Introduction

On the surface, 2023 may seem like a pretty uneventful year for DeFi. The chaotic global macro environment and bloodbath of insolvencies from centralized entities in mid 2022 extinguished capital from on-chain finance. The collapse of FTX in Nov. 22 was a cruel final stroke, from which DeFi has been licking its wounds throughout 2023. But DeFi is far from dead.

In a vacuum, the DeFi sector performed well in 2023. Many tokens rallied over 100%, with few tokens registering a loss on the year. Pendle showed aspirations of becoming this bear market’s LINK/SPELL, turning in a 20X and resurrecting the forgotten yield stripping niche. 2023 gave us an expected yet inconclusive bounce off of 2022 lows.

The year was plagued by widespread lethargy as rising interest rates muted on-chain activity. DeFi had never experienced a rising rates environment before. The highest fed funds rate since 2001 proved an insurmountable hurdle for depressed DeFi yields. By and large, fundamentals were disconnected from price. There were rarely any injections of fresh capital or hype around a new project, token, or design.

2023 was a relatively quiet year for spot DEXs, and market share was understandably stable. Spot DEX volume made up ~8% of the top 5 CEXs. The biggest storyline involved the expiration of Uniswap V3’s BSL and a shift in focus towards the upcoming Uniswap V4. 2024 is shaping up to be much more eventful.

The area in which DeFi made the most progress is decentralized perpetuals. As discussed in our DYDX Valuation Analysis & DEX Perps Comparison, 2023 was the most eventful year yet for DEX perps. Rollups and appchains have allowed for a greater variety of orderbook protocols. dYdX v4 is transitioning to Cosmos appchain, Aevo is pioneering the OP rollup stack with a unique offering of pre launch markets, Vertex has pushed DEX UX to new heights, and RabbitX has come out of nowhere to bootstrap usage on Starkware. The peer-to-pool model transformed as well. Synthetix and GMX have implemented risk management measures establishing peer-to-pool as a truly viable perps model for the first time.

These breakthroughs have thus far failed to move the needle against CEX dominance. DEXs have a ~3% market share of the top 4 CEXs. The use of top 4 CEXs for comparison skews results in favor of DEXs. The all-in DEX market share is closer to 3% and 1% for spot and perps, respectively.

Given the tailwinds for DEXs heading into 2023 and the progress that was made, DEX perps’ lack of traction demonstrates DeFi’s apathetic atmosphere in 2023.

Heading into 2024, the positive energy is palpable. There is volatility on the horizon and a slew of potential catalysts. It is clear that we have entered the Early Innings of a New Cycle. But even during broader market uptrends, DeFi has been treading water relative to other crypto sectors since its peak in Sep. 2020. DeFi has emerged on the other side of a three year bear market with new faces, new ideas, and a new meta.

Heading into 2024, the positive energy is palpable. There is volatility on the horizon and a slew of potential catalysts. It is clear that we have entered the Early Innings of a New Cycle. But even during broader market uptrends, DeFi has been treading water relative to other crypto sectors since its peak in Sep. 2020. DeFi has emerged on the other side of a three year bear market with new faces, new ideas, and a new meta.

In this report, we offer you a comprehensive briefing on the themes we believe will dominate the narrative in 2024, and will get you caught up to speed if you’re just tuning back in.

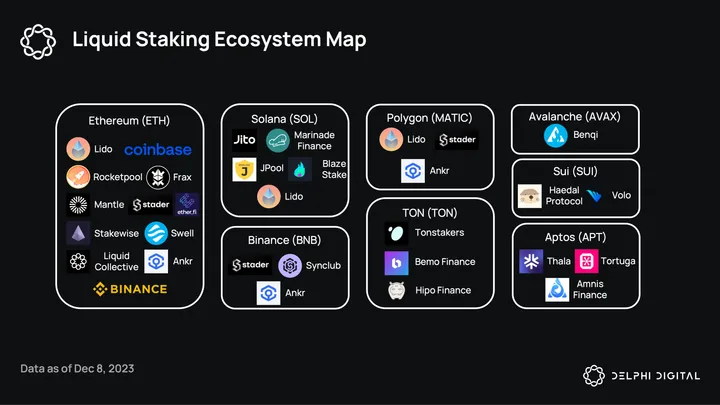

Theme 1: Competition Between LSDs and the Restaking Economy

Liquid staking has been widely implemented within various L1 ecosystems to make staking easily accessible. Protocols like Lido help enhance the liquidity of staked assets while allowing the underlying to continue earning rewards and providing economic security to the network.

As the largest L1 blockchain, Ethereum presents a highly competitive environment with numerous protocols vying for market dominance. In contrast, other L1 ecosystems face less competition, with only a handful of protocols competing.

As the largest L1 blockchain, Ethereum presents a highly competitive environment with numerous protocols vying for market dominance. In contrast, other L1 ecosystems face less competition, with only a handful of protocols competing.

Protocols such as Lido, Ankr, and Stader, despite their expansion across multiple L1 blockchains, haven’t achieved significant market presence compared to native protocols on these blockchains. For instance, Lido’s success in the Ethereum ecosystem hasn’t been replicated in the Solana ecosystem, leading to a phase-out from Solana.

Here, we’ll focus primarily on the liquid staking landscapes in Ethereum and Solana — as these have seen the most substantial adoption and development — as well as the most important development across the staking landscape, restaking.

State of Ethereum Liquid Staking

Ethereum staking saw significant growth in 2023, primarily driven by the Shapella upgrade, which allowed for withdrawals from the Beacon Chain. The quantity of ETH staked rose substantially, from around 16M ETH at the beginning of the year to 28.6M ETH by December 2023, marking a year-to-date increase of 79%.

This represents a staking rate of 23.7% against the total supply of 120.2M ETH. As noted in our previous liquid staking report, staked ETH is gradually approaching the estimated target of 33.5 million ETH, or 27% of the total ETH supply, which is considered optimal for robust network security.

Furthermore, the adoption of liquid staking derivatives (LSDs) has also expanded, with ~44% of all staked ETH now in these protocols. This growth is fueled by yield-hungry ETH holders and the increasing utility of LSDs in DeFi. Liquid staked ETH is being deeply integrated into money markets and DEXs. We’ve also seen the emergence of aspiring L2s like Blast and Mantle leverage LSDs to offer native yield-earning opportunities for users.

The growth in Ethereum staking has shown signs of slowing, with the monthly ETH stakes experiencing a downward trend since May 2023. A notable spike in growth was observed around May 2023, coinciding with the implementation of Ethereum’s Shapella upgrade which allowed staked WTH to be withdrawn. This addressed the duration risks that previously existed and kept many ETH holders from staking their tokens.

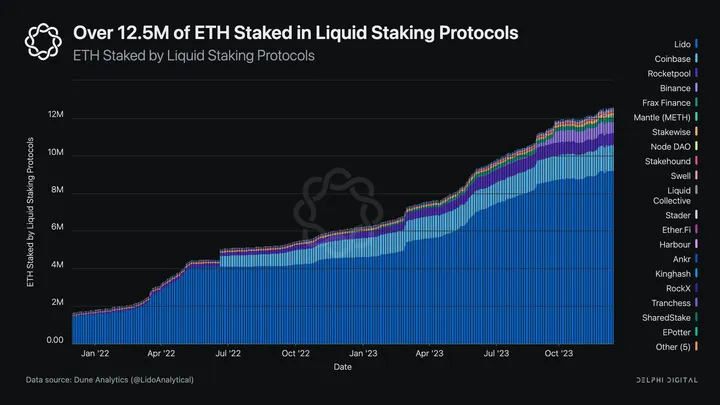

As of now, the amount of ETH in liquid staking protocols has reached over 12.5M, doubling from 6.25M at the beginning of 2023.

Lido stands as the predominant leader in this burgeoning market, with 9.2M ETH staked. This is followed by Coinbase’s cbETH, with 1.35M ETH, and RocketPool, which has 630K ETH staked. Lido maintains its market dominance and exhibits the most significant growth among these platforms, with an increase of 4.57M ETH, representing a 99% rise since the year’s start. In comparison, Coinbase and Rocketpool have seen 348K ETH (a 34.4% increase) and 294K ETH (an 88% increase) added respectively.

Lido remained resilient even as the competitive landscape expanded, underscoring its strong network effects via stETH integrations. The enhanced utility of stETH, compared to other LSDs, gives it a massive competitive advantage. Since most LSDs offer similar yields, stETH stands out due to its higher secondary market liquidity and broader utility in DeFi. This competitive edge is crucial since the underlying yield is similar, making liquidity and utility the key differentiators.

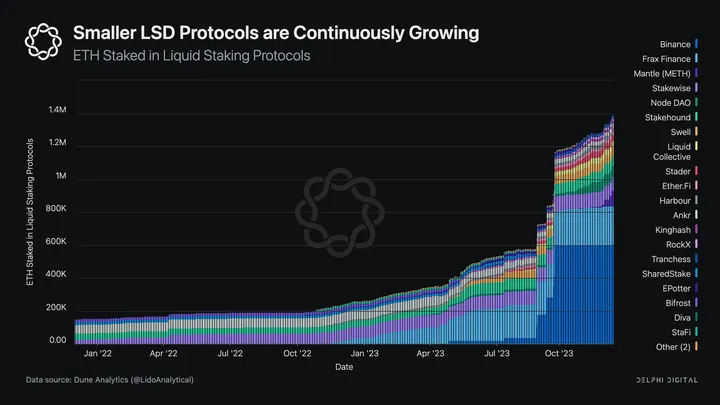

Excluding the major players like Lido, Coinbase, and Rocketpool, there have been developments from smaller LSDs in the Ethereum ecosystem:

- Frax has displayed steady growth, expanding from 38K to 233K ETH staked in 2023. Frax’s edge lies in its innovative sfrxETH design and integration within its ecosystem, notably in Fraxlend.

- Binance has been experiencing a significant influx of ETH into Binance’s bETH, likely from new stakers opting to stake directly through the centralized exchange.

- Mantle has leveraged its protocol-owned ETH to bootstrap its mETH offering. The mETH from the protocol is intended to generate yield for Mantle and facilitate liquidity on DEXs.

- Emerging protocols in the liquid staking space have struggled to capture significant market share, often not exceeding the 100K ETH mark. Notable examples include ether.fi and Swell, which have introduced various incentives for stakers.

