UST issuance every year.

We’ve talked a lot over the last couple years about how the US Treasury has been front-loading a lot of new UST issuance with more T-bill’s. This is a trend that started with Yellen but has continued under Bessent, despite his prior criticisms of this strategy.

Why? Because there was little alternative. The US Treasury has become a servant to the bond market — and the UST market is being propped up by a concentrated cohort of opportunistic buyers.

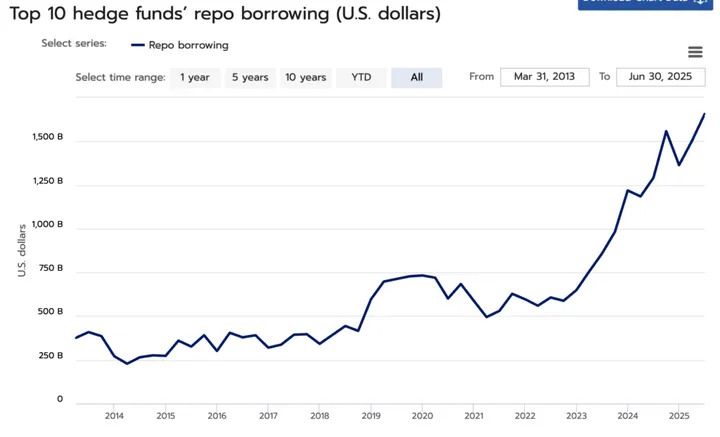

Hedge funds running multi-trillion dollar basis trades have become the incremental buyer of longer duration UST debt — and are now among the largest holders of US Treasury debt, overtaking major foreign official holders like Japan, China, or the UK.

“Cayman-domiciled hedge funds held ~$1.85 trillion of US Treasuries at the end of 2024…Our findings suggest that Cayman Islands hedge funds are, increasingly, the marginal foreign buyers of U.S. Treasury notes and bonds.”

HF’s finance these positions by borrowing heavy in repo markets. HF’s running huge leveraged UST basis trades are now among the largest cash borrowers in repo markets.

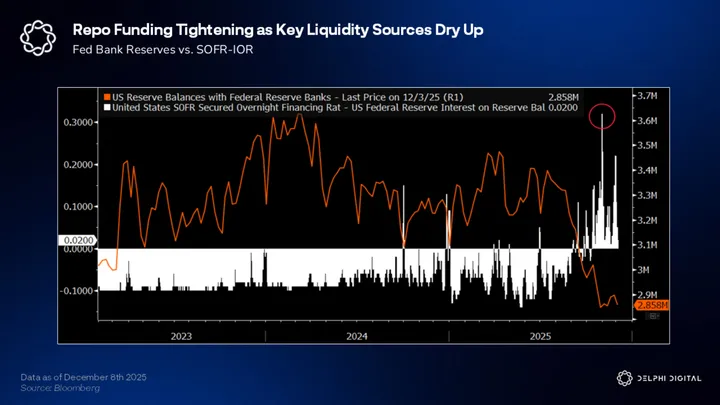

At the same time, the supply of cash lenders in repo is being strained as big sources of funding liquidity like MMFs have pulled >$2T out of the RRP over the last 2 years (to buy more T-bills), and the RRP drawdown has now reached its limit.

Banks are another liquidity source, but reserves have dropped >$500B since July.

Banks have their own balance sheet constraints too, something new bank regulations like changes to SLR requirements will address.

Unlocking bank balance sheets is the easiest and most straightforward path to unlocking more liquidity, and lower rates and less restrictive regulations will help enable this.

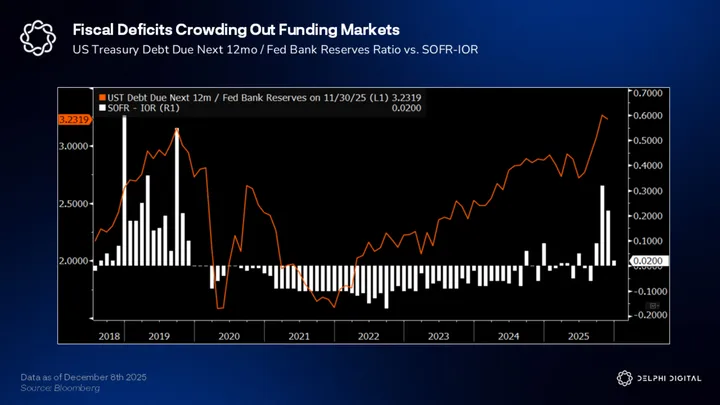

Meanwhile, massive US fiscal deficits are crowding out liquidity in funding markets.

Funding liquidity is tightening, the typical cash lenders in repo are constrained absorbing more T-bill issuance or via restrictive regulations, while strong demand from cash borrowers like HFs is critical to fulfill because those borrowers now represent one of the largest buyers of longer duration USTs.

If the supply of USD liquidity in repo dries up, and strong demand forces borrowing costs to rise, the basis trade could sour, causing HF’s to unwind these massive UST positions. Long-term rates would be sent into a frenzy, bond market volatility would jump, and spillover volatility shocks across risk markets would put further pressure on funds to de-gross and de-risk across asset classes.

This would would hurt Wall Street and Main Street alike.

Bessent can’t term out the debt either because it risks sending bond yields (and volatility) higher, triggering broader disruptions in risk markets as HFs de-gross positioning further, thus threatening the ~$2 trillion UST basis trade that underpins the long end of the UST market in the first place.

It’s all intertwined.

And it’s why the risk of other massive trade unwinds, like the yen carry trade, are drawing so much attention.

Stresses in Japanese funding markets are emerging as the BOJ tries to shift away from years of loose monetary conditions. Higher domestic yields make foreign UST’s less attractive for Japanese investors and institutions (life insurers, pension funds), which have been huge capital allocators to foreign asset markets over the last few decades (something higher US bond market volatility and FX hedging costs could make worse).

The typical buyers of USTs has shifted.

The US Treasury now relies on hedge funds running multi-trillion dollar basis trades, at a time when it’s vulnerable to reduced buying from major foreign holders, like Japanese institutions, making it even more vulnerable to volatility shocks that could trigger a big unwind of the status quo.

This is why Bessent & Co have to keep bond market volatility suppressed, why the Fed needs to end QT and shore up bank reserves, and why regulatory changes need to remove the shackles from bank balance sheets. The system needs more liquidity, and it can’t afford a volatile shakeup in the process.

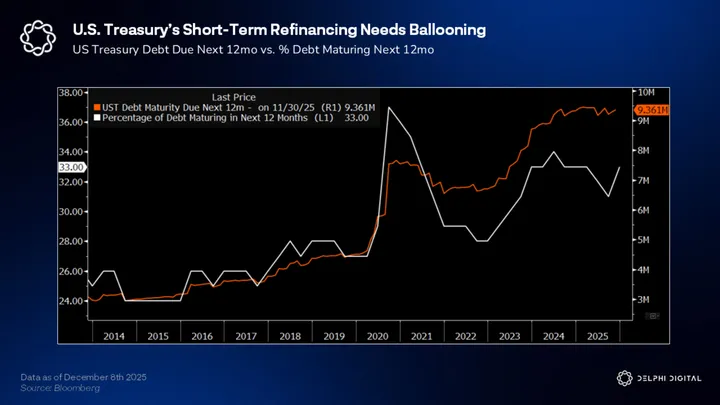

The move to front-load T-bill issuance bought more time, but it was never a permanent fix. The amount of short-term debt the US Treasury has to refinance has surged, with large swaths of both T-bill’s (~$150B) AND existing coupon debt (~$300B) maturing every month. And that number is getting bigger.

The US now has nearly $10 trillion of debt it has to refinance over the next 12 months.

This increase could make the TGA more volatile, as more balance sheet is needed to rollover more and more public debts; this would drag on bank reserves and tighten liquidity — if more liquidity valves aren’t opened.

The Fed’s Standing Repo Facility (SRF) is viewed as the ultimate safety stopper to plug these funding gaps right now, and officials are even encouraging banks to utilize it more to arbitrage the funding spread (i.e. borrow cash from Fed at lower rate, lend it out in private repo at higher rates). Many say this isn’t QE because the SRF is a temporary stop gap, but it essentially functions like an open liquidity valve — and one policymakers are actively telling banks to use more.

Whether the SRF becomes permanent, and/or bank regulations are revised to free up more balance sheet capacity, it all gets us to the same end goal we’ve been moving towards — the US Treasury will monetize its debts via the banking system.

Fiscal dominance is in the driver’s seat now.

Fiscal, Take The Wheel

One of the big focuses in 2026 will be on directly stimulating Main Street with more targeted fiscal spending, rate cuts (tackling affordability crisis, lower borrowing costs, mortgage rates, etc.), and a weaker dollar.

Domestic industrial production and capital investment is another one. China will continue stimulating, spending, and subsidizing to extend its lead in critical industries (robotics, advanced manufacturing, critical minerals / rare earths, alternative energy) and to play catch up in others (AI chips, compute). Neither superpower is going to back down in a battle for national security and global supremacy.

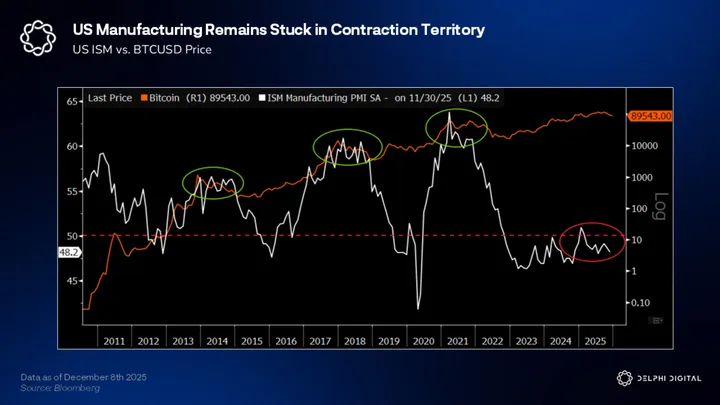

The “broken” business cycle is adding to more stagflation calls and worries the US is headed for economic purgatory. The US ISM is has been stunted below 50 for going on 3 years now.

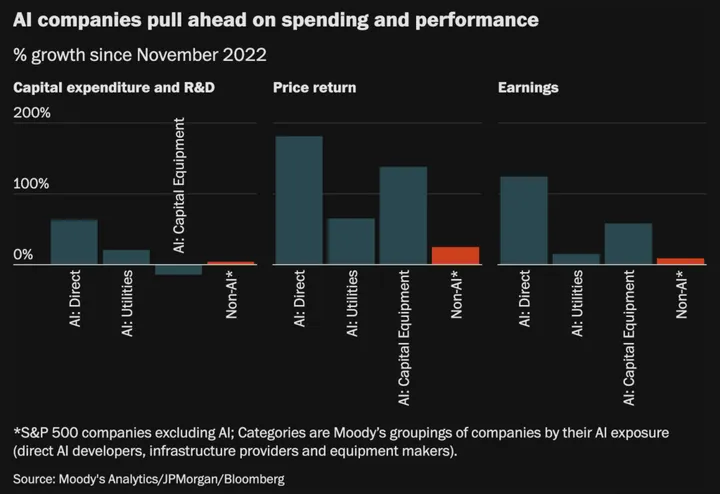

When you exclude Big Tech, capex has been relatively stagnant for the rest of the “real economy”.

