Current State of the NFT Market

It’s been a wild ride for NFTs.

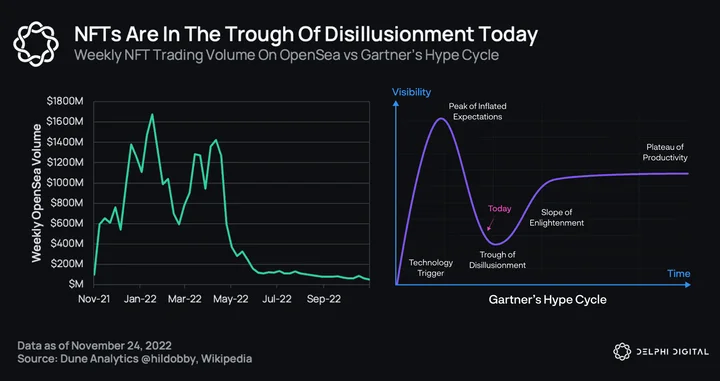

When we map NFT trading volumes on OpenSea with Gartner’s Hype Cycle — which represents the maturity and adoption of new technologies in solving real business problems — we can infer that NFTs hit the peak of inflated expectations from late 2021 to early 2022.

Since then, transaction volume and attention have been down only. Cobie describes NFTs as just “altcoins with pictures.” We are in the trough of disillusionment. The only way forward is to build our way out, finding real-world use cases for the technology. Only then will we see mainstream adoption really take off.

I’m convinced we will get there. NFTs are inherently interesting to more people because they lie at the intersection of technology, art, culture, and entertainment. They have the power to be the trojan horse that onboards the next big wave of people into crypto.

Reality vs. Expectations

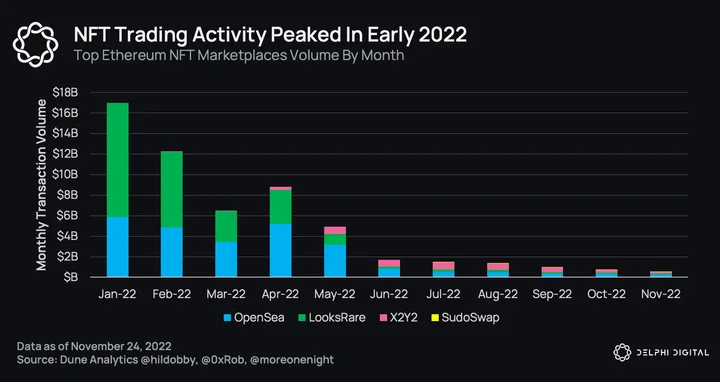

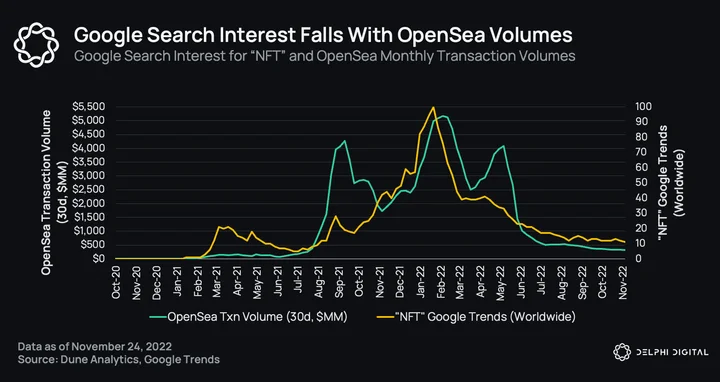

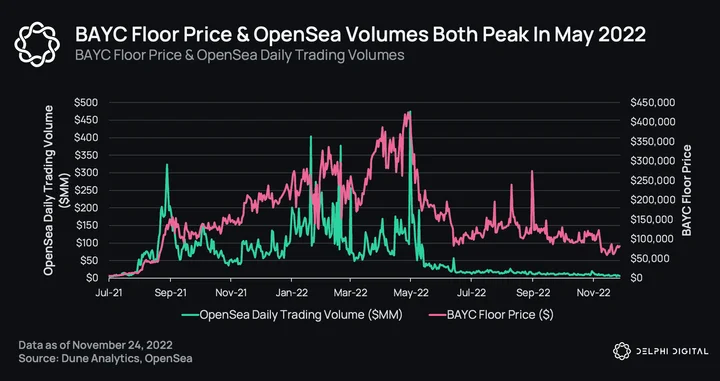

While it’s easy to get caught up in the future of what this space could look like, we must also recognize where things stand today. The reality is that NFT trading activity peaked early this year and has since succumbed to the same pressures weighing on the broader crypto market. NFT trading volumes are down across the board, but the last few months have been particularly depressed; November was the lowest month for NFT marketplace volumes since June 2021.

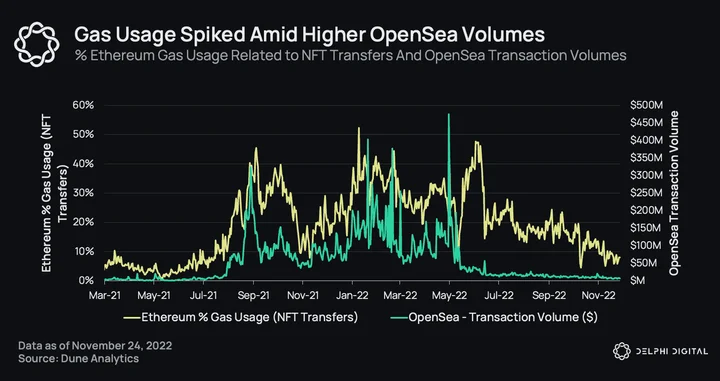

As NFTs took the world by storm last year, on-chain activity on Ethereum also rose considerably. More on-chain activity meant more demand for block space, and “gas wars” for popular NFT drops often resulted in sharp spikes in transaction fees. At a certain point, periods of high congestion actually pushed transaction fees above the sale price of many less-expensive NFT collections. This priced out many potential participants, some of whom were new entrants with little-to-no prior Web3 experience.

Low-cost transactions are critical for mainstream adoption. The decline in on-chain transaction activity and increased adoption of L2 solutions helped reign in average transaction fees. But even that hasn’t been enough to reverse the downtrend in NFT volumes, which means high fees weren’t the only culprit. Several months of bullish price action and “JPEG flipping” turned into buyer exhaustion as the novelty of new NFT projects started fading away.

There have been a lot of inspiring projects that have built great communities over the last 12 months. But generally speaking, we saw an acceleration in copycat projects and half-baked drops that caused supply to outpace new demand. As a result, prices for most NFT collections have trended lower, hitting holders with the double whammy of lower ETH-denominated prices as the price of ETH itself tumbled.

NFTs, like the rest of crypto, are subject to strong bouts of momentum and reflexive price action. For example, we can see that total trading volume on OpenSea peaked around the same time as floor prices for BAYC, as buyer demand started to show signs of exhaustion.

