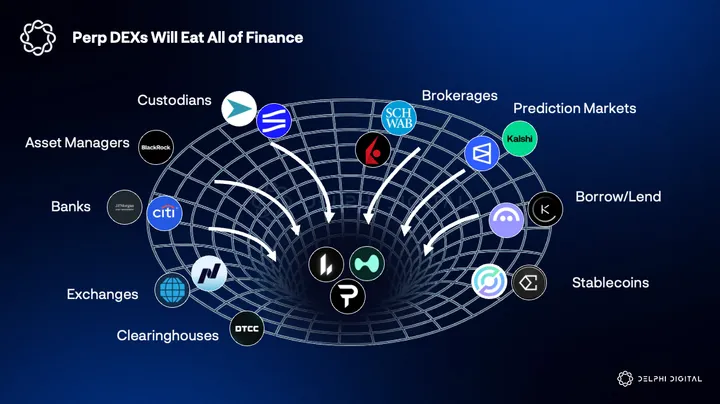

Report Summary

Crypto is entering the aggregation era: Value is shifting to platforms that own the user interface as distribution costs collapse.

Crypto superapps are aggregation layers: They unify best-in-class protocols into one interface with one identity, one balance, and one activity feed.

Aggregation consistently wins: Across e-commerce, social, and fintech, users pay a premium for convenience, fewer apps, and reduced friction—crypto follows the same pattern.

Crypto superapps scale faster than TradFi: Features can be added via protocol integration rather than costly builds or acquisitions, enabled by 24/7 markets and composability.

Why now: UX maturity, regulatory clarity (US, EU, Asia), and real-world financial utility have removed prior adoption bottlenecks.

The core battle is the daily surface: Winning platforms secure a high-retention wedge product, then expand vertically once user attention is locked in.

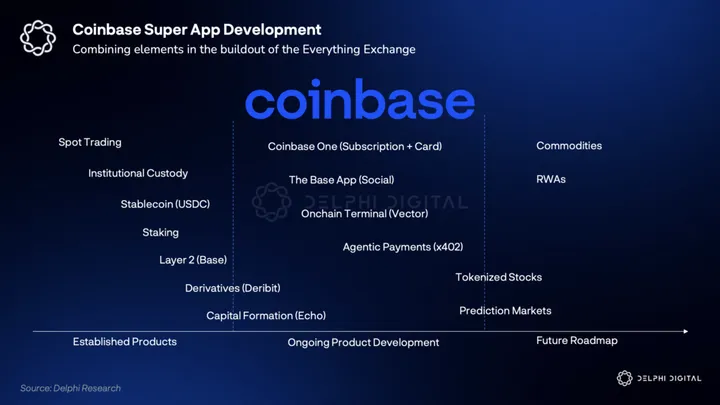

Coinbase’s strategy: Evolving from a cyclical exchange into an “Everything Exchange” via Base (OS), Base App (interface), stablecoins, subscriptions, and derivatives.

Endgame: The durable moat is distribution and attention—platforms that seamlessly blend centralized trust with decentralized rails become financial infrastructure.

The Quest for Crypto Superapps

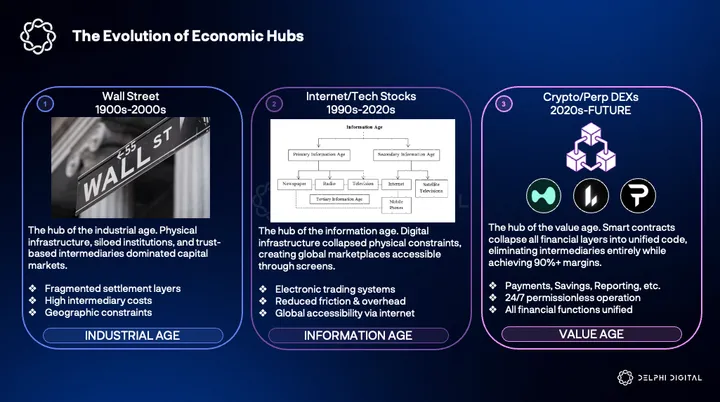

The aggregation era follows a familiar rule of digital markets: when distribution gets cheap, value shifts to whoever owns the user. In crypto, this idea showed up as the Fat Wallet thesis earlier. What’s different now is that the stack is finally mature enough for true crypto superapps (aggregated giants) to exist without being limited to the wallet form factor.

Coinbase’s Q3 shareholder letter reads like a claim to become the first Everything Exchange: spot, derivatives (Coinbase Advanced, Deribit), payments (USDC, Coinbase Commerce, x402), launchpad (Echo), and a pipeline of new products distributed through Base. It’s one of the clearest signals that the market is moving toward consolidation at the application layer.

What is a Crypto Superapp?

For the purpose of this report, a crypto superapp isn’t a monolithic do-everything product built end-to-end by one company. It’s an aggregation layer: a unified interface that curates and integrates best-in-class protocols already available in open markets.

Their job is to compress most of a user’s onchain and financial life onto one surface, built around:

- One identity (wallets/accounts)

- One balance (majors, stablecoins, tokenized assets)

- One feed (a single interface for onchain actions)

Why Aggregation Wins

Aggregation has been the internet’s most valuable business model: companies that don’t own supply, but win by owning discovery, workflow, and distribution. The pattern shows up repeatedly:

- Internet aggregators: Amazon (marketplace aggregation), Meta (social/content aggregation).

- Mobile superapps: WeChat’s mini-program ecosystem; Grab’s expansion from ride-hailing into a multi-product platform.

- Fintech: Nubank, Revolut, Cash App – each bundling services to outcompete legacy banks by reducing friction.

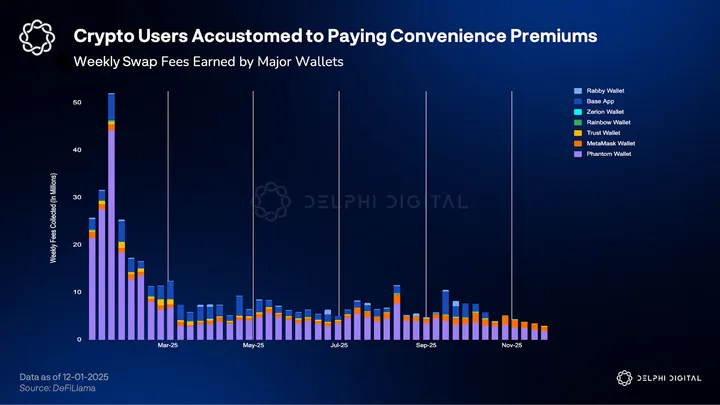

Different sectors, same outcome: users pay a steep convenience premium for fewer apps, fewer logins, fewer handoffs. Wallets and trading terminals raking in millions of dollars in fees proves that crypto users too aren’t opposed to paying additional fees for such convenience.

Different sectors, same outcome: users pay a steep convenience premium for fewer apps, fewer logins, fewer handoffs. Wallets and trading terminals raking in millions of dollars in fees proves that crypto users too aren’t opposed to paying additional fees for such convenience.

Integrate vs. Acquire

Fintech aggregation works, but it’s constrained by the cost of expanding on legacy infrastructure. Adding a new line of business usually means one of three slow, expensive paths:

- Build (years of licensing + R&D across jurisdictions)

- Acquire (e.g., Block buying Afterpay to gain BNPL capabilities)

- License-hunt (buying entities primarily for regulatory permissions)

Crypto overhauls the expansion economics: a superapp can add functionality by integrating a protocol, not buying a company. Basic integration advantages compared to fintech start compounding:

- Global, 24/7 liquidity by default. No market hours or T+1/T+2 settlement constraints.

There was a time when you couldn’t trade stocks on your phone. Imagine explaining to someone in 2035 that back in 2025, markets closed on weekends and holidays.

Tokenization will unlock 24/7 markets, and once people experience it, they’ll never go back.

It’s the same story…

— Vlad Tenev (@vladtenev) November 11, 2025

- Composability: Protocols share a global backend. Users can chain actions that would require legal contracts and long drawn partnerships in fintech e.g., borrow against tokenized T-bills, receive USDC, and deploy it into perps.

- Mini-app distribution: Crypto superapps can become the distribution layer, allowing 3rd party developers to build and share mini-apps within their ecosystems. Think Tencent’s Wechat strategy applied to financial services.

This is in line with a larger shift: as app-store gatekeeping weakens globally, distribution will expand beyond Apple/Google’s playstores and their high taxation of third party developers will clear the way for new app distribution channels. In that environment, embedding inside dominant surfaces (superapps) becomes a rational strategy for smaller apps.

Why now?

- Tech Maturity: Smart accounts, secure bridging and cheap L1, L2 blockspace have finally solved the UX and cost friction that stalled previous cycles.

- Regulatory Clarity: The shift from enforcement to clear frameworks [US (FIT21, GENIUS), EU (MiCA) and Asia (AGDM)] has de-risked the sector and invited institutional capital.

- Expanded Utility: The ecosystem has moved beyond pure speculation to offering a complete menu of actions from RWAs, yields, consumer credit to prediction markets.

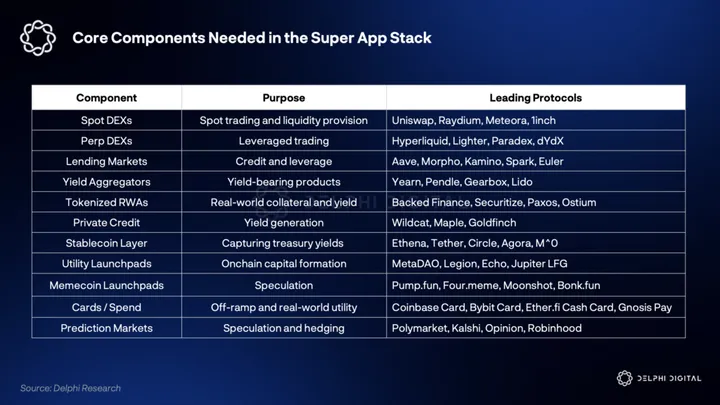

The Superapp Stack

The most bullish aspect of the crypto superapp thesis is that no single team has to build it all. The supply of these services is already permissionlessly available. The task now is to aggregate these modules into a single seamless interface.

Improvements at the individual component level are going to happen in a staggered manner with step function improvements coming infrequently. Some developments that we are looking forward in 2026 includes:

- Broader proliferation of Prop AMMs e.g. HumidFi, Tessera V, SolFi

- Liquidity Infrastructure like 1inch Aqua, Barter Superposition

- Orderbook based lending e.g. Avon

- Under collateralized lending and consumer credit e.g. 3Jane

- Growth of non-USD denominated stablecoin bring FX volumes onchain

- Non-custodial crypto cards embedded with DeFi yield for idle assets

- Launchpad auction mechanisms maturing for fairer launches e.g. Uniswap’s Continuous Clearing Auction, Doppler Multicurve

The GTM Battleground

Building a Superapp is not a one time event; no one can build everything at once. Success in the web2 world has proven time and again that it requires a team to identify a specific, high-retention wedge – a singular value prop that hooks a user base and then verticalizes aggressively from there.

We will dive into the forerunners and counter-positioned teams in the market to understand the path they are taking to realize this vision.

Coinbase

Coinbase is running multiple plays at once. On one flank it’s cementing itself as the institutional partner and custodian that Wall Street can work with. On the other it’s pushing hard into the onchain economy through Base, and building the crypto native social layer via The Base App.

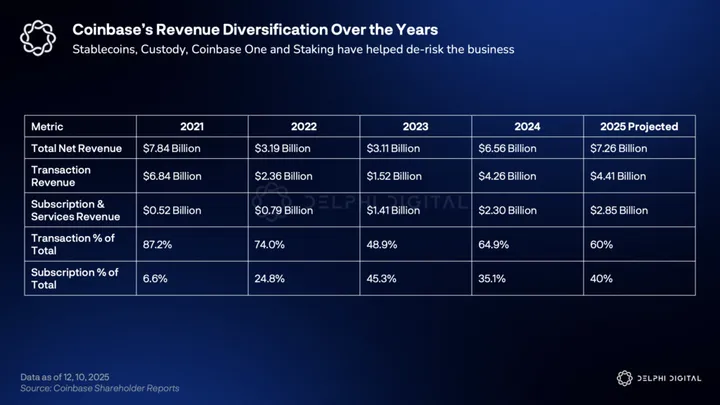

This duality explains the urgency of Coinbase’s 2024–2025 pivot. For most of its life, Coinbase’s P&L behaved like a leveraged instrument on Bitcoin: bull markets meant retail frenzy and transaction revenue; bear markets meant volumes evaporated. The last few years have been an explicit attempt to de-risk the business model. They’re doing this by turning Coinbase into a platform that earns when users trade, hold, stake, spend, and build.

