Intro

2023 has been a somewhat slow year for blockchain gaming. Although there are many reasons to remain optimistic for the future, the sector fell short of mainstream levels of adoption despite several notable game releases.

However, several noteworthy industry developments occurred throughout the year, along with a significant uptick in market attention in Q4. For this reason and many more that we will highlight in this report, we are excited for the new year and believe there has never been a better moment to prepare yourself for what is to come.

The Year So Far

The total combined market cap of 183 gaming projects has remained roughly between $4B and $7B throughout the year (as much as 86% lower than the ATH in 2022). Compare this to DOGE, a meme coin with arguably zero utility, and it is easy to say there is a lot of room for future growth.

Helping to facilitate that growth is market sentiment and the return of market liquidity. If the current momentum is maintained, 2024 is shaping up to potentially be the year we enter the slope of enlightenment and start to feel the beginnings of true scale.

Further supporting this is that this year we saw even more industry giants dip their toes into Web3. Including Zynga’s casual gaming platform Sugartown, Sony subsidiary Sony Communications Network Web3 joint venture with Startale Labs (and the strong connection it has with Astar), and Roblox CEO’s recent acknowledgment of the value in ownership-based asset agency via blockchain rails.

Additionally, after some initial rumors of an NFT marketplace in the works, Amazon has continued to strengthen its Web3 initiatives with multiple Amazon Prime Gaming partnerships with notable blockchain games. This is in addition to the launch of Amazon Web Service’s blockchain offerings, which include Amazon Managed Blockchain (AMB) Query and AMB Access.

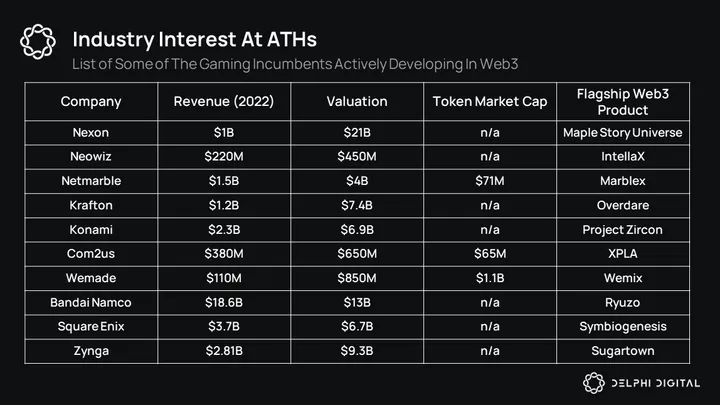

There is also the release of some more notable blockchain-powered UGC platforms to look forward to, such as Nexon’s Maple Story Universe and Krafton’s Overdare. Evidently, industry interest from gaming incumbents is at all-time highs.

Following Epic’s progressive stance on blockchain games listed on the Epic Games Store (EGS), self-publishing was unlocked on the discovery platform in late 2023. This move was less for the betterment of blockchain gaming and more a move to try and capture market share from Steam in the two platform’s ongoing rivalry (it should be noted that Epic maintains its distance, stating the games’ publisher is responsible for all asset transactions, customer service, refunds, and fraud).

That said, it undoubtedly had some positive downstream impact for Web3, with 81 blockchain games on EGS at the time of writing — up from 70 at the end of October, and many more reported to be arriving soon. Not all these games are playable, and most use the platform to boost discoverability early on (along with listing on Steam).

In regulatory updates, sizable progress has been made for blockchain gaming over the past year. Although much more progress still needs to be made, we saw Android take a more progressive stance toward both blockchain integrations in mobile games (which went into effect on December 7th), as well as the advertising guidelines these games must adhere to (a positive change from the original outright ban).

However, there were some negative implications from the SEC related to the legality of some of the token models and GTM strategies used by blockchain projects. In June, as a part of the SEC’s case against Binance (a recently settled case), a handful of gaming tokens (Decentraland’s MANA, The Sandbox’s SAND, and Axie Infinity’s AXS) were highlighted as potential securities. In a separate case, the SEC went after Impact Theory, a Web3 community business, and labeled the project’s NFT collection as securities.

Blockchain Game Funding

It should be no surprise that 2023 has been a tough year for game funding. A total of 133 deals were disclosed, and $1.18B in funding was raised (note that funding data from December 2023 is absent from these figures). Although the monthly number of disclosed deals has remained relatively stable, averaging 15 deals per month, the funding amount has steadily declined.

Unsurprisingly, when we zoom out, a similar trend extends to the start of the bear market in Q1 2022. The average yearly funding amount has dropped by 66% since 2022 and 56% compared to the year prior.

The total number of deals dropped by just under 50% from 2022, illustrating the relative decline in VC interest since the height of last cycle’s bull market.

However, this figure was almost the same as the number of deals closed in 2021 (135), not including December metrics. This suggests that the standards held by VCs operating in the space have increased, and valuations have also become more representative of wider market conditions.

Somewhat encouragingly, the traditional gaming industry is going through a similar downturn. Q3 funding in 2023 fell 64% year-on-year (YoY), compared to Web3 gaming’s 66% decline. Compared to Q3 2021, Web3 game funding fell “only” 73%, compared to traditional gaming’s 85%.