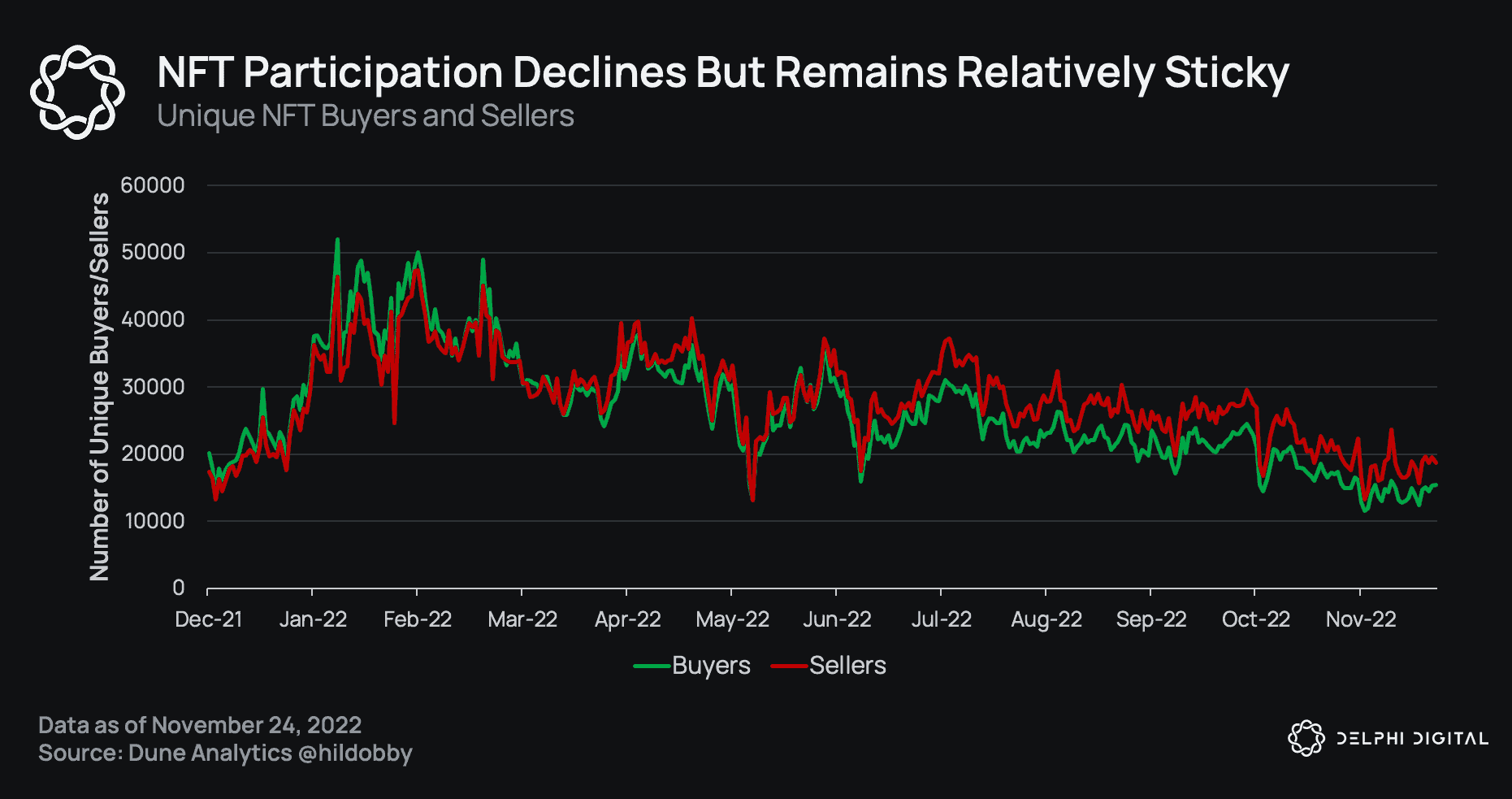

Despite the market drawdown, NFTs are still wildly popular compared to where they were 18 months ago. The average number of unique NFT buyers and sellers has declined from prior highs, but many participants are still active in the NFT market.

What’s amazing is we’ve only seen the tip of the iceberg when it comes to experimentation in this space. As more creators, brands, and communities develop their Web3 strategies, NFTs will likely capture even more mindshare.

Let’s dive into the most significant themes in the year ahead for NFTs (ex-gaming).

Five Big NFT Themes for Next Year

Theme #1: Cambrian Explosion for NFT Finance

When an NFT is minted, it gains “superpowers” — it can be bought, sold, and transferred. An economy forms around it. Like a seedling in the soil, the economy can flourish with the right tools. Greater financialization unlocks a new level of utility for NFTs. It brings new participants into the space (market markets, lenders, etc.) which are necessary for NFTs to truly become an established asset class.

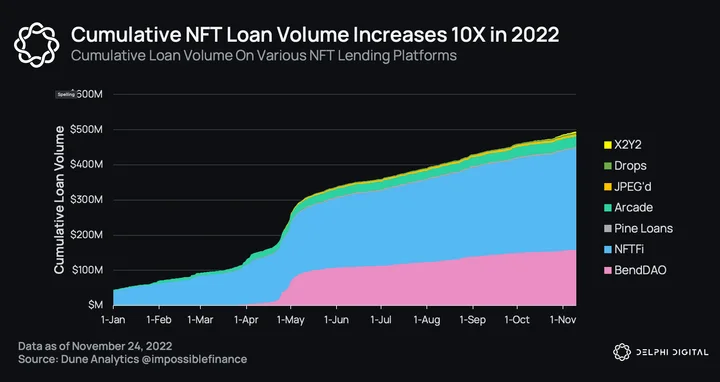

We will look back at 2022 as the year the foundation was laid for NFT finance to take off. From January to November, the cumulative volume of loans taken out using NFTs as collateral more than 10x’d, hitting >$500M. The upward trajectory shows no signs of stopping, even when considering the bear market. Borrow/lend is the basic financial utility that lubricates an economy, similar to how AAVE is a core pillar of DeFi.

NFTfi and BendDAO account for 90% of NFT loan volumes. They exemplify the two different lending models today. NFTfi follows a peer-to-peer lending model with a single borrower and lender. Here, the counterparties are known and the terms are transparent. On the other hand, BendDAO is a peer-to-pool protocol where the borrower secures a loan from a liquidity pool instead of an individual lender. Peer-to-pool lending is a newer and yet-to-be-proven concept that introduces additional risks. However, it is highly alluring because of the potential efficiency gains and instant liquidity.

For a deeper dive into NFT lending, refer to our report NFT Lending: A rising Opportunity When NFTs Meet DeFi.

Expectations for 2023 and Beyond

There will be an NFT-Fi summer at some point, similar to the DeFi summer of 2020. In the coming weeks and months, many interesting financial products centered around NFTs will be launched. Several will likely use their own native token to bootstrap initial users and incentivize liquidity providers. This could draw in capital flows from DeFi players who may have little direct interest in NFTs but are lured in by potential profits and yields.

It is also worth noting that NFTs went through an entire cycle without any leverage primitives, which is quite a feat. Leverage is a “hell of a drug,” and something the NFT ecosystem has yet to truly experience. When leverage tools are made easily available to users, we could see sparks fly.

NFT derivatives (options and perpetuals) launch. Imagine having direct exposure to the Bored Ape Yacht Club without having to fork over 60 ETH to buy an NFT. This will enable many more people to participate in the economy. Conversely, the ability to hedge NFT exposure will make it less risky for investors to own NFT assets and bring large, sophisticated players in.

Derivatives introduce greater leverage into the system and can dramatically alter the price action of NFT collections. There will be greater volatility, liquidity, and more efficient markets. The main challenge is finding the right protocol design so that these derivatives have low spreads and attract actual usage. Examples:

-

NFTPerp is a decentralized exchange for NFT perpetual futures that covers 9 NFT collections, including Azuki, Doodles, and Bored Ape Yacht Club. It is currently in private beta.

-

Hook Protocol is an NFT-native options protocol that allows users to buy and sell call options on NFT collections, including Otherdeeds and CryptoPunks.

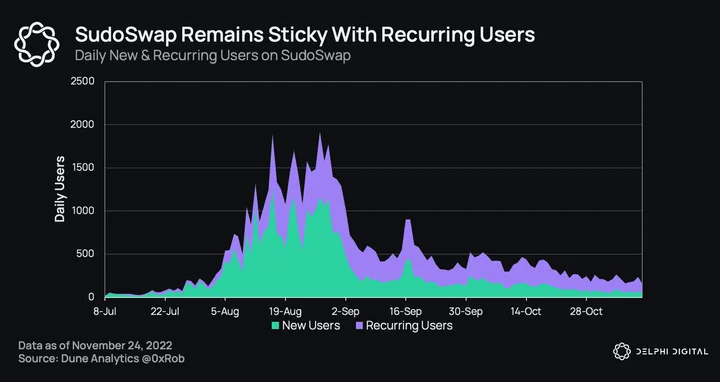

NFT AMMs gain traction. Sudoswap is the NFT equivalent of the Uniswap moment for ERC-20s. Sudoswap is an automated market maker (AMM) for NFTs that enables instant liquidity. User retention has been good (recurring users as a % of daily users) even as NFT transaction volumes fell. AMMs are well-suited for “fungible” NFTs, such as in-game items or membership passes where most items are similar. As GameFi takes off in the coming years, I expect greater volume to flow through AMMs.

In an interesting twist, Uniswap itself has launched an NFT aggregator feature that pulls marketplace listings from seven top marketplaces including OpenSea and LooksRare. This was expected after its acquisition of Genie in June. Using its new Universal Router smart contract, it claims to be more gas-efficient than other marketplace aggregators and enables complex swaps in a single transaction. Uniswap sees NFTs as another format for value in the growing digital economy and not separable from ERC-20s.

NFT lending version 2.0. Capital efficiency is the elusive beast everyone is chasing. Peer-to-pool protocols with new, experimental designs will go live. For example, Astaria, by ex-SushiSwap CTO Joseph DeLong, introduces a 3rd actor (strategist) to determine the best loan terms for an NFT. Loan aggregators like MetaStreet will also see increased usage as they make it easier for lenders to participate while managing their risk profiles.