Financial Diversification

The clearest proof is the revenue mix shift. In 2020, transaction revenue made up 96% of the top line. By late 2025, the profile looks meaningfully different and transaction revenues are projected at 60%, with Subscription & Services expanding to 40%.

This is how revenue diversification should happen. Coinbase has been productizing based on its balance sheet and monetizing all the plumbing: custody, yield, payments, stablecoins and infrastructure.

The Subscription and Services Business

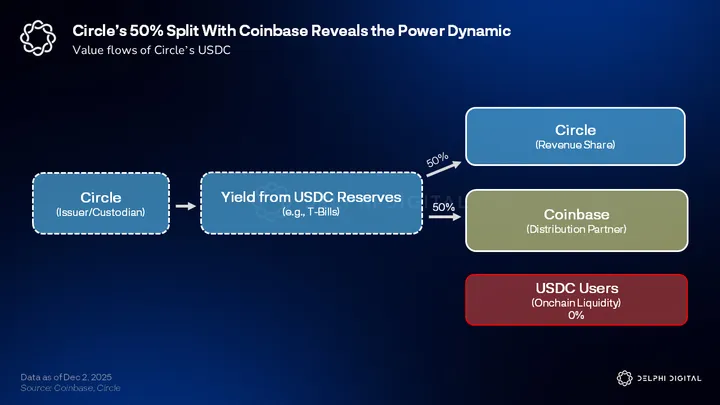

USDC

The most important non-exchange lever is stablecoin revenue, driven by Coinbase’s economics with Circle around USDC reserve yield. As USDC grows on Coinbase and spreads across DeFi via Base, Coinbase’s take expands with it.

In Q3 2025, stablecoin revenue hit $354.7M (+44% YoY) changing the shape of Coinbase’s previous cyclicality. Trading volumes can collapse in a bear market, but stablecoin balances tend to be stickier because many users park risk-off capital in stables on the exchange. Coinbase gets paid in both moods: risk-on speculation and risk-off cash management.

And if USDC keeps growing to become the default settlement currency across Coinbase, Base, and payment rails (like Tempo by Stripe), they get something crypto products rarely enjoy: an earnings floor that doesn’t require market euphoria.

Staking Rewards

The transition of Ethereum to Proof-of-Stake provided Coinbase with an opportunity to monetize its assets under custody (AUC). By offering Staking as a Service, holders of ETH, SOL, and other PoS assets can earn yield without managing complex validator infrastructure.

Whilst being a relatively smaller revenue driver, this is a valuable business line as it improves customer retention and allows Coinbase to monetise on top of user holdings. The growth in this segment is driven by institutions, who have become comfortable with holding crypto via Prime and are now seeking yield on idle assets. Coinbase’s ability to offer regulated, secured staking is a significant competitive advantage over decentralized protocols or offshore competitors.

Coinbase One

This is where Coinbase is trying to convert their problems (customer dissatisfaction and high trading fees) into a relationship product.

For a tiered monthly fee, users get fee relief on capped volume, boosted rewards, and priority support. They are reshaping user behavior by introducing the subscription plan. A subscription creates a sunk-cost effect: once users pay, they’re incentivized to consolidate activity and asset holdings on Coinbase to maximize value, starving competitors of volume.

This again dampens the most painful part of exchange economics: the lumpy dependence on retail trading spikes. Coinbase doesn’t need users to overtrade; it just needs them to stay subscribed now.

International Exchange and Derivatives

The final piece of the business diversification is the expansion into derivatives, with the launch of the Coinbase International Exchange and the Deribit acquisition. In the global crypto market, spot trading represents a small fraction of volume and derivatives account for up to 80% of volume. Historically, Coinbase gave way to other players like Binance, Bybit, OKX, Deribit to capitalize on this opportunity.

With the Deribit acquisition they’ve shown intention to grow this business line. With Deribit the orderflow is unique and perennial. Institutional hedging occurs throughout the market cycle, ensuring transaction revenue persists even when prices are falling.

The Superapp Buildout: Base L2 (OS) + The Base App (Interface)

With the financial diversification in place, Coinbase has started the next leg of their everything exchange vision. Superapps learn that having every feature matters less than being where users show up every day. If they own the daily interaction surface for users, they can route them to anything: CEX, DEX, loans, payments, yield, mini-apps without losing the relationship.

The Base App

The Base App has been designed to become this daily surface. It caters to a wider audience by becoming a social feed rather than a financial tool. And they’ve made the UX visibly simpler for a new user –

- Passkeys over seed phrases (biometric recovery)

- Sponsored transactions (paymasters) so users aren’t forced into buying ETH for gas

- Magic Spend for users to complete onchain actions with their Coinbase Exchange balances

The goal here is clearly to push the larger user funnel of the centralized exchange to come onchain to Base. And on Base, third party developers are building additional apps and experiences for users to get further immersed in the coinbase ecosystem.

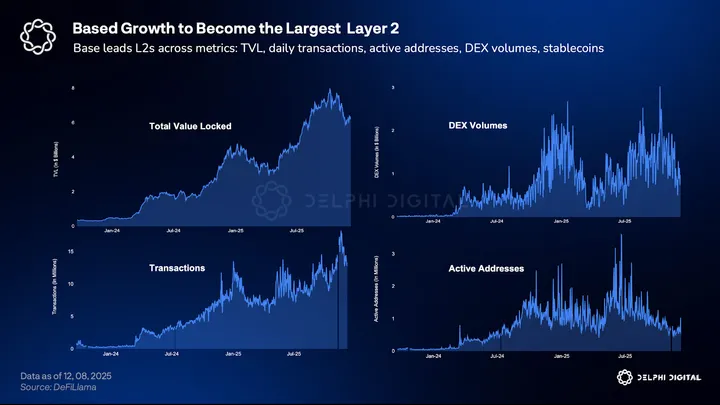

Base L2

If Base App is the interface, Base L2 is the operating system. The strategic choice to build an Ethereum-aligned rollup instead of a closed, proprietary chain has worked well. Coinbase gets to reap the benefits of the developer tooling and community while still capturing the economic benefits that come with being the dominant distribution surface.

Coinbase’s distribution power is visible in the growth of their Morpho loans product. Offering BTC backed loans for their users directly from the Coinbase App has grown Morpho markets on Base to issue over $905M in active loans. The flywheel on display is amazing: builders use coinbase’s strengths to grow products on Base and Coinbase will utilize this growing DeFi ecosystem to introduce new financial products and services in their superapp.

Base has been among the most vocal ecosystems to explore and support apps beyond DeFi, particularly emphasising on consumer crypto and payments. Crypto has had a tendency to alienate users with hyper-financialization. This is an attempt by Base to utilize the core competencies of crypto but while still catering to previously alienated users.

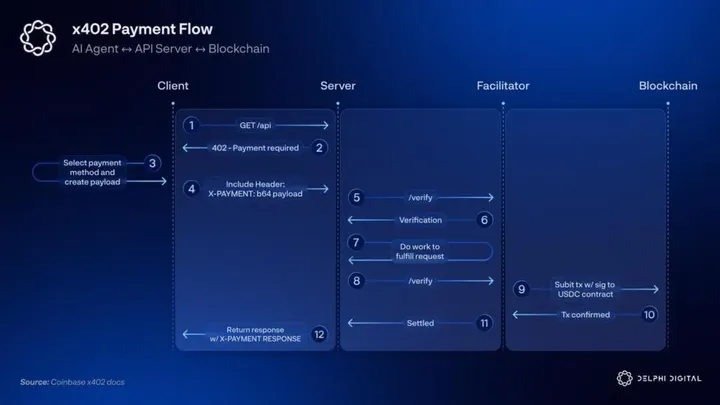

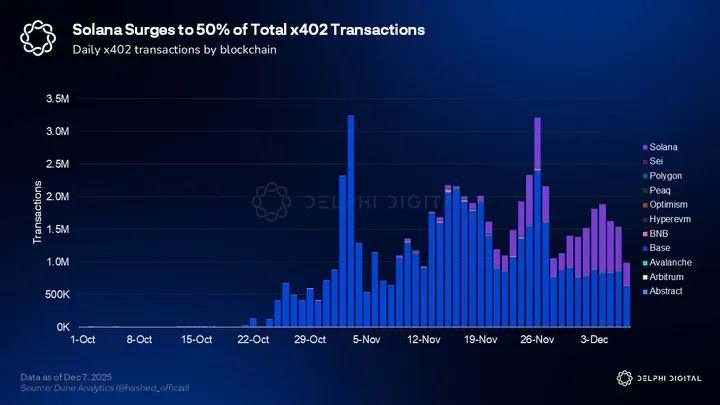

Coinbase should expect fierce competition from Stripe in the crypto payments category with the upcoming Tempo launch. To match with Stripe’s dominance of the payments category: Coinbase has been gearing up to provide agentic payment rails with x402.

Mergers & Acquisitions: Buying Missing Primitives

Every crypto superapp will take pages out of the Amazon playbook. Proven product categories will be either built inhouse or will be quickly acquired to maximize the revenue capture (The Amazon Basics model). Coinbase has completed a few strategic acquisitions recently:

- Deribit (May 2025 – For $2.9B): Brings in deep derivatives liquidity and institutional options dominance. Deribit also plugs into the International Exchange whilst capturing ~90% of the Bitcoin options open interest

- Echo (Oct 2025 – For $375M): Brings fundraising and asset issuance closer to Coinbase. An exchange’s lifeblood is new assets, and Echo moves Coinbase earlier in that lifecycle. Post acquisition, Coinbase hosted the biggest ICO of 2025 (Monad raising $187.5M)

Tying it Together

Coinbase over the last decade has cemented its position as the most trusted crypto exchange visible in their monopoly as the ETF asset custodian. They’ve focused on strengthening their global regulatory positioning by securing licenses in key jurisdictions: EU approvals through MiCA license, Singapore and Bermuda (for the International Exchange).

There’s still room for improvements in their current offerings: reduced fees, prompt customer support and a competitive listing strategy. And they have been addressing these problems slowly so that they can then focus on the future – The Everything Exchange

Coinbase has placed its bet – that the future winner won’t be the most decentralized system or the most centralized one. It’ll be the company that blends both without the seams showing.

- a WeChat-like surface in Base App,

- an open OS in Base,

- an NYSE-grade liquidity hub in Exchange + Deribit,

- a Institutional vault in Prime,

- a Membership program in Coinbase One that keeps users from wandering.

If it works, Coinbase graduates from exchange to financial infrastructure. Not because it wins a category, but because it wins the right to sit between everyone: traders and builders, stablecoins and RWAs, humans and agents. The moat Coinbase has started digging is a distribution-and-attention moat. And those are the ones that last.

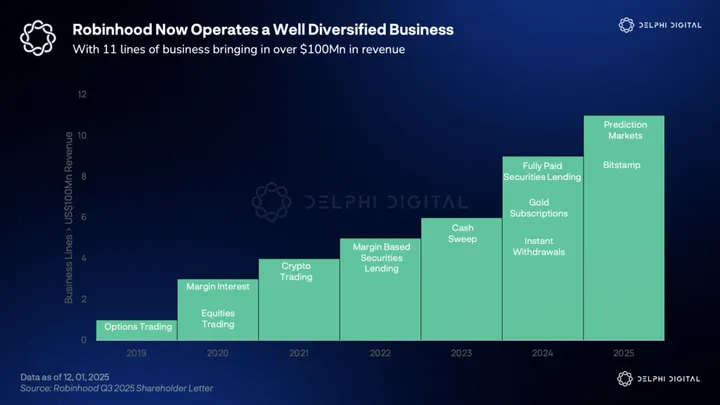

Robinhood

Robinhood is a beneficiary of a macro swing most fintechs only talk about: after a decade of unbundling (separate apps for trading, banking, crypto), the next era will be defined by rebundling as everyone realizes fragmentation strands capital. When funds are trapped behind settlement windows and app boundaries, users keep more money idle than they should.