Covid played a large role in the fast and easy money available in 2021-2022. The metaverse hype train and P2E craze were just extra fuel for the fire that moved the spotlight slightly towards blockchain integrations.

This bubble is further supported by the fact that the number of Web3 gaming deals fell 48% YoY in Q3’23. This is compared to traditional gaming’s relatively smaller decline of 34%, not to mention the numerous crypto market disasters over the past ~2 years.

That said, more concentrated and calculated bets should be considered an overall positive for the industry. Further, funding data remains a lagging indicator of growth and interest. VC funding is often reactive rather than proactive, and this is particularly true for gaming, where the success of the application layer strongly influences future funding.

It will only take a short series of bullish announcements or the discovery of a killer app/business model for the funding landscape to reverse. With many well-funded, quality blockchain games releasing in the coming 12 to 24 months and the more recent in-flow of capital to secondary markets, we may have reached the bottom of the funding cycle. If so, private markets will start to reflect this reversal over the next six months.

Key Themes & Future Trends

With that out of the way, the remainder of this report will dive deeper into some of the key themes, as well as the notable trends to look out for in 2024. We will also highlight the projects we are most excited about and the key challenges they will face over the coming 12 months.

#1 – Mobile Markets

Until recently, browser-based gaming has been the only achievable channel for Web3 developers. As onboarding improved and more lenient regulations came into effect, mobile is now an increasingly more attractive gaming platform for Web3 developers.

Simultaneously, some Web2 incumbents are being forced to adapt their existing monetization models to better fit a post-ATT/IDFA landscape. With the mobile market accounting for roughly 50% of global gaming revenue and several synergies in monetization models, we expect to see more mobile games launch with blockchain rails soon.

As our recent mobile gaming report outlined, there remain ample opportunities for Web3 teams to build with this platform in mind. An estimated 26% of all Web3 games were building mobile-native games (compared to PC + browser’s 43%), making this market relatively uncompetitive for blockchain companies despite the adverse UA landscape and highly saturated Web2 market.

Furthermore, several mobile-dominant genres are well suited for blockchain rails. A recent report indicates that RPGs are the favorite pick for blockchain gaming teams (22%). Followed by Action (17%), Strategy (15%), and Casual (12%), with the honorable mention of Social Sims, which have seen significant levels of adoption in Web3 thanks to titles such as IMVU, Highrise, and ZTX.

The abovementioned genres present key markets for Web3 teams implementing blockchain models that utilize NFT collectibles, skill-based real-money tournaments, and on-chain player progression.

A final mention that has seen relatively lower amounts of experimentation but is equally promising is mobile games that can leverage blockchain-based nano-transactions. As highlighted in our recent report on the topic, this represents a meaningful new business model for mobile games, especially those that lean more toward hypercasual loops.

Although this model is still in the early stages of growth, a number of developers and publishers already exist, with Lightning-based fintech company ZBD leading the charge, using Bitcoin as a preferred payment layer that facilitates nano-rewards for increased retention and conversion. We are excited to see how this space continues to innovate and expect to see more teams use blockchain rails in their tech stack to boost profitability in an increasingly competitive landscape.

Asia Primed For Growth

Just as mobile is the largest platform, Asia is the largest region, accounting for roughly 50% of global revenues. Moreover, Asia is predominately a mobile-first gaming region, with console and PC adoption recently showing signs of growth.

It has also been reported that the leading markets (in order) for blockchain gaming are the Philippines, Nigeria, Pakistan, Singapore, Vietnam, South Korea, Hong Kong, China, and the United Arab Emirates. All of which have maintained a position within the top 15 over the past three years.

Although the West, and the US in particular, may lead in terms of sheer numbers of Web3 gaming stakeholders, there are several Asian countries that come top of the list on a per capita basis.

Additionally, APAC remains the region with the largest number of Web3 game developers (49% of the total in 2023) according to a recent report by Game7. Further, the number of games built by APAC-based teams has also grown at a yearly average of 15% since 2021.

However, it should be noted that per country data shows that the USA has the highest number of teams (30%), followed very closely by South Korea (27%), and then Japan (10%) (China was not included in the list).

Mobile is the medium of choice for most leading publishers in Korea, Japan, and China (which happen to be the three largest markets for players and developers). It should then come as no surprise that this is also the case for blockchain gaming.

Therefore, Asia will likely be the biggest market for blockchain games in the coming years based on the relatively high levels of consumer acceptance and the numerous synergies between mobile monetization models and blockchain.

This is further supported by activity surrounding some of the most popular projects in the region. Matr1x, Fusionist, Gas Hero (the team behind STEPN), and Mahjong Meta have all seen impressive metrics throughout 2023.

In recent months, ZTX and L3E7 stand out as Asia-focused projects that have built significant social traction and are close to a full launch. Additionally, as shared in our KBW and Token2049 roundup report, all eyes are on Nexon and the coming release of Maple Story Universe.

Nexon has had a killer year, financially outperforming quarter after quarter. They have the capital, the clout, and a masterful team to bring some much-needed legitimacy to blockchain gaming. The Maple Story IP is also one of the best, if not the best, positioned to onboard millions of traditional gamers into Web3 with their simple yet impactful use of UGC blockchain rails.