Lower rates, largesse fiscal spending, and policy like the One Big Beautiful Bill are a powerful combo to catalyze industrial growth, with critical industries like AI, robotics, energy, and large scale power infrastructure leading the push.

America needs to get back to building, and the transition to looser monetary coupled with expansionary fiscal spending point to a growth revival next year, not an impending recession in our view.

This is an environment where stocks and BTC can both do well.

No Longer The Only Game In Town

The last two years has felt distinctly different from what crypto natives have been conditioned to expect from previous crypto cycles. In other words, things that worked well in the past haven’t worked nearly as well this time around.

In prior cycles, we saw sustained periods of time where the totality of the crypto markets went on absolute tears to the upside. This time around, we’ve had pockets of the market that have gone on absolute tears to the upside, but the majority of the market has been left behind. On top of this, the pockets of outperformance mostly occurred at distinctly different times rather than together; the hot ball of money.

The result is a huge disparity in returns amongst market participants versus the shared winning experience from prior crypto cycles. This is further compounded by the fact that crypto in general (outside of the few outliers) has massively underperformed many other risk assets for much of the last two years as well.

None of this is new. Many people, including us (notably in our Year Ahead report from last year), have written about this dynamic many times from various lenses over the past 18 months. And given the excruciatingly painful start to Q4 relative to other risk markets, questions have started swirling; ‘is it joever for crypto?’

No. The earliest days may be behind us (we are in my 4th crypto ‘cycle’ and I don’t consider myself OG by any stretch), but crypto is still early in its overall journey. All else equal, the market is simply starting to mature. This isn’t inherently good or bad, it just is what it is. Everything with competition evolves over a long enough timeframe.

The most obvious direct comparison to crypto’s market maturation path and evolution would be traditional finance markets, and we’ll get to that. Take sports as another analogy. Sports are a pure expression of competition. This competition exists at all levels and ages of play.

NBA in the 1950s 😭😭 pic.twitter.com/irbfolOXEF

— DraftKings (@DraftKings) June 16, 2025

The base level floor of participation in these sport competitions is magnitudes higher than it was back in the ‘vintage eras’. Its not even comparable, just watch any NBA video from the 1950s and compare the play to the modern version we see today. Things that are seen common today, and even seen as the price of admission for the high level athletes of today (such as extreme physicality & technicality, health & fitness regimes, sports science, sports psychology) were alien concepts to everyone decades ago, save for a few pioneers ahead of their time.

If you dropped LeBron into the 1950s NBA, he would score 100+ points a night. After a week he would be burned at the stake for witchcraft. Nowadays, 13 year old tik tokers are health-maxxing with saunas and cold plunges. Times change and things progress.

The same thing happens everywhere in which competition exists. Poker, Chess, Go, video games, the list goes on.

Financial markets, and crypto, are another relatively pure expression of competition. As the crypto native market participants continue to level up, and as the more sophisticated participants from TradFi enter the arena, the crypto market will continue progressing onto the next stages of market maturity.

Competition From All Angles

Crypto participants continue to level up over time, from one cycle to the next. Back in 2017, CT barely knew what the FOMC was, and certainly didn’t watch monthly CPI prints. Perps were new and most people didn’t know how to use funding rates and open interest properly!

Nowadays, CT regularly follows macro trends & JPow press conferences (global liquidity is a household investor term now), and perps have become one of crypto’s killer products.

And while many people fail to learn and adapt, this is generally not true of the overall market. Think back to the early days of memecoin trading from the current market cycle. At first it was relatively easy, there was little competition and the market was relatively inefficient. Fast forward several months, and the memecoin game has become extremely competitive.

Mafia style memecoin deployers & farms pump out memecoins at the same rate as industrial revolution era widgets. Whatever alpha originally existed has all but been found out and captured. Think of NFTs, DeFi farms, low float high FDV chain launches, and so on. It is all the different versions of the same phenomenon.

On top of this, crypto has reached the point in which the flagship asset, BTC, has attracted the attention of institutional investor class. Traditionally seen as ‘sophisticated’ these market participants are making their way into crypto from a variety of angles. To identify a few:

- Institutionalization & corporate chain launches

- ETF products

- RWAs

- Stablecoins

- Market Making

- Exchange Venues

This increased competition will likely fracture the total amount of investment capital available for crypto allocations further, thus driving further disparity in crypto returns.

Speculation has always been a hallmark of crypto markets, and for a while crypto was the hotbed for speculative capital to flow. The historic stimulus that ushered in the post-COVID investing era absolutely turbocharged the crypto industry, and pound for pound the crypto market was the biggest beneficiary of any market anywhere, at least for a while.

Over the last several market cycles, crypto was the obvious destination for speculative dollars looking to venture far out onto the risk curve. It was obvious due to its seemingly reflexive upside potential from a monetary perspective, as well as obvious from an ‘interesting pioneer tech’ perspective.

Yet the investing landscape today has shifted — and the surface area of speculative growth opportunities is much larger today than it was even just a few years ago.

The 2020-2021 cycle happened pre-AI’s ChatGPT moment. Fast forward a few years and we now have multiple exponential technologies all vying for investors’ attention and speculative dollars.

TLDR: for every $1 of new liquidity, there’s way more investable growth assets for that dollar to flow into.

Here’s just a few quick examples…

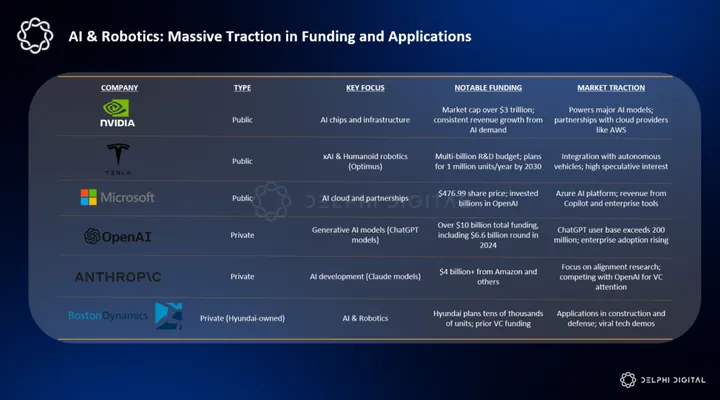

Competition from AI & Robotics

The AI and robotics sector has seen explosive growth in the last 24 months, with private investments in generative AI reaching nearly $35 billion in 2024 (an 18.7% increase from the prior year and over 8.5 times 2022 levels). Robotics startups alone secured over $2 billion in Q1 2025 funding, with 70% directed toward warehouse and manufacturing automation. This surge positions the sector as a prime alternative for speculative dollars, offering exposure to transformative technologies like AI, machine learning, robotics, and more.

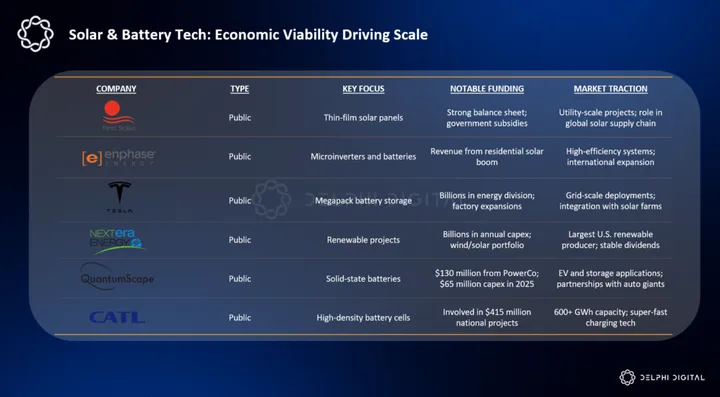

Competition from Solar/Battery Tech

It wasn’t long ago when alternative energy was more of a play on goodwill and sustainability, rather than one of the most cost effective (and commercially viable) energy sources of the future.

Solar and battery technologies are now economically competitive, with U.S. solar capacity additions reaching 7 GW in Q1 2025 (an 11% increase YoY).

Cost curves for solar panels fell, adjacent technologies like lithium battery storage got a lot better (and cheaper), and the mad scramble for power — catalyzed by AI’s insatiable needs — is accelerating the buildout of more economically viable alternative energy solutions. The biggest demand catalyst imaginable (AI) is now the forcing function for turning the pipe dream of alternative energy into a booming investable sector, with one of the largest supply-demand imbalances to be fulfilled over the coming years.

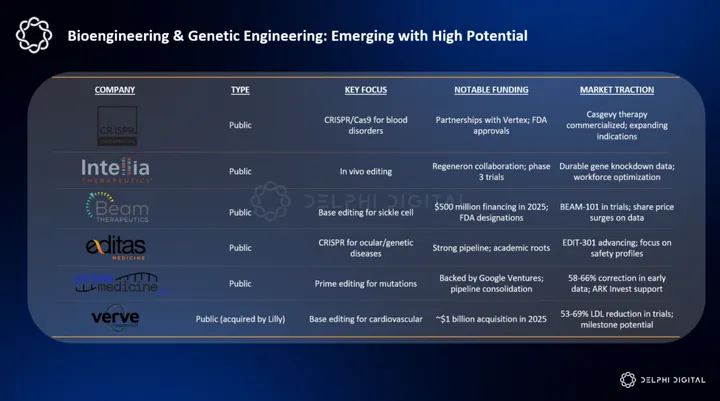

Competition from Bioengineering and Genetic Engineering

Bioengineering, especially CRISPR-based genetic editing, is projected to expand at 15.7% CAGR to $40.1 billion by 2034, fueled by clinical successes and high commercial potential. U.S. biopharma clusters like Cambridge, MA, drew in over $2 billion in NIH funding and $657 million in VC funding over the last 18 months. This sector attracts investors with breakthrough therapies, though regulatory and moral debates introduce potential headwinds.

Simply put, crypto is no longer the only game in town. Liquidity has other viable alternatives now, and as crypto graduates into the big leagues, it has begun to face competition from other assets for capital allocation and speculative investment dollars.

Another expression of this can be found when looking at crypto equities versus crypto altcoins.

Now that institutions are unequivocally interested in crypto as an investable asset class and emergent technology, crypto related equities have begun re-rerating in reflection of this. Over the past 24 months, crypto equities have outperformed the majority of crypto altcoins.

Institutional capital has been more interested in spot ETFs on the crypto majors like BTC/ETH and crypto-related equities such as Robinhood, Coinbase, or Galaxy. Crypto equities have effectively vampire attacked a portion of the speculative bid & liquidity that would have otherwise flowed directed into altcoins.

This shouldn’t be all that surprising, and was something we cautioned about in our Year Ahead report from last year, namely the behavior pattern that institutions would likely gravitate towards businesses and protocols that generate fees, revenues and cashflows with value accrual mechanisms.