NFT pricing gets solved. The pricing of NFTs has been opaque and unreliable. This is a critical piece of NFT finance infrastructure that is missing — we need a robust pricing feed that is difficult to manipulate while providing granular data beyond floor prices. New pricing protocols use machine learning algorithms (e.g., Upshot) to provide accurate, low-latency price feeds. These will be used more widely as we become comfortable with their accuracy.

Theme #2: The Great Unbundling of NFT Marketplaces

“The marketplace that wins is the marketplace that figures out how to make their buyers and sellers meaningfully happier than any substitute.” – Sarah Tavel

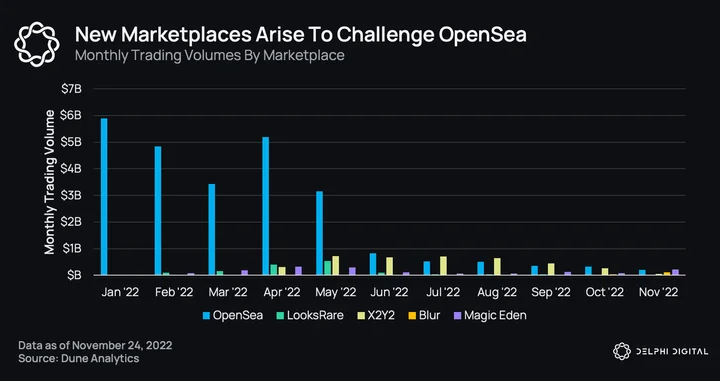

NFT marketplaces are the crown jewels of the industry. They are highly scalable cash flow businesses that are not dependent on the success of any individual NFT project. Plus, they operate in a growth market that could expand to trillions of dollars one day. Despite the bear market, OpenSea (OS) still generated >$500M in revenue this year (and over $1.8B in total fees), so it’s no wonder that many challengers have arisen.

Heading into 2021, OpenSea was one of the only NFT marketplaces available, benefiting from relatively little competition. As NFTs gained popularity, other marketplaces started to emerge, but OpenSea already had a big head start in terms of supply (NFTs listed) and demand (OpenSea was the default marketplace if you wanted to buy and sell NFTs).

In January, >90% of NFT trading volume passed through OpenSea. Today, that dominance has shrunk significantly, with several serious competitors emerging: LooksRare, X2Y2, Magic Eden, and Blur. Fee competition is real. OpenSea has the highest fees and full royalties, while its competitors have lower (or zero) marketplace fees and/or optional royalties. LooksRare and X2Y2 use native tokens to incentivize listings and trades, and Blur is launching its token soon. A steep drop in NFT trading volumes has exacerbated the hyper-competitive dynamics as marketplaces compete for a smaller pie in the short-term.

(For more on NFT marketplaces, refer to our reports Looksrare vs. X2Y2 : A Story of Incentivized NFT Marketplaces and A Primer on NFT Wash Trading)

Marketplace Business Models

Marketplaces are in the business of matching supply and demand for certain products and services. Exchanges like Coinbase and Kraken create markets for buying and selling crypto assets. Uber and Lyft created markets to connect drivers and users who need rides. Airbnb created a market for travelers (demand) to connect with homeowners (suppliers) to rent underutilized space in their homes. But not all marketplaces are created equal.

Bill Gurley is one of the top thinkers in understanding marketplace opportunities. In his seminal post, “All Markets Are Not Created Equal: 10 Factors To Consider When Evaluating Digital Marketplaces,” he outlines ten key characteristics for evaluating marketplace opportunities. Among them is the concept of high fragmentation, which many consider one of the most important factors in determining the potential success of marketplace businesses.

“High buyer and supplier fragmentation is a huge positive for an online marketplace. Likewise, a concentrated supplier (or purchaser) base greatly diminishes the likelihood of a successful online marketplace.”

Building on the work of Sarah Tavel, David Phelps also examined some of the key characteristics that help determine the success of different marketplaces models. Phelps cites several examples to illustrate his conclusion that non-fungible supply and demand are foundational ingredients for winner-takes-all marketplaces.

Content is an example of non-fungible supply. Each incremental user that joins Twitter or TikTok creates more value for existing users because users on these platforms are not interchangeable. They provide their own unique content (non-fungible supply) and sometimes content that you can’t find on other social platforms. Social media platforms also benefit from non-fungible demand; each Twitter user has unique preferences and interests because not everyone likes the same content.

Airbnb is another example Phelps cites as a marketplace that benefits from non-fungibility. Each additional unit of supply (homes) increases the value and “happiness” of its users because it provides them with more options that cater to their unique tastes. Compare that with Uber, where the value of the 10,000th driver to a user is far more negligible.

Marketplaces that cater to fungible supply and demand eventually see diminishing returns from each new user, because each incremental increase in supply is interchangeable with the last.

Exchanges, for example, compete in a market characterized by fungible supply and demand dynamics. “It doesn’t matter who you’re trading with, just that there is someone to complete the transaction.” Similarly, each new driver that joins Uber is interchangeable with all the other drivers already there.

There’s no denying that these companies have built huge businesses, but they aren’t winner-takes-all marketplaces. They operate in markets where there isn’t a ton of differentiation in the services they offer, nor is there a lot of variation in user preferences for those services.

When the supply of the service provided is fungible, and user preferences are homogeneous (i.e., users want a ride from A to B), users become more incentivized to care about price. “Homogeneity of buyer need kills the possibilities for a winner-takes-all marketplace.”

These concepts are prescient for analyzing any internet marketplace, including those for NFTs. For starters, NFT marketplaces benefit from a high degree of buyer and supplier fragmentation.

Aggregating supply can help bootstrap a new marketplace, but to build a strong moat – and true network effects – it has to aggregate demand, which is a harder challenge. OpenSea initially captured most of the market share because it aggregated both supply and demand.

OpenSea also benefited from the non-fungible supply (pun intended). Many NFT collections have a wide spectrum of characteristics between individual NFTs. While some carry similar attributes, there’s often a lot of variation within and between different collections. The demand side may be less diverse, but it includes non-fungible buyers which are arguably more unique in their individual preferences than the average trader on fungible-token exchanges.

However, we’ve seen a reduction in switching costs between NFT marketplaces because non-fungible tokens can be listed on multiple exchanges (similar to the same house being listed on Airbnb and VRBO). Going back to the Airbnb example, while it’s the dominant player in its vertical, it isn’t isolated from competition because it operates in a market where switching costs aren’t that prohibitive (another measure of fungibility). VRBO may not have as many options to choose from, but if it offers different options than those on Airbnb, users are incentivized to check both marketplaces before booking their perfect vacation.

Since non-fungible supply is becoming less of a moat, OpenSea has started to compete on price, because users are more incentivized to care about transaction costs if they can buy/sell the same NFTs on other marketplaces. One manifestation of this is the trend towards optional royalties, akin to the race to the bottom in fees for competitive marketplaces.

The rise in competition among alternative marketplaces also puts pressure on OpenSea’s ability to be the ultimate aggregator of demand for NFT buyers and sellers, further limiting its ability to operate a true winner-takes-all marketplace. Again, we revisit Sarah Tavel’s intro quote (emphasis our own):

“The marketplace that wins is the marketplace that figures out how to make their buyers and sellers meaningfully happier than any substitute.”

The key here is how to make buyers and sellers happier than any substitute. That is why, as in other industries, the race to the bottom in fees on NFT marketplaces will likely continue because it creates more happiness for buyers and sellers.

Putting aside the debate as to whether this trend is right or wrong – and more specifically, the adverse impact it has on creators – the history of marketplaces offers a lot of insight into the possible fate of their crypto counterparts.

Expectations for 2023 and Beyond

If we study the history of successful marketplaces (Craigslist, eBay, Amazon), we see a similar pattern emerge — a large incumbent with a bundled platform is challenged by startups with an unbundled product that customers prefer. Sometimes, they grow even larger than the original platform they disrupted (e.g., Zillow now generates 10x more revenue than Craigslist).

OpenSea and its main competitors are large marketplace platforms covering all NFTs. We will see the landscape for NFT marketplaces change significantly. A great unbundling is about to happen.

Vertical marketplaces will gain prominence. We’ve seen the rise of specialized marketplaces in nearly every other industry where internet marketplaces are present. We know that the rise of internet marketplaces unlocks economic value by matching those who own or produce goods with large cohorts of buyers specifically interested in those types of goods.

I am closely watching marketplaces focusing on NFT verticals such as PFPs, art, virtual land, music, and fashion. The buyer’s journey for an art collector is very different from that of a PFP trader — an art collector wants to know the history and meaning of the work and the artist’s brand and be able to admire the aesthetics in detail. In contrast, the PFP trader looks at floor price changes, rarities, and the strength of the community.