- Ether.fi and Renzo are new projects implementing liquid native restaking on EigenLayer, allowing ETH to earn multiple forms of yield, including native points and EigenLayer points.

The liquid staking market on Ethereum is highly competitive and saturated, making it challenging for new, non-CEX-affiliated LSDs to gain substantial market share. The absence of strong network effects and limited adoption in DeFi ecosystems are significant hurdles. To succeed, these protocols must not only offer innovative features to attract depositors but also strive to integrate their LSDs into established DeFi protocols like Aave to gain traction.

LSDfi

As liquid staking brought in a new wave of innovation to the DeFi product stack, LSDfi started to cement a story as the shiniest new thing. However, many of these projects lost traction as their incentive-driven high yields compressed. Select few, like Prisma and Lybra, seem to be finding their footing as liquid staking centric DeFi legos.

The total value of LSDs held across DEXs, CDP protocols, and lending protocols has reached $7B. This growth has occurred in tandem with the expansion of LSDs, fueled by the increasing availability of DeFi applications.

Distinct leaders have emerged within each sector of LSDfi: Curve dominates the DEXs, MakerDAO is at the forefront of CDP protocols, and Aave leads in the lending category.

Given that stETH from Lido holds the majority market share among Ethereum LSDs, it’s expected that stETH constitutes the bulk of the TVL in LSDfi activities. On the other hand, frxETH from Frax, despite having a smaller supply, boasts a higher TVL in DeFi compared to rETH.

This can be attributed to two main factors, Frax’s influence in Convex which allows them to direct incentives towards frxETH and deepens frxETH liquidity and its integration within Fraxlend. These aspects provide frxETH with a distinct advantage over other LSDs, offering it greater utility and making it a more competitive option in the DeFi space.

Overall, it’s difficult to expect any material changes to the core liquid staking landscape on Ethereum. Lido will probably continue to enjoy the lion’s share of the market, while other protocols vie for what remains. There is one major development that will undoubtedly change the Ethereum staking landscape over the next year or so — restaking.

Restaking: The Biggest Staking Development of 2024

EigenLayer is a protocol that expands the utility of staked ETH by using it to not only secure Ethereum, but also other pieces of infrastructure like bridges, appchains, rollup sequencers, and data availability networks. It is essentially an external protocol that rehypothecates staked ETH and utilizes the underlying economic value to help secure a third-party network — commonly called Actively Validated Services (AVS).

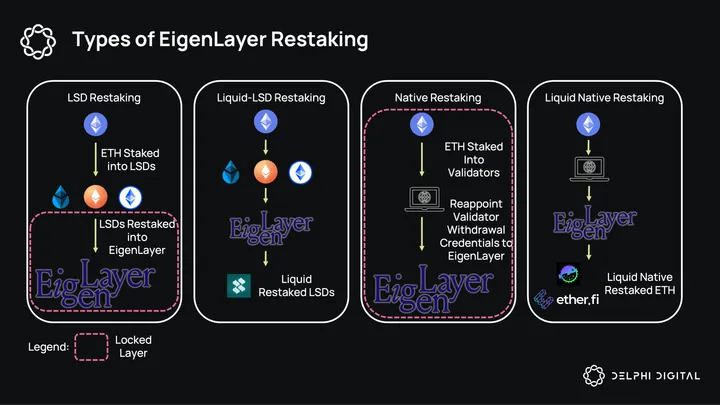

EigenLayer offers two primary restaking options – LSD restaking and native restaking. The current landscape of EigenLayer restaking can be categorized into four distinct types:

EigenLayer offers two primary restaking options – LSD restaking and native restaking. The current landscape of EigenLayer restaking can be categorized into four distinct types:

- LSD Restaking (EigenLayer Native): This involves depositing an asset like stETH into the EigenLayer smart contract, thus enabling them to be used for restaking.

- Liquid-LSD Restaking: Targeting the locked layer of LSD deposits in EigenLayer smart contracts, protocols like KelpDAO aim to unlock liquidity for restaked LSDs. This approach allows depositors to enjoy greater liquidity and provides the flexibility to exit restaking by swapping out their positions. However, this is currently constrained by EigenLayer’s LSD deposit limits.

- Native Restaking (EigenLayer Native): For restaking staked ETH on the Beacon Chain, validators need to redirect their validator withdrawal credentials to EigenLayer. This is done through an EigenPod smart contract, which manages the balance and withdrawal status of validators.

- Liquid Native Restaking: Differing from LSD restaking, which depends on the underlying LSD, liquid native restaking offers a comprehensive service encompassing both staking and restaking of ETH. This model is advantageous for protocols as EigenLayer doesn’t impose limits on native restaking amounts. Protocols adopting this method can also accrue fees from the staked ETH, making it a potentially more profitable option.

EigenLayer has quickly garnered traction, evidenced by how quickly the deposit caps fill up. There are currently $250M of LSDs restaked with EigenLayer as of Dec. 17 (before the deposit cap was increased).

At the current moment, restaking ETH through EigenLayer does not introduce additional risks associated with securing other applications. Realistically, it simply presents an attractive opportunity to earn EigenLayer points for a potential airdrop in return for bootstrapping the protocol’s managed asset base.

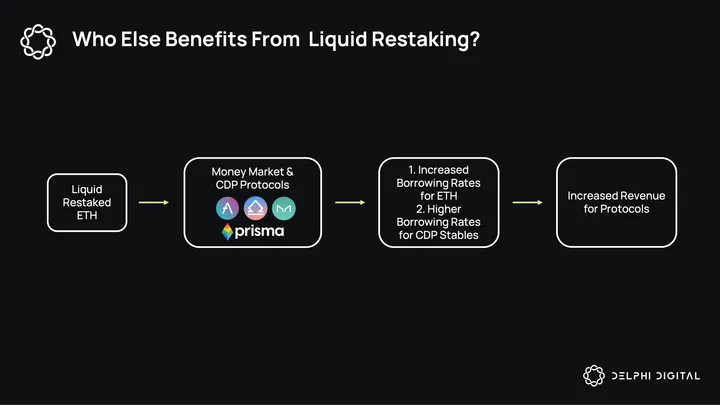

As liquid restaking cements its role in the market, money markets and CDP protocols stand to benefit from it. Liquid restaked ETH, offering higher yield rewards than traditional staked ETH, positions these protocols advantageously to impose higher borrowing fees.

As liquid restaking cements its role in the market, money markets and CDP protocols stand to benefit from it. Liquid restaked ETH, offering higher yield rewards than traditional staked ETH, positions these protocols advantageously to impose higher borrowing fees.

As we’ve seen from stETH, where users looped by lending stETH and borrowing ETH to stake, the same can happen for liquid restaked ETH.

MakerDAO has been consistently increasing borrowing rates for ETH over 2023 as LSD yields subsidize the net cost of loans. With liquid restaked ETH pushing ETH yields higher, it is likely that CDP protocols will be able to capture part of it through higher borrowing fees.

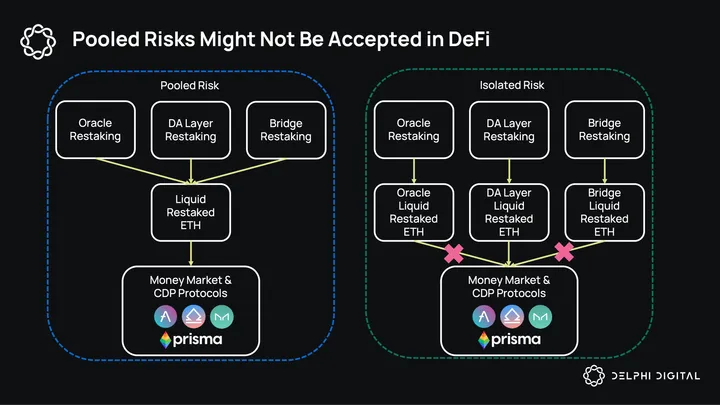

However, as each restaked layer offers a differing risk profile, this presents a nuanced challenge for DeFi protocols, particularly concerning their willingness to integrate certain types of liquid restaked ETH exposed to pooled risks. For instance, bridges have been notably vulnerable to exploits and have suffered significant financial losses; protocols may be hesitant to adopt liquid restaked ETH with exposure to bridges.

However, as each restaked layer offers a differing risk profile, this presents a nuanced challenge for DeFi protocols, particularly concerning their willingness to integrate certain types of liquid restaked ETH exposed to pooled risks. For instance, bridges have been notably vulnerable to exploits and have suffered significant financial losses; protocols may be hesitant to adopt liquid restaked ETH with exposure to bridges.

Protocols might be more inclined to include liquid restaked ETH that has siloed exposure towards networks they perceive to have lower risk, as this would minimize the chance of a large slashing event. A cautious approach is required when considering integrating liquid restaked ETH, especially as restaking goes live and more AVS allocation strategies launch.

However, this differentiation in risk profiles could result in a future where not all restaked ETH assets are perceived equally, leading to a fragmentation not only in how these assets are implemented across various DeFi protocols but also in their liquidity. Such a scenario could create a complex landscape, where the value and utility of restaked ETH vary significantly based on their associated risks.

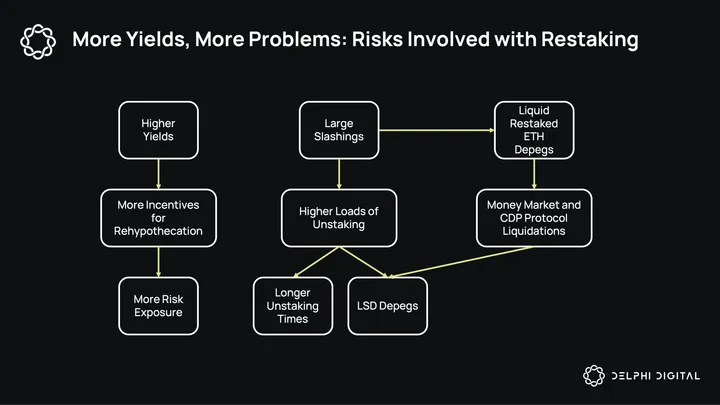

Restaking carries larger risks that could have significant implications for the overall industry. One key concern is the allure of higher yields, which might encourage the rehypothecation of ETH to riskier networks in the chase for higher yields.