However, with great power comes great responsibility, and it should be noted that if Maple Story Universe ends up being a flop, then it could have significant ripple effects that influence the decisions of any established incumbents paying attention.

#2 – The Fight For Player Liquidity

A major theme in 2024 will be the coming war over player liquidity. There are a number of leading factors as to why many projects will be fighting over the limited pool of Web3 users, but it is helpful to start with the infrastructure layer first.

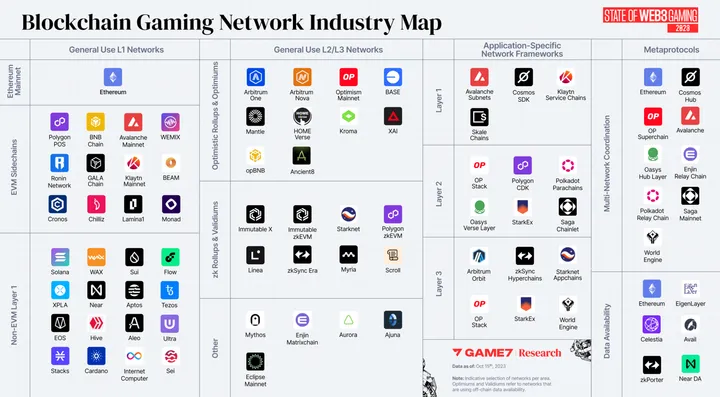

The total number of gaming-focused, or adjacent, networks has been increasing year-on-year. In 2023 alone, a reported 76 new networks, comprised of general-use L1s, L2s, and appchains, popped up.

Further, the number of gaming-specific networks has also increased. Ancient8, Beam (Merit Circle), and Lattice’s Redstone are just a few of the many that have emerged over the past 12 months. This doesn’t include the soon-to-be-launching game-specific appchains using Avalanche’s subnets, Polygon’s zkEVM, and Arbitrum Orbit.

On-chain activity is one of the more important metrics for value accrual, community sentiment, building network effects, and fundraising. With blockchain gaming generating, on average, 23x more on-chain transactions compared to DeFi protocols in 2023, this will undoubtedly be a key area of focus for many.

This brings us to the applications layer. 2023 saw several new game releases, bringing the total number of blockchain games to roughly 2,500 to 3,500.

The number of actively played games is another matter. Just over an estimated 5% of all playable blockchain games have an active daily player base above 100 user wallets. Furthermore, financialized player incentives and the increased costs associated with launching and running live ops for Web3 games make these games expensive to sustain.

UA for blockchain games is also incredibly expensive, with some case studies pointing to customer acquisition costs (CAC) for mobile hypercasual being 77% higher than non-Web3 alternatives. To reach profitability and scale, many of these games will need to increase the long tail of monetized users, deepen the spending of whales, or both.

For now, only the strongest IPs or best UA teams can scale in Web2. The rest will have to compete over the small pool of existing Web3 users and try to increase player lifetime value (LTV) with Web3-native monetization models.

There is currently only roughly 1.2M total number of daily unique active wallets interacting with gaming protocols and between 15M and 25M daily gaming transactions. A single game that successfully captures mindshare can significantly impact an ecosystem’s on-chain metrics.

For example, the sudden spike in transactions illustrated in the above chart came from the launch of Ethos Wallet’s game Sui 8192. Additionally, Sage Labs, a FOCG RTS made by Star Atlas with idle mechanics, currently has only ~1.5k daily active player wallets but is generating 1.8M daily transactions (accounting for approximately 10% of all transactions on Solana).

Player liquidity will soon become a scarce and highly valuable resource. Publisher-type platforms, such as Ready Games, that can bridge over existing Web2 players into Web3 will be in high demand along with Web3-native networks, like Ronin and Treasure.

![]()

Pixels, a Web3 social simulation game, saw this firsthand when it went from relatively few active users to between 50k and 100k DAU simply by migrating from Polygon to Ronin. Strong Web3 communities can become low-cost brand ambassadors, significantly increasing reach and revenue once their attention has been effectively captured.

Play-to-airdrop

In line with the fight for player liquidity, financialized Web3-native UA models have and will continue to rise in popularity. Last year, we commented on free NFT mints as a new UA mechanism made popular by Limit Break’s DigiDaigaku Genesis collection, which reached an ATH average price of over 20ETH late last year.

Around the same time this year, we saw more teams leverage financialized incentive models in the form of fungible token airdrops to capture consumer attention and onboard new users. AKA play-to-airdrop, this model rewards stakeholders who complete quests, test early game builds, or obtain on-chain assets with tokens.

Although blockchain protocols have long used token airdrops to acquire market share, they have largely been unexplored in gaming. This changed when BigTime, a blockchain-powered MMORPG that has been in early access and off many people’s radar for roughly a year, airdropped BIGTIME tokens to beta testers in October.

In a series of surprising events, the token price proceeded to rise by more than 370% over 24 hours. BigTime was by no means the first blockchain gaming project to raise eyebrows in 2023. That award would likely go to Parallel and its PRIME token.