Robinhood’s play is to centralize liquidity and maximize velocity of the money flowing in their system. Sell a stock, redeploy instantly, spend through a card, sweep cash into yield, or rotate into crypto without leaving the Robinhood app. It’s the superapp thesis in its simplest form: own the balance, own the behavior.

There’s also another tailwind no platform can ignore: the great wealth transfer. As assets move from baby boomers to a digital-native generation over the next two decades, Robinhood wants to be the on-ramp where that cohort manages their wealth. The signal is already visible in Robinhood’s balance sheet: Retirement AUC hit $24.2B in mid-2025, doubling YoY, proving the platform is graduating from a trading app to a wealth manager.

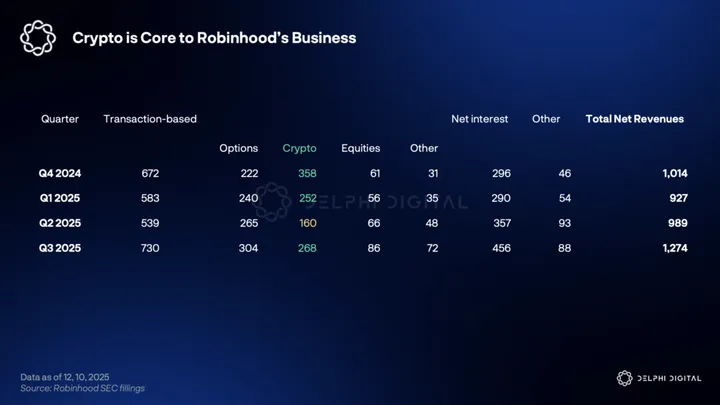

Robinhood already is a financial superapp by all accounts. Within less than half a decade they have moved away from a reliance on volatile retail trading revenue (PFOF).

Crypto has become comparable to their options transaction revenue and shows how crypto is no longer a side note but a major business line. And Robinhood’s crypto ambitions are going to be critical in their attempt to build the financial superapp.

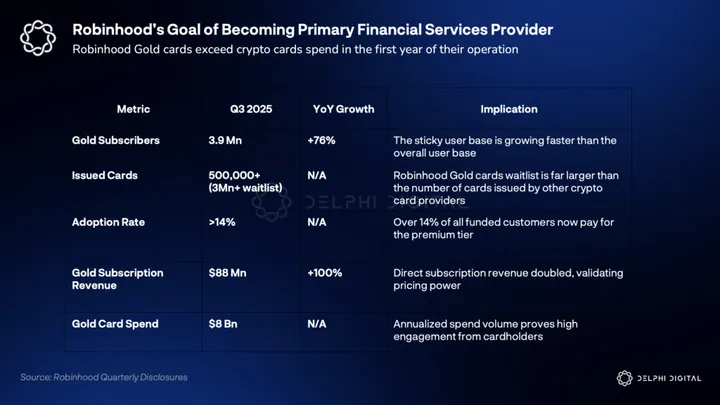

Robinhood Gold

If Coinbase’s flywheel starts with USDC yield, Robinhood’s starts with Gold. Robinhood Gold has evolved from a simple premium tier into an inescapable flywheel of value and lock in.

The 77% YoY growth in Gold subscribers is arguably one of the most critical metrics in their Q3 report. It proves their transition to a relationship bank is working. As part of the Gold flywheel, Robinhood uses Gold ($5/month or $60/year) as a loss leader to incentivize asset consolidation. The logic is simple:

- Create The Hook: Offer market-leading rates (3% Cash Back Card, 3% IRA Match, 3.5% interest on cash) that are mathematically irrational for a user not to take if they have significant assets.

- Lock-in Users: To keep these benefits, users must remain subscribed and keep assets on the platform (e.g., the 3% IRA match requires a 5-year hold).

The Gold Card also closes the loop on spending data. Robinhood now sees a user’s paycheck (Direct Deposit), their savings (Cash Sweep), their investments (Brokerage), and their daily spend (Credit Card). This in time will allow for superior credit underwriting compared to other banks.

The 3% IRA Match, 3% Cashback and 3.5% interest on cash deposits are risky and expensive customer acquisition costs (CAC). If the Fed cuts rates significantly in 2026, Robinhood’s Net Interest Income (NII) drops, but they could be locked into these high payouts.

Capturing the Prosumer

Given that Robinhood is currently in the lead to build the financial superapp, one major risk for them has been to reduce churn or graduation of most profitable users to other platforms like Charles Schwab or Coinbase Advanced. Robinhood’s solution to this is to build a trading venue for the Active Traders.

Robinhood Legend: Closing the Tooling Gap

Legend is a defensive moat: it gives serious users pro-grade workflows without forcing them into a different ecosystem. The most important feature is the platform continuity. Dynamic linking keeps mobile and desktop as one session, which matters when the app is trying to be the one surface for all user interactions.

Futures: Gateway to 24/7 Markets

The introduction of Futures (S&P 500, Oil, Gold) is a neat behavior modification tool. Futures trade 24 hours a day, 5 days a week. This product bridges the gap between the rigid NYSE schedule and the 24/7 crypto market, keeping users engaged with the app around the clock. Add the 60/40 tax treatment for products like Index options and they’re explicitly targeting higher-net-worth, higher-velocity traders.

Tokenization Play: Export Robinhood to the World

If Gold is the retention mechanism, tokenization is their expansion mechanism. Robinhood’s tokenized equities push (starting in Europe) is basically a play to bypass the friction of cross-border investing and compete with local incumbents (like Revolut) on access and simplicity. A fundamental rethinking of the product led them to issue assets as tokens which simultaneously appeals to the crypto-native audience too.

Market Breadth & Depth: They already offer over 400 US-listed companies and ETFs (e.g., Nvidia, Apple, Vanguard S&P 500) to EU customers. In a controversial move to drive adoption and hype, Robinhood offered tokenized shares of private companies like OpenAI and SpaceX, signaling a future where retail investors could access pre-IPO equity via tokens.

In Beta Phase

It is important to understand that the current iteration is akin to them testing the waters and building investor appetite. In its current form, users are trading derivatives that track the price, not the actual underlying stock.

Robinhood (via a SPV) holds the actual share of Apple or Tesla as a US custodian. They then mint a shadow token onchain that tracks the price 1:1. This model has its limitations:

- No Self-Custody: Users cannot withdraw these tokens to a non-custodial wallet yet.

- Trading Hours: Currently limited to 24/5 (closed on weekends), unlike true crypto markets.

- Counterparty Risk: Users currently hold IOU. If the entity becomes insolvent, the claim on the derivative can fail.

Robinhood’s stated endgame is to migrate these assets from a private database into a public L2 built on Arbitrum Orbit. This unlocks:

- True Instant Settlement: Moving to L2 enables Atomic Swaps. Trade settlement happens in the time it takes to produce a block, freeing up capital stuck in the T+1 settlement cycle.

- 24/7 Markets: A decoupling from the NYSE’s schedule allows trading to reflect real-world events (e.g., an earnings report or geopolitical event) instantly, regardless of time zone.

Scaling Distribution: Bitstamp

To go global quickly, Robinhood needed licenses and institutional-grade crypto infrastructure. The $200M Bitstamp acquisition (June 2025) is best understood as a regulatory shortcut to gain a footprint that would have taken years to assemble organically.

It also creates another line of business that most people will underweight: Bitstamp-as-a-Service, a white-label stack for banks and fintechs that want to offer crypto exposure without building it themselves.

Entering into more Crypto Profit centers

Stablecoin Issuance

Robinhood has taken note of the economics behind stablecoin issuance and Coinbase’s USDC revenue. USDG (Global Dollar Network) is Robinhood’s entry into this category. By co-creating this network with partners like Kraken, Galaxy, and Anchorage, Robinhood moves from a mere distributor to a co-issuer.

Instead of earning a small transaction fee on crypto purchases, Robinhood will now share in the Net Interest Income (NII) generated by the US Treasury reserves backing the USDG held by its users.

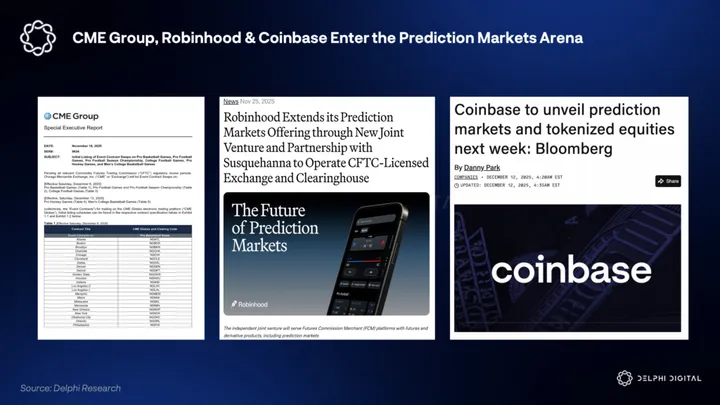

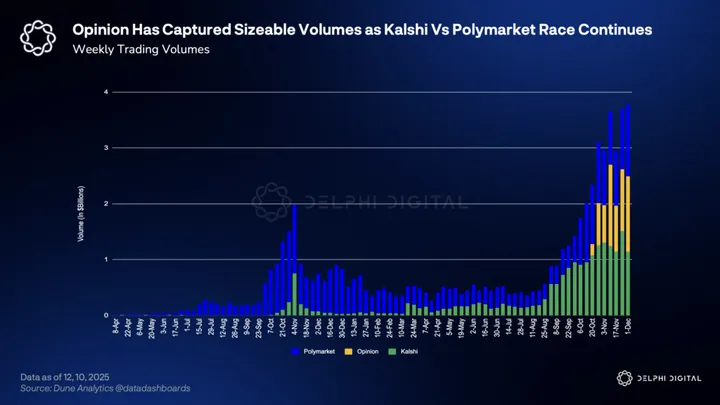

Prediction Markets

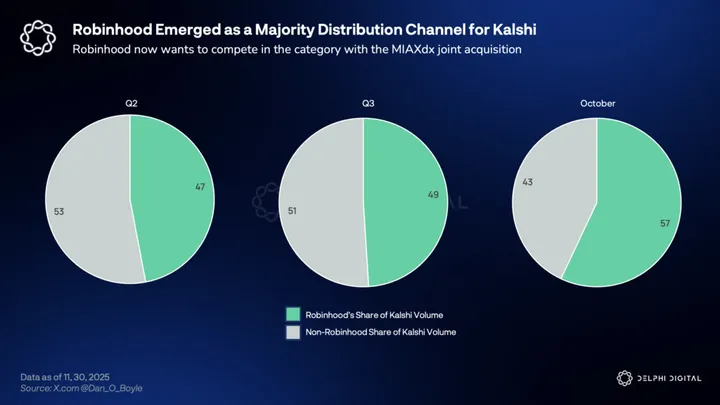

Robinhood was the earliest mainstream broker to treat prediction markets as an important product category. They started by routing event contracts through Kalshi, while Robinhood supplied what matters most: distribution. Estimates range from ~25–35% of Kalshi’s daily volume coming from Robinhood with an even higher share of volume in recent months.

Robinhood signaled back in October that they were looking for acquisition opportunities to vertically integrate and keep a larger share of the revenue. In November, they announced a joint venture with Susquehanna International Group (SIG) to acquire MIAXdx (a CFTC-licensed derivatives venue) to offer prediction markets natively.

Strategically, prediction markets fit Robinhood’s playbook perfectly: they’re high-frequency, culturally-driven, and complementary to both crypto’s 24/7 mindset and Robinhood’s push into derivatives.

Web3 Access: Connect, Wallet & The Embedded Future

Robinhood already has the building blocks to bring onchain access to their users:

- Connect is the on-ramp that lets users fund external wallets from their Robinhood balance. This allows them to monetize even when users leave the platform.

- Robinhood Wallet is the long-tail DEX interface (Using 0x, LI.FI integrations) for users who want assets beyond the limited listings.

The missing step is obvious: bring these into the main app with embedded self-custody. If Robinhood can make onchain feel like a normal tab within the app rather than a separate product, its superapp surface extends across TradFi and DeFi.