(For a deep dive into generative art, refer to our report Generative Art Takes Off – Is it the Defining Art Movement of the Century?)

Vertical marketplaces enable a better user experience and business models tailored to their specific verticals. For example, SuperRare recently sold out its inaugural membership pass (RarePass), which gives members a new 1/1 piece of artwork from its stable of top artists every month. This is difficult for platforms like OpenSea because they are pulled in many different directions and cannot please all their customers.

The gross merchandise value (GMV) of these vertical marketplaces is tiny compared to OpenSea today, so they’re easy to dismiss. But we must consider that they are still in the early stages of growth, optimizing for customer happiness over GMV. At the right time, they could reach an inflection point where the product is superior enough that the market starts tipping in their direction. Some tipping points could include:

-

Inclusion of unique features not available on OpenSea, such as sector-specific analytics and insights.

-

Curation of strong vertical communities, which remain sticky because of the social bonds formed.

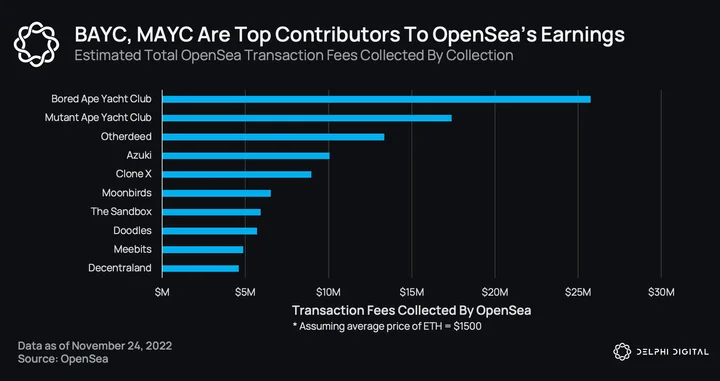

More NFT teams will opt to launch project-owned, white-labeled marketplaces. The Bored Ape ecosystem collections (BAYC, MAYC, Otherdeeds) have generated over $50M in transaction fees for OpenSea. Imagine if BAYC had its own marketplace and could capture all of those fees. The fees would go back into building out their vision and bringing value to NFT holders instead of being extracted by a middleman. This is a key unlock, because NFT creators (artists, brands, talent, etc.) can capture more of the economic value they create and share that with their community of supporters (NFT holders).

In the past, it was a heavy lift for NFT teams to launch their own marketplaces. Now, providers like Rarible and Zora allow others to build on their existing infrastructure, making it much more manageable. Reservoir is another NFT infrastructure piece that we believe will be very important in the coming years. It aggregates liquidity across major marketplaces and allows others to leverage their open and on-chain orderbook via APIs.

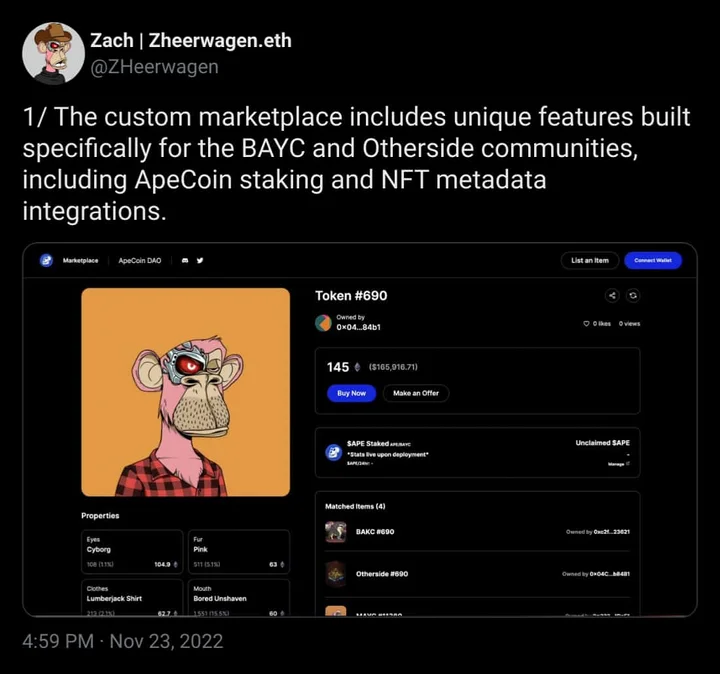

With a private marketplace, NFT teams have better control over their economy. They can set appropriate fees and royalties, enable trading in their native currency, and provide discounts or benefits to community members. For example, ApeCoin DAO and Snag Solutions have partnered to launch a marketplace that enables APE to be used for trading, has lower fees than OpenSea, and will support the Bored Ape and Otherside economies.

Thematic marketplace aggregators will bring order to the chaos. Aggregation in Web3 is extremely powerful and scalable. The composability and on-chain provenance enabled by the blockchain reduces friction typically encountered by Web2 aggregators (legal licenses, authenticity checks). Gem and Genie have shown how aggregators can grow very quickly.

The fragmentation brought about by new vertical and private marketplaces will be mitigated by thematic marketplace aggregators, who will emerge to match buyers and sellers for specific types of NFTs. For example, a gaming marketplace aggregator that pulls listings from all the top gaming marketplaces becomes very interesting once gaming is more widely adopted and trading, lending, and borrowing in-game assets are more commonplace.

OpenSea – Fate or Fortune?

The trend towards vertical marketplaces doesn’t mean OpenSea is doomed. An incumbent can still run a successful business model despite increased competition. Craigslist is still a big player in the market for classified ads because it benefits from tremendous supply, the scale of which is difficult to replicate.

OpenSea seems to be doubling down on its own supply-side scale, which makes sense, given multi-chain support is one of its current competitive advantages (similar to other centralized exchanges that offer cross-chain compatibility).

OpenSea is also one of the most heavily searched platforms in all of crypto (averaging ~30M visitors per month, according to SimilarWeb). Many smaller creators and project teams are still incentivized to list on OpenSea because that’s where most of the demand (buyers) is. Creators or brands with large existing distribution channels may choose to launch on other vertical marketplaces or create their own marketplaces, but those with limited reach are more incentivized to leverage OpenSea’s distribution to drive awareness and discoverability.

This brand recognition is another advantage – anyone somewhat active in NFTs has used or at least knows of OpenSea. Leaning into this, if they can position themselves as the most trusted and secure platform for buying, selling, and minting NFTs, they may be able to fend off rivals who don’t have the same pedigree. Offering a secure experience will become increasingly important as more “non-crypto” users enter this space. Many will turn to a platform they can trust over one that is less established, even if the alternative offers a better user experience.

TL;DR: The trend towards vertical marketplaces doesn’t mean OpenSea is going away, but it does present opportunities for more specialized marketplaces to thrive – and possibly even surpass – the industry incumbent.

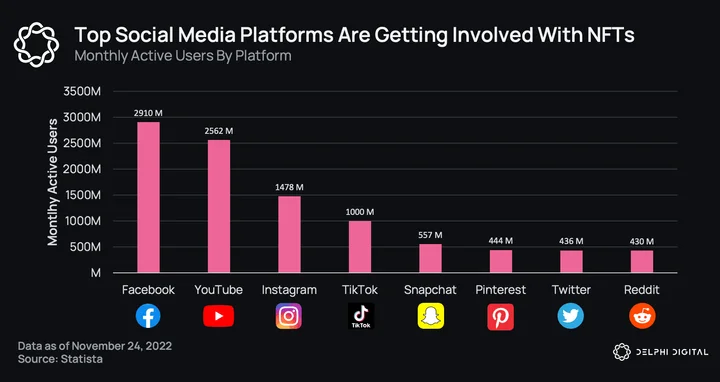

Theme #3: NFTs Go Mainstream: Big Tech and Brands

Strong tailwinds will accelerate the mainstream usage and adoption of NFTs in 2023. I want to highlight two of these trends.

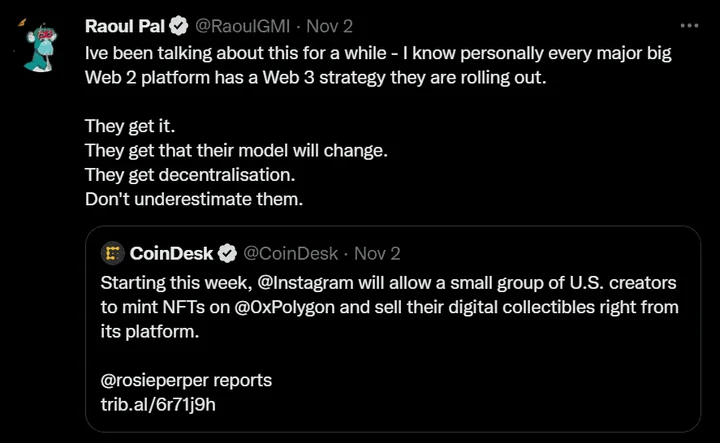

Big Tech Is Embracing NFTs

Instagram enables creators to mint, buy, and sell NFTs on Polygon while also supporting NFTs on Solana, Ethereum, and Flow. Reddit launched its collectible avatars with over 3M crypto wallets created. YouTube includes NFTs in new creator tools. Apple allows in-app minting, buying, and selling of NFTs — although there is controversy over its intentions with its blocking of Coinbase Wallet’s NFT transfer feature unless 30% of gas fees were paid to it.