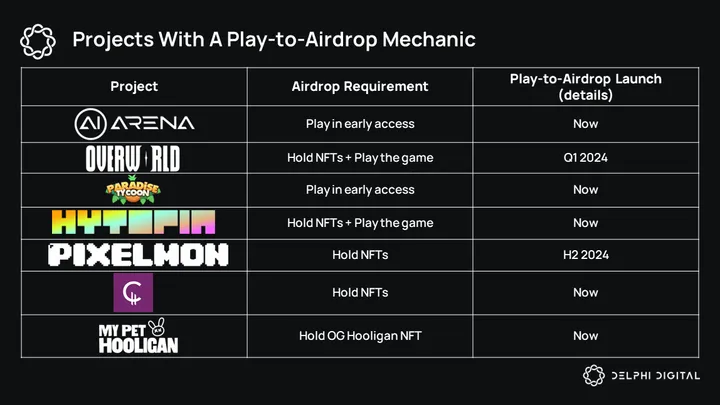

However, it did act as a catalyst for the gaming airdrop meta and was shortly followed by projects like Zepeto (ZTX) and Shrapnel (SHRAP). At the time of writing, play-to-airdrop remains a strong narrative in the space, and we expect this to continue into 2024, provided the markets remain strong. In the above table, we have highlighted some projects with an upcoming airdrop for stakeholders.

It is important to note that although airdrops can act as a great UA or reactivation mechanism, they are typically quite bad at increasing retention. As illustrated by the previously mentioned Sui 8192, any increase in metrics, such as registrations, active players, or on-chain in-game transactions, will predominately be comprised of airdrop farmers who will abruptly leave once any incentives are gone.

Additionally, if the industry abuses this incentive structure in the short term, there is a risk of obfuscating organic player demand. This could negatively impact long term sustainable growth.

To combat this, we encourage teams to continue experimenting with these emergent Web3 UA models. Leveraging delayed incentives, for example, could help align emissions with key milestones/KPIs. Additionally, pairing financial incentives with tailored Web3-orientated conversion flows should better retain additive player types as opposed to purely extractive ones.

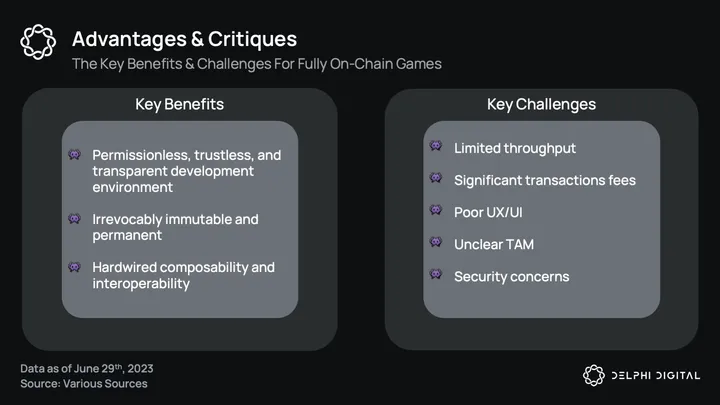

#3 – FOCG Of The Future

2023 was a big year for fully on-chain games (FOCG) and the tools that empower them. We won’t go over every major development and encourage you to refer to our high-level primer here if that interests you.

The TL;DR is that FOCGs rely on blockchains at a fundamental level and leverage this technology to unlock persistent, composable, interoperable, and hardened FOCGs. 2023 saw several major advancements in the ecosystems and tools built to empower fully on-chain environments, including the emergence of FUCG engines. Below are some of the current sector leaders spearheading this sub-sector.

Optimism and the OP Stack framework have become arguably the most popular option for FOCG developers. This increased adoption from the community can largely be attributed to the support shown by the Lattice team after they positioned their in-house title, OPCraft, in close proximity to the Optimism ecosystem.

Furthermore, a key piece of FOCG infrastructure being built with the OPStack by a Lattice team is MUD. MUD is an open-source development framework and currently the most widely used FOCG engine. After the relative success of OPCraft, we are excited to see more complex games launch with deeper gameplay mechanics, such as Sky Strife and Primodium.

Starknet is another of the more popular infrastructure choices for FOCG despite being one of the few that isn’t EVM-compatible. Although, nine times out of ten, the closer to Ethereum, the better when it comes to accessing liquidity, Starknet provides a number of advantages over the other popular alternatives, such as using Cairo and including native support for account abstraction.

- Realm ecosystem, with Bibliotheca DAO and its LORDS token, being the driving force behind the ecosystem’s growth, along with support from the LORDS-governed Frontius House.

- Dojo is Starknet’s version of the MUD on-chain gaming engine, built by the Cartridge team, that uses an Entity Component System (ECS) framework to make building FOCG easier.

- Cartridge aims to improve discoverability for games being built on Starknet.

Arbitrum can be viewed as the FOCGing underdog. The vast majority of gaming activity on Arbitrum has historically come from blockchain gaming publisher Treasure (learn all about the Treasure ecosystem here). In 2023, we saw Arbitrum take several steps to encourage more growth in gaming, including a move to onboard more FOCG teams.

The network is made up of a series of L2s. Arbitrum One is the flagship project and the L2 with a thriving DeFi ecosystem ($1.6B in TVL), but limited throughput makes it not an ideal destination for gaming. Arbitrum Nova leverages a third-party data availability layer (Arbitrum AnyTrust), making it much more suitable for games despite the weaker security guarantees.