Restaking carries larger risks that could have significant implications for the overall industry. One key concern is the allure of higher yields, which might encourage the rehypothecation of ETH to riskier networks in the chase for higher yields.

A substantial slashing event could lead to an increased volume of unstaking requests, resulting in prolonged unstaking times. If liquid restaked ETH becomes a large source of collateral in DeFi, an event like this is almost certain to cause carnage.

As the staking withdrawal queue expands, people will rush for the gates via secondary markets, which could lead to substantial depegging event. Users who have levered up against their restaked liquid ETH likely get liquidated, and with secondary market liquidity drying up, this would result in bad debt for money markets.

The possibility of a tail event causing widespread issues across the ecosystem could be significant deterrent to the widespread adoption of liquid restaked ETH within DeFi. This risk is particularly pronounced in designs that involve pooled risks.

Given these considerations, the adoption of liquid restaked ETH in money markets should lean towards isolated pools to silo any risk.

Solana Staking: An Eye to the Future

In 2023, Solana’s liquid staking market initially saw Marinade as the dominant player. However, as the year progressed, particularly in Q4, Jito emerged as a strong competitor. Jito managed to attract a substantial number of stakers, partly through the distribution of Jito points, which eventually led to a significant airdrop event. The lowest tier of users were given 4931 JTO tokens each, which is estimated to be worth ~$10K on the day of airdrop.

Another noteworthy protocol is BlazeStake, a relatively new entrant offering token-incentivized rewards for staking. This strategy has been successful in providing bSOL holders with additional yield opportunities.

In Solana’s LSDfi ecosystem, we see a similar story, where money markets dominate. Platforms like Solend and Marginfi have become central hubs for LSD activity. Marginfi and Kamino recent growth can be partly attributed to users engaging with the protocol in hopes of an airdrop.

Solana LSDs have low liquidity on DEXs. Despite that, they usually have an extremely high turnover, resulting in organic yields from swap fees. However, this liquidity is incentivized by token rewards, which can be expensive over time. Furthermore, when holders actively sell in the markets, this can lead to a depeg as seen recently with mSOL.

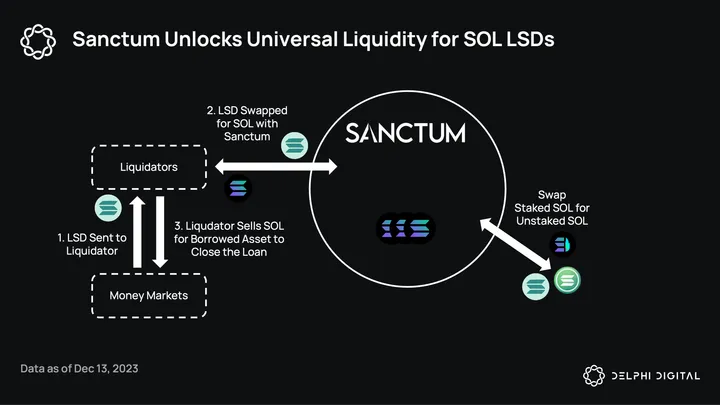

Sanctum, formerly known as unstake.it offers a novel solution for providing immediate liquidity to any liquid-staked SOL. This platform enables users to exit their staked positions at any time, without having to wait for the end of an epoch. The process involves users transferring their staked SOL to Sanctum, in return for unstaked SOL from the pool, incurring minimal swap fees. This approach offers instant pooled liquidity for all staked SOL, as opposed to the fragmented liquidity often seen across multiple SOL LSD stableswap pairs.

Sanctum, formerly known as unstake.it offers a novel solution for providing immediate liquidity to any liquid-staked SOL. This platform enables users to exit their staked positions at any time, without having to wait for the end of an epoch. The process involves users transferring their staked SOL to Sanctum, in return for unstaked SOL from the pool, incurring minimal swap fees. This approach offers instant pooled liquidity for all staked SOL, as opposed to the fragmented liquidity often seen across multiple SOL LSD stableswap pairs.

Sanctum’s system also plays a crucial role in facilitating a more liquid environment for handling liquidations related to SOL LSDs on money market protocols. With the current DEX liquidity, it is evident that there is insufficient liquidity to uptake larger swap amounts. Sanctum unlocks deep liquidity for such liquidations until all unstaked SOL in its pool is utilized. Subsequently, Sanctum will unstake the corresponding LSDs to replenish the SOL pool, ensuring a continuous and efficient liquidity cycle.

As mentioned in our Infrastructure Year Ahead report, “this has the potential to be a massive unlock for Solana DeFi as all LSTs could be added to DeFi protocols without a vigorous underwriting process. Most of the reason why LSTs are winner take most is because the moat they get from on-chain liquidity. With Sanctum, they are willing buyers of any LST, for a fee. This would also reduce contagion risk in Solana as no single LST would garner a monopoly. This would also allow Solana’s single stake pools to be more viable. They recently announced Sanctum Infinity with plans to go live in the next ~2 months.”

Theme 2: All Eyes on Uniswap Liquidity

Uniswap is the most dominant protocol in the history of crypto, and in many ways is the reference point for DeFi’s adoption. In 2023, DEXs have plateaued in their pursuit of CEXs in both trade execution and user experience.

Once again, Uniswap found itself shrouded in controversy after revealing its new aggregator, UniswapX, which will leverage intents to take trade execution off-chain. Uniswap v4, Uniswap X, and other intent based DEXs are shaping up to be the major theme of 2024.

We’ve covered Uniswap X/V4 and the rise of intent based apps extensively in Reflecting on EthCC, The Future of On-Chain Liquidity, and the Anoma series.

The introduction of hooks in Uniswap v4 will blast open the design space for Uniswap liquidity pools, which will all exist under a single contract, the Singleton. The extensive ecosystem of hooks will require innovation on the routing side, which is where UniswapX comes in.

UniswapX utilizes an intent-based trading architecture where off-chain fillers compete to settle taker volume. A trader signs a message, indicating the parameters at which they would like to perform a swap. Fillers then compete against one another in Dutch Auctions to earn the right to settle taker volume with the optimal route.

With UniswapX, routing is no longer limited to one universal router smart contract. Navigating the vast array of hooks and pockets of liquidity on Uniswap, other DEXs, and CEXs is now (in theory) an altruistic group effort by off-chain entities; a group effort that both starts and finishes on Uniswap.

This shift to off-chain execution and on-chain settlement is seen by some as an abandonment of core values, and by others as a bold commitment to a paradigm shifting tool. Intents are a fundamental reimagination of how transactions are structured, allowing for gas free transactions, cross-chain applications, and much more.

The potential improvements of UniswapX come with a lot of uncertainty around passive liquidity provision. UniswapX will allow off-chain solvers a first look at order flow before routing through the AMM. This could leave passive LPs as a dumpster for toxic flow leading to dangerous trickle-down effects.

The toxic flow concept is essentially an escalation of the harsh environments LPs already have to deal with. In today’s landscape, sophisticated narrow tick LPs and JIT liquidity dominate Uniswap liquidity on major pairs, particularly on the ETH-USDC 5bp pool.

Passive LPs, on any given trade, see their pro rata share of order flow diluted by sophisticated market makers, while experiencing the same exposure to the underlying. Periodically, on juicy trades, passive LPs are diluted out of picture almost entirely by the instantaneous adding and removal of liquidity within the same block, for the purpose of filling specific orders. As a result, passive LPs are very rarely earning fees commensurate with their price risk, or even with their share of TVL in the pool. The dilution by concentrated liquidity is understandable, but JIT liquidity is stealing a meaningful share of desirable flow, and not sticking around for the remaining order flow.

The problem with UniswapX for LPs is that it enshrines this process into the system. Solvers monitor incoming order flow and fill trades they can make money on, leave trades they can’t for the liquidity pool. This almost certainly means that the liquidity pool’s price will always be stale, and much of its volume will come from stat arb.

The general consensus at this point is that UniswapX will provide an improvement in trade execution initially, and have negative effects for LPs on major pairs. There is little debate around these theses.

The dystopian extension of this theory suggests that in the long run, toxic flow will render passive liquidity provision unviable. Passive LPs will flee, removing the liquidity of last resort, leaving the system in a more centralized, opaque state than before and swappers with questionable execution improvement in the long run.

There is certainly some validity to these concerns. Juxtaposing the charts above, we see a substantial jump in UniswapX’s share of trades (5% on Oct. 31 → 18% on Nov. 5) coinciding with the arrival of Wintermute as a filler. Wintermute arrived at the end of October and is now accounting for roughly 75% of solver orders. ~90% of UniswapX trade volume is filled by three market makers.

The counterargument here is that passive LPs don’t necessary care about 5 minute markout and LVR, which are hidden costs to the untrained eye. Retail LPs are bothered much more by impermanent loss. If the price at a future time returns to the price at t = 0, a passive LP is likely happy and sees fees earned as a bonus.

Many passive LPs are characterized by a lack of time preference and an indifference between holding two assets. Both of these LPs views LVR as simply money left on the table. Uniswap v4’s hooks will have the potential to cater to the many unique preferences of passive LPs. The design space of hooks could even bring new sources of non toxic flow (i.e. liquidations for lending hook). A gradual shift of passive liquidity from low fee tier pools for major pairs, towards unique hooks with new capabilities is expected.

There is also the possibility that as Uniswap resumes its traction against CEXs, Uniswap begins to swallow massive amounts of volume, and LPs end up net positive.

Projects We’re Watching:

- Rage Trade

- IntentX

- Aori

- Uniswap

- Cowswap

- 1Inch

- Symm.io

- Across

Theme 3: App-Specific Rollups Will Scale Ethereum DeFi

Ethereum’s entire scaling vision revolves around rollups. The core premise is that the Ethereum L1 layer will gradually become a settlement and data availability layer for an ecosystem of rollups.

While this has been the high-level direction of Ethereum scaling research for several years now, it was only during DeFi Summer and the subsequent rise in demand to use on-chain environments that it was made abundantly clear to everyone that the Ethereum L1 doesn’t have enough blockspace to cater to a large swathe of users alone.

In today’s rollup landscape, we have seen general purpose execution rollups like Arbitrum and Optimism take the lead and set the tone for what this technology can do. They have significantly reduced end-user costs, mostly by virtue of being able to batch many L2 transactions into a single L1 transaction. This splits up the cost of execution amongst a number of users, and allows the network to piggyback off Ethereum’s consensus and economic security.