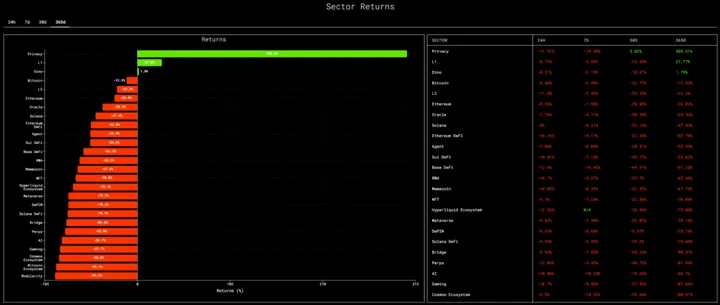

Market of ‘Despair’ity: The Stock Pickers Market

Everything we’ve discussed until this point has contributed to an unprecedented dispersion in crypto returns over the last 18-24 months. At the present moment, it seems likely that this trend is to persist throughout 2026 as well.

https://members.delphidigital.io/reports/year-ahead-for-markets-2025#the-missing-ingredients-3faf

https://members.delphidigital.io/reports/year-ahead-for-markets-2025#the-missing-ingredients-3faf

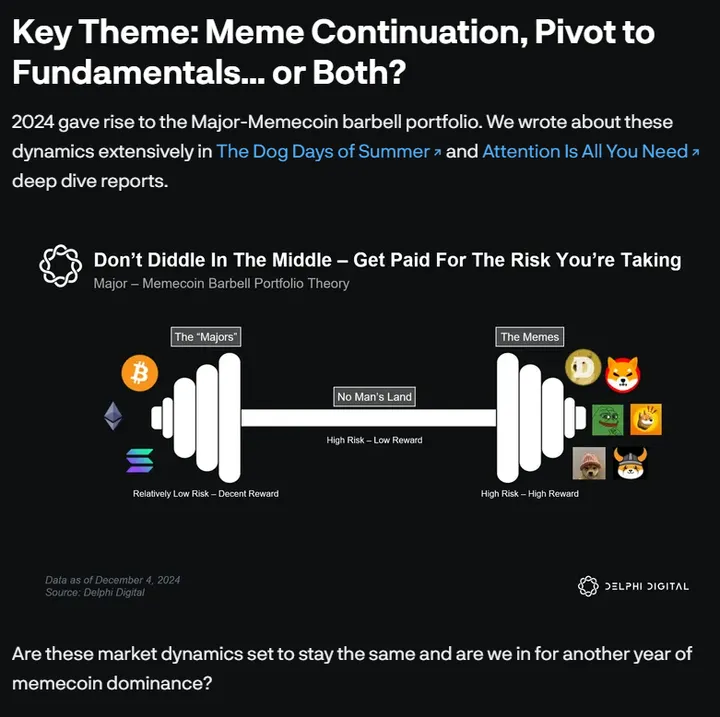

From 2023 throughout the majority of 2024, we had what we referred to in our Year Ahead report from last year as the “Major-Memecoin” barbell portfolio.

We thought that the institutional bid between spot ETF approvals and people like Saylor, bitcoin would continue to outperform the majority of assets. We also thought that memecoins would likely be a sector that outperformed given the regulatory overhang plaguing a large swath of crypto assets. Specifically memecoins on chains with a lot of onchain activity, Solana at the time.

This strategy worked really well for a long time, but eventually the optimal allocation strategy began shifting. From the end of 2024 through 2025 up until today, we’ve seen a few distinct meta narratives emerge.

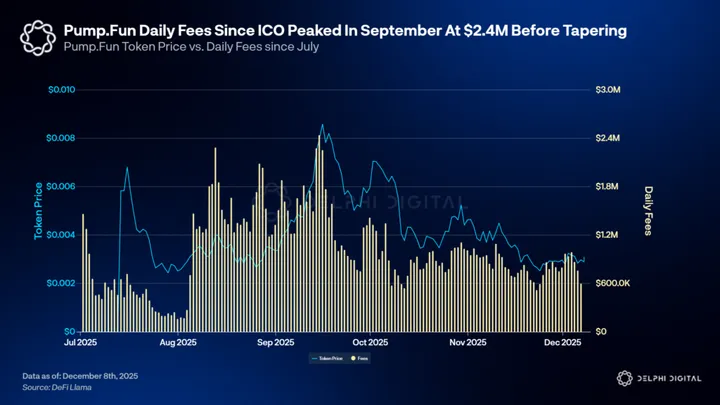

We’ve seen the revenue meta come to fruition with things like Hyperliquid…

…or Pump.Fun.

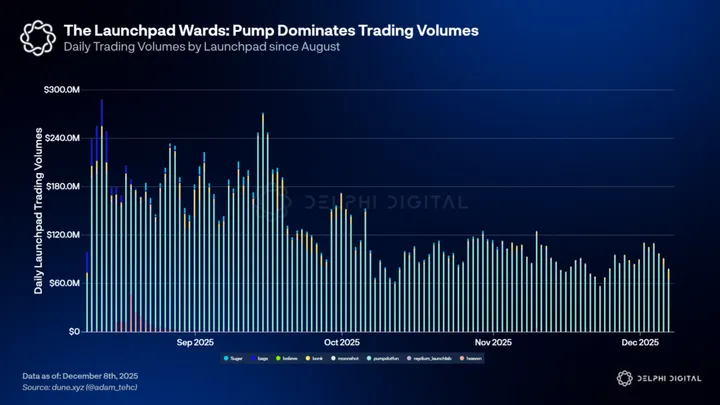

We’ve seen other derivatives of this meta narrative manifest in things like the Launchpad Wars…

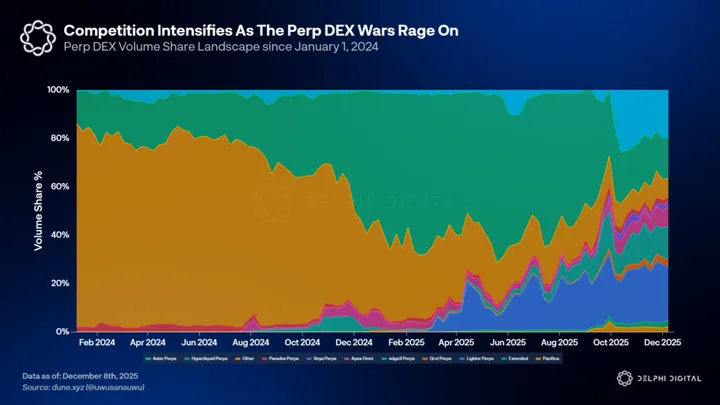

the Perp DEX Wars…

and most recently, the privacy narrative meta.

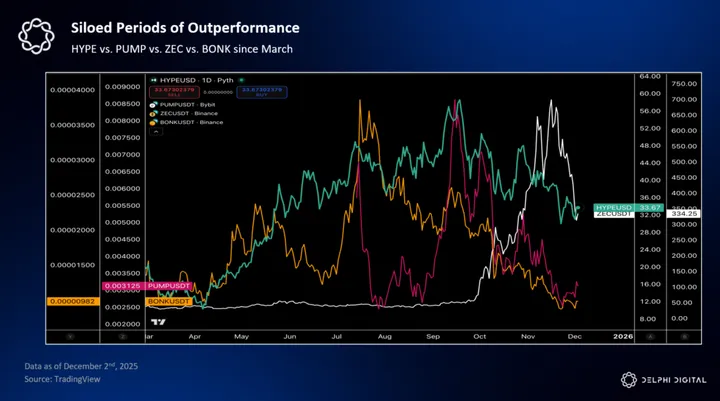

All of these have something in common; they’ve mostly occurred at distinctly separate times (outside of Hyperliquid’s more consistent grind higher).

We haven’t seen any of these main meta narratives take off at the same time. The outperformance of tokens related to these main meta narratives has been distinctly siloed away from the broader market of under performance.

This is clear evidence of the crypto dispersion thesis playing out again after witnesses the “Major-Memecoin” barbell the year prior.

Over the past 30 days or so, since the liquidation cascade of October 10th, everything outside of the privacy sector is deeply negative. Even the strongest altcoins are succumbing to the indiscriminate selling.

This follows a similar trend we’ve seen over the past year, where the vast majority of coins and sectors are generally deep in the red, with only a small cohort of names capturing the entirety of the market outperformance. The crypto market is driven primarily by flows, momentum, and narrative, developing into a market that moreso resembles a stock pickers market rather than a passive allocation market.

In this type of market, crypto flows and attention coalesce around a select few names that are demonstrating strength amongst a sea of weakness (due to ETF flows, token buybacks, social media attention share).

https://novelinvestor.com/sector-performance/

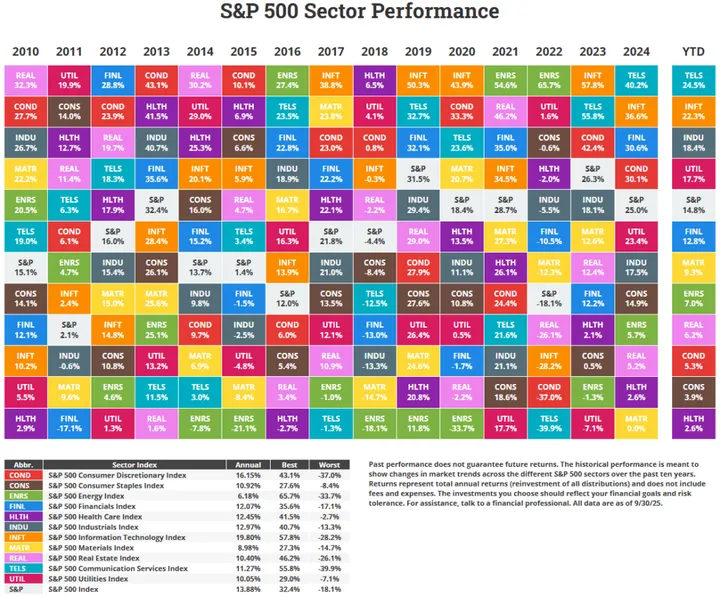

Although the mechanism is different, the result is something similar to equity markets in which the majority of outperformance is confined to a select few winners and sectors (ex. MAG-7, big tech). Crypto has yet to mature to a point where SPY-like fund products allow investors to get passive exposure to “market beta”, because there aren’t that many clear long-term growth assets with obvious secular tailwinds beyond heavy speculation yet.

Markets = f(Supply, Demand)

All markets are a function of supply and demand. Prices simply reflect the supply and demand of different assets at various points in time. When demand > supply for some thing, the price of that thing rises, and vice versa.

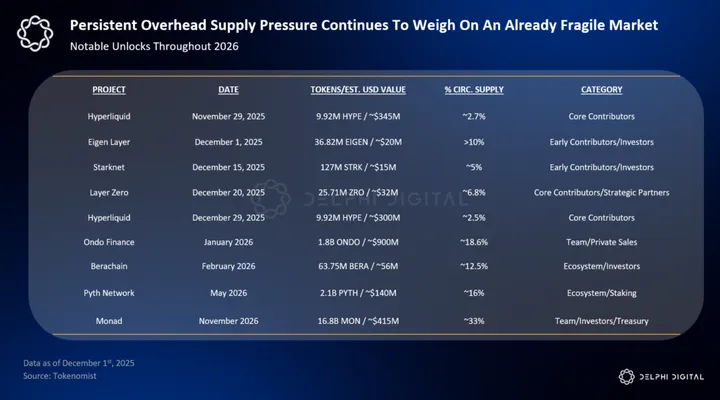

The continued overhead supply issue has further anchored crypto markets.

The supply of crypto tokens has exploded, but demand hasn’t kept pace, so logically most tokens have seen their prices tumble. Over the next 12 months, there is an estimated $3bn+ in major token unlocks.

A lot of this unlock pressure is front and backloaded, dominated by Hyperliquid unlocks in November/December 2025 as well as Monad’s ~$400m cliff in November 2026.

In the first half of 2026, there is expected to be over $1bn in unlocks, led by ONDO, PYTH and another ~$1bn in ongoing linear vests from names like SUI, ARB, STRK, and more. Unlock supply pressure likely peaks sometime in the first quarter of 2026, while the back half of the year remains relatively sparse, except for the aforementioned Monad team/investor unlocks.