Robinhood Social

History shows that some of the most successful superapps achieved scale by adding financial interactions on top of a social layer. At the Hood Summit 2025, they announced Robinhood Social, a verified social feed for traders to be launched in 2026. Robinhood Social will have traders posting alongside verified trades and P&L cards to build a trader/investor centric social media.

We believe it will be monumentally harder for Robinhood to build a social feature with meaningful activity and retention. Layering finance on top of a social layer is very different from adding social layers on a predominantly consumer finance application.

But all in all, Robinhood sits in the Goldilocks zone: Regulated enough to be trusted by Boomers and crypto skeptics, but agile enough to offer crypto to the new investor cohort. Robinhood has effectively blurred the lines between a neobank, a brokerage, and a crypto exchange. The strategy is defined by the convergence of three powerful engines: Gold (the data-rich spending layer), Legend (the active trader retention moat), and the Arbitrum Layer 2 for tokenization.

Binance

Binance didn’t wake up one day and decide to build a superapp. It became one the same way Amazon, Wechat did: by owning the highest-frequency behavior first (trading) and then quietly swallowing adjacent loops: payments, savings, discovery, onchain access, and institutional plumbing. Binance stopped being an exchange and started being many a user’s default crypto home screen.

If Coinbase’s superapp story is convergence (CEX + onchain OS) and Robinhood’s is rebundling (one balance + product velocity), Binance’s story is that of scale with over 270M registered users. Binance has consistently been the volume leader of the crypto industry.

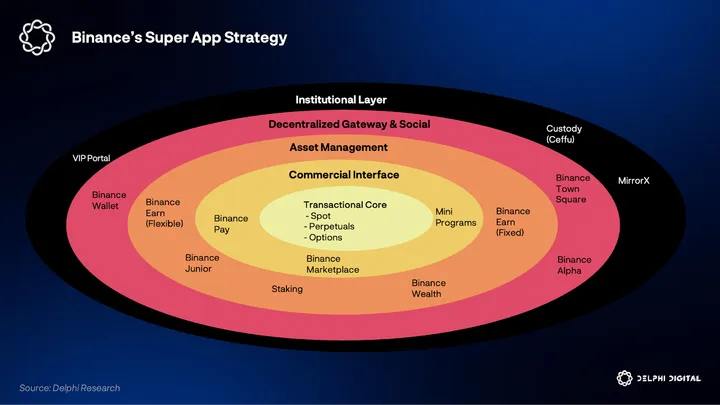

Their super app offering can broadly be broken into 5 parts:

- The Transactional Core: The centralized exchange (CEX) infrastructure.

- The Commercial Interface: Payments, the Marketplace, and Mini Programs.

- The Asset Management Suite: Wealth, Earn, and Staking.

- The Decentralized Gateway: The Web3 Wallet and Alpha platform.

- The Institutional Layer: Custody, Settlement, and VIP services.

The Transactional Core

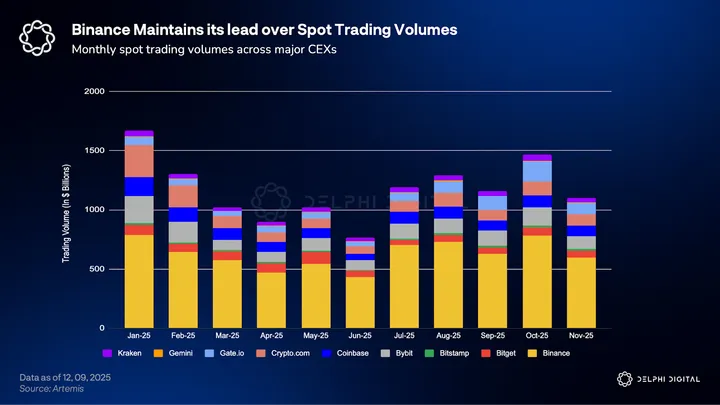

Binance’s superapp starts where the money starts: the exchange. Their scale advantage is the moat: liquidity attracts traders, traders attract liquidity, and the flywheel continues. The core exchange remains Binance’s primary revenue source, facilitating $7.3 trillion of volume in 2024.

Spot

Spot is the mainstream on-ramp and still the largest first action for most users (~26% of users utilize spot trading). After leading USD-denominated liquidity, Binance is now pushing into local fiat pairs (BRL/TRY/EUR) to deepen its global dominance.

Under the hood, Binance is also segmenting UX and building features to retain trading volumes for different user personas:

- Convert (RFQ-style) for users who want just complete a trade

- Order-splitting tools for size without slippage

- Bots + Copy trading as the SocialFi layer attached to the Binance markets

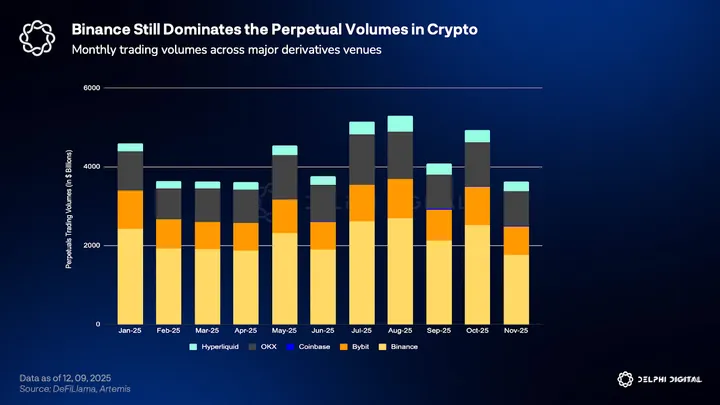

Derivatives

Perps and options are where Binance becomes sticky for power users and where volumes can exist outside of a bull market too as institutions need to hedge their exposures. While their options footprint is small, Binance dominates the perpetual futures category accounting for over 33% of open interest for both Bitcoin and Ethereum.

P2P: Shadow Banking infrastructure

This is the part most people underestimate. In markets where card rails are weak, bank access is uneven, or capital controls are real, Binance P2P has become essential infrastructure.

- Escrow-based matching across hundreds of local payment methods

- A professional merchant tier (P2Pro) that effectively behaves like a distributed FX desk

This is the first place Binance starts acting like a bank without calling itself one.

The Commercial Interface

If the exchange is the engine, Pay is the daily habit builder. Trading is episodic, but payments are a daily necessity. With this offering, Binance is trying to move from a speculation venue to spending. Their numbers tell an impressive story:

- $250B+ Pay volume within 5 years

- 45M+ active Pay users

- 20M+ merchants after a massive merchant network push

- Digital dollar wallet: 98% of B2C payments occur in stablecoins

The most strategic part is the integration with national rails [Pix (Brasil), Bhutan’s tourism platform]. That’s how Pay stops being a crypto feature and becomes part of users’ normal day to day life.

Marketplace and Mini Programs

Binance’s Asian roots are visible in how they’ve borrowed elements from Wechat’s mini-apps into Binance Marketplace. Marketplace is an early sketch of an app-store model: travel, rides, top-ups, gift cards. Users already hold stablecoin on Binance, this gives them places to spend it inside the app.

The success story within their mini-app experiment has been the Travala integration. 8.5% of all Travala transactions (gross volume: $103M) were initiated by Binance app users in 2024. The discovery and variety in Marketplace is lacking and thus the ecosystem feels secondary to the Pay push with most mini-apps offering just gift vouchers.

This is where the Binance Card comes into the picture. It’s the bridge to offline spending while the mini-program layer matures. Binance offers capped 2% cashback on transactions via their card. Although, the card is only available in Brasil, Peru and Colombia for now with spending data sparsely available.

The Asset Management Suite

To capture the revenue potential of a user’s idle balances, Binance has built a series of asset management tools. This pillar is designed to retain Assets Under Management (AUM) by offering yield. The data available for the usage of these features has been limited, but it helps us understand the breadth of financial services that Binance is able to offer within a single app.

Binance Earn

Binance Earn is the savings account of the ecosystem and the second most popular product after Spot trading (25.34% of users). TVL in Binance Earn grew by 144% in 2024.

Staking

Binance has moved aggressively into onchain staking services.

- ETH Staking: A managed service for Ethereum validator staking that has attracted deposits worth $11.1B (3.2M ETH staked).

- SOL Staking: In 2024, Binance introduced liquid staked BNSOL. While far smaller than the TVL in ETH staking, Solana staking has also been able to bring in over $1.1B in deposits.

Binance Wealth

Binance Wealth is Binance recognizing that its top users are aging into HNWIs. Binance is building private banking UX for crypto-native wealth: with portfolio management, onboarding/KYC workflows, and tools designed for capital allocators.

This move signals Binance’s intent to compete with traditional private banks (like JP Morgan) and Robinhood for the asset management category. It provides the infrastructure for traditional wealth managers to offer crypto exposure to their clients without losing custody of the relationship.

Loans and Credit

Overcollateralized borrowing is the logical extension: if users already hold assets and want liquidity without selling, Binance became the easiest place to do that. They started offering fixed-rate loans for borrowers, addressing a major pain point of DeFi borrowing.

The Decentralized Gateway

Binance was early to realize that onchain activity is where new attention centers are formed. Instead of fighting it, it’s trying to own that gateway too. The Web3 wallet integration matters because it collapses the jump from: from Binance → to external wallet → to DeFi

The Binance wallet product is further pushed via campaigns like Binance Alpha. They used the fastest way to acquire users – by routing them toward free money (airdrops, anticipated TGEs, early access). If users believe Alpha is where the first look for new opportunities happens, they will move parts of their onchain life into Binance’s wallet.

- 18 Alpha tokens later listed on Binance Spot

- Users got access to TGEs at better entry prices compared to day-1 spot closing price

- Binance wallet users have received up to 8 airdrops

Wallet adoption becomes cheaper than paid marketing. This is Binance’s distribution edge expressed in the most Binance way possible.

Institutional Layer

Binance doesn’t want to be the superapp that only serves retail. The whales and institutional market brings liquidity, tighter spreads, and volume. Post-FTX, custody trust became the core constraint and Binance built around it.

- Ceffu as the secure custody solution

- MirrorX allows Ceffu assets to be mirrored onto Binance Exchange for trading

Reducing the exchange’s counterparty risk perception helps them draw in higher institutional participation. And just like Robinhood and Bitstamp, Binance is also pushing Crypto-as-a-Service: selling liquidity and infrastructure to tradfi institutions that want crypto exposure without building the rails.

Binance’s flywheel is simple and brutally efficient

Liquidity pulls users in → Derivatives + Earn keep assets parked → Pay + Card to create daily utility → Wallet + Alpha capture onchain activity → the resulting flow feeds back into exchange volume, listings, and liquidity.

Binance doesn’t need to convince users to adopt a superapp. It needs to keep behaving like the place where every onchain action is the easiest to execute. The risks associated with such scale are significant. Regulatory compliance, reputational overhang, limited market adoption in the west and the complexity of shipping five apps worth of features inside one container. But on pure product mechanics, Binance is one of the only players that can credibly claim it’s already running a crypto superapp in production and at global scale.

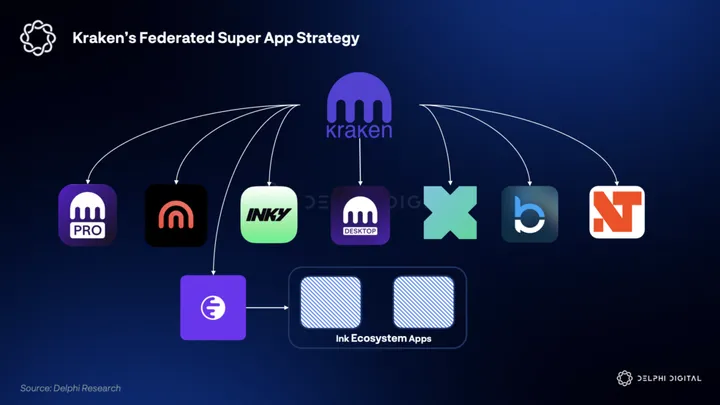

Kraken

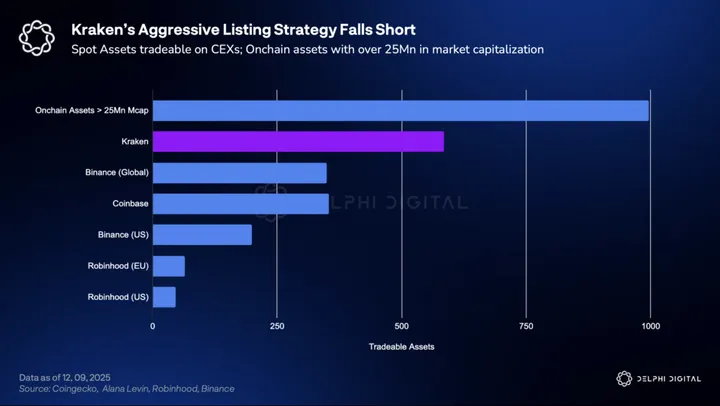

Kraken’s answer to building the super app is unique as they’re not building a single cluttered everything-app. Their plan is to unbundle the interface while rebundling the infrastructure. Kraken is aiming to counterposition in each category they operate in: starting with their aggressive listing strategy.