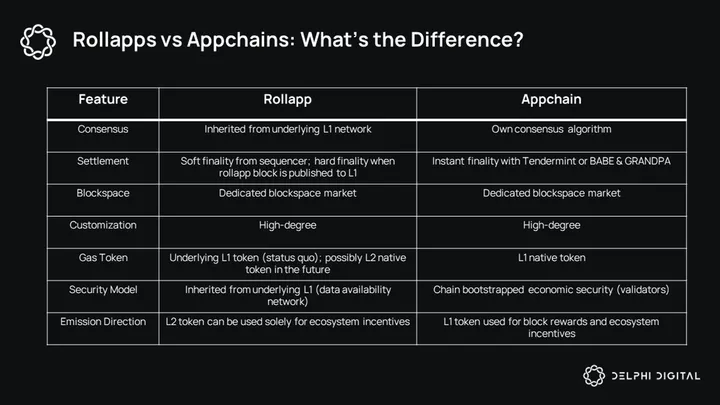

However, rollups can be so much more than just a replica of Ethereum mainnet. Just as we see Cosmos spearhead the concept of application specific L1 chains, there is also scope for application specific rollups — or rollapps. The rollup idea, and modular blockchains at large, have quickly become something bigger than Ethereum, the network. Data availability layers like Celestia, Avail, and EigenDA offer a much more competitive solution for teams looking to optimize on costs.

Rollups, in general, require less financial overheads than L1s. Each new Cosmos chain has to bootstrap its own economic security, incentivizing people to buy the token and stake it in a validator. Theoretically, the token’s value must also scale with the amount of value it secures. As such, rollups provide a simpler way for application developers to build their own configurable execution environment and opt out of L1 fee surges without the need to bootstrap security.

Rollups, in general, require less financial overheads than L1s. Each new Cosmos chain has to bootstrap its own economic security, incentivizing people to buy the token and stake it in a validator. Theoretically, the token’s value must also scale with the amount of value it secures. As such, rollups provide a simpler way for application developers to build their own configurable execution environment and opt out of L1 fee surges without the need to bootstrap security.

However, from a decentralization perspective, it cannot be denied that the current state of rollups versus the current state of appchains heavily skews towards appchains. Rollups, at large, have a lot of work to do in order to bridge that gap. But the upside of doing so is very high — which is why there are so many high-caliber teams building in this space.

From rollup frameworks and RaaS providers to data availability layers and shared sequencing networks, there is a lot to be excited about. We believe rollups will be core to further scaling out DeFi applications while giving app developers a larger degree of control over the infrastructure.

Why Rollapps Can Be a Great Choice for DeFi

Rollups are a sound choice for a variety of apps — DeFi just happens to be the focal point of this report. It’s abundantly clear by now that the Ethereum mainnet isn’t going to be able to handle a large influx of activity and provide competitive costs to users. However, Ethereum mainnet is still the largest chain in terms of capital and liquidity. Users want their precious funds to be hitched to Ethereum’s economic security — and that is a priority. Cost is secondary, as so many willingly pay between $5 – $200 as transaction fees.

Rollups offer users the best of both worlds in this regard. Users of rollups like Arbitrum and Optimism benefit from the economic security of Ethereum, as hard transaction finality is achieved by settling rollup transactions on the L1. The added benefit is that by batching rollup blocks and settling multiple user transactions as a single L1 transaction, the cost on end-users is reduced significantly.

These rollups also use native ETH for gas, which addresses the usual run around to swap into the native gas token that exists for most L1s. There’s also the perception of these chains being “Ethereum aligned,” which, memes aside, is also true. Other than the memes, it’s just hard facts that ETH powers the most liquid DeFi ecosystem. Smart contract rollups on Ethereum feel more like extensions of Ethereum rather than a new chain.

It’s a much easier path for someone with a handful of ETH to move over to Arbitrum or Optimism over Solana or NEAR. And this has resulted in several ETH whales, and smaller fish, being willing to move their liquidity to Arbitrum ($2.3B) and Optimism ($830M). These two rollups, combined, represent over $3B in cumulative capital locked.

It would be false to say activity on Ethereum has come to grinding halt, but it is true that many are priced out of using Ethereum mainnet. Rollups are the escape hatch. They allow users to trade on the closest thing to Ethereum, with similar security guarantees, and an easy path to liquidity. Rollups are Ethereum’s answer to chains like Solana and Aptos that promise fast transactions at a cheap cost.

As extensions of Ethereum, rollups benefit from the demographic of high-profile traders that Ethereum boasts. This was a big reason for dYdX’s StarkEx rollup success. It was much easier to attract heavy users and the top market makers on a chain that had the “Ethereum seal of approval”.

Once again, rollups are bigger than Ethereum. A gaming centric rollapp, for example, would probably choose a purpose-built data availability network like Celestia over Ethereum for the massive cost advantage. Given the nature of the underlying product, keep user costs low is probably more important than inheriting Ethereum’s security/consensus. But a DeFi rollapp responsible for billions in user funds probably wouldn’t agree with that trade off.

Aevo Paves the Way for Rollapps

Birthed from Ribbon Finance, an automated structured product platform, Aevo is a derivatives exchange built on the OP stack. The team essentially forked Optimism and deployed their DEX on it in order to scale the amount of usage it can support. It’s important to note that Aevo’s trade matching happens off-chain, but order execution and settlement are on-chain.

As a derivatives DEX, success usually means you need to process a massive load of orders every block. It also needs to be cheap for users to place orders, cancel orders, rebalance positions, and everything else. None of this is viable on Ethereum mainnet.

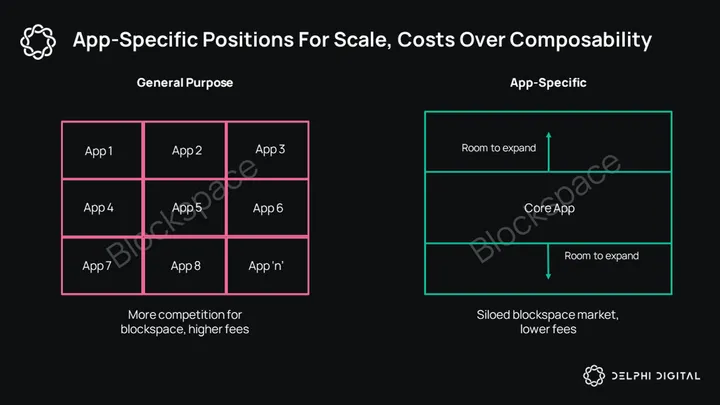

Aevo could have just deployed on Optimism and benefited from the capital and tokens that already existed on the network. The choice to make Aevo a rollapp is one that takes the future into account. As usage on Optimism rises, it will inevitably result in a re-pricing of blockspace. Aevo’s users will have to compete with every other application for blockspace, pushing fees higher. With their own rollup, this is less of a concern. And derivatives generally involve a lot of transacting. It’s not that Aevo needs their own blockspace market right now, but rather that its more straightforward for them to establish their own network and put in the work to get assets migrated than it is to migrate to a new infra stack after hitting escape velocity.

Most DEXs, especially derivatives-focused ones, would benefit from having their own execution environment. Demand for blockspace is directly related to the demand to use the application and is not a side effect of some other application’s users clogging the chain. In the long term, if you expect your application to have tens of thousands of users, deploying as a standalone rollup is a way to eliminate the need to bootstrap economic security.

Most DEXs, especially derivatives-focused ones, would benefit from having their own execution environment. Demand for blockspace is directly related to the demand to use the application and is not a side effect of some other application’s users clogging the chain. In the long term, if you expect your application to have tens of thousands of users, deploying as a standalone rollup is a way to eliminate the need to bootstrap economic security.

There are two key options for an app that expects a large scale of activity: become an appchain or become a rollapp. An appchain requires a lot more work to maintain and set up. The chain has to use tokens to incentivize validation and block production. It can take a significant amount of time to get to a healthy threshold, and requires a willing set of validators to purchase the amount of tokens required to be bonded.

A rollapp abstracts a lot of this away, as previously discussed, and is a more shrewd business decision. Instead of having to use its token treasury to incentivize validators, a rollapp can instead use its token distribution to try and drive more usage/liquidity to the app without needing to worry about economic security. Of course, this is based on assumptions that exist with today’s network. Rollup token economics is ripe for disruption, and there are several levers (sequencers, provers, validators, gas token, etc) that can be pulled.

Aevo is currently operating with safeguards but has done well for itself. In the network’s early days, the team has been able to focus on growing volume and liquidity. Users do not really have to worry about it being a new chain since it’s a fork of Optimism, which has run fairly smoothly since launching. With Aevo building on the OP stack, the team doesn’t have to worry about how they upgrade infrastructure from here — they can simply piggyback off the work done by the Optimism team and spend more time figuring out the product side. And the same will hold for any project building on top of an existing rollup framework.

Achieving Interoperability Across Rollups

If the future holds hundreds or thousands of different rollups, there is a lot of work to do on the interoperability side. Smart contract apps on a general purpose chains enjoy a high-degree of composability. If rollapps are siloed, it kills the composability advantage.

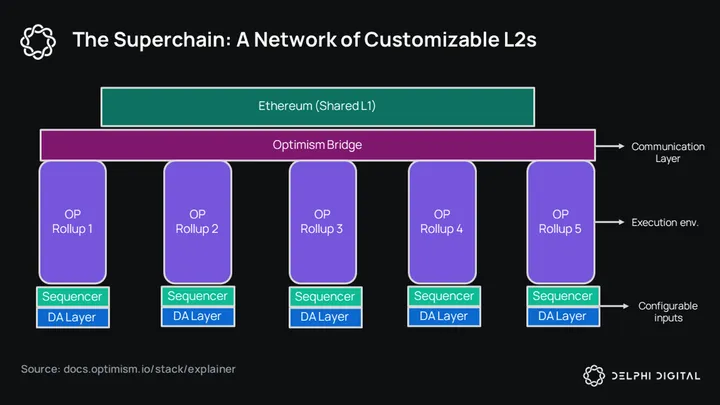

Ethereum’s roadmap relies on rollups for execution. But each individual rollup has limited blockspace. We cannot expect all activity to happen on a handful of these rollups. All rollup builders understand this and are turning their tech/standards into frameworks to enable app-specific rollups. Arbitrum has Orbit, Optimism has the Superchain, zkSync has hyperchains.