This is a dynamic that has been consistently present for much of the last 18-24 months, and one that is likely to continue weighing on altcoin performance well into 2026, further enforcing the prudence and ‘stock picker’ mentality needed to outperform going forward.

Where Does This Leave Us For 2026?

If this dispersion of returns is set to continue, where do we look for pockets of opportunity?

Firstly, we remain steadfast in the view the BTC occupies a narrative niche of its own, and will likely continue to decouple from the altcoin market. Bitcoin has graduated into a true macro asset with its own distinct investor profile, and this ascendence results in higher correlations with traditional markets and global macro trends. Our long-standing thesis surrounding the endgame of currency debasement remains strong.

Beyond BTC, crypto assets with structural bids are good places to start. Structural bids can be demand drivers like ETF flows, real revenues and value accrual to token holders via buybacks or real yield — things that can actually drive sustained demand for the asset itself. For example, several majors like BTC, ETH, SOL can have structural bids from their respective ETFs.

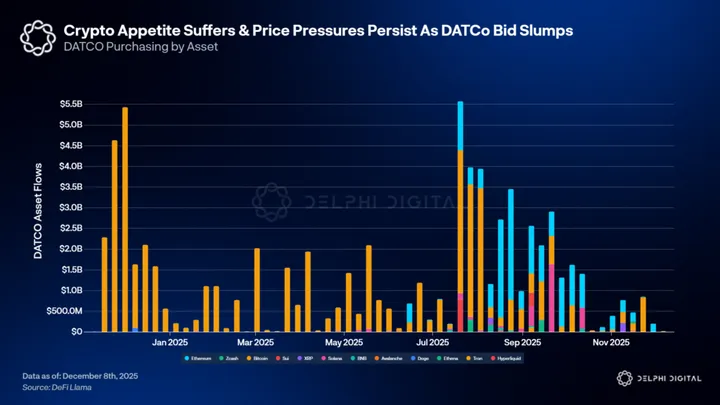

However, this structural bid can be reflexive and cut both ways, as we’ve seen with the recent downturn in ETF flows…

…or Digital Asset Company (DATCo) flows.

Undoubtedly, flows from these vehicles have been significant contributors to price appreciation and momentum this year.

Look no further than BTC and Strategy…

…especially in light of the recent headlines.

Dispelling FUD (part 3) – Saylor FUD

I’ll be the first to admit that MSTR mNAV < 1 is not a good look, but before you dunk on him at least appreciate what he did for crypto over the past 4 years

Take him out of the equation and ask yourself if BTC would have had the same… pic.twitter.com/jJ91dIfFc8

— Kevin Simback 🍷 (@KSimback) December 1, 2025

Absent these source of demand, we’ve seen how thin the bid has been over the last several weeks and months.

Similar to the majors, there are silos within crypto that are trying to achieve a similar type of structural bid, such as as the revenue meta mentioned earlier, or things like the launchpad wars or perp DEX wars. We believe capital and attention will continue to coalesce around these types of assets as you need both narrative and fundamentals to sustain outperformance in a tougher allocation environment. Anchor to reality.

In our Year Ahead report from last year, we highlighted Hyperliquid as a standout protocol heading into 2025.

One year later, we’ve seen how well the thesis for Hyperliquid has played out — from HyperCore to HyperEVM, ecosystem traction, new apps using builder codes — and continue to believe Hyperliquid is worth paying attention to in the year ahead.

It has been impressive to see how the Hyperliquid team continues to execute on their roadmap and vision with HyperCore and HyperEVM. The continued traction and revenue generated by Hyperliquid core business has been equally impressive, even amid a sea of competitors vying for the perp DEX crown.

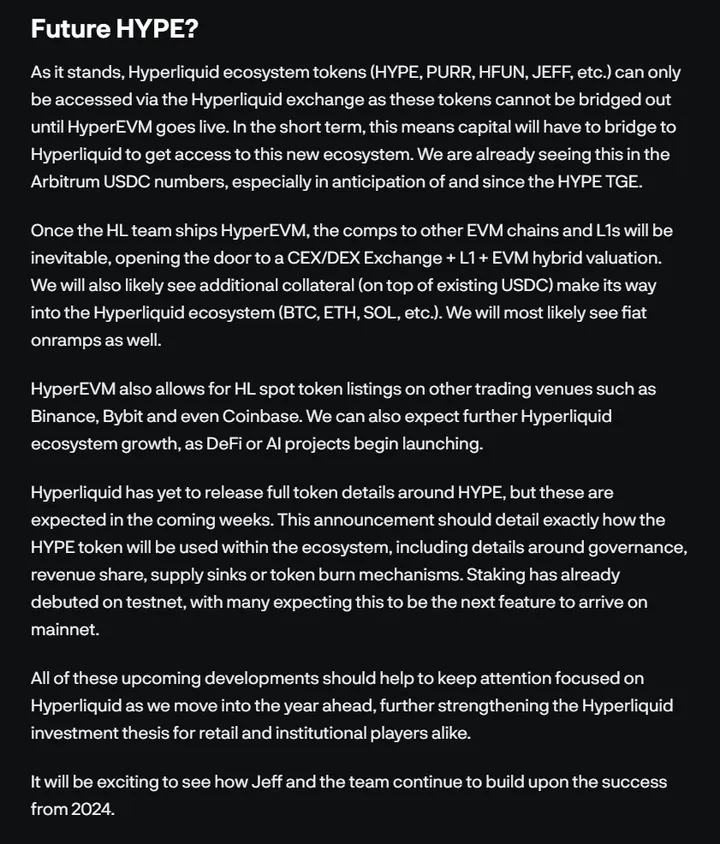

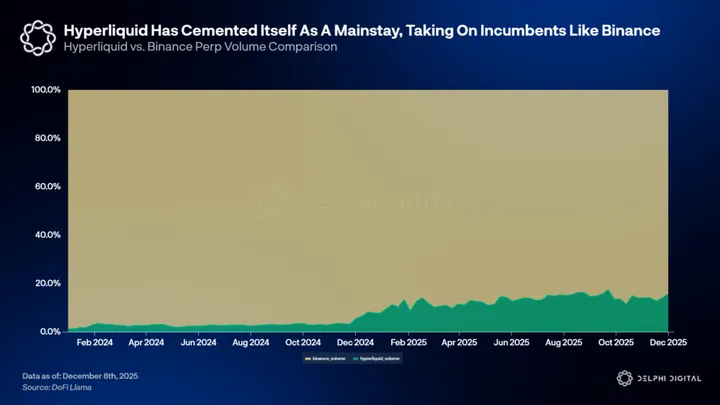

As it stands, Hyperliquid continues to encroach on incumbent territory.

Hyperliquid’s perp volume as a percentage of Binance is in the 10-20% region. When compared against the other major CEXs, we see even more encroachment.

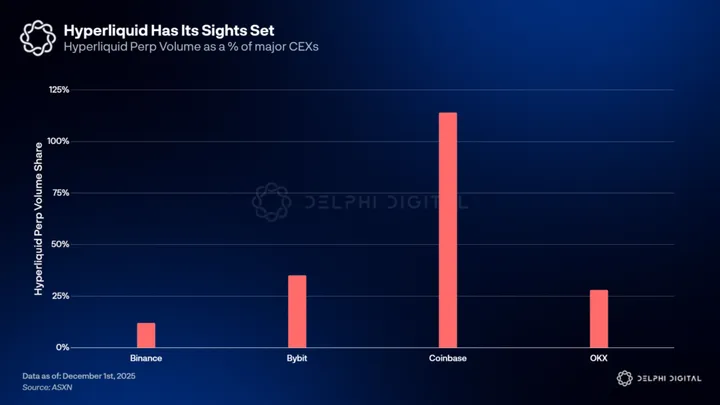

Hyperliquid’s success has been so strong that we’ve seen an all out war break out between perpetual DEXs.

As it stands, Hyperliquid remains at the head of the pack, but competitors like Binance’s Aster, Lighter, Paradex and others gaining traction quickly.

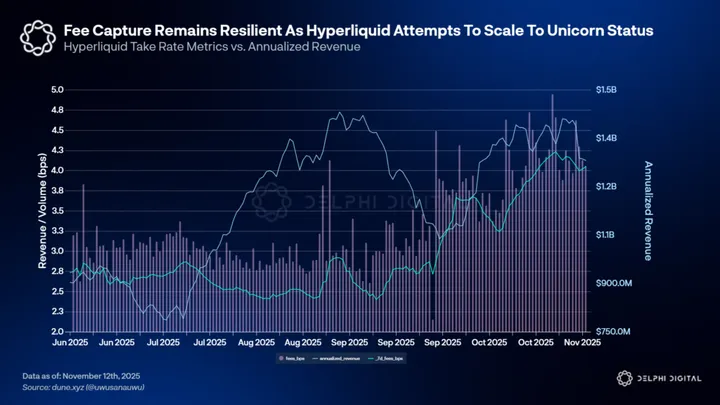

Despite this onslaught of competition, Hyperliquid’s key metrics remain resilient.

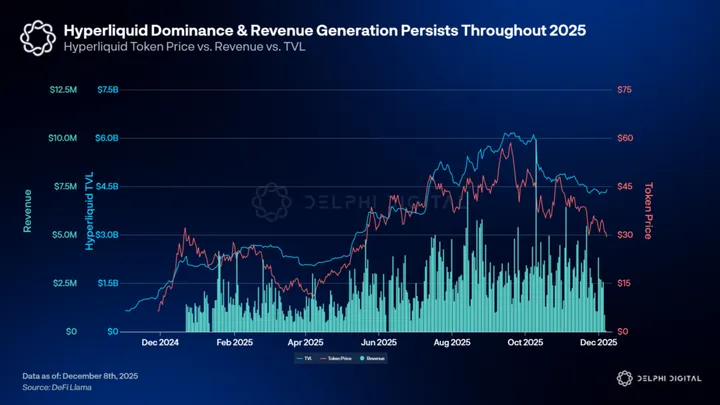

Over the first week of December, Hyperliquid facilitated over $45B of perp trading volume, bringing total traded volume on the platform to over $3.2 trillion since inception. Hyperliquid is now the 4th largest exchange by OI, sitting at $6.75B despite the October 10th liquidation event.

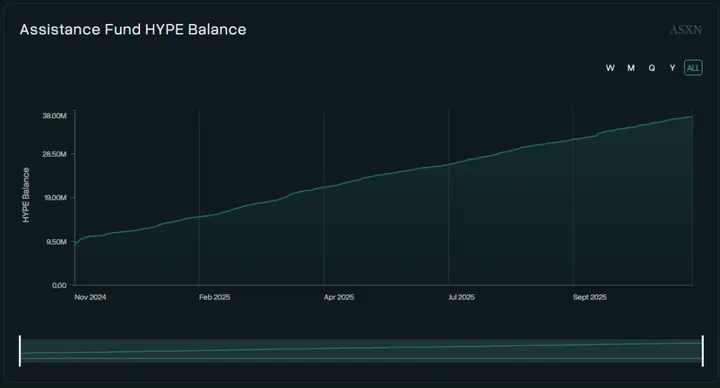

Over this same time period Hyperliquid made about $18M of revenue. The Hyperliquid assistance fund bought back ~$10.5M of HYPE (~334K HYPE).