Web2 companies own the distribution channels that give them access to billions of users today. The top social media platforms have hundreds of millions to billions of monthly active users (MAUs). By leveraging their expertise in building great UX products and integrating with familiar payment systems like Apple Pay, these platforms can abstract away a lot of the friction in onboarding new people onto NFTs. Many are already developing their own NFT initiatives, some of which are likely to launch in 2023.

Crypto’s mainstream moment is close at hand. Never before in our history have there been hundreds of millions of potential users interfacing with blockchains. Many people’s first step into crypto and NFTs will be through these Web2 platforms — and some may not even realize they own NFTs.

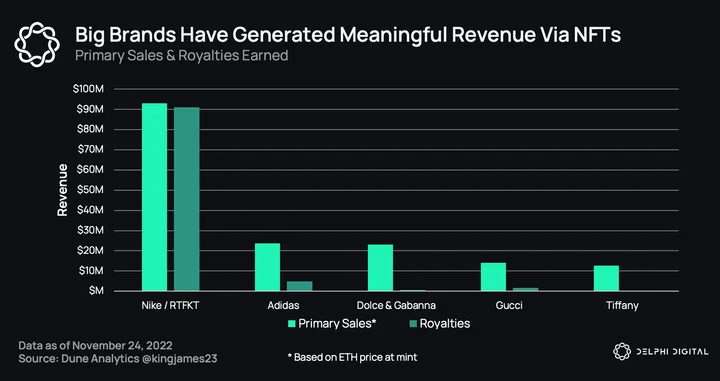

Big Brands Are Embracing NFTs

Several big brands have generated meaningful revenue from NFTs, including Nike, Adidas, Gucci, D&G, Tiffany & Co., and Time. Tiffany & Co. sold $12M of NFTs in August, entitling owners to claim custom-made CryptoPunk-inspired pendants. The Web3 audience is affluent and willing to spend, and the success of these trailblazers is drawing attention.

Most large consumer companies are already thinking about opportunities in the metaverse. They’re starting to take Web3 seriously because it offers them a way to build more direct relationships with loyal patrons while creating new ways for people to engage with and experience their brands.

Customer acquisition costs for many brands have also increased dramatically in recent years. Increased regulatory scrutiny on targeted advertising practices, changes in privacy settings, and the inherent limitations in data collection for social commerce are pushing more companies to invest in DTC strategies. Social media advertising is a huge market for acquiring customers, but brands are actively trying to push customer traffic to their own sites, which allows them to collect first-party data so they can market to these customers (purchases through social media apps limit their ability to do this).

Every brand is different, but many have overlapping goals that make Web3 enticing. Some see an opportunity to sell digital items to their customers, while others are looking for ways to foster more engagement with their brand’s community (including building virtual spaces for their communities to gather). As social channels become more saturated, brands will need to find better ways to acquire and retain customers. Web3 may be the next battleground, as it’s still a green field ripe for growth.

We’re starting to see forward-thinking brands enter the fray, which will eventually bring a fresh segment of future Web3 participants with them. Not every brand will get this right, and many brands may not be able to create a sustainable Web3 strategy yet. But those that understand the power of community, and have the willingness to lean into the benefits Web3 has to offer, are the brands that have the biggest opportunity to create strong moats to thrive in this new era.

Expectations for 2023 and Beyond

More brands and big tech companies will integrate NFTs into their business models in meaningful ways, resulting in a flurry of creative use cases for NFTs. Starbucks is one example of a large multinational that has integrated NFTs with its loyalty program, allowing members to earn or purchase limited-edition stamps that unlock additional benefits.

Dynamic NFTs, which change according to real-world events or user actions, also have a lot of potential to drive brand engagement. The big question is who will be the first to achieve product-market fit? And who will write the playbook for more brands and companies to follow?

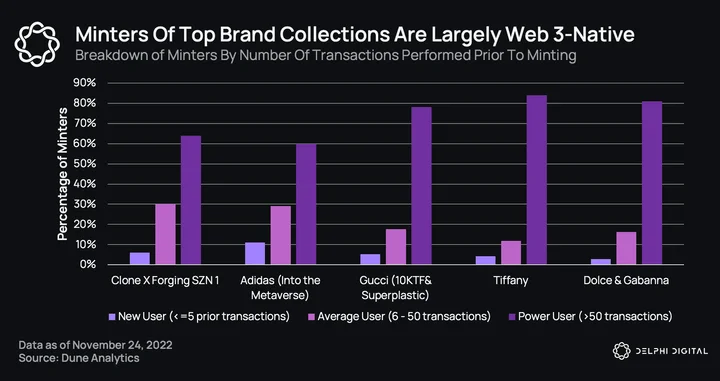

The Web3 creator playbook comes to life as new users surge. Minters of NFTs launched by big brands have mostly been Web3-natives and power users so far. This will change as more new participants enter. Talented creators can monetize through NFTs, bootstrapping an initial audience of fans. This kickstarts a virtuous cycle of content creation, audience growth, and business growth. The creator economy is going to thrive.

(An example: Aku is one of the first web3-native media companies funded via NFT sales. For more details, refer to our report Aku, The Moon God & The New Age of Web3 Media)

M&A activity will heat up. Large corporations convinced of the space’s potential will make strategic investments or acquisitions to gain a leg up against their competitors. A prime example is Nike’s acquisition of RTFKT in late 2020 — RTFKT has become its experimental Web3 playground while Nike’s core business operates as usual.

There will be consolidation within Web3, too. Yuga Labs acquired 10KTF and WENEW, adding them to their ecosystem this month. Could Web3 companies that have shown traction, like VeeFriends, Azuki, Nouns or Art Blocks, be acquired? It’s not out of the question.

(For a deep dive into the Nouns ecosystem, refer to our report Nouns — Hyperscaling a Brand & Treasury From Zero)

Theme #4: NFTs — The New Social Tokens

As a concept, social tokens are compelling. For the first time in history, we have verifiably-scarce digital assets that can be tied to an individual’s (or community’s) reputation and success. Social tokens represent and govern how influencers and creators transfer value to their communities. They have the potential to remove rent-seeking intermediaries involved in the value transfer.

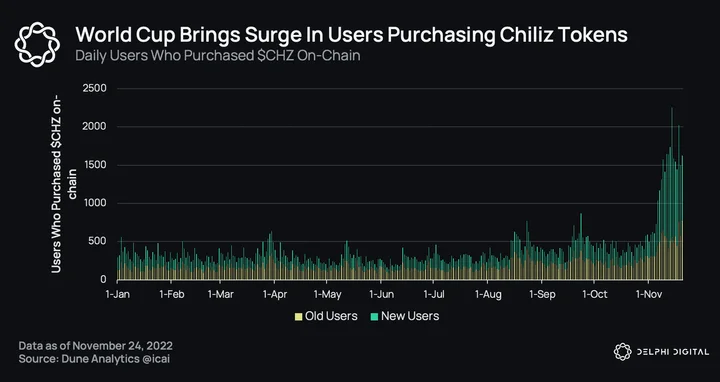

The ongoing World Cup highlights an example that has received much attention. Chiliz launched over 50 sports-related fan tokens (ERC-20s), partnering up with football giants such as Inter, Rome (ltaly), and Manchester City (UK). Token holders get discounts on merchandise and can vote on club decisions such as the jersey design. However, there have been valid concerns over their tokenomics. Only a small % of the fan tokens are available to the public, and the large majority are held by Chiliz and the teams.

Increasingly, social tokens are being launched as NFTs. A few examples this year include:

-

Steve Aoki launched his A0k1 credits in February. The NFTs can be used to upgrade passports to the A0k1verse. Passports provide fans with free merch, exclusive access to Aoki concerts, and the opportunity to create a song with Steve Aoki.

-

Cristiano Ronaldo worked with Binance to launch an NFT collection just before the World Cup, allowing him to better connect with his fans. There are several rarity tiers, with perks ranging from autographed Ronaldo merchandise to a personal message from the football star himself.