The Optimism Superchain and zkSync hyperchains are fairly similar. I’ll use Optimism as an example to illustrate this idea. The Superchain is essentially an ecosystem of OP stack rollups, all linked to Ethereum via a shared bridge layer. OP chains will have standardized security models and share consensus on the same L1 (Ethereum), thus enabling a more straightforward path to bridging assets between chains.

However, this doesn’t mean developers don’t have the freedom to configure their rollup as they see fit. An OP chain can choose to post data to Celestia instead of Ethereum; they can also have their own independent sequencers rather than share a sequencer. With EIP-4844, Ethereum will bring KZG commitments into the mix. And this will allow Ethereum to verify any computation or data posted to an external data availability layer.

However, this doesn’t mean developers don’t have the freedom to configure their rollup as they see fit. An OP chain can choose to post data to Celestia instead of Ethereum; they can also have their own independent sequencers rather than share a sequencer. With EIP-4844, Ethereum will bring KZG commitments into the mix. And this will allow Ethereum to verify any computation or data posted to an external data availability layer.

Arbitrum Orbit is a framework to deploy rollups that settle to Arbitrum, which in turn settles to Ethereum mainnet. Orbit chains are essentially L3s, and as such have a significant cost advantage over a normal L2 that settles to Ethereum.

Shared sequencers are another concept that could stand to improve interoperability between rollups. In essence, rollups can plug into a network of shared sequencers who decide the ordering of the transactions. The core assumption here is that the shared sequencer network will provide services to many different rollups, and since they control ordering for all these rollups, they can provide atomic inclusion of transactions, i.e., the sequencer can promise to include both the burn of token XYZ on rollup A and the mint of token XYZ on rollup B in the block they send a proposer (who verifies the block).

What this means is you can bridge assets from one rollup to another, not that you can do atomic cross-chain swaps. So it does stand to enable cross-rollup asset flows, but not atomic cross-rollup DeFi.

Resilient Rollup Design: Things to be Addressed

Time for a quick detour away from DeFi.

Many today think of rollups as just glorified multi-sigs. And they’re not entirely wrong. Virtually every rollup today has a multi-sig security council that can upgrade the L1 smart contract. But thinking of this as the end-state rather than a protective measure to get an MVP is also the wrong way to think about; it’s naive to think these networks will not progressively move towards more decentralization as the technology to do so is developed and gets more battle testing.

The lowest hanging fruit for Optimistic rollups (ORUs) is enabling fault proofs — and in the case of the Arbitrum stack, enabling permissionless fault proofs. Fault proofs exist to contest any invalid state changes to the rollup on L1. They provide a mechanism for nodes to call out any potential fraud from the block proposer.

At the moment, Arbitrum has 13 permissioned validators that are allowed to build rollup blocks and publish them on L1. Optimism has a single sequencer/verifier set up and doesn’t have fault proofs yet.

ZK rollups (ZKRs) use validity proofs, which are attestations that a state transition is valid rather than an assertion of invalidity like a fault proof. TLDR, a validity proof confirms the validity of a state transition while a fault proof asserts fraud.

Both ZKRs and ORUs have sequencers. Decentralizing the sequencer is a step in the right direction for several reasons. Sequencers can censor transactions/specific users and extract MEV through their control of ordering (and inserting their own transactions for optimal ordering) — but they cannot help make invalid blocks, because rollup nodes will simply discard invalid transactions. Still, to make the overall system resilient and guarantee liveness, all single points of failure need to be eliminated — and that includes the sequencer.

The Other Side of the Coin

dYdX is a notable story of a DeFi application successfully pulling off progressive decentralization. It evolved from a smart contract on Ethereum to a StarkEx rollup, into its (seemingly) final form as a sovereign app chain. dYdX v3, the StarkEx rollup, was obviously centralized in certain ways. The order book and matching engine was hosted on an entity-controlled AWS server — something I have talked about way too much. However, the most important part — fund flows and monetary settlement — was always on-chain. Therefore, there was no tangible rug risk, but the overall decentralization of the application was far from ideal.

When dYdX was on a rollup, the DYDX token was a “valueless governance token”. For a short period of time, staked DYDX (or stkDYDX) was used as insurance to backstop the protocol. There was clear value against the token because it only represented a vote in the dYdX DAO.

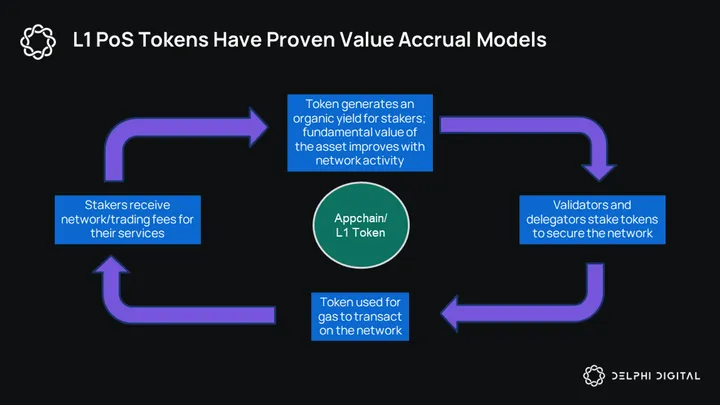

Today, DYDX is an L1 token — used as gas on the dYdXChain and as the asset validators must bond. It is a revenue-positive token, as all fees earned by the network go to validators. dYdX v3 was a revenue-positive application, but all that revenue went to the dYdX Foundation — so the token was undisturbed.

DYDX’s token economics finally makes sense and has a clear path to sustainable value accrual. And this brings up an interesting question: are rollups just a stepping stone into an app chain for highly successful products? Is there a path to value accrual and token utility for a rollup?

Realistically, an OP stack rollup doesn’t need a token. Even Optimism’s OP token is purely used to vote in governance. There is a path to rollup tokens being valuable, however, by eventually using them as bonds/stake when the sequencer operation is decentralized, as gas tokens on the rollup, or for proving networks (ZKRs) and as bonds for block proposers (ORUs). There is a real path toward L2 tokens finding a tried and true token model like L1s.

Realistically, an OP stack rollup doesn’t need a token. Even Optimism’s OP token is purely used to vote in governance. There is a path to rollup tokens being valuable, however, by eventually using them as bonds/stake when the sequencer operation is decentralized, as gas tokens on the rollup, or for proving networks (ZKRs) and as bonds for block proposers (ORUs). There is a real path toward L2 tokens finding a tried and true token model like L1s.

Personally, I don’t believe rollups are merely a stepping stone to sovereign chains. However, projects like Aevo and Vertex using rollups as a mere settlement engine isn’t all that reassuring either.

Some successful products may want complete control of their infra — from consensus to transaction execution. And appchains will make sense for them. But rollups have implications for various kinds of products that, almost permanently, remove barriers to entry and make everything plug-and-play. And this is extremely beneficial for a wide range of applications — from DeFi, to gaming, and even enterprise adoption of blockchains for private and public use cases.

Projects We’re Watching:

- Aevo: a rollapp with off-chain matching and on-chain settlement; building up to volume via viral asset listing strategy (pre launch futures)

- Lyra: a rollapp promising less centralized matching process vs Aevo and Vertex; focus on perpetuals, options, and spot trading.

- Caldera, Rollkit, Conduit, Dymension: simplified rollup deployment

- Astria, Espresso Systems: shared sequencing networks

Theme 4: RWA Design Space Opens Up

Real world assets were quietly one of crypto’s most successful sectors in 2023. The private credit niche, made up of Maple, TrueFi, Goldfinch, Centrifuge was in free fall throughout the second half of 2022. The collapse of FTX, 3AC, and other institutions exposed the vulnerability of the trust assumptions in this business model.

Insolvencies hit Maple, Ribbon and others as the private credit sector plunged from an ATH of nearly $1.5B in Jun. 22 to a trough of roughly $225M in Jan. 23. The private credit sector built upon this base throughout 2023, grinding up to $650M on the back of increased market share from Centrifuge.

The market for tokenized treasuries has been even more promising, surging over 700% to $800M over the course of the year. The rise of tokenized treasuries makes sense given the risk off attitudes in a rising rates environment.

RWAs have been a polarizing topic in crypto, as they represent the promise of institutional adoption, as well as many of the tradeoffs necessary to onboard them, such as KYC, trust assumptions, and permissioned usage. Many RWA projects are composed of a vault/pool that can only be accessed by accredited investors (Maple) or a token whitelisted only to accredited investors (Ondo). The problem with this arrangement is that once the user takes possession of the asset, the blockchain serves little purpose beyond a non-custodial brokerage account. In this way, a lot of DeFi’s transformative potential is wasted due to the lack of composability.

When considering permissionless RWAs, some may be tempted to discuss MakerDAO or Flux Finance. By issuing stablecoins against tokenized assets as collateral, retail users are able to earn borrow interest from the accredited investors holding tokenized RWAs. The issue here is that the borrow rate is not a function of the underlying yield, meaning a) the interest rate will never exceed that of the underlying, limiting its viability to rising rate environments, and b) the entire structure is only useful for increasing the collateral pool. While increasing the TAM of crypto assets with heterogeneous collateral types is a good thing, this is not offering any sort of RWA beta to the retail users involved, or composability for other useful projects.

While KYC and permissioned finance will remain big part of the RWA landscape going forward, there are a few ambitious projects bringing a much needed permissionless component to the RWA scene.

Backed Finance – A Promising New Flavor of Tokenized Treasuries

Contrary to Ondo Finance, which allows users to KYC and earn T-bill yield by depositing into a vault, Backed Finance operates similarly to USDC — accreditation/KYC to issue and redeem assets, with permissionless transferability for use on-chain. There is blacklist of OFAC sanctioned wallets, just as is the case with USDC. Decentralization puritans will be quick to point out that this is by no means a best practice arrangement, but it is a big step forward compared to existing solutions.

Backed currently offers several assets, including tokenized fixed income and tokenized equities. Its most popular assets at the moment are GOVIES 0-6 Months Euro Investment Grade (bC3M) and IB01 $ Treasury Bond 0-1yr (bIB01).