The HYPE assistance fund now holds 35.83M HYPE ($1.15B USD) or roughly 10% of circulating supply.

At TGE, the Hyperliquid Foundation validators had a combined HYPE stake of 300M HYPE, representing effectively 100% of the total HYPE staked. Over the past year, an additional 114M HYPE has been staked, with the total HYPE stake reaching just over 41% of total supply.

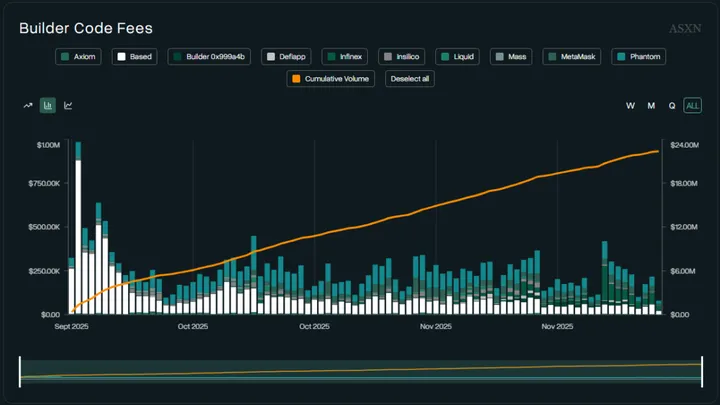

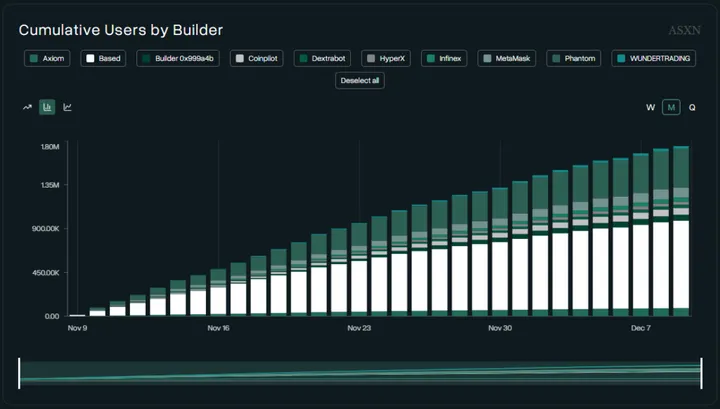

More recently, we’ve seen the explosion of HIP3, Builders and Integrations within the Hyperliquid ecosystem, providing further validation of the Hyperliquid thesis.

Projects like @tradeperps have listed over a dozen equities markets & have recently enabled growth mode on their NASDAQ market XYZ100. The XYZ100 market has become consistent top 5-6 market on Hyperliquid by trading volume.

@felixprotocol has launched equity perps, with TSLA and CRCL perps available for trade.

Total builder fees have surpassed $45M.

With over 2 million users, Builder codes actually make up ~40% of daily Hyperliquid users.

The below ecosystem map does a pretty good job highlighting a lot of what is going on in the new Hyperliquid ecosystem (although ASXN is missing from the Data Analytics section). Another comprehensive map can also be found here.

https://x.com/redstone_defi/status/1963285899300806858/photo/1

But what about the unlocks? Valid question.

Hyperliquid’s ~$300M monthly HYPE unlock began on November 29, 2025, representing one of the largest single unlock risks over the next 12-24 months. The terms are as follows.

Total HYPE unlocking: 238,000,000 HYPE (23.8% of total supply)

Vesting Structure:

- Cliff Period: 12 months post-TGE (November 29, 2024 – November 29, 2025)

- Linear Vesting: 24 months (November 29, 2025 – November 29, 2027)

- Monthly Release: 9,916,667 HYPE (~$300M at current price)

Update about the unlocks from Hyperliquid:

2.6M unstaked

854k restaked by Hyperlabs team

1.745M distributed to team walletsFrom these team wallets the following is done:

* 609k sold OTC (through Flowdesk)

* 235k is staked again by team members

* 902k is still in spot on… pic.twitter.com/lr4LQhaklx— Hyperliquid Eco (@HyperliquidEco) November 29, 2025

So far, the post-unlock actions are as follows:

- 2.6M HYPE unstaked

- 854K HYPE restaked by Hyperlabs team

From these team wallets the following has occured:

- 609K HYPE sold OTC (through Flowdesk)

- 235K HYPE staked staked by team

- 902K no additional actions, still in spot on Hypercore

While it is still too early to extrapolate out for the next 12-24 months, the actions taken by the Hyperliquid team are encouraging with respect to signaling around unlock-related sell pressures. These unlocks have been a large uncertainty for some time, and HYPE holders finally have an idea of what to expect.

Since August, Hyperliquid has generated over $375M in revenue, driven by primarily by trading fees and emerging HyperEVM/HIP-3 revenue streams. If the Hyperliquid team’s actions remain consistent for 2-3 months, it will likely be enough to extrapolate sell pressures further out.

Combining the continued core product performance and traction with the flourishing HyperEVM ecosystem, Hyperliquid’s bull case remains one of the strongest in the industry (outside of BTC). Even with the recent market downturn, price pressures, and unlock uncertainties, Hyperliquid remains in a fundamentally strong position in our view. Given the team’s track record thus far, the future of Hyperliquid could be very bright.

There are some other projects that have a similar structural bid-type thesis backing them. The below X.com article highlights a few here.

— blocmates. (@blocmates) December 1, 2025

Even with structural bids, projects like Hyperliquid have faced serious performance pressures. Now think about the near infinite universe of tokens that don’t have any of these redeeming factors? The severe underperformance borders on inevitable.

Earlier in this section, we spoke about areas in which the sophisticated TradFi investor class are most keen on, like:

- Institutionalization & corporate chain launches

- ETF products

- RWAs

- Stablecoins

- Market Making

- Exchange Venues

It stands to reason that opportunity will inevitably arise in some of these areas, which we cover throughout the rest of this report.

Allocating over the year ahead will require prudence, discretion and timing. The advantage has gradually shifted from generalists to specialists and those who can sift out the noise in order to find a few key signals and trends as the industry matures.

Institutionalization Isn’t Coming, It’s Already Here & Starting To Take Over

On-chain Credit Migration: Over-collateralization to reputation

One of the larger trends making waves is the migration of credit markets onto blockchain rails. In the past, almost all of DeFi was some form of over-collateralized lending. While this has been good for trustlessness and solvency, it has remained quite fragmented compared to the behemoth that is the global debt market (Billions vs. Trillions!).

Thus, it seems clear that 2026 will bring with it more digitization of credit/reputation (already being done via ZKTLS by teams like 3Jane), more professionalization of underwriting for blockchain-based assets, and further integration of tokenized real-world assets and securities to marry on-chain liquidity with faster time-to-market. All made possible and advantaged by the massive off-chain global economic activity.

A New Challenger Approaches:

DeFi protocols and OnChain neobanks are perhaps the first genuine challengers to incumbent banking systems in a long time. In fact, Aave’s recent October peak of over $45B in total value locked would put it near the top 50 US commercial banks by total deposits, exceeding financial institutions like Barclays and Deutsche Bank.

The “banking flip,” as we like to call it, highlights a meta-shift rather than a simple accumulation of assets. Traditional banks have high overhead costs, dated infrastructure, and a slow, manual compliance process.

Places like Aave are software protocols that automate liquidity provision, interest rate changes, and liquidations all via smart contracts. This speed, combined with its global accessibility, has been evident in Aave’s 2025 success, which rivaled that of mid-cap fintech companies in sustainable fee generation. Not only is the revenue impressive, but Aave has been incredibly resilient, processing $180 million collateral liquidations in under an hour during the mass freakout on October 10th.

This resilience, combined with Aave’s steady TVL growth, proves that capital allocators do not simply view on-chain liquidity markets as gambling venues, but as truly viable places to let their capital go to work without giving up a massive cut to some banking incumbent. Looking forward to 2026, Aave’s liquidity consolidation creates a strong network effect, with the deepest pools getting the best rates. Aave will remain the central bank of the DeFi ecosystem.

Legitimizing Underwriting and Private Credit Onchain:

While Aave continues to dominate the over-collateralization onchain market into 2026, an opportunity arises in Aave’s inability (by design, not a dig!) to service unsecured or under-collateralized borrowing demand. Unfortunately, the mass crime on crypto lending platforms in previous cycles has quickly shown the necessity of onchain auditability and transparency in private credit markets.

This year has seen the growth and expansion of major on-chain private credit protocols like Maple and Centrifuge, which have grown to billions in deposits. Unlike the smart-contract/algorithmic model of Aave, which uses its code to automatically liquidate collateral, platforms like Maple and Centrifuge use human credit professionals to be pool delegates. The delegates then assess the creditworthiness of borrowers off-chain whilst managing the loans onchain. 2026 will see the emergence of a second form of DeFi, one characterized by reputation and revenue-backed credit.

To understand why this new form of DeFi will characterize 2026, we must first understand the ceilings of the trustless lending model of our previous cycles.

In a market where most people remain pseudo-anonymous and legal recourse is basically non-existent, the only way to protect a lender is if that borrower has more to lose by defaulting. This is partially why over-collateralization became so popular, as it essentially formed a self-policing ecosystem.

However, the proper credit of the modern economy is the ability to borrow against future productivity rather than just one’s current assets. While some protocols in the past have attempted this via delegated underwriting, this brought the same pains of trad-banking onchain rather than actually innovating, and, in turn, created a lack of transparency that led to credit contagion like that in Celsius and 3AC.

One such solution to this problem can be seen today in protocols like 3Jane, which operate as credit-based point pools for money markets. While 3Jane is still relatively small (31m in TVL as of writing), its algorithm-driven, instant, undercollateralized USDC credit lines are, in my opinion, a peek into the future of credit–based DeFi at large.

The issue with credit onchain that immediately arises is privacy. To underwrite a loan effectively, a lender by definition needs invasive access to the borrower’s identity and financial history. Naturally, this is quite the opposite of what nearly all DeFi participants seek. Thus, 3Jane utilizes zkTLS to solve this.

We won’t go too deeply into the technical specifics of zkTLS, as we wrote a full report on it earlier this year, but what you need to know now is that zkTLS enables the creation of a zero-knowledge proof attesting to the content of a TLS session. Basically, this can generate a proof that says: “I certify that a TLS session occurred with chase.com at, signed by Chase’s verified certificate, and the data packet contained a balance > $150,000,” without revealing anything else about the user’s data or identity. In practice, 3Jane doesn’t see anything about the user’s account number or transaction history; it only receives the verification that the user meets the underwriting criteria (a simple yes/no or true/false). This unlock is quite massive, as it allows 3Jane to utilize the already established credit scores/balances/cash flows of Web2 to verify a borrower’s legitimacy without creating a data silo or exposing user information.

3Jane further innovates on credit-based DeFi via its credit algorithm, which assigns credit scores to wallet addresses by fusing users’ web2 data verified via ZKTLS with their onchain history (e.g., User has been liquidated X times on Aave). This algorithm monitors the borrower in real time onchain and can thus dynamically reduce the credit limit or increase the loan’s interest rate. Furthermore, 3Jane can underwrite AI agents via this method, treating an agent’s performance history as its credit score, perhaps enabling a new agentic form of DeFi in 2026 with the proliferation of trading agents like that in Jay Azhang’s Nof1

While 3Jane is an excellent example of what credit defi could look like in 2026 from the borrower identity vector, the Sky ecosystem (formerly MakerDAO) pursues it from the asset origination vector, transforming the industrialization of the stablecoin sector.