Arbitrum Orbit is the latest layer in the stack and the most scalable of the three, enabling teams to create their own L3 (transactions are settled on Orbit). XAI is one such example and recently launched its gaming L3 (also using Arbitrum AnyTrust for data availability). It should be noted that XAI plans to launch its testnet in December and will be governed by the native gas token, $XAI.

There are several other notable mentions that are in the early stages of development or traction, including:

- Curio (Keystone)

- Paima Studios (Paima Engine)

- Argus Labs (World Builder)

Future Outlook

The FOCG sector is undeniably still in the early stages of experimentation and thesis validation. Although there was significant buzz during ETH Global, the AW hackathon earlier in the year, and the more recent Dev Connect conference, excitement is largely concentrated within relatively small developer circles.

As such, the total number of FOCG consumers is relatively small. Capital is also largely concentrated around infrastructure. Applications are having a much harder time raising funds, and this will ultimately slow growth. That said, there are still plenty of grants, with ecosystems such as DAO-driven Frontius House (of the Realms ecosystem) funding over 20 small teams to date.

Despite this, the barriers to entry for players to enjoy these games are falling. Evidently, it is still too early for a mass-market-ready product. However, we are excited to get hands-on with the growing number of accessible FOCG over the coming months, such as Pirate Nation.

At the same time, projects such as Cambria (Dual Arena) and Doomsday demonstrate what can be accomplished with a Web3 purist approach to game design (only recommended for the more degenerate readers).

Looking forward, we are excited by games that aim to set a new standard in terms of quality. Projects such as Influence and Citadel hope to bridge the gap between enthusiastic developers and hard-core gamers. Despite the fact this will inevitably increase their timeline to launch, we are totally here for it.

Finally, there is also a lot to look forward to on the tech side of scalable FOCG. One such example includes continued experimentation with verifiable off-chain computation with on-chain state management. The application of ZK proofs, as well as ZKML, in this context, will likely create a meaningful step forward for the sector outside of existing use cases, such as asymmetric information generations.

#4 – Emerging Trends

Now for a quick look at emerging trends that are too early to expect mass adoption in 2024 but show enough potential to hold firmly on your radar.

Telegram Crypto Gaming

The Open Network (TON) is, for intents and purposes, Telegram’s very own blockchain network. Although the majority of TON’s ~1M active wallets and ~200k daily transactions are focused on token trading, TON has a rapidly evolving blockchain gaming ecosystem.

With a reported 800M MAU, Telegram is one of the world’s largest social networking apps. It is also a key communications tool used by many blockchain communities and businesses. It is, in theory, a great game distribution channel for both Web2 and Web3 gamers.

However, at the time of writing, there are fewer than 100 active blockchain games on the platform. The good news is that gaming is one of TON’s core focuses for 2024, and there is a lot to look forward to in the near future.

Two notable developer publishers early to TON are Nakamoto Games and GAMEE. The former recently created its own multi-coin TON wallet and ported 50 of its casual games to the platform. The latter, creators of hypercasual blockchain gaming portal Arc8, are also one of the largest distributors of games on Telegram. Additionally, Animoca Brands (parent company of GAMEE) recently became the largest validator for TON and will undoubtedly support future gaming initiatives in the ecosystem.

TON gaming still faces several challenges, including the fact that discoverability is pretty bad as far as distribution platforms go. Additionally, a major obstacle to broader adoption on the developer side is the lack of a clear path for monetization.

Currently, the main way apps monetize is via IAPs, which is a little clunky and unideal for a predominantly hypercasual platform. If TON is able to deliver on a privacy-preserving ad network, the platform is likely to see increased developer interest and the beginnings of the network effects needed to scale.

The Future Of AI Gaming

AI received a lot of attention in 2023, and gaming is one of the key verticals ready for disruption. Generative art will increase productivity, raising the quality bar for small teams, and AI-driven “generative agents,” as described by a recent Stanford study, will create entirely new player experiences.

However, we are still years away from any significant real-world applications of this tech, especially in the case of the latter point. That said, progress continues to be made every day, and we will undoubtedly see the AI hype train return again in the near future, so it is better to be prepared.

At the intersection of AI, blockchain, and gaming, there are a small handful of projects leveraging the tech in interesting ways. If we do see renewed interest in AI-related projects, these are all worth having on your radar.

Colony, the AI NPC social sim from the makers of Parallel, will likely be the first to cause a stir in the market due to its proximity to the aforementioned TCG and its being the second title in the Echelon Prime ecosystem. The game will not only feature emergent NPC behavioral gameplay loops but will also share the PRIME token and provide additional utility to Parallel NFT avatar holders. Note that a clear release date for this game is TBA.

Today The Game and AI Arena are two more AI-powered games of different genres. Today is an MMORPG meets farming sim and city builder. The game will feature several AI-powered UGC tools, as well as an AI chatbot. AI Arena is an interesting PvP battler similar to Super Smash Bros that, instead of player-controlled characters, features an AI training room and autonomous fighting. AI Arena already has NFTs on the market, which have already appreciated in price as a beta to the AVAX gaming narrative. Note that both projects will also feature a play-to-airdrop mechanic during early testing.

Two much earlier stage projects are Gepetto and Avalon. The former is developing a number of AI-powered tools for creators, including a powerful text-to-3D Image generator. Avalon is an MMORPG with fully AI-driven NPCs and a really impressive suite of UGC builder tools.