Backed Finance bAssets are currently on Ethereum and Gnosis, and can be used on Ethereum L2s. Once bAssets have made their way to liquid Uniswap and Curve pools, they could then be used to collateralize options contracts, fund principal-protected yield vaults, pay off Alchemix loans, and plenty of other creative DeFi use cases that are out of reach for other RWA models.

Superstate

Superstate is a RWA tokenization project similar to Backed that is focusing more on the US market. While Backed does not offer issuance or redemption to any US users, accredited/KYC-ed or otherwise, Superstate intends to serve the US market, pending regulatory approval. Superstate is will be playing catch up one it reaches the market, and its focus on the US could prove to make the regulatory aspect more cumbersome. Should they succeed, they will be well-positioned to lead the the tokenized treasuries market.

RWAs carry the inevitability of trust assumptions and regulations. Current implementations may seem lame, but it’s naive to think DeFi can succeed without RWAs. Eventually, trading upcoming car makes, models, and new/used spreads will be a thing. 2030 is really gonna knock socks off, and RWAs is one of the few narratives that gets TradFi excited about crypto. Projects like Backed, and Superstate are well positioned to push RWAs forward and demonstrate DeFi’s value add to a massive audience.

Theme 5: New Use Cases Spark Traction for Interest Rate Derivatives

In our Interest Rate Swaps report back in May, we explored the underdeveloped IRD sector, focusing on Voltz and IPOR. The sector was showing promise at the time, but 2023 ultimately became another tough year for IRDs. Voltz has struggled since the report, suffering from insolvencies and poor LP performance, ultimately sunsetting the project and leaving IPOR as the only IRS protocol.

The chart above paints a deceptively optimistic picture, with TVL among key protocols tripling over the course of the year. Pendle is the only grower, and although it has come a long way with its v2 and has separated itself from the once saturated yield stripping sector, its usage is heavily incentivized by a veToken program and Arbitrum STIP incentives beginning in October.

Pendle

Pendle’s resurgence was primarily the result of an abundance of liquidity from composable LSD tokens and the narrative around LSDs leading to organic volume for rate trading. LSDs account for over 60% of Pendle TVL today.

Yield stripping protocols like Pendle will continue to be an important part of shaping crypto native activity and behavior towards interest in IRDs. But these designs are unlikely to usher in a robust interest rate derivative ecosystem that IPOR can.

IPOR

IPOR has lost some of its usage and momentum, but the protocol has run smoothly and its v2 was just soft-released on mainnet.

IPOR v2 includes:

- Upgraded infrastructure, improved spread model that will ensure more competitive pricing in times of volatility

- Extended term structure, now offering 2 and 3 month contracts

- IPOR Stake Rate Swaps

- Bridging TradFi – DeFi by unlocking real world rates for DeFi users (SOFR, Treasuries)

- Liquid fixed rate lending/borrowing

- Offering LPs leverage against their liquidity

This is a very bold roadmap that, once executed, would elevate IPOR as the key player in interest rate derivatives space.

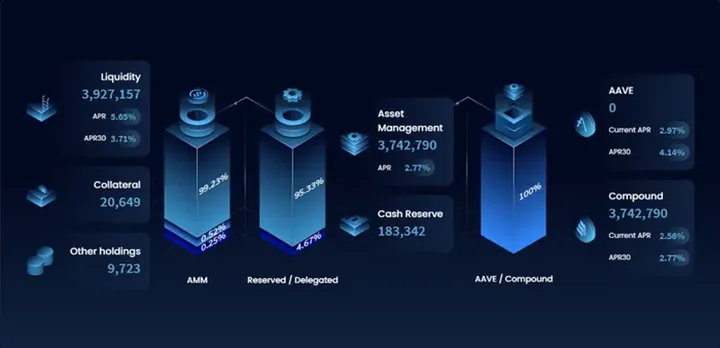

As discussed in our report, IPOR is a great situation for LPs. It generates organic yield on top of money market yield via asset management contracts. This graphic from IPOR is a helpful look under the hood of the asset management contracts.

As discussed in our report, IPOR is a great situation for LPs. It generates organic yield on top of money market yield via asset management contracts. This graphic from IPOR is a helpful look under the hood of the asset management contracts.

Traditionally, users have to choose between competing yield venues. On IPOR, a user who is agnostic to smart contract risk has no reason to choose money markets over IPOR. IPOR offers money market yields + a bonus yield from a roughly breakeven business built on top.

The problem with IPOR – and all IRD projects – has been volume. The potential use cases for IRD projects are self-evident, but DeFi, in its current immature state, can only support speculative use cases.

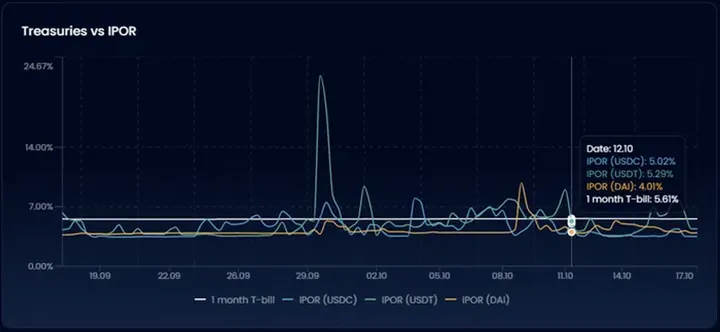

IPOR will soon bring TradFi yields on-chain and has begun teasing this feature on their IPOR index analytics page. Allowing users to capture the best rate between DeFi <> TradFi could provide a better habitat during rising rate environments, and would likely become one of the stickiest yield venues in DeFi.

IPOR will soon bring TradFi yields on-chain and has begun teasing this feature on their IPOR index analytics page. Allowing users to capture the best rate between DeFi <> TradFi could provide a better habitat during rising rate environments, and would likely become one of the stickiest yield venues in DeFi.

Pendle and IPOR are penciled in as the kingpins of the tattered IRD sector for the time being by virtue of the last man standing.

IPOR’s impressive mechanism design has been held back by the markets’ fleeting interest in IRSs. If we see a prolonged bull market in 2024, IPORs growth will likely be further limited by mainnet gas costs.

Pendle is singlehandedly carrying product market fit for IRDs now and will be instrumental in continuing to mold consumer behavior towards this vertical. IPOR has a higher execution risk than Pendle but a broader scope and a greater ability to entrench itself in the future of this narrative.

Fixed Rates

Fixed-rate lending in DeFi remains nonexistent. Yield protocol shut down, and Notional Finance’s $24M in TVL is a far cry from its all-time high of $1B in 2021. Exactly Finance gathered some momentum and brought fresh ideas, but usage was heavily incentivized by OP incentives and native token emissions.

So, what is holding IRDs back, and how will these issues be addressed?

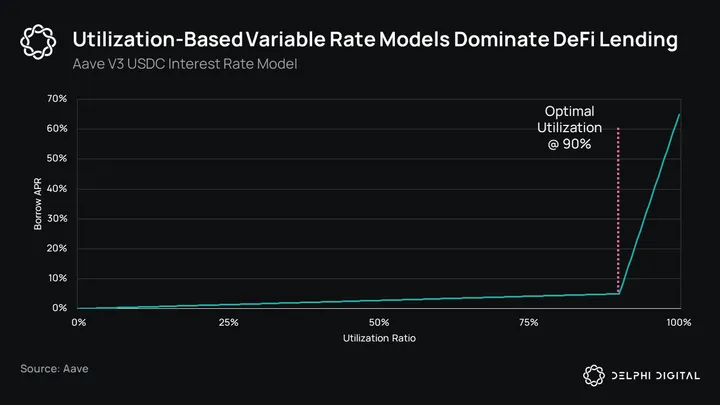

Flaws of floating rates – Most peer-to-pool lending protocols employ a utilization-based interest rate model. The increased slope of the rate curve above optimal utilization is effective at bringing utilization down, but this model is generally ineffective and pushes utilization towards optimal utilization. Since the borrow interest paid is dispersed among all suppliers, the supply rate = borrow rate * utilization ratio * (1 – reserve factor).

This leads to some egregious rate spreads that are unacceptable for a mature financial system. Even if institutional-sized liquidity were willing to enter, there would be slippage on large loans. Rate spreads need to be fixed for DeFi to go mainstream.

The negative impact of rate spreads holds everything back. For example, the IPOR rate is essentially the weighted average of DeFi mid-market rates which are a weighted average of arbitrary utilization rates within arbitrary compartments of liquidity on fragmented chains. DeFi’s interest rates are a pseudo representation of the appetite for leverage, and have little to do with market forces. Exciting crypto-native applications of yield derivatives are within reach, but DeFi lacks a healthy interest rate foundation.

Better traction in fixed-rate lending will remedy rate spreads and form a legitimate yield curve that more complex derivatives can be built on top of. Fixed-rate lending protocols can be bucketed into three main approaches.

Peer-to-pool – Peer-to-pool models attempt to match lenders and borrowers at the same rate, pooling liquidity in several isolated, non-interoperable pools that correspond to different maturities. These models typically utilize a utilization-based interest rate model, which runs into similar issues as described above. It can be difficult to organically populate the pools necessary for a robust lending platform, especially with the suboptimal utilization-based model. Examples of this model are Notional Finance and Exactly Finance.

Batching – Term Labs places lenders and borrowers into batches, arriving at a marked clearing interest rate through recurring auctions. This model is effective at price discovery even when liquidity is sparse, a significant disadvantage of the peer-to-pool model. Term Finance auctions frequently shift from ~50K in volume to $1M +, generally clearing at similar prices. The use of auctions also solves slippage, a huge problem for peer-to-pool borrows with size.

A key drawback to Term’s model is its lack of flexibility, as there is no secondary market or position management capabilities. It also appears to exhibit some of the same waste that is often found in the peer to pool model. While Term Labs is, at the moment, probably the closest thing we have to a true yield curve, it’s unclear if this yield curve will ever be representative of the entire DeFi ecosystem. In its current state, Term Finance is ideal for smart money but is unlikely to attract retail users.

Order books – Order books offer a clear solution to the issues of the peer-to-pool model without the sacrifices of the batching method. Order books allow the seamless transfer of collateral and debt across various markets and maturities, making this model the best candidate to deliver a true yield curve with negligible rate spread. Orderbooks rely on market makers for liquidity and are generally too computationally intensive for Ethereum at this stage.