For almost 10 years, MakerDAO was in the evoked set for all of DeFi stability. It’s stablecoin, DAI, was largely censorship-resistant and backed primarily by ETH and other tokens. However, MKR and DAI faced trouble in the real world during the recent high-interest-rate environment, which threatened yield starvation in crypto. To address this, Maker rebranded completely to Sky, did a token split, and renamed DAI to USDS.

The most controversial yet significant change in the rebrand and transition was the introduction of a freeze function for USDS, which allows protocol admins to freeze funds in wallets to comply with orders/enforcements. This is quite the move, especially for what was once a more cypherpunk DAO project. Still, it makes sense given their aim to integrate into the global banking system, hold billions in RWAs, all while meeting OFAC regulations.

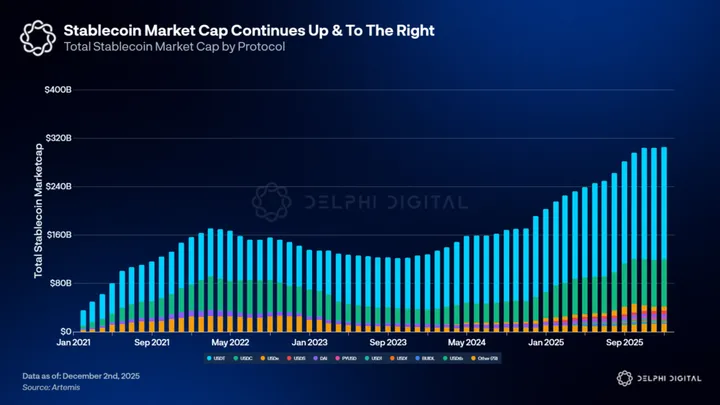

Ok, but why mention Sky? Well, that’s because one thing that defined 2025, and will continue to define 2026, is more stablecoins (boring, I know). We have over 300 stablecoins and counting, with more being launched by companies every day (Klarna just announced its own).

As such, Sky wants to be at the forefront of this trend in 2026, creating Obex: a $37 million incubator backed by Framework Ventures, LayerZero, and the Sky Eco fund to give USDS high-yield places to deploy capital and scale the stable. Obex then functions as the dedicated capital allocator for the Sky protocol, with a mandate to create the next generation of collateral for USDS.

Obex functions as a Y-combinator for stablecoins, with a 12-week cohort-based program in which teams receive tech support from LayerZero and strategic guidance from Framework. The “winners” of Obex get access to Sky’s massive balance sheet, which recently received the go-ahead to deploy $2.5 billion into qualified Obex projects, helping solve the biggest crux for any new stablecoin/yield-bearing asset: starting liquidity.

We are mainly mentioning this in the year ahead because of the direction of Obex investments, which they claim to be “unconventional RWAs.” T-bill tokenization is largely solved via BlackRock’s BUIDL and others, so Obex is looking for assets that offer both high yield and strategic value to the digital ecosystem.

Things like energy infrastructure via solar/battery/grids, compute infrastructure via GPUs/data centers/AI credits, and private credit via specialized corporate debt and fintech lending. Energy and Compute are perhaps two of the most essential commodities in 2026, so it makes sense that they will be tokenized and used for yield in DeFi.

In the year ahead, more corporations will have their own private chains (discussed later) and their own stablecoins for their own products, thus DeFi’s competitive advantage can not be derived solely from government debt yield, but rather upon democratization of yield for assets that are otherwise very cumbersome to own/invest in. We believe that Obex is just the start of more DeFi Initiatives seeking to bring under-collateralized lending or RWA yield into a safer, more friendly package.

In the past, RWA basically either meant faux proxies for real estate or just tokenized T-bills. In 2026, RWA will mean productive infrastructure, targeting the seemingly insatiable global demand for these assets and bringing them onto blockchain rails.

Daylight is one such example, emerging as a leader in the DePIN space by aggregating distributed energy sources such as solar panels and batteries into virtual power plants. Their financial layer, DayFi, allows users to mint yield-bearing tokens backed by the distributed power grid’s revenue.

- Homeowners pledge their battery capacity to the daylight network

- During peak load times, the network discharges this power to the primary grid and earns revenue from utility companies

- Revenue flows back to the yield token holders. DayFi yields are then derived from energy arbitrage

- Operates as an undercollateralized model and relies on flows of revenue rather than the liquidation of the asset

Another example is USDAI, which tokenizes AI compute. USDAI is a stablecoin pegged to the dollar, and sUSDAI is the yield bearing version. The stablecoin is backed by loans issued to AI infrastructure companies to purchase GPUs; thus, the yield comes from the lease payments they make to “rent” the GPUs.

USDAI is another form of undercollateralized or reputation-based lending due to the rapid depreciation of the underlying hardware. The protocol relies on the AI sector’s cash flow to remain solvent, while leveraging the transparency of onchain revenue streams to monitor the borrower’s health in real time.

The Obex incubator, the recent success of Daylight, and projects like USDAI represent a trend shift towards commodity-backed currencies and more undercollateralized and reputation-based lending. As we move into 2026, where regular FIAT currencies are increasingly untrustworthy, we will see more and more currencies backed by the capacity to do work (like energy or compute) to better act as a hedge against inflation and debasement.

Corporate Chain Wars: Verticalization Over Everything

Stripe’s Tempo: Payments, Payments, Payments

For the longest time, the central thesis of L1 chains in crypto was that they would accrue value as crypto usage grew, but this has been effectively invalidated. The largest FinTech companies that are now adopting blockchain rails have no desire to be tenants on another chain. They would much prefer to be landlords of their own than renters.

The crypto economy is about to be filled with specialized L1s and L2s launched by FinTech giants such as Stripe, Robinhood, Kraken, and others. Every major bank will get in on the action, expanding beyond “stablecoins” into areas like tokenized deposits. Distribution is the primary driver of blockspace value, and these FinTech companies must build their own chains top-down rather than bottom-up. After all, why would any company with tens of millions of users not own its vertical stack?

Firms like Stripe already have millions of users and distribution. In contrast, a new L1, by definition, starts with no users and no distribution. It is far easier for firms like Stripe to build their own chains for their existing user base and applications than to migrate that user base to another existing chain. It’s akin to creating your own headquarters rather than trying to move into another company’s while it still exists there.

Stripe is obviously the biggest company we’ve seen in this category with their announcement of Tempo earlier this year. Tempo is explicitly built for Stripe’s payment velocity, not meant as a general-purpose base layer chain.

Crypto payments have always been relatively limited by the gas token issue, in which merchants using stablecoins still need to hold ETH or SOL to pay network fees. Tempo gets rid of this via their Enshrined AMM, which allows transaction fees to be paid in any supported stablecoin (KlarnaUSD/USDC/USDT, and many more). The protocol then automatically converts these stablecoins for the validator compensation in the background.

This enables a deterministic cost model for businesses: a merchant using Stripe on Tempo can calculate costs strictly in USD and treat gas fees as COGS, without having to worry about hedging volatile native gas tokens. With a claimed throughput of 100,000 TPS and sub-second finality, the chain obviously isn’t that decentralized, with permissioned/semi-permissioned validator sets composed of key partners.

Just recently, Klarna announced it would build KlarnaUSD on Tempo, allowing it to bypass the middleman fees of incumbent credit card providers for many of its internal settlements and cross-border payouts. The implications of this are significant. Suppose a neobank or payment processor can simply issue their own stable on Tempo and settle transactions for a fraction of a cent. In that case, the 2-3% interchange fee (a small part of which obviously goes to fraud protection) of tradfi is under quite a threat (good riddance tbh).

Robinhood L2: Tenev Tokenization

While Stripe is focused explicitly on payments, Robinhood is also building its own blockchain to tackle the tokenization of equity markets. They are choosing the layer 2 route, using the Arbitrum Orbit Stack and Arbitrum Stylus to enable smart contracts written in multiple programming languages.

Robinhood’s choice of Arbitrum Orbit over the OP stack (which Base and Ink use) is a technical decision rooted in the requirements of its trading engines. Stylus supports multi-VM compatibility, meaning Robinhood’s existing matching engines, often written in C++, can be ported easily rather than rewritten in Solidity. The chain will be specialized for Stock settlement and real-time risk control. Robinhood will enforce strict whitelisting and KYC at the sequence level, enabling only compliant participants to trade the securities.

The recent launch of tokenized stocks and ETFs is the beachhead, with the L2 enabling easy auditability for the assets.

Vlad Tenev has perhaps been the most vocal supporter, aside from Larry Fink, of tokenization, and as such, he sees the value in using crypto and blockchain as rails. It is worth glancing at the note LTR wrote earlier this year when he interviewed AJ Warner (Offchain Labs/Arbitrum CSO) about the Robinhood chain.

I believe tokenization is the greatest capital markets innovation since the central limit order book https://t.co/NHwcR7OCmV

— Vlad Tenev (@vladtenev) July 8, 2025

Fragmentation to Abstraction and Aggregation

While corporate chains will continue to be launched and announced throughout 2026 (Circle already announced ARC), the proliferation of these chains obviously comes with more liquidity fragmentation. A user holding KlarnaUSD on Tempo can’t just buy a tokenized stock on Robinhood’s L2 without first swapping and bridging, creating friction that introduces new problems. That being said, every major FinTech will most likely have its own stable. Xai is already hiring for its “X-money” service, signaling perhaps a new era of P2P and Agentic commerce defined by a reduction in the middleman in favor of verticalization.

Such fragmentation has already driven, and will continue to drive, demand for chain abstraction layers or aggregation apps. These allow users to interact with all sorts of applications, chains, and protocols without even knowing which specific chain they are on. So, while corporate chains may create a walled-garden effect on liquidity, the success of apps like Fomo and businesses like Privy and Turnkey that abstract and simplify onchain actions will continue to accrue value on top of these chains.

The aggregation funnels will matter greatly, which is why media/content is another such thing that will expand massively in 2026. As our industry continues to grow beyond the “CT bubble,” new consumers will look for places where they can easily find Eli5s or TLDRs on industry happenings.

There is no more evident proof of concept than ThreadGuy and CounterpartyTV’s recent meteoric rise, leveraging long-form streaming with short-form clip virality to take over crypto media.

Information discovery is increasingly a social act; people want to find out about new trades, ideas, and news, with live reactions and a more hands-on experience. In one sense, media like livestreaming and new trading applications are becoming increasingly akin to video games, a trend we only see accelerating as younger generations have their main social media networks within open-world games like Roblox.

It seems obvious, then, that the next massive social media platform that rivals the likes of X, Instagram, Facebook, etc., is actually a video game rather than a normal website (see the new Robinhood Social). The gamification of crypto, social media, and entertainment will continue at a far greater pace in 2026, as we have already seen many live events of “trading as an e-sport.”

A New Financial Actor: Agent Economies

2025 was the year when AI Agents learned to read the blockchain, but 2026 will be the year they write on it. The rise of the Agentic Economy in the year ahead is one where agents can transact autonomously amongst themselves, and will create a brand new economic layer distinct from human consumers.