Although the use of AI in the gaming industry and what that may unlock in the future is exciting to think about, it is fair to say that this technology is still 3 to 5 years from fruition. We may see a metaverse-like level of excitement again in 2024, but it is unlikely this will sustain for long.

New Blockchain Advancements

Every new year brings with it a set of new technological advancements. Blockchain is no different, but instead of highlighting everything, we will select a few that are more relevant to the gaming sector. Account abstraction was the big one on everyone’s mind this year. Numerous unlocks have been made possible, but the key takeaway is that it will hopefully drastically improve the new user experience for both FOCG and more hybrid titles.

Account abstraction was the big one on everyone’s mind this year. Numerous unlocks have been made possible, but the key takeaway is that it will hopefully drastically improve the new user experience for both FOCG and more hybrid titles.

We are particularly excited to see the wider implementation of session keys, MPC wallets, and social recovery as white-label solutions, like those offered by Stardust and Blockus, become more readily available.

Additionally, as mentioned in the Year Ahead: NFTs report, advancements with the ERC-6551 token standard should have meaningful implications for blockchain-based games. Depending on the game genre, use cases can range from being able to store all your in-game on-chain items within a single NFT backpack to AI-powered NPCs enacting on-chain transactions without human intervention.

High-Potential Projects

Hytopia Back From The Brink

Hytopia, previously NFTWorlds, was highlighted in last year’s report but for entirely different reasons. Back in Q4 2022, the project was doing damage control to try and stop the bleeding caused by Mojang (the creators of Minecraft) rug. Fast forward two years, and the team has rekindled stakeholder confidence and recently closed a $3M investment round led by Delphi Ventures.

Hytopia is a Minecraft-inspired open-world UGC platform with a number of unique quality-of-life upgrades. These include being F2P, facilitating player-owned assets, vastly improved payment rails for users and creators, and an incentives model that rewards players for their time.

The problem was that, at the time, Hytopia was being built on top of the Minecraft client, so when Microsoft, the owner of Mojang, renounced all connections to Web3, the project was seemingly dead before it had even begun.

Fast forward 12 months, and the team has not stopped shipping. A lot of the blockchain tools that had already been built out, such as gasless transactions, wallet creation, and onboarding, were packaged into an open-source developer kit called Metafab, which has since seen over 2M API calls since September and by ~1k protocols, including Treasure and ExPopulus.

Additionally, the team is just around the corner from delivering on its first-party game client and engine. The beta, which saw 20k registrations within 8 hours and surpassed 1M at the end of October, will be released by the end of the year or early 2024. It is still early days, but we are excited to get hands-on by the beginning of the new year.

The bull case for Hytopia is that they are able to capture market share from Minecraft and Roblox’s combined 350M MAU. An ideal target audience will be groups that are starting to age out of existing platforms but are not attracted to the alternatives, such as Fortnite.

If Hytopia can attract these churning players with a truer sense of ownership (think how much these players already spend on Minecraft without agency over their assets) and economic incentives, then prices are very attractive at current levels.

Roblox is currently valued at $28.8B; Hytopia’s market cap, on the other hand, is ~$35M, not including the NFTs, which have a floor price of 0.3ETH. All IAPs in Hytopia are settled in the native token, and this revenue stream is redistributed to the project and stakeholders via a number of mechanics outside the scope of this report. The important part is that if they can capture just 1% of Roblox’s market (not including Minecraft’s), then the upside is significant.

The bear case for Hytopia is that they are unable to execute on delivering a superior user experience than the competition. Additionally, the project’s land NFT model is outdated and significantly limits scale if provided with too much utility. Remove, however, and you jeopardize current holder sentiment utility might be the easiest way to piss off your holders, but the team has managed surprisingly well so far.

Regulations and the potential to unleash the wrath of Microsoft are also risks, but that goes without saying. UA will also be a challenge. Hytopia is a PC game with its own launcher; acquiring users is going to be extremely difficult and expensive. The team’s best bet is to go slow and steady by organically onboarding creators and influencers who will then bring their fans. This approach will take time, so funding might become an issue later down the line.

It should be noted that Hytopia is still in the early stages of development, with the next major catalyst being the public beta in Q1’24 and relatively few publicly announced after that.

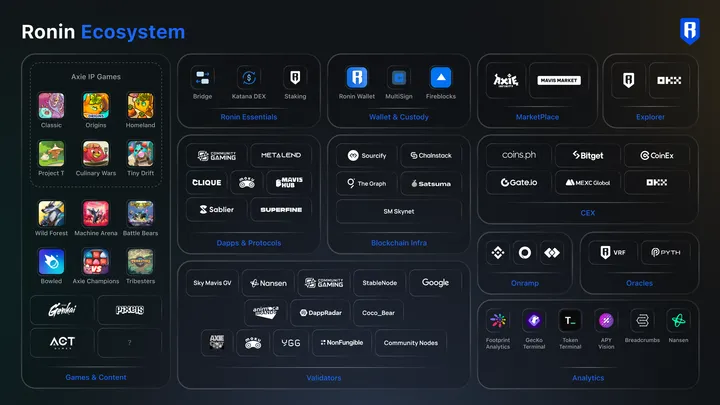

Ronin, The Chain With Gamers

Ronin has received a fair amount of attention over the past couple of months, and RON has more recently increased in price by more than 2x since we last mentioned it here and here. That said, looking at the fundamentals and comparing Ronin to the competition, there is possibly a lot more room for the token price to grow.