Infinity Exchange and Coupon Finance are some interesting examples of this model. It will be interesting to see if a successful fixed-rate lending protocol can emerge on Solana, given it has the throughput to support a performant order book. For now, MarginFi, Solend, and other large Solana lenders only offer variable rates based on the utilization model.

The Consumer Behavior Disconnect

Even if a perfect solution existed, today’s DeFi may not use it. Despite a 98% dominance of fixed rates in TradFi, DeFi fixed rate market share is below 1%.

This lopsided usage of variable rates is strange, considering there is now a clear economic advantage of borrowing fixed. Term Labs’ rolling 4-week auctions have produced a fixed rate substantially below Aave’s variable rate for several months.

It is important to consider that Term Finance is very new, and often has auctions clearing less than $50K notional with just a handful of users. However, Coupon Finance, Exactly Finance, and Notional Finance offer similar rates with improved liquidity. It seems safe to infer that the true market price of borrowing is much lower than Aave’s variable rates.

Exactly Finance and Coupon Finance offer similar rates to Term Labs, beating Aave on cost before considering any token incentives. DeFi’s preference for variable rates over fixed is widely acknowledged and could stem from several factors:

- Use cases for borrowing – With a shortage of tangible use cases, the majority of borrowing activity is used for leverage, leading to few cost-sensitive borrowers.

- Lending TVL is notoriously sticky, and users can be lazy.

- Lack of awareness – DeFi has had some pretty rough attempts at fixed rates. Aave’s stable rate was once a 2x multiplier over the variable rate. Users may be accustomed to uncompetitive fixed rates.

- Security premium – Aave has been around for 4 years and largely unscathed despite operating in the most dangerous crypto sector besides bridges.

- Superior UX – Loans on Aave and Compound do not expire, and require much less upkeep on the user end.

This ignorance of fixed-rate lending will prove costly to DeFi’s growth if it persists. Fixed rates are foundational to many of the more complex rate derivatives in TradFi.

Given the market’s treatment of fixed rates so far, it is unlikely that 2024 will be the year of DeFi hyper-maturation and a newfound preference for fixed-rate lending. But there are strong new tools emerging, and there are clear synergies between rate derivatives and RWAs.

Interest rate swaps, caps, floors, inverse floaters, swaptions, forward rate agreements, expirable futures, carry trades, etc, are all inevitable components of a complete DeFi ecosystem. With their high complexity, enormous TAM, and potential for degeneracy, IRDs could become one of crypto’s more captivating narratives.

Theme 6: Decentralized Stablecoins’ Tough Path Ahead

Decentralized stablecoins represent a foundational application of DeFi. Yet, users are progressively favoring centralized stablecoins such as USDC and USDT, attracted by their user-friendliness, scalability, and wider-spread acceptance on CEXs and in payments.

To put it into perspective, the largest decentralized stablecoins, each with a supply exceeding $100M, collectively account for only 5.08% of the total market share for stablecoins. Decentralized applications are only as censorship-resistant as the money that flows through them.

In 2023, the market share for decentralized stablecoins has shown little change, oscillating between 4.21% and 5.75%. The first two quarters of the year witnessed a gradual reduction in the supply of these stablecoins. However, the trend reversed in Q3 following MakerDAO’s introduction of the Enhanced DAI Savings Rate (EDSR), which led to a boost in DAI’s circulation.

Additionally, 2023 saw the emergence of ETH LSD-backed stablecoins like eUSD by Lybra and mkUSD by Prisma, which managed to capture interest. As it stands, mkUSD’s supply has reached $170M, and eUSD’s supply is at $123M. Even with this noted progress, these coins still represent just a fraction of the broader stablecoin market capitalization.

MakerDAO and Frax have strategically positioned their protocols to offer returns comparable to those of U.S. Treasury bills, appealing to holders seeking stable yields. MakerDAO’s EDSR offers a 5% APR, while Frax’s sFRAX provides a slightly higher yield of 5.4% APR.

MakerDAO’s DSR has been met with substantial uptake, securing around $1.55B of DAI deposits. This accounts for a significant 29.5% of the total DAI supply, showcasing effective use of its revenue to drive demand for DAI.

In contrast, Frax’s offering has seen more modest adoption, with about $20M deposited, representing close to 10% of the non-protocol-owned FRAX supply. This lower adoption rate could be due to FRAX holders finding more attractive yields in Convex finance pools, thus overshadowing the benefits of a 5.4% APR.

MakerDAO and Frax democratize U.S. Treasury Bills and allow anyone to get access to traditional yields on-chain. This has allowed DAI to set the on-chain “risk-free rate” at 5%.

Looking at DAI in DSR vs BTC Price, we see that there is a slight inverse relationship between them. As BTC prices goes up, DAI in DSR has a tendency to drop, which indicates the demand for on-chain stablecoin yield during risk-off regimes.

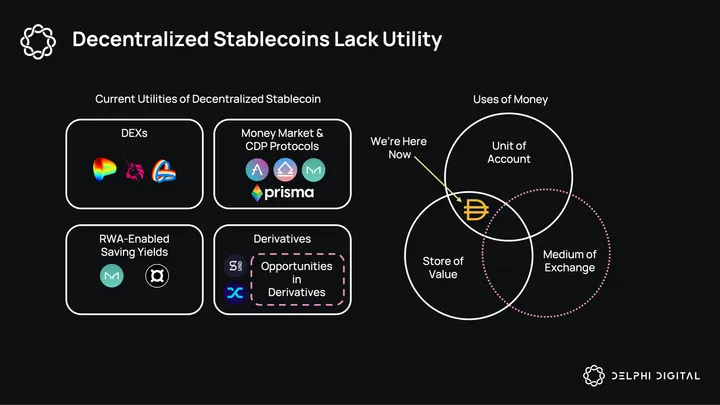

Decentralized stablecoins have carved out a niche in the on-chain ecosystem, serving in DEXs, money markets, CDP protocols, savings, derivatives, and as an censorship-resistant store of value. Predominantly, their adoption is yield-driven.

Decentralized stablecoins have carved out a niche in the on-chain ecosystem, serving in DEXs, money markets, CDP protocols, savings, derivatives, and as an censorship-resistant store of value. Predominantly, their adoption is yield-driven.

However, as most use cases reach saturation, the derivatives market emerges as a key area with untapped potential. Currently, many derivatives platforms rely on centralized stablecoins like USDC for margin trading. This reliance poses a fundamental question about the degree of decentralization in these protocols. Synthetix’ Perps v2 module stands out as a rare example that utilizes a decentralized stablecoin, sUSD. This highlights an opportunity for other protocols to adopt decentralized stablecoins in a bid to improve the censorship resistance of their platforms.

However, the hesitancy to adopt decentralized stablecoins in broader applications is understandable, given the added risk layer, such as potential exploits leading to de-pegging incidents.

If we look at the decentralized stablecoin landscape today, they currently function as stores of value and units of account. Their utility as a medium of exchange in commerce remains limited. While solutions like Crypto.com and Basedapp’s crypto debit cards offer workarounds by enabling swaps to the required currency, the ideal scenario would involve direct transactions with decentralized stablecoins (e.g., using 10 DAI to buy $10 worth of groceries). This shift would mark a significant milestone in the mainstream adoption of decentralized stablecoins. But is this even viable?

Will Decentralized Stablecoins Ever Gain Mass Adoption?

For decentralized stablecoins to achieve widespread adoption, they must address several critical challenges:

- Over-collateralization Issue: Currently, most decentralized stablecoins require more than $1 in collateral to mint $1 worth of stablecoin, leading to capital inefficiency and limiting the user base to those with on-chain wealth. Although protocols like MakerDAO have introduced USDC as collateral to mint an equivalent value in DAI, this, in turn, actually raises concerns about the true decentralization of the stablecoin.

- Medium of Exchange and Off-Ramp Solutions:

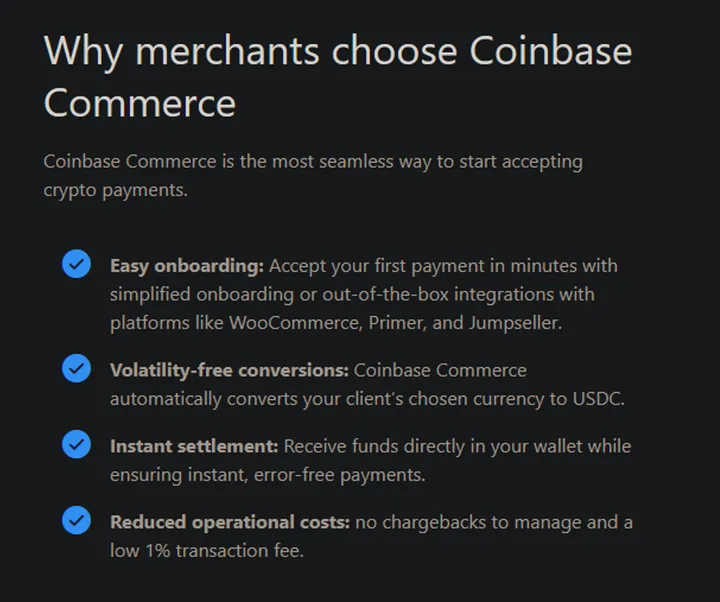

- Usability for Real World Transactions: A significant barrier for decentralized stablecoins is their utility in everyday transactions, such as purchasing goods. Currently, there is a lack of infrastructure for merchants to accept decentralized stablecoins directly. Given the existing solutions like Coinbase Commerce that provide reliable off-ramp and commerce solutions for centralized stablecoins like USDC, merchants have little incentive to adopt decentralized stablecoins if their ultimate goal is to convert to cash.

- Off-Ramp Limitations: Converting decentralized stablecoins to cash often involves an indirect process, typically requiring a swap to a centralized stablecoin before redemption for fiat currency.

- Navigating the Regulatory Landscape: Decentralized stablecoins face significant regulatory challenges, particularly concerning their use in the real world. Compliance with regulations, especially around anti-money laundering (AML) and Know Your Customer (KYC) requirements, is a major hurdle.

Projects we’re watching:

Ethena and Resolv Labs are two protocols utilizing a delta-neutral design for their stablecoins. These delta-neutral stablecoins provide high capital efficiency with no need for over-collateralization while enabling organic yields to be generated by both the long and short positions.