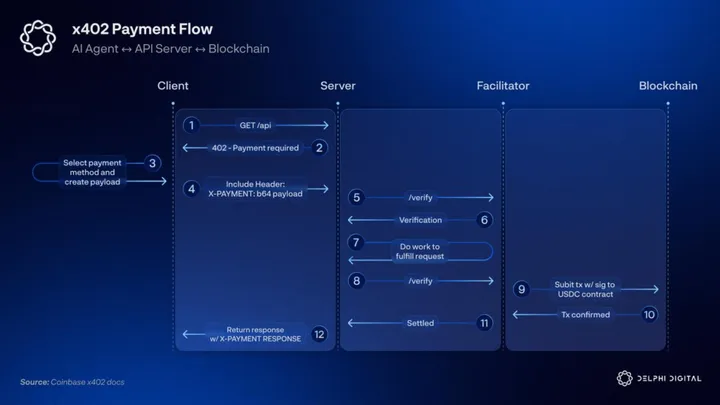

Now, I’m sure you’ve already seen tons of hubbub surrounding the “x402” protocol, but less has been talked about what it means more simply and what it WILL mean as payment chains like Tempo (who will have agents!) start utilizing it.

The x402 protocol allows any web resource or any API to gate access via crypto payment requests. The workflow for this is actually quite simple:

- AI Agent says: “Yo, I need to use/access this thing” (Request)

- Server replies: “Bro, you need to pay for that, here’s my price and wallet address” (402 payment required challenge)

- Agent says: “Alright, bet, I’ll sign the transaction and give you my proof of payment”

- Server says: “Sick, got your payment confirmation, here’s the thing you wanted.”

This solution means AI agents don’t have to navigate shopping carts, credit card entry, or CAPTCHA to access/purchase something. Now they can get it instantly via programmatic and instant settlement, allowing agents to “pay as they go,” thus eliminating subscriptions and the need for sign-in accounts.

Major companies are already adopting it, with providers like Cloudflare and Coinbase supporting x402, giving millions of websites the ability to generate a new, sustainable stream of revenue via agent monetization with a single line of code.

While payments are outstanding and x402 unlocks tons of agentic monetization, trust is still the primary friction in an anonymous M2M economy. If Agent A pays Agent B for some service, how does Agent A know that Agent B isn’t a malicious actor or some hallucinating bot?

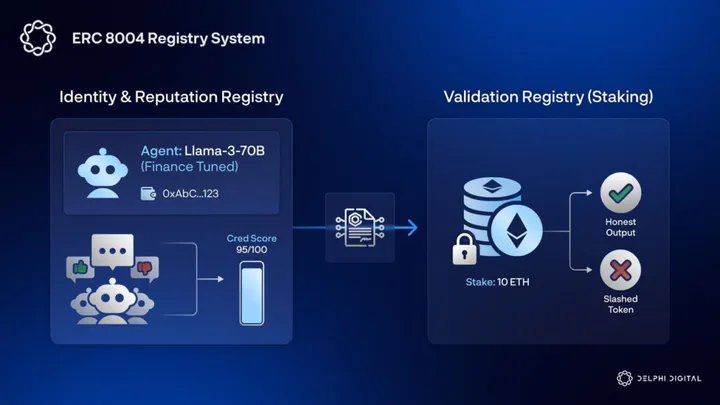

This is where ERC-8004 combines with x402 to put things in overdrive. ERC 8004 introduces a registry system for AI Agents to solve these trust issues.

First, an identity registry maps an agent’s wallet address onchain to its off-chain model specifications (Model Type, What it’s tuned for: e.g., “Llama-3-70B fine-tuned for finance”). Then other agents can leave immutable feedback on the agent’s performance, effectively giving every agent a cred score for their intelligence and prowess.

In addition to this reputation registry, a second validation registry enables staking. An AI agent can put their money where their mouth is by staking ETH to prove their honesty; if the agent delivers a bad output, their stake is slashed.

Now, if we combine the payment of x402 with the identity of ERC 8004, we can create a closed-loop agent economy that can operate at speeds beyond those of human consumers.

Imagine, for example, that a consumer delegates a task like “plan my vacation.” The user’s ERC-8004-verified AI could then subcontract a flight search agent that uses x402 to pay for a real-time flight data API. The travel agent then books and pays for the flight onchain with stablecoins, and the value transfer happens instantly and immutably without human intervention. In 2026, we will see Agent-to-Agent transaction volume start to scale.

More Crypto IPOs, Tokens as Equity, Tokens as Distribution

Now, with more and more corporate chains and tokenized stocks, the political environment has clearly shifted (bye Gensler). 2026 will see many more Crypto company IPOs. Kraken’s IPO has been announced, Securitize has announced theirs, and many more to come. If you think about it, aside from ETFs and DATS (yuck), it’s tough to get exposure to crypto companies via equities. You have the obvious ones like Circle, Coinbase, Galaxy, Bitcoin miners, etc, but beyond those, you run out of options relatively quickly.

As more equities get tokenized, more crypto companies will become equities. Not only will more crypto companies explore the IPO route, but we have seen, and will continue to see, projects/protocols in crypto that attempt to make tokens more akin to equity.

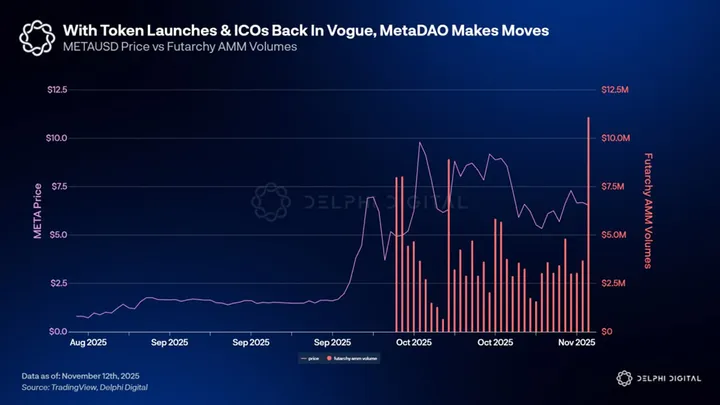

MetaDAO has seen a recent explosion of success with their ownership coins, and the recent Uniswap fee switch regulatory win signals a new era where both IPOing and ICOing can be viable options for legitimate companies seeking legitimate stakeholders.

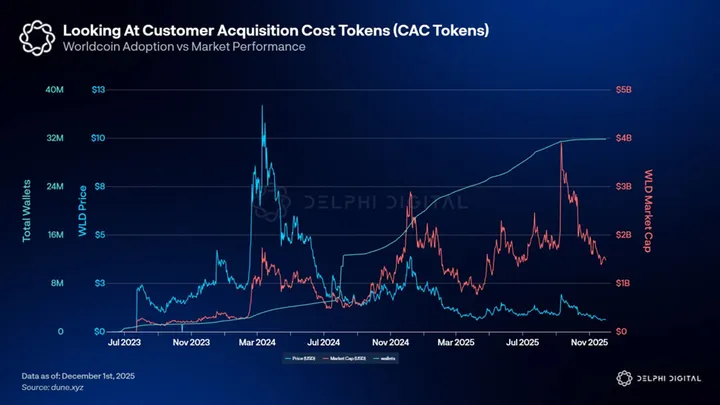

That being said, more companies are beginning to explore tokens beyond purely a claim on the business and/or a forward revenue stream. I’ve been playing with the idea of a token as a distribution means for a company. A prime example of this is WLD and the World App ecosystem as a whole. Despite the coin’s relatively poor price performance, the app’s metrics have never been better and are growing rapidly.

Essentially, WLD is used as a payment or bribe to get a user to scan their iris and onboard, reminding me a lot of how PayPal achieved initial distribution by paying every user $10 to join.

In the end, PayPal burned over 60 million in VC cash on these incentives. World Coin has distributed over 500+ million WLD tokens (over $300M at average prices) but spent zero actual cash on these acquisitions. Token holders hold the cost via inflation, a different economic structure that enables scale that would be impossible or extremely expensive with a normal cash-based CAC.

WLD is thus more like a “CAC” token (Customer Acquisition Cost), used to subsidize the acquisition of verified humans. The marginal dollar of WLD price appreciation is directly converted into user growth via Orb grants.

The token grants also decrease over time, which has incentivized early adoption. Original launch users received more money than current users. Such a declining reward curve mimics normal growth marketing, having high starting incentives and reducing them as network effects take over.

We can see this quite clearly when overlaying their safe/wallet growth over time with their market cap and price. Over time, user numbers rise, prices fall slowly, and the market cap stays relatively stable due to higher inflation in rewards.

We bring this up mainly because, as we enter 2026, the token identity crisis is only growing. More equity will be tokenized, more tokens will try to mimic equity (MetaDAO/Futarchy experiments), but some tokens will be neither and explore other token models.

We have seen WLD do this quite successfully thus far. As more companies like Coinbase issue their own tokens through their products (like $BASE), it makes sense that these tokens would not be equity but rather a new form of rewards/CAC mechanism to drive more value into the company’s actual equity.

Essentially, in the CAC token model, there is an equilibrium in which market cap stabilizes (as seen in the chart) despite users growing and tokens inflating. This happens mainly because new token emissions are absorbed by new users rather than by existing, stale holders, with the price decline offsetting the supply increase.

When the market values 1 dollar worth of tokens distributed as more than 1 dollar of normal marketing spend, thanks to superior liquidity, holder rights, and slick accounting, the tokens serve as a superior acquisition tool.

WLD’s CAC token design also helps it avoid security scrutiny, as it explicitly states that the token is distributed “simply for being a verified human,” rather than for any returns, dividends, or rights. Thus, tokens distributed as “rewards” may not satisfy the Howey Test’s investment-of-money prong. If there are no profit expectations ingrained in the utility/promotion, then the efforts of other dependencies weaken.

Now, as more companies with equity (like Coinbase/Stripe, etc) explore tokens for their crypto products (Base and perhaps Tempo), the CAC model could become more popular. In fact, as Coinbase explores the BASE token, it could be the largest CAC token launch yet.

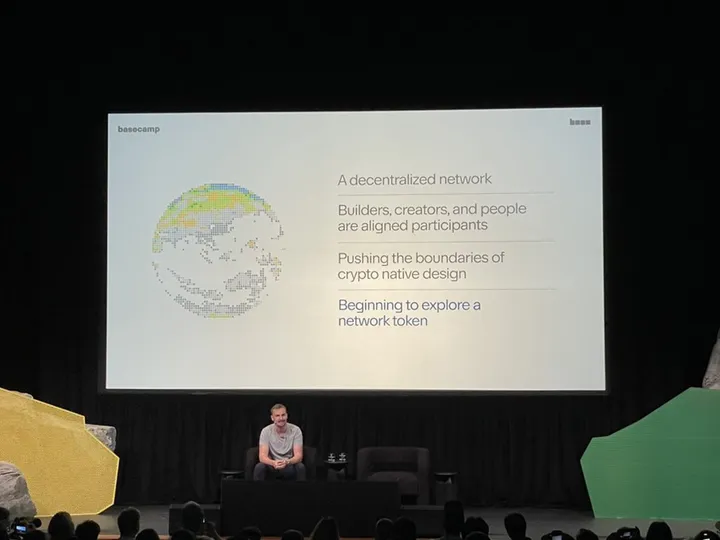

Jesse himself announced this year at BaseCamp that they were exploring a Base network token, with an October 2025 job posting for a “Token & governance research specialist,” indicating that something is cooking. Base’s number one espoused value is to “bring a million developers and a billion users onchain,” an axiom that very much points to a rewards/distribution token like WLD’s, rather than a typical DAO/Buyback token.