-

VaynerSports is a talent representation and brand agency for professional athletes in football, baseball, combat, and gaming. Founded by AJ Vaynerchuk, it launched a membership pass NFT that allows holders to meet VaynerSports athletes and win tickets to professional sporting events.

Expectations for 2023 and Beyond

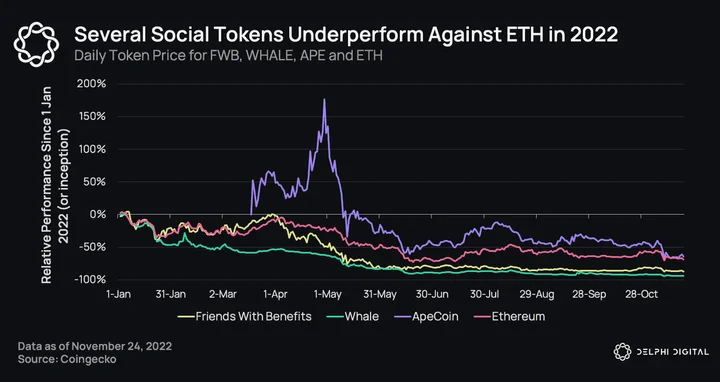

NFTs will be the preferred medium for social and fan tokens. While early social tokens started out as fungible tokens (e.g., Friends With Benefits, AC Milan, WHALE), we foresee that future social tokens will launch as NFTs rather than ERC-20s. NFTs can be tied to rich media like videos, music, and images, allowing them to accrue cultural and memetic value beyond financial value. NFTs are well-suited to be the primary assets used for social flexing and digital identity. They can also function as a membership pass for token-gated access. The design space and potential for gamification with NFTs are huge.

A huge wave of creators, celebrities, and sports brands will launch NFTs. This will be larger than anything we have seen thus far.

-

The technical infrastructure to support this is rapidly improving. No-code platforms, token-gating solutions, and tooling for dynamic NFTs are just a few things I’m excited about.

-

An increasing number of people, especially decision-makers, are being educated about the potential for NFTs to grow their brands and create new revenue streams.

Asia could be the place where social and fan tokens take off first. Fan culture in Asia is rabid, and fans are willing to financially support their favorite stars by purchasing large amounts of merchandise. K-pop is one obvious example. Merchandise and album sales are very significant revenue streams for K-pop entertainment agencies. There is a greater cultural acceptance of NFTs in Asia since property rights are often not as robust as in the US.

So far, only a tiny % of creators and influencers in the sports and entertainment industries have launched their own social tokens. This will change in the coming years.

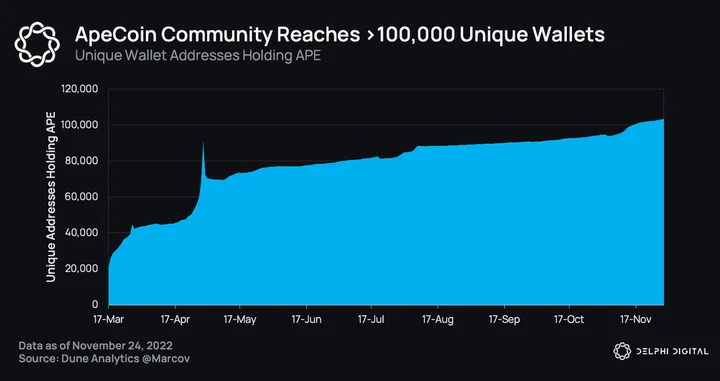

NFT projects will launch their own fungible tokens. Fungible tokens and NFTs complement one another when building an economy around people and brands. They enable the community to expand beyond the limited set of NFT owners. The clearest example is ApeCoin, launched to support and complement the Bored Ape economy. From an initial community of 20,000+ APE holders, it has expanded to 100,000+ unique wallets today. Watch out for Azuki, Moonbirds, and Clone X tokens in the future.

Native fungible tokens are the currencies that lubricate the ecosystem — a medium of exchange for value transfers. Community members who contribute significantly with their time and effort can be rewarded with tokens. Fungible tokens can also be used to purchase merchandise, mint future NFT drops, or as a gamification tool (stake your NFTs for tokens, earn tokens for completing tasks).

Importantly, greater emphasis should be placed on thoughtful approaches toward tokenomics. Simple stake-and-earn mechanisms are not meaningful. Tokens should be channeled towards those creating value, rewarding productive contributions with additional ownership.

A cautionary note: Social tokens are still in their infancy. Value capture remains a key problem. Tying ownership and profits back to a token involves legal challenges, as these tokens could be classified as securities and subject to stringent laws. Regulatory guidance around tokens and digital assets has been vague and will continue to be for a while.

Other headwinds include discoverability issues, since the social token landscape is quite fragmented and there is no aggregated platform for consumers to find out about tokens. There is also a lack of material, demand-driving utility. We believe that these are solvable challenges in time.

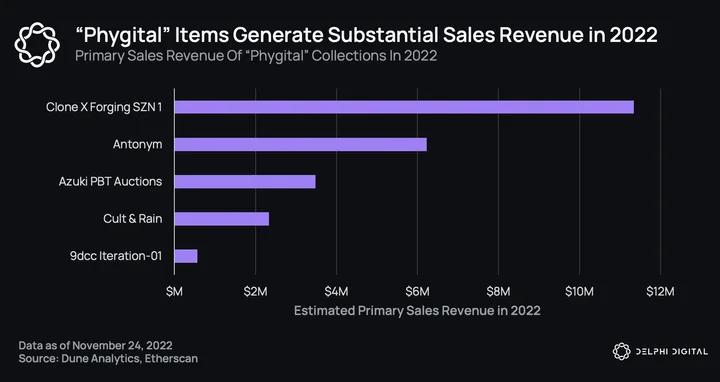

Theme #5: “Phygital” Brings Physical and Digital Together

The lines between our digital and physical worlds are blurring. Objects can now exist in the metaverse and the real world, linked through technology. NFTs are the bridge, functioning as an immutable representation of authenticity and ownership in both realms. They empower physical items with new utilities, such as unlocking token-gated benefits and unique AR experiences.

This year, RTFKT released a Nike AR hoodie that can be worn on Clone X avatars and entitles owners to claim the same physical hoodie. 9dcc, a luxury fashion house by gmoney, launched a collection of t-shirts with embedded NFC chips that enable the NFT to move together with the physical item. Azuki launched its physical-based token (PBT), using an open standard that ties physical items to an NFT.

These early phygital items have already generated millions in sales, indicating the latent demand for such goods. For more on “phygital” and digital fashion, refer to our deep dive report on Why the Future of Fashion is in the Metaverse.

Expectations for 2023 and Beyond

More physical items will be sold with accompanying NFTs. The technology that enables NFTs to be tied to physical items is not complex, and it will get cheaper and more intuitive. Brands will utilize this to create delightful customer experiences that complement their physical products.

Giving free NFTs that accompany purchases of physical items also allows brands to start building out their own on-chain social graphs, which they can then query, segment, and reward based on who’s engaging with their brand and products most. This is the first step in bringing more real-world items onto the blockchain.

High demand for digital artists and designers. Phygital opens up a new world of storytelling and experiences for physical items. The use of AR filters in fashion is a growing trend among the social media-addicted crowd today. Talented digital artists and designers are essential to creating great content.

Phygital gets a better name. If there’s one thing that unites the NFT community, we hate the term “phygital.” It’s an ugly word for a powerful concept, and many have called it by different names (gmoney calls it a “networked product”). I hope someone finds a better term we can all agree to use.

What Surprised Us This Year

Surprise #1: Creator Royalties Crash and Burn — New Business Models Needed

The ability for artists to earn royalties is a core value proposition for NFTs. It brings many artists and creators into the space. Royalties are a source of income that allows them to continue their creative work without the pressure of constantly selling new works to make ends meet. Royalties typically range from 2.5-10% of the sale price.

Yet, it appears that NFT royalties are trending toward zero. The slippery downward slope began with the launch of Sudoswap in July, a new marketplace that gives fees to liquidity providers but does not include a royalty feature. X2Y2 saw this as an opportunity, and shortly after made royalties optional. Weeks later, LooksRare and Magic Eden followed.

Few people are willing to pay royalties when there’s no incentive to. We observe a steep decline in trades that includes royalties (e.g., only 10-20% on Magic Eden) once royalties are made optional.

OpenSea remains steadfast in its support of creator royalties and is fighting back. It released a code snippet for NFT smart contracts that restricts the transfer function if it falls under OpenSea’s list of operators that do not support royalties. OS stated that it would only enforce royalties for NFT projects that include this code or similar enforcement tools.