Instead of forcing every user into one UI, Kraken is building a constellation of apps. Kraken Pro, Wallet, Inky, and Krak are all tied together by the same identity, liquidity, custody, and (soon) a platform layer in Ink. It’s a new superapp strategy: specialized surfaces, shared rails.

In recent times, the centralized exchange (CEX) model has been under significant pressure to adapt. The traditional fee-based revenue model, slow listing strategy and reliance on cyclical retail trading volumes, is becoming increasingly difficult to operate under.

Closing the Growth Gap

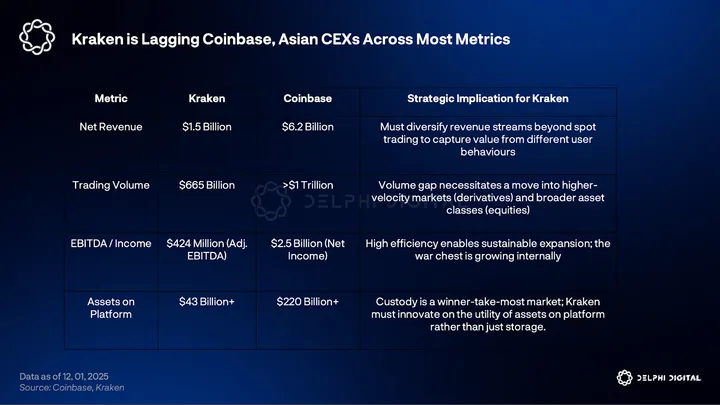

Kraken is large and profitable, but a comparison with Coinbase reveals the problem: it’s not yet the default surface at Coinbase scale. In 2024, Kraken did $1.5B net revenue on $665B volume, with $424M adj. EBITDA. A strong business, but still a fraction of the size compared to the other CEXs.

Kraken has a self-funded war chest that lets them buy and build capabilities without needing to chase fee wars. But the implication is simple: Kraken can’t bridge the gap to other CEXs without expanding into higher-velocity markets or growing new product categories.

To fuel this growth and expansion, Kraken recently raised $800 million at a $20 billion valuation before its planned IPO in 2026. This raise represents a vote of confidence in Kraken’s upcoming plans from institutions like Citadel Securities, which contributed a $200 million strategic investment.

The Unbundled Superapp

Kraken’s unique insight is that the attempts to replicate superapps in Western markets has often resulted in cluttered applications that try to do too much and serve no one effectively. Rather than forcing a high-frequency trader, a memecoin speculator, and a remittance user into a single interface, Kraken is unbundling its services into distinct apps while rebundling them at the infrastructure layer.

The Constellation of Apps

Kraken’s ecosystem is now segmented into use-case specific containers. Each app targets a distinct user profile and behavioral loop.

Inky

Inky’s swipe UX isn’t a gimmick, it’s a funnel redesign. It moves the user’s job from analysis to discovery, abstracts away chain complexity, and turns the memecoin game into a simple low stakes acquisition. If one believes the next retail trading wave looks more like TikTok than Bloomberg, Inky is Kraken’s attempt to grab a slice of that future.

It acknowledges that for a new generation of users, finance is entertainment.

Krak

Krak is the functional opposite of Inky: it targets the payments category. The pitch combines remittances and global transfers with a stablecoin balance that behaves like a high-yield checking account. The integration of USDG and an advertised 4.1% APY is key because it creates a reason to keep balances parked, not just pass through.

Crucially, Krak closes the loop on real-world utility with a Mastercard debit card, allowing users to spend their yield or crypto balances instantly with 0% foreign exchange fees and up to 1% cashback. By bridging high-yield savings with instant spending, the app aims to capture a significant share of the $800 billion global remittance market across 160+ countries. For a user looking at crypto purely as a payments layer, this offers a far simpler alternative to a complex super app.

Ink

If the mobile apps are the specialized interfaces, Ink is the operating system (OS) that underpins the entire App Store vision. Ink is Kraken’s layer 2 built on the OP Stack underpinning the shift from being a “store” (selling crypto) to a “platform” (hosting crypto businesses).

The team envisions Ink as an environment where third-party developers build the applications that Kraken chooses not to build itself. Kraken can effectively act as the trusted gatekeeper: like Apple curating the app store.

Developers building on Ink gain access to Kraken’s distribution to over 10M+ verified users. Kraken can feature trusted dApps within its Wallet or Main App, effectively funneling massive liquidity to partner protocols. They want Ink to become a top venue for the trading of tokenized stocks and the next acquisition gives them a headstart in the category.

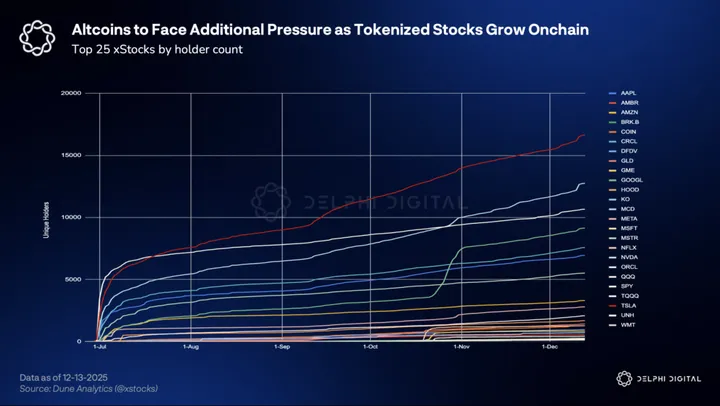

xStocks

Kraken very recently acquired Backed Finance, the issuer behind xStocks. It is among the most used tokenized equity frameworks and positions the company to accelerate issuance, trading, and settlement across global markets. We believe this acquisition positions Kraken much further than most of their competitors in the tokenization space.

xStocks are structurally better than many other tokenized stock offerings as:

- Backed 1:1 by underlying shares held in regulated custody

- Withdrawable to self-custody: this is the unlock Robinhood’s early structure doesn’t offer. Once equity tokens can leave the venue, they can become collateral, liquidity, and building blocks

Over $180M of tokenized stocks have been issued via the platform across Ethereum and Solana with $400M in DEX trading volume. Early behavior suggests that people are utilising these as investment instruments rather than a trading instrument.

NinjaTrader Acquisition and Entry into TradFi

Kraken’s acquisition of NinjaTrader for $1.5B shows that Kraken thinks a financial super app needs to expand beyond crypto. NinjaTrader is a retail futures brokerage in the US, holding a Futures Commission Merchant (FCM) license with the CFTC. Acquiring an FCM allows Kraken to offer regulated futures products in the US.

This acquisition instantly diversifies Kraken’s revenue. Even if a crypto bear market freezes volumes, NinjaTrader provides steady income from traditional futures markets (oil, gold, indices), smoothing out Kraken’s earnings volatility.

Breakout (Prop Trading)

Even after achieving product and feature parity, Kraken is in a competitively difficult position compared to other CEXs. Thus they need to be operating in categories where other exchanges are not present.

They recently acquired Breakout: a crypto prop trading platform. Unlike a standard exchange where users trade their own money, a prop trading platform allows qualified traders to trade the firm’s capital. Breakout uses an evaluation-based model where traders pay a fee to take a test to prove they are skilled and disciplined. On passing the evaluation, traders get a funded account with $200k (using Kraken’s capital) and can keep up to 90% of the profits they generate.

Kraken plans to integrate Breakout’s features directly into Kraken Pro, creating a seamless experience where one can eventually access funded trading directly from the main Kraken interface. This is a part of the push to bring up & coming traders to choose Kraken as their go to trading platform.

Kraken’s Contrarian Bet

Most of Kraken’s recent moves show how they are trying to counter position in each product category with Inky (memes), Krak (payments) and Breakout (prop-trading). For categories where Kraken isn’t present, they are partnering with best-in-class providers rather than building from scratch.

The Legion partnership (Kraken Launch) is the proof of this playbook: rather than building another launchpad, Kraken is acting as the distribution layer for Legion’s onchain reputation engine. This effectively federates the ICO vertical to a partner capable of filtering for merit-based users (checking GitHub commits, onchain history and social clout) while Kraken keeps the user experience compliant and seamless.

Their superapp bet is to launch:

- Many surfaces that appeal to different personas (Trader, Explorer, Spender, Speculator)

- With One spine (identity, liquidity, custody) that keeps users inside the ecosystem even as they move between behaviors

- One platform layer (Ink) that lets Kraken scale to new products via external builders

If Coinbase is building a converged mega-surface and Binance is already a large applications container, Kraken is trying to win with federation: a cleaner UX that has worked better in the US combined with an app-store style platform strategy.

X (Formerly Twitter)

Putting X in the superapp conversation is not a longshot as Elon has been vocal about building it up to become the Everything App. Unlike Coinbase, Binance, or Robinhood that have deep financial stacks, X is still at the “should they? can they?” stage.

𝕏 just rolled out an entire new communications stack with encrypted messages, audio/video calls and file transfer.

𝕏 Money comes out soon.

Join us if you want to build cool products.

𝕏 will be the everything app. https://t.co/7DyLNEgNnw

— Elon Musk (@elonmusk) November 13, 2025

But the potential is undeniable: crypto culture lives on X. The most valuable distribution surface for crypto ideas, narratives, and coordination is already there. If X ever turns that attention towards native financial rails, it doesn’t need to build everything. It just needs to make moving and deploying money as native as posting.

The WeChat of the West dream has been floating around tech circles for a decade. What’s changed is that for X, the pivot starts to look less like ambition and more like business necessity.

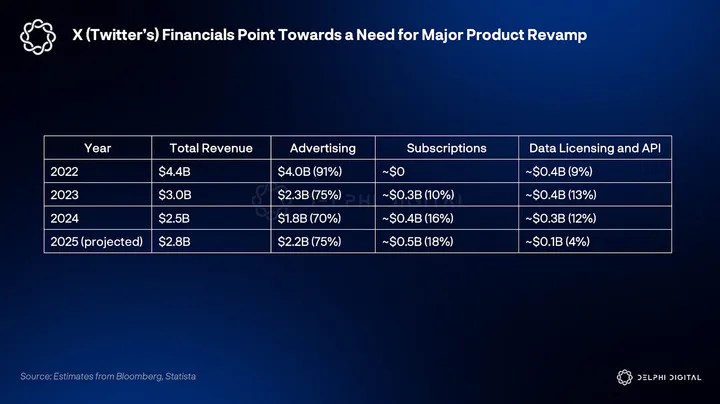

Post-acquisition, the revenue mix took a hit as ad revenue declined sharply from prior highs. Subscription revenue is growing but not enough to fill the gap yet. Layer in the cost of building and running frontier AI (xAI) and we get the real motivation: X needs high-margin, low-lift revenue streams that scales with usage. Financial services fit that pattern better than most categories.

If X converts attention into transactions, it will be able to carve out new revenue streams that it needs.

Trojan Horse Rollout: Payments First, Crypto Second

Phase 1

The credible path for X is to ship a boring Fiat wallet and then quietly expand what that wallet can do. The X Money route is the sensible trojan horse as X has already acquired money transmitter licenses across 38 states in the US. They can start with P2P fiat transfers and add Venmo-like utility within X as soon as they acquire the remainder of these licenses.

X is already working with Visa to make this a reality with instant funding to X Wallet via Visa Direct. Users will be able to connect to Visa debit cards for P2P payments. Once the wallet infrastructure is live, X can activate its latent advantage in phase two by combining payments and social media.