Jesse announces the possibility of $BASE at BaseCamp 2025

One could argue that Base doesn’t need any form of CAC token, as they have already had massive distribution with no token at all. To us, that just means Base doesn’t need to bootstrap from 0-1 with a token, but can instead accelerate from 1-N more easily with a CAC token. The actual structure would probably be similar to most tokens we see. Some form of Cayman Base foundation entity separate from Coinbase, with a token distributed to active users/builders via airdrop or ongoing “quest” rewards.

Brian Armstrong himself has explicitly stated that a token would be a “great tool for accelerating decentralization,” which again may be hinting at a CAC function to incentivize new users and a more progressive decentralized governance structure.

We’re exploring a Base network token.

It could be a great tool for accelerating decentralization and expanding creator and developer growth in the ecosystem.

To be clear, there are no definitive plans. We’re just updating our philosophy. As of now, we’re exploring it. https://t.co/BK3asbMpar

— Brian Armstrong (@brian_armstrong) September 15, 2025

The CAC framework, which has gone relatively overlooked by most of the CT-sphere, is a genuine innovation for how more established companies can leverage token economics.

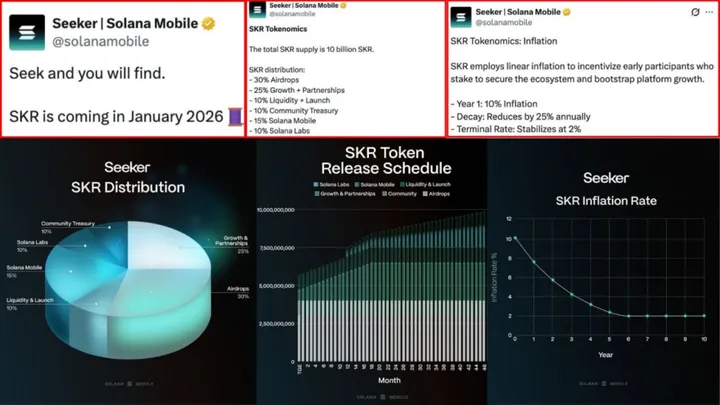

We’ve even seen Seeker on Solana follow a similar path laid out by the CAC framework model:

Seek and you will find.

SKR is coming in January 2026 🧵 pic.twitter.com/cwtlp8G8Zf

— Seeker | Solana Mobile (@solanamobile) December 3, 2025

Unlike previous eras of “utility tokens” that promise future value or DeFi tokens that dress speculation as voting rights, CAC tokens are more transparent in their use case as “signup bonuses” that fund distribution. The question, thus, as always, remains one of company execution, but the trajectory is quite clear. As our regulatory frameworks continue to mature under Paul Atkins, and if Worldcoin’s model proves durable (barring no country bans like the recent one in Thailand), then CAC tokens could be a better distribution strategy for corporations going forward, enabling faster scale.

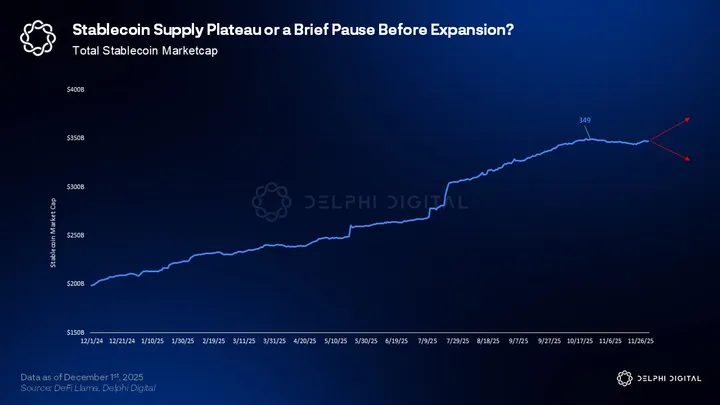

Stablecoins: From Market Primitive to Global Financial Infrastructure

We briefly touched on stablecoins earlier, but a section dedicated to their meteoric rise and promising year ahead makes the most sense to us.

Stablecoins have become one of the clearest expressions of institutionalization across the entire crypto market. The takeaway for 2026 is simple: Stablecoins are no longer just used for trading pairs and exchange liquidity, but instead are quickly becoming a core component of the plumbing of global dollar & treasury markets.

This institutional shift shows up in 4 ways that reinforce each other.

- Treasury Absorption: Stablecoins are turning into predictable buyers of US Treasury bills, pulling the asset class deeper into digital circulation.

- Global Yield: Treasury-backed reserve model is creating another global distribution channel for US dollar yield, similar to Eurodollars

- Geopolitical Pushback: The rise of portable, yield-bearing dollar tokens is triggering geopolitical pushback, especially in countries where capital controls or fragile currencies make this kind of monetary leakage hard to tolerate.

- Payment Rails: Stablecoins are becoming a settlement rail competitive with card networks and fintech processors, enabling a new wave of neobanks built around tokenized dollars.

1. Treasury Absorption Becomes the Anchor Use Case

Stablecoins have long been treated as a thermometer for crypto liquidity. Looking forward, they will begin to operate more like part of the financial system plumbing. With regulated issuers scaling up and tokenized money market funds gaining traction, stablecoins are no longer passive holders of reserves. They are turning into a structural buyer of short-term Treasuries.

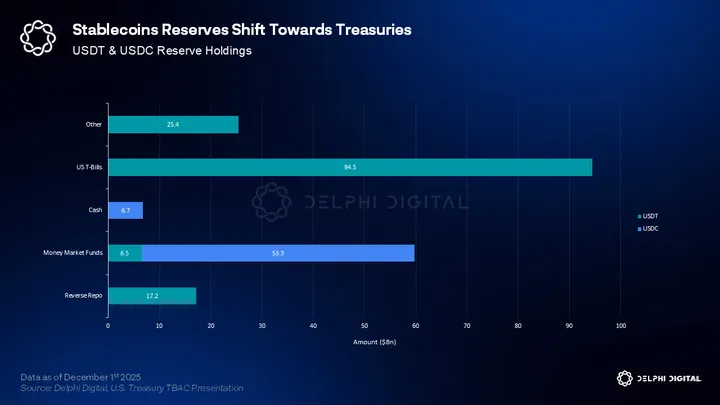

This modest shift began during 2023 and 2024. Stablecoin issuers once held large cash buffers and substantial bank deposits. However, that model broke down after the regional banking stress and regulatory pressure on custodial risk and the industry pivoted toward a pure Treasury standard. By early 2025, the reserves behind USDT and USDC were dominated by T-bills, reverse repos and government-only money market funds.

By August 2025, Tether reported about 66% of its reserve base in Treasury bills, totaling roughly $94.5 billion dollars. Circle placed more than 80% of USDC reserves in a BlackRock-managed government-only fund, holding $53.3 billion dollars in short-duration T-bills and repos. Across the market, more than $120 billion dollars of stablecoin reserves are now tied directly to US government debt. This already puts issuers ahead of many sovereign reserve managers.

The implications for 2026 are significant.

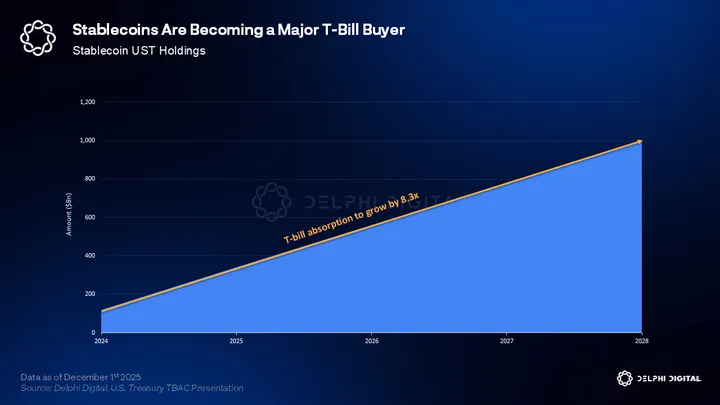

Stablecoins are moving from a crypto-specific liquidity gauge to a meaningful component of the Treasury funding ecosystem. As the supply of dollar stablecoins grows, so does the mechanical demand for new Treasury issuance. This creates a feedback loop between digital dollar adoption and fiscal capacity.

The US Treasury projects that stablecoin T-bill holdings could rise from about $120 billion dollars in 2024 to $1 trillion dollars by 2028. That is an 8.3x increase over 4 years. Even if adoption tracks the low end of this forecast, 2026 becomes a transitional year where stablecoins are no longer a rounding error in funding markets, but rather a visible, predictable buyer base.

This shift also alters how liquidity shocks propagate. In previous cycles, a drop in crypto activity led to a contraction in stablecoins, which amplified stress across exchanges and funding markets. The new reserve structure changes the transmission. Stablecoins can now absorb liquidity through Treasury bills and recycle it back into markets as tokens are minted or redeemed.

As stablecoins gain share as a preferred cash rail, capital is likely to migrate from bank deposits to tokenized money backed by government debt. The more users trust stablecoins to store value and settle payments, the stronger this Treasury demand channel becomes.

The Near-Term Risk … A Temporary Supply Contraction?

One caveat for 2026 is that stablecoin supply may not rise in a straight line. After 2 years of strong expansion, stablecoin growth rates have begun to flatten and a pullback is possible.

The drivers are straightforward: Front end yields will move lower as the Fed continues to cut, trading activity may cool after a volatile 2025, redemptions tend to pick up when cash becomes more attractive in traditional savings products and T-bill roll yields for issuers will drift down as coupons reset.

However, none of this breaks the structural story. Stablecoins are now plugged directly into real funding markets, which means their supply responds to shifts in front end rates and cash demand.

Our view is that a contraction in this environment is mechanical rather than a sign of stress. Short term supply can wiggle as macro conditions shift, though the long term slope remains intact. Stablecoins are still on a path toward deeper Treasury absorption, wider distribution and a larger share of global dollar flows.

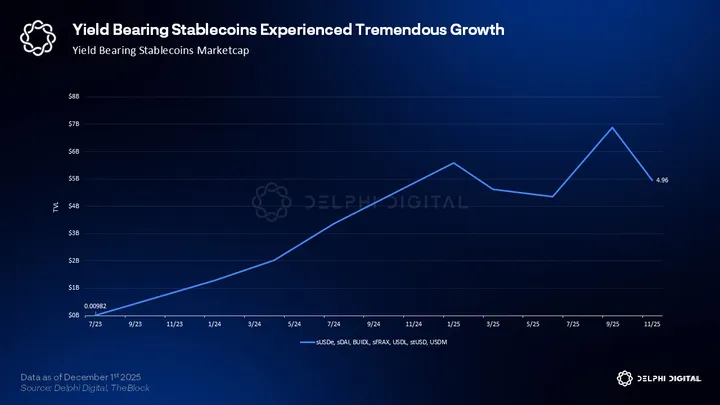

2. The Globalization of US Yield via Stablecoins

Stablecoins began as a way to move dollars quickly. In 2026 and beyond, they will evolve into a way to earn dollars globally.

Once issuers fully adopted short term Treasuries as their reserve backbone, the natural next step was to package that yield into tokenized products that anyone can hold. A parallel distribution channel for US yield is emerging outside the banking system.

The momentum is strongest in yield bearing stablecoins. They deliver the characteristics that made US Treasuries the world’s preferred savings asset, only without the paperwork, custody requirements, or local banking frictions. In regions with capital controls or limited access to dollar instruments, the shift is even more powerful. Stablecoins open a route to US yield that is not mediated by domestic banks or political constraints.