Gyroscope is a fully collateralized stablecoin backed by isolated vault reserves to mitigate overlapping risks that can potentially lead to contagion risks. They implement a Dynamic Stability Mechanism where if a collateral vault is exploited, the redemption will initially start at $1 and once it hits a certain point of supply redeemed, it will implement a circuit breaker that utilizes a bonding curve with decreasing redemption quotes.

Theme 7: Payments, Crypto’s Largest and Oldest Challenge

Crypto and payments go together like wine and cheese — they’re meant for each other. Yet, for several reasons, crypto payments haven’t hit the scale or audience people envisioned 5 years ago. We can boil it down to a number of factors, but the most important ones are:

- Fairly cumbersome on/off ramp process

- Lack of commerce integrations across the Web 2 stack

- Regulatory uncertainty of the industry as a whole

- Notion of the industry being comprised of high-volatility assets

Stablecoins have been on a tear for the last five years. In the beginning, the crypto payment vision was centered on Bitcoin. The emergence of stablecoins and tokenized dollars has been a huge breakthrough in establishing a medium of exchange everyone can rally around. The market, at large, has put its weight behind digital dollars as the high-velocity asset of choice in crypto.

Since the emergence of Tether, Circle, MakerDAO, and several others, stablecoins have begun to dominate trading volumes. They have been cemented as the quote asset of choice on CEXs and even many DEX pairs. The entire world runs on the dollar, so why shouldn’t crypto? There are several strong arguments for why the dollarization of crypto markets is a bad idea. But the market has already rallied around this, and stablecoins solve a lot of key pain points with crypto payments. In the last couple of years, we’ve seen the perception of stablecoins evolve dramatically around the world:

- The Monetary Authority of Singapore (MAS), the country’s premier financial market regulator, finalized rules around stablecoin issuance for operators in the country.

- Nubank, the largest Fintech bank in Brazil, recently partnered with Circle to bring USDC to its user base. It will serve as a means of facilitating crypto trading as well as payments.

- SBI Holdings, a large financial services firm in Japan, partnered with Circle to explore how USDC can improve banking services in the region.

- Paypal launched its own stablecoin, pyUSD.

- Several neobanks and fintech companies are looking to stablecoins to unlock the next level of payment efficiency.

An Influx of Fintech Stablecoin Usage

Over the next few years, I believe we’ll see a large number of traditional fintech players and neobanks look to stablecoins as a new unlock for their business. Apps like Venmo are closed ecosystems. Meaning you can send money from one Venmo account to another but not a Google Pay account. Ultimately, all payment apps in a region utilize the same monetary standard — be it dollars, pounds, or rupees. However, the vast majority of payment apps are not easily interoperable.

Adopting, say, USDC, as a standard across multiple payment apps enables users to be able to exit the walled garden and send their money to other apps. It mimics, trustlessly, what India’s Unified Payments Interface (UPI) does — establish a unified backend for payments that apps build on top of. Some businesses see their walled garden as a moat, so this narrative is appealing for users but not for the payments business in question. However, when we try to expand the scope from day-to-day payments to a larger scale, the appeal for fintechs and neobanks starts to take shape.

It can take a long time to remit money abroad. Several countries like India, Mexico, and China receive large amounts of gross remittances every month. Remittances are estimated to account for $850B + of transfer volume. Even for businesses, there is a lot of cross-border flow between North America, Europe, and Asia — all of which costs a pretty penny in fees and can take days to clear. New age blockchains like L2s and fast/cheap monoliths like Solana can vastly improve the overall experience. And new fintech platforms would be naive to not explore crypto as a pathway to greater margins and a better experience for users.

To be clear, I am not asking these platforms to become permissionless and open their gates to the unknown. Their customer base will still undergo KYC/AML processes. But in the background, they will have:

- Better economics for the platform and users. Cheaper transaction costs and faster transaction confirmation.

- Leaving regional regulatory registration aside, acquiring customers globally becomes more viable as blockchains can be accessed from any region. There’s no need to figure out the right back-end setup beforehand.

- Allow customers to take custody of their stablecoins, putting the onus of fiat conversion on them. And charge a fee for access to priority banking channels.

Even as a walled garden, stablecoins make sense for virtually any payments or financial services businesses. You don’t have to open up the walled garden — and you can expand it relatively simply.

This takes me back to a section in last year’s DeFi thesis, where we laid out the idea of “Robinhood, but plugged into DeFi”. Simply put, the idea was for a centralized platform like Robinhood that simply helped custody user funds and plugged into DeFi for liquidity to trade, obtain leverage, and otherwise.

The idea for fintechs becoming a source of stablecoin originations and relying on them to improve the payment experience is an extension of this idea. You have a separation between the user layer and the blockchain. The user only directly interacts with the centralized app. For all intents and purposes, the blockchain is simply a backend that the platform uses instead of traditional channels. Liquidity protocols like Uniswap aren’t consumer apps — but consumer apps can build on top of them, abstracting a lot of the complexity away.

I believe we will see large-scale penetration of Fintech companies using stablecoins as payment facilitators in 2024.

Plug and Play Solutions Become More Popular, Expand the Utility of Stablecoins

The idea for why stablecoins present an opportunity to any payments business is straightforward — in a vacuum. In reality, stablecoins can’t be used for much other than crypto trading and or on select merchants. Off/on ramping is still required to do most of what a person would want with stablecoins, which poses some degree of dependence on legacy banking infra. In order to overcome this, we have a simple yet difficult task ahead: make stablecoins more widespread and integrated in commerce.

The easiest way to have more meaningful stablecoin usage is by allowing people to buy goods and services with their coins — not just 100 vol assets. Plug-and-play solutions are easy-to-use tools that enable any kind of online merchant to accept crypto for payment. Coinbase (Commerce API) is the market leader in this segment. Shopify also has crypto payments enabled, but they don’t have their own infrastructure; they merely allow merchants on the platform to integrate a solution like Coinbase Commerce, Crypto.com, or Solana Pay.

The process is straightforward: the buyer is shown a blockchain address that they need to send their asset to. It can range from volatile assets like ETH and BTC to stablecoins like USDC. For volatile assets, Coinbase uses its CEX to convert the asset into USDC before passing it on to the merchant.

Products like this add value to crypto assets, allowing them to be useful in real commerce. And stablecoins are perfect as a solution for both customers and merchants to facilitate fast payments without the overhang of asset volatility. ETH may be ultrasound money, but I promise your neighborhood grocer doesn’t really care about that (yet).

Products like this add value to crypto assets, allowing them to be useful in real commerce. And stablecoins are perfect as a solution for both customers and merchants to facilitate fast payments without the overhang of asset volatility. ETH may be ultrasound money, but I promise your neighborhood grocer doesn’t really care about that (yet).

It’s fairly simple to integrate something like Coinbase Commerce. It’s just an API that merchants have to add to their platform. So, what stops every online merchant from doing this?

The first, again, comes down to the lack of clarity around crypto. Businesses that don’t foresee crypto payments being a big driver in future revenue wouldn’t really care too much. For an automotive spares seller or an online tutoring service, will enabling crypto payments move the needle?

Merchants will begin to care about crypto when it legitimately opens a new door for them — in the same way Miami nightclubs started accepting crypto when they realized a lot of their customers were “crypto millionaires” who would be willing to spend larger amounts when provided with the right payment option.

Right now, users who have stuck around for a couple of cycles in crypto likely have a meaningful portion of their cash as stablecoins. As the stickiness around stablecoins expands, and as more people start to see the value in owning them, merchants will start to realize there is a real market to buy goods/services with crypto. And plug-and-play solutions like Coinbase Commerce will be vital at that stage.

Other Things to Watch Out For

It’s impossible to talk about on-chain payments without mentioning Solana. Amongst of all the blockchain infra that exists today, Solana is uniquely positioned to target the retail payments market. Between transaction fees that cost a fraction of a cent, 400 ms block times, and native USDC, Solana has a competitive advantage in being that trustless backend for payment businesses.

SolanaPay is a payment app that launched in 2022, aiming to empower both consumers and merchants with P2P payments. Transactions settle near instantly, and merchants and consumers can have a more direct relationship sans intermediaries. You also have Sphere, a new payments service that aims to consolidate everything from on/off ramps, invoicing, and accounting into a single platform. And TipLink, which is a way to use crypto for payments without the recipient needing to have a wallet beforehand.

It would also be remiss to ignore PayPal’s new stablecoin, pyUSD. When announced, PayPal’s CEO noted that the main goal here is to facilitate better digital payments. pyUSD probably cannot compete with USDC and USDT as far as trading volumes go, but they can carve out their own moat with payments, given the lack of penetration thus far. PayPal’s global standing as a payments giant is obviously something we cannot dismiss here. And they very well could be the stablecoin that Fintech and Neobanks rely on, given their track record.

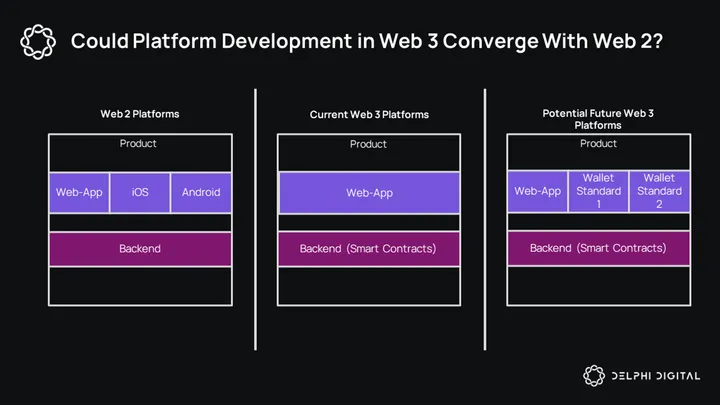

Theme 8: Wallets Make Drastic UX Strides and Become “Consumer Apps”

In last years report, I laid out my thesis for UX aggregation and how its set to simplify the on-chain experience. I didn’t expect it to play out in a year (and it didn’t), but the core idea around enhancing the user experience remains relevant. I won’t focus on the same ideas as last year, because there is more to flesh out here.

But before we get to that, we need to address some recent concerns over making UX a priority. Some of the top thinkers in crypto have recently been talking about why UX enhancements shouldn’t be a primary focus — the real problem to solve is building better, more functional apps that solve a real pain point.

This tbh

Solve an important problem first, worry about UX and UI later

Those who badly need your solution will happily jump through hoops to get it