Phase 2

Once money starts moving natively on the timeline, the floodgates open. They can enable and create SocialFi behaviors that feel clunky on other platforms.

Imagine a seamless version of Solana Blinks, where swapping into a trending coin, or betting on a prediction market happens directly as a response to a tweet – no popup windows, no wallet connection. Creators could move beyond receiving tips and subscription payments to new Proof of Engagement models, where followers earn micro-rewards for amplifying quality content.

X could even offer low-risk DeFi yields on idle cash balances. Instead of money sitting dead in a wallet, it could auto-route to treasuries or stablecoin yield protocols, effectively becoming a high-yield savings account that you can tweet from.

Conclusion

X is nowhere close to the depth of the other players we’ve discussed in this report. But as everyone knows, Elon and team are exceptional operators capable of building and executing at breakneck speeds once the decision to pursue a new vision has been made.

Adding limited crypto functionality to boost social features is the logical starting point. YouTube is already dipping its toes in the water alongside PayPal, but X’s entry will be far more impactful because the crypto community already lives here.

X is the wildcard. If they do pull the trigger, we can’t wait to see what happens in 2026. While the forerunners covered above have secured a headstart, the landscape is far from settled. A diverse cohort ranging from native DeFi teams to ambitious new networks like Worldcoin are actively converging on this thesis. We believe the race to build “The ONE Interface” will be one of the defining narratives of 2026.

SocialFi Is the New Frontier

There are two secular trends emerging in 2025: trading is being socialized while social media is being financialized. These trends loosely coalesce under the SocialFi umbrella.

The social trading trend was jumpstarted by Roaring Kitty’s Gamestop call in 2021. Internet creator culture has continued to grow and naturally extends to finance. Two of the bigger financial memes over the past few years- Pelosi Tracker and Inverse Cramer, now have copytrader indexes via Autopilot.

This behavior has manifested in crypto through copy-trader products and social trading apps like Fomo. The other side is the financialization of social media.

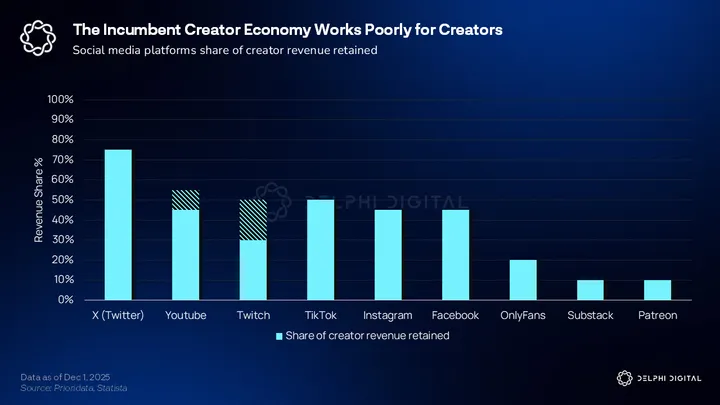

The creator economy is a massive ~$320B industry. The internet is usurping television as the premier information arena, in the same way television took over radio and newspaper. The COVID lockdowns accelerated the prominence of influencers. Entirely new forms of content have established markets now. Watching influencers react to content replaces watching with friends. There are async reality shows filmed by creator groups, etc. Internet-native influencers often emerge out of nowhere, wielding massive power. Boomers are late and they are scrambling. They haven’t achieved a sustainable model and time is running out.

Social media largely runs on ads. Even still, the Twitter model and streaming model are treading water.

Twitter was struggling before and after Elon took over. xAI now buoys its valuation. Bluesky is subsidized by VC money and has no model. Twitch is owned by Amazon, and while not individually profitable, it is hard to quantify the broader enterprise value it brings. Kick does not run ads and is subsidized by Stake. Vine infamously shut down due to its inability to monetize.

YouTube, TikTok, Instagram, and Facebook ‘work’ in the sense that they are profitable businesses with network effects, but they fail in achieving alignment with creators.

Many creators shift to running their own ads through sponsored content, bypassing the web2 ad infra, gaining control over the ads and earning more. This is in some ways a worse experience for users, who are less immersed in the content and cannot pay to remove this.

The alignment problem has prompted a shift in attitude from incumbents and an opportunity for crypto to infiltrate.

Base has been pushing the idea of the creator economy so hard that they seem to won it, but this is a real phenomenon that the major players are positioning for. Instagram has an entire web page dedicated to helping creators monetize their audiences, using a lot of the same buzzwords. Legacy powers know they must adapt and work with creators or they will lose their position. There is a fundamental incentive alignment issue with Web2, preventing them from executing on this effectively. Crypto is very well-positioned here.

fomo

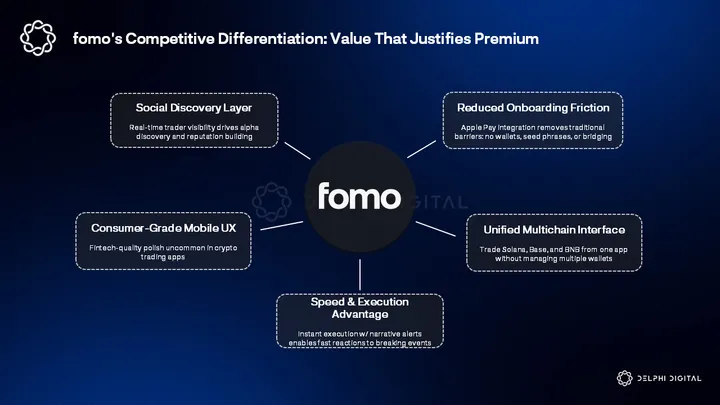

fomo represents another attempt to modernize onchain trading, but with a clear emphasis on delivering a Robinhood-level mobile experience rather than relying on crypto-native workflows. fomo abstracts away nearly all of the traditional friction that makes onchain trading with any real edge difficult.

Where Pump’s core business remains anchored to prebonded memecoin trading on Solana, with its expansion efforts tied to the Padre acquisition and its broader streaming vision, fomo has intentionally moved toward a more general purpose, chain-agnostic trading experience. If the team succeeds, fomo could meaningfully expand the pie by bringing a much wider retail audience into onchain speculation in the same way Robinhood pulled a new generation into equities.

Thrilled to announce our Series A investment in fomo. This remarkable team led by @PaulErlanger and @pseudosey have a clear vision to make digital assets accessible to consumers by abstracting away all the technical complexity. And their growth on all metrics is exceptional. https://t.co/DyUWchDwwW

— Chetan Puttagunta (@chetanp) November 6, 2025

fomo’s team are ex dYdX and ex Uniswap, and recently raised a seventeen million dollar round led by Benchmark. Benchmark is not a crypto-native investor, which makes the conviction here particularly high signal given their track record in traditional tech venture.

The product reflects that pedigree. The app is aggressively mobile first and is, in my opinion, the most polished trading experience in the category. It feels fluid, intuitive, and genuinely consumer friendly in a way that is rare in crypto.

The company launched in May, and what stands out is that its earliest users have been crypto natives. These are traders who do not need abstraction and would normally avoid paying higher fees than what is possible with onchain execution. Yet, they still choose fomo because the mobile UX, discovery tools, and social element combine into a meaningful perceived edge, or enjoyable experience, even for traders who naturally optimize for the lowest-fee, fastest onchain paths.

That dynamic makes the early traction especially meaningful given the product has not yet reached the broader retail audience it is designed to cater towards

For a long time if you traded onchain, you had 100 wallets or trading bot terminals with money on every chain and managed them manually

fomo has completely solved this wallet logistics nightmare for the average retard. You can buy and sell instantly on any chain

Hyperliquid

— Sisyphus (@0xSisyphus) November 11, 2025

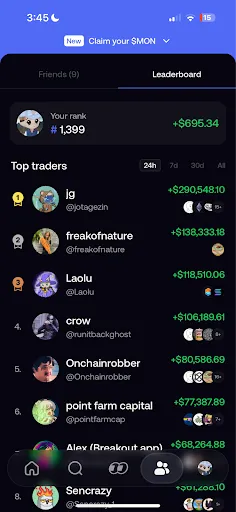

The social context is a major part of fomo’s appeal. Users can see friends’ PnLs, receive alerts when people they follow buy or sell, read or share trade theses, and compete for top spots on leaderboards. The result is an experience that is fun, addictive, and socially reinforcing.

There is also a practical advantage. Having capital on fomo is often +EV even with the 0.5% fee, because the combination of alerts, discovery, and instantaneous execution meaningfully improves reaction speed. And compared to other retail-friendly surfaces, fomo is actually cheaper. Most onchain terminals and Telegram bots charge 0.85–1%, Phantom’s in-app swap is 0.85%, and Moonshot ranges from 1–2.5%. On top of that, trading through fomo on Base, BNB, and Monad has been completely free for users so far.

The edge is most obvious during real time market events where convenience and speed matter more than marginal fees. Users do not need to bridge, manage slippage, juggle idle balances on multiple chains, or sit at a computer to react to headlines. Everything happens through a mobile interface that lets them trade instantly when a narrative breaks.

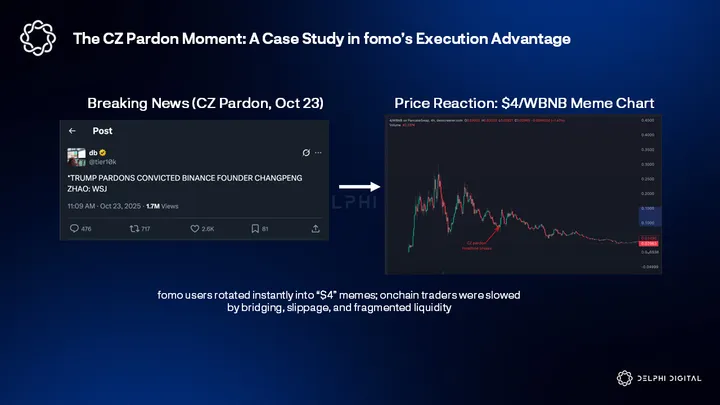

For example, during fast moving headline driven moments like the recent CZ pardon news, a fomo user could immediately rotate into the leading CZ related memes (like “$4”) on BNB with almost no friction. They do not need to have funds already sitting on BNB, they do not need to bridge, and they do not need to be at a computer to manage slippage or swap through multiple steps.

A trader relying on traditional onchain routes has a much higher bar, and those extra minutes can easily cost them during a moment when the market is still digesting the news. On fomo, users also see in real time what top traders in their network are buying through alerts and wallet tracking. Moments like this highlight why fomo can win not only with retail, but also why its beginning to attract experienced crypto natives.

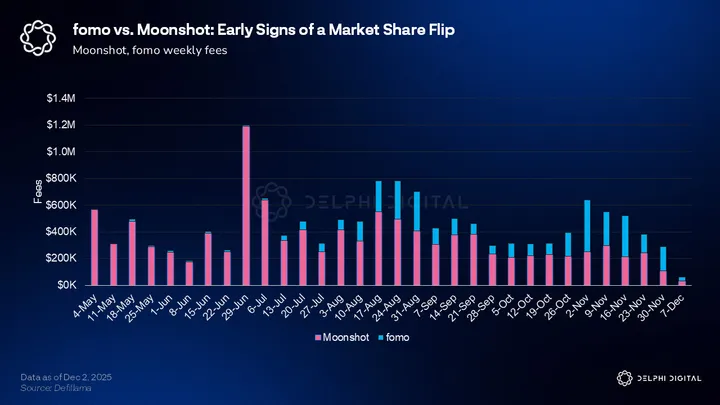

Moonshot is another useful comparison point. It sits in a similar mobile forward niche and was eventually acquired by Jupiter, but its trajectory has diverged meaningfully from fomo’s.

Moonshot reached a much higher peak during the Trump memecoin spike, generating nearly thirty five million dollars in fees in January 2025, but that performance was heavily timing driven. It benefited from a hyper concentrated retail moment and a market structure that no longer exists. Since then, revenue has declined steadily throughout the year, falling to roughly one million dollars in November.

Moonshot also continues to lag in listing newly launched tokens. Both platforms require vetting before pairs go live, but Moonshot’s slower approval and listing cadence makes it far less useful during fast moving meme cycles where early flow and speed matter most. The difference now shows up directly in the numbers. Moonshot still holds the higher historical peak, but its revenue has trended downward since while fomo’s has consistently risen. In November, for the first time, fomo generated more monthly fees than Moonshot, despite being a much younger product and charging far lower fees.