The challenge is that there is no perfect way to enforce royalties on-chain in an open, permissionless system like Ethereum. All solutions involve tradeoffs in decentralization. Do you genuinely own your NFT if OpenSea dictates which addresses you cannot transfer your NFT to? A bad actor could one day decide to blacklist all addresses except for OS. It brings us back to the centralized, permissioned systems of Web2.

We are heading into an era where new business models for creators beyond royalties will be found. This could mean a tipping service. Creators could keep a stash of NFTs to be sold later on, or create a tiered membership system where those who pay royalties are entitled to additional benefits (I like this). Human ingenuity will light the path forward.

Surprise #2: The Rise and Fall of the Solana NFT Ecosystem

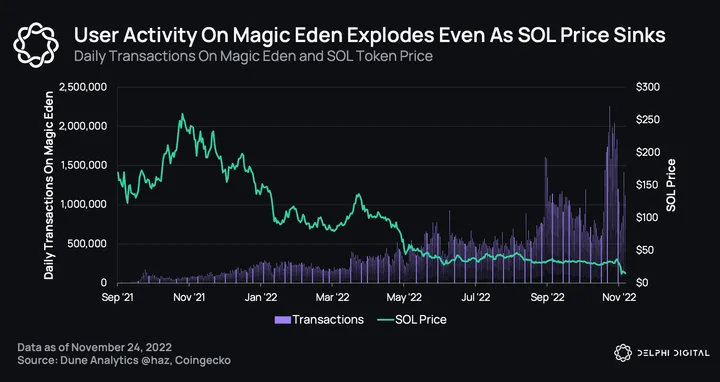

Solana NFTs took on a life of their own this year. The ecosystem expanded rapidly to become the 2nd largest NFT ecosystem, with approximately 1/6th of Ethereum’s trading volume. It evolved into a vibrant sub-culture that was quite different from Ethereum. Trading, PFPs, and community tribalism were focal points, fanned by vocal influencers like ShiLLin VilLLian and Frank.

This propelled Magic Eden (ME) into the spotlight. Previously viewed as a niche marketplace, ME cemented its position as the dominant NFT marketplace on Solana by focusing on communities and its launchpad. User activity on ME grew by several multiples through the year, with over 2M transactions on some days. ME was able to rake in significant revenue from transaction fees and expand rapidly. Today, it has expanded cross-chain to compete directly with OpenSea, showing that its ambitions are not limited to Solana.

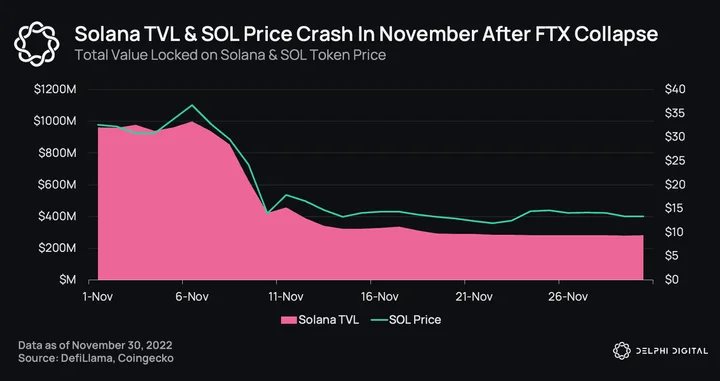

Unfortunately, meteoric rises are often accompanied by a fall. Solana faces an existential crisis with the collapse of FTX/Alameda and its founder Sam Bankman-Fried, two of its most prominent backers. The SOL price crashed by >50% in November, and much liquidity has since fled its ecosystem.

Since NFTs were denominated in SOL, this triggered panic among the Solana NFT community and team members. Several teams are considering moving their projects off Solana to another chain, including top projects such as DeGods and Solana Monkey Business. FTX/Alameda hold many SOL tokens which could be liquidated in bankruptcy, putting downward pressure on its price. This, together with the reputational hit from being associated with SBF, continues to be a significant overhang on the entire ecosystem.

Still, the Solana community remains resilient, and development announcements at the recent Breakpoint conference are promising. It remains to be seen if the Solana NFT ecosystem can pick itself back up in the coming year, but I’ll be watching.

Surprise #3: Music NFTs Remained Niche

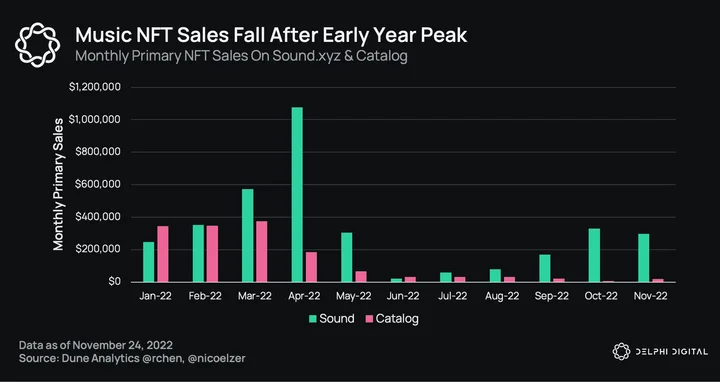

Earlier this year, we put out our thesis on music NFTs and how they will drive new revenue streams and engagement models that allow artists to build more successful and sustainable careers. We viewed music NFTs as a potentially game-changing moment for the music industry that could enable a new wave of independent artists to circumvent incumbents and middlemen.

There was a lot of excitement and activity early this year, with platforms like Sound and Catalog seeing tremendous month-over-month growth in sales. In hindsight, this was the peak of the hype phase around music NFTs. Since then, the primary sales volume on platforms like Catalog and Sound has fallen significantly. Sound is doing much better than Catalog sales-wise, and volume is starting to pick up again. It is safe to say music NFTs are still a niche market today.

One reason for this is the collective realization that using music NFTs – which represent IP ownership and accrue royalties – will take years, not months. They challenge an entrenched system where record labels and publishers wield dominant power in an industry with little reason to innovate and change. Platforms like Royal are pushing the boundaries, and we expect similar breakthroughs to emerge despite the uphill battle ahead. Meanwhile, music NFTs can function primarily as:

-

Digital collectibles to fund artists’ creative work and establish an early fan base (indie artists).

-

Fan engagement tokens that bring fans closer to their favorite artists (more popular/mainstream artists). They could be channeled towards concerts and merchandise sales (e.g., discounted tickets, exclusive merch) and collectible digital moments for attendees or phygital NFTs fans can redeem when they purchase merchandise.

Despite the lull in music NFT adoption, our long-term thesis still holds, and it will take time to play out. The events of 2022 – with worsening macro conditions and multiple major crypto-related blowups – certainly dampened consumer adoption. But innovation and progress have not stopped. Music NFTs are still a life-changing opportunity for many artists, allowing them to earn more for their work than they’d receive through other channels like streaming platforms. TL;DR: We are still in the early innings.

For those interested, Coopahtroopa publishes a weekly newsletter highlighting the latest developments in music NFTs.

Futuristic Ideas (Longer-Term)

Everything Will Be Tokenized

NFTs allow verifiable proof-of-ownership and proof-of-authenticity while minimizing administrative overhead. These are very compelling use cases for blockchain technology. The cost of creating an NFT is negligible, so a future where NFTs represent (almost) everything we own is entirely possible.

Already, there are some examples of this.

-

In October, Roofstock sold its 1st on-chain house for $175k. Each house is owned by an LLC, and the NFT represents sole ownership of the LLC. Once the asset is on-chain, there will be many new use cases enabled by DeFi interoperability. For example, the house NFT can be fractionalized, and portions of it resold. More people can participate in its upside and earn sustainable yield, which democratizes access to high-quality, real-world assets. An on-chain loan can be taken out using the house NFT as collateral via a lending protocol like Arcade. This can be done in minutes, with no legal paperwork or middleman necessary.

-

Hoseo Univesity in South Korea will issue diplomas and degrees as NFTs beginning this year. In the future, many academic and real-world qualifications (e.g., driver licenses, vaccination certificates) will be issued as verifiable credential NFTs or soulbound tokens. These are tamper-proof and can easily be checked for their authenticity. Such verifiable credentials are essential to a decentralized identity where the user owns their identity instead of the organization, and the identity is portable and interoperable. Decentralized identity is a core component of the Web3 technology stack and will unlock a new set of use cases in crypto.

For a deep dive into digital identities, verifiable credentials, and the reputation layer in crypto, please refer to our report Reputational Identity — 2022 Progress Update.

These are just the tip of the iceberg of possibilities. New multi-billion-dollar businesses will emerge around this; it’s only a matter of time.