Over the past 30 days, Ronin has seen an increase in on-chain active wallet addresses of more than 600%, and transactions are up by roughly 300%. Although we do not know for sure how many of these ~140k wallets are genuine users, the significant growth in KPIs is a testament to increased market interest in the ecosystem.

A large contributing factor to this renewed interest is the previously mentioned migration of Pixels. Despite the undeniably effective use of various mechanics to funnel player liquidity into the game, as well as the >$150k worth of RON spent on Pixel VIP passes since the beginning of November, it is likely many of these newly onboarded players are simply farming the soon-to-launch PIXEL token airdrop.

Regardless, Ronin’s core value proposition remains the same. A gaming-focused community of active and sticky users that can be funneled to any one of Ronin’s ecosystem products (with the help of some financial incentives). The same can’t be said for many of the other leading blockchain networks.

The bull case for Ronin is that it is able to onboard more in-demand gaming content and provide this content with its first golden cohort of true fans. Games can then leverage this core user base as brand ambassadors to efficiently scale.

This is a strong offering in the current market, in line with our fight for player liquidity thesis, and places Ronin on the shortlist for projects in search of an infrastructure partner with active users. We highlighted earlier the impact a single game could have on an ecosystem, and with Ronin’s current value proposition, it is well-positioned to capture the next Axie Infinity.

With a current market cap of just over $300M, in the bull scenario, RON has ample room to grow when compared to competing chains. For perspective, ecosystems such as GALA and Immutable have a respective market cap of almost $750M and $1.7B each.

The bear case for Ronin is that it is unable to onboard new players at the same rate it onboards new games. If Ronin’s player liquidity becomes diluted, it loses one of its main competitive advantages.

Sky Mavis will undoubtedly be looking to replicate Pixel’s success elsewhere in order to maintain momentum behind the “Ronin Effect.” Despite the promising-looking early partnerships, it is still unclear how successful they will be at sustaining this narrative throughout the year.

Another risk would be if the ecosystem leans too much into financial incentives. The more value extractive Ronin’s users, the more harm they can cause in an early-stage game. Furthermore, financially incentivized players will easily churn. The prospect of welcoming a swarm of locusts only for them to leave for the next pasture before you can establish a core user base is a daunting thought for any development team.

It should be noted that there is a relatively large portion of the total token supply yet to be unlocked and comparatively low token utility (essentially just a gas token with a staking function) when compared to some competing ecosystems.

There is also the point that there are many other projects tackling the same issue of player liquidity the previously mentioned Ready Games, as well as projects like GameSwift, GuildFi, YGG, Treasure, and XPLA, are all taking a similar approach to Web3 publishing.

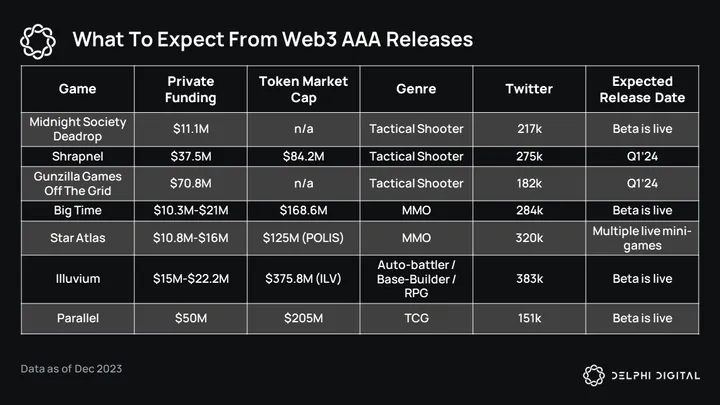

Opportunities in AAA Gaming

One area of blockchain gaming that has undoubtedly captured the most private and public attention over the past two years is triple-A gaming (AAA). Looking past the validity of these claims (8-fig funding alone is not enough to warrant a AAA moniker), it is worth briefly diving into some of the most anticipated blockchain games.

Many of the games listed in the above table are already playable, and all should be made available via either a beta or full launch by the end of 2024. Further, all have curated a strong social following and leveraged this to complete large primary sales of blockchain assets.

Now that liquidity is returning to the market and we are fast approaching the official launch of these games, which are best positioned to see the most upside in 2024?

Let’s first address arguably the most contested genre of Web3 AAA titles — Shooters.

Although some nuances remain between Shrapnel, Deadrop, and Off The Grid, at a high level, they are competing not only amongst themselves but also with the wider Web2 Shooter market.

Deadrop has the largest head start of the three in terms of time on the market, with the beta opening in early 2023 (although it was token-gated). It also has the largest social following, with a combined 217k X (Twitter) followers and a co-founder (Dr. Disrespect) with 4.6M YouTube subs.

Shrapnel has the largest standalone X following (not accounting for bots), and the team stands out in its ability to design and deliver a rich narrative-led experience. The game was also the first to launch its in-game token, which has increased in price by more than 300% since we first spoke about it.