On Solana alone, fomo’s volume now runs roughly five times higher than Moonshot’s; across Base and BNB that gap expands closer to 10x. Moonshot also lacks the social layer that has made fomo so sticky for crypto natives, which further limits its ability to recapture momentum.

fomo’s execution and product quality look materially stronger. It simply feels like the better product. The ceiling is also likely higher: if fomo succeeds in capturing non crypto users it could meaningfully surpass the outcome Moonshot achieved before its acquisition.

Looking ahead to 2026, fomo’s model could extend well beyond memecoins. The core strengths of the product, including mobile native execution, social discovery, and a simplified UX, translate naturally into new verticals. RWAs, synthetic assets, leverage products, and even tokenized equities fit cleanly into the existing interface. Given the team’s background at dYdX and Uniswap, it would not be surprising to see fomo introduce a light perps product or other forms of leverage. The combination of mobile convenience and social signals could make these categories far more accessible to casual users than anything currently available.

fomo may look like a crypto trading app but that’s shortsighted

fomo is the the fist future proof trading application because it’s built on crypto rails

as everything moves on chain, everything will be available on fomo. watch closely as the incumbents try to catchup

— Paul (@PaulErlanger) October 23, 2025

More broadly, the universe of onchain assets is set to expand meaningfully over the next few years. As more assets become tradable onchain the surface area for mobile-first trading will grow alongside it. In that environment, fomo is structurally well positioned. The team can ship faster, iterate more aggressively, and respond to new narratives at a pace that large, regulated brokerages simply cannot match.

The most credible long term competitive threat is arguably Robinhood, given its distribution and the likelihood that it eventually moves deeper into onchain markets. But even in that scenario, fomo is well suited to compete. The product already fits the “onchain Robinhood” slot more naturally, and its social loop and mobile-native UX are difficult for incumbents to replicate within a heavier regulatory and product framework. It is also not hard to imagine Robinhood viewing fomo as an attractive acquisition target if onchain activity continues to accelerate. Earlier in the year, it was reasonable to think Pump might pursue something similar given its sizable war chest, but that now feels less likely.

It is worth addressing what I see as the primary risk, which is tied directly to one of fomo’s greatest strengths. The social visibility model effectively forces users to trade in public. Positions, sizing, timing, and PnLs are surfaced to followers in real time and, for many users, are tied directly to their Twitter identity.

That creates clear opsec concerns: traders cannot scale in quietly, manage size discreetly, or hide taxable events or mistakes. On top of that, the visibility itself introduces incentive issues. A user can accumulate supply through external wallets, corner meaningful float off-platform, and then trade from their linked fomo wallet in ways that influence follower behavior. That dynamic can be used to generate artificial social proof or exit liquidity if the product does not build guardrails. One obvious mitigation would be to surface wallet transfers the same way buys and sells are broadcasted, making in- and out-flows visible to all users.

Long term defensibility will depend on whether the team can introduce privacy controls, reputation systems, or visibility layers that preserve the social loop without requiring users to trade fully exposed or opening the door to these misaligned incentives.

Taken together, fomo is positioned to remain one of the leading venues for onchain trading heading into 2026. The combination of instant execution, multichain coverage, social context, and real time narrative awareness creates a trading environment that web based interfaces cannot replicate. If retail flows increase at any point, fomo is the app most normies are likely to use.

It is also the product I would recommend to a non crypto friend over Moonshot or any web based interface.

Pump can improve its mobile experience and narrow the gap, but for now the product and UX differentiation give fomo a meaningful advantage. If the team continues executing at this pace, and expands into perps, RWAs, or tokenized equities, the potential outcome is significantly larger than the Moonshot acquisition and represents one of the more compelling consumer facing opportunities for the coming year.

Pump

Since our initial, pre fundraise Pump report, a lot has happened. Many of the dynamics we predicted have played out, while several areas have fallen short, frustrating both users and investors. The core challenge, though, remains unchanged. For Pump’s broader vision to materialize, the team will need to manage the tension between crypto’s relentless short-termism and their longer-term ambitions for the platform. To that note, once a project launches a token, the operating environment shifts; the token becomes a product of its own, inherently reflexive, and constantly shaping user expectations. Pump has been no exception here.

The Pump team has continued to invest in crypto-native streaming since their fundraise but this has not unfolded the way we had hoped it might. At least not yet.

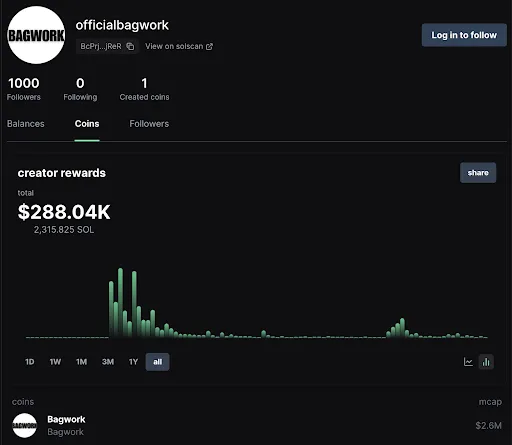

Pump hasn’t onboarded meaningful creators from outside the crypto ecosystem, and the CCM meta that emerged on Pump was short-lived. The standout moment came from the “Bagwork” run which highlighted both the potential of creator-driven tokens and the structural issues that still hold the model back.

bagwork guys just ran on the court in the middle of the nuggets vs clippers game 💀

— Jack (@Jackkk) November 13, 2025

This breakout was led by a group of teenagers, supported in part by Pump, who pulled off a series of viral stunts: stealing Bradley Martyn’s hat, running onto the field at a Dodgers game, storming the Knicks court, and even getting Pumpfun and Bagwork tattoos.

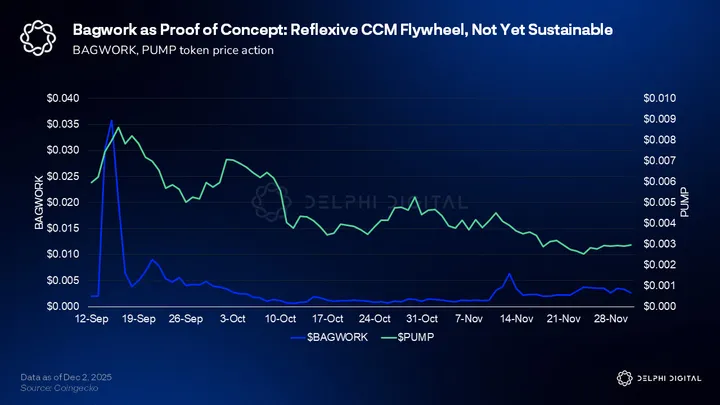

Bagwork’s emergence aligned almost perfectly with Pump.fun’s blowoff top in mid-September, when $PUMP reached an FDV of roughly $8.5 billion while Bagwork briefly traded above a $50 million market cap.

No creator coin since has come close to replicating that level of organic momentum or peak valuation. The Knicks stunt occurred more recently, well past the initial hype cycle, with Bagwork trading at a market cap of just over $2 million today.

Bagwork was one of the only cases where Pump’s streaming experiment actually worked as intended. The Bagwork team made more than 2,300 SOL in creator earnings from $BAGWORK trading fees (roughly three hundred thousand dollars at current prices). Mind you, this was all generated without the team needing to sell any of their holdings. The viral stunts translated directly into attention, volume, and fees, creating the closest thing to a real creator-token flywheel that Pump has seen so far.

Outside of Bagwork, however, Pump has struggled to deliver on its streaming ambitions. Creator coins have consistently failed to hold value. This goes back to the structural point that tokens are part of the product itself.

The economic reason to own or support a streamer coin is still unclear. The early success of Bagwork faded quickly, and every major streamer coin since has failed to gain similar traction and has ultimately trended toward zero.

Creators can make short-term revenue through the CCM fee structure, but the reputational cost of being associated with a collapsing coin makes it unattractive for larger, more established creators who could help onboard wider audiences. From the trader’s perspective, these coins remain zero-sum environments rather than genuine communities.

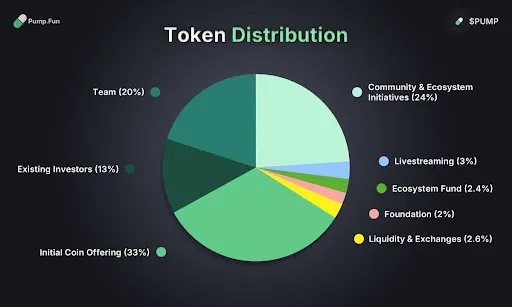

This is the single most important problem Pump needs to solve going into 2026. The team has not yet meaningfully experimented with deeper creator incentives, and the airdrop allocation remains untouched. Outside of the informal support given to Bagwork during its run, there has been no coordinated attempt at things like targeted airdrops, creator rewards, or other incentive mechanisms that could be used to bootstrap early activity, create more PvE style incentives, and give creators room to experiment without immediately blowing up their communities.

The good news is that this gives Pump significant optionality. The unspent “Community & Ecosystem Initiatives” pool are still major levers the team can pull when the model is ready. If Pump can design a sustainable incentive structure for creator tokens, it would unlock an entirely new economic category for creators who want to use crypto mechanics to monetize and scale their audiences. The upside is real but until then streaming will continue to function as a series of short lived hype cycles rather than a durable, recurring vertical.

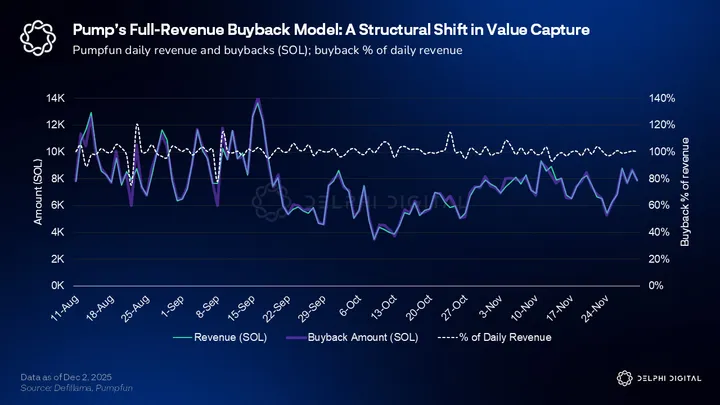

On the token side, the main catalyst for $PUMP’s rally from roughly 0.025 to 0.085 was the decision to commit one hundred percent of net revenue to buybacks.

Pump shifted from an initial plan of allocating only about a quarter of revenue to buybacks to essentially adopting the full Hyperliquid-style model after the market made it clear that a partial approach would not be rewarded. The shift helped ignite one of the strongest large cap rallies of the year in an otherwise illiquid and unforgiving altcoin environment.

On a buyback-to-market-cap basis, no major token currently trades at cheaper multiples.

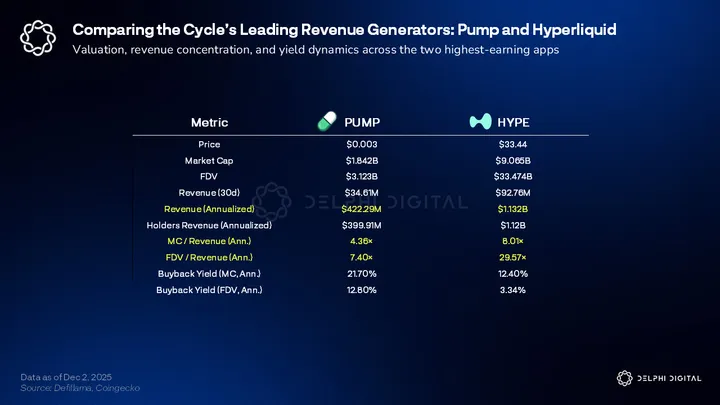

At today’s numbers, Pump generates $422M in annualized revenue against a $1.84B market cap, implying a 4.36× MC/Rev multiple and a ~12.8% annualized buyback yield, levels that are materially below every other large-cap token, including Hyperliquid’s ~8.01× MC/Rev and ~3.34% yield.