Yes, it will take years to get there. We need to onboard the everyday person into NFTs intuitively and frictionlessly, making it as simple to use as WhatsApp. New legal frameworks must be developed to recognize NFTs as property. Governments and large corporations have to buy into the vision of transparency and decentralization enabled by the blockchain. New utility layers need to be built so people will want to use these NFTs.

Digital Items >> Physical Items

Digital items could be worth more than their physical counterparts. Here’s why:

The metaverse will inevitably be a more significant part of our lives. Technology is advancing rapidly, enabling a greater sense of presence in these virtual worlds. New, beautiful experiences can be created that were not possible before. Persistence and interoperability make our actions in the metaverse meaningful, and NFTs help enable this.

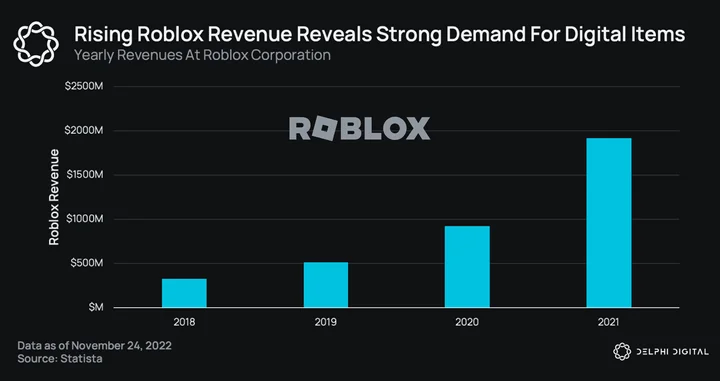

At the same time, the young generation (Gen Z and soon Gen Alpha) today is highly comfortable with technology and the ownership of digital assets. Look no further than Fortnite and Roblox, where sales of skins in these proto-metaverses are through the roof. Roblox player spending is rising, and the total market for skins is estimated to be worth $40B per year. Roblox gamers represent only a small fraction of our population, too.

The confluence of metaverse expansion and positive demographic factors will lead to digital identities becoming as important, if not more important, than our physical identities. We are willing to spend to make our digital identities unique — a new, more powerful version of social flexing. We’re already seeing early signs of this in fashion. A digital version of Gucci’s Dionysus Bag with Bee in Roblox’s virtual world was sold for $4,115, significantly more expensive than the physical bag which sells for $3,400.

NFTs Are No Longer…NFTs

It’s time for a change. “Non-fungible token” is a technical description. It has little meaning to most people, especially mainstream audiences interacting with NFTs in the future. It still functions adequately as a catch-all term today. But as the various NFT verticals mature, it no longer makes sense to use “NFT” to describe generative art, virtual lands, and that sword in your favorite Web3 game — all very different things.

Reddit used the term “digital collectible” to refer to its NFT avatars with great success. It has resonated well with its audience. Similarly, we will reach a consensus over new terms to better represent each use case.

The technology could become so pervasive that it becomes an integral part of everything we do. No one uses “TCP/IP” to describe the internet today. Either way, I give it 50% odds that the term “NFTs” will no longer be widely used in 5 years, even as the industry grows 10-100x larger.

Final Thoughts

Like most markets in crypto, NFTs have taken it on the chin this year. The price of a Bored Ape was once north of $400,000. Today, you can buy one for less than 20% of that cost. Focusing on prices, however, often leads us to miss the forest for the trees. The amount of development and creative energy in the NFT space is staggering, and shows no signs of stopping. Every day, more people are being educated about the power of Web3 and the benefits NFTs can provide. Some of the world’s largest companies and brands are getting involved in meaningful ways. The genie is out of the bottle, and there’s no going back.

NFTs are crypto’s first major mainstream opportunity. The tiny market cap of NFTs relative to the entire crypto market shows how early we are. NFTs have the potential to grow into a multi-trillion-dollar industry, and that future may not be as far away as many believe.

NFTs: The Gateway to Web3

The following excerpt was written by our Head of Research, Kevin Kelly:

As this year’s bear market drags on, it’s given us time to reevaluate our core theses and why we still have so much conviction in this space. One question I’ve been grappling with is what will be the catalyst that attracts more users – and capital – to the crypto economy sooner?

One way is to build new use cases beyond decentralized finance applications. Real-world assets (RWAs) are one example of a huge market opportunity. But another big one – and the one I’m personally most excited about – is the expansion of NFTs and Web3-enabled assets. In my view, they have the power to onboard a majority of new entrants over the next few years.

As the dust settles on this latest hype cycle, it’s becoming clearer to me that NFTs will serve as a primary gateway to onboard the next generation of Web3 participants.

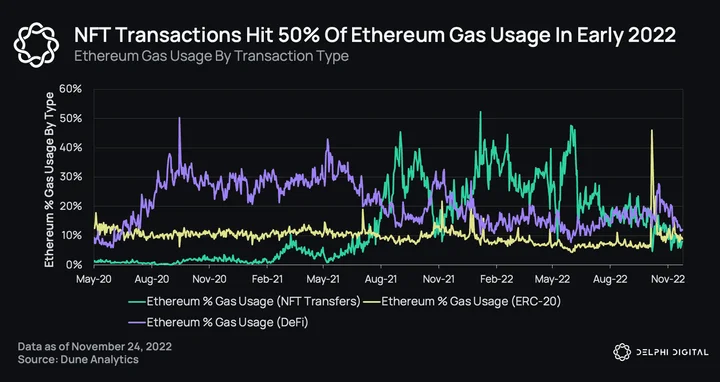

We’ve already seen the power of this sector. At their peak, NFT transactions made up over 50% of Ethereum gas usage, flipping their ERC-20 and DeFi counterparts.

Of course, we’re still a ways away from mainstream adoption, but this space isn’t just theoretical anymore. We’re seeing real engagement and creative experimentation to build new use cases for a growing list of digital asset types – and that’s incredibly exciting if you ask me.

If we took anything away from last year’s NFT craze, it’s that crypto applications go way beyond just decentralized money and DeFi. Like all novel innovations, the NFT boom-bust cycle was a classic example of markets getting overextended on overly hyped expectations of what this new technology would enable in the short run. This attracted a ton of speculators taking advantage of an inefficient market that no one knew how to price.

Each wave of adoption follows a similar trend where hype starts to build, new entrants pile in, prices rise which brings in even more people, speculation takes over (driving prices even higher), new entrants start to get priced out, demand wanes, and assets finally reprice to more justifiable valuations given the market’s current state. We saw this during the 2017-18 ICO mania. We saw this during “DeFi Summer” in 2020. We saw it in the NFT market in 2021. And we’ll see it again in the future because that’s how innovation cycles work.

What’s important is that not everyone leaves after the excitement fades. Each hype cycle carries forward a larger number of active participants who intend to contribute, invest, and build the next generation of new “things,” whether that be protocols, applications, or complementary products and services that push the industry forward.

Interactive Digital Assets (IDAs): Increasing the Surface Area

When I try to explain NFTs to my non-crypto friends, I often refer to them as interactive digital assets because, in my view, that’s what they are. And these types of assets have massive potential — I believe most of us are still underestimating how big their impact will be (myself included).

The creation of new asset types will also benefit the entire crypto economy by increasing the total surface area for new participants to engage with digital assets and the networks they’re built around. The customization and relatability of NFTs makes them uniquely positioned to attract a wider audience, bringing in new sources of demand and buying power.

NFTs are often placed in the same generic bucket, when in reality there are stark differences between collections. This versatility is already enabling a ton of creative use cases, creating more opportunities for NFTs to find product-market fit (or “community-market fit”). Eventually, we’ll see the term “NFT” retired in favor of more specific terminology that better represents the differences between asset types and their core attributes.

If we look at the adoption curve of the internet, there was a certain inflection point where the growth rate of adoption accelerated. This partly stemmed from better infrastructure that made accessing the internet cheaper and more accessible. As more and more people started actually using it, eventually, network effects started to take hold.

What we need now is another creative renaissance that prioritizes novelty and utility over hype and speculation. If the first NFT wave was driven by collectability and novelty, the next wave has to build on these core pillars by introducing new layers of utility that excite both Web3 enthusiasts and non-crypto folks alike. Simply put, what we really need is to create more things that more people care about, and more things that people actually want to use and engage with.

I have a lot of thoughts on this topic that I’m going to air out in another context, but I wanted to share a snippet of what’s got me excited because I really believe this is just the tip of the iceberg. This movement’s best days still lie ahead.

Special thanks to Cheryl Ho for designing the cover image for this report and to Ashwath Balakrishnan and Brian McRae for editing.

0 Comments