Off The Grid (OTG) has been in development for roughly two years (potentially closer to launch than Shrapnel), has arguably the strongest visual design team, and raised the largest amount of private funding of the three. However, even $70M doesn’t come close to the $200M+ it usually costs to develop, launch, and promote a traditional AAA shooter.

At a high level, it is going to be extremely hard for any of these projects to capture any meaningful market share away from the giant incumbent IPs, such as Counter-Strike, Call of Duty, or even indie smash hits like Escape From Tarkov.

This is not a level playing field, and new entrants need to bring something other than player ownership to be competitive. Therefore, all things remaining equal, it is likely that the project with the most social influence will capture the lion’s share of Web3 attention in the short to medium term.

Deadrop is best positioned in this regard, but with current NFTs (cosmetic avatars) already costing several hundred dollars, I would be more interested in a fungible token play if/when one is launched.

On the other hand, Avalanche is in the process of building a strong gaming narrative for the next cycle. If this meta continues to gain traction into the launch of Shrapnel and OTG (both using Subnets), then we could see larger amounts of new capital flow into these two projects as the ecosystem’s leading games. If so, OTG would be my preferred choice, depending on Shrapnel’s ability to build a thriving player-driven UGC economy.

The remaining four titles are all relatively further along in their development cycles and have all launched both NFTs and fungible tokens. Despite them occupying different genres, all claim to be AAA and aim to compete with incumbent Web2 games at the highest level in order to onboard the next 1M+ gamers into Web3.

Right next to Shooters, in terms of highly competitive markets, are Trading Card Games (TCGs). TCGs have long been considered a natural fit for Web3, largely in part due to the collectible nature of these games and what NFT-based ownership hopes to bring to the table.

As such, there have been dozens, if not hundreds, of Web3 TCGs coming to market. Some notable mentions are Splinterlands, Gods Unchained, and Cross The Ages. Parallel is the latest TCG to launch in beta and created a lot of buzz thanks to its high-production graphics and good marketing.

Despite being highly monetized, the traditional TCG market is relatively small and highly competitive. This makes it incredibly difficult for new entrants without drastically innovative gameplay and a powerful IP to scale. The odds for Parallel reaching mass adoption with the mechanics that are currently on offer are slim, but that will not stop it from likely remaining Web3’s top pick within the genre.

PRIME has performed well despite launching in the middle of the bear market, and the buzz around the game has only been growing. This hype will aid the project in onboarding more third-party titles into the Echelon Prime ecosystem, which will accrue further value to the token. Add on the fact there is an AI play with avatar NFTs and the upcoming Colony game and PRIME is an interesting token to keep an eye on.

Big Time is another standout performer that recently launched its token. As previously mentioned, BIGTIME TGE was timed well, going live just as the market started to pick up. This led some players to earn as much as $2k a day in in-game token rewards, resulting in the token price increasing by 300% shortly after.

Star Atlas and Illuvium hit their peaks during the previous bull market. As asset prices start to creep back up to previous highs, some stakeholders will inevitably look to exit. However, the mix of strong community building, highly invested fans, and sunk cost fallacy can also become a project’s biggest asset. As demonstrated by Axie Infinity and Ronin, an empowered community has the potential to act as an effective marketing tool, bringing in new stakeholders.

Additionally, games like Illuvium and Star Atlas play significant roles in their respective blockchain ecosystems. Illuvium is one of the biggest gaming projects on Immutable (second only to Gods Unchained), and as previously mentioned, Star Atlas is currently the largest game on Solana by transaction volume.

For as long as this persists, each game should not only receive ongoing support from their respective networks but also see the asset’s price performance somewhat correlated to the narrative surrounding the ecosystem.

My largest concerns of the three games are:

- Star Atlas is incredibly ambitious in both scope and timeline. For perspective, Star Citizen, an MMO that shares many similarities with Star Atlas, has spent 12 years and $600M on development and is still not ready for a full launch.

- Illuvium is a big-budget game competing in an arguably quite small and very competitive genre. The project is similarly ambitious, building three games at once (read more about the Illuvium ecosystem here). Further, the project has had assets live on public markets for years now, with many stakeholders >80% below their entry price.

- Big Time started the play-to-airdrop gaming meta and recently saw its market cap reach $240M. However, the project has been struggling to balance its economy, and the relatively few players who kept playing after rewards were reduced are still locked inside a predominantly earning-focused gameplay loop. The main concern here is that without significant quality-of-life improvements, most players still in the game will either churn completely or leave for greener pastures.

Conclusion

As we highlighted in the 2022 year ahead gaming report, the market has remained within the trough of disillusionment for the majority of the year. The past two months have been great for a quick boost to morale, but it is important to remember we are not out of the woods just yet.

That said, if momentum continues over the Christmas period and into the New Year, then 2024 is shaping up to be a very exciting year for the industry. That said, there are still plenty of challenges awaiting those actively building in the space. Teams will need to face further regulatory uncertainty, the remnants of blockchain onboarding frictions, and expensive UA combined with a highly competitive attention economy.

We will soon see if 2024 is the year that private capital inflows will reinvigorate the funding landscape, enabling more teams to experiment and build quality products – Renewed market activity will provide ample opportunities for the most well-informed investors – Gamers will now finally get their hands on great games that provide altogether new player experiences.

0 Comments