Even so, the market remains skeptical of Pump’s long-term business trajectory. Concerns likely include whether the team can continue shipping meaningful product, the impact of future unlocks given that ~40% of supply is still locked, and uncertainty around how the airdrop and creator incentive allocations will ultimately be distributed. This is compounded by the broader contraction in memecoin and terminal activity and lingering questions about the durability of Pump’s revenue base.

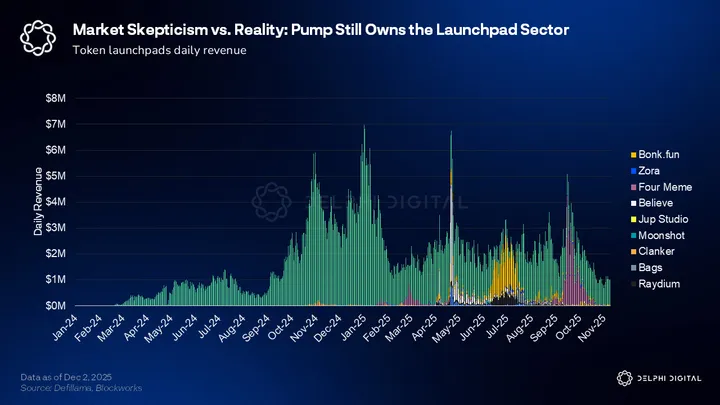

Despite these concerns, Pump continues to dominate the memecoin launchpad sector and is still earning (and buying back) roughly one million dollars per day even in what has been an extremely rough market.

Daily launchpad revenue is down nearly 85% from the early-year peak of almost $14M/day to closer to ~$2M/day today, yet competitors have not meaningfully challenged Pump’s position for more than brief periods. This is consistent with our expectation from the original report during the short-lived Bonk and Raydium challenger phase: even with cyclical volume compression, Pump has retained a structurally advantaged share of sector activity.

The acquisition of Padre supports the idea that Pump intends to expand beyond Solana and reach a multichain audience, with support for BNB ecosystem assets already live via the Padre frontend. This also fits with our earlier prediction that Pump would eventually acquire a terminal or terminal-adjacent property to strengthen the top of funnel and consolidate more of the user journey. Outside of these moves, however, the team has kept a low profile. An investor call is scheduled, although it has not occurred at the time of writing, so additional clarity may be forthcoming.

internet capital markets on pump dot fun.

— alon (@a1lon9) October 28, 2025

Leadership has also indicated interest in the broader ICM category, although this is not an area we view as core to Pump’s current identity or product strengths. The original attempt at this model was Believe, which failed to gain real traction, and MetaDAO has since become the dominant player in the “high quality founder + community” fundraising space. ICM also feels culturally and structurally misaligned with Pump’s brand, which is built around speculation, speed, and creator memetics rather than long-form governance or futarchy-style systems.

For Pump to succeed in ICM, they would need to lean into governance-heavy structures and attract non-crypto teams that want to operate onchain, which is not where most of Pump’s current users or creators sit. While there is theoretical upside if the team committed meaningfully, I view this as a secondary or optional direction rather than a natural extension of Pump’s existing flywheel going into 2026.

Looking ahead, the main questions for 2026 revolve around whether Pump can finally create an incentive aligned model for creator tokens, whether it meaningfully expands into multichain markets through Padre, how it manages unlocks and declining revenue visibility, and which product vertical it chooses to lean into most aggressively. Right now the strategy feels spread across several surfaces, from streaming to ICM to mobile.

At some point the team likely needs to commit to a primary wedge, and for most of 2025 that wedge appeared to be streaming. Today that is much less clear.

The bigger question is whether Pump can still attract larger non-crypto creators. That likely requires reworking the creator-token flywheel with stronger, longer-term incentives that can sustain virality outside the crypto-native cohort. The raw ingredients exist. In 2025, the Bagwork run showed a glimpse of what it could look like when the model hits, Pump looked close to crossing the chasm.

$SHFL is already a top-10 project in crypto on a revenue basis.

In the past 30d it generated ~$17M net revenue (~$200M annualized), yet it isn’t tracked on DeFiLlama and mostly flies under the radar.

Unlike $HYPE and $PUMP, both priced at their theoretical max with ~100% of… pic.twitter.com/NTOLNVtWuP

— Simon (@simononchain) September 21, 2025

Pump also retains meaningful surface area to expand its product suite. One strategic vector the team should be seriously evaluating is a move into iGaming or casino-adjacent verticals; a Kick/Stake-style model that fits naturally with Pump’s speculation-driven user base. It would be deeply synergistic with its memecoin and streaming ambitions, and the earnings potential in this category is already proven. Shuffle’s net gaming revenue and weekly lottery distributions show how large this opportunity can be when executed well.

Pump’s mobile app is another underutilized advantage. A deeper push into mobile could broaden the top of funnel, make the product more accessible to mainstream users, and give creators more surface area to monetize. Combined with iGaming, it would meaningfully expand Pump’s addressable audience while reinforcing the parts of the platform that already work.

Despite the uncertainty, Pump continues to operate as one of the cycle’s most resilient consumer apps, maintaining dominance even as the broader landscape has shifted. Material progress on any single vector could catalyze a meaningful sentiment reset and position Pump for a broader breakout beyond the crypto native cohort.

Zora & The Base App

Zora is the tokenization infrastructure behind tokenized content on Base. Its creator coins and content coins are piloted by the flagship Zora app, a crypto Instagram and Twitch. We recently covered Zora in Can’t Stop Coining.

Zora has become synonymous with Base’s vision, offering a concentrated bet on the Web3 creator economy. By tokenizing the individual content, Zora creates a spot market to work around that is agnostic of the app itself. This future-proof design can take the creator economy thesis farther than Pumpfun. It also offers numerous paths to success: through its native social media app, as a backend for the Base app and Base ecosystem, or through a rumored connection to Robinhood Social app.

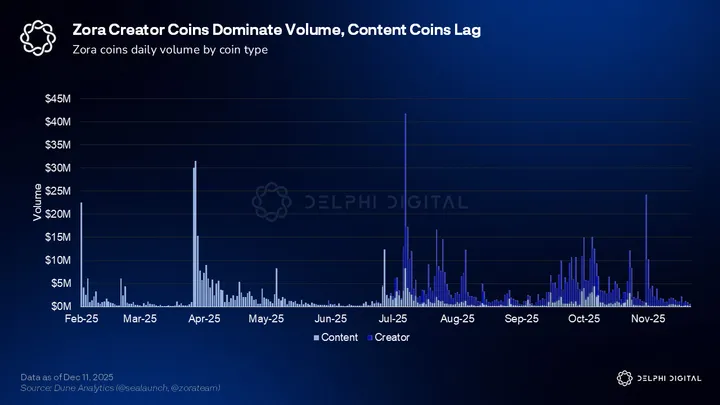

So far, creator coins dominate speculation. No one cares about content coins, despite intense efforts by Zora to boost demand through trading competitions and subsidies.

Content coins have been heavily criticized, likened to memes with better branding. The big issue at the moment is that there is no reason people care about content coins. Coinbase has been vague about discussing economic value drivers of content coins. Content coins will not work without economic drivers.

Content coin economics

The Web2 model, in a nutshell, charges advertisers for the attention of their target users. It is easy to see how a viable model could emerge by working backwards from Web2.

The price of an ad is a function of engagement, among other things like targeting and attribution. Social media apps are really just peer to peer marketplaces like Uber & Doordash, where consumers are selling attention to creators who earn it. Advertisers pay to insert themselves within this attention matchmaking process. The value of the attention scales with the network effects of the user base and the data it produces. From the platform’s perspective, creators are producers, advertisers are consumers. From the advertiser’s perspective, users are the producer. This is why the saying holds: if it is free, you’re the product.

An ad that Jeff Bezos sees on his phone is worth, say, $2K. If Bezos scrolls for 5 minutes and sees 100 pieces of content, each post generated roughly $20 in value. Each piece of content on twitter has an implied value based on its share of attention, and its proximity to the attention monetization vehicle, which is ads. Content coins aren’t memes any more than their web2 counterparts are, they just lack a fee switch.

The entire Web2 social media industry is built on the lie that the platform generated that value. That Jeff Bezos is there for the platform. We all know that isn’t true, and it is becoming harder to deny as creators become more liquid and demonstrate leverage by moving their audiences.

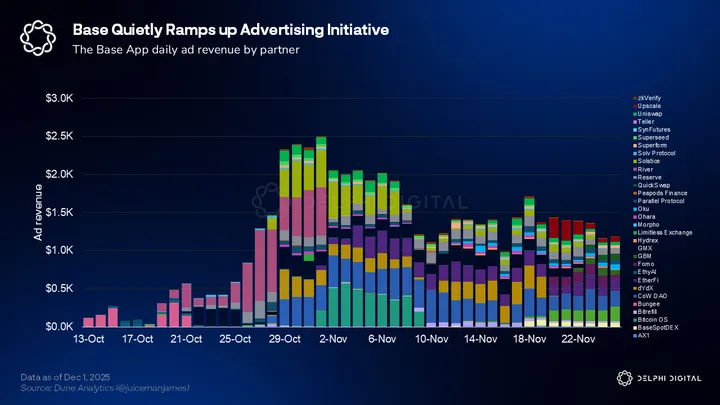

Coinbase is dedicating substantial resources to its creator economy initiative on Base. In Jan-25, Coinbase acquired Spindl, a Web3 user attribution platform, and is currently scaling up an advertising business.

With Spindl, builders can define what “return” means (Users minting, staking, swapping, etc); reach users based on onchain behavior, traits, or custom lists; and only pay when users take the action. Ads are slowly ramping up since late October, reaching $57K in revenue across 30+ advertising partners. We’re starting to see more of a push to talk about Base ads by ecosystem leaders. Base ad revenue will be important to monitor as the Base App is fully released to the public. This could be as early as Dec-17, Coinbase’s highly anticipated system update.

1/ Spindl was built to bring modern growth marketing onchain and enable you to see real return on ad spend.

Spindl-powered ads are now running natively in @baseapp, letting builders launch wallet-targeted campaigns that drive real value.

You built it. Now find your people. pic.twitter.com/AMmKHTDUar

— spindl (@spindl_xyz) July 29, 2025

It is clear Coinbase has a plan for monetization, but unclear why they are being discreet about it. Perhaps to protect their lead against competitors, or maybe to avoid scrutiny around unregistered securities before legislation is passed. Regardless, it is encouraging to see that there is clearly an intention to build rails for real value accrual with content coins.

The lack of open dialogue about the roadmap for content coins allows the memecoin accusations to go unrefuted. It appears Coinbase wants to take a hands off approach to the monetization aspect, laying the groundwork and allowing others to come in and experiment.

an open stack for the global economy https://t.co/AcaDJDQEk8

— jesse.base.eth (@jessepollak) November 5, 2025

There is a lot of execution risk with Base, but the mission is far more ambitious than consensus is willing to acknowledge. The market has a clear negative bias towards Base’s creator economy, which could offer major opportunities for those that cut through the noise. Content coin trading volume will be the ultimate indicator of a healthy creator economy.

Zora as a social media app

Zora’s overall vibe and implementation of social media has been polarizing as well. Zora leans hard into the hyperfinancialization theme, completely removing traditional functionality of likes and replacing them with buys and sells. Market cap and creator coin holders even replace the traditional followers benchmark.

Zora faces some valid criticism for its uncompromising commitment to a fully financialized social media platform. Critics claim these behaviors do not exist but there are clear parallels with existing models. Streaming is a great example.

- Twitch : Zora

- Subs : token gated chats

- Hype trains : ATH meter

- Tips, donations, bits : Content coin buys

- Announcement chime feedback : Word art feedback

- Hosting : ZoraTV?

Zora isn’t completely reinventing the wheel, it is repackaging existing behaviors into a radical new form factor.

Once economic levers are activated, you have a familiar product suite with the potential for radical new experimentation. Users see the value their community enclave is producing. Their content and graph is portable across other social media apps/clients building on the stack. The algorithm, which is really the main proprietary feature of legacy social media platforms, becomes democratized and composable. The possibilities thereafter are endless:

- Ad revenue to creator coin

- Watermarking content and earning royalties

- Pay over x402 to be hosted by ZoraTV

- Continuous dutch auctions for algo boost

- Paying to reach anyone. shoot your shot with Elon

- Invest in a tweet (routinely referenced, seems to be Base’s north star)

- Hands-on brand engagement